Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Let’s be honest — few things deflate a listing appointment faster than hearing: “Well, another agent said we could get $100,000 more.”

Cue the crickets.

Or how about this one: “Maybe we’ll just go with the agent we used last time.”

That can feel like a double punch to the confidence if you’re not ready for it. But here’s the good news: Objections aren’t rejection. They’re just requests for more information. And when handled right, they’re the gateway to winning trust — and the listing.

Let’s break down two of the most common objections sellers throw our way and how to handle them like a seasoned pro.

Objection No. 1: ‘Another agent told me I could get more money’

Classic, right? A homeowner hears a big shiny number and starts mentally spending that imaginary money. Suddenly, you’re the bad guy for bringing them back down to earth.

Here’s how I coach my agents to handle it: Stop saying, “This is what your home is worth.” That opens the door for opinion-based ping-pong.

Instead, shift your language to:

“This is what your home will likely appraise for.”

Why that distinction matters: When you say worth, it feels personal. Subjective. Open for negotiation. But appraisal? That brings the bank into the conversation. And nobody argues with the bank — not even your cousin Sal, who still thinks Bitcoin’s coming back.

Ask the seller to imagine they are the appraiser. Three similar homes in the area sold for $500,000, $515,000, and $525,000. Which number are they going to pick to protect the bank’s interest? Probably the lowest. Not because they’re cheap, but because they’re covering their assets — literally.

Remind them: The bank isn’t just loaning money — they’re investing in the property. And after 2008? Let’s just say banks got real cozy with caution. So, no matter which agent they hire, the home still has to pass the appraisal test.

I like to lighten the mood by saying:

“I’d love to be wrong — if it sells for $100,000 more, that’s more commission for me!”

That kind of transparency builds trust. You’re not chasing a paycheck — you’re preparing them for reality. And that’s exactly what they want: a straight shooter.

Objection No. 2: ‘We’ll just use the agent we had last time’

Sometimes this sounds like loyalty — but more often, it’s about comfort and assumed advantage. The sellers might figure, “We’ve worked with them before … they know us … they’ll probably cut us a deal or work harder to get us top dollar.”

But here’s the reality: Just because you know an agent doesn’t mean their strategy is right for this market — or for your goals.

Try something like this:

“If you had a great experience last time, that’s awesome. But even great agents can get too comfortable using the same approach. My job is to give you a pricing strategy that works in today’s market — and get your home sold at a price the bank will support, not just what sounds good on paper.”

Then bring it back to the facts:

“At the end of the day, no matter who you hire, the home still has to appraise. No agent — no matter how friendly or familiar — can change that.”

And if you want to sprinkle in a little humor?

“If I could promise $100,000 over asking just for being nice, I’d be out here hugging every homeowner in town.”

That line usually gets a laugh — and diffuses any lingering tension.

The goal isn’t to bash the other agent. It’s to position yourself as the one with the most relevant, up-to-date, and bank-backed strategy. The relationship might earn the old agent a seat at the table — but it’s pricing smarts that earn the paycheck.

Presenting a strategy that works

Try this: Present a pricing range instead of a fixed number. Give them the high and low ends of what similar homes are selling for, and explain:

“We can test the higher end if you’d like — but I want to make sure we don’t scare off qualified buyers or risk losing the deal in appraisal.”

Let them make the final call. After all, it’s their home. Your job is to educate and guide, not arm-wrestle.

Here’s how you win the listing

When a seller says, “We’re thinking of listing with someone else,” don’t panic. Pivot. Use it as a chance to prove your value.

Here’s the game plan:

Reframe the pricing convo around appraisal, not opinion

Teach them how banks determine value

Use a pricing range to give them control

Position yourself as a marketer, not a price-guesser

Stay calm, stay clear, and stay kind

At the end of the day, sellers aren’t looking for the slickest pitch or the biggest promise. They’re looking for someone who will tell them the truth, guide them through the process, and help them make informed decisions without the salesy pressure.

And when you can do that with confidence, clarity and a little humor? You don’t just win listings. You win clients for life.

Broker and lead gen consultant Josh Ries shares strategies for demonstrating to sellers how your tech tools will get the results they’re looking for.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

When I first got into real estate, my listing presentations were rough. I’m a tech nerd, obsessed with data and systems, so I’d spend the entire appointment talking about all the tools I used to market properties.

CRM automations, email sequencing, targeted ads — I thought it was impressive. But here’s the truth I learned the hard way: Sellers don’t care how slick your systems are. They care about what those systems do for them.

And more importantly, they care about seeing those results before they even hire you.

Your tech stack isn’t the selling point. Execution is

What sellers want is implementation, not explanation.

You can talk about CRMs and ad platforms all day, but it doesn’t land unless you connect it to an outcome they actually want. Selling their home faster. For more money. With less hassle.

So we stopped talking about the tools and started showing what those tools could do. Before the listing appointment even happens.

How we get sellers noticing our marketing before we even meet

Here’s how we changed our process.

As soon as a seller books a listing appointment with us, we send them a link to a custom landing page. The page is framed as a quick survey about their home — basic stuff like number of bedrooms, condition, timing and so on.

What they don’t realize is that the page also has a Google conversion tag embedded in it.

So the moment they open the link, whether it’s on their phone or laptop, they get added to a custom audience inside our Google Ads account.

That means the next time they go online, they start seeing our branding across the web.

And it works.

Turning the tables during the appointment

By the time we sit down for the actual listing appointment, the marketing has already started doing the heavy lifting.

One of the first questions we ask is, “Have you seen any of our ads since we booked this appointment?”

Most of the time, the answer is yes.

That’s when we let them in on the secret.

“Remember that page we sent you? That had a Google conversion tag built in. So when you filled it out, we were able to start showing you ads across the internet.”

Suddenly, everything clicks.

We’re not just talking about digital marketing. We’re already demonstrating it in real time.

What if they don’t see the ads?

This system isn’t perfect. Sometimes you don’t have enough time between booking and the appointment. Or the seller is using a privacy-focused browser that blocks ad tracking.

That’s OK. You can still walk them through the process and explain how it works. Even if the ads didn’t hit them, the explanation still builds trust and shows that your marketing has real strategy behind it.

But more often than not, as long as you have a couple of days, the seller does see the ads. And when that happens, the conversation changes.

Why this works so well

This approach does two things.

First, it builds credibility immediately. You’re not just another agent making promises. You’ve already delivered on one.

Second, it shows instead of tells. You’re not asking them to imagine what your systems might do. You’re letting them experience it firsthand.

It’s one thing to say, “We use advanced digital targeting to market your home.”

It’s another to say, “You’ve already seen how we do it — because you’re part of the system.”

Forget the CRM. Prove you know how to use it

Sellers don’t care how impressive your tech is. They care whether it helps them sell their home.

The best way to prove that? Show them.

If you’re using great tools, don’t just explain them. Demonstrate them. Build them into the seller journey before the listing agreement is signed. That’s how you turn systems into signed contracts.

Josh Ries is a real estate broker and a lead generation consultant. You can connect with him on TikTok and Instagram.

The progress came even as competition for listings cooled across the country. Inman breaks down how the industry navigated the spring homebuyer season using insights powered by Market View.

This is a monthly breakdown of national market data powered by Inman Market View. The goal: to put more local data in the hands of the Inman community, and to place it in a context that’s highly relevant for the U.S. brokerage industry.

