by Holly Brink | Jun 4, 2025 | Industry, News Feed

Tailor your outreach and communication to the individual agent so that you’re providing what they need to thrive, broker Holly Brink writes.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

You know the cost of losing an agent — hundreds of hours spent recruiting, onboarding and coaching, only to watch them walk away chasing the next shiny thing. In 2025, the brokerages that make their people feel seen, heard and genuinely supported will win the war for talent.

1. Map out a real career roadmap

Agents need more than a commission split — they need a roadmap. Last year, during a one-on-one meeting, I sat down with Emily, who was eager for her next milestone. We set a target: Earn her Broker Associate designation by her next renewal, then lead a Wednesday Business Builder on the topic of CapCut. By spring, she’d nailed both and had the momentum to recruit and mentor two new agents herself.

How you do it: Sketch each agent’s “next three wins” (on a whiteboard or in a shared doc), assign deadlines, then revisit quarterly — no radio silence — just clear, bite-sized steps toward big ambitions.

2. Carve out ‘show up and chat’ time

Every weekday morning for the past four years, I’ve hosted a Zero-agenda coffee chat from 9 a.m. to 9:30 a.m. CST on Zoom. Agents drop in to vent, brainstorm or celebrate. Newbies get solutions quickly, veterans share battle-tested tips and mentorship sparks organically. For anything confidential — such as contract snags or client conflicts — we offer 15-minute one-on-one meetings via Calendly. Those office hours say loud and clear: “I’ve got your back.”

3. Champion wins—At work and beyond

Agents aren’t just revenue engines — they’re people with life-defining milestones. When Lindsey welcomed her baby, we surprised her with a curated “baby box.” When Ki’erra made the dean’s list, we ran a social media shout-out. When Angela secured dual U.S./Australia citizenship, we cheered her on just as loudly as any sales award.

Sharing these moments in our weekly huddle and across social channels builds real connection — and loyalty — far beyond what another ping-pong table could ever achieve.

4. Automate the admin, not the relationship

Nobody sticks around for paperwork. At MyRECo, we automate tedious tasks so agents can focus on building relationships, not data entry. From lead follow-up reminders to compliance check-ins and a living template library, our systems handle the “busy,” so agents can sell and serve. That productivity boost isn’t a “perk”; it’s why our people feel truly supported.

5. Keep the conversation flowing

“Your vibe attracts your tribe,” so we’ve woven feedback into our daily rhythm — no fancy surveys required:

- Daily coffee chat: 9 a.m. to 9:30 a.m. CST on Zoom — no slides, just straight talk.

- Monthly one-on-ones: Book a 15-minute slot via Calendly for deeper or confidential check-ins.

- #agent-feedback and private-support-chat Slack channels: Ideas, kudos and pain points go straight to leadership.

- Regular vibe checks: We pull top topics from Slack and coffee chat and dedicate our next live huddle to what we’re stopping, starting or doubling down on.

Regular touchpoints demonstrate that we’re listening — and taking action.

Yes, your agents are independent contractors, and nobody wants Big Brother hovering. The key is tailoring your outreach: Some agents crave a quick text, others prefer a video call or a lengthy one-on-one coaching session. Ask what they need, then deliver. That custom touch, powered by systemized automation and genuine facetime, is the retention secret for 2025.

Retention isn’t about free signs or flashy swag. It’s about career clarity, dependable access, genuine celebration and a listening culture. Nail these five fundamentals, and your agents will stick around long past the next commission check — because they won’t just work for you, they’ll want to work with you.

Holly Brink is the co-founder, COO and managing broker of My Real Estate Company in Iowa, Minnesota, Nebraska and Illinois. Connect with her on Instagram or LinkedIn.

by Matt Carter | Jun 3, 2025 | Industry, News Feed

Although Rocket’s plans to acquire Mr. Cooper and Redfin are structured as all-stock deals, assuming their debts will leave Rocket more highly leveraged, Fitch analysts said of possible debt rating downgrade.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Rocket Companies will make the most of the company’s credit rating to issue $4 billion in debt and use the proceeds to retire notes held by a subsidiary of the nation’s largest mortgage servicer, Mr. Cooper, which Rocket plans to acquire this year.

Rocket said Tuesday it plans to issue $2 billion in senior unsecured notes due in 2030 and another $2 billion due in 2033.

After the Mr. Cooper acquisition closes, Rocket will use part of the proceeds to pay off $1.95 billion in notes owed by Mr. Cooper subsidiary Nationstar Mortgage Holdings Inc. that are due in 2026, 2027 and 2028.

The remaining proceeds may be used “at the company’s discretion” to pay off, purchase or amend additional Nationstar notes that will be due in 2029, 2030, 2031 and 2032.

Mr. Cooper had $11.3 billion in outstanding debt as of March 31, including $4.95 billion in unsecured senior notes at interest rates ranging from 5 percent to 7.125 percent. Due dates for the notes are spread out over six years, from 2026 to 2032.

Rocket’s plans to acquire not only Mr. Cooper but real estate brokerage Redfin attracted the attention of analysts at Fitch Ratings, who in March warned that they may downgrade debt issued by subsidiary Rocket Mortgage to junk bond status.

In placing Rocket Mortgage’s issuer default rating on “rating watch negative,” Fitch analysts said Rocket has a “strong liquidity profile,” but will probably have to keep borrowing in order to fund loans and acquire mortgage servicing rights after it closes the deals to acquire Mr. Cooper and Redfin.

Fitch analysts said they will weigh a downgrade on Rocket Mortgage’s long-term issuer default rating (IDR) to “‘BB+’ from ‘BBB-,’” which would make it more costly for Rocket to borrow money.

Although both the Mr. Cooper and Redfin acquisitions are structured as all-stock deals, assuming Mr. Cooper and Redfin’s debt obligations will leave Rocket more highly leveraged.

Fitch estimates that the Mr. Cooper deal will more than double Rocket’s corporate leverage ratio, from 0.6x to 1.4x after the deal closes.

Mr. Cooper’s corporate leverage ratio was 2.1x at the end of last year, and Fitch analysts said they expect to upgrade the company’s BB issuer rating.

At the time the deals were announced, the all-stock transactions valued Mr. Cooper at $9.4 billion, while Redfin was valued at $1.75 billion.

In reporting first-quarter earnings, Rocket executives said they expect the Redfin deal to close as soon as this quarter, which ends June 30, and that the Mr. Cooper acquisition remains on track to close by the end of the year.

Speaking at an investment conference in May, Rocket CEO Varun Krishna said over the past several years, Rocket has invested about $500 million in AI and other technology that will help the company scale its business without a proportionate increase in expenses after the merger.

He said Rocket’s acquisition of Redfin will help it achieve its goal of capturing 8 percent of the purchase loan market, and the Mr. Cooper deal will put Rocket in touch with more homeowners who might be ready to refinance.

Rocket wants to handle 20 percent of U.S. mortgage refinancings. After acquiring Mr. Cooper, Rocket will be collecting payments on $2.1 trillion in mortgage loans — about one in six U.S. mortgages. When those homeowners are ready to refinance, Rocket will have a leg up on “recapturing” their business, Krishna said.

“Having a relationship at the top of the funnel and with real estate agents allows you to build a stronger organic purchase business,” Krishna said of the Redfin deal. “Having a servicing book allows you to build an organic servicing recapture business.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Craig C. Rowe | Jun 3, 2025 | Industry, News Feed

Goby Homes officially launched its flagship product designed to center transaction management around better communications and transparency.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Real estate software startup Goby Homes has formally launched its flagship real estate software solution, a product “designed to improve the transparency, document management and security of residential real estate transactions,” according to a June 4 statement.

Augmenting the company’s announcement is the National Association of Realtors naming founder Terrence Nickelson as the recipient of its iOi Innovator of the Year Award. This year’s award will be presented at the 2025 Realtors Legislative Meetings, taking place May 31 through June 5 in Washington, D.C.

Previous iOi Innovator awardees include Pritesh Damani, chief technology officer at The Real Brokerage; Inés Hegedus-García, managing partner at Avanti Way Realty; and Kathleen Lappe, CEO of DirectOffer.

“Receiving the Innovator of the Year award is a tremendous honor,” Nickelson said. “It reinforces my belief that while technology plays a crucial role in streamlining processes, in the real estate industry, particularly when dealing with our clients’ most significant investments, there’s truly no such thing as a completely ‘end-to-end’ platform driven solely by artificial intelligence.”

Inspiring the creation of Goby Homes is the pace at which real estate deals fall through before closing. While the reasons are many, increased transparency and more multi-party collaboration on how to address common transaction challenges can only help. The company summarizes its value proposition as “introducing alignment, visibility, and structured collaboration to every transaction.”

“Despite countless tools available, transactions still fall apart because key information gets missed, roles and responsibilities are unclear, and real-time transparency is almost nonexistent,” Nickelson said. “Without a shared source of accountability, confusion builds, leading to friction, a poor client experience, and ultimately, fallout.”

Nearly 760 home sales collapse every day, totaling a quarter of a million per year, according to Goby Homes. Redfin reported in May that “Roughly 56,000 U.S. home-purchase agreements were canceled in April, equal to 14.3 percent of homes that went under contract that month.”

Additionally, Goby Homes has found that digital security remains a major risk throughout the lifecycle of a common home sale, due in part to fragmented communications spanning email, text and other transaction systems. While wire fraud is always a risk, so is long-term data risk and the spilling of personal financial information into the coffers of bad actors.

The product’s centralization of all transaction information can help alleviate security risks by ensuring a single, secure hub is the only landing spot for deal point documents, terms and workflow.

In addition to NAR’s recognition, the National Fair Housing Alliance (NFHA) presented Nickelson the “Innovation Impact Award” at the 2025 Responsible AI Symposium. He was also a panelist at Inman Connect Miami, on stage for a session entitled, “Built for Real Estate: Tech Solutions That Deliver Results.”

Goby Homes is a member of the second cohort of fledgling companies being supported by Equity Angels, a woman-founded and -led organization focused on equitable access to financial and entrepreneurial resources. A member of its first cohort, Upfront, recently acquired MoxiWorks’ backoffice product, MoxiBalance. It will be rebranded as Vero.

Email Craig Rowe

by Andrea V. Brambila | Jun 3, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

As soon as Wednesday, June 4, the National Association of Realtors may vote to rescind its controversial “no-commingling” policy, which currently allows multiple listing services to prohibit brokers from displaying listings from MLSs together with those from non-MLS sources.

NAR’s Multiple Listing Issues and Policies Committee voted on Tuesday to rescind the policy, formally known as “the no-commingling rule,” at the trade organization’s annual midyear conference, the Realtors Legislative Meetings, in Washington, D.C.

The rule is currently under scrutiny from the U.S. Department of Justice (DOJ) and was the subject of an antitrust lawsuit brought against NAR and Zillow by now-defunct real estate brokerage REX. NAR and Zillow prevailed in that case, in part because the rule is optional, not mandatory. According to legal filings in that case, 29 percent of Realtor-affiliated MLSs have chosen not to adopt the rule.

NAR’s MLS Technology and Emerging Issues Advisory Board, which is part of the committee, put forward the recommendation to revoke the policy to the full committee Tuesday afternoon.

“Rescission of these optional model MLS rules and the corresponding policy language is in response to requests for its removal due to its outdated application under current marketing strategies and diminished benefits,” the advisory board’s rationale for the change reads.

The committee voted to eliminate the policy without any discussion, and it was the only proposal the committee voted on, committee members and attendees told Inman after the meeting. Panelists also reportedly did not take questions, and audience mics were turned off.

The MLIP Committee meeting was closed to the press this year for the first time in at least 13 years, if not for the first time ever.

“The meeting was an internal NAR member event, and it was decided that it should be closed,” NAR spokesperson Tori Syrek told Inman in a statement.

Inman has asked NAR whether the meeting was therefore live-streamed so that non-attendee NAR members would have access to the event. Inman also asked why the meeting was not therefore labeled “NAR members only” and therefore left open to non-member attendees, such as vendors. Inman will update this story if and when responses are received.

NAR’s Executive Committee will vote on the rescission tomorrow, and it will become final if approved. Due to NAR’s governance changes, if the Executive Committee approves the change, it does not need to go to the NAR board of directors.

Matt Consalvo, CEO of Arizona Regional MLS and a member of the committee, told Inman he doesn’t like NAR’s optional rules and believes removing the no-commingling rule provides brokers with greater clarity. ARMLS never adopted the rule.

“When brokers operate in multiple MLSs and there are the optional rules, it confuses them because one MLS may adopt something and another MLS may not,” Consalvo said.

Asked what happened in the rest of the meeting, Consalvo said NAR Senior Counsel Charlie Lee had given “a great presentation,” making sure everyone had a common understanding of Internet Data Exchange (IDX) and Virtual Office Website (VOW) policies.

There was also a discussion about the new Multiple Listing Options for Sellers (MLOS) policy, though the attendees Inman spoke to said they did not hear anything new.

“Nothing in it was enlightening for myself,” Consalvo said.

According to Consalvo, ARMLS’s Coming Soon status “checks all the boxes” of the new policy. ARMLS added it in 2020 in response to the passage of NAR’s Clear Cooperation Policy, which requires listing brokers to submit listings to Realtor-affiliated MLSs within one business day of publicly marketing them.

“We saw what needed to happen for choices for brokers to be able to comply … and we put a very robust Coming Soon in that is exactly the intent of what that policy is,” Consalvo said.

“So we have no change needed.”

Listings can stay in that status for 30 days, it allows for showings and offers, and listings aren’t distributed across the internet until they’re ready to be active, “but all the agents know about it and the agents can grab the listing and share with their clients freely,” he added.

Here is the policy language set to be eliminated:

Section 18.3.11

Listings obtained through IDX feeds from REALTOR® Association MLSs where the MLS participant holds participatory rights must be displayed separately from listings obtained from other sources. Listings obtained from other sources (e.g., from other MLSs, from non-participating brokers, etc.) must display the source from which each such listing was obtained.* (Amended 05/17) O

Note: An MLS participant (or where permitted locally, an MLS subscriber) may co-mingle the listings of other brokers received in an IDX feed with listings available from other MLS IDX feeds, provided all such displays are consistent with the IDX rules, and the MLS participant (or MLS subscriber) holds participatory rights in those MLSs. As used in this policy, “co-mingling” means that consumers are able to execute a single property search of multiple IDX data feeds resulting in the display of IDX information from each of the MLSs on a single search results page; and that participants may display listings from each IDX feed on a single webpage or display. (Adopted 11/14)

Section 19.23

A Participant shall cause any listing displayed on his or her VOW obtained from other sources, including form another MLS or from a broker not participating in the MLS, to be searched separately from listing in the MLS.

Editor’s note: This story has been updated with a comment from NAR, as well as additional questions from Inman that NAR has not yet responded to.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

by Andrea V. Brambila | Jun 3, 2025 | Industry, News Feed

NAR’s Professional Standards Committee on Tuesday moved to make the Realtor Code of Ethics applicable only to real estate-related activities. The board of directors will take a vote on Thursday.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Following hours of passionate debate, proposed changes to the National Association of Realtors’ hate speech policy went forward largely unchanged Tuesday morning and now head to the trade group’s board of directors.

At its meeting on Tuesday, NAR’s Professional Standards Committee approved the changes to the Realtor Code of Ethics’ Standard of Practice 10-5, which currently prohibits Realtors from using “harassing speech, hate speech, epithets, or slurs based on race, color, religion, sex, disability, familial status, national origin, sexual orientation or gender identity.”

The policy, which was approved in 2020, currently applies to all of a Realtor’s activities, not just those related to real estate. A Realtor who violates the policy is charged under Article 10 of the Code of Ethics, which prohibits denying equal professional services to anyone in those protected classes.

At the meeting, which took place at NAR’s midyear conference, the Realtors Legislative Meetings, the committee voted to amend SOP 10-5 so that it reads:

“Realtors, in their capacity as real estate professionals, in association with their real estate businesses, or in their real estate-related activities, shall not harass any person or persons based on race, color, religion, sex, disability, familial status, national origin, sexual orientation, or gender identity.

As used in this Code of Ethics, harassment is unwelcome behavior directed at an individual or group based on one or more of the above protected characteristics where the purpose or effect of the behavior is to create a hostile, abusive, intimidating environment which adversely affects their ability to access equal professional services or employment opportunity.”

The amendment removes the language referencing “harassing speech, hate speech, epithets, or slurs” and adds a definition of harassment that NAR says aligns with its Member Code of Conduct.

The committee also voted to amend Policy Statement 29 to change the Code of Ethics’ applicability so that Realtors would be encouraged, but not required, to follow the code “in all of their activities.” That amendment reads:

“While Realtors are encouraged to follow the principles of the Code of Ethics in all of their activities, a Realtor shall be subject to disciplinary action under the Code of Ethics only with respect to their capacity as real state professionals, in association with their real estate businesses, or in their real estate-related activities.”

The NAR board of directors will vote on the proposed changes at its meeting on Thurs. June 5.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

by Richelle Hammiel | Jun 3, 2025 | Industry, News Feed

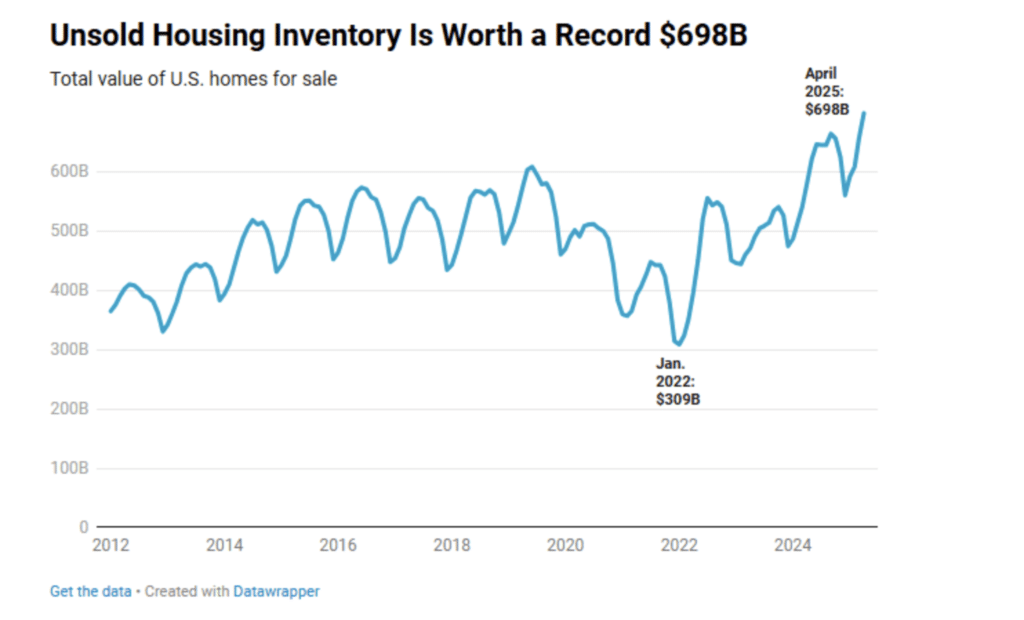

U.S. home inventory hit a record $698 billion in April, a 20.3 percent increase from the previous year. However, sales aren’t keeping pace, a new analysis from Redfin shows. While listings are rising, buyer activity remains muted, leaving many homes sitting unsold far longer than usual.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

U.S. home inventory hit a record $698 billion in April — a 20.3 percent increase from the previous year — but sales aren’t keeping pace, a new analysis from Redfin shows.

While listings are rising, buyer activity remains muted, leaving many homes sitting unsold far longer than usual.

Redfin | Unsold Housing Inventory

In April alone, total listings jumped 16.7 percent year over year, the highest level in five years, while new listings rose 8.6 percent, hitting a three-year high, yet buyers haven’t followed. Redfin reports there are now nearly 500,000 more sellers than buyers nationwide.

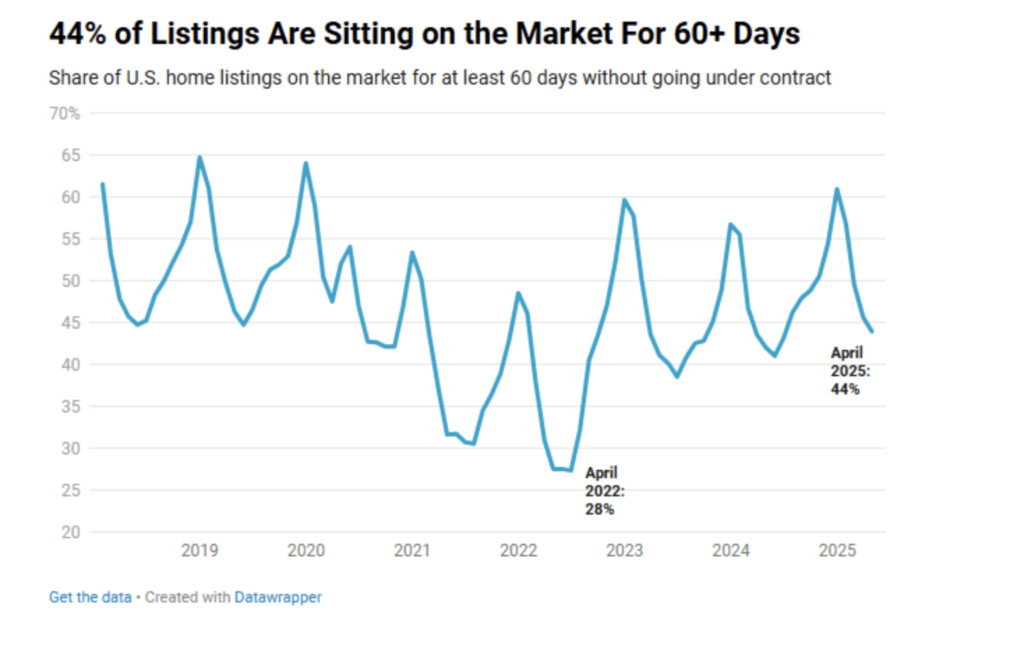

Homes are lingering on the market and getting stale. The typical home took 40 days to go under contract in April — five days longer than last year. More than 44 percent of listings were on the market for 60 days or more. That stale inventory alone accounts for $331 billion, nearly half the total market value.

Redfin

Chen Zhao | Redfin’s Head of Economics Research

“The record-high dollar value of all homes listed for sale is one way to quantify this buyer’s market,” Chen Zhao, Redfin’s head of economics research, said in Redfin’s analysis. “Not only are there more homes for sale than there have been in five years, but the value of those homes is higher than it has ever been.”

Contributing to this slowdown are record-high monthly housing costs, economic uncertainty and rising home-sale prices. The median U.S. home-sale price in April was up 1.4 percent from the previous year, but many sellers are now willing to negotiate.

“A huge pop of listings hit the market at the start of spring, and there weren’t enough buyers to go around,” Matt Purdy, a Redfin Premier agent in Denver, said. “House hunters are only buying if they absolutely have to, and even serious buyers are backing out of contracts more than they used to. Buyers have a window to get a deal; there’s still a surplus of inventory on the market, with sellers facing reality and willing to negotiate prices down.”

Matt Purdy | Redfin Premier Agent

In stark contrast to today’s slower market, inventory in early 2022 bottomed out at $309 billion. Mortgage rates hovered around 3 percent, and homes sold in a median of just 24 days. Now, with rates near 7 percent and affordability stretched thin, the stockpile of unsold homes keeps growing.

Zhao says there may be a silver lining for buyers as incomes continue to increase.

“We expect rising inventory, weakened demand, and the prevalence of stale supply to push home prices down 1 percent by the end of this year, which should improve affordability for buyers because incomes are still going up,” she said.

Email Richelle Hammiel