by Daniel Houston | Jun 21, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

To help figure out where the industry is heading next, Inman invites you to take real estate’s most ambitious monthly survey: the Inman Intel Index.

Each month, the Intel Index survey leans on the expertise of Inman’s readership to discover what’s top of mind for agents, mortgage professionals, proptech players and industry executives.

TAKE THE INMAN INTEL INDEX SURVEY

The insights gathered from these responses help illuminate industry sentiment on real estate’s most important topics: the NAR settlement, inventory opportunities, new U.S. tariff policy and its impact on real estate, and more.

Click through to add your insights to the industry’s knowledge base, and check back for analysis of the results in the weeks to come.

Thank you,

Team Inman

by Darryl Davis | Jun 21, 2025 | Industry, News Feed

Are your clients “waiting for the market to recover”? They’re often talking about fear and uncertainty, coach Darryl Davis writes. Ask these questions to shift from uncertainty to clarity.

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Let’s talk about one of the most common phrases I hear from agents lately: “My clients say they’re going to wait until the market recovers.”

Sound familiar?

It’s an easy thing for buyers or sellers to say. But let’s pull the curtain back a little — because when someone says, “We’re waiting for the market to get better,” they’re often not talking about real estate at all. They’re talking about fear. About uncertainty. About wanting guarantees in a world that’s anything but predictable.

The problem is, they’re trying to drive with one foot on the gas and one on the brake.

And your job? It’s not just about selling homes — it’s about helping people get unstuck.

‘We’re waiting for the market to recover’

But what does that even mean?

This came up in a coaching call recently. I said, “Recover from what? A bad breakup? The sniffles?” We all laughed, but the truth underneath that joke is important: Recovery is vague — and vagueness keeps people stalled.

Is your client waiting for rates to drop? Prices to rise? Inflation to ease? Political changes? A cosmic sign?

It’s like standing on the shore, waiting for the “perfect wave,” but the tide keeps shifting. If you wait too long, the opportunity passes.

That’s why one of the best things you can do in these moments is ask a question that shifts the conversation from external uncertainty to internal clarity.

Flip the focus: From market conditions to life decisions

Try this with a client:

“Are you committed to waiting for interest rates, or are you committed to making the move that supports your life goals?”

That one question changes everything.

It’s like switching the lens from a telescope (always scanning the horizon) to a mirror (what do I want?). It gets people out of waiting mode and into decision mode.

For a buyer renting or living with family:

“Are you committed to renting for another year, or are you ready to step into the next chapter of your life as a homeowner?”

You’re not pressuring. You’re coaching. You’re helping them reconnect with what they can control — their decisions, not the market’s whims.

Because here’s the truth …

The market will shift. Rates will rise and fall. Inventory will tighten and loosen. That’s the nature of the business.

But if your clients are waiting for all the stars to align before they act, they’ll be standing still while others move forward.

Imagine someone sitting in a car, engine running, GPS ready, but refusing to hit the road until every light on the highway turns green. It’s not realistic, and it’s not necessary.

You serve the committed

Let me be clear: Not everyone is ready to move. And that’s OK.

Some sellers will say, “If I get my price, I’ll sell,” but deep down, they’re just testing the waters. There’s no urgency, no vision, no commitment. You can’t coach someone who isn’t ready to play.

You serve the ones who are ready to take that next step, even when it feels a little uncomfortable.

Your role is to help them move from Point A to Point B, not just physically, but emotionally and mentally. And that means bringing empathy, clarity and courage to the table.

Try these conversation starters:

When someone says, “We’re waiting for the market to improve,” try asking:

- “What would ‘recovered’ look like for you?”

- “How will you know when it’s the right time?”

- “What’s more important to you — external timing or personal progress?”

- “What would moving now make possible in your life?”

We teach agents to lead conversations, not chase them. To guide with heart. To stop selling and start serving.

Because at the end of the day, this business isn’t just about keys and contracts; it’s about people and possibilities.

And if you’re reading this thinking, “Yes, but I’m feeling the weight too,” let me say this: You’re not alone. These are challenging times. But they’re also full of opportunity, especially for agents who know how to help clients cut through the noise and make decisions that serve their future.

You’re not just in real estate. You’re in the business of transformation. Keep leading with questions. Keep listening. And keep helping people move forward — one thoughtful conversation at a time.

Darryl Davis is the CEO of Darryl Davis Seminars. Connect with him on Facebook or YouTube.

by Taylor Anderson | Jun 20, 2025 | Industry, News Feed

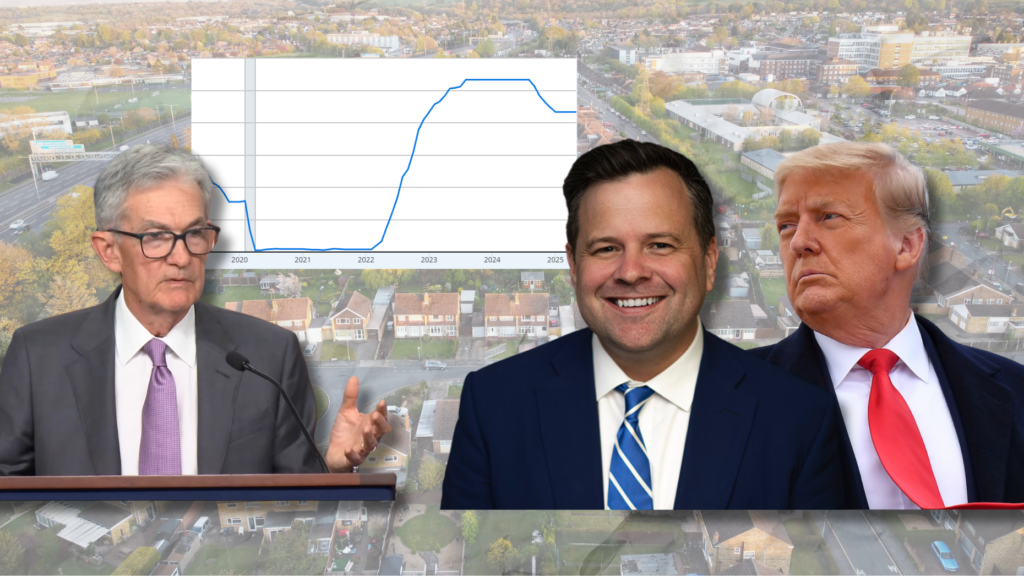

The chair of the Federal Housing Finance Agency, Fannie and Freddie has spent the past day calling on Powell to step down, saying he’s responsible for high home prices.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools, and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The chair of the Federal Housing Finance Agency (FHFA) is in an outright war against Jerome Powell, chair of the Federal Reserve, saying he is responsible for housing unaffordability and demanding that he resign.

Bill Pulte took to the social media platform X as well as national cable TV to call for Powell’s resignation in the days after the Federal Reserve opted to hold rates steady — a decision it made earlier this week. Pulte blamed Powell for keeping interest rates high.

“Jerome Powell is a main reason for the Housing Supply Crisis in this Country,” Pulte wrote Thursday in one of several X posts on the topic. “By improperly keeping interest rates high, Jerome Powell is trapping homeowners in low-rate mortgages and choking off existing home sale — directly fueling the housing supply crisis. He must lower rates.”

Pulte and President Donald Trump have both been putting pressure on Powell — who was appointed to the chair position in 2018 during Trump’s first term in office — to lower the federal funds rate. The federal funds rate can indirectly impact mortgage rates, automobile loans and credit card rates.

Powell’s term ends in May 2026. Pulte took to Fox News to spread his message on Friday morning, saying that Powell should either lower rates before the end of his term or resign.

“Peoples’ mortgage affordability has been crushed in the last four years,” Pulte said. “People have to pay double what they had to pay compared to President Trump’s first term in order to buy a home.”

Pulte said that Powell was “one of if not the biggest reason for the housing supply crisis that we have in this country.”

“It’s hurting Americans right now. Nobody wants to sell their existing homes,” he said. We need to get that inventory churning in this country again.”

Pulte didn’t answer when asked if he had heard from Powell since calling for his resignation.

Trump took to his Truth Social platform to share Pulte’s message.

“Too Late—Powell is the WORST. A real dummy, who’s costing America $Billion!” Trump wrote. In a separate message he wrote that the federal funds rate should be 2.5 points lower than it is.

The Federal Reserve began quickly raising the federal funds rate in March 2022 to combat high inflation and an overheated labor market. It stopped raising the rate in August 2023 and implemented a brief series of cuts in September 2024 but has not cut them since Trump’s second inauguration.

The board has continued to express caution, saying it was waiting to see the impact of Trump’s tariff policy before moving to lower rates.

Powell said this week that he expects a “meaningful amount of inflation” to arrive in the coming months.

“We have to take that into account,” Powell said.

“Increases in tariffs this year are likely to push up prices and weigh on economic activity,” Powell said. “The effects on inflation could be short-lived, reflecting a one-time shift in the price level. It’s also possible that the inflationary effects could be more persistent.”

Email Taylor Anderson

by Dani Vanderboegh | Jun 20, 2025 | Industry, News Feed

Turn up the volume on your real estate success at Inman On Tour: Nashville! Connect with industry trailblazers and top-tier speakers to gain powerful insights, cutting-edge strategies, and invaluable connections. Elevate your business and achieve your boldest goals — all with Music City magic. Register now.

Every Friday, Inman Service Editor Dani Vanderboegh rounds up the most popular, most read, most critical stories of the week to give you a quick catchup on the big headlines you might have missed in the hustle and bustle of the workweek. Here’s this week’s Top 5 as chosen by our readers.

P.S. Don’t miss The Download, our weekly column that breaks down one of the week’s top stories and equips you with what you’ll need to meet next Monday head-on.

The daily habits of top agents allow them to separate themselves from the competition, so they can thrive in any market, Real’s Jimmy Burgess writes.

Anthony Lamacchia

Ahead of Inman Connect San Diego in July, Lamacchia revealed what he said at Trump’s West Palm Beach golf club this year that drew the president’s ire. “He was not happy to hear it,” he told Inman.

Master the power and potential of artificial intelligence, and you’ll position yourself for success in the years to come, trainer Terry LeClair writes.

AJ Canaria of PlanOmatic

The real estate brokerages want to pause a commission case known as Gibson while they wrap up a different lawsuit. But the Gibson homeseller plaintiffs don’t want their case put on ice.

Rawpixel/Unsplash

“All low-commission brokers employ at least some competent, experienced agents,” but sellers should comparison shop, according to a new analysis by advocacy group Consumer Policy Center.

Email Editorial

by Lindsey Harn | Jun 20, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools, and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The luxury real estate market is changing, and it’s all about who’s buying and what they’re looking for. Baby boomers (ages 60–78) are dominating the housing market, making up 42 percent of buyers and 53 percent of sellers.

This is a massive shift from millennials, who now only account for 29 percent of buyers (a record low). Boomers are in a strong position to buy, often without financing, thanks to the equity they’ve built up in their homes, and about half of boomers are purchasing homes in cash.

The average age of first-time buyers is now 38, and their share of the market has dropped to just 24 percent. While many younger buyers are delaying homeownership due to financial trouble, their influence is not unseen; in-law suites and properties that offer flexible spaces are becoming in demand, accommodating multigenerational living.

Even though they’re waiting longer to buy, many have built up substantial savings or secured high-paying remote tech jobs. These younger generations are now entering the market with the ability to invest in more luxury homes.

To them, luxury doesn’t just mean big square footage and fancy finishes; it’s all about smart technology, sustainability, and versatile living spaces. Features like accessory dwelling units (ADUs), home office sheds and energy-efficient systems are now highly sought after. These buyers aren’t just purchasing homes but changing the very definition of what luxury means.

Tech-savvy buyers are redefining luxury

We are seeing tech-savvy buyers, specifically younger ones from Asia and the Middle East, who have built wealth through the tech industry and startups, and are now bringing that innovation mindset to the real estate market. These buyers are looking for the latest in smart home technology.

Smart homes are no longer a neat, futuristic idea; they’re a necessity. Security systems, climate control, automated lighting and voice-activated assistants are now basic features buyers expect.

In fact, 44 percent of Americans looking for move-in-ready homes say smart home technology is non-negotiable, and it’s no surprise that 61 percent of millennials feel the same way. So, if you’re looking to attract today’s luxury buyers, you’d better be ready to embrace the latest in home tech.

Since the pandemic, technology has been increasingly influencing the luxury real estate landscape. Buyers are prioritizing homes that offer privacy, space and luxury amenities, such as home offices and health-focused features (like a standing desk or cold plunge). As remote work continues to grow in popularity, the need for a home that suits this lifestyle also increases.

Sustainability in luxury living

Sustainability is becoming the new expectation in luxury real estate. Buyers are now seeking eco-friendly homes that align with their values, and developers are beginning to take notice of this trend. Sustainable living is revolutionizing the design and marketing of luxury properties, proving that “green living” is no longer a niche but a mainstream trend.

Remote work redefines luxury

Remote work has fully renovated the way people think about home design. Almost 14 percent of the entire U.S. workforce, approximately 22 million people, are now working fully remote, and most people prefer to work from home at least part-time. The more time people spend in their house, the more they want their house to have all the new perks and look great.

This change has created a boost in demand for homes that are ideal for both living and working. Buyers now seek spacious offices, high-speed internet infrastructure and wellness-focused amenities, such as home gyms and spas.

New features are being introduced into luxury homes, including circadian lighting systems, soundproof rooms, and purified air systems. Buyers are increasingly seeking spaces that promote health, productivity and overall well-being, while also offering the comfort and luxury they expect. This shift is one of the key factors reshaping the luxury market, with more emphasis on functionality alongside opulence.

The luxury real estate market is evolving

With younger generations seeking out homes that reflect their tech-savvy, sustainable and wellness-oriented lifestyles, luxury real estate is becoming more personalized than ever. At the same time, older generations remain a driving force in the market, with a focus on homes that support aging in place and multigenerational living.

This shift is also affecting mid-tier markets, where we’re seeing a rise in prices as wealthy buyers seek to expand beyond major cities. Real estate developers are blurring the lines between luxury and more standard living, introducing high-end design features into more accessible properties. However, while luxury real estate is thriving, this trend also exacerbates the broader housing affordability crisis, making it even more challenging for middle-class buyers to gain a foothold.

As millennials and Gen Z continue to take center stage in luxury homeownership, the industry will have to adapt to meet the needs of these buyers, who demand more from their homes than just luxury; they want spaces that align with their values, needs and ambitions.

With remote work becoming a permanent fixture and sustainability at the forefront, the future of luxury real estate is exciting, and we can expect to see tremendous growth in demand in the coming years.

Lindsey Harn is an agent with Christie’s International Real Estate Sereno and a certified Divorce Real Estate Expert. Connect with her on Instagram and LinkedIn.

by Jimmy Burgess | Jun 20, 2025 | Industry, News Feed

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Every agent dreams of building a business that has a consistent flow of referrals. Not just because it reduces marketing spend or shortens sales cycles, but because it’s a business built on trust, service and long-term relationships. The best agents I know, the ones who weather every shift in the market, have one thing in common: Their business is powered by referrals.

This article outlines seven strategies to help you build your own referral machine. These are timeless, proven approaches that agents across the country are using right now to create businesses that grow regardless of market conditions.

1. Create a digital referral farm

You’ve heard of geographical farming. But what about farming agents in other markets?

Start by building an email list of real estate agents from outside your area. These are people you’ve met at conferences, connected with on social media or worked with on deals in the past. This collection of individuals is your “digital farm,” and it’s one of the most overlooked yet powerful referral strategies.

