by Lillian Dickerson | Jun 30, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

At one time, luxury broker Rod Watson was fortunate enough to play professional basketball for a living — in Brazil, no less.

Those days are 20 or so years behind him now, but the experience was invaluable in shaping his current career serving professional athletes and entertainment professionals in LA’s luxury market.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Today, Watson also owns his own independent luxury firm, Distinct Concierge Real Estate, which he proudly runs with his family.

Next month, Watson will speak on the Inman Connect San Diego stage to share insights he’s gained over the years as a luxury broker and business owner. In advance of that, he sat down with Inman to share thoughts on the market, challenges of serving elite clients, potential business expansion and what he’s looking forward to at the event. This is what he had to say, edited for brevity and clarity.

Inman: Tell me about your background as a professional athlete and how you ended up transitioning into the industry.

Rod Watson: I played sports the majority of my life — in high school, college, and then was fortunate enough after finishing up a successful college basketball career to play basketball in Sao Paulo, Brazil, which was a great experience. I coached in college while I was getting my MBA, after playing professionally. So that opened up a lot of doors for me, which I believe really made it a seamless transition into what I’m doing now, working with athletes and representing [them] when it comes to real estate.

When I look back on [my career in sports, I] think, man, if I hadn’t stuck with it, and gone through those challenges and the ups and downs of just trying to pursue my dreams, it wouldn’t be possible for me to do the things I’m doing today.

You work with a lot of high-profile clients, particularly athletes and entertainers. What do you see as the biggest challenge today in assisting them with their real estate transactions?

I think understanding their needs and the personalities of each individual and working with their team in a cohesive manner, getting everyone on the same page and getting everyone to understand the mission and the goal. We like to go deeper, meaning that if a player says, ‘Hey, I want to buy a home in LA for the off-season,’ it’s like, why? What does that entail? And are you aware of the oftentimes overlooked cost that comes with maintaining an estate?

The biggest thing is understanding the players’ needs, the why behind wanting to buy, whether it’s a second home or primary residence, and working cohesively with their teams to reach the goal, which is to have a successful transaction in a discrete, private manner, where it’s a good deal for the player and something that can help them going forward.

I’m sure that they appreciate that insight, too.

There are a lot of moving pieces when it comes to the channels that you have to go through to successfully navigate the transaction with each individual who’s involved, from the business manager to the agent to the attorney, mom and dad or wife and any other family members who are involved in the transaction and have an opinion.

You really have to be able to balance those expectations, personalities, egos, and then, of course, be able to assert myself and be confident in my ability and my over 20 years in the business.

That’s great. And how is the luxury market in LA doing right now?

The ultra-luxury market and overall luxury market are seeing a correction. We’re seeing inventory go up and a large number of price reductions right now. I think in the last four-and-a-half months, we’ve seen 15 percent to 20 percent price reductions. And that hasn’t happened since maybe 2016.

Average days on market is around 100-plus, 120-plus. Obviously, in the ultra-luxury market, you’re still seeing some big-ticket sales. Recently, we had a $51 million sale in Beverly Hills, a $56 million sale in Bel Air, a $200 million sale three months ago. We saw Paris Hilton buy Mark Wahlberg’s old estate for $61 million. So that market is never going to truly be impacted by what’s going on in the economy and overall market itself, just because those people have the wealth, and they make decisions when they’re ready.

Good to know. As an independent brokerage owner, do you feel any pressure, in this economy, to consolidate or merge with another brokerage, as many are doing now?

I don’t. I know that a lot of companies are choosing that route for longevity, but we have a different focus in regards to who our ideal client is. That independence means a lot, because it’s a family business that my wife, my daughters and I work in, and we have 10 other agents who work with us, and we have a very cohesive group that is learning how to be successful in this space.

You previously mentioned to me you’re considering expanding into Africa, which sounds interesting. Tell me more.

I have a high school friend, and he’s been in Tanzania reaching out to me for probably three years, telling me, ‘You really need to make a strong consideration of Tanzania, because it is a really new country — only 60 years old — and they’re starting to see a lot of transformation with their real estate market, primarily in Zanzibar and the coast of Tanzania.’

Tanzania is going through a redevelopment phase right now. In Zanzibar, specifically, there’s a lot of development that’s taking place in hotels, new construction, communities … And there’s also a growing [number of] African Americans who are choosing to live abroad now. They’re leaving the U.S. and building their future wealth in Tanzania, specifically in the real estate space.

