by Matt Carter | Jul 2, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Mortgage rates continue to trend down, sparking interest in refinancing but not doing much to get homebuyers off the fence last week, according to a weekly survey of lenders by the Mortgage Bankers Association.

The MBA’s Weekly Mortgage Applications Survey showed applications to refinance were up 7 percent last week compared to the week before, and 40 percent from a year ago.

Demand for purchase loans was essentially unchanged from the week before, but up 16 percent from a year ago.

Joel Kan

Requests to refinance accounted for 40 percent of all mortgage applications, “as overall uncertainty continues to hold homebuyers out of the market,” MBA Deputy Chief Economist Joel Kan said in a statement.

At 6.64 percent Tuesday, rates on 30-year fixed-rate mortgages are down 28 basis points since May 21 and 41 basis points from a 2025 high of 7.05 percent registered on Jan. 14, according to rate lock data tracked by Optimal Blue.

Mortgage rates trending down

But there’s no telling if the downward trend in mortgage rates is sustainable, economists say. Hopes that home sales will pick up could depend on additional inventory coming onto the market, which could cool or reverse home price gains.

MBA economists are forecasting that rates on 30-year fixed-rate loans will end the year about where they are now, while Fannie Mae predicts rates will drop to 6.5 percent by Q4 2025 and to 6.1 percent by the end of next year.

Federal Reserve policymakers have signalled that they expect to cut short-term interest rates twice later this year to keep unemployment in check. They’ve been holding off on taking action until they see whether the Trump administration’s policies in areas including tariffs, immigration, taxes and regulation impact inflation.

Ongoing tariff negotiations have added to the uncertainty, with a 90-day pause on country-specific “reciprocal tariffs” set to expire on July 9.

With consumers already paying baseline tariffs of 10 percent on about 35 percent of all imports and even higher rates on some other goods, the average effective tariff rate on imports is currently 15.8 percent — the highest since 1936, according to a June 17 analysis by The Budget Lab at Yale.

If the Trump administration follows through on threats to raise tariffs on imports from the European Union to 50 percent, to 35 percent on imports to Japan, and to 25 percent on other countries, the average effective tariff rate will rise by 6 percentage points, economists at Pantheon Macroeconomics said in their July 3 U.S. Economic Monitor report.

That would boost the impact of tariffs on consumer prices to 1.5 percent, up from 1 percent today, Pantheon forecasts.

“In the end, however, we expect any ratcheting-up of the tariffs to be short-lived,” Pantheon economists Samuel Tombs and Oliver Allen wrote. “Other countries will respond forcefully; they all saw Mr. Trump fold to pressure from China in May.”

Inflation moved away from Fed’s target in May

The latest reading of the Federal Reserve’s preferred inflation gauge, the personal consumption expenditures (PCE) index, shows consumer spending shrank by $29.3 billion in May, and that the annual rate of inflation moved away from the Fed’s 2 percent goal, to 2.3 percent.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 2, 2025 | Industry, News Feed

Housing trade groups — including NAR, MBA and NAHB — like tax breaks for homebuyers and businesses, and urge lawmakers to put the bill on Trump’s desk

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

It might not be a big hit with most Americans, but the “big, beautiful bill” that squeaked through the Senate Tuesday includes a number of perks the real estate industry has lobbied hard for.

The budget reconciliation bill — which would extend tax cuts enacted in 2017 and cut spending on programs like Medicaid, among other things — is headed back to the House for final approval after a 51-50 Senate vote.

With Republicans Susan Collins, Rand Paul and Thom Tillis voting against the bill, it was up to Vice President J.D. Vance to cast the tie-breaking vote in the Senate.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

Key provisions for the real estate industry include protections for the mortgage interest deduction — which makes interest payments on mortgage debt up to $750,000 tax deductible — and a quadrupling of the state and local tax (SALT) deduction cap.

Lobbyists for the National Association of Realtors have been working to persuade lawmakers for months of the value of those and other perks, the trade group said Tuesday, boasting that NAR secured its top five objectives in the Senate bill.

Shannon McGahn

“We were invited to the White House on Friday — just days before the final vote — to continue advocating for our members and consumers as the Senate version took shape,” NAR Chief Advocacy Officer Shannon McGahn said in a statement. “The administration and Congress respect the voice of our members and the roles they play as leaders in their communities. We are an army of advocates living and working in every ZIP code in America with a unique insight into the state of the economy.”

In addition to the mortgage interest deduction and SALT deduction cap, NAR’s top priorities included a permanent extension of lower individual tax rates, an enhanced and permanent qualified business income deduction, and protection for business SALT deductions and 1031 like-kind exchanges.

The Mortgage Bankers Association also had praise for the bill, including a provision that would raise the federal debt ceiling by $5 trillion and avert a government shutdown that could send mortgage rates soaring.

Bob Broeksmit

MBA President and CEO Bob Broeksmit said the bill builds on the version previously passed by the house by allowing continued tax breaks for investment in Opportunity Zones, and improvements to the Low-Income Housing Tax Credit (LIHTC) program that will facilitate more housing production.

“MBA will work with congressional leaders in the coming days to ensure that these beneficial tax policies remain intact in any final package signed into law by President Trump,” Broeksmit said in a statement.

David Dworkin

National Housing Conference President and CEO David Dworkin has called the LIHTC “the most effective tool to build and preserve affordable rental housing,” and estimated that plans to lower the bond financing threshold could produce or preserve more than 1 million affordable rental homes over the next decade.

In more general terms, the National Association of Home Builders (NAHB) urged House passage of the bill, saying it will spur economic growth and allow builders to invest more in multifamily rental construction, land development for single-family homes, and new equipment.

Buddy Hughes

“This will create a better business climate that allows builders to increase the nation’s housing supply, which is crucial to help ease America’s housing affordability crisis,” Lexington-based homebuilder and 2025 NAHB Chairman Buddy Hughes said in a statement.

Outside of real estate industry trade groups, the bill has been polarizing. Many Americans are specifically anxious about the “big, beautiful bill’s” cuts to federal programs including Medicaid, and some Republicans share those concerns, Axios noted. But some fiscally conservative Republicans who are concerned the bill’s tax breaks will add to budget deficits had advocated for even deeper spending cuts.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 1, 2025 | Industry, News Feed

With closure of merger, homebuyers get temporary rate buydown or up to $6,000 in lender credits from Rocket Mortgage when the buyer or seller is represented by a Redfin agent.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Mortgage giant Rocket Companies closed its deal to acquire real estate brokerage Redfin Tuesday, and immediately rolled out “preferred pricing” to borrowers involved in deals in which the buyer or seller is represented by a Redfin agent.

The new program, Rocket Preferred Pricing, provides a 1 percent temporary rate buydown for the first year of a loan, or up to $6,000 in lender credits to homebuyers taking out a conventional, FHA or VA mortgage from Rocket.

The program is available not only to homebuyers represented by a Redfin real estate agent, Redfin partner agent or Rocket Homes Partner Agent, but is also offered on listings represented by Redfin agents.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

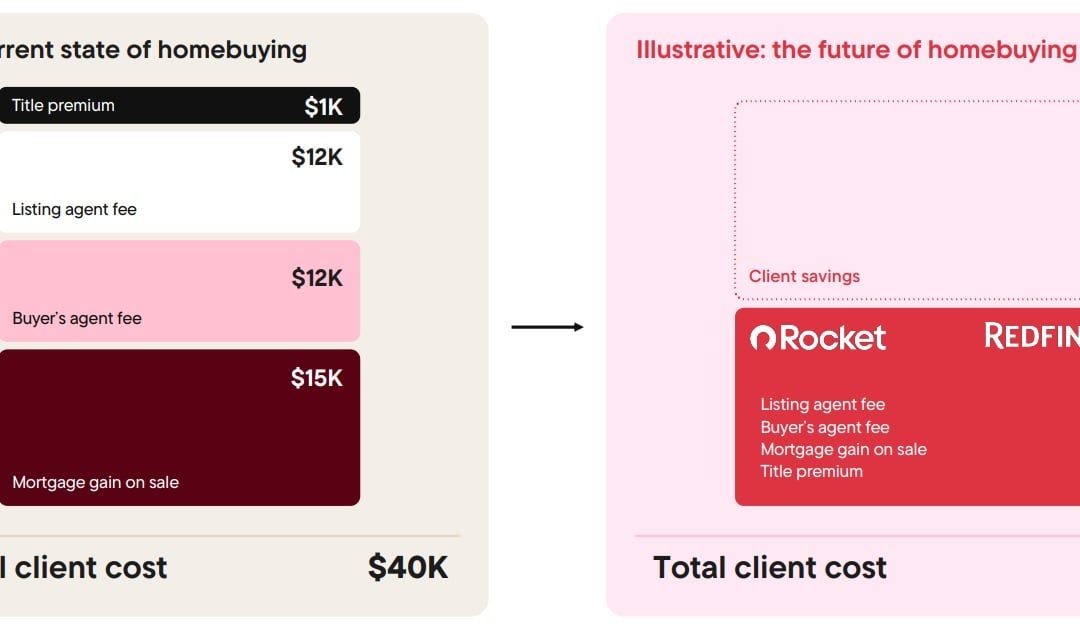

In announcing an agreement to acquire Redfin in March, Rocket executives said the deal could cut consumers’ transaction costs in half by trimming agent fees, mortgage gain-on-sale and title premiums.

