by Michael Zaransky | Jun 12, 2025 | News Feed

Leave The U.S.: A Village In Italy Is Selling Homes To Americans—For $1

Why This Matters to Texans Watching Housing Costs Rise

In Texas, buyers have spent the past few years navigating higher mortgage rates, elevated insurance premiums, and—especially in fast-growing metros—prices that still feel “sticky” even when the market cools. So it’s no surprise that headlines about $1 homes in Italy catch attention, particularly among would-be retirees, remote workers, and families ready to escape American lifestyle stressors and try something new.

But here’s the key: a Buy a home in Italy for $1 program is not a “free house.” It’s an incentive used by Italian villages selling homes to revive shrinking communities. If you’re considering an international move—whether to Move to Italy from the US permanently or spend part of the year abroad—this guide breaks down how it really works, what it costs, and the smartest way to approach it.

The $1 Home Trend: What’s Really Being Sold?

Across rural parts of Italy, municipalities have offered symbolic-price properties—often old, vacant homes that need significant renovation. These programs are designed to attract new residents, boost local trades, and preserve historic housing stock. That’s why “Cheap homes in Italy” and “Affordable real estate in rural Italy” often go hand-in-hand with strict rules.

While a village on Sardinia has been highlighted in recent coverage, similar programs have appeared across the country over the years. The common thread is that buyers take on a renovation obligation within a set timeline. For Americans, it’s an appealing story—Escape the US by buying a home in Italy and live the Italian dream—but the details determine whether it’s a great opportunity or an expensive detour.

What You Typically Get for $1

- A distressed property in a small town, often vacant for years

- Structural or systems issues (roof, plumbing, electrical, moisture) that require professional work

- Local oversight from the municipality, including deadlines and permit requirements

- A chance at Italian countryside living—but usually not a turnkey home

Why Americans Are Moving to Italy (And What Texans Should Consider)

The reasons behind Why Americans are moving to Italy are practical as much as romantic: a slower pace, walkable towns, food culture, historic architecture, and the possibility of relocating to Italy on a budget compared with high-cost U.S. areas. Many US expats in Italy also say they value community-centered living and the idea of start over in Italy with fewer day-to-day pressures.

From a Texas lens, it’s worth comparing what you’re leaving and what you’re gaining. Texas offers space, newer construction, and (in many counties) relatively lower taxes than coastal states—but costs like insurance and HOA dues can add up. Italy can feel more affordable in some daily expenses, but renovations, bureaucracy, and energy-efficiency requirements can surprise first-time international buyers.

Green Flags vs. Red Flags for Would-Be Buyers

- Green flag: You have a realistic renovation budget and a local professional team lined up.

- Green flag: You can spend time in Italy during planning, permitting, and construction.

- Red flag: You’re counting on a $1 home to be “move-in ready.”

- Red flag: You assume U.S.-style timelines—Italian permitting and contractor schedules can move slower.

How to Buy a $1 Home in Italy as an American (Step by Step)

If you’re serious about How to buy a $1 home in Italy as an American, treat it like any major real estate purchase—just with additional international layers. Here’s a clear process that mirrors the discipline Texas buyers already use for big transactions.

Step 1: Confirm the Program Rules (They Vary by Town)

Each municipality sets its own terms. Many require buyers to submit a renovation plan, start work by a deadline, and complete the project within a fixed window. Some require a refundable deposit or bond to ensure follow-through. Before you commit to Italy real estate for Americans, verify the fine print in writing.

Step 2: Budget Beyond the $1 Price Tag

Think of “$1” as the entry ticket—not the total cost. Your real budget should account for design, permitting, labor, materials, utilities setup, and professional fees. For Texans used to budgeting for inspections, appraisal gaps, and closing costs, apply the same mindset here—only broader.

Step 3: Visit and Inspect Like a Pro

Even if the town doesn’t require a full inspection, you should. Bring a qualified local technician or engineer to evaluate structure, roof, moisture issues, and seismic considerations in older masonry homes. This is your equivalent of a Texas option period—your chance to avoid buying a problem you can’t solve affordably.

Step 4: Line Up Your Team

Successful buyers typically have:

- A local real estate professional (or municipal contact) to coordinate access and paperwork

- A notary (common in Italian transactions)

- A geometra/architect or engineer for plans and permits

- Reliable contractors familiar with historic renovations

Step 5: Understand Residency, Visas, and Remote Work Realities

Buying property does not automatically grant residency. If your plan is move to Italy from the US full-time, talk to an immigration professional about legal pathways. If you plan on remote work from Italy, confirm your employer policies, tax implications, and time zone expectations. Many buyers start with a long-term stay strategy before making a permanent move.

What “Cheap Homes in Italy” Usually Cost After Renovation

Most $1 homes require meaningful investment. While totals vary widely by region, home condition, and finish level, the renovation budget often becomes the true purchase price. In Texas terms, think “major rehab” rather than “cosmetic fixer.” Your cost can rise quickly if you need:

- Roof replacement and structural stabilization

- Full electrical and plumbing updates

- Moisture remediation and insulation upgrades

- New windows/doors that meet local standards

- Interior rebuilds (floors, stairs, kitchens, baths)

This is why many buyers broaden their search beyond $1 programs to other cheap homes in Italy that might cost more upfront but require less work overall.

Are These the Best Italian Villages Offering $1 Homes?

“Best” depends on your goals: access to airports, healthcare, fiber internet for work, year-round livability, and whether you want a true small-town experience. Some buyers want deep rural charm and slow living in Italy; others want a village setting within reach of a larger city.

When evaluating the best Italian villages offering $1 homes, focus on practical livability:

- Distance to a regional airport and major rail routes

- Internet speed and reliability (critical for remote work)

- Local contractor availability and renovation backlogs

- Year-round services (grocery, pharmacy, clinics)

A Texas-Friendly Reality Check: Financing, Timing, and Risk

Texas buyers are used to conventional mortgages, predictable closing timelines, and standardized disclosure norms. Italy can feel different. You may not be using a U.S.-style mortgage for a $1 property, and renovation financing can be more complex. Plan for longer timelines and more hands-on oversight than a typical Texas purchase.

Common Mistakes Americans Make

- Underestimating renovation costs and time

- Not budgeting for professional fees and permitting

- Assuming they can manage construction remotely without local help

- Skipping thorough due diligence on property condition and legal status

What About Patrica, Italy? A Related Option in Lazio

Even when the headline focuses on Sardinia, many Americans also research central Italy for its balance of scenery and accessibility. Interest has grown in places like Patrica Italy homes, where buyers look for value without being too far from larger hubs. If you’re comparing regions, Lazio region real estate can appeal to buyers who want countryside life with the option of reaching Rome for travel, services, and cultural amenities.

If your search includes Homes for sale in Patrica Italy, you may find opportunities that aren’t $1 but still qualify as affordable real estate in rural Italy. Sometimes, paying more upfront for a better-condition home can reduce renovation risk and get you living there sooner.

$1 Program vs. Low-Cost Traditional Listing: Pros and Cons

- $1 home pros: Symbolic purchase price, municipal support, community revitalization energy.

- $1 home cons: Heavy renovation requirements, strict deadlines, higher uncertainty.

- Low-cost listing pros: Often fewer structural surprises, faster move-in potential, clearer budgeting.

- Low-cost listing cons: Higher purchase price, less “program” assistance.

Can You Really “Start Over in Italy” and Make It Work?

For many, the appeal isn’t just price—it’s lifestyle. The idea to escape the US by buying a home in Italy, embrace Italian countryside living, and live the Italian dream is powerful. And yes, it can be done—especially for buyers who approach it with patience, cash reserves, and a realistic plan.

If your goal is to escape American lifestyle pressures and redesign your day-to-day life, the best path is usually a phased approach: rent first, test the town in multiple seasons, and confirm you can access healthcare, groceries, and reliable internet. Then buy—whether that’s a $1 project or another form of cheap homes in Italy that fits your timeline and budget.

Practical Tips for Texans Considering the Leap

- Plan a scouting trip: Visit at least once in the off-season to understand weather, services, and vibe.

- Price the renovation before you buy: Get local contractor input and a written scope of work.

- Build a buffer: Renovations in older homes often uncover surprises—budget accordingly.

- Think long-term: If you may rent it out, confirm local rules and realistic demand.

- Match the town to your life: If you need remote work from Italy, prioritize connectivity over postcard views.

The Bottom Line

The surge of interest in Italy real estate for Americans reflects a real shift: more people are questioning where and how they want to live. For Texans in particular—used to big horizons and big decisions—an Italian $1 home can be a meaningful project and a doorway to slow living in Italy, but only if you treat it like a serious investment, not a gimmick.

If you’re drawn to the idea to buy a home in Italy for $1, start with due diligence, build a strong local team, and budget for the renovation that turns a symbolic purchase into a real home. Done right, it can be a smart way of relocating to Italy on a budget—and, for some, a true chance to start over in Italy.

by Taylor Anderson | Jun 11, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

WeWork is finally WeProfitable again.

One year after restructuring its debt after declaring bankruptcy in November 2023, WeWork has regained profitability and is debt-free, the coworking company told Bisnow Tuesday.

The company became notorious for its shared working office spaces across the globe, ballooning to over 800 locations and reaching a market cap of nearly $10 billion in 2022 and a peak valuation of $47 billion.

The company renegotiated with creditors as a way to shed expensive and unprofitable leases and clear up its $4 billion in debt.

In April 2024, real estate tech company Yardi Systems announced that it had become the majority owner of WeWork and said it would guide it through its bankruptcy and into the future.

“We were burdened for many years with our portfolio that everybody knew about and saw,” WeWork Regional President for North America Luke Robinson told Bisnow.

Robinson told the news outlet that the company has now posted six-consecutive months of positive revenue before accounting for interest, taxes, depreciation and amortization, or EBITDA, a figure that indicates strong revenue but which doesn’t mean WeWork is turning a net profit.

It also confirmed to Inman that it now has 170 locations, which puts it among the largest coworking companies in the U.S. despite being far smaller than its 2019 peak.

In its previous heyday, the company gained fame both for its size, flashy office spaces and eccentric CEO Adam Neumann, who was behind the company’s rapid rise and its failure to successfully go public.

Under its new leadership, WeWork has also tweaked its approach at some locations, working directly with landlords to act as a property manager that leases space in buildings and shares revenues with the owners.

That’s alongside its more traditional approach of leasing space and then renting that space to people who need office space.

Several investors and landlords told Bisnow that WeWork’s leadership had shifted and regained trust in the industry, leaving the company an open pathway to rebuild and continue growing.

“When you have a firm where the pendulum has swung back and forth many times, when someone can provide trust and stability, that is a very precious commodity,” Cushman & Wakefield Chairman of Global Brokerage Bruce Mosler told Bisnow.

Email Taylor Anderson

by Matt Carter | Jun 11, 2025 | Industry, News Feed

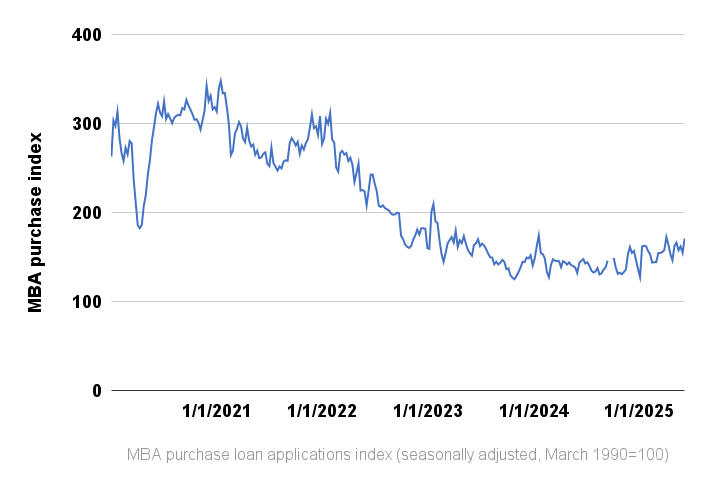

Purchase loan applications soared 10 percent last week to the highest level since April, even though rates have been stuck in the high sixes, the Mortgage Bankers Association reported Wednesday.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Mortgage rates aren’t coming down, but improving inventory in many markets helped drive up homebuyer demand for purchase loans to the second highest level of the year last week, the Mortgage Bankers Association reported Wednesday.

Demand for purchase mortgages was up by a seasonally adjusted 10 percent last week when compared to the week before, and 20 percent from a year ago. Requests to refinance were also up 16 percent week over week and 28 percent from a year ago, the MBA’s latest Weekly Mortgage Applications Survey found.

“Coming out of the Memorial Day holiday, mortgage applications increased to the highest level in over a month, driven by growth in both purchase and refinance applications,” MBA Deputy Chief Economist Joel Kan said in a statement.

Joel Kan

“Despite ongoing uncertainty surrounding the economy, homebuyers seem to be taking advantage of loosening housing inventory in certain markets,” Kan said.

Consumer sentiment about the housing market improved in May to the highest level since November, according to Fannie Mae’s monthly National Housing Survey.

While just 26 percent of Americans said May was a good time to buy, that’s up from 23 percent in April and 14 percent from a year ago, a survey low.

Mortgage rates stabilize

Rates for 30-year fixed-rate mortgages hit a 2025 low of 6.48 percent on April 4, according to lender data tracked by Optimal Blue.

Since climbing in early April over fears about the potential for tariffs to reignite inflation, rates for 30-year fixed-rate loans have been rangebound in the high sixes for the last 2 months.

Although inflation is nearing the Fed’s 2 percent goal, Fed policymakers are in a wait-and-see mode, while they assess the impacts of the Trump administration’s policies on tariffs, immigration, taxes and regulation. The job market is cooling off, but not quickly enough to alarm Fed policymakers.

The CME FedWatch tool, which tracks futures markets to predict the probability of future Fed moves, shows investors see no chance that the U.S. central bank will cut rates when policymakers meet next week.

But after an encouraging inflation report from the Bureau of Labor Statistics on Wednesday, futures markets tracked by the CME FedWatch tool priced in a 70 percent chance of a Sept. 17 rate cut, up from 62 percent on Tuesday.

Inflation moving in the right direction

The Consumer Price Index (CPI) showed the price of goods and services rose 2.35 percent from a year ago in May. While that’s up slightly from 2.31 percent in April, forecasters were expecting a bigger jump.

So far, tariffs are only having a “microscopic” impact on consumer prices, Pantheon Macroeconomics Chief U.S. Economist Samuel Tombs said in a note to clients. But he noted that it usually takes at least 3 months for retailers to pass cost increases on to consumers.

“Looking ahead, we continue to expect increases in prices for CPI core goods to gather momentum in June, then peak in July and remain above-trend for the rest of the year, assuming the current set of tariffs remain in place,” Tombs said.

The Federal Reserve’s preferred gauge of inflation, the personal consumption expenditures (PCE) index, showed the price of goods and services rose 2.1 percent in April from a year ago, the Bureau of Economic Analysis reported May 30.

The PCE index for May will be released on June 27.

Tombs said Pantheon Macroeconomics forecasters expect core PCE inflation, which excludes volatile food and energy prices, will climb to a peak of 3.25 percent around the end of the year.

Purchase loan demand rebounds

The MBA’s seasonally adjusted purchase loan index, which is benchmarked to March 1990, soared above 300 when mortgage rates plummeted to historic lows during the pandemic. But as inflation and mortgage rates surged in 2022, the index dropped below 200.

At 170.9 during the week ending June 6, the index is up 34 percent this year and approaching a 2025 high of 172.7 registered during the week ending April 4.

In addition to adjusting for seasonal factors — demand for homes usually peaks in the spring — last week’s index results included an adjustment for the Memorial Day holiday.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Marian McPherson | Jun 11, 2025 | Industry, News Feed

New York City’s broker fee bill went into effect on Wednesday, prohibiting property owners from passing broker fees onto renters. REBNY attempted to block the bill’s enforcement but failed.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

New York City’s controversial broker fee bill has gone into effect. This means rental property owners — not renters — must pay broker fees when they enlist a broker to help them lease a unit.

The New York City Council passed the bill, formally known as the Fairness in Apartment Rental Expenses (FARE) Act, in November with a vote of 42 to 8. The Real Estate Board of New York (REBNY) sued the City in December to stop FARE’s enforcement and filed an injunction on Tuesday, saying the bill shouldn’t be enforced until the lawsuit ends. However, Southern District of New York judge Ronnie Abrams denied REBNY’s request.

James Whelan | Credit: REBNY

“New Yorkers will soon realize the negative impacts of the FARE Act when listings become scarce, and rents rise,” REBNY President Jim Whelan told The Real Deal.

NYC Councilmember Chi A. Ossé pitched the FARE Act for two years and finally got traction in 2024 amid record rental growth. Ossé and his 33 co-sponsors said broker fees exacerbate high rental costs, with New Yorkers typically paying five figures to rent a unit, which includes the first month’s rent, a security deposit and a broker fee of one month’s rent or 10 to 15 percent of the annual rent.

“A party that purchases or contracts a good or service should be responsible for the cost,” Ossé, who represents Brooklyn, said last year. “This is the case in every other transaction across our vast economy, and should be true for New York City Rentals as well. The FARE Act has the potential to alleviate prohibitive upfront costs for workers and growing families searching for a new home.”

“If you want a broker, great, hire them. And if you don’t want one, my bill says you don’t have to pay,” he added.

Ossé said the bill will improve affordability for New Yorkers, an outcome that Zillow-owned StreetEasy supported through a report that found upfront rental costs had grown 19.28 percent from 2023 to 2024. For renters who leased a unit with broker fees, StreetEasy said they “likely spent 42.9 percent more” in upfront costs than renters who leased a unit without broker fees.

“This is a big win for renters,” StreetEasy Senior Economist Kenny Lee said.

However, early market trends hint that FARE’s supporters might be wrong.

The Wall Street Journal tracked rental listings in the days leading up to the bill’s enforcement, and found that property owners had hiked prices by hundreds of dollars. One unit that The WSJ tracked included a notice that the price would go from $3,300 per month to $3,975 per month if it wasn’t rented before the FARE Act’s enforcement.

REBNY warned that FARE would cause higher monthly rents, as property owners look for a way to offset the cost of brokers’ fees.

“What it really is going to do is complicate the transactions even further to where effectively that cost is going to have to be accrued through higher rent,” former REBNY VP of Government Affairs Ryan Monell told Inman in June 2024. “So while you may save some money on the front end of a transaction, the reality is the cost of the broker fee isn’t actually going to be evaporated into thin air.”

“For those who decide to renew the lease year over year, it’s going to be a problem,” he added. “When you’re looking at a higher base rent for the first year you’re in an apartment, it’s going to be effectively amortized over time because when you go to renew, generally in New York City, they raise your rent, say 5 percent.”

Even as rents experience a post-enforcement pop, New York City renters still seem to see FARE as a win — for now.

The WSJ spoke to 27-year-old NYC renter Rita Liu, who spent half of her savings to get into an apartment during a previous move.

“Landlords are going to jack up the rents no matter what,” she said. “If broker’s fees aren’t a factor now, moving would be a lot more feasible.”

Despite several hiccups in their suit, including Judge Abrams’ criticism of REBNY’s claims that the Act violates First Amendment rights and limits consumer choice, the Association said it won’t give up easily.

“We will continue to litigate this case as well as explore our avenues for appeal,” REBNY President Jim Whelan said.

Email Marian McPherson

by Matt Carter | Jun 11, 2025 | Industry, News Feed

Fort Wayne, Indiana-based Hallmark Home Mortgage is licensed in 18 states. Company founder and CEO Deborah Sturges is joining Fairway as a division manager.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Fairway Independent Mortgage Corp. will expand its presence in the Midwest with a deal to acquire “significant assets” of Indiana-based Hallmark Home Mortgage.

Hallmark will operate as a new division of Fairway, with CEO and founder Deborah Sturges joining Fairway with the title of president, Hallmark Home Mortgage, the companies announced Wednesday.

Deborah Sturges

“This strategic decision brings Fairway’s expanded product portfolio, enhanced technology, and deep support resources into Hallmark’s orbit,” Sturges said in a statement.

Terms of the deal were not disclosed.

Steve Jacobson

“Deborah and I worked together at Waterfield [Financial Corp.] decades ago and have remained industry acquaintances ever since,” Fairway founder and CEO Steve Jacobson said, in a statement. “Our shared values and our trust in each other make this partnership a natural fit. Our shared vision will make us even stronger together.”

Based in Fort Wayne, Indiana, Hallmark Home Mortgage is licensed in 18 states, sponsoring 45 mortgage loan originators who work out of 19 branch locations, according to Nationwide Mortgage Licensing System (NMLS) data.

In 2022, Hallmark hired former Finance of America divisional manager Marc Wadman to spearhead the lender’s expansion into Colorado, Georgia, Kansas, Louisiana, Missouri, South Carolina and Texas.

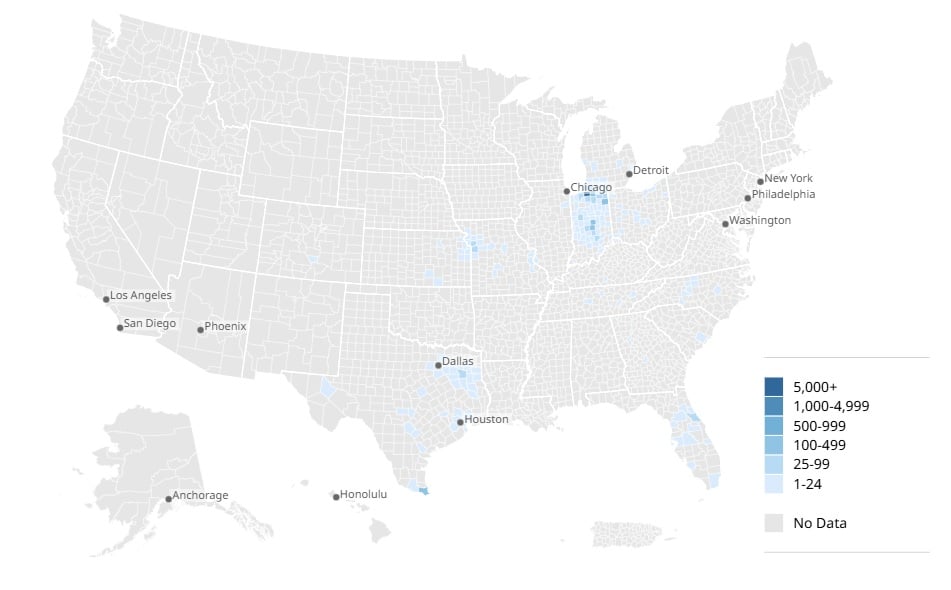

Hallmark mortgage originations by county

Source: iEmergent analysis of Home Mortgage Disclosure Act (HMDA) data.

Hallmark originated $591 million in mortgages last year, with most of that business in Indiana ($399 million), Texas ($88 million) and Missouri ($38 million), according to Home Mortgage Disclosure Act data tracked by iEmergent. Of the 2,640 loans Hallmark originated in 2024, 95 percent were purchase loans taken out by homebuyers

Based in Madison, Wisconsin, Fairway is licensed in all 50 states and sponsors 2,474 mortgage loan originators working out of 604 branch offices, according to NMLS data.

Fairway originated $23.7 billion in loans last year — 91 percent of them purchase loans — making the company the sixth-largest provider of loans to homebuyers, according to iEmergent data.

Fairway’s other trade names include 62PLUSHOMEBUYER.COM, CG HomeLoanPartners, Corporate Lending Group, MortgageBanc, Northpoint Mortgage and The Mortgage Reel. Fairway also owns the domain home.com, which redirects to the company’s homepage.

Last year, Fairway agreed to pay $10 million to settle allegations by federal regulators that the company engaged in redlining in the metro Birmingham, Alabama, market, which it entered in 2009 with the acquisition of MortgageBanc.

Fairway denied wrongdoing, saying regulators “did not identify any evidence of redlining or other discrimination,” and accused the government of acting in “bad faith” by characterizing Fairway’s actions as intentional, willful and reckless.

“Fairway vigorously defended itself against the government agencies’ allegations and continues to deny that the company engaged in any discriminatory behavior,” Fairway said in a statement in October.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Lillian Dickerson | Jun 11, 2025 | Industry, News Feed

The new allegation of aggravated sexual abuse by force, threat or intoxicant against Oren and Alon brings the total number of counts against the brothers collectively up to 10.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A third indictment was filed against former luxury brokers Tal and Oren Alexander and their brother, private security executive Alon Alexander, in the federal sex-trafficking case against them on Tuesday, which brings the total number of counts against the brothers up to 10.

The brothers now face one count of conspiracy to commit sex-trafficking; five counts of sex-trafficking by force, fraud or coercion; one count of sex-trafficking of a minor by force, fraud or coercion; two counts of inducement to travel to engage in unlawful sexual activity; and the new count of aggravated sexual abuse by force, threat or intoxicant.

The count added to the superseding indictment alleges that Alon and Oren used force to administer a “drug, intoxicant or other substance” to a seventh female victim who was unaware that she was being intoxicated in order to control her and cause her to engage in sexual acts while “on a Bahamian flagged cruise ship which departed from and arrived in the United States.” The previous indictment against them had identified six victims, one of whom was a minor.

The new indictment further states that as a result of the alleged offenses in the new count against them, Oren and Alon are to forfeit any real and personal property that was used or intended for use to commit the offense, “including but not limited to a sum of money in United States currency representing the amount of proceeds traceable to the commission of said offenses.”

The Alexander brothers were arrested on conspiracy to commit sex trafficking and sex trafficking charges in Miami in December 2024. A superseding indictment submitted by prosecutors in May added six new charges against them.

All three brothers have denied the charges against them.

A lawyer representing Alon told Inman in an emailed statement that, “The government continues to move backwards — the latest charge changes absolutely nothing and is merely a reheated version of the same case in an effort to keep the media firestorm going against the brothers.”

Another lawyer for Alon pointed Inman to a polygraph test that he passed in January while denying had ever had sex with a woman he knew had been given drugs.

Lawyers representing Oren and Tal did not immediately respond to Inman’s request for comment for this story, but after the superseding indictment was filed in May, attorneys for Tal said the new indictment “changes nothing,” and that it was “a reheated version of the same case — and still does not include conduct that amounts to federal sex trafficking.”

At that time, a lawyer for Oren told Inman that, “These new accusations, like the previous ones, are meritless, and reflect a failed prosecutorial effort to salvage a factually and legally unfounded case built on readily disprovable claims.”

Oren and Alon, as well as family friend Ohad Fisherman, also face state rape charges in Florida. Oren has been charged with three counts of sexual battery and Alon and Fisherman have been charged each with one count of sexual battery.

Several civil lawsuits submitted by dozens of women are also outstanding against the Alexander brothers in New York State and elsewhere. The majority of the lawsuits were filed in New York under an extension of a city law that allowed alleged victims of gender-motivated violence to sue their supposed perpetrators, no matter how long ago the alleged act of violence occurred. Victims were allowed to file lawsuits through the end of February 2025.

The brothers are currently being held in Brooklyn’s Metropolitan Detention Center.

Update: This story was updated after publishing with a comment from a lawyer representing Alon Alexander.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson