by Lillian Dickerson | Jul 9, 2025 | Industry, News Feed

With the partnership, RLTYco CEO and cofounder Briggs Elwell will join the association’s board, and agents who subscribe to RLTYco will also have access to AREA membership through the company’s suite of services.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The American Real Estate Association (AREA), an alternative that emerged last year to the National Association of Realtors (NAR), has partnered up with real estate services company RLTYco and made one of its cofounders a board member, the companies have informed Inman.

With the move, Briggs Elwell, RLTYco’s CEO and cofounder, will join AREA’s board, giving the company further insights into agent needs and giving AREA industry insight from a seasoned veteran who has been active in a variety of real estate endeavors.

Briggs Elwell | RLTYco

Elwell said the partnership came about because of a shared vision for the future of the industry.

“The alignment of efforts [by] us to provide services to the agent community and then the efforts of what Jason [Haber and Mauricio Umansky] were doing with the American Real Estate Association was just incredibly logical because we’re both working in the same talent pool, same industry and we’re just really aligned at the overarching goal of bettering the community,” Elwell told Inman.

Jason Haber, cofounder of AREA and a Compass-affiliated agent, said that as the trade organization ramps up for a period of expansion, they were looking for leaders who would help drive growth, and Elwell seemed like a clear asset to add to the team.

Jason Haber | Compass

“We’re at a point where we’re ready for our next phase, which is going to be rapid expansion, and when we go into expansion mode in this next phase, who do you want helping guide you?” Haber said. “Who are the players to help make you this nationwide hub to bring together people who may have differing opinions on where the industry needs to go, but share the same belief that there’s a lane for us to operate outside of NAR — not in competition with them, in some ways in collaboration — but to create our own voice and to say, ‘Here’s what we think is best for the industry. Here’s what we want to put out into the public square. Here are the things we can be doing better.’

“I think by bringing in someone of Briggs’ caliber, you’re going to see us attract a full swath from around the country of talent, both at the executive level, meaning CEOs, general counsels, people in the C-suite, to the agent community as well, that’s hungry for new voices to help galvanize and organize the industry.”

Elwell started off as a licensed agent and spent a significant portion of his early career working with New York City developer Related Companies, where he worked on the firm’s luxury rental portfolio. He also led small- to mid-size brokerages in New York City before launching RLTYco with Daniel Kennedy in 2021.

Because of his location in New York City, which does not have a multiple listing service (MLS), Elwell said he has never been a Realtor.

Mauricio Umansky | The Agency

“We’re excited to partner with RLTYco and welcome Briggs to the board,” Mauricio Umansky, cofounder of AREA and CEO of The Agency, said in a statement. “Agents deserve to set themselves up for success with resources and knowledge that are sometimes elusive based on where you are and how you choose to hang your license, and I’m a big fan of the work that RLTYco is doing.”

With the partnership, agents who sign up for RLTYco’s services — including commission advances, legal and tax assistance, and a healthcare marketplace — will now also have the option to become a member of AREA at a preferred price, which is yet to be determined. Haber told Inman that dues for a base membership are $20 for 2025, but 2026 dues have not been set yet and likely will not be announced for several months.

“I’m very excited to help push across the direction and efforts of the association,” Elwell told Inman. “But because of [this] relationship, we’re going to offer all the members preferred pricing, preferred access to things that we roll out as we build the company.”

RLTYco is also prepping to launch RLTY Blue, which is a benefits program tailored to real estate agents, akin to something like the benefits W2 employees receive through their employers or those received through certain credit cards, the company said. Earlier this year, the company raised $20 million in a Series A funding round.

Email Lillian Dickerson

by Lillian Dickerson | Jul 9, 2025 | Industry, News Feed

The firm was founded in 2005 and closed $922.3 million in sales volume in 2024, according to RealTrends. About 180 agents will be making the move to Compass.

July is Luxury Month at Inman. We’ll take the temperature of the luxury market, talk to top producers in the ultra-luxury space and dive into the luxe trends of today — all culminating at Luxury Connect in San Diego, where we’ll announce this year’s Golden I Club honorees.

As it continues to grow across the country, luxury focused brokerage Compass has welcomed another brokerage into its ranks with the acquisition of Colorado-based PorchLight Real Estate Group.

