by Craig C. Rowe | May 20, 2025 | Industry, News Feed

Canadian real estate software company Virtuo is bringing its homeowner-centric concierge solution to buyers, builders and agents the United States, launching in Texas.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Canadian real estate software company Virtuo is bringing its homeowner-centric concierge solution to buyers, builders and agents the United States, Inman has learned.

A May 15 statement said that the company will launch operations in Texas.

“Although this marks Virtuo’s formal expansion into the American market, the company is no stranger to the U.S. Through longstanding relationships with Canadian builders operating stateside, including Shane Homes, Virtuo has already supported new home buyers in four states in the U.S.,” the release stated.

Virtuo brings together homebuilders, agents and buyers into a single ecosystem to ensure every stage of the purchase process remains connected. Rooted in new construction, the platform is part transaction manager and part post-close home assistant.

It uses an artificial intelligence called HomieAI to work alongside human counterparts to parse and empower construction and deal data into a wide array of productivity features, which in turn offers support, insights and reminders even after the home is built.

Plans call for the company to target homebuilders in Houston, Dallas and Austin. The construction space serves as the starting point for Virtue’s value proposition, as it marks the most logical starting point if the goal is to digitally manage a home transaction. The Lone Star State’s rapid and ongoing growth in the last 10 years continues to offer growth opportunities for any line of business in or adjacent to residential real estate.

Virtuo co-founder and CEO Casey Kachur said in a statement that Texas was a natural choice. Many of its major markets are also tech-friendly.

“From energy roots to entrepreneurial grit, the parallels between Alberta and Texas are striking,” Kachur said. “Having seen firsthand the appetite for a more connected, digital and stress-free experience, we’re excited to bring that same value to builders and homebuyers across the state.”

Inman reviewed Virtuo shortly before its formal launch in the States, noting its sharp balance between artificial intelligence and human guidance through the home transition.

“The features and benefits aren’t specifically delivered in any truly unique way, but Virtuo provides notable value as the digital source of truth for a home. It’s like being handed a CarFax as a car rolls off the assembly line, adding a great deal of authenticity to its history and, frankly, addresses what I disliked about all the other home management solutions that have come before it,” the review stated.

Email Craig Rowe

This post was originally published on this site

by Matt Carter | May 20, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Surveys show consumers and real estate professionals are increasingly anxious about the economy. But many would-be homebuyers would actually welcome a recession as an opportunity if it leads to lower prices and rates, polling shows.

The University of Michigan Index of Consumer Sentiment slipped to 50.8 in May, its second lowest reading ever, and only 23 percent of Americans surveyed by Fannie Mae in April said it was a good time to buy.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

And now a majority of Americans shopping for homes on Realtor.com (63%) expect the economy will dip into a recession within a year, according to a survey Monday from the official search portal of the National Association of Realtors.

“Confidence in the economy has clearly taken a hit amid ongoing headlines around trade, tariffs and rate uncertainty,” Realtor.com Chief Economist Danielle Hale said in a statement.

But 30 percent of would-be homebuyers visiting Realtor.com in the first three months of the year said a recession would make them at least somewhat more likely to buy — nearly twice the share (16 percent) who said they’d be less likely to buy if the economy tanks.

Danielle Hale

“Well-prepared buyers who have been waiting on the sidelines are likely motivated by personal and lifestyle needs like growing families, new jobs, or retirements and these considerations can outweigh short term economic uncertainties,” Hale said.

Elevated mortgage rates and a surge in home prices have priced many buyers out of the market, and a recession could bring relief on both fronts. That helps explain why last fall, 36 percent of Americans polled by LendingTree said they were hoping the housing market would crash in 2025.

While it’s unlikely many Americans want to relive the pain of the 2007-2009 Great Recession — in which millions of Americans lost their homes to foreclosure — a milder economic downturn could unlock inventory in markets where listings are scarce.

The mortgage lock-in effect — which makes homeowners with low rates reluctant to trade up or down because they’d have a higher rate on their new mortgage — diminishes when mortgage rates fall.

During the first week in May, demand for purchase loans picked up for the second week in a row as mortgage rates stabilized and more listings came on the market. Lenders received 18 percent more purchase mortgage applications during the week ending May 9 than had the same time a year ago, surveys by the Mortgage Bankers Association (MBA) show.

Mike Fratantoni

“Despite the economic uncertainty, the increase in home inventory means there are additional properties to buy, unlike the last two years, and this supply is supporting more transactions,” MBA Chief Economist Mike Fratantoni said of the most recent survey results.

Nationwide, there were 31 percent more homes for sale in April than there were a year ago, according to Realtor.com data. The 959,251 active for-sale listings that homebuyers had to choose from last month marked a new post-pandemic high.

What loan originators are seeing

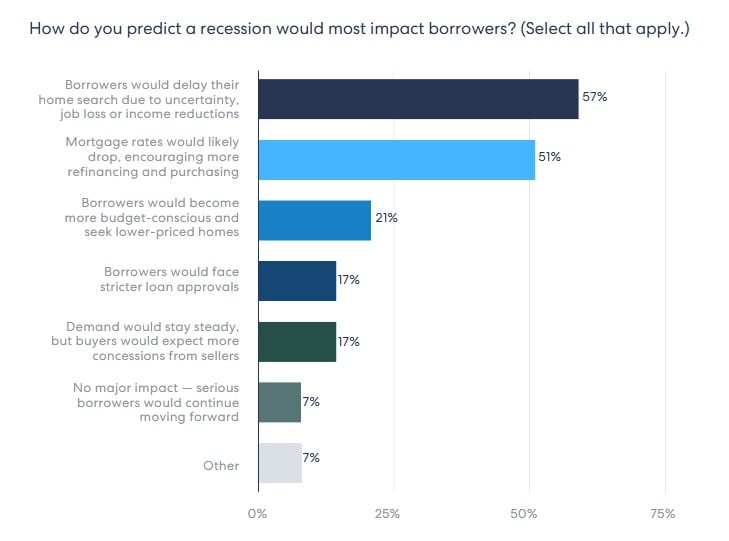

Most mortgage loan originators (63 percent) are also expecting a recession, and 57 percent think a recession would cause would-be homebuyers to delay their search due to uncertainty, job loss or income reductions, according to a recent survey by HomeLight.

But loan originators see a recession as a mixed bag, with slightly over half (51 percent) expecting that mortgage rates would also come down, leading to more homebuying and refinancing.

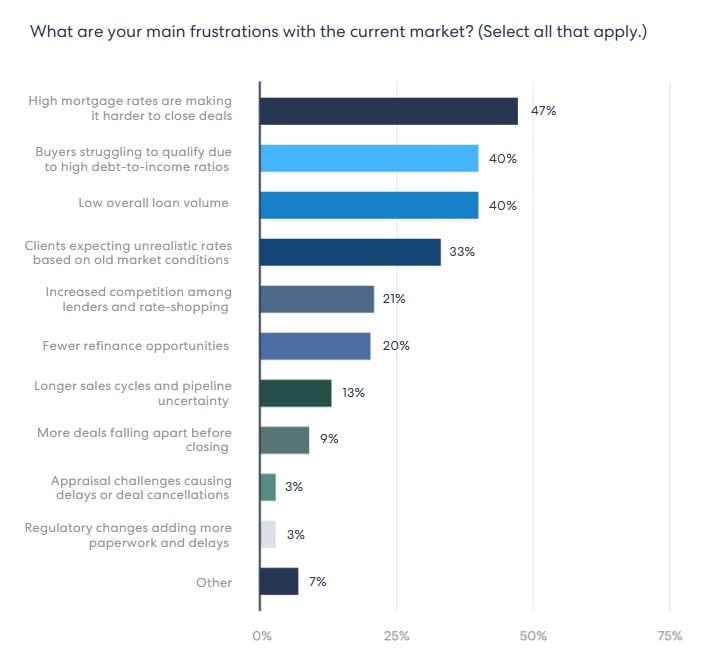

HomeLight’s Q2 2025 Lender Insights and Predictions survey, which was fielded between April 17 and 26, showed that loan originators expect that a recession would lead homebuyers to seek better deals and demand more seller concessions — and also have a harder time qualifying for a loan.

Seeing buyers struggling to qualify due to high debt-to-income ratios is already the second biggest frustration of loan originators, topped only by closings being derailed by elevated mortgage rates, HomeLight’s survey found.

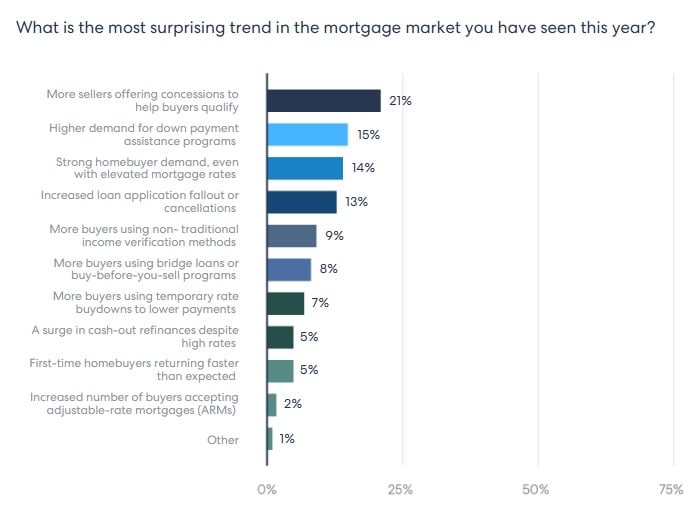

One in five loan originators (21 percent) said seller concessions are rising as a “surprising trend in the mortgage market” to help buyers qualify, and 15 percent said there’s more demand for down payment assistance programs.

Only 9 percent of loan officers surveyed by HomeLight say more deals are falling apart before closing, but that trend is on the rise.

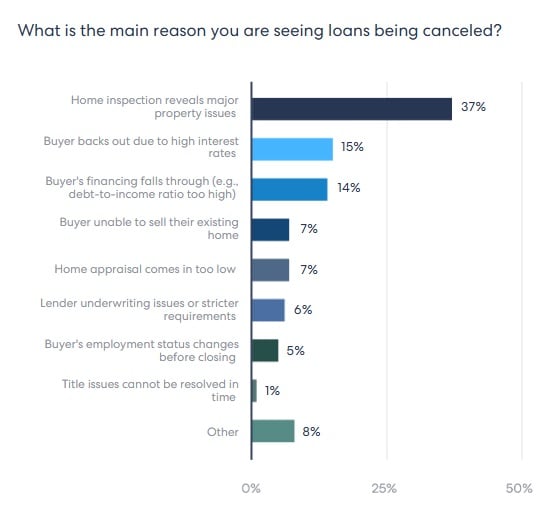

Home inspections are the main reason deals fall apart, 37 percent of loan originators said, followed by buyers getting cold feet over mortgage rates (15 percent) or seeing their financing fall through (14 percent).

Michelle Jacinto

“Buyer commitment is wishy-washy,” Michelle Jacinto, a branch manager at Direct Mortgage Loans LLC in Indiana, told HomeLight. “Any slight challenge, and they want to cancel. Anything from payments, cash to close, inspection items, or timeline changes.”

Devon Rowe, a mortgage advisor with Advantage Mortgage in Woodland, Washington, said buyers get nervous and news scares them.

A home inspection can “serve as a reason to back out of the contract, even when sellers are willing to do the repairs,” Rowe told HomeLight.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Richelle Hammiel | May 20, 2025 | Industry, News Feed

Roben Farzad took the stage at Inman On Tour Miami with a message that struck a rare balance between realism and resilience: We’re living in uncertain times, but history has shown that people adapt.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

At Inman On Tour Miami, journalist and public radio host Roben Farzad took the stage with a message that struck a rare balance between realism and resilience: Yes, we’re living in uncertain times, but history has shown time and time again that people adapt, markets evolve and somehow, we always find a way forward.

Farzad, who jokingly calls himself a “distressed journalist,” didn’t sugarcoat the moment we’re in. From the Great Recession to the chaos of COVID-19, from surging mortgage rates to the long tail of Trump-era tax policies, he painted a picture of a global economy that’s been rattled repeatedly.

Still, he urged the audience to zoom out and reflect.

TAKE THE INMAN INTEL SURVEY FOR MAY

In his Tuesday morning session, “Upside Down and Back Up Again: What’s Next for the Global Economy,” Farzad encouraged the audience to imagine it was 2007. Could anyone have predicted what was coming next? A housing crash, a financial meltdown, and eventually, a once-in-a-century pandemic? Of course not, but the world didn’t end. It rebalanced. It evolved.

“If you go to a Walmart, if you go to a Target, if you go to a Men’s Wearhouse, China is the manufacturer and the exporter of the world,” he said. “You’ve been able to take advantage of that peace dividend.”

Even Walmart’s chief procurement officer, Farzad noted, has been in a public back-and-forth with the White House, trying to hold prices down.

Then, there’s the bond market. Farzad recalled a surreal moment when the 10-year yields dropped below 0.5 percent. “I want you to put yourselves in that mindset, that weightlessness,” he said.

Despite all the instability, he returned to one key point: perspective. During the depths of the 2008-9 collapse, no one wanted to touch real estate in Miami. But in hindsight, that was exactly the time to buy.

Now, here we are again, caught in another moment that feels just as foggy. Farzad admitted he’s worried.

Credit card delinquency rates are rising, and people are struggling to make minimum payments even as job numbers grow.

“There are people not able to make the minimum debt payment over the next three months,” Farzad said. “You should not have that kind of deteriorating credit quality when jobs are being added.”

AJ Canaria Creative Services

The housing market, especially in places such as Miami, is flashing warning signs.

“This has left a lot of homebuyers thinking, maybe now, maybe never,” Farzad explained. “Are we at the fork in the road where inflation is going to worsen and the Fed has to come and finish the job?”

Farzad didn’t hold back on structural concerns either. Without workers, income or affordability, who will live in these places? Who will staff the buildings? Who will drive the Ubers? he asked the audience.

In Midtown Manhattan and Miami’s booming Brickell Avenue, hedge fund managers are buying up entire blocks. Goldman Sachs and others are doubling down on Palm Beach. But Farzad asked the question no one wants to answer: “Who’s going to keep the engine running?”

Even with all the glamour and investment, there’s a cost. “You’re getting tax benefits, but you’re paying more in quality of life, in staffing shortages, in basic services,” he said. “Welcome to Miami.”

That line carried weight for Farzad, who grew up just north of Surfside — the site of one of the most devastating building collapses in recent U.S. history.

To Farzad, it was inconceivable that the disaster could happen so close to where he grew up, but also in a place with zoning laws, building codes and condo boards.

What’s happening now, he said, feels like déjà vu. The skyline looks shiny again, but beneath the surface, cracks remain — figurative and literal. And that’s real estate. The wild ride from boom to bust — and sometimes, back again.

Email Richelle Hammiel

This post was originally published on this site

by Lillian Dickerson | May 20, 2025 | Industry, News Feed

Zillow will send warnings about non-compliant listings beginning May 28, but enforcement won’t start until June 30. Agents will receive two warnings before their third non-compliant listing is blocked, executives said.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Zillow on Tuesday published additional details for agents and brokers regarding how its new listing standards will play out once they go into effect in June.

In April, Zillow said it would begin enforcing the National Association of Realtors’ Clear Cooperation Policy with a ban on real estate listings that fail to make it on a multiple listing service or IDX feed of a portal within one business day of being marketed privately. The company also noted that listings that violated these new standards would be banned from the portal for the life of the listing agreement between that specific listing broker and homeseller.

TAKE THE INMAN INTEL SURVEY FOR MAY

The announcement spurred questions about what qualified as public marketing and which types of listings would violate Zillow’s new terms. With the more detailed guidance directed at industry professionals published on Tuesday, Zillow sought to bring more clarity to the standards as they are rolled out later this month.

“These listing access standards are how we’re implementing NAR’s Clear Cooperation Policy on Zillow sites and reflect our belief in fair access for all,” Zillow’s post states. “The standards apply to listings regardless of any applicable MLS rule. They apply to all listings subject to an exclusive for-sale listing agreement between a broker and a seller and therefore do not apply to builder inventory represented directly by the builder, rental listings or for sale by owner listings.”

The full listing access standards are now available for reference within Zillow’s Terms of Use.

Zillow clarified that it would be rolling the new standards out in phases, beginning in large markets in the U.S. and then nationally over the summer.

Agents will begin receiving notifications about non-compliant listings on May 28. However, the portal won’t begin blocking listings until June 30.

Zillow also noted that it will be adopting a type of ‘three-strikes, you’re out’ policy, where agents will only receive warnings about a listing violation for their first two non-compliant listings, and then their third non-compliant listing will be blocked from Zillow and Trulia starting on June 30, without warning. Still, those listings that meet Zillow’s standards — even if held by an agent who has received past violations — will remain visible on the platform.

“This notification period is designed to give agents ample time to understand and ensure they’re complying with the new listing access standards so all publicly marketed listings can reach the broadest audience of home shoppers online,” Zillow said.

In the guidance published on Tuesday Zillow addressed specific types of listings that agents had doubts about following their initial announcement in April, including office exclusives, coming soon listings and “sneak peeks” of listings. Under Zillow’s standards, office exclusives are permitted if a homeowner signs a seller disclosure and a listing is only shared within a single brokerage or during a one-on-one with clients, and not marketed publicly. Coming soon listings that are entered into the MLS within one business day and made available via IDX or VOW are also allowed. Likewise, sneak peeks on social media or in newsletters are also considered ok if they don’t include details that would liken it to a listing, including price and address or any call to action.

Zillow also specified that for sale by owner listings will not be impacted by the new standards, nor will new construction listings, unless they are listed with an agent under an exclusive listing agreement — in which case, those listings will be held to the new standards.

Zillow also said that delayed marketing listings, a new designation recently established by NAR, will also be allowed under the new standards as long as they are entered into the MLS and available to all MLS participants, including in an IDX or VOW listing feed.

The portal pointed out that sellers who want to sell their home privately still have multiple options available to them, including posting their property on the MLS for all participants to see but opting out of internet display, and hiding their address while still publishing a home on the MLS and to other websites that receive MLS feeds. If sellers wish their listing to remain completely private, Zillow said, they should be informed of the tradeoffs and sign a written agreement with their agent not to distribute the listing in the MLS or elsewhere online.

Email Lillian Dickerson

This post was originally published on this site

by Taylor Anderson | May 20, 2025 | Industry, News Feed

Vince Leisey, who is CEO of BHHS Ambassador Real Estate in Omaha, was named president of HSF Affiliates in the third leadership shakeup since rumors of a sale to Compass.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Berkshire Hathaway HomeServices continued shaking up its leadership team by appointing Vince Leisey as president of HSF Affiliates, the group’s parent company announced on Tuesday.

HomeServices of America, the owner of BHHS, noted that Leisey has been with the brand network for nearly three decades before he was tapped to lead the franchisor of the BHHS network.

The announcement came five weeks after Berkshire Hathaway replaced its former CEO Gino Blefari with Chris Kelly. The company also promoted its chief financial officer and named a new executive vice president, among other changes.

“Vince’s passion for the network and our franchisees, coupled with his results-oriented approach, makes him exceptionally well-suited to guide our affiliates through the next chapter [in] our rapidly evolving industry,” Kelly said in a statement. “He brings a rare combination of energy, insight and operational know-how, along with a deep respect for people. He is ideally suited for this role.”

HomeServices of America owns the Berkshire Hathaway HomeServices franchise network and is owned by Berkshire Hathaway Energy, a subsidiary of Warren Buffett’s Berkshire Hathaway.

Christy Budnick is the former president and CEO of HSF Affiliates. She stepped down last June, and Blefari took over her role until his retirement in April.

Leisey has served as CEO of BHHS Ambassador Real Estate in Omaha, where he leads an organization of over 1,000 agents transacting nearly $3 billion in annual sales, the company said. He will remain in that role while serving as president of HSF Affiliates.

Leisey is also the founder of the Explosion Real Estate Conference and a contributor to BHHS REthink Council.

“I have so much respect for the leaders across this network, and I look forward to partnering even more closely to drive growth, deliver value, and challenge ourselves to think differently about what’s possible,” Leisey said in a statement. “Together, I believe we can continue to build the most trusted, innovative, and agent-empowered brand in real estate.”

The changes to Berkshire Hathaway’s real estate unit started one month after reports emerged that the company was negotiating to be sold to Compass. HomeServices of America denied that any such negotiation was taking place.

“The good thing is, we can say there is no contemplated, no pending transaction with Compass or any third party at this point,” Kelly told Inman in April. “We’re hopeful that these management transitions that we’re making are kind of reflective of our parent entity’s complete, full faith in us moving forward.”

Kelly denied at the time that Blefari’s retirement had anything to do with the rumored sale. Instead, he said that Blefari decided to weather the storm the industry and company faced during the past 18 months before retiring.

“It was important to him to help shepherd us through those challenging moments,” Kelly said. “As we’ve come out on the other side and we and the broader industry are kind of turning the page on that chapter of real estate and we’re moving forward under the new rules and everything else that are now put into place, he felt this was the right time to do it.”

Email Taylor Anderson

This post was originally published on this site

by Richelle Hammiel | May 20, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The black dress, the effortless glamour and that signature blue door became timeless symbols thanks to Audrey Hepburn’s unforgettable turn in the 1961 classic Breakfast at Tiffany’s.

Now, the storied Upper East Side townhouse that served as the famous backdrop is on the market for $15 million, offering more than just a prestigious address, but a rare piece of cinematic history.

TAKE THE INMAN INTEL SURVEY FOR MAY

This landmarked residence, located at 169 East 71st Street in New York’s Upper East Side, has been meticulously reimagined to blend old Hollywood glamour with contemporary elegance.

Caroline Bass of The Corcoran Group is representing the property listing.

(Photo by Donaldson Collection / Michael Ochs Archives / Getty Images)

Loosely based on a Truman Capote novella, Breakfast at Tiffany’s follows the young socialite Holly Golightly as she navigates love and life in Manhattan. While the film’s interiors were shot on Hollywood sets, it’s this townhouse’s classic brick facade and signature blue door that drew people in and turned the property into a style icon in its own right.

(Photo by Paramount / Getty Images)

The iconic townhouse spans 4,465 square feet, encompassing five floors.

The parlor floor welcomes guests into a formal reception area, adorned with antique chandeliers and designer fixtures from Porta Romana. This level also houses an elegant living room and an intimate dining area.

The parlor floor features a gourmet kitchen, including a center island topped with Calcutta Gold marble.

The third floor offers two spacious bedrooms with spa-style baths, while the fourth floor is dedicated to the primary suite, complete with a custom dressing room and makeup vanity. At the top, a full-floor den boasts a wet bar, wine fridge and a Juliet balcony.

A garden unit at street level offers its own private entrance, built-in bookshelves, a den and a large bedroom. Its open kitchen leads directly to a 466-square-foot landscaped garden framed by custom Walpole lattice fencing.

The fully excavated basement adds another dimension to the home with nearly 8-foot ceilings, a powder room, a wine cellar and cold storage.

Canva / Google Maps

In total, the two-family residence includes four bedrooms, four full bathrooms, three powder rooms and a full-sized elevator servicing every level.

The home’s renovation was led by current owner Joseph Harkins, a retired beverage executive and entrepreneur, who purchased the home for $7.4 million in 2015, the New York Post reported.

The landmarked townhouse “doesn’t just sit on one of the Upper East Side’s most enchanting blocks; it defines it, Bass said. “There are homes. And then, there are icons.”

Email Richelle Hammiel

This post was originally published on this site