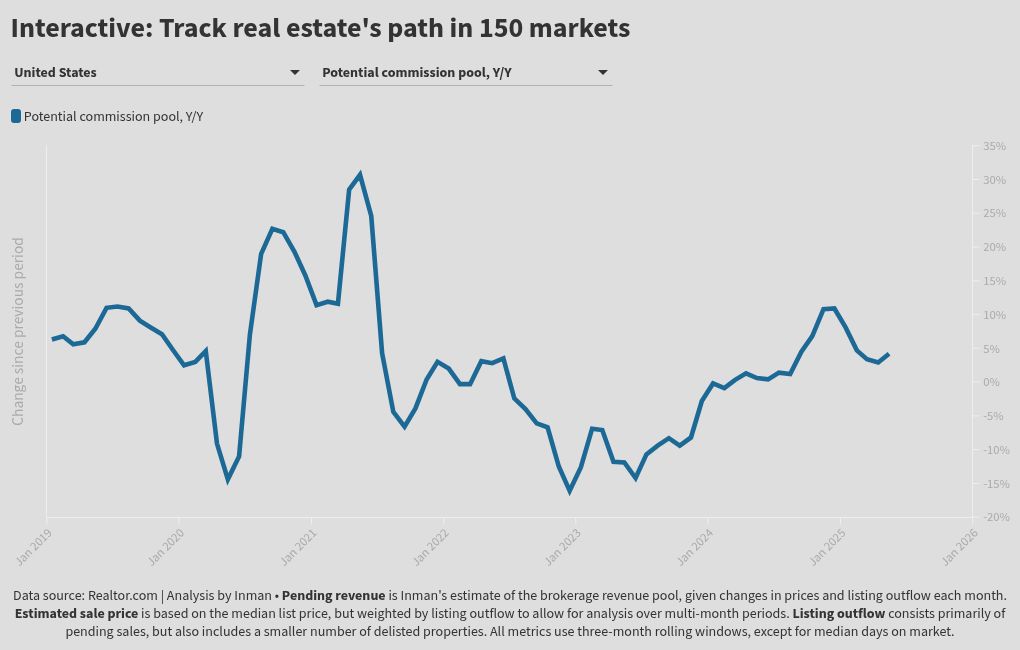

Brokerage revenues made sneaky gains over the past year even as a rising tide of new listings — not a decline in sales — continued to erode the homeseller’s once-intractable negotiating edge.

The pool of potential commissions available to real estate brokerages was 4 percent higher this spring than it was during the same period last year, according to an Inman Market View analysis of listing data from Realtor.com.

These revenue gains were made possible by home prices that were bid up to unprecedented heights in the early pandemic real estate boom, then proved durable even through the subsequent downturn in transactions.

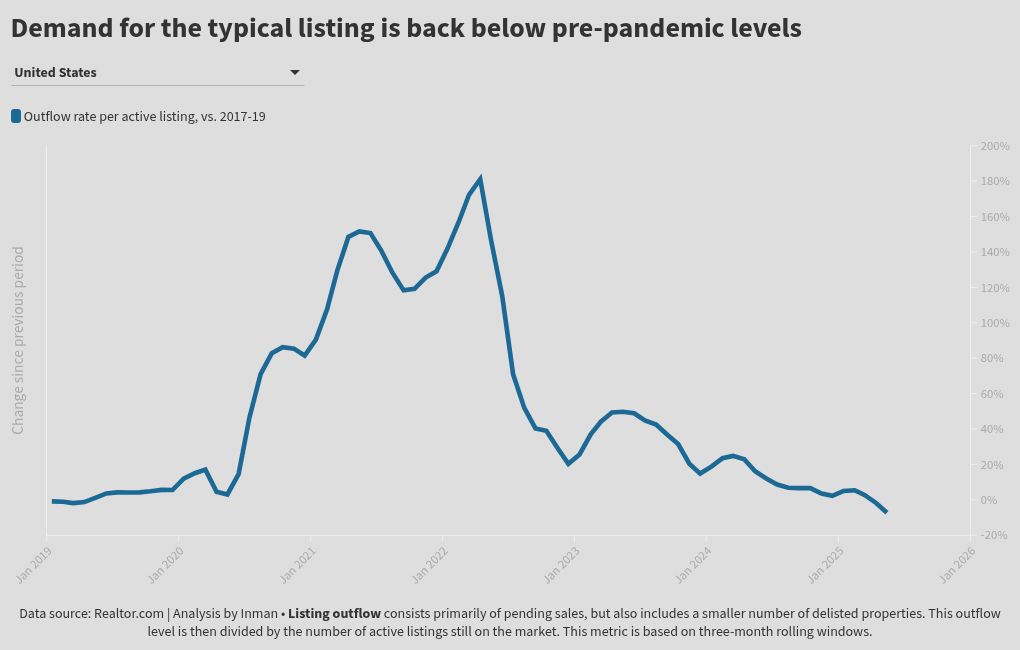

But notably, the spring market, which officially makes way for summer on Friday, also blew past a significant milestone: For the first time, the demand for the typical home listing has dropped below where it was in a typical pre-pandemic spring.

The result? A national environment that is still admittedly seller-friendly, but the least seller-friendly it’s been since well before the pandemic housing era.

And the elevated price levels that have supported agent income for years could become a casualty in many markets as inventory further rebalances.

A healthier path — and a looming risk

To understand where real estate stands right now, it’s essential to place data in context of where it stood before record-low mortgage rates and a pandemic-fueled demand boom completely warped the contours of the market.

But first, let’s take an extra close look at how the business has evolved in the last year alone.

Change in March-May levels, year-over-year

New listings: +9%

Listing outflow: +4%

Weighted list price: +0.1%

Potential commission pool: +4%

We see here the reason behind the buyer-friendly shift in most parts of the country: Not a decline in listing outflow — which is Inman’s proxy for sales activity — but a bump in new listings that outpaced a more modest increase in transactions.

From a brokerage-business perspective, this represents a healthier path through a rebalancing period than what happened in 2022, when the primary driver of the inventory shift was a precipitous drop in home sales.

Still, despite the recent replenishing of inventory, the national market is a far cry from normal.

As every real estate agent is painfully aware, mortgage rates remain elevated far above the rates most homeowners have locked in on their existing loans, and also well above the rate levels that made today’s price levels affordable for buyers.

Zooming out, we see how distorted the market remains compared to what we thought of as “normal” before the pandemic housing boom.

Change in March-May levels, vs. pre-pandemic baseline

Spring 2024 → Spring 2025

New listings: -23% → -16%

Listing outflow: -26% → -23%

Weighted list price: +47% → +48%

Potential commission pool: +10% → +14%

For the most part, price growth during the pandemic has held up even amid the downturn in sales, allowing many brokerages to weather the sales drought.

But it’s worth noting that while the raw value of the commission pool is technically higher than in the spring seasons of 2017-19, consumer-price inflation over that same period has more than offset these nominal gains. This means that in real terms, brokerage earnings are still worth less today than they were six years ago.

And downward pressure on prices may only be beginning.

The level of transaction activity on a typical active listing was 16 percent above pre-pandemic levels in spring of 2024. Even though the market had already substantially rebalanced by this point, this ensured that most markets remained deep seller’s markets.

This spring, the typical listing saw 7 percent less demand than it did pre-pandemic — taking substantial pressure off prices in the process.

As a national matter, the rebalancing toward buyers isn’t complete. After all, we were in a national seller’s market long before the pandemic.

But it does appear to be entering a new era — one where today’s buyers have a noticeably more prominent place at the table.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Want to level up your business? Inman Access offers expert-led tutorials with insights, advice and ideas designed to help you build your skills every day.

Every brand and team is different, but using Vija Williams’ Rules of 3s to evaluate your agents will help you build a recruiting plan and determine what agent productivity systems are needed to hit your business goals.

Elevate your skills and set yourself up for success in 2025. Watch the session above, plus get fresh content added weekly, with Inman Access.

With interactive maps and charts, Inman’s data team helps track the course of 500 local housing markets in this new monthly series.

This is the first installment of Inman Market View, an ongoing monthly data series. The goal: to put more local data in the hands of the Inman community, and to place it in a context that’s highly relevant for the U.S. brokerage industry.

Real estate agents and brokerage leaders are inundated with data each month from dozens of sources.

But that data can often be incomplete, siloed or otherwise difficult to place in a useful context.

That’s why we’re launching Inman Market View, a new interactive project from Inman’s data and news team that seeks to put more local market data directly in the hands of real estate professionals.

This new series aims to allow our Select subscribers to see how their own local market has navigated the treacherous path through a pandemic boom and resultant slowdown, and to compare its path to that of other markets across the country. The tools below utilize listing data from Realtor.com and data wrangling and analysis by the Inman team.

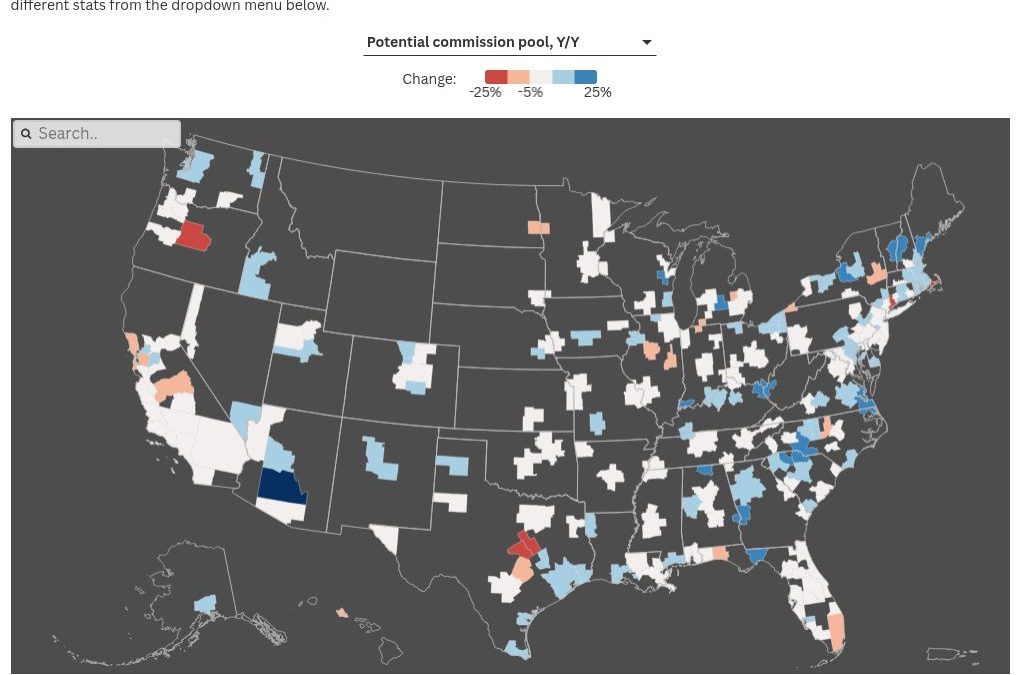

The first result is an interactive map of 500 major metro areas, which together account for nearly 90 percent of the U.S. population.

In the tool below, you can toggle between metrics. Each metric has two views: a “Y/Y” approach that compares the most recent three months’ data to the same period last year; or a “vs. 2017-19” option that compares the same recent three-month period against a 2017-2019 baseline to see how the pandemic era has reshaped different parts of the country.

(For the best experience, view the tool on a desktop browser or in landscape mode in mobile.)

To drill down even deeper into the path each market has taken through the pandemic years, explore the interactive chart tool below.

Use the first dropdown menu to select from any of the nation’s 150 largest housing markets — a collection of metros that contains nearly 75 percent of Americans. Then, use the second dropdown menu to select from the same metrics seen in the map above.

With the tools above, special care has been taken to help account for the occasional noisiness of month-to-month data in small and midsize markets.

By using three-month rolling windows, these tools are able to avoid much of the month-to-month volatility and spot durable trends. And by comparing all recent periods to the same span of time in previous years, the tools account for seasonal patterns in this highly seasonal business.

Each of the metrics above is intended to represent a core concept that Inman tracks on a regular basis. Understand the definitions below to get the most out of the tools.

Metric glossary

Below are the main core concepts that Inman is tracking, and definitions and other notes for each of the metrics.

SUPPLY — New listings

The number of new listings that entered the market in a given month

DEMAND — Listing outflow

The number of properties that left the active-listing pool in a given month, either due to a pending sale or a delisting from the market

This level of listing outflow offsets the number of new listings coming online to explain the total monthly change in the active-listing pool

Note: Delistings are a problematic component of this metric, but cannot be removed due to data limitations. The vast majority of outflowing properties consist of pending sales, and the metric generally tracks closely with sales trends over time. Still, Inman’s listing outflow metric will be less accurate than your local sales data.

INVENTORY SNAPSHOT — Active listings

The total number of active listings on the market that are not marked as “pending” at a given point in time

SPEED OF SALE — Median days on market

The amount of time a typical property sits on the market before it either closes on a sale or is removed from the market

Half of listings spend longer than this on the market, while the other half spend less

Note: This is the only metric in the tools above that is expressed in terms of a single month, instead of a three-month rolling window.

BUYER COMPETITION — Outflow rate per active listing

A market’s listing outflow over a given period, expressed as a share of its active-listing pool at any given time during the same period

This is essentially the inverse of “months supply” — higher outflow rates generally indicate more buyer demand for a typical listing, and higher upward pressure on home prices

PRICE MOVEMENT — Weighted list price

The price level assumed for a given three-month window, using each month’s median list price weighted by each month’s total listing outflow

BROKERAGE REVENUE — Potential commission pool

The value of the estimated pool of commissions that were available to brokerages during a given period, based on list price multiplied by total listing outflow

Note: This metric is blind to important factors that vary by market, such as average commission rates and splits, as well as the number of serious agents competing for business in the area. It’s not adjusted for inflation. It also doesn’t consider how much real estate activity is a result of new construction. The metric best used for a broad overview and tracking trends over time.

This is a deep dive into a local real estate market powered by Inman Market View. The goal: To put more local data in the hands of the Inman community, and to place it in a context that’s highly relevant for the U.S. brokerage industry.

One of the biggest housing stories this spring has been a much-needed boost in inventory in many parts of the U.S.

Nationwide, inventory exceeded 1 million for the first time since the winter of 2019, with 50 of the largest metros in the country posting annual inventory gains in May.

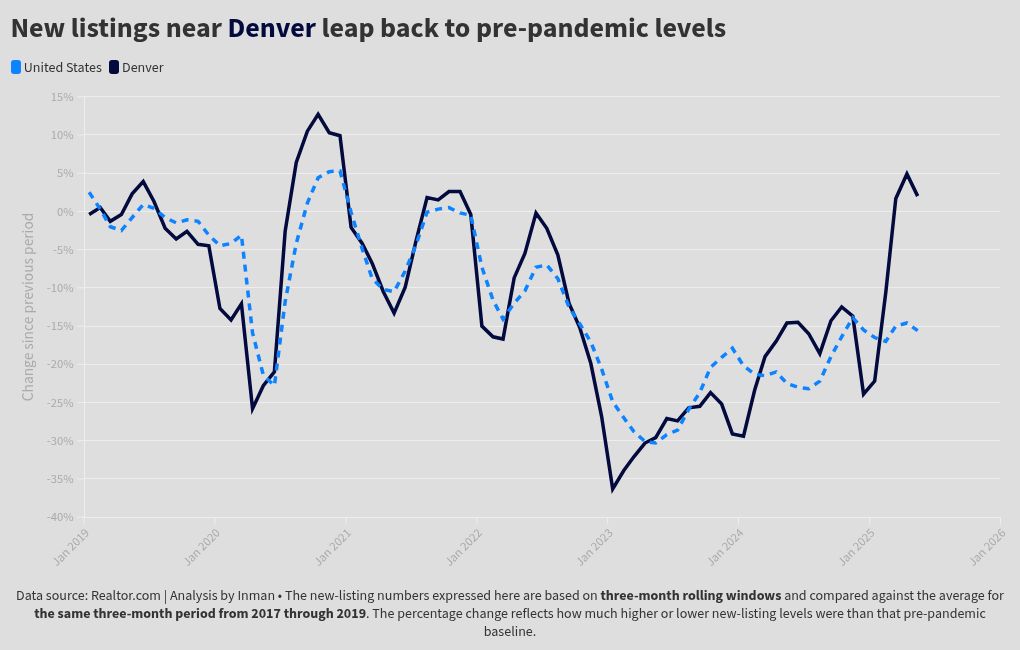

Out of those metros, one that has seen a significant inventory improvement is Denver. The Western mountain market posted a 20 percent annual growth in new listings during the three-month period of March through May, the second-highest jump among any large U.S. market, according to listing data from Realtor.com.

In a market where many buyers have felt locked into their existing low-rate mortgages, and where current prices are unaffordable for many, some have pointed to new construction as a possible explanation of a listing resurgence in places like Denver.

But local agents and Denver market experts who spoke with Inman suggested that existing homeowners — not builders — have done the most to provide new supply to the market over the past year.

The reasons Inman’s sources gave were complex, ranging from broad factors that much of the country is experiencing alongside the greater Denver housing market, and unique issues with regulations and ownership costs that are sending some investors and other owners packing.

These are the numbers — and reasons — behind Denver’s year of extraordinary inventory gains.

Steady gains

The Denver-Aurora-Centennial, Colorado, metro area has seen sustained growth in new listings this spring, providing buyers with more options and opportunities.

Almost 20 percent more new listings hit the market in the greater Denver area this spring than during the same period last year, bringing overall new supply levels to roughly where they were in a typical spring before the pandemic began.

Active listings over the same three-month period were up 65 percent in the metro on an annual basis, and were 89 percent higher than their 2017-2019 levels at the same time of year, according to data from Realtor.com. All in all, inventory in May represented a solid, three-months’ supply.

Still, there were signs that this robust momentum in new supply might be slowing down in recent weeks.

During the month of May alone, new listings were up only 4 percent year over year to 7,017 new listings, according to REcolorado numbers that align closely with those tracked by Realtor.com.

As inventory has grown, sales have also been a mixed bag.

Closed listings were down 5 percent year-over-year in May, according to REcolorado. In perhaps a more encouraging sign for June sales, however, the number of pending listings over the same period was up 12 percent from the year before.

Buyers taking their time

While new listings are up across the board, subdued demand for homes in Denver and nearby areas has further pushed the local market in a more buyer-friendly direction, Inman found.

Because of high prices (the median closed price on Denver homes has hovered around $600,000 since 2022, according to REcolorado) and mortgage rates, as well as general economic uncertainty in the U.S., many potential buyers have taken a more careful approach to homebuying than has been typical in recent years.

Christine Dupont-Patz | RE/MAX of Cherry Creek

“I feel right now that the buyers are just being very selective,” Christine Dupont-Patz, broker and co-owner of RE/MAX of Cherry Creek Inc., told Inman. “There seems to be no rush.”

Jackie White of Your Castle Real Estate said she sees a lot of what she calls “tire-kickers” these days: buyers who want to take their time and do more due diligence than they’ve been afforded in recent years during what used to be a rapid-fire market.

“With the cost of insurance having gone up in recent years as well as the interest rate [increasing the cost of homeownership], it’s just making [buyers] do a lot more due diligence before making an offer,” White said. “The total cost of ownership is being met with more scrutiny because of those increasing costs, and with homes having longer days on market, they feel like they have time to consider the home and it’s OK if it goes under contract and they lose out because there’s likely several other homes active that they would consider.”

By contrast, in the years during and shortly after the COVID-19 pandemic, buyers were scrambling to find any home that would suffice, Dupont-Patz explained, both to find shelter and hop on low interest rates. Without those factors at play today, and with more inventory at their finger tips as well as impending economic uncertainty in response to tariffs, there’s no real urgency for buyers.

“Now, you really feel where buyers are, ‘I want this to be my forever home. I want this to be where I’m going to raise my kids,’” Dupont-Patz said. “And I have clients who are downsizing, so the big thing is, how can they age in place? Is the neighborhood walkable for them? Does it have the amenities that they want as they get older? So it’s really taking a much longer term view of what they want to buy.”

People from all over the country for a long time have found Denver an attractive market to move to because of its city amenities paired with easy access to nature. But some buyers from out-of-state today can be surprised by the area’s price points, Dupont-Patz said. As she’s seen the parents of millennials and Gen Z’ers start to move to the area to be closer to their grandchildren, their homebuying process is often more prolonged than expected because those transplants have slightly unrealistic expectations about how much property their can get for their dollar.

Insurance and homeowners association fee hikes have also put a significant damper on demand in the condo market in Denver, Dupont-Patz said.

Insurance premiums increased by an average of 58 percent between 2018 and 2023, according to the Rocky Mountain Insurance Information Association, and are expected to rise by about 11 percent this year in response to wildfire and hailstorm risks, according to Insurify.

One of Dupont-Patz’s clients decided to pull their relatively new one-bedroom one-bath condo from the market after two months without a single showing.

“Unfortunately, we were not the only condo in the building that did not have one showing,” Dupont-Patz continued. “[Other agents and I] all came together and said, ‘OK, we’re all going to have an open house at the same time on a Saturday. We’re going to all cross-advertise it.’ If people came to the open house, we would give them a gift card to see the Rockies — and you can make all the jokes you want, ‘Well you can’t give that shit away with your Rockies,’ I know that’s a whole ‘nother conversation — no one, no one came to see the condos.”

Sellers ready to cash out

Jackie White | Your Castle Real Estate

White said that many condo owners are wanting to list now because those higher insurance fees, which are spurring higher HOA fees, are making it so that it’s more expensive to own a condo than to rent an apartment. “So we’re finding much longer days on the market for condos and townhomes and a really big inventory in that product.”

Some investors are likewise considering offloading rental properties because of recent legislation in the state that places more restrictions on landlords, White said.

As of last year, restrictions were put in place that make it more difficult for landlords to evict tenants, put limits on the cost of pet security deposits and rent and prohibit municipalities from limiting the number of people who can live together in a unit based on familial relationships, among other measures.

“So there are investors that are opting to cash in on the equity that they’ve gained on their properties as well,” White said. “When they look at the annual cash flow compared to the equity in their home, in many cases, the returns are 3 to 4 percent and so choosing to take that money and invest it elsewhere, perhaps out of state or in the stock market, would serve them well compared to hanging onto these properties with a lot of the legislation and regulation that’s in place.”

New construction’s part

Denver’s commitment to building during and after the pandemic seems to have had some role in its current healthy inventory levels, according to a Realtor.com report.

“Metros that built more housing like Austin, Nashville and Denver have generally returned to pre-2020 inventory levels,” the report stated. “Those with less new construction like New York, Boston and Buffalo, New York, have not.”

Ted Leighty | Colorado Association of Home Builders

However, more recent new construction is contributing little to new inventory this spring, Ted Leighty, CEO of the Colorado Association of Home Builders, told Inman.

“We do not believe that new construction is adding a lot of homes to the current number of properties on the market in the metro Denver area,” Leighty said in an email. “In 2024, our members pulled about 650 to 700 permits per month, and those homes are either coming to the market now or are already sold to their future owners. These new homes would represent a small fraction of the 13,000-plus homes currently on the market.”

In 2021, 30,006 building permits were issued in the Denver metro area, according to the U.S. Census Bureau’s Building Permits Survey, and in 2022, 23,009 permits were issued. By comparison, just 15,570 permits were issued in 2024.

That support from new construction was further weakening in the early months of this year, the data shows.

Only 4,881 residential permits were issued in the first four months of this year, down 10 percent from the year before. This annual decline was driven primarily by a 17 percent reduction in permits for single-family homes, while permits for multifamily units remained steady.

This multiyear decline has yet to feel much impact from the Trump administration’s tariffs on the kinds of imported goods that are used in residential construction, Leighty said.

According to the National Association of Home Builders, roughly $204 billion worth of goods were used in constructing new multifamily and single-family homes in 2024, $14 billion (or about 7 percent) of which were imported from outside of the U.S.

Colorado has not felt an impact as of yet, Leighty said, but builders are trying to prepare for them.

“At this point, we are not seeing tariffs having a direct impact on permits here in Colorado,” Leighty said in an email. “Mostly we are hearing that our members are adjusting their supply chains and budgets to adapt to the tariff situation. Like other markets across the U.S., we believe that mortgage rates and a general lack of consumer confidence are having a bigger impact on home sales and demand for new construction.”