At least once a month, send an email that adds real value to these agents. Share something that helped your business, like a script that worked, a marketing strategy you implemented, or templates for high-converting direct mail campaigns. It’s even more personal and impactful if you include a short video walking them through the tip you’re sharing.

Sign off each email with something like:

“This is your friend in real estate in [Your City]. Thanks in advance for keeping me in mind if someone is moving to the area.”

The key is consistency. Lead with value. Ask them to forward your emails to other agents and to let you know if they want to be added to the list. Over time, this positions you as the go-to referral partner in your market.

2. Create an MVP list for referrals

Just like you’d farm a neighborhood, you need to cultivate your most valuable relationships. These are your MVPs. These are past clients and sphere contacts most likely to send you referrals.

Create a list of 25, 50 or 100 people. Then, focus on showing up intentionally in their lives. Don’t just “check in.” Engage with their lives. DM them to congratulate them on life events. Comment meaningfully on their social media posts. Notice them, celebrate them, and let them know you care.

The goal is to remain top-of-mind. This isn’t achieved through constantly asking them for referrals, but through authentic connection. This builds goodwill and ensures that when the opportunity for a referral arises, you’ll be the name they recommend.

3. Build relationships with former agents

The past few years have pushed many agents out of the business. Some went part-time; others left entirely. These individuals still have contacts, relationships and influence, and they’re often open to earning referral fees.

Reach out to former agents, and show them how to keep their license active in a referral-only capacity. If your brokerage offers a referral company, explain how it works and how they can earn passive income by sending business your way.

Reassure them that you’ll treat their referrals like family and that you’ll keep them in the loop. When they see a path to stay connected to the industry and be compensated for their past efforts, many will jump at the opportunity, and you’ll gain a new referral source.

4. Post with purpose

Want to generate organic referrals on social media? Start posting with a clear purpose.

Instead of just posting closings, share “little help” posts — specific buyer needs or sneak peeks of upcoming listings.

For example:

“I’m working with a couple moving to [your city] looking for a 3-bed, 2-bath in [neighborhood] under $600K. If you know someone who’s been thinking about selling, please share this or DM me.”

These posts tap into the law of reciprocity. People want to help. They’ll tag friends, DM you, and engage with the post. That interaction puts your content in their feed more often, expanding your reach.

5. Focus on feeder markets

Where are the buyers for your area relocating from? These are called feeder markets, meaning the other city feeds a steady stream of buyers to your market. Identify where your buyers are coming from, then build a referral strategy to tap into those markets.

Send handwritten notes to top agents in those cities. Include something simple like:

“I love paying referral fees for buyers moving to (Your City).”

You can increase the likelihood of referrals from specific agents in feeder markets by:

- Following agents in those markets on social media

- Commenting consistently on their content

- Adding them to your digital farm email list

When those agents have clients relocating to your area, you’ll be their go-to local expert.

6. Tell referral stories publicly

Every time you receive a referral, tell the story on social media. Here are a few ideas on how to share these stories publicly:

- Thank the referring agent on social media

- Explain the referral process and your system for keeping agents updated on social media

- Share the story of helping a referral you received, and thank the referring agent in the story

When agents see you making other agents’ clients happy and they see you publicly thanking the referring agent, they’re more likely to send you a referral when the opportunity arises for them. Sharing these stories publicly builds your reputation and shows how easy you make the referral process.

7. Reward referring agents generously

Finally, show appreciation to the agents who trust you with their clients. A 30 percent referral fee instead of the usual 25 percent speaks volumes. A thoughtful thank-you gift or handwritten note after closing leaves a lasting impression.

Treat them like you treat your best clients. Show them you value their partnership and want more of it.

If you want more referrals, start by giving more value. Give ideas, resources, recognition and gratitude. Build relationships with agents and clients alike. Create systems that make it easy for others to send you business and reward them when they do.

A referral-based business isn’t built overnight — but it’s built to last. And when done right, it becomes the foundation of a business that thrives in any market.

Jimmy Burgess is the Chief Coaching Officer for HomeServices of America and Berkshire Hathaway HomeServices. Connect with him on Instagram and LinkedIn.