The formerly indie firm was founded in 2005 and has become well-established in Denver and Boulder since then with five sales offices. PorchLight, which is women- and LGBTQ+-owned, closed $922.3 million in sales volume in 2024, according to RealTrends.

PorchLight Realty Group was also recognized in 2024 and 2023 by the LGBTQ+ Real Estate Alliance as an alliance-member brokerage with the highest sales volume.

With the acquisition, 180 agents from PorchLight will now be affiliated with Compass.

“I’m excited to welcome the talented agents of PorchLight who have built a reputation for caring deeply about their clients and providing personal, standout service,” Compass founder and CEO Robert Reffkin said in a statement. “I am confident that, together, we will be able to learn from each other and better serve Coloradans.”

In the last several months, Compass has also acquired @properties Christie’s International Real Estate and Washington Fine Properties.

Amy Bayer and Carol Bayer founded PorchLight under the mantra that “agents thrive when they are fully supported,” according to a media statement.

“Joining Compass feels like the natural next step for PorchLight,” Amy Bayer, who is also co-CEO of PorchLight, said in a statement. “We’ve always believed in empowering agents to do their best work, and Compass offers the scale and technology to help take that to the next level. I’m incredibly proud of what our team has built over the past two decades and excited to see how our agents will thrive in the years ahead with Compass.”

Email Lillian Dickerson

by Lillian Dickerson | Jul 9, 2025 | Industry, News Feed

This marks the luxury firm’s second new market of 2025. It launches with more than 30 agents, led by Principal Broker Maryanne Moyers and founding agents MJ Frazier, Lizzy Conroy and Antonio Nguyen.

July is Luxury Month at Inman. We’ll take the temperature of the luxury market, talk to top producers in the ultra-luxury space and dive into the luxe trends of today — all culminating at Luxury Connect in San Diego, where we’ll announce this year’s Golden I Club honorees.

Ryan Serhant’s eponymous luxury brokerage has entered its second new market of 2025, the Washington, D.C., metro area, the firm has informed Inman.

Earlier this year, SERHANT. launched in Phoenix, Arizona — its first big move outside of the East Coast.

With the launch into the D.C. metro area, SERHANT. enters the District of Columbia, Maryland and Virginia, also known as the DMV region, with over 30 new affiliated agents that represent $500 million in collective sales volume over the last 12 months.

“The demand for SERHANT. across the United States is stronger than I ever anticipated,” Serhant, founder and CEO of the brokerage, said in a statement.

“I am so excited to expand into the D.C. metro area, not just because of its economic strength and influence, but because of the caliber of professionals we’ve aligned with. We’re building with intention, and aligning our platform with incredible salespeople who share our commitment to innovation and pushing the industry forward. With the recent launch of S.MPLE, we’re giving agents in D.C., Maryland and Virginia a powerful edge — an AI platform that changes how agents onboard, operate and scale their business.”

Maryanne Moyers is serving as the new location’s principal broker, and founding agents include MJ Frazier, Lizzy Conroy and Antonio Nguyen.

Moyers joins the firm from Weichert, where she recently served as a branch vice president in Alexandria, Virginia. The 25-year industry vet has ranked in the top 5 percent of Realtors across the country for the past six years and, in 2015, was recognized as manager of the year by the Prince William Association of Realtors. Over the course of her career, she has trained more than 1,000 agents and led various growth initiatives. Before her affiliation with Weichert, she was a managing broker with Long & Foster for about six years.

“Joining SERHANT. was a deliberate decision grounded in shared values: integrity, innovation and excellence,” Moyers said in a statement. “It’s the only real estate company truly built for agents, by one of the industry’s most influential agents, with a technology platform that doesn’t just stay ahead of the curve, it redefines it.

“I was drawn to SERHANT.’s unwavering commitment to surrounding itself with best-in-class leaders across every discipline and its ability to stay ahead of industry trends,” she continued. “This move marks more than just a new chapter; it’s a strategic partnership with a company that shares my vision for the future of real estate.”

