by Lillian Dickerson | May 21, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

At every industry conference for about the last 15 years, there’s the obligatory social media panel. But, there’s a reason for that, panelists at Inman On Tour Miami argued.

“Social media has evolved and is what catapults a lot of people to success,” moderator Katie Kossev of Side said.

TAKE THE INMAN INTEL SURVEY FOR MAY

The session’s three panelists — Angel Nicolas of Compass, Tiffany McQuaid of SERHANT. and Jonathan Vega of One Sotheby’s International Realty — have all developed social media presences over the years that have helped them garner business. And their different approaches to the marketing tactic show that there’s no one-size-fits-all approach when it comes to finding success through social media.

Nicolas started out by hiring a few different companies to help him with his social media presence, but ended up moving the work in-house to his team because “the equality wasn’t there.”

Meanwhile, McQuaid said she has always managed her social media presence herself, “and it’s mostly not real estate-related.” She draws on whatever she’s thinking about at that time, with a focus on authenticity and being true to herself, and it helps draw like-minded clients into her sphere.

“What a difference it makes when you’re walking into a listing appointment or a buyer walks into the office specifically to meet you because they follow you,” McQuaid said. “Talk about skipping steps in terms of engagement and conversion and standing out over your competition. Content to creation to conversion — aren’t those the three C’s that we’re all after?”

Vega also has a team in-house that manages his social media presence for him while he acts as “the brains.” But when he first launched his real estate career, Vega said he hired someone to film him for about $15 per hour, and then he would edit the videos himself.

But he realizes that not everyone, especially new agents, has the resources to hire out someone else to handle their social media, so he said, “It’s just getting your phone out and recording as much as you can, and figuring out as you go.” Today, agents can also use AI tools to help edit content for social media for free, he added.

Posting about listings or the market are all fine ideas, but it’s important to provide value for your followers about topics unrelated to real estate, too, panelists said.

“When you’re on social media for a long time, there’s only so much you can post of sharing properties, and I think there comes a time — and you start to feel it — when you need to evolve out of that space and into that authentic space and sharing who you are,” McQuaid said.

It can be hard to watch oneself on social media, Kossev pointed out, but it’s important to get past that in order to share yourself with followers.

Nicolas said that when he first started posting videos of himself, he “almost threw up” watching himself. His wife also pointed out how much his accent came through, which made him self-conscious. But he learned not to worry about his accent so much, because it’s part of who he is.

“I’m like, ‘I’m from the Dominican Republic; what do you want me to do?’” Nicolas joked with his wife after cringing during one of his early videos. “But I will post it anyway, and I think that creates relatability, right? People can relate to that, and for me, it was from the beginning, I want to be genuine. I want to be myself and, love it or hate it, if people are going to connect with my vibration, that’s what matters the most.”

It’s important to learn how to connect with your specific audience and find a platform that works for you, panelists urged the Inman On Tour audience.

“You gotta find what works for you, and the only way to do that is trial and error,” Vega said. “You have to try the different platforms and figure it out.”

Vega was stuck at about 500 YouTube followers for what seemed like forever, he said, but after a lot of fine-tuning and refining his content, those followers ultimately grew to the more than 28,000 he has today on YouTube. He urged agents to post consistently and post about their personal lives.

Vega shared that he recently posted a video of himself showing a penthouse in Brooklyn to his grandfather, who had never been in a penthouse before, and “it’s gotten the most engagement that I’ve had.” He said he originally made the video to have it to show to his own kids someday, but it has the added benefit of performing well for his business, too.

“That’s what we’re all doing this for, is family, and for our lives,” Vega said, “so I think if people feel like they can relate to you through social media, then they’ll want to reach out to you.”

Email Lillian Dickerson

This post was originally published on this site

by Jim Dalrymple II | May 21, 2025 | Industry, News Feed

NextHome’s James Dwiggins argued during Inman On Tour Miami that Compass is “steering” clients. Compass’ Mark McLaughlin said Compass clients aren’t being “duped.”

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The ongoing and ever-heated real estate industry debate over private listings spilled onto the Inman stage Wednesday as panelists debated the wisdom of the concept and whether it amounted to “steering.”

The debate took place during an afternoon panel at Inman On Tour Miami, which featured NextHome CEO James Dwiggins, Compass Chief Real Estate Strategist Mark McLaughlin and the Keyes Company President Christina Pappas.

Midway through the conversation, Dwiggins argued that sellers can do whatever they want and that there are many different flavors of listing right now. However, when “we talk about seller choice, there’s a difference between choice and steering.”

TAKE THE INMAN INTEL SURVEY FOR MAY

Dwiggins’ comment was a reference to Compass, which has made private listings a centerpiece of its marketing efforts, and which disclosed in a recent lawsuit that nearly half of its listings are “pre-marketed” — meaning they first begin as Compass private exclusives or with “coming soon” status before later entering the local multiple listing service.

“That’s called steering,” Dwiggins added.

However, McLaughlin quickly objected, saying that Dwiggins’ argument essentially amounted to saying that “20,000 of Compass’ clients are duped and steered.”

Dwiggins then shot back, saying that most consumers likely don’t understand or read contracts that lay out how privately listing their home might work.

Dwiggins has become one of the most prominent voices in the real estate industry pushing back against private listings, while Compass CEO Robert Reffkin is among the concept’s most prominent advocates.

From left to right, moderator Brad Inman, Christina Pappas, James Dwiggins and Mark McLaughlin at Inman On Tour Miami Wednesday. Credit: Mike Nyffeler with AJ Canaria Creative Services.

The debate over private listings engulfed much of the homeselling business in late 2024 and early 2025 as different players put pressure on the National Association of Realtors to take action on Clear Cooperation, a rule that requires NAR members to put their listings into their local MLS within a day after they begin marketing. In the end, NAR staked out a kind of middle ground, keeping Clear Cooperation in place but adding a new delayed marketing option.

During Wednesday’s debate, McLaughlin responded to a frequent criticism of Compass’ position — namely, that the company merely wants to double-end more deals — by saying that more than 50 percent of the brokerage’s listings that don’t hit the MLS are co-brokered.

Later on Wednesday, after this story had published, a Compass spokesperson suggested to Inman that by penalizing agents or brokers who fail to enter their listings into the MLS within one business day, multiple listing services were the ones engaged in “steering” practices.

“It’s worth noting that the MLSs fine agents up to $5,000 if the agent doesn’t steer their clients into the MLS,” the spokesperson wrote in a statement to Inman. “The Clear Cooperation Policy’s ‘mandatory submission’ rule results in agents steering clients into the MLS out of fear of being fined by the MLS.”

Meanwhile, Pappas took a kind of middle position — and offered a warning. Regarding seller choice, she said, “I believe in allowing our sellers a choice in how it gets marketed. They need all of the information possible to make the best decision.”

However, she also recalled a situation during the COVID-19 pandemic in which a buyer sued her company after buying an off-market property. Turns out, because the property was off-market, the buyer didn’t have a good sense of the home’s market value.

“The buyer sues us because he thought he overpaid,” Pappas said.

After the story ended, Dwiggins added that “there’s a lot more of that coming.”

Alternatively, McLaughlin had earlier argued during the discussion that “the one opinion that’s missing here is the opinion of the homeseller.” And he said he believes “the decision on how to do marketing should create a competitive environment.”

“It should be,” he added, “at the intersection of the seller’s desire and the agent’s professional advice.”

Email Jim Dalrymple II

This post was originally published on this site

by Taylor Anderson | May 21, 2025 | Industry, News Feed

Weeks before the current owners planned to sell the home in Dolton, Illinois, by auction, the Chicago suburb announced it would take ownership with its eminent domain powers.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The village that is home to the house where newly selected Pope Leo XIV grew up said Tuesday that it planned to take ownership of the dwelling, either by buying it or through its eminent domain power.

TAKE THE INMAN INTEL SURVEY FOR MAY

The 750-square-foot home was slated to be auctioned off to the highest bidder in a private, sealed bid auction scheduled for June 18.

But attorneys for the village of Dolton came out with a strong message on Tuesday: Don’t bother bidding.

“The Village intends to work with the Chicago Archdiocese and other agencies to allow the home to be viewed and visited by the public as a historic site,” according to a letter sent by attorneys for the small village to the company handling the auction.

The auction of 242 East 141st Place is being handled by Paramount Realty USA, which is offering bidders the chance to “Own a Sacred Piece of History.”

“Born Robert Francis Prevost, Pope Leo XIV made history as the first American pope upon his election in May 2025,” Paramount Realty USA wrote in its description. “His childhood home is being offered for sale via private auction. Located in a suburb of Chicago, Illinois, this modest brick home was owned by the Prevost family for nearly 50 years and served as the foundation of a life that would lead to the Vatican.”

The minimum, all-cash price for the home is $250,000 plus a 10 percent buyer premium.

The home was bought a year ago for $66,000 and substantially updated by a suburban investor who couldn’t immediately be reached on Wednesday. After renovation, the investor-owner put the home on the market in January for $219,000, Crain’s Chicago reported. The price fell to $199,000 in February before it was taken off the market after the pope was elected.

Paramount Realty USA didn’t immediately respond to a request for comment on Wednesday. Steve Budzik, the broker handling the home sale, declined to comment.

Louis Prevost sold the home in October 1996, according to state records shared as part of the due diligence process for potential bidders.

Under Illinois law, local governments have the power to take private property for public use if they pay fair compensation to the owner.

“Please inform any prospective buyers that their ‘purchase’ may only be temporary since the Village intends to begin the eminent domain process very shortly,” the village attorneys’ letter said.

The attorneys told Crain’s Chicago that the eminent domain plan came at the direction of newly elected Mayor Jason House, who was elected May 5, three days before the new pope’s election put the house in the national crosshairs.

The attorneys told the news outlet that, if the village doesn’t buy the property, any would-be buyer would be blocked from using it as anything other than a single-family house, noting it sits within an area zoned for single-family residential.

“We don’t want it to become a nickel-and-dime, ‘buy a little pope’ place,” the attorney told Crain’s.

Email Taylor Anderson

This post was originally published on this site

by Taylor Anderson | May 21, 2025 | Industry, News Feed

The short-term rental platform vowed to appeal the ruling on Monday and said it would keep the listings active while it battles the latest push to enact strict rules amid an acute housing shortage.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Airbnb went dark in New York City. Now, it’s facing the possibility of going dark in Spain.

In response to an acute housing shortage and amid tension with tourists, Spain’s High Court affirmed an order requiring the short-term rental platform to remove nearly 66,000 listings in the country, a ruling Airbnb has vowed to appeal.

TAKE THE INMAN INTEL SURVEY FOR MAY

The court affirmed a ruling by the Ministry of Social Rights, Consumption, and the 2030 Agenda, which ordered Airbnb to block more than 65,000 listings on its platform. The government considers the short-term rental listings to be illegal.

The rulings come amid a broader effort by Spanish leaders to crack down on illegal tourist accommodations, the nation said.

The ruling is a blow for the leading short-term rental platform as it seeks to grow its market share overseas amid tepid demand in the U.S., and as it seeks to grow its highly profitable business internationally.

The high court ordered Airbnb to immediately remove 5,800 listings, a number that was later lowered to just under 5,000 after the company showed a number of listings were in compliance with regulations.

But the Directorate General for Consumer Affairs said the country justified the removal of the more than 65,000 Airbnb listings in the country because the ads don’t include a license or registration number; they don’t indicate whether the owner is a professional or an individual; or they include inaccurate license numbers.

Airbnb said that the ruling wouldn’t take immediate effect, and that it would appeal.

The action was a departure from past rulings, including by the Spanish Supreme Court, which ruled in 2022 that individual hosts were responsible for making sure to provide accurate and necessary information on the listing.

Airbnb has said that short-term rentals account for a miniscule amount of total housing in markets that have enacted stringent regulations, like Barcelona and Amsterdam.

In 2023, tens of thousands of Airbnb listings were removed from New York City as part of a crackdown on short-term rentals in the Big Apple. The company has said such regulations are a boon for the hotel industry, which has seen prices soar in New York City after the regulation took effect.

“No evidence of rule-breaking by hosts has been put forward, and the decision goes against EU and Spanish law, and a previous ruling by the Spanish Supreme Court,” an Airbnb spokesperson said in a statement.

Instead of cracking down on tourist housing options, the spokesperson said, Spain should focus on building more housing to meet existing demand.

“The solution is to build more homes – anything else is a distraction,” the spokesperson said. “Governments across the world are seeing that regulating Airbnb does not alleviate housing concerns or return homes to the market – it only hurts local families who rely on hosting to afford their homes and rising costs.”

Email Taylor Anderson

This post was originally published on this site

by Matt Carter | May 21, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Cloud banking solutions provider nCino Inc. surprised investors with a sneak peek at its upcoming earnings report Tuesday, revealing that revenue and income exceeded the cautious guidance it provided last month.

Shares in nCino hit an all-time low on April 2, the day after the company reported an $18.6 million fourth quarter net loss despite growing revenue by 14 percent from a year ago, to $141.4 million.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

Company executives issued guidance for Q1 last month predicting:

- Total revenue of between $138.75 million and $140.75 million.

- Subscription revenue of between $121.75 million and $123.75 million.

- “Non-GAAP” operating income between $22.5 million and $24.5 million.

Preliminary financial results for the first quarter ended April 30, 2025, “exceed the top end of previously disclosed financial guidance ranges for total revenues, subscription revenues, and non-GAAP operating income,” the company announced Tuesday, without providing further details.

Ncino will report first quarter results after the market closes on May 28. Shares in nCino, which in the last 12 months have traded for as little as $18.75 and as much as $43.20, gained 4 percent Tuesday to close at $25.81.

Non-GAAP financial measures exclude factors like acquisition-related expenses and stock-based compensation. The company also provides GAAP measures that follow Generally Accepted Accounting Principles (GAAP) as required by securities regulators.

In a May 9 annual report to security holders, nCino said the company’s unrecognized compensation expenses related to non-vested stock-based compensation totaled $145.7 million as of Jan. 31. Those costs are expected to be recognized over the next three years, as shares granted to executives and employees vest.

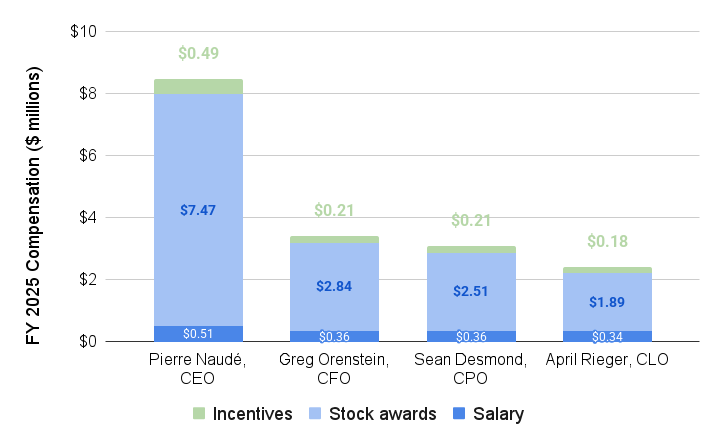

In notifying shareholders of the company’s upcoming annual meeting on June 18, nCino detailed past compensation of top executives including former CEO Pierre Naudé, and Chief Product Officer Sean Desmond, who succeeded Naudé as CEO on Feb. 1.

Stock awards to top executives

The company’s five top executives — Naudé, Desmond, Chief Financial Officer Greg Orenstein, Chief Legal Officer April Rieger and former president Josh Glover — have been granted $49.8 million in restricted stock awards over the last three years.

Naudé’s compensation has included $21.6 million in stock awards during that period, including $7.47 million in fiscal year 2025, which ended on Jan. 31.

Although Naudé, 66, is no longer CEO, he is still employed by the company as executive board chair. His son, Pierre W. Naudé, and daughter, Petra Sheaffer, are also nCino executives.

As senior manager, product management, the younger Naudé earned $360,000 last year, including restricted stock grants valued at $154,000.

Sheaffer was paid $506,000, including $299,000 in restricted stock grants, for her role as associate director, technical partner relationship manager.

Excluding the senior Naudé, the median annual compensation of all 1,832 nCino employees as of Jan. 31 was $112,179, meaning the CEO was paid 76 times as much, the company disclosed.

Ncino offers an employee stock purchase plan that lets rank-and-file workers buy shares in the company for 85 percent of their fair market value.

At launch in 2020, the program authorized the company to issue a total of up to 1.8 million shares for sale to participating employees, a number that automatically increases each year. As of Jan. 31, 5.48 million shares of nCino common stock remained available for employees to purchase.

NCino, which raised $268.4 million in a July 2020 initial public offering, on April 1 announced plans to repurchase up to $100 million of the company’s outstanding common stock.

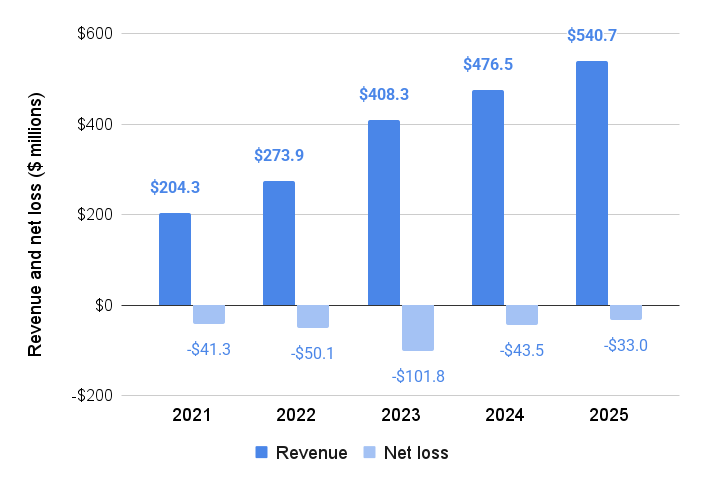

Growing revenue in search of profits

Ncino revenue and net losses, fiscal years 2021-2025 ending Jan. 31. Source: NCino regulatory filing.

Since launching in 2011, Wilmington, North Carolina-based nCino has racked up $385.3 million in cumulative losses.

The company, whose clients include independent mortgage banks Synergy One Lending and Fairway Independent Mortgage Corp., has grown revenue in part through strategic acquisitions of SimpleNexus, DocFox, FullCircl, Integrated Lending Technologies (ILT), Visible Equity and FinSuite.

In some cases, nCino will issue restricted stock to key employees of companies that it acquires in an effort to incentivize them to stay.

Last year the company paid $74.3 million in cash to acquire DocFox. But it also issued 198,505 restricted stock units in nCino to certain DocFox employees valued at $6.1 million. The stock grants, which will vest over four years if the employees continue to work for nCino, were recorded as stock-based compensation after the acquisition.

On nCino’s April 1 earnings call, Desmond said nCino’s most recent acquisition — of Boston, Massachusetts-based integration technology provider Sandbox Banking for $52.5 million in February — is likely to be its last for now.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Brad Inman | May 21, 2025 | Industry, News Feed

Transcendent enthusiasm, like falling in love, grabs hold when buyers find a home they adore, Brad Inman writes of the couple who bought his Spanish-style West Hollywood home earlier this month.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

I knew I would live there when I first walked into the 102-year-old condominium in San Francisco’s Nob Hill neighborhood last month. The feeling was indistinguishable from when I bought my first home in Oakland 45 years ago.

Nostalgia and imagination inspire powerful feelings when buying a home. You are launched into an orbit of transcendent enthusiasm, like falling in love.

TAKE THE INMAN INTEL SURVEY FOR MAY

Brad Inman

As my wife Yaz and I were closing on the San Francisco unit, the young buyers of our 98-year-old Spanish-style West Hollywood home felt the same magical enchantment. The Brooklyn transplants wrote a poignant letter describing their enthusiasm about purchasing our house — they fell in love.

This is one reason why selling or leaving a home is so difficult. It’s not just the memories; your soul becomes welded to the place, making it difficult to let go. Before moving in, your imagination lays the first psychic rebar, connecting you to a future of joy and meaning with all of life’s experiences ahead of you.

Brad Inman’s chair in Palm Beach, Florida

Millions of other people embark on this same journey, which, as a journalist, has always drawn me to real estate.

Homeownership has never been an elite privilege — at least not in the United States. It was always meant for everyone. As with our current housing affordability crisis, market forces often step in to correct the imbalance when it becomes too much. A more balanced market is beginning to take shape now.

To achieve homeownership, aspiring buyers must make sacrifices, stretch their household budgets, accept smaller living spaces, and choose geographical trade-offs.

Young people — Gen Z, the Zoomers — are setting out on a new wave of geographical reshuffling, this time to affordable Midwestern states. No personal or economic obstacle can squash their determined real estate ambitions. Like love, desires take over.

Right now, I sit in a chair, in a room, in my home, where I write, read and reflect.

Homes aren’t just a dream for me — they are who I am and what I love.

Email Brad Inman

This post was originally published on this site