by Matt Carter | Jun 25, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Economists and investors expect Federal Reserve policymakers to continue to resist calls by the Trump administration to lower interest rates until they see more data on how tariffs and other policies are impacting inflation and employment.

Grilled by House and Senate lawmakers at separate hearings this week, Fed Chair Jerome Powell defended the central bank’s reluctance to resume cutting rates, saying the job market remains solid and that there’s no rush to make a decision.

After the Fed voted unanimously on June 18 to hold rates steady, Associated Press Reporter Chris Rugabar asked Powell if “cracks in the jobs market” and housing data “that have been pretty weak” could justify future rate cuts.

“I think if you look at the overall picture, what you’re seeing is 4.2 percent unemployment, and an economy that’s growing at a rate [that] appears to be 1-1/2, 2 percent — maybe a little better than that,” Powell said.

TAKE THE INMAN INTEL SURVEY FOR JUNE

While consumer sentiment has “come up off of very low levels,” it’s still depressed, Powell acknowledged.

“The housing market is a longer run problem, and also a short run problem,” Powell said. “Basically, we have a longer run shortage of housing, and we also have high [mortgage] rates right now. I think the best thing we can do for the housing market is to restore price stability in a sustainable way and create a strong labor market.”

Trump took to social media after the vote and urged the Federal Reserve Board to “override this Total and Complete Moron!” referring to Powell. “Maybe, just maybe, I’ll have to change my mind about firing him?”

Vice President J.D. Vance and Federal Housing Finance Agency Director Bill Pulte kept up the heat on Tuesday, with Vance saying he’d “love to hear an argument for why Powell cut rates 50 points right before an election but can’t do it now with inflation lower.”

Pulte claimed Powell’s interest rate policies “are not based on data but instead on Powell’s politicization of the Fed,” calling them “dangerous.”

On Wednesday — a few hours before ordering Fannie Mae and Freddie Mac to study allowing homebuyers to count crypto holdings as an asset — Pulte called on Powell to resign.

Trump told reporters Wednesday that he already has “three or four people” in mind who might replace Powell — although it’s unclear whether he will try to fire him.

Trump appointed Powell to lead the Fed during his first term, and his term is not set to end until May 2026.

One reason the Trump administration has grown impatient with Powell is that inflation has been nearing the Fed’s 2 percent goal. The personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred gauge of inflation, showed the price of goods and services rose 2.1 percent in April from a year ago, the Bureau of Economic Analysis reported last month.

But while the Fed can pull levers that give it direct control over short-term interest rates, mortgage rates are determined by investor demand for mortgage-backed securities (MBS), which fund most home loans.

As the Fed cut short-term interest rates by a full percentage point in its final three meetings of 2024, mortgage rates moved by about the same amount in the opposite direction, as incoming economic data suggested inflation was on the rise again.

The last time the Fed cut rates, mortgage rates went up

Powell has been saying for months that Fed policymakers need more time to assess the impacts of the Trump administration’s policies in areas including tariffs, immigration, taxes and regulation.

The “dot-plot” in the Fed’s latest Summary of Economic Projections shows members of the Federal Open Market Committee (FOMC) expect to cut the short-term federal funds rate just twice later this year, to between 3.75 percent and 4 percent.

“Lawmakers this week have been no more successful than journalists last week in getting Chair Powell to set out a more concrete timetable for the policy easing anticipated by a slender majority of [Fed policymakers] this year,” economists at Pantheon Macroeconomics said in their latest U.S. Economic Monitor.

The CME FedWatch Tool, which tracks futures markets to predict future Fed moves, shows investors think there’s only a 25 percent chance of a July rate cut. But bets placed by futures market investors as of June 25 put the odds of a September rate cut at 90 percent — up from 64 percent on June 18.

Fed policymakers will receive “substantial extra information” if they hold off until September to make a decision, Pantheon economists Samuel Tombs and Oliver Allen wrote Wednesday.

By September, “we think the FOMC will have seen a sequence of three weak labor market reports through August,” Tombs and Allen predicted, with the unemployment rate hitting 4.5 percent by August — 4 months sooner than currently projected by the Fed.

“That would represent a resounding call to ease policy, even before the full effect of the tariffs on inflation is visible in the data,” Pantheon forecasters wrote.

In the meantime, mortgage rates have been holding steady in the high sixes.

Mortgage rates stabilize

After hitting a 2025 low of 6.48 percent on April 4, rates on 30-year fixed-rate conforming mortgages have been rangebound between 6.75 and 7 percent in May and June, according to lender data tracked by Optimal Blue.

Weekly surveys of lenders by the Mortgage Bankers Association show that demand for purchase loans was up 12 percent last week from a year ago.

“Applications increased slightly overall driven by FHA refinances, but conventional applications saw declines over the week,” MBA Deputy Chief Economist Joel Kan said, in a statement. “The average loan size for purchase applications declined to $436,300, the lowest level since January 2025, driven by decreasing conventional purchase loan sizes.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 25, 2025 | Industry, News Feed

Head of Fannie Mae and Freddie Mac’s federal regulator says mortgage giants should consider what risk mitigation might be required when counting mortgage borrowers’ crypto holdings as an asset, “including adjustments for market volatility.”

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The head of Fannie Mae and Freddie Mac’s federal regulator has directed the mortgage giants to consider allowing borrowers to count cryptocurrency as an asset without having to convert their holdings into dollars.

In a post on the social media platform X Wednesday — Federal Housing Finance Agency Director Bill Pulte’s preferred channel for issuing official communications — Pulte said cryptocurrency is “an emerging asset class that may offer an opportunity to build wealth outside of the stock and bond markets.”

TAKE THE INMAN INTEL SURVEY FOR JUNE

Pulte is a crypto investor himself — in addition to millions of dollars in annual dividends from his stakes in Pulte Group and several heating and air conditioning companies, he listed $500,000 to $1 million in bitcoin among the assets he disclosed in a financial disclosure statement for executive branch personnel.

The order Pulte issued Wednesday directs both Fannie and Freddie “to prepare a proposal for consideration of cryptocurrency as an asset,” but only in cases where the assets are “evidenced and stored on a U.S.-regulated centralized exchange.”

Bill Pulte

Fannie and Freddie must also consider what risk mitigation might be required when counting mortgage borrowers’ crypto holdings as an asset, “including adjustments for market volatility and ensuring sufficient risk-based adjustments to the share of reserves comprised of cryptocurrency,” Pulte said.

The mortgage giants were instructed to submit any proposed policy changes regarding the treatment of crypto to their board of directors for approval — Pulte chairs both Fannie and Freddie’s boards — before submitting them to FHFA for review.

Commenting on Pulte’s proposal, Annapolis, Maryland based mortgage banker John Downs said asset reserves are not as much of a factor in obtaining loan approvals as they used to be.

“That prevents the crypto rug from truly impacting the borrowers ability to repay,” Downs wrote, alluding to the dramatic ups and downs in crypto valuations.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 25, 2025 | Industry, News Feed

The 2023 order, aimed at ensuring the collection of information about applicants’ race, ethnicity and gender, wasn’t scheduled to be lifted until 2028. Regulators say the bank has fulfilled its obligations.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

In its latest move to ease regulations, the Consumer Financial Protection Bureau (CFPB) has terminated a 2023 consent order with Bank of America aimed at addressing allegations that the lender reported false information about mortgage borrowers to federal regulators.

Bank of America was accused of failing to ask some mortgage applicants demographic questions about their race, ethnicity and gender as required by the Home Mortgage Disclosure Act (HMDA) — data that’s collected to uncover potential discriminatory lending patterns.

The CFPB claimed that in addition to failing to collect that demographic information from some borrowers, Bank of America falsely reported that the applicants had chosen not to respond.

Bank of America knew “that many loan officers receiving applications by phone were failing to collect the required data as early as 2013, but the bank turned a blind eye for years,” the CFPB alleged in announcing a $12 million settlement.

Under the terms of a Nov. 27, 2023, consent order, Bank of America also agreed to implement a compliance plan ensuring that it collected, recorded and reported required HMDA data used by the CFPB and other federal regulators to detect redlining.

While the consent order was to remain in effect for a minimum of five years — until late 2028, if no further reporting violations occurred — Office of Management and Budget Director Russell Vought on June 4 signed an order terminating it, saying Bank of America had fulfilled its obligations.

The CFPB did not publicize the action, which was first reported by Reuters this week. Bank of America declined Inman’s request for comment on the early termination of its consent order with the CFPB.

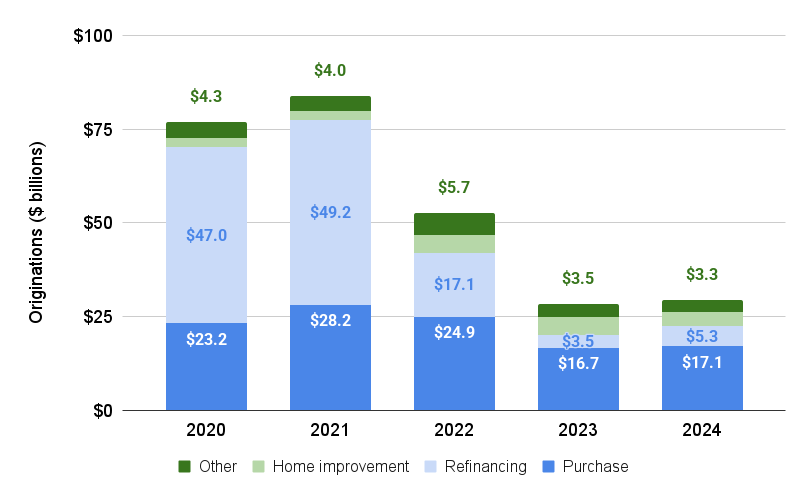

Bank of America mortgage originations, 2020-2024

Bank of America was the nation’s fifth-largest mortgage lender last year by dollar volume, with $29.5 billion in originations, according to an analysis of HMDA data by iEmergent.

Since the end of the pandemic-era refinancing boom fueled by low interest rates, most of the bank’s mortgage business has been with homebuyers, with $17.1 billion in purchase loans funded in 2024.

Regulatory rollback

Vought and his top deputy at OMB, Dan Bishop, are leading the Trump administration’s efforts to downsize the CFPB, with Vought serving a dual role as the bureau’s acting director.

The Trump administration, which is seeking to cut 90 percent of the CFPB’s workforce, has put about 20 active enforcement cases on hold and sought to vacate a number of settlements that the bureau reached under the Biden administration.

The acting director of the CFPB’s enforcement division, Cara Petersen, resigned on June 10, saying in a farewell email that “the bureau’s current leadership has no intention to enforce the law in any meaningful way.”

Two days later, U.S. District Judge Franklin Valderrama declined the CFPB’s motion to vacate a settlement it reached last year in a fair lending case involving Chicago mortgage broker Townstone Financial, saying that doing so “would erode public confidence in the finality of judgments.”

Russell Vought

Vought had claimed that an internal review of the case determined that the CFPB “abused its power” in pursuing the case against Townstone in order to “further the goal of mandating DEI in lending.”

Consumer groups that defended the Townstone settlement in court called the CFPB’s request to vacate it “unprecedented,” and argued that granting it would establish a “dangerous and destabilizing precedent.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 24, 2025 | Industry, News Feed

New offering lets existing homeowners tap their equity to buy before they sell and make non-contingent offers to better compete with cash buyers in competitive markets.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

After leading the nation in refinancing last year, Rocket Mortgage hopes to do more business with homebuyers with a new bridge loan product that lets existing homeowners buy before they sell and make non-contingent offers to compete with cash buyers.

Rocket Mortgage’s bridge loan, announced Monday, gives homebuyers up to six months to sell their home and make interest-only payments during that period.

Bill Banfield

The average homeowner has $181,000 in untapped equity, and providing immediate access to that money for a down payment or closing costs “removes one of the biggest barriers to moving,” Rocket Chief Business Officer Bill Banfield said in a statement.

In markets that remain highly competitive for buyers, Rocket said, the ability to make non-contingent offers can help win over sellers who are considering multiple offers.

Even in less competitive markets, bridge loans help buyers “avoid the hassle of double moves and temporary housing, while taking the time to secure the best offer on their existing property,” the company said.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

Homebuyers can also turn to competitors including HomeLight and Calque, who partner with multiple lenders to offer “Buy Before you Sell” products, and power buyers like Knock and Zavvie.

Detroit-based Rocket Mortgage is licensed in all 50 states and Washington, D.C., sponsoring 3,602 mortgage loan originators working out of 57 branch locations nationwide, according to records maintained by the Nationwide Mortgage Licensing System (NMLS).

Rocket Mortgage was the nation’s second biggest mortgage lender in 2024, with $97.6 billion in funded loans accounting for 5.4 percent of originations by volume, according to Home Mortgage Disclosure Act (HMDA) data tracked by iEmergent.

Pontiac, Michigan-based United Wholesale Mortgage, which overtook Rocket as the leading U.S. mortgage lender in 2022, originated $139.7 billion in mortgages last year, accounting for 7.7 percent market share, according to iEmergent HMDA data.

Most of Rocket’s 2024 origination volume came from refinancing existing mortgages (56 percent) or providing home equity loans (6 percent). UWM did most of its business (63 percent) with homebuyers, iEmergent HMDA data shows.

With $44.5 billion in refinancings last year, Rocket Mortgage edged out UWM’s $43.4 billion in 2024 refi volume.

Rocket expects its pending acquisition of the nation’s biggest loan servicer, Mr. Cooper, will help grow its refinancing business, while a deal to acquire national real estate brokerage Redfin will put it in contact with more homebuyers.

Speaking at an investment conference in May, Rocket Companies CEO Varun Krishna said the lender has set a goal of handling 8 percent of purchase mortgages and 20 percent of refinancings.

After acquiring Mr. Cooper, Rocket will be collecting payments on about one in six U.S. mortgages with $2.1 trillion in outstanding balances. When those homeowners are ready to refinance, Rocket will have a leg up on “recapturing” their business, Krishna said.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 24, 2025 | Industry, News Feed

After pilot tests in 11 markets, iBuyer expands its Key Connections program that puts partner real estate agents in touch with “high intent” sellers who want to explore their options.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

IBuyer Opendoor is hoping to reach more sellers by “flipping the script” and giving them the option of listing their home with an Opendoor preferred agent with an all-cash backup plan.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

Opendoor’s new Key Connections program connects partner real estate agents with high-intent sellers in their market who want to explore their options.

After pilot tests of Key Connections in 11 markets, Opendoor announced Tuesday that it’s expanding the program and will invite more vetted agents to reach sellers in additional markets.

“Today, a meaningful percentage of our acquisitions come to us through an agent who is bringing their customer to Opendoor and requesting a cash offer,” Opendoor CEO Carrie Wheeler said on the company’s May 6 earnings call.

Carrie Wheeler

“We are taking our existing vibrant partnership with agents and flipping the script, so to speak, by sending Opendoor customer referrals to embedded agent partners,” Wheeler said of Key Connections. “Those agents are able to talk through the options that a customer has to sell, from an Opendoor cash offer to a full listing.”

In pilot tests of Key Connections, Wheeler said customers have been receptive to having a local expert explain their options.

“Agents benefit from high-intent seller referrals from our marketing engine and are able to bring all options to the table in assessing the smartest move for the customer,” she said.

The program can help Opendoor improve its conversion rates, whether sellers accept a cash offer or opt to list with a partner agent, which generates “asset-light” revenue without the need for Opendoor to buy and sell the property itself.

The Key Connections program has also allowed Opendoor to deliver final, underwritten offers faster, because partner agents do an in-home assessment in their first meeting with prospective sellers, Wheeler said.

Since launching in Phoenix in 2014, Opendoor has expanded into 50 markets as of March 31 and sold more than 13,500 homes last year.

But the company has been operating in the red, racking up a $392 million 2024 net loss and cumulative losses of $3.81 billion through March 31.

The Nasdaq Stock Market notified Opendoor on May 28 that the company could be delisted from the exchange after its price per share fell below the minimum $1 per share requirement for 30 consecutive business days. Shares in Opendoor, which over the past year have traded for as little as 51 cents and as much as $3.09, closed at 53 cents Monday.

To get its share price back above $1, Opendoor will ask shareholders on July 28 to approve a reverse stock split at a ratio between 1-for-10 and 1-for-50, at the discretion of the company’s board.

If Opendoor were to execute a 1-for-10 reverse stock split, the number of issued and outstanding shares would decrease from 729 million to 72.9 million, and the company’s price per share would rise above $5, based on Monday’s closing price.

But because a reverse split would not decrease the number of shares of common stock the company is authorized to issue, the number of shares authorized but unissued would increase from 1.78 billion to 2.88 billion, shareholders were informed on June 16.

“The board believes that a higher stock price, which may be achieved through a reverse stock split, could help facilitate the company’s ability to raise new equity capital,” shareholders were told.

In addition to allowing Opendoor to land more funding — privately, or by issuing more shares — a reverse stock split could stimulate investor interest in the company and help attract, retain and motivate employees, the company said.

Email Matt Carter