But that’s a future endeavor, I would say, something that, if we were going to fully go through with it, it would be in the next three to four years that we would announce.

What are you looking forward to at Inman Connect San Diego?

I look forward to the opportunity to collaborate with Inman and also learn and connect with other high-level, producing professionals who will be attending the event. Hopefully, learn a few new things when it comes to service in the luxury market that other agents are actually doing and successfully utilizing to grow, not only their brands, but their businesses.

San Diego is right in our backyard, and I went to college in San Diego, [so] it’s my second home. Being able to walk away, even with one trade secret or one thing that I didn’t know, that I can go back and apply in our business to help us grow, is something I’m looking forward to.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Lillian Dickerson | Jun 27, 2025 | Industry, News Feed

Former mortgage loan originator Andrew Josephson claims the company failed to adequately pay him and other employees for time worked in an effort to cut costs and gain a leg up on competitors.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

A mortgage loan originator who previously worked for Zillow Home Loans has filed a class action lawsuit against the portal giant’s mortgage lending arm, alleging that it failed to adequately pay him and other employees for time worked in an effort to cut costs and gain a leg up on competitors.

Andrew Josephson | Credit: LinkedIn

The disgruntled former employee and lead plaintiff in the case is Andrew Josephson, who worked for Zillow Home Loans from 2023 to 2025, according to his LinkedIn profile. Josephson is now a product specialist at Federal First Lending and has worked in the past at Escrow.com and Network Capital.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Representatives for Zillow said they were unable to comment on pending litigation. Lawyers for Josephson did not immediately respond to Inman’s request for comment.

The complaint filed on Wednesday in Orange County, California, alleges that Zillow Home Loans failed to pay minimum wages and overtime, provide meal and other breaks, reimburse business expenses, provide accurate itemized wage statements, pay all wages within a timely period of Josephson’s separation from the company, and violated business and professional codes.

The suit further alleges that Zillow Home Loans intentionally created “an artificially lower cost of doing business in order to undercut their competitors and establish and/or gain a greater foothold in the marketplace.”

The plaintiffs are requesting a jury trial and damages to recover unpaid wages, non-reimbursed business expenses, benefits and attorneys’ fees and expenses. California citizens currently or previously employed by Zillow Home Loans, any time between June 25, 2021, and the date of class certification, who have similar grievances as those outlined by the lawsuit, may be included in the class of plaintiffs.

This is not the first time that Zillow or one of its entities has been on the receiving end of a lawsuit regarding wages. In 2019, business consultant Nicole Correa filed a class action suit against Zillow Group, alleging labor code violations, including a failure to pay overtime wages, and Zillow settled that suit in 2021 for a little over $342,000. In 2014, former inside sales consultant Ian Freeman also sued Zillow Group in a class action suit that alleged the company violated wage laws. Zillow settled the case in 2016 for $6 million.

Read Josephson’s full complaint here.

Email Lillian Dickerson

by Lillian Dickerson | Jun 27, 2025 | Industry, News Feed

The two laws provide more generous timelines for condo associations and potential homebuyers on inspections and the reviewing of documents, among other measures, which should ease assessments that can negatively impact homeowners and buyers.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Florida Governor Ron DeSantis on Monday signed into law two new bills aimed at providing condo owners in the state with financial relief and reassurance about condo association oversight.

HB 913 intends to provide condo owners and buyers more affordability in regards to mandated condo safety measures through changes like an extended deadline on the “Structural Integrity Reserve Study” (SIRS) and alternate funding options for associations. HB 393 incorporates feedback from condo owners regarding the My Safe Florida Condo Pilot Program, including lowering approval requirements and restricting eligibility to buildings that are at least three stories and contain two single-family units.

TAKE THE INMAN INTEL SURVEY FOR JUNE

“We’ve heard the concerns of condo owners throughout Florida, and we are delivering reforms that will provide financial relief and flexibility, strengthen oversight for condo associations and empower unit owners,” Gov. DeSantis said in a statement.

“People need to be able to afford to live in these units, especially if they’re getting assessments on things,” DeSantis said during a bill signing event in Clearwater. “Maybe [repairs] do need to be done but it isn’t like the integrity of the structure is at risk here. They need to be able to work those out and you shouldn’t have this mandate apply in this way.”

The bills were largely supported by Florida Realtors, and the association is releasing updated forms in response and will host a webinar on June 30 at 1 pm ET to review the changes.

Florida Realtors was not immediately available to respond to a request for comment on this story.

Previous condo reforms that had been passed in 2022, 2023 and 2024 in the wake of the devastating Surfside condo collapse required “milestone inspections” of older condo buildings and “structural integrity reserve studies” to determine how much in funding should be reserved for repairs. Milestone inspections on older buildings of three or more stories initially had a completion deadline of 2024, and in response, some condo associations implemented new assessments to help meet those earlier deadlines.

In addition to extending the SIRS deadline to Dec. 31, 2025, and narrowing the milestone inspection and SIRS to buildings of three habitable stories or more, the new law also puts a temporary pause on reserve funding for two years following a milestone inspection and gives condo associations flexibility in meeting reserve requirements, as well as allowing them to use lines of credit, if a majority of owners approve, in order to meet reserve obligations.

Condo associations are also now required to post on their website approved board meeting minutes for the previous year to help potential buyers learn about proposed special assessments that may not have yet gone into effect. Buyers also receive an extended period of seven days in which to cancel a contract after receiving the association’s governing documents.

On July 1, Florida Realtors will release three new forms to address the legislation:

- Comprehensive Rider to the Florida Realtors/Florida Bar Contract for Sale and Purchase (CR-7): Revised to extend a potential buyer’s right to review condo association documents to seven business days, excluding holidays and weekends. It will also include revisions as recommended by the Florida Realtors-Florida Bar Joint Committee, as part of a regular forms review.

- CRSP17x_F Condominium Addendum – CRSP17x_F (Addendum to the Contract for Residential Sale and Purchase (CRSP17)): Notifies involved parties that the seller should complete this form, and updates timelines for the buyer to review all documents, inspections, and Structural Integrity Reserve Study Reports from three to seven days.

- Cooperative Addendum (COOP-4): Incorporates new language regarding the milestone inspection, turnover inspection and SIRS reports, and timelines for buyer’s review. A notice has also been included for the seller to complete the addendum.

Home prices have started to fall in Florida in recent months, with the median home price down 4 percent year over year in April — the largest drop in single-family home prices in the state since 2011 — and down 2.2 percent year over year in May, according to Realtor.com. The state’s median list price is now $439,999.

The Florida metros with the greatest price declines in recent months include Cape Coral-Fort Myers, Naples-Marco Island, Miami-Fort Lauderdale-West Palm Beach, Punta Gorda and Panama City-Panama City Beach, Realtor.com said.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Lillian Dickerson | Jun 25, 2025 | Industry, News Feed

A steady course is predicted for luxury real estate throughout the remainder of 2025, the firm’s mid-year luxury report said, creating “compelling opportunities for strategic homebuyers and sellers,” according to CEO Philip White.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Many Americans may feel shaken right now because of economic uncertainties and stock market volatility, but their confidence in luxury real estate as a safe haven remains firm.

Bradley Nelson | Sotheby’s International Realty

The conclusion comes from Sotheby’s International Realty’s 2025 Mid-Year Luxury Outlook, released on Wednesday, which pulled intel from Sotheby’s International Realty agents across the globe who specialize in transactions priced at US$10 million and above. Those insights are also paired in the report with data from investment bank UBS, J.P. Morgan, Moody’s, McKinsey and Company, Bain and Company, Cotality, the National Association of Realtors (NAR) and the National Association of Home Builders (NAHB).

“The luxury real estate landscape continues to evolve at an unprecedented pace, creating opportunities for homebuyers and sellers with the right market knowledge,” Sotheby’s International Realty Chief Marketing Officer Bradley Nelson said in a statement.

“Our global network of affiliated agents brings unparalleled expertise and market insights that only Sotheby’s International Realty can deliver. This report is designed to empower both homebuyers and sellers with the strategic intelligence needed to make informed real estate decisions throughout the remainder of the year.”

TAKE THE INMAN INTEL SURVEY FOR JUNE

Luxury real estate continued to outperform the market at large during 2024 and the first months of 2025, Sotheby’s Realty noted, with the top half of the wealthiest U.S. households benefiting from the greatest gains in real estate value, according to data from Realtor.com.

Philip White | Sotheby’s International Realty

As some buyers pull away from the market during economic uncertainty, it also creates opportunity for other buyers who are ready to pounce when there’s less competition, the report said. The economic landscape, as well as movement in key markets, rebuilding opportunities in disaster areas and more, will all have an impact on the luxury real estate market this year, Sotheby’s International Realty concluded. But a steady course is predicted as 2025 continues.

“Ultra-high-net-worth individuals continue to view real estate as an essential portfolio component,” Sotheby’s International Realty President and CEO Philip White said in a statement. “Even amid economic uncertainty, the resilience of the luxury housing market provides compelling opportunities for strategic homebuyers and sellers, and this report serves as a roadmap for navigating today’s complex luxury real estate landscape.”

Economic headwinds

Odeta Kushi | First American Deputy Chief Economist

“On one hand, sharp swings in equities can prompt some high-net-worth individuals to delay big purchases due to uncertainty,” Odeta Kushi, deputy chief economist of First American Financial Corp, said in Sotheby’s International Realty’s report. “On the other, real estate — especially in prime markets — might be seen as a safer, more tangible store of value.”

- Construction costs may be exacerbated by Trump administration tariffs, Kushi said, which could drive luxury homebuyers toward turnkey properties to avoid elevated construction costs.

- Real estate represents 18.7 percent of the top 10 percent of wealthiest households’ investment portfolios, according to an April 2025 Realtor.com report, which is down from 19.9 percent a year ago.

- The segment of $1 million homes in the U.S. continues to grow, and represents nearly 13 percent of recent existing-home sales, according to April 2025 data from NAR, suggesting affluent buyers see real estate as a safe harbor for their investments.

- A weaker dollar in response to trade wars could lead to more overseas real estate investor purchases in the U.S., as could President Trump’s proposed “Gold Card” visa program, which creates a path to citizenship for individuals who invest US$5 million in the country.

Key US markets

Kara Warrin | Golden Gate Sotheby’s International Realty

“Our luxury property market isn’t impacted by interest rates because 85 percent of transactions are with cash,” said Kara Warrin, an advisor with Golden Gate Sotheby’s International Realty in Marin County and San Francisco. “Our team sold more than US$65 million between October and December 2024, with an average sale price of US$6 million. The buyers tend to be local people who want something bigger and better and have the cash to pay for it.”

- Buyer confidence seems to be growing in San Francisco, driving momentum at Sotheby’s International Realty – San Francisco, where the firm closed several transactions over $20 million in 2024, breaking old records.

- Momentum picked up in the New York City luxury market after the election as a result of pent-up demand and more liquidity from stock market performance, local Sotheby’s Realty advisors say. Condos are especially in demand because of their fewer restrictions than co-ops.

- Low inventory and restrictions on new development in Aspen have led to sustained elevated prices in the luxury ski town.

Rebuilding after disaster

“The number of such damaging natural disasters is growing,” Sotheby’s International Realty’s report said. “According to data released in January 2025 by the National Centers for Environmental Information, part of the National Oceanic and Atmospheric Administration, in 2024, the U.S. alone suffered 27 natural disasters where the estimated damage exceeded US$1 billion.

This trend is having profound consequences for high-end property markets around the world, reinforcing the increasing importance of considering climate resilience when investing in luxury real estate.”

- 2024 was the fifth year straight in which insured global losses from natural disasters exceeded US$100 billion, marking sustained climatic disruption, according to a January 2025 Moody’s report. One-third of losses were attributed to hurricanes making landfall in the U.S.

- In the last five years, 23 percent of U.S. homeowners saw property damage or loss as a result of severe weather, and 65 percent are prepping homes for future weather events, according to a Bank of America Institute report from May 2025.

- Rebuilding after a disaster can slow the inventory recovery, potentially bumping up prices while inventory is still constrained, the report noted. Relocation to other areas after a disaster can shift demand and create more pressure on nearby markets.

- Low inventory in the Pacific Palisades in the wake of fires in January 2025 has led to the average list price for surviving homes to grow to US$9.7 million, significantly higher than historic norms. Many of those who are rebuilding are now incorporating fire-preservation features in homes to prepare for future wildfires.

Global highlights

Tammy Fahmi | Sotheby’s International Realty

“What’s driving today’s high-end market is the feeling a home delivers as much as its address,” said Tammy Fahmi, senior vice president of global servicing and strategy at Sotheby’s International Realty. “What we’re witnessing in luxury real estate isn’t just a trend — it’s a fundamental redefinition of value. This experiential revolution transcends cultural boundaries, with buyers willing to pay substantial premiums for properties that offer exceptional features that reflect their lifestyles.”

- With the Saudi Vision 2030 economic development initiative, executives and foreign companies coming into Saudi Arabia are driving luxury developments with high-end amenities. The Red Sea Project, just off Saudi Arabia’s west coast, is also expected to drive tourism to the region after it is unveiled around 2030.

- Demand for high-end properties in India has surged in the last two years, and the luxury real estate market is expected to reach a value of US$105 billion by 2030.

- Between 2012 and 2021, the highest-priced transaction in Puerto Rico rose from US$2 million to $30 million. The island has seen growth in the luxury goods market, with revenue from the industry set to reach US$533.44 million in 2025, according to Statista Market Insights.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Lillian Dickerson | Jun 25, 2025 | Industry, News Feed

Homebuyers continued to respond to market headwinds like high mortgage rates and economic uncertainty and failed to be drawn in by builder sales incentives.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

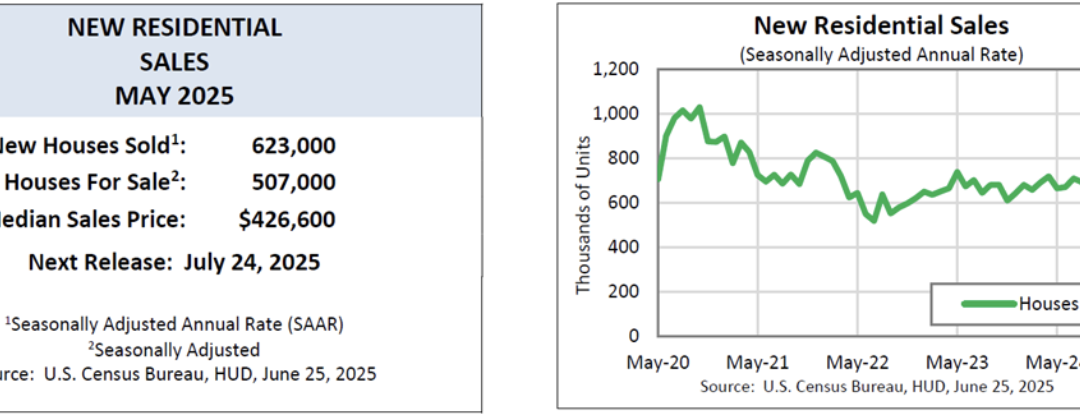

Sales of newly constructed single-family homes dropped 13.7 percent in May 2025 from the previous month, as homebuyers continued to respond to market headwinds like high mortgage rates and economic uncertainty and failed to be drawn in by builder sales incentives.

The seasonally adjusted annual rate of sales hit 623,000 in May, which was 6.3 percent below the May 2024 rate of 665,000, the U.S. Census Bureau and U.S. Department of Housing and Urban Development reported on Wednesday. The figure represented the most severe drop in new-home sales in nearly three years.

TAKE THE INMAN INTEL SURVEY FOR JUNE

The report comes on the heels of the Census Bureau and HUD’s report last week showing that housing starts slid by 10 percent in May to their lowest level since 2020.

“New home sales plunged in May,” Navy Federal Credit Union Chief Economist Heather Long said in a statement sent to Inman. “The spring and summer are shaping up to be very tough for the real estate market. Buyers are staying on the sidelines as they worry about uncertainty and high mortgage rates. New-home inventories edged up in May and remain at elevated levels. Buyers are waiting for deals and there just aren’t many of them right now.”

The seasonally adjusted inventory estimate for new homes was 507,000 at the end of May 2025, 1.4 percent above April 2025’s estimate and 8.1 percent above inventory levels in May 2024.

The figure represents 9.8 months of supply of new homes at the current sales rate, which is 18.1 percent above the April 2025 supply of 8.3 months, and 15.3 percent above May 2024 levels of 8.4 months.

In May 2025, the median sales price of new homes sold was $426,600, 3.7 percent above the median price in April and 3 percent higher than the median sales price in May 2024.

The average sales price for new homes sold in May 2025 was $522,200, 2.2 percent higher than April and 4.6 percent higher than the average in May 2024.

Email Lillian Dickerson