Frazier, who closed more than $120 million in the past 12 months, joins SERHANT. from Real Luxury. In addition to working in residential and commercial sales, he currently manages roughly a dozen new development projects for investor clients. He also leads the RAZR Group, which includes Lacey Fox, Taylor Megonigal, Monica Manosalva, Jessie Thiel, Robby Salehi and Kriza St. Thomas.

Conroy was most recently affiliated with Keller Williams Realty McLean/Great Falls, where she served as principal of the HBC Group, the No. 1 team at the office for the past eight years. The HBC Group was also the No. 5 medium team in Virginia in 2024, according to RealTrends, and has been recognized as a top team by Washingtonian and Northern Virginia Magazine.

Conroy closed more than $120 million in sales volume in the past 12 months. Team members Sue Bender, Karen Briscoe, Steve Conroy, Pam Micciche, Jenny McClintock, Elena Morales, Holly Rasmussen, Colleen Stoltz and Beth Walker are also joining her at SERHANT.

Nguyen joins SERHANT. from eXp Realty, and before that, Keller Williams Capital Properties, where they sold more than $40 million in the past year. Between 2021 and 2024, Nguyen was a top 1 percent Keller Williams agent in the U.S., a top 1.5 percent agent in the country, according to RealTrends, and a “Star Real Estate Agent” award recipient from The Washington Post Magazine. Teammates from Nguyen’s former team, the Nguyen Chon Properties Group, are also joining Nguyen at SERHANT., including Eddie Chon, Derek Lee and Roberto Garcia.

Other agents who are joining SERHANT. DMV include Kathleen McDonald and Amanda Etro of Corcoran Group; Gary Boylan of Compass; Kat Massetti of Real; Christian Givens of RLAH; Dwayne Moyers, Dave Ingram, Debbie Ingram, Hunter Lang and Dawn Gurganus of Weichert; and Chris Itteilag of Washington Fine Properties.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Lillian Dickerson | Jul 8, 2025 | Industry, News Feed

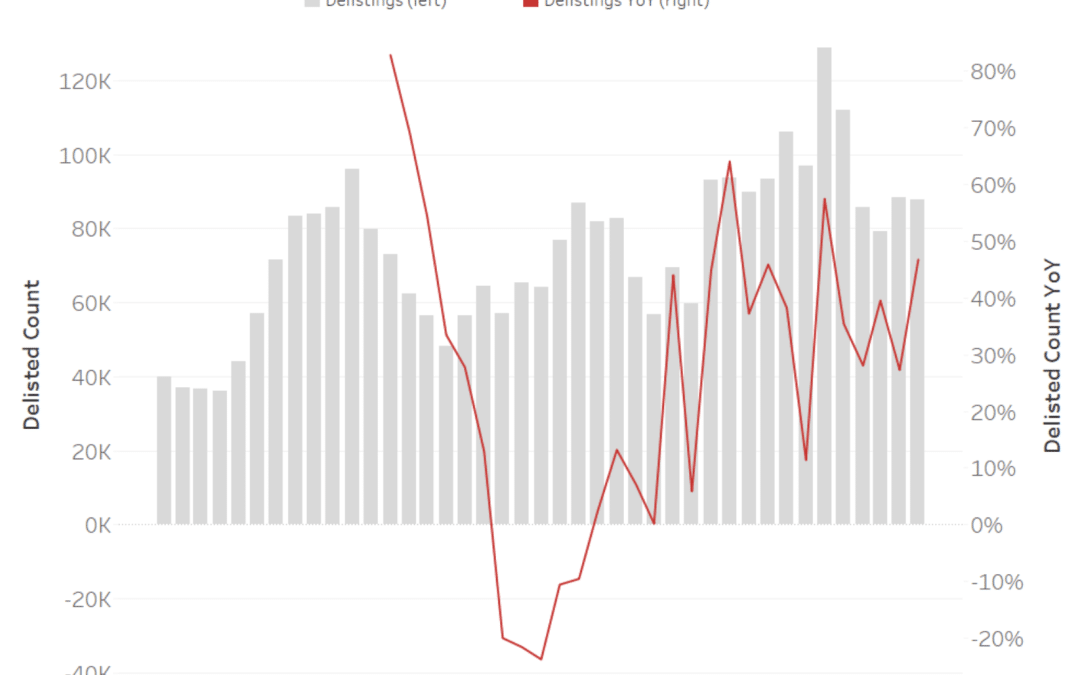

Delistings outpaced inventory growth in June even as price cuts surged, showing that a growing number of sellers are unwilling to compromise when it comes to their selling goals.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

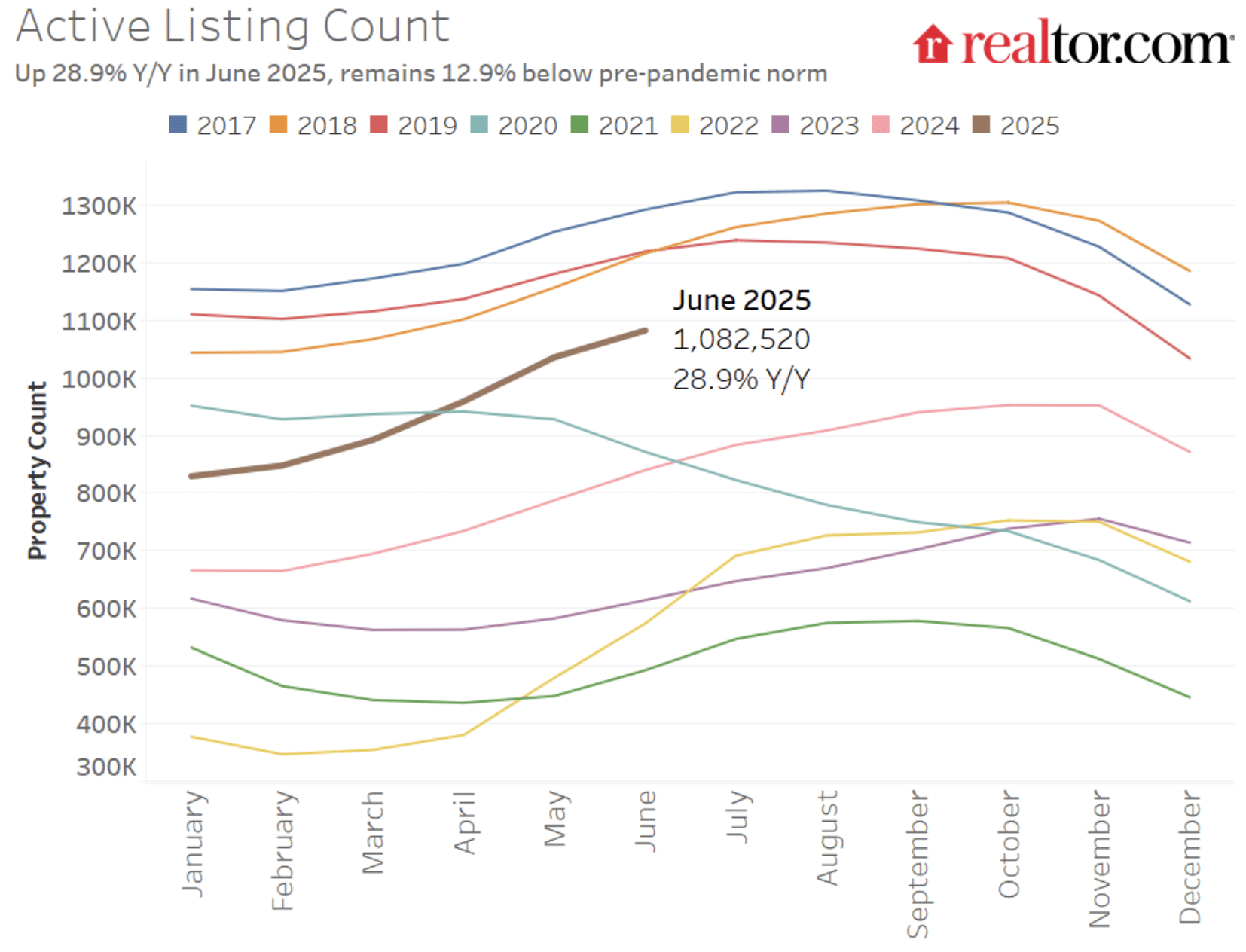

Active inventory hit a post-pandemic high in June as it grew 28.1 percent year over year, yet sellers are showing signs of becoming impatient with slower buyers, as delistings are also on the rise.

In fact, growth in delistings outpaced inventory growth, with delistings up 35 percent year-to-date and up 47 percent year over year in May, according to Realtor.com’s June Housing Trends Report. Even so, delistings make up a relatively small number of listings — 90,000 out of 452,000 new listings that went up in June.

As inventory continues to grow, it’s putting increased pressure on home prices, spurring some sellers to slash asking prices and causing home prices to decline significantly in some markets.

The data shows that many buyers and sellers today are engaging in a face-off of sorts.

All four major regions in the U.S. saw inventory increase in June, with inventory in the West up by 38 percent and, in the South, up by 30 percent. All 50 top metros saw annual inventory gains, too, with Las Vegas (up 77.6 percent) and Washington, D.C. (up 63.6 percent), in the lead.

Price cuts also surged in June, hitting their highest level for any June since at least 2016, with 20.7 percent of listings reducing their prices. Price cuts and growing inventory have not yet made a dent in the national median list price though, which remained roughly the same year over year at $440,950.

Credit: Realtor.com

“This year’s market is a study in contrasts,” Danielle Hale, chief economist at Realtor.com, said in a statement. “Buyers are seeing more choices than they’ve had in years, but many sellers, anchored by peak price expectations and upheld by strong equity positions, are deciding to step back if they don’t get their number. Looking forward, this dynamic will affect whether we tip from a balanced to buyer’s market, and if so, how quickly that happens.”

There’s no doubt that more homeowners are opting to take their listings off the market now, but even so, buyers still have more options at their fingertips than since the COVID-19 pandemic started. Active listings in the U.S. exceeded 1 million for the second consecutive month, Realtor.com said, placing inventory levels just 13 percent below pre-pandemic levels.

Meanwhile, delistings now make up about 4.1 percent of the market, compared to 3.2 percent of all active listings in May 2024.

Even with more active inventory on the market, it seems a growing number of sellers who aren’t gaining attention on their listings at their preferred price today are electing to delist instead of compromise with a price cut or continue to rack up days on market. From March through May, the ratio of delistings to new listings hit 13 percent, compared to the 10 percent seen during the same periods in 2024 and 2023, and the 6 percent seen in 2022.

Agents say that sellers in hot markets (Miami; Phoenix; Riverside, California) are especially likely to be selective about which offers to accept, oftentimes choosing to delist instead of compromising on their selling goals.

“We’re seeing hesitation on both sides of the market,” Anthony Djon, founder of Anthony Djon Luxury Real Estate, said in Realtor.com’s report. “Inventory is rising, giving buyers more options and making them more price-sensitive and selective. At the same time, some sellers — especially those not getting immediate traction — are stepping back. The market has clearly shifted from the urgency and intensity of recent years, and today’s homeowners are having to recalibrate their expectations.”

Update: This story was updated after publication with additional context.

Email Lillian Dickerson

by Lillian Dickerson | Jul 8, 2025 | Industry, News Feed

July is Luxury Month at Inman. We’ll take the temperature of the luxury market, talk to top producers in the ultra-luxury space and dive into the luxe trends of today — all culminating at Luxury Connect in San Diego, where we’ll announce this year’s Golden I Club honorees.

With almost exactly half of 2025 now in the books, its clear this is turning into a year of challenges. Global uncertainty spread, the economy rested on shaky ground, and political divisions have deepened — all of which are weighing on the minds of real estate professionals.

But amid all the challenges raining down on the housing market right now, one segment is still chugging along: luxury. In fact, in conversations with Inman, experts who specialize in the higher end of the market said that broader challenges notwithstanding, what they’re seeing right now looks more like resilience than collapse.

Mickey Alam Khan, CEO of full-service marketing agency Luxboro, was among those experts. He told Inman tariff policies have largely driven recent ups and downs in the economy, and will certainly impact the cost of construction materials and appliances, which will trickle down to the new development market. But otherwise, ultra-luxury buyers remain active.

Mickey Alam Khan

“So that impacts the future development of branded residences and new projects in that area,” Khan said. “That uncertainty is definitely hurting the overall market. When it comes to actual sales of luxury homes across the country, I feel that it’s the same situation as last year — the ultra-luxury market, or over $10 million, is always cash. So I think that market is as strong as ever, and ironically, it will grow stronger simply because of the swings and the volatility in the stock market.

“[Real estate] is becoming a more tangible asset of stored value,” he added.

Luxury real estate consistently outperformed the market at-large in 2024 and the first few months of 2025, adding to luxury agent optimism, Sotheby’s International Realty President and CEO Philip White told Inman, despite any other “noise” in the market right now.

“Luxury real estate agents must maintain unwavering focus on their business fundamentals rather than being swayed by daily market noise,” White said in an email to Inman. “Consistent client communication is paramount — ensuring buyers and sellers have current, accurate market intelligence positions agents as trusted advisors.”

Luxury trends

With interest rates still elevated, luxury buyers are heavily favoring cash transactions. There’s also little appetite for properties that require any kind of work, White said.

Philip White

“We’re observing a compelling dynamic where limited inventory of premier properties is driving competitive bidding for the most desirable locations,” White said in an email.

“Properties that have undergone strategic repricing to align with market comparables are moving successfully. There’s particularly strong demand for new construction and turnkey properties that require minimal renovation. Additionally, the vast majority of transactions are being completed as all-cash purchases. In fact, nearly 90 percent of our agents surveyed in the 2025 Mid-Year Luxury Outlook agent survey reported that the top transaction method for luxury property was cash.”

A wave of “smart luxury” buyers are also on the rise. According to Coldwell Banker Global Luxury’s 2025 Mid-Year Report, buyers who are seeking out perceived deals and investment opportunities want homes that have sat on the market.

With the value of the dollar weakened, more luxury buyers are being attracted to invest in U.S. real estate, Khan also pointed out, and even more are being compelled by President Trump’s “Gold Card” visa program, which creates a path to citizenship for individuals who invest $5 million in the U.S.

The program has received nearly 70,000 applicants, Commerce Secretary Howard Lutnick told the Financial Times, although it still faces legal challenges. Still, if those 70,000 applicants go through, it could mean a $350 billion investment in the country — much of which would likely be made in real estate.

“Where will that money go? It will go into buying either residential real estate or commercial real estate, investing in machinery, investing in talent,” Khan predicted. “But, I personally feel at least one-fifth of it will go into buying a home.”

Biggest deals of the year

There has been no shortage of big-ticket residential transactions so far this year, as investors have proven a continued penchant for luxury real estate.

The year’s priciest sales thus far have largely been concentrated in hot markets in South Florida and communities in and around Los Angeles. But other old-standbys like Manhattan, Honolulu and Aspen have seen their share of high-end deals too.

A three-home estate in Naples, Florida, marks the most expensive public sale of the first half of 2025 so far, with a jaw-dropping total sales price of $225 million. The property spans more than 15 acres and includes 800 feet of beach frontage. Michael McCumber of Gulf Coast International Properties represented the listing.

That sale was the only one thus far to surpass the $200 million mark — but there have also been several sales that have gone above and beyond $100 million, showing that ultra-high-net-worth individuals aren’t slowing down when it comes to buying the most elite luxury properties.

Stay tuned for a full list of the year’s top deals later in July.

Private listing networks

Few luxury brokerages have held back from weighing in on the private listings/office exclusives debate that has gripped the industry this year.

From staunch proponents of a client’s right to privately market their home (i.e. Compass, The Agency) to those who only support office exclusives in the rarest of circumstances (i.e. eXp Realty), brokerage opinions on the matter run the gamut.

It remains to be seen how and when the real estate industry may reach some sort of sustained status quo on this issue, and executives continue to weigh in — and call each other out. Compass, Corcoran Group and Douglas Elliman also all recently announced new platforms for their private listings.

And while any listing could theoretically be a private listing, the trend in practice is much more likely to concentrate at the higher end of the market. That’s because luxury homeowners are more likely to have wealth or notoriety that leads to privacy concerns, and thus an interest in selling without a traditional listing.

As a result, it’s already clear that the rise of private listings is poised to become one of the most consequential trends in the luxury space.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson