by Christy Murdock | May 6, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Sixth-generation Fairfield County, Connecticut, resident and two-decade Realtor Libby McKinney-Tritschler knows her market. Her deep roots in the community are informed by her deep involvement in local volunteer efforts, serving on the board of the Pequot Library, the Westport/Weston YMCA, the Bedford Family Social Responsibility Fund and the Stewart B. McKinney Foundation.

A consistent top-producer, McKinney-Tritschler leverages her extensive personal and professional network and strong local reputation to navigate the complexities of the market and make every transaction as seamless as possible. Find out what she’s learned along the way and what advice she’d offer new agents just starting out.

Name: Libby McKinney Tritschler

Title: Sales agent

Experience: 20+ years

Location: Fairfield County, Connecticut

Brokerage name: William Raveis Real Estate

Rankings: Executive Vice President of Sales

Team: On The Harbor

Transaction sides: 400

Sales volume: $727 million

As a child, what did you want to be when you grew up?

I think I wanted to be a politician. When I was young, I loved spending time with my father, who was a congressman. He would spend his weekends canvassing his community and talking to his constituents. He built relationships, understood people’s needs and earned their trust — much like what I do in real estate.

Both require strong communication, a personal touch and the ability to connect with people from all walks of life. In real estate, you must be present, listen and show your clients you genuinely care.

What’s the best advice you ever got from a mentor or colleague?

Without signatures, you have nothing. In real estate conversations, promises and verbal agreements mean nothing without signatures. Nothing is certain until it is in writing.

It’s a reminder to stay proactive, protect everyone’s time and ensure the deal is solid before getting too excited about an opportunity. This is a very important lesson, and if you can learn it early on in life/your career, you’ll be ahead of the game.

What would you tell a new agent before they start out in the business?

I would tell a new agent that real estate isn’t just about selling homes. It’s about building relationships, staying consistent and playing the long game. Success doesn’t happen overnight, so stay patient and persistent, and never stop learning.

Provide value, be reliable and genuinely care about your clients, and in time, the business will come.

What do clients need to know before they begin a real estate transaction?

This is a challenging process, and those who can control their emotions have the best chance of capitalizing on an opportunity.

What do too few agents know that would make their lives easier?

The best agents master what others overlook. Emotional intelligence gives you the ability to read people, adapt and build trust quickly. Real success comes from adaptability — knowing when to pivot based on conversation.

Setting clear expectations with your clients upfront prevents headaches down the road, while wise follow-ups ensure you are adding value, not just checking in. Knowing when something is truly urgent and when to let things breathe keeps both deals and everyone’s sanity intact.

Storytelling is another game changer. Facts inform and stories sell; try to tell the story every time.

What is the best thing you can do for your life and business?

Love what you do and build real connections. Whether it’s with clients, colleagues or in your community, people want to work with someone they trust and enjoy being around. Stay in touch, and be helpful without always expecting something in return.

Most importantly for me is to make your work something you’re excited about. When you love what you do, success follows.

If you could do anything other than real estate, what would it be?

Honestly, I couldn’t imagine doing anything else. Real estate is the perfect blend of relationships, strategy and problem solving; every day is different.

I love the people, the challenge and the ability to make a real impact on someone’s life. Any job I choose would have to involve working closely with people, helping them navigate big decisions and building something meaningful. That being said, nothing excites me the way real estate does.

Tell us a story about your most memorable transaction

Some properties are more than just real estate — they hold stories, legacies and deep historical roots. Selling 66 Beachside Ave in Westport was not just a transaction; it was an honor.

This waterfront estate was a rare gem, the largest parcel available at the time, with a history stretching over a century. Built in the early 1900s, it remained in the same family until 2015, a testament to its significance and the deep connection the owners had to the land.

The indigenous inhabitants once called it “Machamux,” meaning “beautiful land,” a name that still felt fitting as the waves kissed its private shoreline. Later, the family lovingly referred to it as “Banrock,” inspired by the striking rock formations along the beach.

Beyond its natural beauty and history, what made this sale truly special was its purpose. It was part of an estate sale, with proceeds directed to three nonprofit organizations. Knowing that this transaction would help fund meaningful causes added more fulfillment.

Additionally, this was the last piece of land belonging to the Bedford family, marking the end of an era for a lineage that had long been woven into the fabric of Westport. Facilitating this transition was both a privilege and a responsibility, ensuring that the next chapter of this property’s story was handled with care and respect.

Selling homes is often about numbers, negotiations and contracts. But every so often, a sale like this comes along — one that reminds me why I love what I do.

Email Christy Murdock

This post was originally published on this site

by Matt Carter | May 5, 2025 | Industry, News Feed

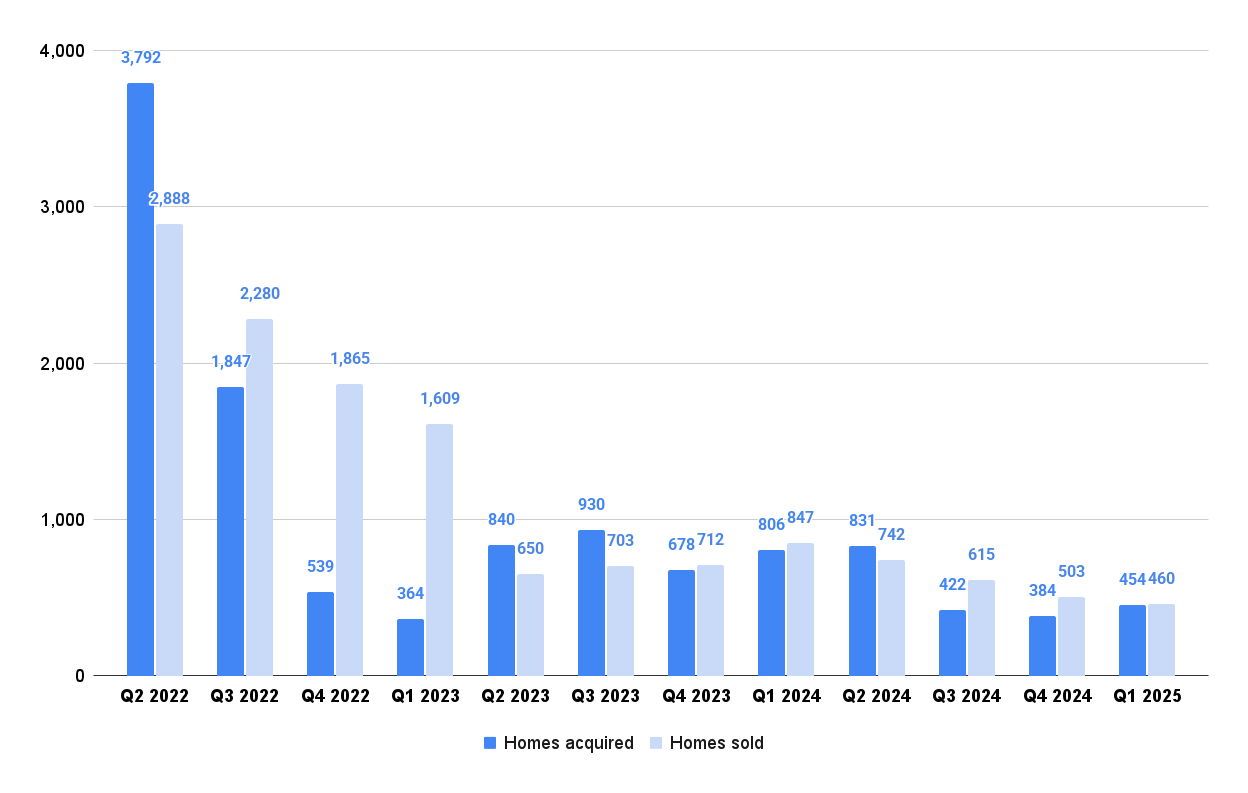

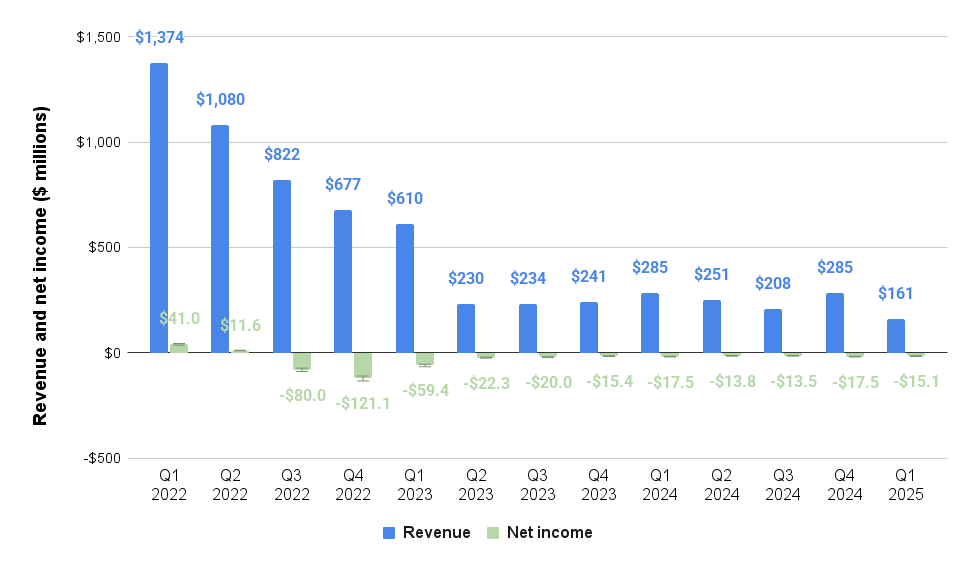

Offerpad’s $15.1 million Q1 net loss is down 14 percent from Q4 2024, with home acquisitions up 18 percent from the previous quarter to 454.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Cash offer and renovation platform Offerpad Solutions Inc. trimmed its first quarter loss by 14 percent while upping its home purchases, but brought in less revenue as it sold fewer homes.

Offerpad reported a $15.1 million Q1 net loss Monday, down from $17.5 million in Q4 2024, with home acquisitions up 18 percent from the previous quarter to 454.

With Q1 home sales down 9 percent from Q4, revenue shrank by 8 percent to $160.7 million.

Brian Bair

Offerpad CEO Brian Bair said the company’s cash offer program “performed as expected,” while “asset light” services like the company’s B-to-B Renovate business, Direct+ buyer program and Agent Partnership Program “contributed significantly to the top and bottom line.”

Offerpad’s Renovate business closed 209 projects in the first three months of the year, up 12 percent from Q4, generating record revenue of $5.3 million.

Bair announced a new partnership with Auction.com in which Offerpad’s Renovate service will become a preferred provider of renovation services for buyers on the platform.

“It’s a meaningful step forward as we help buyers transform properties into move-in-ready homes, expand our renovation business and deliver greater value to buyers, sellers and communities across the country,” Bair said.

Shares in Offerpad, which in the last 12 months have traded for as little 92 cents and as much as $7.88, closed at $1.03 before Monday’s earnings release, and were up 2 percent in after hours trading.

Offerpad was put on notice by the New York Stock Exchange last month that it could be delisted from the exchange because its market capitalization has dropped below $50 million.

With 27.38 million shares outstanding, Offerpad’s price per share would need to rebound to at least $1.83 for the company’s market capitalization to meet the $50 million threshold.

The company said at the time it was confident it would be able to submit a business plan detailing how it will get back into compliance with the stock exchange’s listing standards within 18 months.

Offerpad Q1 2025 acquisitions up, sales down

Offerpad acquired 454 homes during Q1, up 18 percent from Q4 but down 44 percent from a year ago.

Close to half of those acquisitions (42 percent) were driven by Offerpad’s Agent Partnership Program, up from 28 percent a year ago.

While Offerpad sold 43 fewer homes during Q1 2025 than it did in Q4 2024, gross profit per home sold was up 8 percent quarter over quarter to $22,800.

Offerpad finished the quarter with 671 homes in inventory, but said only 13 percent were owned for more than 180 days, down from 22 percent at the end of the year.

Company executives said they expect home sales to rebound to between 500 and 550 sales in Q2.

Offerpad trims losses and expenses as revenue drops

Although slower Q1 sales dented revenue, operating expenses for the quarter were down 39 percent from a year ago to $22 million, helping Offerpad trim $2.4 million from its Q4 loss.

Offerpad executives said they expect Q2 revenue of $160 million to $190 million, and “sequential improvement” in adjusted earnings before interest, taxes, depreciation and amortization (EBITDA).

At negative $7.8 million, Q1 EBITDA represented a 32 percent improvement from $11.5 million in Q4.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 5, 2025 | Industry, News Feed

Bellevue, Washington-based Evergreen hires Wells Fargo and Bank of America veteran Andrew Leff as head of national business development as it continues to expand beyond its roots as a regional independent mortgage bank.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Evergreen Home Loans continues to expand beyond its roots as a regional independent mortgage bank, hiring Wells Fargo and Bank of America veteran Andrew Leff as head of national business development.

Leff, who’s also held senior leadership positions at JPMorgan Chase and U.S. Bank, will be responsible for expanding Evergreen’s footprint through partnership-driven growth strategies including builder and affinity relationships, the lender announced Monday.

Robert Lipston

“Andrew’s reputation in the industry speaks for itself,” Evergreen executive Robert Lipston said in a statement. “He brings the experience, strategic vision, and leadership we need as we continue to grow our national presence. We’re thrilled to have him on board.”

Based in Bellevue, Washington, Evergreen in January announced an expansion into five Southeastern states — Florida, Georgia, North Carolina, South Carolina and Tennessee — with former Guild Mortgage executive John Porath overseeing its operations in those states.

The cash offer pioneer in March announced its entry into the New Mexico market with branches in Albuquerque and Carlsbad under the leadership of Area Manager Barry Abt.

Launched in 2021, Evergreen’s CashUp program has grown into a suite of products that also includes a buy-before-you-sell product, “StepUp,” and a rate-lock product for sellers, “Lock and List.”

Evergreen has fueled growth through partnerships with real estate agents and builders, a strategy that Leff has extensive experience with.

Leff was head of business development programs at Wells Fargo, managing builder, corporate affinity, relocation and wealth management partnership channels. During a 10-year stint at Bank of America, Leff was instrumental in building and scaling the bank’s national builder and affinity platforms, Evergreen said.

Andrew Leff

“I truly admired Evergreen’s people-first culture and entrepreneurial spirit,” Leff said in a statement. “I’m excited to help build on that foundation by creating scalable, value-driven partnerships that support both the business and the communities we serve.”

Evergreen sponsors 227 mortgage loan originators who work out of 51 branch locations in nine states — Arizona, California, Idaho, Montana, New Mexico, Nevada, Oregon, Texas and Washington — according to records maintained by the Nationwide Multistate Licensing System.

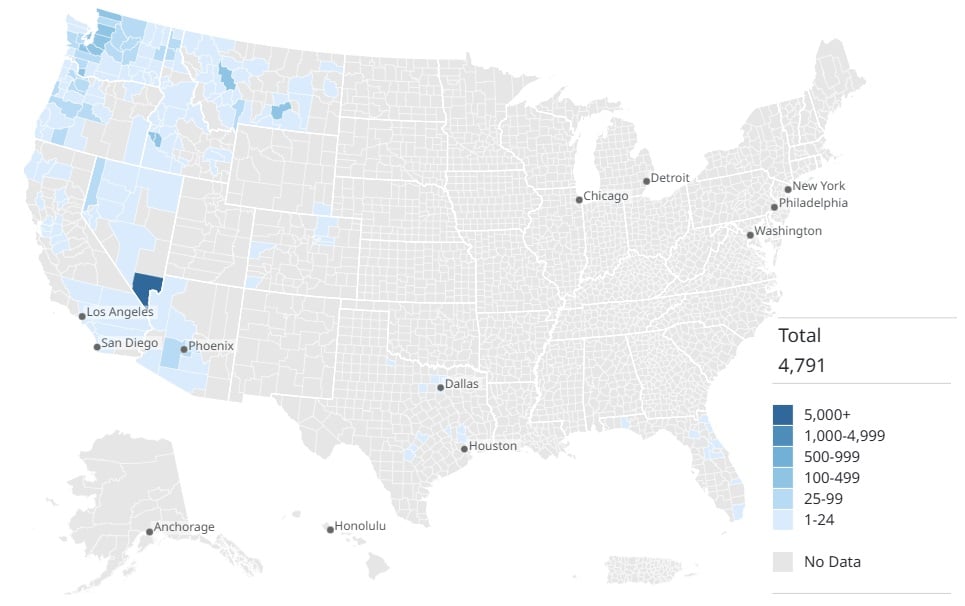

Evergreen Home Loans’ growing market presence

Evergreen Home Loans 2024 business by county. Source: iEmergent analysis of Home Mortgage Disclosure Act (HMDA) data.

Last year, Evergreen funded 4,791 mortgages totalling $1.92 billion, up 22 percent from 2023, according to an analysis of Home Mortgage Disclosure Act (HMDA) data by mortgage business intelligence provider iEmergent.

According to iEmergent data, purchase loans accounted for 85 percent of Evergreen’s business in 2024, most of which was done west of the Rocky Mountains, with a growing presence in Texas and Florida.

Evergreen on Monday was advertising 11 positions on its website, with openings for loan officers and funders, investor accounting manager and a branch marketing assistant.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Marian McPherson | May 5, 2025 | Industry, News Feed

The Neal & Neal Team has joined eXp Realty after 15 years with Keller Williams, according to an announcement on Monday. The Neal & Neal Team closed 2024 with 914 transactions worth $338 million, making it KW’s second-largest team by closed units.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The Neal & Neal Team has joined eXp Realty after 15 years with Keller Williams, according to an announcement on Monday. The Neal & Neal Team closed 2024 with 914 transactions worth $338 million, making it KW’s second-largest team by closed units.

Clint Neal

Brothers Clint and Shane Neal co-founded The Neal & Neal Team after completing degrees in agricultural economics, real estate, and finance at Texas A&M University. During their tenure with the Texas-based franchisor, the duo closed more than $1 billion in sales and grew their team to 80 agents and 20 staff members.

NNT was named one of Inc.’s 5000 fastest-growing companies in 2024, and clinched the No. 1 spot on the San Antonio Business Journal’s 2025 “Best in Residential Real Estate” list.

“We’ve reached a point where we need a platform that can scale with us,” Clint said in a prepared statement. “EXp gives us the flexibility, innovation and global reach to take things to the next level, for our agents and for ourselves.”

Clint Neal

Added Shane, “We already had the systems and mentorship in place. But eXp takes everything we’re doing and supercharges it. It’s a win for our agents and a win for the people they serve.”

EXp Realty CEO Leo Pareja said the duo’s “commitment to culture, scalability and agent success aligns perfectly with what we’re building at eXp.”

“Shane and Clint have built one of the most systemized, high-performing real estate teams in the country,” Pareja said. “We’re thrilled to welcome the entire Neal & Neal Team to eXp.”

EXp has struggled in recent quarters with agent count growth, with the cloud-based brokerage’s fourth-quarter and full-year 2024 earnings revealing its agent count had declined 5 percent year over year to 82,980. Although that’s not a number to sneeze at, it does fall short of company founder Glenn Sanford’s 2021 prediction that eXp would hit 500,000 agents by 2026.

Although agent count growth has been lagging, the brokerage’s transaction sides and volume have remained robust — signaling that its focus on recruiting experienced teams and brokerages, like NNT, is working.

“We’re very much focused on attracting producing agents and teams. So that top tier of the industry,” eXp Chief Marketing Officer Wendy Forsythe told Inman in November. “This year, we have had a campaign and mantra around ‘eXp is where the pros go to grow.’ That has really been an anchor of our recruiting efforts, especially given the market.”

“Agents are looking for stability and legacy and all of the important fundamentals that a proven model and brokerage like eXp can provide,” she added. “So that’s very much been an overarching focus of our recruiting efforts this year.”

Email Marian McPherson

This post was originally published on this site

by Andrea V. Brambila | May 5, 2025 | Industry, News Feed

This is the first in a two-part interview with Howard Hanna Real Estate Services CEO Howard “Hoby” Hanna IV. The interview was conducted in the weeks leading up to the independent brokerage’s settlement on May 2 in the Gibson antitrust commission lawsuit. Read the first part HERE.

In choosing to keep its pocket listing rule and add a new delayed marketing option, the National Association of Realtors has been accused of trying to mollify its biggest broker members.

Did it work? Not according to Howard W. “Hoby” Hanna IV, the CEO of Howard Hanna Real Estate Services.

Inman reached out to Hanna last month to ask how NAR’s new Delayed Marketing Exempt Listings category might impact Howard Hanna’s listing displays. The 1.5-million-member trade group added the category after choosing to keep the Clear Cooperation Policy, a controversial rule that requires listing brokers to submit listings to Realtor-affiliated multiple listing services within one business day of publicly marketing them.

NAR’s new listing category allows brokers to keep listings off of MLS subscribers’ Internet Data Exchange (IDX) listing websites, but not Virtual Office Websites (VOWs), which require registration in order to see certain information.

Hanna told Inman that as a result of the change, Howard Hanna is “seriously considering moving to registration in all markets” and is looking at options to re-launch its Find It First program for listings that had not yet been entered into the MLS as well as for sellers choosing to keep their listings off of the MLS altogether.

According to Hanna, Howard Hanna first tested a VOW in the summer of 2023 in the Cleveland area in Northeast Ohio, where the company has a big market share, and the move resulted in increased traffic and better lead generation with more qualified leads.

“We have not moved completely to all markets but are now looking with pure intent to maximize our customer experience and create the best consumer experience for buyers and sellers,” Hanna told Inman in a statement.

“We also think our Buy & Borrow Bundle with Find it First will tie into creating a great experience for the clients that choose Howard Hanna.”

The company’s Buy & Borrow Bundle offers a closing cost credit of 0.5 percent of a buyer’s loan amount — up to $10,000 — for qualified buyers who choose to buy their home with Howard Hanna and also get a mortgage with Howard Hanna Mortgage Services.

But Hanna also offered his thoughts on long-term changes he’s contemplating for the company, including the potentially industry-changing step of leaving NAR and its affiliated MLSs.

This interview has been edited for length and clarity.

Inman: Some say that VOWs present a registration hurdle that people might not want to bother with when they’re searching websites for listings; they may see the registration requirement and leave. Is that not something you’re concerned about? You also mentioned the customer experience — how is that a better experience?

Hoby Hanna: How many retail, consumer-based websites are you personally registered on so that you get a deeper level of retail experience? You can get Nordstrom’s customers to sign up, and they have your information, and you’ll get information about bonus days, new items, new luxury goods and other things because you’re a customer before the general public does.

If [a customer] can know about the market earlier, faster, quicker and know about special items before everybody else, that doesn’t hurt the market. It just makes those of us who may offer that experience pick up more clients and have the ability to cross-market different products and other things. So I’m not as concerned.

You mentioned before how having these Find It First listings helps with stickiness — people go to your website to see the latest listings. The new policy around Delayed Marketing Exempt Listings allows you to have those listings in your VOW, right? So if other brokers, which at this point also include Redfin and Zillow, have VOW sites, it means they can display these delayed marketing listings as well. How do you feel about that?

That’s part of the competition, and they can do that. I actually think that’s another proverbial shoe that’s gonna drop. Whether you want to do it as a VOW feed and have those there, or whether you don’t and go away from a VOW and make it more just that you’re gonna get our Find It First or [office] exclusives, all you have to do is register.

We’re having conversations with people both at Zillow and Redfin because if we go to everything Find It First and exclusives and not feed from VOW or IDX at all with those listings, they’re not gonna have them. They want to make sure they can still showcase our listings for their business model that they may have to change, and maybe they have to pay for those listings in some capacity, as opposed to just receiving them through an MLS feed.

I’d be willing to send them that if they’re willing to accept it and maybe work a deal out where they’re giving us our leads back on those and not monetizing them to other partners if they want that ability for a period of time.

What is it that you can do that would prevent Zillow and Redfin from getting your listings? What is it that they’re bargaining with you for?

I won’t put them in a VOW. I won’t have a VOW. I don’t need a VOW. I don’t need IDX. I might not be in MLS anymore. The world’s changed. I don’t need to listen to NAR. There might not be MLS five years from now, if people are going to dictate where I have to send things.

Quite honestly, this rule that they changed, the thing’s called Clear Cooperation. We don’t need to cooperate with each other anymore. That was taken away by the lawyers.

We love to cooperate with other brokers. We love to share our data and our listings, those that the seller says, “Fine, put it into the open market and share.” But if we want to [we can] put everything on our website and say to the consumer, “We don’t put it in an MLS anymore. We do direct feeds to Zillow. We do direct feeds to Realtor.com. We have it on our website. We send a letter to every broker in the country and say you’re still welcome to show a house.”

We’re not going to follow rules based on NAR telling us how to operate our business. That’s not the role NAR should play.

Is that your plan?

I’m considering it.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Lillian Dickerson | May 5, 2025 | Industry, News Feed

The seasoned investor has served as Berkshire Hathaway’s CEO since 1970. He will continue to serve as chairman as Greg Abel takes on the CEO role in 2026.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Long-time Berkshire Hathaway CEO Warren Buffett announced during the company’s annual meeting on Saturday that he would be retiring from his position at the end of the year, and that he would recommend Greg Abel to the board as his successor.

“The time has arrived where Greg should become the chief executive of the company at year-end,” the 94-year-old investor said during the surprise announcement.

Buffett’s choice of successor was no secret — he had announced in 2021 that he had his eye on Abel to take over the company’s reins. But only Buffett’s children, Howard Buffett and Susan Buffett, who are both Berkshire directors, knew in advance that this would be the year for the leadership transition to take place. Buffett has served as CEO since 1970.

The savvy investor shepherded Berkshire Hathaway through decades of changes, transitioning the company from its textile beginnings into a conglomerate starting back in 1965. HomeServices of America is owned by Berkshire Hathaway Energy, a subsidiary of Berkshire Hathaway.

Over the years, Buffett has become known for his quotable, sound investment advice, which has had an impact on aspiring entrepreneurs worldwide. Thousands of investors and admirers made the pilgrimage to Omaha, Nebraska, each year to attend the company’s annual meeting, which Buffett called “Woodstock for Capitalists.”

Buffett said that he will continue to be active, serving as chairman at Berkshire Hathaway as Abel takes over.

Abel, who is a native of Canada, became involved in Berkshire Hathaway in 1999 when the company invested in MidAmerican Energy, the precursor of Berkshire Hathaway Energy. Abel and David Sokol, Abel’s former boss, were instrumental in building Berkshire Hathaway Energy through a series of acquisitions. In 2018, Buffett promoted Abel as vice chairman and a member of the board, placing him at the head of all noninsurance operations.

During Saturday’s annual meeting, Buffett said he generally prefers to invest in stocks versus real estate, because with multiple parties involved in real estate deals, things can sometimes get messy.

“Well, in respect to real estate, it’s so much harder than stocks in terms of negotiation of deals, time spent and the involvement of multiple parties in the ownership,” Buffett said. “Usually when real estate gets in trouble, you find out you’re dealing with more than just the equity holder.”

“There’s just so much more opportunity, at least in the United States, that presents itself in the security market than in real estate,” Buffett added.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

This post was originally published on this site