by Alyssa Stalker | May 31, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

In the age of AI, it has never been easier to generate content that sounds polished and informative. From listing descriptions to social media captions, tools like ChatGPT and other generative AI platforms promise to save time and elevate your presence online. But as more of this content floods the market, it is clear that it often has a certain sameness. And that can be a problem.

TAKE THE INMAN INTEL SURVEY FOR MAY

I have seen it firsthand in my work with real estate agents and entrepreneurs. AI-generated content can be a great starting point, but it is easy to spot when something is missing: your real voice, your lived experience and the nuances that make you, you.

6 telltale signs it’s AI

Here is how to tell if what you are looking at was written by AI and, more importantly, how to avoid falling into these traps yourself.

1. Phrases that feel like a pattern, not a conversation

One of the biggest giveaways is the kind of language that feels like it was pulled from a script, not spoken in a real conversation. You know the type: Phrases like “Here’s why this matters” or “It’s not just a home, it’s a lifestyle” that pop up again and again. While these can help make a point, they do not sound like how you would naturally talk to a client or colleague.

In real estate, that difference really stands out. Clients want to hear your authentic voice, something that reflects how you would naturally explain things in a conversation. If your listing description or Instagram caption starts to read like a set of talking points, it is time to step back and bring in more of your real thoughts and feelings.

2. Overuse of punctuation that does not match your style

Another telltale sign is the punctuation itself. I have noticed that AI-generated writing often leans heavily on em dashes or semicolons. While these are perfectly acceptable punctuation marks, they can feel out of place if they do not reflect how you normally write or speak.

When reviewing your content, read it out loud. If the punctuation does not flow with your natural rhythm, it might be a sign you are leaning too much on AI. Simplify where it makes sense and let your authentic voice guide the structure.

3. A tone that does not match how you speak

This might be the biggest giveaway of all. If you know someone’s voice well, you can tell when they are speaking differently. AI content often lacks the nuance of your real-world experiences. It can sound overly formal or too casual in a way that does not match your personal style.

As a real estate coach and brand strategist, I have found that this is where most agents get tripped up. They will use AI to write a property description or an Instagram caption, and it just does not sound like them.

Your clients are not just reading words on a page, they are listening for the voice of someone they trust so make sure the tone aligns with how you would actually speak if you were talking to them face to face.

4. Data without context or perspective

AI is great at pulling together facts and stats. But it often falls short in weaving those numbers into a larger narrative. If you are reading something that feels like a data dump with no real insight or perspective, that is a red flag.

In real estate, you see this with market updates that list median prices, days on market and price per square foot without tying those stats back to what they actually mean for your clients. If the writing does not connect the dots between the numbers and the impact on your ideal audience, it is missing the point.

When you are using AI tools, make sure to add your own perspective. Talk about how those stats affect your clients or your market. Bring the data to life with your insights and stories.

5. No personal experience or real stories

One of the most valuable things you can bring to your content is your own experience. AI does not have that. It can pull together information from thousands of sources, but it cannot replicate the feeling of walking into a house for the first time with a client, the excitement of negotiating a great deal, or the challenge of helping someone navigate a tricky market.

This is why AI-generated content often feels hollow. It might be technically accurate, but it does not have the weight of lived experience. That is something only you can offer.

In my own writing, I always try to share what I have seen in the field, whether that is insights from agents I coach or observations from my own time in real estate. It is those real-world moments that connect with people and make your content stand out.

6. A sense of déjà vu

Finally, if what you are reading feels like you have seen it a hundred times before, there is a good chance AI wrote it. These tools are trained on existing content, so they are great at recreating what is already out there. But they struggle to push beyond that and create something truly new.

This is why I encourage agents to always start with their own perspective. Use AI to help with the structure or to find the right words, but make sure you are the one driving the story. Fresh ideas come from real people, not algorithms.

How to keep your content sounding like you

So, what is the fix? You don’t need to swear off AI entirely; in fact, you shouldn’t. These tools can be incredibly helpful for brainstorming, outlining or even tightening up your writing.

Here is what I recommend:

- Start with your voice first. Use AI to clean up your drafts, but make sure you are the one setting the tone and direction. Consider uploading previous content you have actually written, from property descriptions to Instagram captions, to help the AI better understand your voice.

- Fact-check everything. AI can get things wrong, so double-check stats, numbers and even basic information.

- Add your own perspective. Clients hire you for your insights, not a generic script.

- Read it out loud. If it does not sound like you, rewrite it until it does.

At the end of the day, AI is just another tool in your toolbox. It is not a replacement for your real-world expertise, your perspective or your ability to connect with clients. In a world where AI-generated content is everywhere, your voice is more valuable than ever.

Alyssa Stalker is a real estate branding strategist and host of the Above Asking podcast. Connect with her on LinkedIn or Instagram.

This post was originally published on this site

by Inman | May 30, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Want to level up your business? Inman Access offers expert-led tutorials with insights, advice and ideas designed to help you build your skills every day.

In any market, but especially in today’s marketplace, recruiting the best of the best agents can be a challenge. Vija Williams, head of industry at Place.com, provides an actionable framework to help you create a better value proposition to recruit experienced agents.

Elevate your skills and set yourself up for success in 2025. Watch the session above, plus get fresh content added weekly, with Inman Access.

Watch now.

This post was originally published on this site

by Matt Carter | May 30, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Inflation continued to move closer to the Federal Reserve’s 2 percent target in April, but central bank policymakers are expected to resist calls by the Trump administration to cut interest rates as they continue to assess the impacts of the administration’s policies in areas including tariffs, immigration, taxes and regulation.

The personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred gauge of inflation, showed the price of goods and services rose 2.1 percent in April from a year ago, the Bureau of Economic Analysis reported Friday.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

It was the second month in a row that the annual increase in the PCE price index moved in the right direction. The core PCE price index, which excludes volatile food and energy costs and is seen as a better indicator of inflation trends, showed costs were up 2.5 percent from a year ago — the lowest reading in 4 years.

Inflation moving toward Fed’s goal

Before the latest inflation numbers were released, Federal Housing Finance Agency Director Bill Pulte urged Fed policymakers to cut rates when they meet next on June 17.

Bill Pulte

“First and foremost, inflation is lower than it was the last time they cut,” Pulte said Thursday in an appearance on Bloomberg’s The Close. “President Trump has been very successful at reducing inflation, and so therefore it just only makes sense that if inflation was higher and they did cuts, then why can’t they do cuts now?”

While the Fed has tight control over short-term interest rates, mortgage rates are largely determined by investor demand for mortgage-backed securities (MBS), the ultimate source of funding for most home loans.

As the Fed cut short-term interest rates by a full percentage point at the end of last year, mortgage rates moved in the other direction, as economic data coming in last fall showed inflation moving away from the Federal Reserve’s 2 percent target.

But Trump himself remains fixated on the Fed, calling Federal Reserve Chair Jerome Powell “a FOOL, who doesn’t have a clue” in a May 8 Truth Social post after Fed policymakers voted unanimously to keep the short-term federal funds rate at 4.25 percent to 4.5 percent.

At a press conference following the meeting, Powell said the job market remains “solid,” but tariffs implemented and threatened by the Trump administration could reignite inflation. “The new administration is in the process of implementing substantial policy changes in four distinct areas: trade, immigration, fiscal policy and regulation.”

Tariff increases announced so far have been “significantly larger than anticipated,” the Fed chair said, and if implemented, “are likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment.”

Forecasters at Pantheon Macroeconomics are seeing early signs that tariffs are having an impact on prices, with core PCE inflation up 0.3 percent from March to April, Pantheon Senior U.S. Economist Oliver Allen said in a note to clients Friday.

Oliver Allen

“Much bigger increases in core goods inflation probably loom as the costs of the new tariffs are eventually passed on,” Allen said. “Accordingly, we still think core PCE inflation will peak later this year between 3 percent and 3.5 percent, if the current mix of tariffs remains in place.”

The CME FedWatch tool, which tracks futures markets to predict the probability of future Fed moves, shows investors don’t expect the Fed to cut short-term rates until September. But bets placed by investors on Friday indicate a 72 percent chance of a September rate cut, up from 66 percent on Thursday and 60 percent on May 23.

When the European Central Bank continued to cut rates in April while the Federal Reserve continued to take a wait-and-see stance, Trump complained that Powell “is always TOO LATE AND WRONG” and said his “termination cannot come fast enough!”

In a May 22 order, the Supreme Court made it clear that Trump can’t fire Powell without cause — the constitutionality of for-cause removal protections for members of the Federal Reserve’s Board of Governors are not in dispute.

Powell met with Trump at the White House Thursday “to discuss economic developments” including growth, employment and inflation, the Fed disclosed after the meeting.

“Chair Powell did not discuss his expectations for monetary policy, except to stress that the path of policy will depend entirely on incoming economic information and what that means for the outlook,” the Fed said in a statement. Fed policymakers will base their decisions “solely on careful, objective, and non-political analysis.”

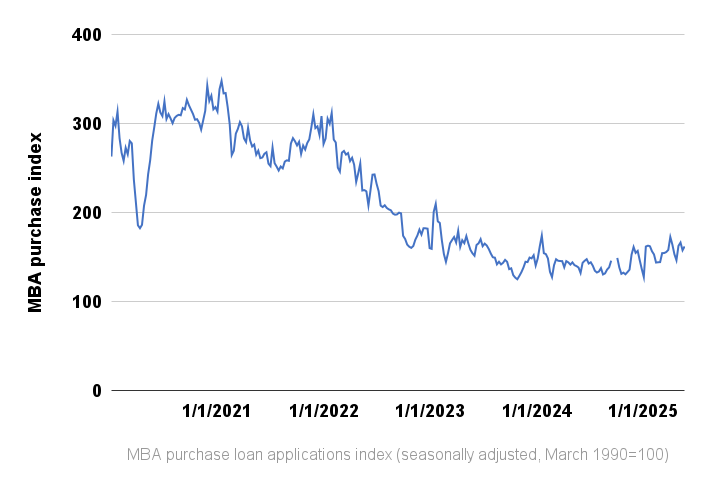

Mortgage rates on the rebound

Since hitting a 2025 low of 6.48 percent on April 4, rates on 30-year fixed-rate conforming mortgages have been trending back up and flirting with January highs, according to lender data tracked by Optimal Blue.

A weekly survey of lenders by the Mortgage Bankers Association shows demand for mortgages has slipped in recent weeks, but is stronger than it was a year ago.

Joel Kan

Thanks to more homes coming onto the market, applications for purchase loans were up by a seasonally adjusted 3 percent last week compared to the week before, and 18 percent higher than a year ago, MBA Deputy Chief Economist Joel Kan said.

With mortgage rates returning to the highest level since January, applications to refinance were down 7 percent week over week, but up 37 percent from a year ago.

“Purchase applications were up over the week and continue to run ahead of last year’s pace as increased housing inventory in many markets has been supporting some transaction volume, despite the economic uncertainty,” Kan said in a statement.

After hitting a 2025 high of 172.7 during the week ending April 4 as mortgage rates were touching lows for the year, the MBA’s seasonally adjusted purchase index retreated to 146.6 during the week ending April 25.

At 162.1 during the week ending May 23, the MBA purchase index is up 28 percent from its 2025 low of 127.7 registered during the first week in January.

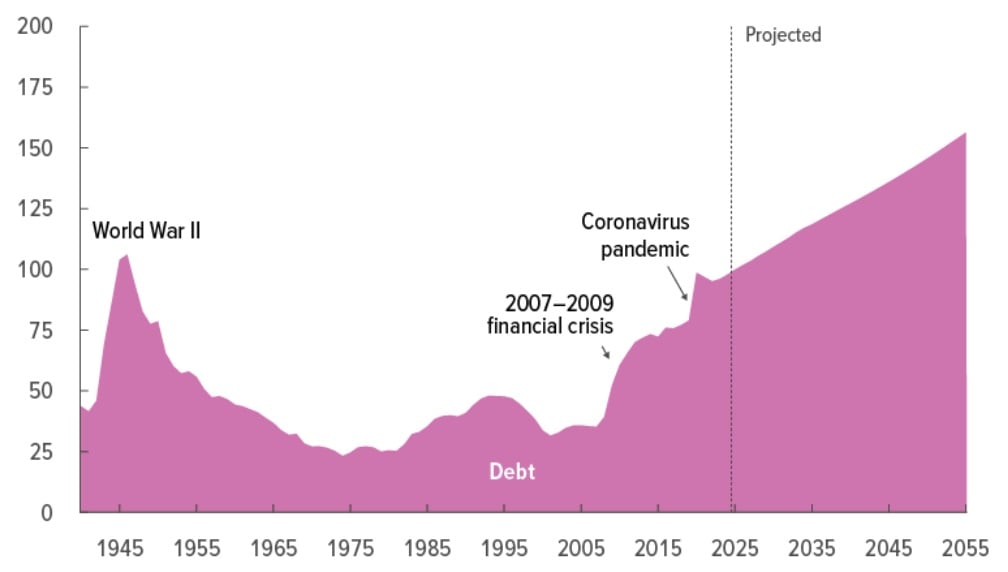

While the potential for tariffs to reignite inflation is an immediate concern for investors that has helped drive up mortgage rates, the potential for tax cuts proposed in Trump’s “big beautiful bill” to drive up federal debt is also on their long-term horizon.

On May 16, Moody’s Ratings became the last of the big rating agencies to downgrade the U.S.’s credit rating, over concerns that “successive U.S. administrations” and Congress have failed to tackle the nation’s annual budget deficits and growing interest costs.

CBO projects record government debt by 2029

The Congressional Budget Office in March projected that federal debt as a percentage of gross domestic product (GDP) will hit record levels in 2029 and continue to rise.

Trump has complained that dire projections of how extending tax cuts granted by the 2017 Tax Cuts and Jobs Act will impact deficits underestimates the boost in revenue the federal government might see if the U.S. economy grows at a faster clip.

Trump revisited that debate on Friday, calling growth projections by the Congressional Budget Office “ridiculous and unpatriotic.”

Trump advisor Peter Navarro provided more insight into Trump’s thinking Wednesday in an opinion piece for The Hill.

Navarro said that investor demands for higher yields on 10-year Treasurys — a key barometer for mortgage rates — “reflects fear, not facts.”

Peter Navarro

Bond investors, he said, “are pricing in a future where the government borrows trillions more with no offsetting revenues. They believe the tax cuts are not paid for.”

But Navarro claimed, “Trumpnomics and the Trump tariffs will put America on a sounder fiscal footing than any policy proposal in decades. That’s the complete information our financial markets should be working from – and bond investors should yield to that wisdom.”

Yields on 10-year Treasurys were essentially unchanged Friday at 4.41 percent, despite the encouraging April inflation numbers.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Christy Murdock | May 30, 2025 | Industry, News Feed

The National Association of Realtors will tackle the topic at its midyear Legislative Meetings next week, even after a Texas speech bill targeting NAR and other groups died abruptly on Wednesday.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Each week on The Download, Inman’s Christy Murdock takes a deeper look at the top-read stories of the week to give you what you’ll need to meet Monday head-on. This week: Now that the Texas speech bill is dead, NAR prepares to tackle the topic at its midyear Legislative Meetings.

Since it went into effect in November 2020, Standard of Practice 10-5 has courted controversy while seeking to ensure that members of the National Association of Realtors (NAR) put the best possible face on the industry and on their individual businesses.

TAKE THE INMAN INTEL SURVEY FOR MAY

While NAR has attempted to explain the specifics of the SOP, many members argue that it violates their right to free speech. Now, following its multi-million dollar settlement in the commission lawsuit and the onboarding of new counsel, the trade group is showing signs that it’s hedging its bets when it comes to the controversial rule.

In an appendix to this year’s agenda for its Legislative Meetings, running from May 31 to June 5, a note indicated that NAR has identified part of the Code of Ethics and one of its policy statements as “sources of potential risk” or potential legal liability.

The Code of Ethics rule bars Realtors from using “harassing speech, hate speech, epithets, or slurs” based on any number of protected classes, while the policy statement indicates that members of the trade organization can face disciplinary action for violations of the Code of Ethics.

The agenda states that any changes under consideration are meant to add “clarity” and “to reduce risk to state and local associations and their volunteer leadership.” The consideration comes amid the hubbub surrounding a bill in the Texas legislature that was designed to push back against trade groups’ speech rules, with implications for the real estate industry in particular.

That bill, however, died in a House committee on Wednesday following its passage in the Texas Senate.

EXTRA: Texas hate speech bill ‘dead’ as NAR considers ethics code change

As you consult your own moral compass, provide leadership to others and balance personal perspectives with professional obligations, this week, Inman contributors had plenty of food for thought to help you navigate today’s treacherous cultural divides.

The real estate industry prides itself on professionalism and ethical conduct. When it comes to LGBTQ+ clients and colleagues, broker Justin Ziegler writes, it’s time to put words into action.

EXTRA: Parents, families and allies of LGBTQ+ kids, it’s time to step up

Confident leadership is woven from truth, not titles. You build it from the inside out, Debra Trappen writes in the latest installment of her Lead with Fire series.

EXTRA: The top 10 characteristics of a great real estate broker

Tanya Monestier’s appeal to the commission settlement isn’t just a legal challenge, compliance expert Summer Goralik writes. It’s a reality check the industry didn’t see coming.

EXTRA: How has being a buyer’s agent changed in the past year? Pulse

This post was originally published on this site

by Lillian Dickerson | May 30, 2025 | Industry, News Feed

The fourth amended settlement, if approved, would prohibit offers of cooperative compensation on MLS PIN’s platform and raises the total proposed settlement fund from $3 million to $3.95 million.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The Department of Justice (DOJ) has suggested that it will likely approve a fourth amended settlement agreement in the commission lawsuit known as Nosalek, according to a legal filing submitted on Thursday.

The amended settlement negotiated by MLS Property Information Network (PIN) and homeseller plaintiffs would prohibit offers of cooperative compensation on the MLS’s platform, a move that other MLSs previously made in the settlement of the Sitzer | Burnett commission case. It also raises the total proposed settlement fund from $3 million to $3.95 million, which the filing notes is the same amount it would have cost MLS PIN to join NAR’s settlement in Sitzer | Burnett.

TAKE THE INMAN INTEL SURVEY FOR MAY

The filing submitted Thursday states that, “in addition to working to address the concerns expressed by the Court following [the April 1] Hearing, Plaintiffs and MLS PIN also conferred with the Antitrust Division of the United States Department of Justice. After considering the proposed amendments, the Division indicated that it would no longer object to the proposed settlement on the basis of Rule 23.”

However, the memorandum in support of preliminary approval of the amended settlement also notes that this doesn’t mean the DOJ is completely finished scrutinizing the case either.

“The parties understand that the Division intends to file a brief statement with the Court withdrawing its previous objection while otherwise retaining all rights to bring a separate enforcement action,” the filing said.

Lawyers for the plaintiffs and the defendants did not immediately respond to Inman’s requests for comment.

A preliminary settlement approval hearing is scheduled for June 10 in Massachusetts federal court.

During the April 1 hearing, Judge Patti Saris of the U.S. District Court for the District of Massachusetts said she would not approve the proposed settlement unless the scope of the settlement was narrowed to only include residential listings, instead of all real estate listings, within MLS PIN’s service area since other types of properties were not applicable to the case’s plaintiffs. MLS PIN has since made that amendment to the proposed settlement.

MLS PIN was the first defendant in the case to reach a settlement with plaintiffs in 2023. However, the terms of the settlement have continued to be intensely scrutinized by the DOJ, which has delayed the parties from reaching a final settlement. MLS PIN is also broker-owned, and therefore not bound by the terms of NAR’s settlement in antitrust cases. In ultimately agreeing to remove offers of cooperative compensation from its platform, however, the MLS settlement is more in line with that agreed upon in Sitzer | Burnett.

Other defendants in the Nosalek case, including HomeServices of America, Keller Williams, Anywhere and RE/MAX, have all now been granted final approval of their settlements. NAR’s $418 million settlement was granted approval in November.

Email Lillian Dickerson

This post was originally published on this site

by Dani Vanderboegh | May 30, 2025 | Industry, News Feed

Turn up the volume on your real estate success at Inman On Tour: Nashville! Connect with industry trailblazers and top-tier speakers to gain powerful insights, cutting-edge strategies, and invaluable connections. Elevate your business and achieve your boldest goals — all with Music City magic. Register now.

Every Friday, Inman Service Editor Dani Vanderboegh rounds up the most popular, most read, most critical stories of the week to give you a quick catchup on the big headlines you might have missed in the hustle and bustle of the workweek. Here’s this week’s Top 5 as chosen by our readers.

P.S. Don’t miss The Download, our weekly column that breaks down one of the week’s top stories and equips you with what you’ll need to meet next Monday head-on.

The changes would offer a specific definition of “harassment” and aim to reduce liability. The prospect of change comes as Texas lawmakers consider a bill that could conflict with current NAR rules.

CEO Hoby Hanna sent a letter to NAR and the more than 70 MLSs the major real estate brokerage belongs to informing them that it will no longer consider itself bound by the policy.

Jimmy Burgess and marketing expert Jason Pantana share perspective on the power of artificial intelligence tools and their place in the modern agent’s toolbox.

Tanya Monestier’s appeal to the commission settlement isn’t just a legal challenge, compliance expert Summer Goralik writes. It’s a reality check the industry didn’t see coming.

Troy Palmquist offers a solution for adding value and staying in front of your sphere by providing a referral directory for local service providers.

Email Editorial

This post was originally published on this site