by Richelle Hammiel | May 5, 2025 | Industry, News Feed

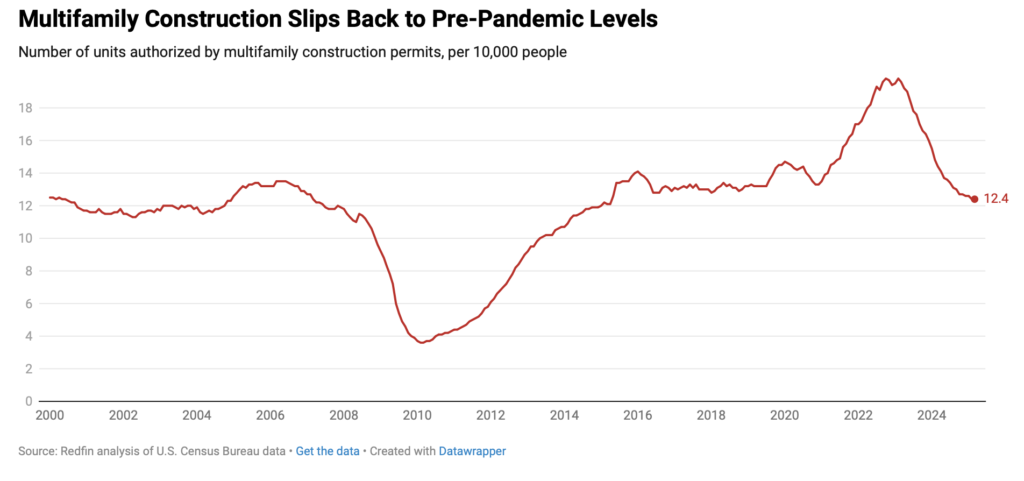

According to a new Redfin report, building permits for multifamily units have plunged 27.1 percent from their pandemic-era highs, with new rentals now hitting the market at the slowest pace on record.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Builders in the multifamily housing market are pumping the brakes — and fast.

According to a new Redfin report, building permits for multifamily units have plunged 27.1 percent from their pandemic-era highs, with new rentals now hitting the market at the slowest pace on record.

Sheharyar Bokhari | Redfin Senior Economist Sheharyar Bokhari

“New apartments are being rented out at the slowest speed on record, and builders are pumping the brakes because elevated interest rates are making many projects prohibitively expensive,” Redfin Senior Economist Sheharyar Bokhari said in the report. “At some point in the next year, the slowdown in building will mean that renters have fewer options — potentially leading to an increase in rents.”

In short, building is getting riskier and more expensive.

During the height of the pandemic, builders were filing an average of 17 multifamily permits per 10,000 residents. Over the past year, however, the average has fallen to just 12.4 permits per 10,000 people, a 5.5 percent drop from pre-pandemic levels, according to the U.S. Census Bureau’s multifamily housing data.

Redfin analysis of U.S. Census Bureau data

It’s not just interest rates dampening builder enthusiasm. Tariffs imposed under the Trump administration are adding costs to construction materials.

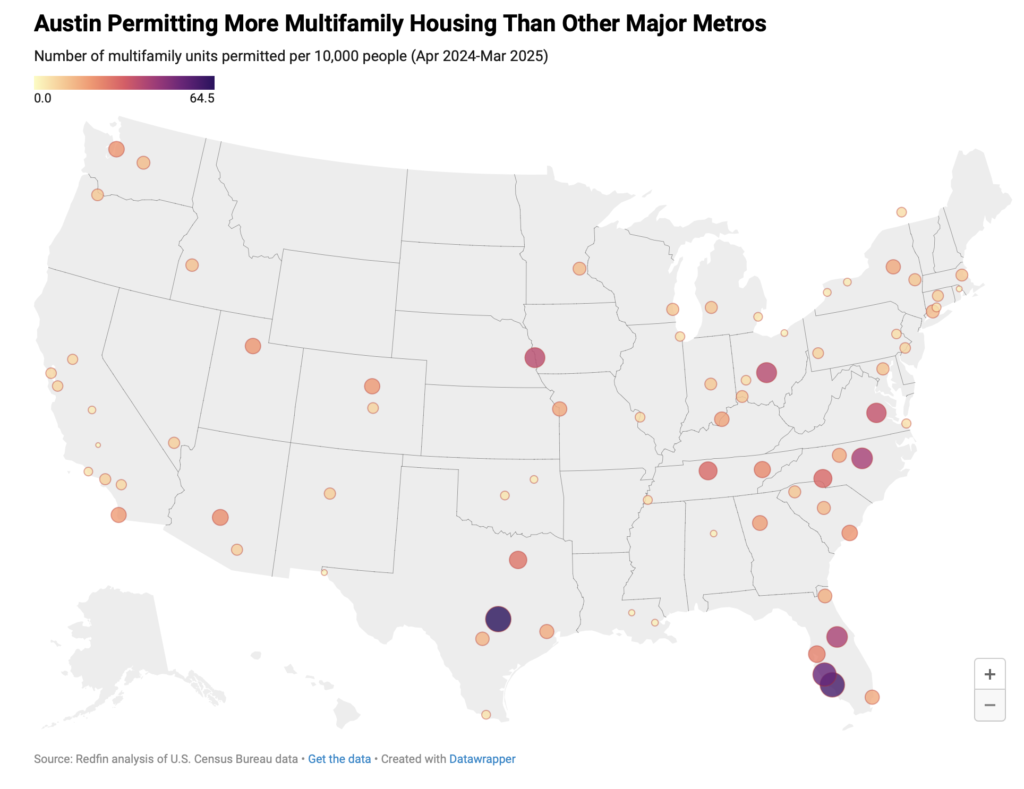

The combined effect of higher borrowing costs, slowing rent growth and steeper material prices have caused builders in many metro areas to pull back. In fact, 63 percent of markets analyzed by Redfin saw a decline in multifamily permitting since the pandemic.

Redfin analysis of U.S. Census Bureau data

Stockton, California, for instance, saw permitting drop to zero. Colorado Springs, Colorado, fell 82 percent to just 8.6 units per 10,000 people, while Boise City, Idaho, declined 64 percent to 12.6 units.

Still, there are bright spots. A few cities are defying the trend and ramping up construction. Oklahoma City led the way with a 193 percent increase in permits — from just 1.7 units per 10,000 people during the pandemic to 5.1 over the past year. Austin, Texas — where remote work fueled a surge in housing demand and construction following the pandemic — led all major metros with 64.5 units permitted per 10,000 people.

Cape Coral, Florida (59.6); North Port, Florida (53.3); and Raleigh, North Carolina (41.1), also saw significant multifamily growth.

Even so, Redfin warns that today’s slowdown could become tomorrow’s supply crunch. If construction continues to lag, renters may soon find themselves facing fewer options and potentially higher rent prices.

Email Richelle Hammiel

This post was originally published on this site

by Jim Dalrymple II | May 5, 2025 | Industry, News Feed

The campaign features McEntire advising would-be homebuyers in sitcom-like scenarios. It’s also the largest such campaign in the portal’s history.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Realtor.com announced Monday that it is launching a new ad campaign featuring country music singer Reba McEntire.

The company has dubbed the campaign “Nearly Home,” and, according to a statement, will rely on McEntire to “offer something many homebuyers haven’t felt in years: optimism.” The company did not disclose what it is spending on the campaign, but did say in the statement that it is the “largest brand investment” in Realtor.com’s history.

Videos from the campaign Inman previewed are structured to imitate a classic sitcom, complete with a laugh track, and show a young couple struggling to choose a house.

McEntire then bursts in through the front door and advises the couple to check Realtor.com for listings. According to the statement, the “episode” is “called ‘The One without the Break-Up,’” and “highlights the very real drama that often comes along with buying a home.”

The campaign will air on TV as well as online and includes a sponsorship of the Country Music Awards, which stream on Amazon Prime on May 8. McEntire is hosting that show.

An image from Realtor.com’s new campaign. Credit: Realtor.com

The campaign arrives against the backdrop of intense competition in the consumer portal space. Though Zillow maintains the No. 1 spot in the space, Realtor.com and CoStar’s Homes.com have battled it out in recent years for No. 2. Homes.com has, in part, managed to grow thanks to CoStar’s intense marketing spend, which has included, among other things, Super Bowl ads.

In the case of Realtor.com, the company said in its statement that it expects the new ad campaign to reach about half of Americans. The statement notes that the campaign is “a direct response to the anxiety, confusion and doubt that define today’s housing market.”

Mickey Neuberger, chief marketing officer at Realtor.com, said in the statement that the goal of the campaign is to “make home search feel more human, more hopeful and less overwhelming — especially for a generation of buyers who’ve been navigating a complex market.”

“As the most trusted brand in real estate and the brand most trusted by real estate professionals, partnering with Reba McEntire was an easy choice,” Neuberger added. “She’s got the trust, the charm and the boots-on-the-ground wisdom to bring a genuine sense of reassurance, and a little humor, to our message. She helps us remind people that finding a home shouldn’t feel impossible — it should feel like coming home.”

Email Jim Dalrymple II

This post was originally published on this site

by Andrea V. Brambila | May 5, 2025 | Industry, News Feed

This is the first in a two-part interview with Howard Hanna Real Estate Services CEO Howard “Hoby” Hanna IV. The interview was conducted in the weeks leading up to the independent brokerage’s settlement on May 2 in the Gibson antitrust commission lawsuit. Check back later today for the rest of Inman’s interview.

Howard Hanna was one of more than 90 large brokerages that were not covered under the National Association of Realtors’ $418 million settlement of multiple commission-related antitrust lawsuits nationwide last year, and its CEO is not about to forget it.

Because Howard Hanna was left out of the deal, its company, Hanna Holdings, was left to fight one of those suits. On Friday, after a year of legal feuds, the company announced it had finally reached an agreement to settle the Gibson commission lawsuit, leaving only an antitrust suit brought by homebuyers to resolve.

“They sold the industry down the river on the lawsuits and didn’t protect all their members,” Howard W. “Hoby” Hanna IV told Inman in a phone interview in April before the settlement was made public.

Inman initially reached out to Hanna after NAR decided to keep its controversial Clear Cooperation Policy and added a new Delayed Marketing Exempt Listings category. The CCP requires listing brokers to submit listings to Realtor-affiliated multiple listing services within one business day of publicly marketing them.

But Hanna had much more to say about how he believes NAR’s MLS rules have harmed brokerages that are trying to innovate during a tough housing market and compete against consolidating rivals with public money behind them.

He mentioned not just CCP, but also Internet Data Exchange (IDX), which allow agents and brokers to display each other’s listings on their websites so that consumers have access to a comprehensive set of listings in a market, and Virtual Office Websites (VOW), which allow agents and brokers to display certain listing information if consumers register on their websites.

Hanna told Inman he’s considering leaving NAR and its MLSs, and Inman drilled down on why.

This interview has been edited for length and clarity.

Inman: You’ve obviously been a part of NAR for a long time, so what is it that is now making you rethink that?

Hoby Hanna: Because they sold the industry down the river on the lawsuits and didn’t protect all their members. We, as an individual broker, are tied up in a lawsuit based upon NAR saying here’s how MLSs had to work and putting dictates and even creating Clear Cooperation to begin with and other items which we voted against as a company and as a member.

Do you know of any other big brokerages like yourself that are thinking this way?

I couldn’t believe that a big broker anywhere isn’t thinking this way or feeling this way today. And I think NAR knows that. I’m a believer that there should be a shared database and that in different markets, the brokers should share and know what’s for sale. But putting rules like IDX and VOW rules in place across the country wasn’t necessary, and coming back and putting Clear Cooperation in place when most MLSs, they worked well. There might have been some bad apples, but they took care of themselves.

Clear Cooperation has obviously been very controversial, and it sounds like you’re very against it. Is there a particular reason why?

I think it limited creativity on how somebody markets the home. Clear Cooperation came out of people’s fear that different brokers were doing unique things with their properties [and] with the technology.

IDX opens a role where the MLS is in a B2B situation because now everybody can put each other’s listings all over their website. That’s fine, but there’s companies that are set up to sell our listings [and] they don’t have any listings. They’re monetizing their business off of us [and] our agents procuring the listings.

In the Buffalo, New York, MLS, it was 300 firms last year that didn’t sell a house … but they have websites that our listings are all over. If a customer went there, who are they talking to? What is that person representing about that listing? Are they saying it’s fairly priced, or saying it’s overpriced? Are they giving good representation? I think this industry went too far saying we have to be able to put data on everybody else’s sites, that it has to be clear for everybody.

This is a silly reaction … as opposed to saying, “Hey, local MLSs, if you don’t have good rules and regulations, clean yourself up and don’t make it a national thing.”

As far as this new policy, it sounds like you’re saying it didn’t really go far enough.

They should have killed Clear Cooperation.

The backers of the Clear Cooperation Policy say that big brokers who don’t want the policy are only out for their profits and they want to double-end deals and that all these things with exclusive listings are going to lead to a fragmented market where consumers have to go to multiple different websites to see all the listings that are for sale and they have to call up each brokerage to get a full picture. What do you say to those criticisms?

We still want to cooperate, but we want to make sure that customers who are choosing to sign a contract to work with Howard Hanna are knowing about the Howard Hanna listings from the source quicker, sooner, earlier.

I go back to the criticism of “the bigger brokers want to make more money.” Well, it is why we’re in business. I don’t see that as a criticism. This is still a capitalistic society. Isn’t that why they’re in the business to figure out how to grow and make their business more profitable? That criticism I’ve never quite understood.

I think the idea is that it’s making profit at the expense of consumers. I guess it depends on your attitude toward dual agency and whether you think that’s in the best interest of consumers, but also the idea of consumers being able to see all of the listings in a market and the agent not being able to restrict the listings to just their own circle of people who are likely to be like them.

Where do you go today to see all the listings on the market?

Zillow, Redfin, sites like that, Realtor.com.

You don’t see the exclusives.

Right, so [NextHome CEO] James Dwiggins’ argument is basically that yes, because the exclusives exist, then that is fragmenting the market, and that’s not good for consumers.

If you go to Zillow, which doesn’t operate a brokerage firm that I know of right now, that has agents paying to get the leads, and the consumer finds a listing, clicks on it, and they get an agent from … a ZIP code from two counties away. Is that a good consumer experience? And for the seller, is that a good consumer experience?

If everything is at Zillow, why does it have to be at the brokerage firm that happens to belong to an MLS that has never sold a house in the market?

I think when we mandate rules, we take away creativity. The creativity is gonna come in because Rocket’s gonna change the game with Redfin. And Zillow’s gonna make rules that change the game. Those of us who have been in this real estate brokerage business trying to do a really good job and don’t have everybody’s publicly-traded money behind us, we’re trying to be innovative and be creative and grow our businesses, and somehow creativity is getting penalized.

I want to drill down on exactly what you might be changing. You mentioned Howard Hanna is considering moving to registration in all markets. Any timeline on that particular decision?

Not right now. What I believe we’ll probably end up doing with our site is figure out that better registration experience as a consumer but still allow people to search without registration for those who are just beginning, but make sure they know throughout the online experience that you get maybe better value options, programs, systems, by registering.

We’re going to see how markets change over the next couple of quarters.

You mentioned potentially leaving MLS, leaving NAR. When should I check in with you about that?

It’s challenging enough in the housing market, low inventory and interest rates being higher than necessary, and now who knows what’s going to happen out of tariffs. As an industry, everything from the DOJ [Department of Justice], from the [Sitzer | Burnett] loss in Missouri, it’s all tied to the National Association of Realtors’ “rules.”

And now, even though a customer signed a contract to work with Howard Hanna, they can’t know about your listings before people who didn’t.

Am I leaving tomorrow? No. But I am sitting back and saying NAR has to get its house in order. NAR has to focus on what they do best, which is homeownership advocacy. And I’ll sit back and watch a little bit and see how it plays out.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Daniel Houston | May 5, 2025 | Industry, News Feed

Many brokerage professionals say they’re concerned about the economy. They’re just not expecting it to hit their client pools quite yet, the latest Inman Intel Index survey results suggest.

This report is available exclusively to subscribers of Inman Intel, the data and research arm of Inman offering deep insights and market intelligence on the business of residential real estate and proptech. Subscribe today.

For the broader economy, the last month has been a disorienting whirlwind.

Sweeping new tariffs were announced on U.S. imports, then some were paused. A trade war with China ramped up to fever pitch. And stock prices plunged, then recovered as investors sifted through financial numbers and hung on policymakers’ every word.

But for the brokerage business, the waters have remained relatively calm, for now.

The uncertainty roiling financial markets has yet to infect agents in their assessment of their current client pool or their business prospects for the year ahead, according to the latest update to Intel’s Client Pipeline Tracker metric.

Still, agents who responded in late April to the Intel Index survey affirmed that their buyer client pools were thinner in the spring than they had once hoped. Their expectations for future revenue growth have also moderated over the past three months.

- The share of agent respondents who said their buyer pipelines are healthier than last year’s has slipped from 55 percent in January to 44 percent in April.

While the overall outlook by agents is less bullish than it was to start the year, agents in late April weren’t anticipating a broad downturn in an already depressed housing transaction environment.

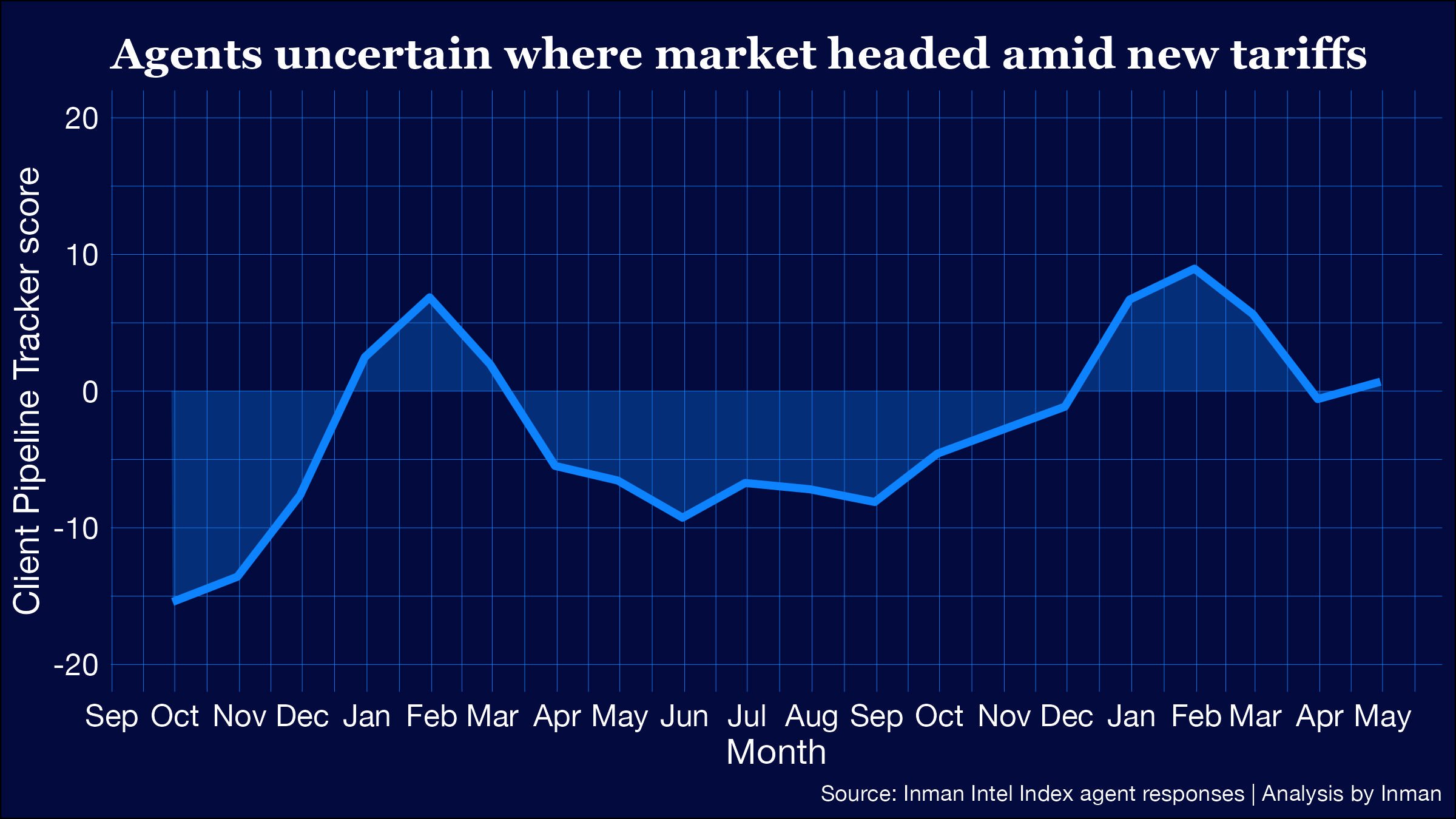

Client Pipeline Tracker score in April: +1

- Previous score: -1 in March

- Recent high point: +9 in January

Chart by Daniel Houston

But under the surface, Intel’s surveys reflect that agent expectations may be shifting — just in one direction for their buyer clients, and a different one for sellers.

Intel explores these complex dynamics in more detail in its latest Client Pipeline Tracker report.

A buyer-seller split emerges?

Intel’s Client Pipeline Tracker is a compilation of how agents feel about their buyer and seller pipelines — both over the past year and in the near future.

Intel described the methodology in this post, but here’s a quick refresher on how to interpret the scores.

- A score of 0 represents a neutral period in which client pipelines are neither improving nor worsening.

- A positive score reflects a market in which client pipelines have been improving, or are widely expected to improve in the next 12 months. The higher the rating, the more confident agents are in that conditions are moving in a positive direction.

- A negative score suggests client pipeline conditions are worsening, or are widely expected to get worse in the year to come.

An extremely positive combined score falls somewhere around the +20 mark. This type of score would signify that much of the industry is in agreement with the fact that pipelines are improving and will continue to improve.

An extremely negative combined score, on the other hand, falls closer to -20. That’s a bit lower than where the industry stood in September 2024, the first time Intel surveyed agents about their pipelines.

For each of the four individual components that go into the score, results as high as +50 or as low as -50 are sometimes observed.

Here are the component scores from the most recent survey, and how each sentiment category changed from the previous one.

Tracker component scores

March → April

- Present buyer pipelines: -22 → -27

- Future buyer pipelines: +5 → +5

- Present seller pipelines: -8 → -3

- Future seller pipelines: +8 → +13

The big takeaway this month: Recent market swings since the beginning of April appear to be further decoupling agent outlooks for buyers and sellers.

As discussed, buyer pipeline scores trended down from March to late April. But at the same time, some agents appear to be gaining in optimism about their prospects for nabbing new listings.

- The share of agent respondents who told Intel they had observed “significant” year-over-year improvements in their seller pipelines jumped from 4 percent in late March to 9 percent in late April.

- Optimism for future listings also grew from month to month. Nearly 43 percent of agent respondents said they thought they would see growth in listing pipelines, up from 37 percent the month before.

The potential explanations for this growing gap between buyer and seller outlooks are complex.

If some agents expect present uncertainty may tilt the economy into recession, that could bring about reductions in mortgage rates and possibly force sales of distressed properties — both of which could free up some new inventory that hits the market.

But recessions have also historically reduced incentives for homeowners to list. Falling sale prices and the expectation of fewer buyers often persuade would-be sellers to remain on the sidelines.

Regardless of the effect on new listings, agents are clearly lowering their expectations that there will be enough buyers to spur a true transaction rebound, at least in the next few months.

The recovery that wasn’t

While the circumstances are different, many agents appear to be experiencing a case of deja vu, Intel survey results suggest.

For the second year in a row, real estate agents opened the year with cautious optimism for the trajectory of their client pools.

And for the second year in a row, they’ve had to tamp down these hopes while their brokerages muddle through another period of uncertainty in the broader economy.

And make no mistake, agents are concerned about the broader economy.

- In Intel’s survey in late April, 3 in 4 agents and 2 in 3 brokerage leaders said they were “concerned” or “very concerned” about the U.S. economy right now.

Throughout much of 2024, this caution deepened into outright pessimism as agents grappled with the implications of new settlement rules and rate cuts that kept getting pushed out into the future.

So far in 2025, agents expectations appear to just be stuck in neutral. Intel will continue to closely follow changes in brokerage sentiment as the year progresses.

Methodology notes: This month’s Inman Intel Index survey was conducted April 17-May 2, 2025, and had received 426 responses as of Friday morning. These results are preliminary and may be revised. The entire Inman reader community was invited to participate, and a rotating, randomized selection of community members was prompted to participate by email. Users responded to a series of questions related to their self-identified corner of the real estate industry — including real estate agents, brokerage leaders, lenders and proptech entrepreneurs. Results reflect the opinions of the engaged Inman community, which may not always match those of the broader real estate industry. This survey is conducted monthly.

Email Daniel Houston

This post was originally published on this site

by Amy Chorew | May 5, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

You may be thinking, “I haven’t finished my payment plan for my 2024 taxes, so why should I worry about 2025 and 2026?”

True confession, I am in the same boat, but based on over 35 years of experience, this is the best time to set up a tax plan for 2025. Also, if you are interested in fiscal fitness, we can show you how to incorporate this strategy into your 2025 business and personal wealth plan.

Are you interested now? If yes, keep on reading.

Tax planning is most effective when you understand it’s a strategic, evolving process that requires you to think ahead, especially when policy changes are on the horizon. Effective Jan. 1, 2026, the Tax Cuts and Jobs Act (TCJA), which went into effect in 2018, might expire, and with it, the potential reversion to the 2017 pre-TCJA tax rates.

What could be the effect on you? Higher taxes in 2026. We will explore five thoughtful strategies to help you take advantage of the lower 2025 rates and if the 2026 rates increase, how to make strategic decisions to optimize them.

1. Understand the changes

What’s changing?

The current tax framework under the TCJA is temporary. Several of its key components — lower individual tax rates, higher standard deductions and special credits — might sunset or revert by Dec. 31, 2025. For instance, consider:

- Tax brackets: Once the TCJA provisions lapse, expect higher tax rates for high earners. The top individual rate may jump from 37 percent to pre-TCJA levels around 39.6 percent.

- Deductions and credits: The expanded standard deduction and enhanced child tax credit will likely shrink. Your current tax planning might have been optimized for today’s generous deductions, so adjusting your financial habits is essential.

If you itemize, you may be excited to get the Salt deduction back; if you do not itemize, the current standard deduction is better for you.

Deep thinking

Ask yourself how these changes impact more than just your annual refund. Reconsider the timing of major financial moves in light of this broader economic reset. In plain language, what can you do?

To take advantage of the lower 2025 rates, think about accelerating income from 2026 into 2025.

Think about taking advantage of maximizing contributions to a retirement plan during 2025 to shelter that accelerated income. Talk to your tax preparer; sometimes, you can defer funding a retirement plan contribution for 2025 until Sept. 15, 2026.

Consider additions to your real estate investment portfolio if you have extra cash.

If you are going to have a lower income in 2025, consider converting funds in a taxable IRA to a Roth IRA. This creates some taxable income now, but it is at lower rates, and after you have your Roth set up for five years, at age 59 1/2, you can start drawing from the Roth tax-free.

On the expense side, if your business entity is an S Corporation or an LLC consider the use of the Pass Through Entity Tax. (Useful if you are in a high state income tax state).

If you are charitable, consider setting up a Donor Advised Fund to shelter some of that accelerated income.

Please note: This is not tax advice.

Discuss these and other personalized ideas with your tax preparer now. As your year progresses, revisit some of the ideas you are thinking about taking. You need to begin implementation no later than October 2025 to have enough time to set things up.

Next up, how to get more deductions with organized financial records.

2. Reassess and organize your financial records

Get a real-time picture

A solid tax plan begins with immaculate record-keeping. This means not only tracking receipts, pay stubs and investment statements, but also understanding the context behind every transaction.

- Digital tools and analysis: Invest in tax software or professional apps that offer real-time insights. Automated categorization and alerts can help you avoid last-minute scrambles when policy changes take effect.

Deep thinking

Beyond organization, this is about creating a financial narrative. How do your daily expenses and sporadic income events weave into your broader financial strategy? A detailed audit of your books might reveal trends, like recurring deductible expenses, that you can optimize for maximum tax efficiency in a changing environment.

3. Reevaluate life changes and their tax implications

Life’s big moments

Whether it’s marriage, divorce, having a child, buying a home or switching jobs, life events directly affect your tax picture.

- Marriage/divorce: These events can change your filing status, eligibility for certain deductions and even the timing of income.

- New homeownership: Mortgage interest deductions could shift in priority if tax benefits shrink or vanish.

Deep thinking

Beyond the immediate monetary impact, consider the long-term fiscal life design. How might these changes interact with a future of higher tax rates or a smaller standard deduction? Develop a narrative that connects today’s events with tomorrow’s fiscal responsibilities — possibly altering long-term plans such as retirement savings or education investments.

4. Strategize on income, deductions and timing

Take control of your numbers

With the possibility of future tax rate increases, consider these strategic adjustments:

- Accelerate income where beneficial: If you anticipate higher tax brackets later, pulling forward income into 2024 or early 2025 could preserve lower tax rates.

- Time your deductions: Align deductible expenses — like charitable contributions or mortgage interest payments — with the timing of these tax changes to maximize their benefit.

- Consider Roth conversions: Converting traditional IRA assets to a Roth IRA while tax rates are still comparatively favorable can lock in your lower rate. The long-term growth potential in tax-free accounts can be a compelling benefit if legislation changes in the future.

Deep thinking

Think of tax planning as dynamic chess rather than checkers. Each decision — from accelerating income to timing deductions — should factor in not only today’s tax code but the likely future environment. Contemplate your “tax timeline” in the context of an evolving economy and be willing to adapt your strategy as laws change and your personal finances mature.

5. Stay engaged with policy developments

Knowledge is power

Tax laws are subject to ongoing debate. In addition to preparing for known expirations under the TCJA, keep a finger on the pulse of legislative changes:

- Monitor reliable sources: Follow updates on the IRS website, financial news outlets or subscribe to tax policy newsletters.

- Consult professionals regularly: A knowledgeable tax advisor can offer real-time insights and help pivot your strategy as new policies emerge.

Deep thinking

Evolving policies can be both risks and opportunities. View your financial plan as a living document — one that adapts to the economic environment. Embrace a mindset of continuous learning, and consider attending workshops or webinars to better understand possible future tax scenarios. This proactive engagement not only mitigates unforeseen costs but might uncover innovative tax-saving strategies that can enhance your overall financial well-being.

Preparing for 2025’s tax changes is more than ticking boxes on a to-do list — it’s about reshaping your financial strategy to align with a shifting economic landscape. By understanding the evolving policy framework, organizing your financial records, reassessing life events, strategically timing income and deductions, and staying informed, you create a resilient fiscal plan capable of weathering legislative changes.

Remember, while no one can predict the future with absolute certainty, proactive measures today will empower you to make confident, informed decisions tomorrow. As you rebuild your tax strategy for 2025, explore new avenues for saving, consider deeper adjustments to your long-term financial plan, and always be ready to engage with the complexities of an ever-changing tax system.

Further considerations

- Scenario planning: Map out different “what if” situations to see how various life events intersect with future tax scenarios.

- Long-term strategy sessions: Consider regular reviews with your financial advisor, creating a quarterly routine to reassess goals, review legislative news and adapt your plan.

- Tech and tools: Evaluate new technologies that offer predictive insights on legislative changes to stay ahead of the curve.

By diving deeper into these strategies, you not only safeguard your finances but also build a more informed, agile approach that could serve you for decades.

What are your thoughts on aligning your personal financial narrative with these impending changes? Feel free to share your experiences or questions on navigating these complexities.

Amy Chorew is an active Realtor involved in investment properties and listing well-staged homes in Connecticut. Connect with her on LinkedIn and Instagram.

Maeda Palius has been a practicing CPA for 40 years, focused on helping small and medium enterprises become more profitable and help the owners grow personal wealth. Connect with her on LinkedIn.

This post was originally published on this site

by Zillow | May 5, 2025 | Industry, News Feed

Even in today’s digital world where listings, 3D tours and market data are just a click away, it’s the agent who brings clarity, confidence and irreplaceable value for consumers.

We’re always learning from top real estate agents, exchanging insights on how they operate, drive success and grow teams. Through these conversations, we’ve discovered five strategies that consistently provide the perfect mix of tech and human touch that set agents apart.

1. Balance digital efficiency with personal connection

Despite the industry’s digital transformation, Zillow research shows 89 percent of sellers consider agents their most valuable resource — above websites (75 percent) or apps (64 percent). Personal connection remains essential, especially during emotional and complex transactions.

Tip: Use technology for routine tasks and data management, freeing your time for meaningful client interactions. Follow Up Boss CRM can help you deliver personalized experiences. The Smart List feature prioritizes client lists so you’re reaching out to those most likely to move at the right time. The Call Transcripts and Summaries AI tool automatically records and transforms every call into clear, actionable summaries with next-step suggestions.

2. Share personalized market insights

While it’s relatively easy for consumers to get their hands on raw housing market data, they need an experienced agent who can interpret this information for their specific situation and goals.

Tip: Create personalized market analysis reports that go beyond public stats. Develop neighborhood-specific insights or community changes that might affect long-term property values.

3. Win more listings with a premium digital experience

While relationships are important, buyers and sellers want an agent who uses technology to their advantage. Our research shows 71 percent of sellers are more likely to hire an agent who includes virtual tours and interactive floor plans in their services.

Tip: Zillow Showcase can help you win more listings in your market. Our data shows Showcase listings are 10 percent more likely to go pending within 14 days compared to similar typical listings on Zillow. They also sell for 2 percent more, a bonus of more than $7,000 on the average home. Showcase can help you develop a consistent visual brand across your listings to distinguish and elevate them.

4. Develop a compelling online presence

Buyers and sellers often research agents online before reaching out. A strong digital presence on social media and real estate websites helps them get to know you.

Tip: Start with a complete Zillow agent profile to highlight your expertise and personality. Agents using Zillow Showcase can add social media handles to their profile and incorporate Zillow Media Experts services, which create professional agent reels featuring you and your listings — optimized for video-centric platforms. These tools help build trust and demonstrate tech-savviness to potential clients.

5. Build trust

Consumers have told us trustworthiness and market knowledge are more important than an agent’s sales record. Positive client reviews consistently highlight agents “exceeding expectations,” “had my best interests at heart” and providing “exceptional service.”

Tip: Ask deeper questions about clients’ life goals. Create an “above and beyond” checklist for each client, identifying three unexpected ways you can deliver exceptional value.

The future of real estate excellence

Agents who combine technological efficiency with personal connection will consistently outperform. We’ve found the most successful agents serve as advisors who bring calm to uncertainty and strategy to major life decisions.

For those looking to stay ahead of the curve, don’t miss Zillow’s Unlock Conference this November. With your success at the center, this unique experience will help you make progress on your business goals — delivering tangible strategies, actionable next steps and valuable connections.

This post was originally published on this site