by Matt Carter | Jul 9, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Declining mortgage rates and a surge in for-sale listings had homebuyers scrambling to apply for mortgages last week at the fastest pace in more than two years, according to a weekly survey of lenders by the Mortgage Bankers Association.

But mortgage rates are on the rebound again as investors who fund most home loans weigh how a strong June jobs report and the Trump administration’s threats to impose new tariffs in August might affect Federal Reserve policymakers’ willingness to cut rates.

Applications for purchase loans were up by a seasonally adjusted 9 percent last week when compared to the week before, and 25 percent from a year ago, the MBA’s Weekly Mortgage Applications Survey showed.

“Mortgage rates moved lower last week, with the 30-year fixed rate decreasing to 6.77 percent, its lowest level in three months,” MBA Deputy Chief Economist Joel Kan said, in a statement.

After adjusting for the July 4th holiday, demand for purchase loans came in at the strongest pace since February 2023.

“Homebuyer demand is being fueled by increasing housing inventory and moderating home-price growth,” Kan said. “The average loan size on a purchase application, at $432,600, was at its lowest since January 2025.”

Active listing inventory was up 28.1 percent in June to a post-pandemic high, according to Realtor.com, and home prices have come down by at least a full percentage point in nearly one-third of the 100 largest U.S. housing markets tracked by ICE Mortgage Technology.

After spiking in April following President Trump’s “liberation day” tariff announcement, mortgage rates were trending down during June on hopes that trade negotiations would forestall implementation of additional “reciprocal tariffs.”

Mortgage rates on the rebound

Rates for 30-year fixed-rate mortgage came down from 6.92 percent on May 21 to 6.64 percent on July 1 — a drop of nearly 30 basis points, according to rate lock data tracked by Optimal Blue.

Although the Trump administration pushed back plans to impose reciprocal tariffs on July 9, mortgage rates are on the rise again as the White House sends warning letters to countries that will face higher tariffs on Aug. 1 if they don’t make trade deals.

Nearly two dozen countries including Japan, South Korea, Indonesia, Thailand and Cambodia have received letters from the Trump administration so far, the Associated Press reported.

At 6.74 percent Tuesday, rates on 30-year fixed-rate mortgages are up 10 basis points from July 1. A basis point is one hundredth of a percentage point.

Tariffs are a concern to investors who buy mortgage-backed securities that fund most home loans because of their potential to be passed on to consumers in the form of higher prices, rekindling inflation.

The Trump administration has been pressuring the Federal Reserve to lower short-term interest rates, and demanded that Fed Chair Jerome Powell resign.

But after cutting short-term interest rates by a full percentage point at the end of last year only to see mortgage rates go up, Fed policymakers have said they’re waiting to see how the Trump administration’s tariff policies shake out, and what impact they have on the economy.

At 15.8 percent, the effective rate of all tariffs already in place is the highest since 1936, and will push prices up by 1.5 percent, according to a June 17 analysis by The Budget Lab at Yale.

Job growth and unemployment

The Fed is wrestling with its dual mandate to maximize employment while keeping inflation in check.

According to the latest numbers from the Bureau of Labor Statistics, the U.S. economy added 147,000 jobs in June — 37,000 more jobs than forecasters had expected.

Job growth cooling

The July 3 report pushed mortgage rates and yields on government bonds up, as it gave Fed policymakers more leeway to wait until September to lower short-term interest rates.

There are even doubts about a September rate cut. The CME FedWatch Tool, which tracks futures markets to predict the probability of future Fed moves, on Wednesday put the odds of a September rate cut at 71 percent, down from 94 percent on July 2.

But in the long term, job growth is cooling, and forecasters at Pantheon Macroeconomics are calling the recent rise in rates “nonsensical.”

Much of June’s job growth, they say, was due to an artificial construct of seasonal adjustments that calls into doubt estimates that state and local government jobs grew by 80,000 last month, including 64,000 education jobs.

With downward revisions of monthly job growth from initial estimates averaging 29,000 since January 2023, “underlying job growth probably was close to zero,” Pantheon forecasters said in their July 7 U.S. Economic Monitor.

Unemployment trending up

Pantheon forecasters expects the unemployment rate to rise from 4.1 percent in June to about 4.75 percent in Q4, which they think would motivate the Fed to cut short term rates by a total of 75 basis points at its final three meetings of the year.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 9, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Mortgage giants Fannie Mae and Freddie Mac weren’t informed in advance that they would be required to sign off on loans qualified using the new VantageScore 4.0 credit score algorithm, mortgage industry insider Christopher Whalen said Wednesday.

Because rating agencies and bank regulators aren’t prepared to work with the new score either, Whalen said he expects lenders will be slow to make the switch to VantageScore 4.0 — a credit scoring algorithm developed by the big three credit bureaus to challenge the FICO Classic score now used by most mortgage lenders.

Bill Pulte, the director of Fannie and Freddie’s federal regulator, announced new rules for evaluating borrowers who apply for conventional loans backed by the mortgage giants on the social media platform X Tuesday.

Changes to those rules were mandated by Congress in 2018, and the Federal Housing Finance Agency had been working with lenders for several years on implementing them.

But Pulte’s announcement appeared to depart from the carefully laid-out plan previously put forward by the FHFA.

The FHFA announced in 2022 that it had signed off on VantageScore 4.0 and a new FICO score, FICO 10 T, for future use by Fannie and Freddie. Under a timeline proposed in 2023, lenders were to move from the current Classic FICO credit score model and start using both VantageScore 4.0 and FICO Score 10 T by the end of this year.

But Fannie and Freddie abandoned that timeline on Jan. 16 — four days before President Trump’s inauguration — with no explanation.

In announcing on X that Fannie and Freddie would be required to start accepting loans evaluated using VantageScore 4.0 on Tuesday, Pulte caught mortgage lenders by surprise — and left them wondering exactly how the new rules will work.

The Mortgage Bankers Association issued a cautious statement welcoming the move, saying Pulte’s proposal “could help to accomplish the goals of added competition in the credit score space and reduced consumer costs, if implemented correctly.” But the trade group said there are “numerous implementation questions” that need to be addressed in order to realize such benefits.

Because the FHFA didn’t issue a formal rule or issue a press release Tuesday, mortgage lenders were left wondering:

- Will lenders be allowed to submit loans reviewed using only VantageScore 4.0, or will Fannie and Freddie also require FICO Classic scores currently in use?

- Are there still plans to allow Fannie and Freddie to accept loans scored by the new FICO Score 10 T?

- Will loan level pricing adjustments (LLPAs — fees charged by Fannie and Freddie according to borrower risk) be different for borrowers scored by VantageScore 4.0?

- Are private mortgage insurers (required by Fannie and Freddie when borrowers put less than 20 percent down) ready to back loans scored using only VantageScore 4.0?

- Will investors in mortgage-backed securities (MBS) — the ultimate source of funding for most mortgages — treat loans scored using VantageScore 4.0 the same as loans scored with FICO Classic?

Rating agencies, banks and investors still use FICO Classic, Whalen said on X, and “there is no track record” of how mortgages evaluated using VantageScore 4.0 or FICO Score 10 T will perform.

(In December, Fair Isaac announced that Cardinal Financial had sold the first batch of government-issued mortgage-backed securities to include VA loans qualified using the FICO Score 10 T. More than 21 mortgage lenders use FICO Score 10 T for non-Fannie and Freddie loans, the company said at the time.)

Whalen, an industry veteran with connections at Fannie and Freddie, is chairman of Whalen Global Advisors LLC. His past experiences include senior research positions at Kroll Bond Rating Agency and Carrington Holding Co.

“This ill-considered decision by Pulte will force buyers of loans to come up with a ‘transition table’ for Vantage 4 to FICO 10, but such attempts will be imprecise,” Whalen posted on the social media platform X Wednesday.

The FHFA, Fannie Mae and Freddie Mac did not respond to Inman’s requests for comment.

The National Association of Realtors welcomed Pulte’s announcement Wednesday, saying it will allow mortgage lenders to use VantageScore 4.0 “alongside or in place of traditional FICO scores” when assessing borrower creditworthiness.

Pulte — who, after being appointed by the Trump administration to lead the FHFA, purged Fannie and Freddie’s boards of directors and made himself the chair of both companies — claims allowing lenders to use VantageScore 4.0 will help more renters qualify for a mortgage.

Bill Pulte

“Today, we allowed for RENT payments to COUNT toward qualifying for a MORTGAGE,” Pulte posted on X Tuesday. “If ‘Obama’ or ‘Biden’ did that (they didn’t), it would be nonstop news coverage. When President Trump does it, very few people report it.”

But FICO Score 10 T also considers “trended credit data and additional data such as rent, utility, and telecom payments, which are not currently considered as part of the Classic FICO score,” Fannie Mae noted in a January update on plans to transition to the new scores.

The move to require Fannie and Freddie to accept VantageScore 4.0 is a victory for the big three credit bureaus who developed it — Equifax, Experian and TransUnion. VantageScore claimed Tuesday that implementation of the new score will boost the eligible pool of mortgage applicants by 5 million borrowers.

The credit bureaus maintain files on consumers, tracking their debts and repayment history — information that’s fed into credit score algorithms developed by FICO and VantageScore to generate credit scores.

Fee increases by both Fair Isaac and the credit bureaus have been a source of frustration for lenders and their clients. But Pulte also backed down from the FHFA’s original proposal to move from tri-merge to bi-merge credit reporting, which would have allowed lenders to pull credit scores from two credit bureaus instead of three.

TransUnion had opposed plans to move to bi-merge reporting, claiming that using only two credit scores “will often result in an incomplete and inaccurate picture being painted of a potential borrower — particularly if a consumer’s most favorable set of credit data is the one that gets excluded.”

In a blog post last month, MBA President Bob Broeksmit characterized tri-merge reporting as “an anachronism from the days when there were significant disparities in coverage by the credit bureaus.”

Broeksmit said the MBA has been studying the feasibility of using a single credit report to score government-guaranteed loans, an approach that “would mirror that of most other consumer finance markets, including home equity loans and auto loans – which have seen success with this structure.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 8, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Fannie Mae and Freddie Mac’s federal regulator will allow mortgage lenders to start using a new credit score algorithm developed by the big three credit bureaus to take on the venerable FICO score.

But when employing the new VantageScore 4.0 algorithm, lenders will still be required to use a “tri-merge” process in which three scores are calculated separately by each of the major credit bureaus.

The Biden administration had proposed requiring lenders to use two credit scoring algorithms — VantageScore 4.0 and FICO Score 10 T — to obtain scores from two credit reporting agencies (in a “bi-merge” report), for a total of four scores.

It’s not entirely clear how the new Federal Housing Finance Agency (FHFA) policy for scoring borrowers will work — if, for instance, lenders will have the option of using VantageScore 4.0 instead of the Classic FICO score now in use, or if they’ll be required to use it in addition to Classic FICO.

FHFA Director Bill Pulte summarized the changes on the social media platform X Tuesday, saying they were “effective today.” The FHFA did not issue a press release, and Pulte did not post a copy of the official directive on X, as he has with some past orders.

The FHFA did not respond to Inman’s requests for comment.

Pulte said that Fannie and Freddie will allow lenders to use VantageScore 4.0, but that tri-merge reporting will stay in effect.

TransUnion — one of the credit bureaus behind VantageScore 4.0 — has long opposed plans to move to bi-merge reporting, claiming that using only two credit scores “will often result in an incomplete and inaccurate picture being painted of a potential borrower — particularly if a consumer’s most favorable set of credit data is the one that gets excluded.”

In a statement Tuesday, TransUnion executive Satyan Merchant welcomed FHFA’s decision to keep tri-merge reporting, saying Pulte’s comments “demonstrate a commitment to responsible mortgage lending and preserving the best possible outcome for consumers.”

“Today’s announcement means more choice for lenders and more certainty for mortgage markets, which puts homebuyers on better footing long-term,” Merchant said.

Pulte has said in the past he was “not happy” about price increases levied by the company behind the FICO score algorithm, Fair Isaac, which an industry trade group, Community Home Lenders of America, claims total 700 percent over the last 3 years.

The Mortgage Bankers Association issued a cautious statement Tuesday, saying Pulte’s proposal “could help to accomplish the goals of added competition in the credit score space and reduced consumer costs, if implemented correctly.”

The trade group said there are “numerous implementation questions” that need to be addressed in order to realize such benefits.

The MBA “looks forward to working with FHFA and [Fannie and Freddie]” to address those questions, “as well as the continued conversations around credit reporting competition,” the group said in a statement to Inman.

Assuming Fannie and Freddie will accept three VantageScore 4.0 scores (one from each credit bureau) instead of three Classic FICO scores, that could encourage competition on price.

When FICO changed its pricing structure in 2023, moving away from volume-based pricing, smaller lenders saw their costs go up by more than 400 percent, Consumer Financial Protection Bureau Rohit Chopra told industry leaders attending the MBA’s annual convention last year.

But it’s the credit reporting agencies — Equifax, Experian and TransUnion — that typically set the wholesale price that resellers pay, which is then passed on to users, Chopra said.

The credit bureaus maintain files on consumers, tracking their debts and repayment history — information that’s fed into credit score algorithms like FICO and VantageScore to generate credit scores.

VantageScore — a joint venture of Equifax, Experian, and TransUnion — claimed Tuesday that implementation of VantageScore 4.0 will boost the eligible pool of mortgage applicants by 5 million borrowers.

Fair Isaac has made similar claims about the new FICO Score 10 T, saying it can help mortgage lenders boost originations by up to 5 percent without taking on additional credit risk.

“FICO Score 10T and VantageScore 4.0 are more predictive than Classic FICO and provide a more precise assessment of credit risk,” Fannie Mae said in a January update on plans to transition to the new scores. “Also, both models consider trended credit data and additional data such as rent, utility, and telecom payments, which are not currently considered as part of the Classic FICO score.”

Legislation signed into law by President Trump in 2018 required mandatory usage of the new credit scores by lenders selling loans to Fannie and Freddie by the end of this year.

But it’s unclear if FHFA will allow mortgage lenders to start using the FICO Score 10 T on the timeline originally proposed by the Biden administration.

Historical data aimed at smoothing the adoption of the new VantageScore 4.0 model was released last year, but similar data for the FICO Score 10 T has yet to be published.

In a statement, Fair Isaac said the company “welcomes competition on a level playing field among credit score providers.” When they’re originating loans not subject to Fannie and Freddie’s requirements, mortgage lenders have “rapidly embraced FICO Score 10 T’s ability to deliver lower costs and greater access for homebuyers,” the company said.

In December, Fair Isaac announced that Cardinal Financial sold the first batch of government-issued mortgage-backed securities to include VA loans qualified using the FICO Score 10 T. More than 21 mortgage lenders use FICO Score 10 T for non-Fannie and Freddie loans, the company said at the time.

Shares in Fair Isaac lost as much as 19 percent of their value Tuesday afternoon, but recovered most of those losses to close down 9 percent.

Editor’s note: This story has been updated to include a comment by Fair Isaac.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 7, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Home prices have come down by at least a full percentage point in nearly one-third of the 100 largest U.S. housing markets even as many homebuyers stretch their finances to the limits to take out a mortgage.

Several markets have seen double-digit price declines from recent peaks, as price softening continues to spread from the Sunbelt into the Western U.S., ICE Mortgage Technology reported Monday.

While the inventory of homes for sale continues to grow at an accelerating pace, it remains to be seen whether softening home prices will keep some would-be sellers on the sidelines — as happened in late 2022 and early 2023, ICE reported.

ICE’s latest Mortgage Monitor Report suggested the market is on track to return to pre-pandemic inventory levels this fall, with listings already normalized in 39 of the 100 largest markets and 11 more on pace to get there by the end of the year.

Denver, where listings are up 100 percent from 2017-2019, has posted the biggest inventory gains, followed by Lakeland, Florida and Colorado Springs, Colorado (up 87 percent), Austin (up 69 percent) and Seattle (up 61 percent).

“California continues to be an area to watch closely, with the 10 largest markets seeing 42-75 percent inventory growth over the past 12 months,” ICE analysts noted. “While only three of its 10 largest markets (San Francisco, San Jose, and Stockton) have normalized, the remaining seven are on pace to do so by the end of this year, which could lead to softening price dynamics across the state.”

Swelling inventory and mortgage rates in the high sixes continues to cool home price growth, with early June data showing national home prices appreciated by just 0.3 percent on a seasonally adjusted annualized rate, ICE reported.

While home prices continue to climb in many Midwest and Northeast markets, 41 Sunbelt and Western markets saw prices drop on a seasonally adjusted basis in June.

Markets in Texas and Florida have seen double-digit price declines from peak levels, and parts of California, Arizona, Colorado, and Idaho have also seen prices come down more than 3 percent from recent highs.

“Thirty-one of the 100 largest markets in the U.S. have now seen prices dip by at least a full percentage point from their recent highs, suggesting the number of markets experiencing annual price declines may be poised to trend higher in coming months,” ICE analysts said.

Markets with biggest price declines from peak

- Austin, Texas (-19.7 percent)

- Cape Coral, Florida (-13.3 percent)

- North Port, Florida (-11.2 percent)

- San Francisco, California (-8.9 percent)

- Phoenix Arizona (-5.7 percent)

- San Antonio, Texas (-5.2 percent)

- Boise City, Idaho (-5.2 percent)

- Deltona, Florida (-4.0 percent)

- Stockton, California (-3.7 percent)

- Denver, Colorado (-3.6 percent)

- Tampa, Florida (-3.5 percent)

- Dallas, Texas (-3.2 percent)

- Palm Bay, Florida (-3.1 percent)

- Lakeland, Florida (-3.1 percent)

- Sacramento, California (-3.0 percent)

- San Jose, California (-2.9 percent)

- Provo, Utah (-2.8 percent)

- Miami, Florida (-2.3 percent)

- Colorado Springs, Colorado (-2.3 percent)

- Jacksonville, Florida (-2.2 percent)

- Oxnard, California (-1.9 percent)

- Orlando, Florida (-1.9 percent)

- Seattle, Washington (-1.9 percent)

- Portland, Oregon (-1.8 percent)

- Ogden, Utah (-1.6 percent)

- Los Angeles, California (-1.4 percent)

- Salt Lake City, Utah (-1.3 percent)

- San Diego, California (-1.3 percent)

- Bakersfield, California (-1.2 percent)

- Memphis, Tennessee (-1.2 percent)

- Riverside, California (-1.1 percent)

Seasonally adjusted price changes from local market post-pandemic peaks. Source: ICE Mortgage Monitor, July 2025.

While mortgage lenders are seeing an uptick in applications, underwriting standards remain tight and buyers face “significant affordability challenges,” ICE noted.

With average back-end debt-to-income ratios hitting 40 percent in May, borrowers needed an average credit score of 738, close to last year’s high.

“Loan amounts for purchase loans topped an average of more than $375,000 in May, and the average loan-to-value ratio topped 85 percent, so affordability is very stretched,” ICE reported.

To get their foot in the door, just over 5 percent of homebuyers are relying on adjustable-rate mortgages, and another 3 percent are opting for temporary interest rate buydowns.

More homeowners are underwater

While falling home prices could provide relief for homebuyers, they could also leave more homeowners underwater on their loan — owing more than their house is worth.

For now, ICE estimates that only about 538,000 homeowners are underwater, up from 339,000 a year ago.

But another 2.5 million homeowners have less than 10 percent equity in their home, up from 2 million a year ago.

If home prices fall by 10 percent, they’ll be underwater too — making it harder to avoid foreclosure if they have trouble making their mortgage payments.

“While the number of homeowners underwater on their mortgage is still relatively low, it’s beginning to grow in some markets, especially among mortgage holders who purchased more recently,” ICE noted.

Buyers who made small down payments are most likely to have no equity, with close to 5 percent of VA mortgages and 2.6 percent of FHA loans underwater.

Only 3.2 percent of homeowners were delinquent on their mortgage payments in May, close to the all-time low.

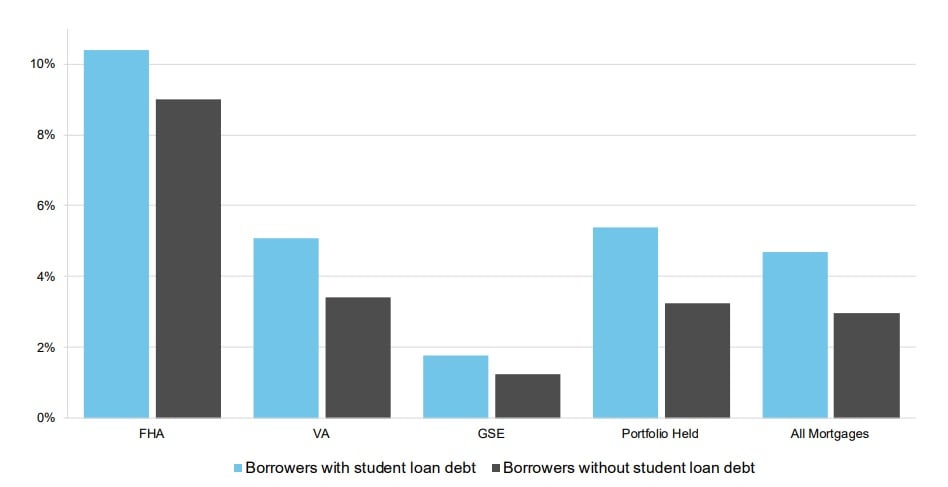

Mortgage delinquencies by loan type

Source: ICE McDash and Tradelines powered by TransUnion.

While delinquency rates are low on portfolio loans made by private lenders and “GSE” loans backed by Fannie Mae and Freddie Mac, late payments on FHA and VA loans have been on the rise.

One issue among those borrowers is student loan debt. After pausing collections on defaulted student loans during the pandemic, the Department of Education resumed those efforts in May.

Nearly 30 percent of FHA borrowers and 20 percent of VA borrowers also have student loan debt.

Tim Bowler

“We’re seeing early signs of risk building within specific markets and within specific borrower populations, like borrowers with limited equity or who are behind on student loans,” ICE Mortgage Technology President Tim Bowler said, in a statement. “This is when proactive monitoring and data-driven risk management become essential. Identifying and engaging these borrowers early may prevent hardship later.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 7, 2025 | Industry, News Feed

Fannie Mae survey echoes polls by the University of Michigan and the Conference Board that found uncertainty over tariffs is weighing on consumer confidence.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

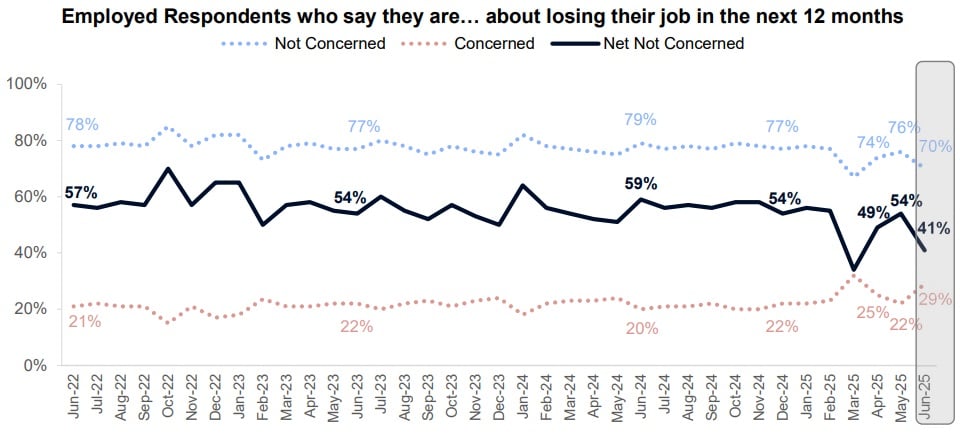

After hitting its highest level of the year in May, consumer sentiment toward housing deteriorated in June as Americans became more concerned about losing their jobs and less certain that mortgage rates will come down in the next year.

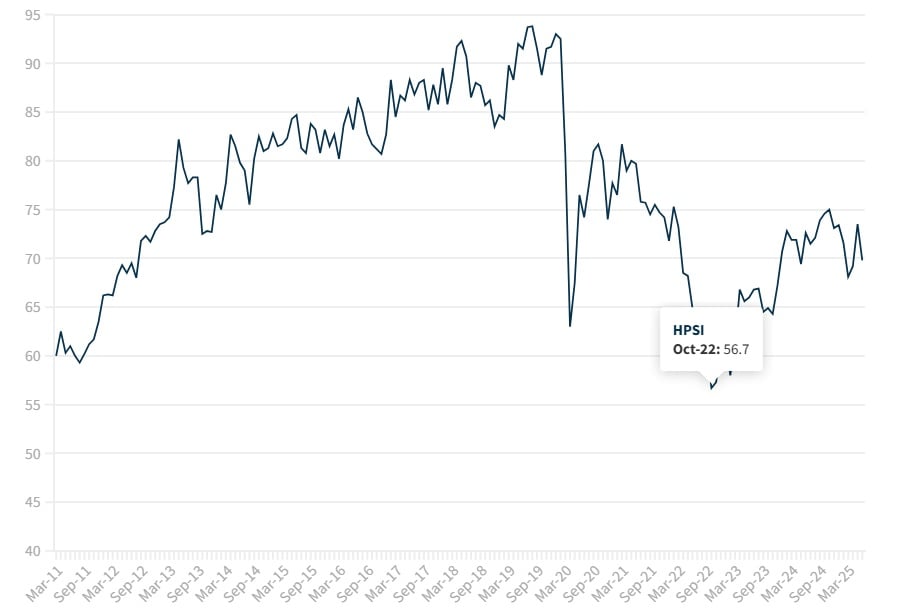

At 69.8, Fannie Mae’s Home Purchase Sentiment Index (HPSI) was down 3.7 points from May to June and 2.8 points from a year ago, the mortgage giant announced Monday.

The decline in Fannie Mae’s HPSI echoes consumer sentiment surveys conducted in June by the University of Michigan and the Conference Board, which showed uncertainty over tariffs weighing on consumer confidence. Consumers are currently paying an average effective tariff rate on imports of 15.8 percent — the highest since 1936, according to a June 17 analysis by The Budget Lab at Yale.

The Trump administration has delayed until Aug. 1 additional country-specific “reciprocal tariffs” that had already been postponed once to July 9. The White House said Monday that 14 countries were notified that they’ll face reciprocal tariffs next month, with additional notifications to go out in the days ahead, CNBC reported.

Goods from Japan and South Korea will be hit with a 25 percent import tax on Aug. 1, for instance, Trump informed the countries in letters shared on Truth Social.

“Tariffs remained on top of consumers’ minds and were frequently associated with concerns about their negative impacts on the economy and prices,” Conference Board Senior Economist Stephanie Guichard said in a statement. “Inflation and high prices were another important concern cited by consumers in June.”

Fannie Mae HPSI tracks consumer housing sentiment

Launched in 2011, Fannie Mae’s HPSI distills six questions from the mortgage giant’s monthly National Housing Survey into a single number.

The index plummeted in the spring of 2020 at the outset of the COVID-19 pandemic and hit an all-time low of 56.7 in October 2022, when home prices and mortgage rates were climbing.

At its current level, the HPSI is about where it was in the summer of 2012, when home purchase sentiment was rebounding from the 2007-2009 housing crash and Great Recession.

While “similar in spirit” to the University of Michigan and Conference Board surveys, the HPSI “is specifically devoted to the housing market,” and increases in the index “have been quite reliably followed by stronger housing markets,” Fannie Mae researchers said in an overview.

Five out of six HPSI components decreased in June. In addition to being more worried about losing their jobs and less convinced mortgage rates will fall, Americans were less certain that home prices will keep rising in the year ahead and that conditions are good for sellers.

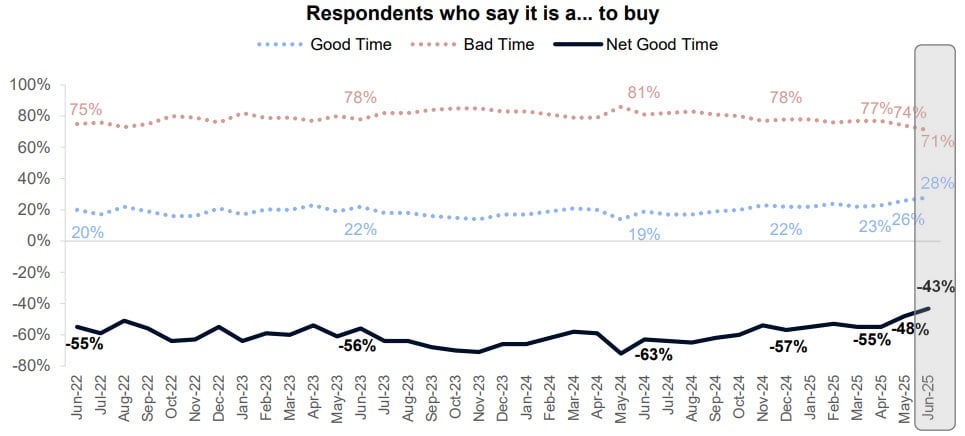

While just 28 percent of the 1,313 household financial decision makers surveyed by Fannie Mae between June 1 and June 17 said it was a good time to buy, that’s up two percentage points from May and nine percentage points from a year ago.

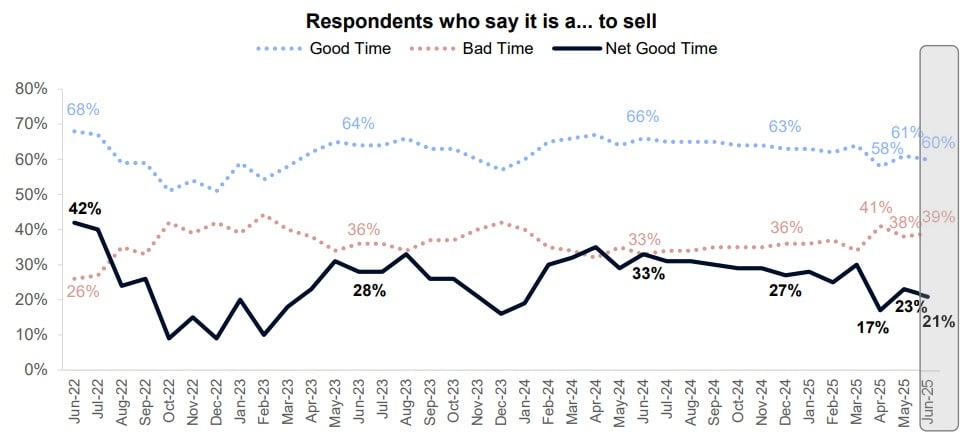

Although six in 10 Americans surveyed in June (60 percent) said it was a good time to sell, that’s down from 61 percent in May and 66 percent a year ago.

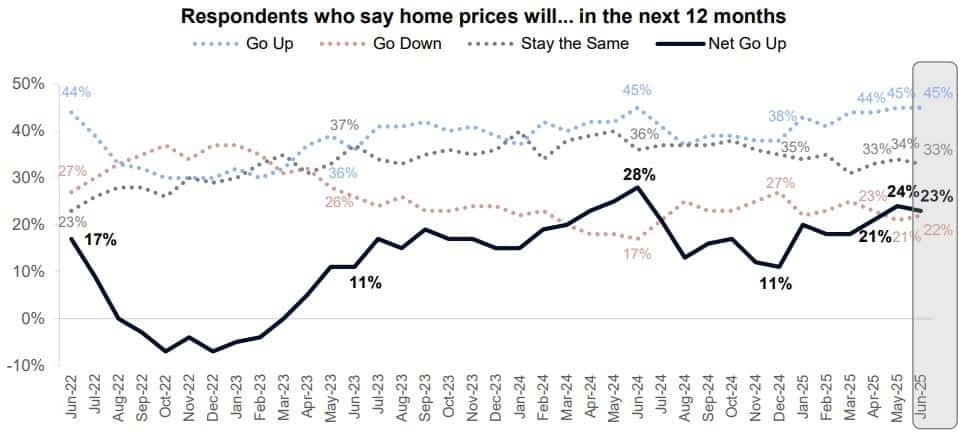

The share of survey respondents who expect home prices will go up in the next 12 months was unchanged in June at 45 percent.

But the share who said they expect home prices to go down — 22 percent — was up one percentage point from May and five percentage points from a year ago.

Although falling home prices might help boost sales, Fannie Mae’s HPSI treats a decline in home price expectations as a negative for consumer housing sentiment.

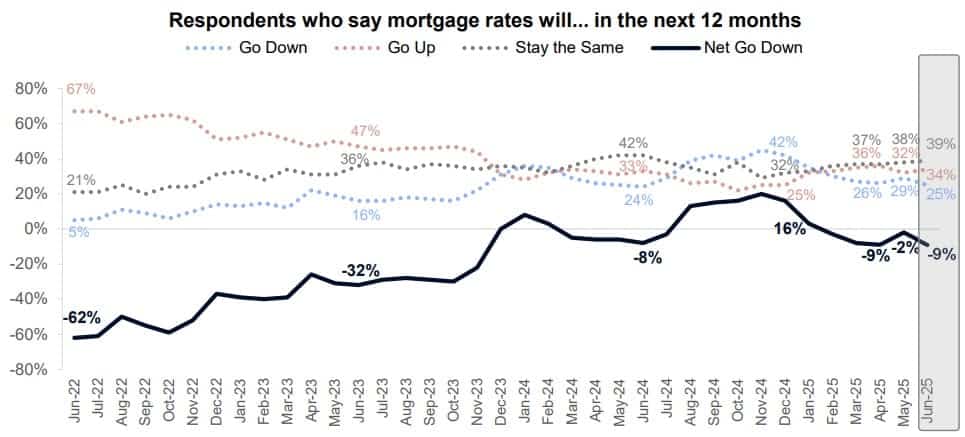

While close to one in three Americans (29 percent) surveyed in May said they expected mortgage rates to come down in the year ahead, that share dropped to 25 percent in June.

The Federal Reserve is expected to hold short-term interest rates steady until September, as policymakers assess the impact of the Trump administration’s tariffs, tax cuts, deregulation and deportations.

Fannie Mae economists last month predicted mortgage rates will drop to 6.5 percent by Q4 2025 and to 6.1 percent by the end of next year. Forecasters at the Mortgage Bankers Association have a more cautious outlook, predicting rates for 30-year fixed rate loans will end the year at 6.7 percent and drop to 6.4 percent by the end of next year.

Although only 29 percent of Americans polled in June said they were concerned about losing their jobs, that’s up from 22 percent in May and 20 percent a year ago.

At 4.1 percent, the unemployment rate in June was down slightly from 4.2 percent in May. But 7 million Americans were out of work, an increase of 1 million from June 2023.

Although not factored into the HPSI, 67 percent of household decision makers surveyed in June said they thought the economy was on the wrong track, up from 64 percent in May.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter