by Matt Carter | Jun 30, 2025 | Industry, News Feed

Payment options, including Automated Clearing House (ACH), card payments, pinless debit and real-time disbursements, simplify loan servicing, improve cash flow management for lenders.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Cloud-based mortgage customer relationship management (CRM) tool Mortgage Automator now boasts a suite of payment processing options provided by Usio Inc., including Automated Clearing House (ACH), card payments, pinless debit and real-time disbursements.

San Antonio, Texas-based Usio — which provides payment solutions to merchants, billers, banks, service bureaus, integrated software vendors and card issuers — announced Monday that integration with Mortgage Automator went live in June.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

Launched in 2013 as a document-generating tool for a small private lender in Toronto, Canada, Mortgage Automator has evolved into a full-fledged originations, servicing and investor management tool with automation

Mortgage Automator became available in the U.S. in 2019 and continues to evolve, offering integrations with CoreLogic, DocuSign, Doss Docs, Hubspot, Lightning Docs, OSC Insurance Services, PrivateLenderLaw.com and Twilio, among others.

Pavel Tchourliaev

“Our mission has always been to provide private lenders with the most powerful and intuitive software solutions,” Mortgage Automator CEO Pavel Tchourliaev said in a statement. “Partnering with Usio allows us to further enhance our platform by offering integrated payment processing that simplifies loan servicing and improves cash flow management for our clients.”

Founded in 1998 as Billserv.com, Usio is a publicly traded fintech company with a $39 million market capitalization.

Usio entered the payment facilitation business with the 2017 acquisition of Singular Payments LLC, launching its “PayFac-in-a-Box” platform the following year to partner with app and software developers in the legal, healthcare, property management, utilities and insurance verticals.

Usio’s 202 acquisition of Information Management Solutions LLC (IMS) put it in the electronic and paper billing business in 2020, and it now serves hundreds of customers in industry verticals including financial institutions and utilities.

Competitors include Fiserv Inc., Elavon Inc., WorldPay, Stripe and Block Inc. (formerly known as Square).

Usio Chief Revenue Officer Greg Carter said the company is excited to partner with Mortgage Automator “and help modernize how private lenders manage payments.”

Greg Carter

“Embedding our payment technology into Mortgage Automator’s platform gives lenders the tools they need to operate more efficiently, reduce friction, and deliver a better experience for their borrowers,” Carter said in a statement. “This is another example of how software vendors in all industries can benefit from the implementation of our unique PayFac-in-a-box technology.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 27, 2025 | Industry, News Feed

Recission of a dozen regulatory policies is aimed at “slashing red tape that drives up costs and shuts families out of the market,” HUD Secretary Scott Turner said.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The Trump administration lifted “a pile of regulations” from FHA lenders Friday afternoon, eliminating a dozen policies governing flood risk management, inspections in disaster areas, appraisals, underwriter qualification and data collection.

The move is aimed at “slashing red tape that drives up costs and shuts families out of the market,” Department of Housing and Urban Development (HUD) Secretary Scott Turner said in an announcement.

TAKE THE INMAN INTEL SURVEY FOR JUNE

The policy recissions, published in a series of Mortgagee Letters, are effective immediately and will be incorporated into a future version of the Federal Housing Administration’s Single Family Housing Policy Handbook for lenders.

Builders constructing new homes in special flood hazard areas or FEMA-designated “coastal high hazard areas” will no longer be required to build homes at least two feet above the base flood elevation for their homes to qualify for FHA financing.

The new elevation standard, announced in November by the Biden administration, “would have limited the land available for development and increased the cost of construction for FHA-insured single family properties, thereby contributing to the insufficient supply of New Construction housing and rising home prices,” HUD said in rescinding it.

Lenders signing off on FHA loans in Presidentially Declared Major Disaster Areas (PDMDAs) will no longer be required to obtain mandatory damage inspection reports that identify and quantify any dwelling damage.

Instead, they “must exercise reasonable due diligence to determine if additional inspections or repairs are necessary,” HUD said.

Requiring inspections by FHA-approved appraisers in disaster areas regardless of whether any damage had occurred, “sometimes resulted in a lengthy waiting period” for mortgage approvals, and led to “unnecessary inspections, delayed loan closings, and postponed issuance of FHA insurance,” HUD maintains.

In scaling back the several requirements for appraisers, HUD said FHA “has historically imposed more extensive property appraisal protocols and more stringent procedures than those required for other mortgage lending purposes.”

Appraisers will no longer be required to confirm that the remaining economic life of a property is longer than the mortgage term. Fewer photos of properties will be required — they won’t be required to take photos of attics or crawl spaces, for example.

When analyzing the housing market in which a property is located, appraisers will still be required to determine if property values are increasing, stable or declining, but won’t have to assess whether the current trend appears to be changing.

“Current appraisal standards no longer support the need for certain FHA-specific protocols, rendering them outdated and misaligned with broader industry norms,” HUD said. “In addition, FHA’s internal collateral valuation technology and data capabilities have significantly improved, further reducing the necessity of these duplicative and antiquated appraisal requirements.”

HUD is also lowering the experience requirements for “Direct Endorsement” underwriters who have the authority to sign off on loans without prior FHA review or approval, and allowing lenders to employ them on a part-time basis.

“FHA recognizes that the financial landscape for smaller lending institutions has evolved significantly over the past decade, presenting both opportunities and challenges in sustaining growth and meeting customer needs,” HUD said of the change.

In eliminating a requirement that lenders collect information about the borrower’s language preference and any homeownership education and housing counseling they may have received, HUD said only 1.2 percent of FHA borrowers completed the form “in a manner that provided any potential benefit to them.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 27, 2025 | Industry, News Feed

Two closely watched surveys show Americans remain concerned that the U.S. is headed for the dual challenge of an economic slowdown and an increase in inflation.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Uncertainty over what tariffs the Trump administration will ultimately impose on U.S. trading partners continues to weigh on consumer confidence, according to two closely watched surveys.

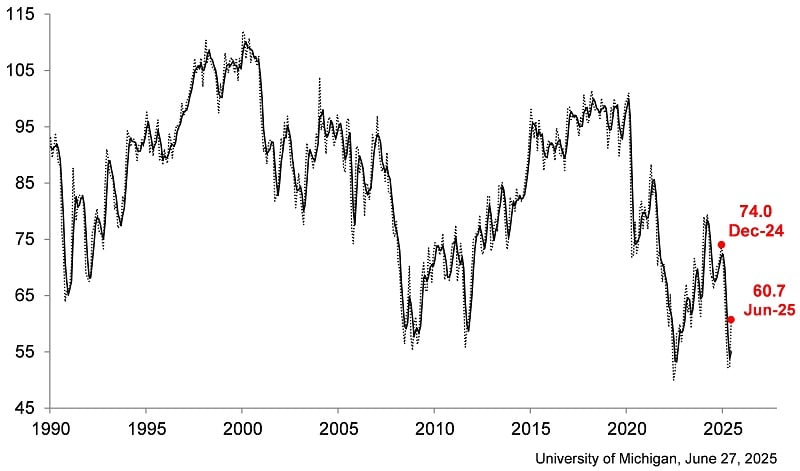

The latest reading from the University of Michigan surveys of consumers released Friday showed consumer sentiment improved for the first time in six months in June, rising 16 percent from May.

University of Michigan Index of Consumer Sentiment

But at 60.7 in June, the U of M Index of sentiment was down 18 percent from December 2024, and “consumer views are still broadly consistent with an economic slowdown and an increase in inflation to come,” survey director Joanne Hsu said in a statement.

Joanne Hsu

“Consumers continue to be concerned about the potential impact of tariffs, but at this time they do not appear to be connecting developments in the Middle East with the economy,” Hsu said.

While rising tensions with Iran initially sent oil prices up by 20 percent in June, they’ve since retreated after attacks on Iran by Israel and the U.S. did not escalate into an all-out war.

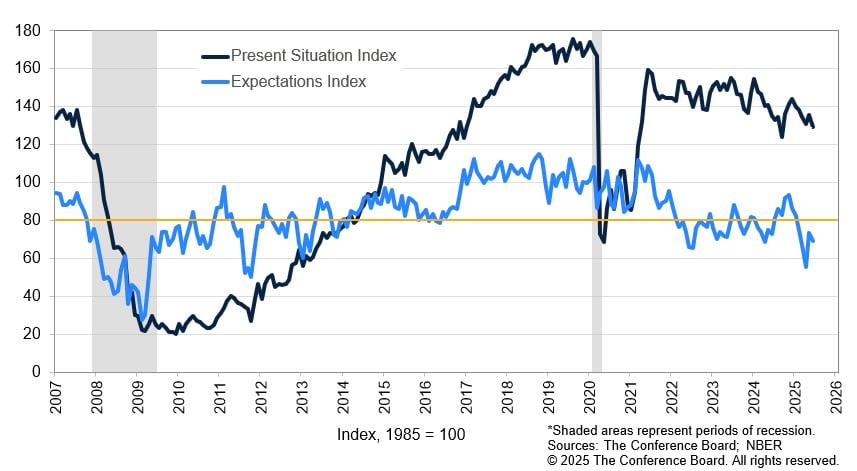

The Conference Board Consumer Confidence Index, released on June 24, retreated by 5.4 points in June, to 93. That index had previously posted its first gain in five months in May, rising 12.3 points.

Stephanie Guichard

“Tariffs remained on top of consumers’ minds and were frequently associated with concerns about their negative impacts on the economy and prices,” Conference Board Senior Economist Stephanie Guichard said in a statement. “Inflation and high prices were another important concern cited by consumers in June.”

Conference Board Present Situation and Expectations Indexes

The Conference Board’s Expectations Index, which is based on consumers’ outlook for income, business and labor market conditions, fell 4.6 points to 69, well below the threshold of 80 that often signals a recession ahead.

While many economists expect tariffs will have an inflationary impact on prices, they could also cause the economy to slow if consumers buy less and hiring slows.

Federal Reserve policymakers have signalled that while they expect to cut short-term interest rates twice later this year to keep unemployment in check, they’ve been waiting to see what impact tariffs have on prices.

The latest reading of the Federal Reserve’s preferred inflation gauge, the personal consumption expenditures (PCE) index, showed consumer spending shrank by $29.3 billion in May, and that the annual rate of inflation moved away from the Fed’s 2 percent goal, to 2.3 percent.

Ongoing negotiations have added to the uncertainty over tariffs, with the Trump administration pushing back many country-specific “reciprocal tariffs,” which were originally slated to go into effect in April, until July 9.

U.S. stock indexes hit new all-time records on Friday on news that the U.S. and China are close to reaching a trade deal, only to reverse course when President Trump said he was ending trade talks with Canada.

In the meantime, consumers are paying an average effective tariff rate of 15.8 percent on imported goods — the highest since 1936, according to a June 17 analysis by The Budget Lab at Yale.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 27, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

As chief economist for NewHomeSource, Ali Wolf manages and analyzes content for Zonda, runs special research projects and strategizes with the nation’s largest homebuilders.

As a featured speaker at Inman Connect San Diego, she’ll provide insights into economic factors, buyer behavior, and how market shifts are impacting consumers.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Wolf took the time to talk to Inman in advance of her July 31 Connect appearance. While mortgage rates and affordability present challenges for homebuyers, she said, uncertainty can be the biggest issue for many — and that’s something real estate agents can help their clients cope with. This interview has been edited for clarity and brevity.

Inman: I’m guessing you probably have a lot of data that you’re looking at. Everybody’s got their own local market, but talking just about the national market, is there anything that you’ve seen recently that stands out?

Ali Wolf: The one thing that I feel most comfortable saying about the national market is that across almost every geographic area, across almost every price point, we are in a housing market today that lacks any sense of urgency. There’s people that maybe want to buy, or can buy, that are just choosing not to. The consumer is fully steering the market today, and their uncertainty about broader things in their lives is resulting in a lot of uncertainty in the housing market.

In the past, rent versus own was kind of a coin toss. It depended on how much you could put down, and interest rates. What is happening now, almost everywhere across the country, is that renting is the obvious choice if you just look at the monthly housing cost. So it’s becoming a market where the dynamics look a lot more complicated and a lot more messy than what they have in the past.

How can real estate agents help their clients get some clarity?

There are going to be certain buyers that will be priced out. But those that could still potentially buy, they’re going to say, “Hey, if I rent, it’s $1,500 a month. If I buy, it’s $1,800 a month. I don’t want to buy because I don’t want to pay that extra money.”

Not everyone should buy, but this is where our industry should say, “What else happens when you buy a home? Well, now you’re starting to invest in yourself. Now you’re paying down your mortgage, now you’re setting yourself for retirement in the future. You’re no longer worried about what your rent increase is going to be, because you’ve now locked in the largest share of your monthly budget.”

If you look at renters versus homeowners, owners have nearly 40 times the wealth of renters. So there’s going to be the immediate objection, which is, “Why would I buy?” But then there is the logic of why you might still want to.

The advice from a lot of real estate and financial professionals is “Don’t try to time the market.” But what would you say to a buyer is thinking, “Well, maybe next year will be a better time to buy.”

People try to time the market when, at the end of the day, it’s time in market that matters. You want to be invested, and paying off that investment as soon as you can, versus trying to save 3 percent or 5 percent on the home price. That is not going to matter 10 years from now. But what you’ve invested in yourself over that time becomes more valuable.

I also would say that you can try to time the market, but you have no idea what’s going to happen in 3 years. Home prices could go down but interest rates go up. You could see interest rates go down but home prices go up. I just think there are too many unknowns.

When you look at consumer sentiment surveys, there’s a lot of uncertainty about what tariffs will mean for the economy. Unemployment has been creeping up, and consumer sentiment has been pretty dismal this year.

Let’s go back to trying to time the market. Let’s say next year, home prices start to come down and interest rates start to come down, but then everyone that’s trying to time the market time tries to come into the market at the same time. So now you’re competing with more people.

But then there’s an extra layer with tariffs, if they go through as discussed, tariffs are taxes. Taxes mean higher costs. Homebuilders, for example, are still building on some supplies that they bought pre tariffs, so their costs are not as bad. If you wait, maybe the building material costs go up, and so a builder maybe wants to lower their price, but they can’t. And then where are you?

Many existing homeowners are feeling the mortgage lock-in effect — they don’t want to sell because they don’t want to give up the low rate on their existing mortgage — and there are affordability issues in many markets. What needs to happen to bring home sales back?

The lock-in effect is one reason why we’ve seen the new home market do better, because builders can basically solve for it (by offering interest-rate buydowns and other incentives). New homes and resale homes are selling at about the same price, and new homes are offering a lot of incentives. So when given the same choice that consumers had in the past, new or resale, more people are saying a new home makes more sense.

I think time heals all wounds. Over time, the mortgage lock-in effect becomes less dramatic. If I bought a house when I was single, and I locked in a 3 percent interest rate, and then I get married and now I have two incomes, I may be in a position to move.

To see a meaningful rebound in the market, though, I think one of the most important things is consumer confidence. I think stability is the most important factor. People can adjust to higher interest rates. They can compromise on where they want to live, on certain aspects of their home. What they can’t adjust to is constant uncertainty and volatility. That will push people to the sidelines.

Obviously if interest rates came down, if home prices came down, if supply went up, if wages went up, those are all factors that could also help with the housing market.

Any predictions on the likelihood of those things happening?

You will not hear me on record forecasting mortgage rates today. There are so many moving parts.

I think the one that seems most likely is that we do see more supply. We’re already seeing that. Now, more supply can be a little bit challenging, because it can result in pricing coming down. But if we’re talking about how do we get some balance in the market, I do think more supply and a little bit of a downward pressure on pricing actually can be helpful to keeping the market moving in.

We calculate that at least 4 million homes will be sold in 2025, even as the housing market feels slow, even as the housing market feels bumpy.

That’s 4 million sales that are up for grabs. So it really becomes how do you capture your share? The pie is smaller, but if you can capture a little bit more of the share, you can still have a thriving business even in a bumpy market.

Email Matt Carter

by Matt Carter | Jun 26, 2025 | Industry, News Feed

Common Securitization Solutions (CSS) has rebranded as U.S. Fin Tech and will look to provide technology and business solutions to companies in addition to its owners.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A little-known joint venture of Fannie Mae and Freddie Mac that processes billions in mortgage-backed securities is getting a new name and an expanded mission — offering its services to other clients.

Common Securitization Solutions (CSS) is rebranding as U.S. Fin Tech, and will look to provide technology and business solutions to companies in addition to its owners.

TAKE THE INMAN INTEL SURVEY FOR JUNE

U.S. Financial Technology LLC, as CSS is now formally known, is a Delaware company co-owned by Fannie Mae and Freddie Mac and regulated by the U.S. Federal Housing Finance Agency (FHFA).

Tony Renzi

“We are excited to have a name that demonstrates that we are leading the United States and the world in financial services technology,” CEO Tony Renzi said in a statement Thursday. Renzi was appointed as CEO of CSS in 2019 and continues to lead the rebranded company.

Established as a joint venture of Fannie and Freddie in 2014, CSS operates the Common Securitization Platform (CSP), a conduit through which the mortgage giants issue and administer trillions of dollars in mortgage-backed securities (MBS) that launched in 2019.

CSS has been a fully virtual, geographically dispersed company since 2020, and boasts that its cloud-based platform provides “unrivaled layered security architecture and traceability capabilities” providing “business continuity with full disaster recovery and zero data loss within 4 hours.”

CSS “meets the challenges of the market, such as data management, processing, and speed of execution, to bridge the gap between the secondary mortgage market and investors,” the company says.

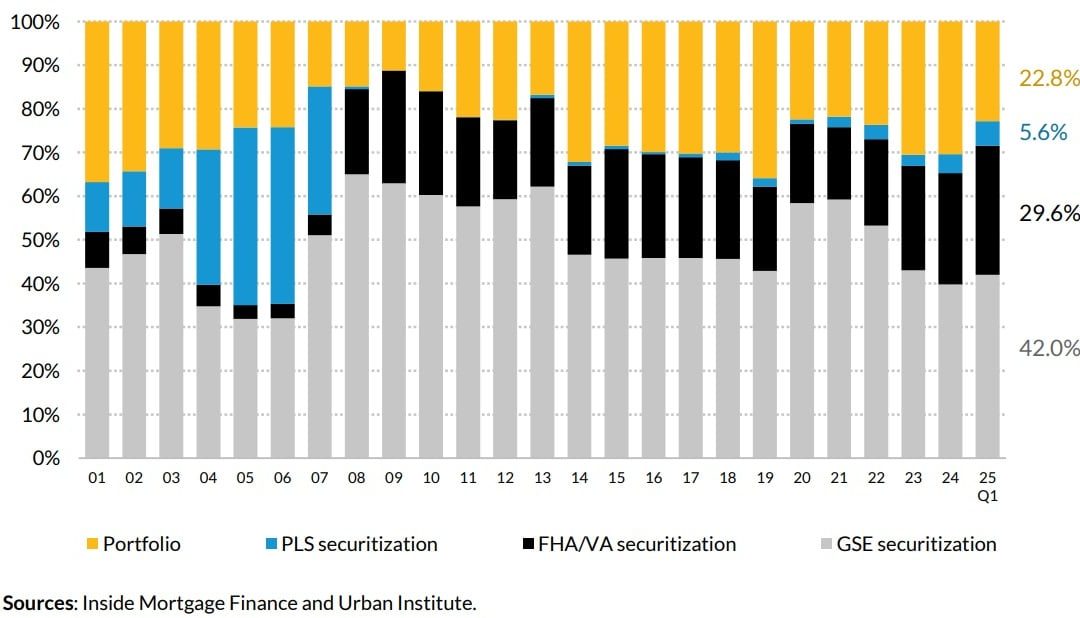

Mortgage funding sources, 2001-2025

Of the $355 billion in mortgages originated in the first quarter of 2025, Fannie and Freddie (the government-sponsored enterprises, or GSEs) packaged up 42 percent into MBS for sale to investors, according to data compiled by Inside Mortgage Finance and the Urban Institute.

Close to 30 percent of Q1 2025 originations were FHA and VA loan securitizations backed by Ginnie Mae, while 23 percent were made by lenders who kept them in their portfolios.

Securitizations of private-label securities (PLS) lacking the backing of Fannie Mae, Freddie Mac and Ginnie Mae were up 24 percent from a year ago, to $20 billion, but accounted for just under 6 percent of first-lien mortgage originations in Q1 2025.

PLS securitizations boomed at the turn of the century when lenders used them to finance subprime mortgages, but vanished for close to a decade after the 2007-2009 housing crash and Great Recession.

Fannie and Freddie were placed in government conservatorship in 2008 as their losses mounted, and the Trump administration is studying ways to restructure them.

Bill Pulte

Bill Pulte, Trump’s pick to run Fannie and Freddie’s regulator, has said the president is interested in taking the companies public, and might “sell a small piece” in the process.

“We created U.S. Fin Tech to demonstrate the incredible ingenuity of American technology under President Trump’s leadership,” Pulte said in a statement.

Pulte on Wednesday directed the mortgage giants to consider allowing borrowers to count cryptocurrency as an asset without having to convert their holdings into dollars.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter