Transcendent enthusiasm, like falling in love, grabs hold when buyers find a home they adore, Brad Inman writes of the couple who bought his Spanish-style West Hollywood home earlier this month.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

I knew I would live there when I first walked into the 102-year-old condominium in San Francisco’s Nob Hill neighborhood last month. The feeling was indistinguishable from when I bought my first home in Oakland 45 years ago.

Nostalgia and imagination inspire powerful feelings when buying a home. You are launched into an orbit of transcendent enthusiasm, like falling in love.

As my wife Yaz and I were closing on the San Francisco unit, the young buyers of our 98-year-old Spanish-style West Hollywood home felt the same magical enchantment. The Brooklyn transplants wrote a poignant letter describing their enthusiasm about purchasing our house — they fell in love.

This is one reason why selling or leaving a home is so difficult. It’s not just the memories; your soul becomes welded to the place, making it difficult to let go. Before moving in, your imagination lays the first psychic rebar, connecting you to a future of joy and meaning with all of life’s experiences ahead of you.

Brad Inman’s chair in Palm Beach, Florida

Millions of other people embark on this same journey, which, as a journalist, has always drawn me to real estate.

Homeownership has never been an elite privilege — at least not in the United States. It was always meant for everyone. As with our current housing affordability crisis, market forces often step in to correct the imbalance when it becomes too much. A more balanced market is beginning to take shape now.

To achieve homeownership, aspiring buyers must make sacrifices, stretch their household budgets, accept smaller living spaces, and choose geographical trade-offs.

Young people — Gen Z, the Zoomers — are setting out on a new wave of geographical reshuffling, this time to affordable Midwestern states. No personal or economic obstacle can squash their determined real estate ambitions. Like love, desires take over.

Right now, I sit in a chair, in a room, in my home, where I write, read and reflect.

Homes aren’t just a dream for me — they are who I am and what I love.

5 Things to Know About Living in a MUD (Municipal Utility District)

If you’re house hunting in Texas—especially around Houston, Austin, San Antonio, and the fast-growing suburbs of Dallas–Fort Worth—you’ll likely see homes located in a “MUD.” That stands for municipal utility district, and it can affect everything from your water provider to your annual tax bill. Understanding how a MUD Texas works helps you compare neighborhoods accurately, avoid surprises at closing, and feel confident about your long-term costs.

Below are five practical things to know—explained in plain language—so you can evaluate a MUD community like a pro.

1) A MUD is a local government that provides utilities (and pays for infrastructure)

What a municipal utility district is

A municipal utility district is a type of special-purpose local government authorized by the State of Texas. MUDs are commonly created in areas outside city limits or in newly developing areas where city utility service isn’t available yet. The district’s job is to build and operate essential infrastructure, most often:

Water (production wells, treatment, distribution lines)

Drainage and stormwater (detention ponds, drainage channels, storm sewers)

Sometimes roads and parks (varies by district authorization)

Why MUDs are so common in Texas

Texas grows quickly, and new neighborhoods often pop up before a city can extend utilities to serve them—or in areas that prefer not to annex into a city at all. A MUD allows development to move forward by funding infrastructure up front, then paying those costs back over time through taxes and utility fees collected from property owners within the district.

In other words, a MUD can help turn “raw land” into a livable community with reliable water, sewer, and drainage—services that are non-negotiable for most buyers.

2) MUD taxes are part of your total Texas property taxes—so your tax bill may be higher

How MUD taxes fit into Texas property taxes

Texas property taxes are typically made up of several taxing entities. Depending on the address, your bill may include:

County taxes

School district taxes (often the largest piece)

City taxes (if inside city limits)

Community college or hospital district taxes (in some areas)

MUD taxes (if the home is in a municipal utility district)

Homes in a MUD frequently have a MUD tax rate added on top of other local rates. This is one of the biggest “budget surprises” for first-time buyers who focus only on the sales price and interest rate.

Why MUD tax rates can be higher in newer communities

When a neighborhood is new, the MUD may still be paying off major infrastructure costs. As more homes are built and the tax base grows, the district can sometimes spread costs across more properties—which may help stabilize or reduce rates over time. That said, tax rates can move up or down based on budgets, debt service, and operational needs, so it’s best to treat any future change as a possibility, not a promise.

How to estimate your real monthly payment

When you’re comparing two homes—one in a MUD and one not—ask your lender to run payment scenarios using the full estimated tax rate. A small difference in tax rate can noticeably change your monthly escrow payment.

Green flag: Your agent and lender provide a complete tax breakdown early, including MUD taxes.

Red flag: Tax estimates that ignore the MUD or use an outdated rate.

3) You’ll pay both MUD taxes and utility bills—because they cover different costs

Taxes vs. utility rates: what each one pays for

This is a common point of confusion. In many MUD Texas communities, homeowners pay:

MUD taxes (collected like property taxes, often used to repay infrastructure debt and support district operations)

Monthly utility bills (water/sewer usage charges, base fees, and sometimes trash through separate providers)

Think of it like this: your utility bill is generally tied to your consumption and service fees, while MUD taxes are tied to the value of your property and the district’s budget and debt obligations.

Practical questions to ask about services

Before you buy, get clear answers on who provides what. In some neighborhoods, the MUD handles water and sewer, while trash pickup might be private. In others, services are bundled differently.

Who is the water provider and sewer provider?

Are there separate fees for drainage or stormwater?

Is trash and recycling included, through the HOA, or billed separately?

Are there irrigation restrictions or water conservation rules?

In many Texas markets, summer water usage spikes due to lawn irrigation—so it’s smart to review typical seasonal billing patterns, especially if the home has a large yard or new landscaping that needs frequent watering.

4) MUDs issue bonds to build the neighborhood—so debt and “build-out” matter

What it means when a MUD has debt

MUDs often finance infrastructure by issuing bonds. Bond proceeds can pay for major systems like water lines, sewer lift stations, and drainage improvements. Then the district repays those bonds over time using tax revenue from property owners in the district.

Debt isn’t automatically bad—without it, many Texas master-planned communities wouldn’t exist in their current form. The key is understanding how the district’s debt and growth stage may affect tax rates and future planning.

How to think about build-out stage

A newer MUD in early build-out may have:

Higher infrastructure spending

A smaller number of homeowners sharing costs

More construction activity nearby

A more mature MUD may have:

A larger tax base

More predictable budgets

Fewer active construction impacts

Neither is inherently “better,” but they feel different day-to-day. If you work from home or prefer quiet streets, ongoing development can be a meaningful lifestyle factor to weigh.

Due diligence tips buyers often miss

Confirm the exact tax rate for the current year and ask whether it includes both debt service and operations.

Ask for recent district information that explains finances, service areas, and long-term plans (your agent can help request what’s appropriate).

Compare similar homes across neighborhoods using total monthly payment, not just list price.

5) Governance, disclosures, and closing details can affect your experience

How MUDs are governed (and why it matters)

A municipal utility district is run by an elected board. The board makes decisions about budgets, tax rates, infrastructure projects, and operations. While most day-to-day utility operations are handled by professional managers and contractors, governance still matters because it shapes long-term planning and financial priorities.

For homeowners, the practical takeaway is that a MUD is a real local governmental body—separate from a city and separate from an HOA—with its own responsibilities and public processes.

Disclosures you may see when buying a home in a MUD

In Texas, buyers are often provided a notice that a property is located in a utility district, along with information about taxes and services. Closings may also include details tied to the district’s tax rate or utility setup.

Here’s a simple step-by-step approach for buyers to stay organized:

Step-by-step: how to evaluate a MUD home before you close

Step 1: Identify the district. Ask your agent for the exact MUD name and confirm the home is within its boundaries.

Step 2: Verify the total tax rate. Compare last year’s and current year’s rates if available, and make sure your lender uses the right number in payment estimates.

Step 3: Confirm service providers. Verify who bills water and sewer, and whether there are additional district fees.

Step 4: Review the seller’s disclosures and any district notices. Pay attention to anything referencing taxes, utility districts, or special assessments.

Step 5: Budget for real-world usage. Ask the seller (or neighbors, if possible) about typical summer and winter utility bills, especially for irrigation and pool ownership.

Common mistakes (and how to avoid them)

Mistake: Assuming “no city taxes” means “lower taxes.” Better approach: Compare the total tax rate, including the MUD and school district.

Mistake: Underestimating escrow changes after the first year. Better approach: Plan for potential payment adjustments if the initial escrow estimate was conservative or if taxes/insurance change.

Mistake: Ignoring drainage and flood resilience.

On that last point: because MUDs often handle drainage infrastructure, it’s still wise to do your own due diligence—review flood history, ask about detention systems, and consider insurance needs. Drainage is a major quality-of-life issue in many Texas regions, particularly in parts of the Gulf Coast and areas prone to heavy seasonal storms.

Pros and cons of living in a MUD community

Pros

Newer infrastructure and planned utility systems

Development can happen in desirable areas outside city limits

Potentially strong neighborhood amenities depending on the community

Cons

MUD taxes can increase your overall Texas property taxes

You may pay both MUD taxes and monthly utility bills

Construction and growth can affect traffic, noise, and local services during build-out

Bottom line: a MUD isn’t “good” or “bad—”it’s a cost-and-services tradeoff

Buying in a MUD Texas community can be a great fit, especially if you want a newer home, planned infrastructure, and access to fast-growing suburban areas. The key is to shop with your eyes open: understand how the municipal utility district impacts services, what it adds to your Texas property taxes, and how it affects your true monthly payment.

If you do that homework early—before you fall in love with a house—you’ll be in a strong position to choose the neighborhood that fits both your lifestyle and your budget.

Whether it’s refining your business model, mastering new technologies, or discovering strategies to capitalize on the next market surge, Inman Connect New York will prepare you to take bold steps forward. The Next Chapter is about to begin. Be part of it. Join us and thousands of real estate leaders Jan. 22-24, 2025.

Everything is fine, or generating fines, as agents and brokers are discovering that their multiple listing services (MLSs) meant business about fines for violations around the commission language and rules created from the settlement lawsuits.

While fines are nothing new in the real estate industry, these fines are still seemingly catching agents off guard, caused by workarounds, misunderstandings, and what seems to be just poor planning and oversight.

But it’s not just MLSs and consumer complaints you need to be ready for; you also need to be ready for the fact that your competition is about to be fierce. In fact, it may be a fellow agent turning you in for violations at the state and local levels as well.

Why? Let’s face it, there is not enough business to go around, and top-producing agents who are determined to stay in business are tired and burned out from other agents who make their jobs more labor intensive — and make transactions a nightmare — because of negligence.

So what is a broker, admin, or agent to do to make sure that unnecessary fines and violations don’t stack up like an unlimited pancake platter at IHOP? What can you do to possibly help prevent landing in a sticky situation? There needs to be a collective plan to make sure that everyone is on the same page, creating a consistent experience for all consumers involved.

Here are three pitfalls that you may have missed in your preparations and some cleanup recommendations that may help avert disaster.

Stop using your presentations and documentation from 2023 or older

Pitfall No. 1: Trying to make dated materials work by just throwing new materials into the mix

It’s time for a fresh approach, meaning you need all new materials, systems and presentations. I think where many folks will struggle is they try to adapt older packages and systems with new materials. In doing that, you may miss sections of language that may be out of context or contradictory to the new systems that will be falling into place.

Clean it up:Do a careful audit, and make sure to throw out all older materials. Craft fresh packages with the latest state-approved revised documents. Carefully document when and how you did this process in case it’s ever brought up in court or in front of a grievance committee.

This also means making sure that you audit all listing descriptions and documentation of active listings that your team has held previously.

Make sure that if you are a broker and you have gone through this audit system and provided guidance and materials to your team that you have written documentation that they understand the new process and that they have culled and removed materials.

Stop creating a digital paper trail online of rants against consumers

Pitfall No. 2: Social media and marketing habits that give the wrong impression about commissions

Many agents are crafting an easy-to-find digital footprint of evidence that could be collected against them to support fines and violations because of their social media rants and activities. For example, depending on the context, ranting in “private” Facebook groups could be a huge problem for you.

Creating and sharing videos about how you are going to treat clients if they pay you less (pretending to rush them or acting like you will do the least amount of work) is not only in poor taste but also implies that you are looking to obtain a certain commission rate and are not going to be open to negotiate.

What’s not a good look if you find yourself in a sticky violation situation or under investigation? Videos that:

Make fun of misinformed or discount-seeking consumers

Are overly aggressive with what services you will not perform if you work at a discount

Are just silly and satirical

In other words, if you find yourself caught with a fine and have to explain yourself, your business, and your dedication to customer service, those videos are not going to do you or your brand any favors.

With the Consumer Federation of America (CFA) heavily invested in protecting consumers, now is the time to make content for supporting consumers, not for entertaining other agents or making fun of the industry. Professional agents are going to work to raise the bar, not polish their stand-up comedy routines.

Liking and commenting on content from influencers and coaches who create hype videos promoting aggressive tactics to manipulate consumers into any type of commission structure leaves a digital trail that can be easily traced with a screenshot. In other words, be careful what you like and share because you never know where it will resurface.

Author’s note: If you don’t think anyone is paying attention, I will caution you this: When I was previously involved in grievances and fines discussions at the association level, it wasn’t the consumers you needed to be worried about. It was the agents who knew how to put a case together against you because you had either intentionally, or sometimes not intentionally, done something to cause them grief in a transaction. They came prepared with enough documentation to win.

Clean it up: Get a handle on your personal and team social media hygiene habits. You will be standing next to them at board grievance investigations and likely have to accompany them to court. Also, beware of anyone who is promoting themselves as an expert to coach you in what to do. This is the Wild West, and there are no experts yet.

Supercharge prospecting with disclosures and respect for the consumer

Pitfall No. 3: Stop over-complicating information for consumers

One thing that is critical moving forward with consumers is to have educational materials available to them with very low friction or incumbrances on their part. They need to obtain information about new practices from reliable sources that are easy to understand and delivered in multiple formats to accommodate accessibility and different learning styles. Think like a fast food drive-through menu; they need to be able to glance at some options and point to what they want.

These could include short video explanations, FAQ pages, informative and professional educational posts in your marketing, and a dedicated area on your website to find disclosures and materials that are easy to understand and that are provided multiple times during your interactions with the consumer.

I sell homes in a retirement community and have been working through some policy changes and purchase language updates. Our team devised a plan of carefully curated updates for our clients in a variety of formats, including a written letter, digital updates and in-person meetings.

What our team has found is that, even though we launched our plan many weeks ahead to give notice of the changes, it took a very personal, hands-on approach to help the clients understand what the changes were.

Many clients simply will not take the time to read the information, and many others are so busy they do not have time to retain the information. Clients will also question your expertise, and bring your materials to consultations to interview you line by line of what they are reading to see how prepared you are.

Perspective is key, and your clients will be interested in their personal outcome, not how you are paid. It’s important to keep the conversation focused on their goals and their desired outcome.

Clean it up: Be clear and concise. Be a good listener. Be willing to repeat and offer presentations often — even if you think your clients understand.

Much of the training and education around prospecting is about how to catch the attention and “convince” a consumer to work with you. There is a great deal of bad and high-pressure advice out there from coaches who are pushing tactics from 20 years ago.

Much like throwing out old presentations, you need to throw out outdated prospecting tactics. You will have to untrain yourself from tactics that may be harmful to working with consumers in this new environment.

Operating with professionalism isn’t necessarily about the suit you are wearing. It’s about your behaviors inside transactions with your peers. You will need to study and be prepared to work in this new environment with your team and other agents, and if you show up unprepared, you could be paying a steep price, where what you don’t know could potentially turn your business into a no-go with some serious debt.

Watch your back, stay polite, and be very careful with what you send in texts and emails.

One last piece of advice: Volunteer at your local association for grievances. This is going to give you the best education possible about pain points, pitfalls and areas where your business could be at risk, and it will potentially be the best new think tank for creating the “experts” we need to help navigate this moving target from now into 2025.

Stay in your lane, stay sharp, keep it clean on social media, and if you mind your own business, you should be just fine — when it comes to avoiding unnecessary fines.

Rachael Hite is a business development specialist, fair housing advocate, copy editor, and former agent. Rachael is currently perfecting her long game selling forever homes in a retirement community in Northern Virginia. You can connect with her about life, marketing and business on Instagram.

HAPPENING NOW! At Inman Connect Las Vegas, July 30-Aug. 1, 2024, the noise and misinformation will be banished, all your big questions will be answered, and new business opportunities will be revealed. JOIN US VIRTUALLY.

Bond market investors who fund most home loans have cleared mortgage rates to continue their descent from 2024 highs after Fed policymakers dropped hints Wednesday that a September rate cut could be in the cards.

Wrapping up a two-day meeting Wednesday, members of the Federal Open Market Committee (FOMC) said they’d leave their target for the short-term federal funds rate at between 5.25 percent and 5.50 percent, as expected.

But the committee made some subtle changes to the language of its post-meeting statement explaining its rationale, Pantheon Macroeconomics Chief Economist Ian Shepherdson noted in an email to clients.

Ian Shepherdson

“Progress towards the committee’s 2 percent inflation objective has been upgraded to ‘some,’ from ‘modest,’ and inflation now is described as only ‘somewhat’ elevated,” Shepherdson wrote of the changes from June’s statement. “Meanwhile, the risks to achieving the employment and inflation goals ‘continue to move into better balance,’ and the committee now is ‘attentive to the risks to both sides of its dual mandate,’ rather than just to the inflation risks.”

In other words, Fed policymakers are acknowledging that while they’re determined not to cut rates until they’re certain that inflation is tamed, they’re also afraid of waiting too long to ease and throwing the economy into a tailspin.

Data released last week showed the Federal Reserve’s preferred measure of inflation, the personal consumption expenditures (PCE) price index, dropped to 2.51 percent in June from a year ago — just half a percentage above the Fed’s 2 percent target.

Mike Fratantoni

“The FOMC did not change its target for the federal funds rate but did shift its statement to acknowledge that inflation is slowing, unemployment is rising, and that there are now more balanced risks to the economy,” Mortgage Bankers Association Chief Economist Mike Fratantoni said in a statement. “While the Fed still hopes for a slower rate of inflation, there is a greater risk now that keeping monetary policy overly tight for too long could lead to unnecessarily higher unemployment.”

At a press conference following the meeting, Fed Chair Jerome Powell dropped more hints that the central bank will be ready to cut rates if it sees signs the economy is weakening.

“We know that reducing policy restraint too soon or too much could result in a reversal of the progress that we’ve seen” on inflation, Powell said. “At the same time, reducing policy restraint too late or too little could weaken economic activity and employment.”

Powell: ‘We are prepared to respond’

“If the economy remains solid, inflation persists,” Powell warned. “We can maintain the current target range for the federal funds rate as long as appropriate. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we are prepared to respond.”

But the CME FedWatch tool, which tracks futures markets to gauge the odds of future Fed moves, shows investors are not only certain that the central bank will cut rates by at least 25 basis points in September but that there’s an 18 percent chance it will approve a more drastic cut of 50 basis points. A basis point is one-hundredth of a percentage point.

Bets placed by futures market investors as of Wednesday also suggest they see a 75 percent chance the Fed will cut rates by at least 75 basis points by the end of the year, up from 20 percent a month ago.

Shepherdson said forecasters at Pantheon Macroeconomics are only expecting the Fed to cut rates by 25 basis points in September, but that it will follow up with 50 basis-point reductions in both November and December.

That would bring the short-term federal funds rate down 1.25 percentage points, to a target range of 4 to 4.25 percent.

“Our view remains that the Fed is recognizing too slowly that the labor market is cooling and that high inflation is yesterday’s problem,” Shepherdson wrote. “With rates well above neutral, the easing cycle likely will be much faster than markets currently anticipate if, as we expect, the labor market data continue to weaken and inflation prints remain benign.”

Fratantoni said MBA forecasters are holding to their call for two rate cuts totaling 50 basis points this year.

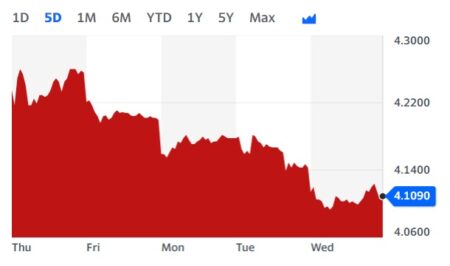

Barometer for mortgage rates falls

Yields on 10-year Treasury notes flirted with 4 percent Wednesday. Source: Yahoo Finance.

Yields on 10-year Treasury notes, a barometer for mortgage rates, remained on track for another weekly and monthly decline after Powell’s press conference. Since hitting a 2024 high of 4.74 percent on April 25, rising demand for bonds by investors who expect the economy to slow has brought yields on 10-year Treasurys down more than half a percentage point.

After closing at 4.14 percent Tuesday, 10-year Treasury yields touched a low of 4.09 percent Wednesday morning before rebounding to close at 4.11 percent Wednesday. That’s a 38 basis-point drop from July 1 and a 63 basis-point drop from a 2024 high of 4.74 percent on April 25.

Conforming mortgage rates in free fall

Rates for 30-year fixed-rate conforming mortgages averaged 6.71 percent Tuesday, down 30 basis points from July 1, according to rate lock data tracked by Optimal Blue.

Since hitting a 2024 high of 7.27 percent on April 25, rates on conforming mortgages have come down by 56 basis points — more than half a percentage point.

Borrowers seeking jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $766,550 conforming loan limit haven’t seen as much relief, as the “spread” between jumbo and conforming loans has widened.

Borrowers were accepting locks on jumbo loans Tuesday at an average rate of 7.22 percent — a more modest drop of 34 basis points from a 2024 high of 7.56 percent registered on April 15.

Before the pandemic, rates on jumbo mortgages tended to be lower than conforming loans by an average of 9 basis points from 2017-2019, according to Optimal Blue data. But tightening by regional banks, which are major providers of jumbo loans, has flipped the spread, with rates on jumbo mortgages averaging 16 basis points above conforming loans in 2023 and 30 basis points so far this year.

With Fed rate cuts on the horizon, bond market investors who fund most conforming mortgage loans are happy to accept lower yields on mortgage-backed securities (MBS) backed by conforming loans. But jumbo lenders typically hold loans on their books, and their funding costs may come down more slowly.

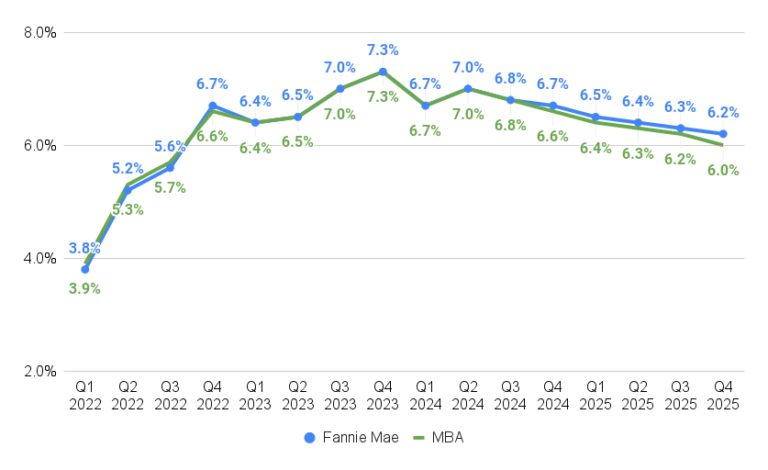

Economists at Fannie Mae and the Mortgage Bankers Association (MBA) predict the rate on conforming loans will continue to drop into the low sixes by the end of next year.

“Mortgage rates are now well below 7 percent, and there has been some modest pickup in refinancing activity in recent weeks,” the MBA’s Fratantoni said. “We expect that mortgage rates will continue to drift lower through the remainder of the year, particularly if the Fed does launch a series of rate cuts in September.”

So far, homebuyers have been slow to respond to the decline in rates, as the runup in home prices during the pandemic and elevated rates have priced many would-be buyers out of the market.

A weekly survey of lenders by the MBA showed applications for purchase loans were down by a seasonally adjusted 2 percent last week compared to the week before and were 14 percent lower than a year ago. Applications to refinance were down 7 percent week over week, but up 32 percent from a year ago.

Eric Orenstein

“Even with a September rate cut possible, mortgage companies will continue to face meaningful earnings headwinds for the foreseeable future,” Fitch Ratings Senior Director Eric Orenstein said, in a statement. “With most outstanding mortgages still carrying rates below 5 percent and record home prices driving down affordability, it may be a long road back to higher origination volumes.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Delian Asparouhov, a partner at Founders Fund, talked on Wednesday about his plans to manufacture drugs in space and urged real estate agents to lean into tech.

HAPPENING NOW! At Inman Connect Las Vegas, July 30-Aug. 1, 2024, the noise and misinformation will be banished, all your big questions will be answered, and new business opportunities will be revealed. JOIN US VIRTUALLY.

When Delian Asparouhov was just a boy, his parents moved from Bulgaria to the U.S. in the wake of the Soviet Union’s collapse. The experience, Asparouhov said Wednesday on stage at Inman Connect Las Vegas, made him a believer in capitalism and the importance of commercial enterprise.

Growing up in the U.S., Asparouhov — who today is a partner at venture capital firm Founders Fund — also became a fan of science fiction and aerospace — so much so that, when he reached adulthood, he began looking for ways to work in the industry. Asparouhov specifically wanted to find ways to make money in space, but, he recalled to the packed Connect ballroom, the technology just didn’t exist to make commerce viable miles above the earth’s surface.

Then something changed. Asparouhov said that in 2018 and 2019, Elon Musk’s Space X began deploying reusable rockets. He compared the development to the advent of the railroad, which once enabled industrialists like the Rockefellers to ship oil with new efficiency.

“Today, in 2024, these types of rockets launch and land every 36 hours,” Asparouhov said of Space X’s technology. “Somebody clearly built the railroads to space; somebody just had to figure out what the oil was going to be.”

Delian Asparouhov on stage at Inman Connect Wednesday. Credit: AJ Canaria Creative Services

Over the ensuing years, Asparouhov focused on ways to harness that new technology and identify the “oil” to be won by working in space. He eventually hit upon pharmaceutical manufacturing. The idea, he explained, is that without gravity, drug companies can do much more precise chemistry, to the point that at least one popular drug could be converted from an IV drip to an at-home syringe system.

The idea could be revolutionary, but it also sounds ludicrous. Manufacturing drugs in space?

But, it turns out, Asparouhov has apparently already done it. While on stage, he showed the audience pictures of an object that looked like a Starlink satellite. However, he added, it was in fact a capsule that created drugs while in orbit and returned this last February.

“The worst environment they saw,” he joked about the drugs’ incredible journey, “was the UPS truck in Houston.”

Though Asparouhov’s efforts to create an orbital drug manufacturing business are unrelated to real estate, he has invested in real estate startups and said that similar principles apply across industries. The point of his presentation, in other words, was that new technologies have the ability to revolutionize industries.

In space, that new technology was reusable rockets. A century ago, it was the railroads. And today, Asparouhov argued, it could be artificial intelligence.

“It’s as fundamental as the steam engine,” Asparouhov argued.

He consequently urged real estate professionals to lean into and understand new technology, and to be prepared for the changes it might bring.

“There will be fewer agents in 10 years than there are today,” he said, “but almost certainly those agents will be able to handle more client volume.”