By handling every aspect of homebuying and selling — from home search to mortgage financing, and title and closing — Rocket aims to cut transaction costs on the median priced home from $40,000 to $20,000.

Rocket: merger will cut transaction costs by $20K

In a March 10 investor presentation, Rocket broke down transaction costs for a $430,000, median priced home price that included $15,000 in lender profits, $12,000 each to listing and buyer’s agent, and $1,000 in title insurance.

Although the company didn’t break down savings for each category, it says it intends to bring total costs of clients who use both Rocket and Redfin down by 50 percent.

Varun Krishna

“For far too long, the homeownership process has been outdated and disconnected,” Rocket CEO Varun Krishna told investment analysts in March. “Home search, brokerage, mortgage, title, closing, servicing, all exist in separate ecosystems, forcing consumers to piece together a complex and frustrating journey.”

Senate Democrats including Elizabeth Warren, Bernie Sanders and Cory Booker expressed skepticism about claimed benefits to consumers in a June 3 letter to antitrust regulators, claiming the Redfin deal and Rocket’s plans to acquire the nation’s largest loan servicer, Mr. Cooper, creates “the potential for Rocket to steer homebuyers to its own products, hike prices based on private data, and block competition.”

Rocket will retire its home search portal, hosted on Rocket.com and Rocket’s mobile app, on Aug. 4, in favor of Redfin’s site, which it’s rebranded “Redfin powered by Rocket.”

“I’ve used Redfin every day for the last 20 years. It helped me find and fall in love with my first home, completely changing how I thought about real estate,” Krishna said in a statement Tuesday. “The Redfin team is best-in-class in building a product experience focused on simplicity. It was a perfect fit for Rocket’s vision of what the homeownership experience should be.”

Redfin will remain headquartered in Seattle, with CEO Glenn Kelman continuing to lead the business and reporting to Krishna.

Glenn Kelman

“Rocket’s and Redfin’s approaches to lending and brokerage service have always just been two halves of one vision to make the whole homebuying process magical,” Kelman blogged in March.

After leading the nation in mortgage refinancing last year, Rocket hopes acquiring Redfin will help it do more business with homebuyers.

Rocket Mortgage was the nation’s second biggest mortgage lender in 2024, with $97.6 billion in funded loans accounting for 5.4 percent of originations by volume, according to Home Mortgage Disclosure Act (HMDA) data tracked by iEmergent.

Speaking at an investment conference in May, Krishna said Rocket has set a goal of handling 8 percent of purchase mortgages and 20 percent of refinancings.

Last week, Rocket Mortgage introduced a new bridge loan product that lets existing homeowners buy before they sell and make non-contingent offers to compete with cash buyers.

Rocket on Monday announced that it had completed a reorganization of its capital structure — a move that paves the way for the acquisition of its next big acquisition target, Mr. Cooper Group Inc., the nation’s biggest loan servicer, for stock valued at $9.4 billion.

Assuming that deal closes later this year as planned, Rocket will be collecting payments on about one in six U.S. mortgages with $2.1 trillion in outstanding balances — giving the company a leg up on recapturing homeowners’ business when they’re ready to refinance.

Editor’s note: This story has been updated to note that Rocket’s home search site is hosted on Rocket.com and Rocket’s mobile app.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 1, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

After staying stuck in the high sixes for two months, mortgage rates are coming back down as investors seeking certainty pull money out of the stock market and move it into bonds and mortgage-backed securities that fund most home loans.

But there’s no guarantee that the downward move in mortgage rates is sustainable, economists say, and hopes that home sales will pick up may hinge more on additional inventory coming onto the market, which is expected to cool or reverse home price gains.

After popping in April over concerns that the Trump administration’s tariff policies could reignite inflation, mortgage rates have been trending down since May 21.

At 6.67 percent Monday, lender data tracked by Optimal Blue shows rates on 30-year fixed-rate mortgages are down 25 basis points since May 21 and 38 basis points from the 2025 high of 7.05 percent registered on Jan. 14.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

A basis point is one hundredth of a percentage point. So rates have come down by 1/4 percentage point in the last five weeks — more than halfway to the 2025 low of 6.48 percent seen on April 4.

“The drop in rates is small but still helpful,” National Association of Realtors Chief Economist Lawrence Yun said in a statement to Inman.

Mortgage rates trending down

Yun noted that 10-year Treasury yields — a barometer for mortgage rates — have made a similar downward move, and pointed out a few key reasons behind the trend.

Lawrence Yun

“First, there is an improved prospect of tariff negotiations,” Yun said. “Second, the likelihood of a Fed rate cut in September — or possibly even sooner — has increased, with two voting members publicly stating support for a July rate cut. Finally, actual inflation is calmer than forecasted in April and May, helped by decelerating shelter costs.”

Although the Trump administration has been putting the heat on Federal Reserve Chair Jerome Powell to lower short-term interest rates, mortgage rates are determined largely by investor demand for mortgage-backed securities (MBS).

When the prospects for economic growth look precarious, investors pile into MBS and government bonds seeking safe returns. More demand for bonds and MBS drives up their prices and brings down their yields.

But when inflation looks like a potential threat to their returns, investors will demand higher yields — driving up borrowing costs for homebuyers.

When the Fed cut short-term rates three times at the end of last year by a full percentage point, mortgage rates went up as investors weighed incoming data showing inflation moving away from the central bank’s 2 percent goal.

Where interest rates are headed next depends in large part on the outcome of ongoing tariff negotiations and Congress’ tax and spending policies, and forecasting mortgage rates can be a tricky business.

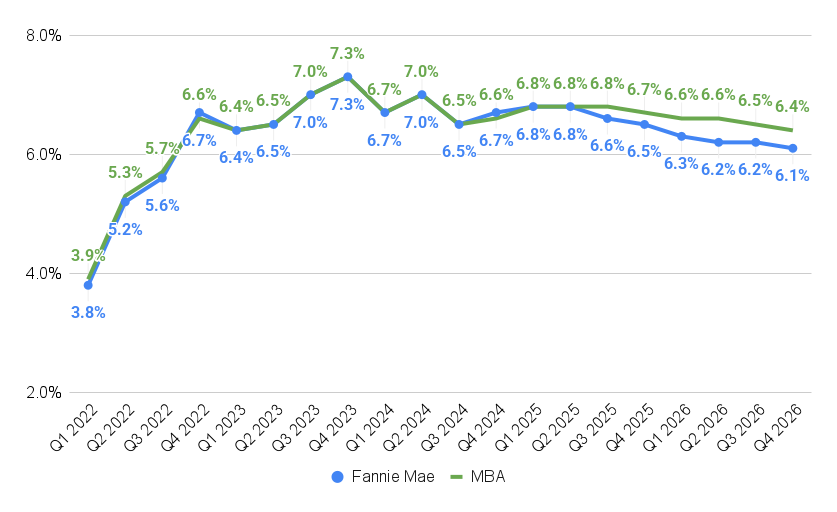

But in their latest forecast, economists at the Mortgage Bankers Association on June 20 predicted rates for 30-year fixed rate loans will end the year about where they are now — at 6.7 percent.

Mortgage rates forecast to stabilize

Source: Fannie Mae and Mortgage Bankers Association forecasts, June 2025.

The MBA sees mortgage rates coming down only gradually next year, to 6.4 percent by Q4.

Edward Seiler

A June 12 forecast by Fannie Mae economists was slightly more optimistic, predicting rates will drop to 6.5 percent by Q4 2025 and to 6.1 percent by the end of next year.

MBA economist Edward Seiler, the executive director of the Research Institute for Housing America (RIHA), told Inman that cooling home price appreciation is likely to have a bigger impact on affordability than mortgage rates.

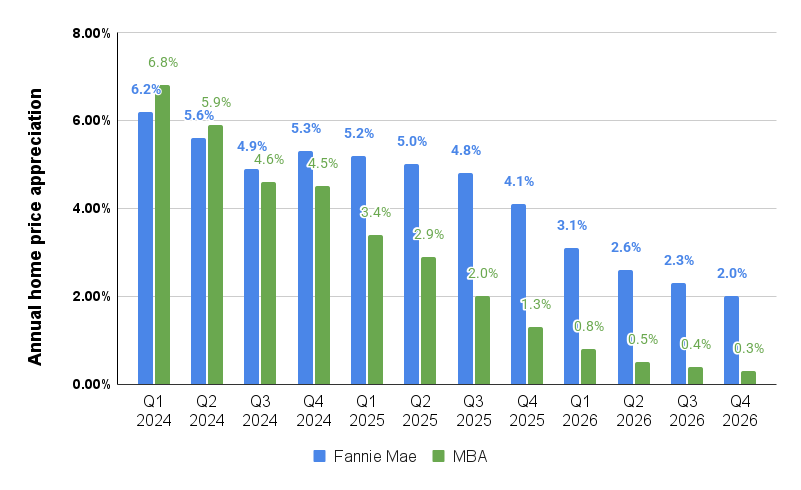

Home price appreciation expected to cool

Source: Forecasts by Fannie Mae (April 2025) and Mortgage Bankers Association (June 2025).

Fannie Mae’s home price appreciation forecast is published quarterly, and hasn’t been updated since April.

MBA forecasters in June predicted that national home price appreciation will cool to 1.3 percent by the end of this year, and to 0.3 percent by Q4 2026.

Since the MBA’s forecast also predicts that inflation will swell to 3.2 percent by the end of next year, that implies national home price growth will be negative in real terms.

Price declines are expected in markets where inventory is coming online faster than houses are sold.

Among the 20 largest housing markets tracked by the S&P CoreLogic Case-Shiller Index, two saw year-over-year declines in April — Tampa (-2.2 percent) and Dallas (-0.2 percent).

Nicholas Godec

“The underlying market dynamics remain challenging but not dire,” S&P Down Jones Indices analyst Nicholas Godec said in a statement.

Elevated mortgage rates are keeping monthly payment burdens near generational highs, and the mortgage lock-in effect continues to constrain housing supply, he said.

The supply-demand imbalance “continues to provide a price floor, preventing the sharp [price] corrections that some had feared.”

It’s a market in transition, Godec said, where “local fundamentals matter more than national trends.”

Housing and mortgage experts polled by Fannie Mae in May saw Austin, Tampa, Dallas, Denver, Houston, Miami, Phoenix, Washington, D.C., and Atlanta as markets where home prices are most likely to underperform national home price appreciation over the next 12 months.

Among the 20 largest U.S. housing markets, Boston, New York, Philadelphia, Nashville and San Diego were viewed as places where prices are most likely to go up faster than the national average.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 30, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Mortgage giant Rocket Companies completed a reorganization of its capital structure Monday that will pave the way for the acquisition of tech-forward real estate brokerage Redfin — a deal it’s claimed could cut consumers’ transaction costs in half by compressing agent fees, mortgage gain-on-sale and title premiums.

The all-stock deal, valued at $1.75 billion when announced in March, went unchallenged by antitrust regulators and was approved by Redfin shareholders on June 4.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

In announcing the completion of its reorganization in a regulatory filing, Rocket said it reduced its classes of common stock from four to two in an “Up-C Collapse” that will improve its ability to use its common stock as acquisition currency for future deals.

That includes Rocket’s next big acquisition target, Mr. Cooper Group Inc., the nation’s biggest loan servicer, for stock valued at $9.4 billion.

Company executives have said acquiring Redfin will help subsidiary Rocket Mortgage capture 8 percent of the purchase loan market, and the Mr. Cooper deal will put Rocket in touch with more homeowners who might be ready to refinance.

Detroit-based Rocket wants to handle 20 percent of U.S. mortgage refinancings, and Rocket CEO Varun Krishna said last month that the company has invested about $500 million in AI and other technology that will help the company scale its business without a proportionate increase in expenses after the mergers.

In a March 10 investor presentation, Rocket executives said that by handling every aspect of homebuying and selling — from home search to mortgage financing and title and closing — they aim to cut transaction costs on the median priced home from $40,000 to $20,000.

“For far too long, the homeownership process has been outdated and disconnected,” Krishna told investment analysts in March. “Home search, brokerage, mortgage, title, closing, servicing, all exist in separate ecosystems, forcing consumers to piece together a complex and frustrating journey.”

Redfin shareholders will receive 0.7926 shares of Rocket common stock for each share of Redfin they own. Shares in Rocket closed at $14.18 Monday, up from $9.51 per share before the deal was announced.

Redfin will remain headquartered in Seattle, with CEO Glenn Kelman continuing to lead the business and reporting to Krishna.

“Rocket’s and Redfin’s approaches to lending and brokerage service have always just been two halves of one vision to make the whole home-buying process magical,” Kelman blogged in March.

In reporting first-quarter earnings in May, Rocket executives said the Mr. Cooper acquisition remains on track to close by the end of the year.

Rocket announced on June 3 that it would issue $4 billion in debt and use the proceeds to retire notes held by Mr. Cooper subsidiary Nationstar Mortgage Holdings Inc.

Editor’s note: This story has been updated to clarify that Rocket Companies announced an “Up-C Collapse” reorganization Monday to pave the way for its closing of deals to acquire Redfin and Mr. Cooper.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter