by Rachael Hite | Jun 5, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

I’m exercising my freedom of speech by writing about the National Association of Realtors’ insistence that their review of potentially changing the Realtor Code of Ethics, which passed intact through committee in preparation for a vote Thursday, is less about Trump’s presidential policy against DEI and more about a drop in revenue, membership and potential future legal battles.

Because let’s be real, that is what’s being pushed back on here. Privileged agents want an exception, a free pass, a Get Out of Jail Free card to do what they want to do, without suffering professional consequences.

NAR wants membership dues to cover its debts, and also wants to ensure that it’s not responsible for the actions of agents under the brand, as it can no longer afford the risk of carrying such a low professional threshold for licensing and poor training, and the results that it produces.

To increase membership numbers, NAR needs to make it more appealing to be a Realtor. And who wants to be a Realtor and pay dues if there are so many rules to follow? Sales is hard enough; let’s remove some barriers and get things cranking like it was 2006 and sell, sell, sell. Who cares about how it’s done? We need to get this train back on track.

The message is that NAR is willing to change its beliefs on DEI because the current state of membership is so chaotic and filled with liability that it’s willing to compromise its Code of Ethics to stay in business.

So, the trade group will continue to offer Code of Ethics training, but perhaps now, it will look the other way and not enforce it. What is the end goal here?

Past is prelude

In 2000, NAR was focused on many of the issues that remain in the spotlight today: fair housing, affordability and affiliated business agreements to ensure consumers had transparency in pricing and who was profiting, laying the groundwork for the founding of the Consumer Financial Protection Bureau.

Essentially, NAR was focused on protecting the interests of the consumers because unfair business practices and happenings were still rampant in the industry.

Since 2000, NAR has failed to address many of the problems it set out to resolve over the past 25 years. Fair housing and fair appraisals remain issues, and transparent commissions continue to be a concern, sparking daily heated arguments. Now, thanks to a series of lawsuits, the public trusts real estate agents less than ever before.

The CFPB is under attack by the current administration, and to make things even more fun, additions to the Code of Ethics that were made during the pandemic to protect consumers, along with DEI and other serious issues, are under the lens because some Realtors feel that their freedom of speech is being violated if they face professional and financial penalties from grievances filed against them under 10-5.

Thoughts and prayers for those against 10-5

I’ve prayed more than I ever have in my whole life recently, and I’ve had a tough road with religion from childhood. My frustration is that this world is a very broken and scary place.

So many people do not have a “fair” or “equal” chance; the playing field is not the same for everyone, and we all don’t have the same tools or skills or even opportunities given to us based on where we grew up, who raised us, physical health, mental health, and modern culture and politics.

I pray for the folks who use their religion as a weapon and an excuse to judge, hurt or oppress marginalized groups and the less fortunate, and that their ignorance or delusion is creating a world that is even less welcoming for current and future children.

I pray for people who are considering suicide because they do not feel welcome in this world, that they find the strength to stay, and someone who helps them understand that their worth has nothing to do with money, status, who they love or what gender they are.

I pray mostly for empathy and compassion, and especially for those in privileged positions who can help others achieve success. I pray for people to worry about their own lives and stop worrying about how others choose to live. I hope that something in the universe teaches them that diversity is what makes our communities stronger.

However, here’s the thing about thoughts and prayers: They don’t accomplish anything without action. I call my reps, I speak out against hate, and I insist on holding people accountable when they are contributing to the problem and not the solution.

That’s what 10-5 is about. It’s a ribbon of protection for consumers, and some guardrails for maintaining the Realtor brand and upholding the pledge of the Golden Rule. When NAR stepped up and created 10-5, it was because it needed to demonstrate to consumers that Realtors care and would not tolerate discrimination. NAR took action.

If the Code of Ethics doesn’t align with your personal beliefs and religious beliefs, then perhaps you should not be working with the public.

If you struggle to explain how you get paid, why you get paid, and what you charge for your work, then you may not be suited for sales with consumers. It’s just that simple. It’s not an if-then scenario when you work with the public.

The public has the right to know if you are engaging in activities on your personal time that would make them feel unsafe, discriminated against or that you don’t have their best interests at heart. They should be able to research you and know not to work with you.

Finally, even if 10-5 is changed or removed, consumers still have the right to file a grievance against you at any time for multiple reasons. If you are behaving in a way that raises questions, you will likely still be called before your governing board to explain what you were doing to warrant the call or grievance.

That’s what democracy is about. You have the total freedom to participate in and say whatever you want, but the public and the Realtor brand do not have to sit next to you while you do it, nor agree with your agenda.

Rachael Hite is a seasoned housing counselor and thought leader in the real estate industry. Connect with her on Instagram and LinkedIn.

by Spencer Krull | Jun 5, 2025 | Industry, News Feed

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Imagine if we licensed drivers the same way we license real estate agents; our roads would look like a bumper car track.

I remember my first day as a real estate agent, wearing my jacket and tie, sitting at my desk, ready to get to work and thinking, “I have no idea what I am doing.”

To clarify, I had learned the basics of prospecting; I had worked on my scripts for hitting the phones or knocking on doors, and even sitting open houses if another agent would give me the chance. I knew the basics of getting clients. What I didn’t know anything about, however, was what I was supposed to do in case someone answered a door that I knocked on and said, “I’d like to write an offer on the house across the street.”

Practical training is a must

Though I’m a licensed broker in six states, with over 20 years of experience, I still had that same lost feeling each and every time I received a new license. I place the blame for agents’ lack of readiness squarely on most states’ licensing courses and educational requirements.

As an illustration, let’s compare the steps necessary to get a real estate license with getting a driver’s license (something with which I have white-knuckled familiarity thanks to my 16-year-old).

Driver’s license training is “skills-focused.” The coursework focuses on the useful, practical knowledge that a driver will use every day — things like what to do at a stop sign, how and when to signal, and whether or not one can cross a double yellow line to pull into a driveway or parking lot (something that sparks an argument almost every time I go to Costco).

Real estate license training is much more scattered. For instance, instead of simply teaching that discrimination is illegal and providing a list of protected classes and people, real estate training and testing is equally focused on things like when different civil and housing rights acts were passed.

When a HUD tester shows up asking if the owner will rent to a person of color, I think it’s more important that an agent knows to say, “Of course,” and not “The first civil rights act was passed in 1866, but was undermined by the 1896 Supreme Court decision in Plessy v. Ferguson … ”

History is great, I love history, but when approaching a stop sign, I thank the DMV that my son knows to apply the brakes instead of looking at me and saying, “In 1954, the Federal Manual on Uniform Traffic Control Devices required that all stop signs must be red and octagonal.” (I would hazard a guess my insurance company is thankful, as well.)

We need traditional blackbelts

A karate instructor once told me that traditionally, students didn’t go out and buy darker and darker belt colors as their skills grew; rather, they wore the same belt, which started off white and darkened over time with experience. When it comes to real estate, it seems many agents “buy” a black belt as soon as they get their license, without having or seeking any practical experience.

On the other hand, the aspiring driver gets their white belt when they pass the written test and starts to “darken their belt” with practical experience behind the wheel (with an experienced driver ready to grab the wheel one seat over).

It’s not until the novice driver has attained a degree of road competency that they are allowed to take a practical driving test, and upon passing, get to give their parents mini heart attacks any time they hear anything that vaguely sounds like metal hitting metal.

Which licensee is better prepared?

Who’s picking up the slack on training?

That lack of actual skills-based education in real estate puts the burden of training on brokerages, and not all brokerages are created equal or up to the task. A friend from my licensing class went to a brokerage that provided her a mentor who drilled her on paperwork and procedures through practice listings, offers, counteroffers and repair requests.

My first brokerage paired me with a mentor who hadn’t done a deal in quite a few years and was more concerned with whether the coffee was fresh or from that morning, instead of whether contingencies were removed actively or passively. (Oh, and she got that one wrong on my first deal, and I was nearly sued.)

Inexperienced karate students and drivers can cause serious physical damage; inexperienced agents can cause serious financial and even civil damages that affect their clients, themselves and their brokerages.

Before getting a license, plumbers and electricians are required to undergo vocational training and years of apprenticeship; I am grateful for this system whenever I flush a toilet or turn on a light switch (especially if the light switch is in my bathroom).

With so much at stake for a client buying or selling a home — something which is, more often than not, the largest and most significant financial transaction of their lives — I think the public deserves better than “off-the-shelf blackbelts.”

If departments of real estate across the country were serious about their mission to protect the public, they would align licensing education and certification with actual practice in the industry. There would be tests on skills or mandated apprenticeships, and continuing education for renewal would reinforce these skills.

But for now, I guess we’ll settle for tests that require an agent to know how many square feet are in an acre (43,560), or what year the Americans with Disabilities Act was passed (1990), instead of knowing how to write a counteroffer properly.

Writer’s note: The opinions in this article represent the author’s opinions and do not reflect those of Side.

Spencer Krull is a managing broker with Side, and also works as a real estate expert witness and consultant for attorneys.

by Carl Medford | Jun 5, 2025 | Industry, News Feed

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

With buyer loyalty down and deals harder to ink, buyer agents need to up the ante if they wish to finish 2025 on a successful note.

It has been a tough year so far for buyer agents: Not only have the rules for buyer engagement morphed and shifted over the past year, but we are still dealing with inventory shortages, high interest rates, potential tariffs, significant shifts in the stock market, declining consumer confidence and more.

All of this has resulted in indecisive buyers who, if not properly nurtured, can turn on a dime and engage in an “out-of-the-blue” real estate transaction that excludes the agent who assumed they would be the “go-to” representative.

Although there is no guaranteed method of ensuring buyer loyalty, there are processes that will help increase the odds. Here are our recommendations:

1. Insist on a mandatory buyer consultation

Regardless of how you connect with a potential buyer — whether at an open house, internet lead, referral and so on — you need to help them understand that a mandatory consultation is critical for getting the homebuying process started.

We ask potential buyers to commit to a consultation that will typically last between 60-90 minutes. Because you only want to work with clients who are actually motivated to buy a home, if they refuse to meet, that is a signal that they are not the type of client you will want to represent. Rather than go into detail about what constitutes an effective buyer consultation, you can click here for a complete outline.

2. Demonstrate your value

Real estate agents, unfortunately, are now viewed as a commodity or even a necessary evil instead of skilled advocates such as attorneys or accountants. This slide in confidence has been dutifully earned, as aptly demonstrated in conversations surrounding the industry’s commission lawsuits. With a substantial percentage of agents doing little or no business, agent professionalism has taken a serious hit.

When something or someone is viewed as a commodity, the goal is to obtain their product or service as cheaply as possible.

If buyer’s agents wish to demonstrate their value and rise above the herd, this can be done in three ways:

- Have a written value proposition that clearly articulates your value.

- Have a number of client testimonials and references you can provide to a prospective client that will validate your value. Ironically, people will believe a third party they have never met more than they will trust a person sitting in front of them.

- Tell stories of past issues you have successfully resolved. While people may appreciate a written value proposition, a story will help connect to their emotions and, at the end of the day, people commit with their emotions more than logic.

3. Complete an exclusive buyer-broker agreement

If you do not have a signed buyer-broker agreement, then you have nothing. Because an agreement is now required in our state to show a single property to a prospective buyer, buyers are beginning to understand the need for formalized representation. Although some are refusing to sign and are utilizing open houses as a way to vet properties, there is growing acceptance among buyers to sign a representation agreement.

How that agreement is filled out, however, is everything. As soon as the realization occurred that buyer-broker agreements were going to become mandatory, we began training with scripts designed to overcome potential buyer objections. Like anything else, conversations concerning representation agreements have to be practiced to ensure success.

Although it’s relatively easy to get a buyer to sign an agreement to view a single property, the goal is to establish a meaningful and exclusive relationship with a buyer that will permit you to work on their behalf for as long as it takes to get them into a home and secure appropriate compensation for yourself.

4. Connect the buyers with a reputable lender

Although we will work with any lender the buyer chooses, not all lenders are created equal. Ideally, connect them with your in-house lender so you can monitor their progress more effectively. The lender will help determine their creditworthiness, verify deposits for down payments, confirm their ability to borrow and establish limits.

Once this is done, they will produce a pre-approval that includes the parameters you will need to know to set up property search parameters effectively. We will not show homes to buyer clients who are not pre-approved, nor will we set up tours for properties that are above their pre-approval limits.

5. Set up buyers on your app

Buyers have a habit of looking at homes in places that may not be helpful to you as their agent. Unless you actively work on setting them up for successful communication, you have no right to be surprised when they go off in a different direction and, depending on how your buyer-broker agreement is written, ink a deal with someone else.

To shift things in the agent’s favor, your clients should be directed to use your app. A robust app will not only be branded to the agent but also will link directly to local MLSs and provide full access to all available listings and notify the agent of the buyer’s activity, favorites and more. This knowledge makes it much easier for the agent to interject themselves into the process and proactively set up showings for homes the buyers have liked.

Further, in the case of robust CRMs, agents can:

- Set up customized property searches and market alerts for their clients based on their preferences (price, size, location, features and more). These apps frequently provide real-time access to MLS data, often more up-to-date than public portals, such as Zillow, Realtor.com or Homes.com.

- Have automated real-time communication and updates when new listings go live or when a listing they are following has a status change (price adjustments, open houses, etc.). Not only does the buyer receive the alerts, but their agent does as well, helping streamline communication and respond immediately to a buyer’s needs.

- Showing coordination. Depending on the app, agents can manage showings directly within the platform, so buyers get timely and efficient viewing opportunities.

- Collaboration and notes. Buyers and their agents can collaborate on favorites, leave notes and rate properties, which makes it easier to narrow down choices and stay organized.

6. Communicate, communicate, communicate

Do not make the mistake of setting your clients up on auto feeds and then waiting for them to communicate. If you have set them up with your app, then you can monitor their activity and reach out continuously to provide additional information, schedule showings and more.

7. Actively look for opportunities

Many agents in the past have been willing to let their buyers do all the work: They would set them up on autofeeds and then wait for them to raise their hand when they found something they liked. Agents that want to succeed in the current market are going to have to raise the bar.

Activities include the following:

- Go with your buyers to open houses they want to visit. Although some agents consider this a waste of time and effort, smart agents will understand that there is no difference between an open house they attend with their client and a private showing; each one is an opportunity to gauge your client’s interest and proactively act. If you are not with them when they see a home they like, you will be left guessing and may miss an opportunity to write an offer. Ironically, if they like a home they visited without you, you will need to go to the property anyway to represent them effectively.

- Take your clients to new builders. Do not wait for them to go on their own — if they drive by a builder’s development and sign anything without you present, your chances of getting a commission will be dramatically diminished. Even if your buyers state upfront that they are not interested in new homes, a quick tour of local builders may be all they need to ink a deal.

- Actively seek off-market opportunities. Many buyers want to live in a specific neighborhood due to access to local schools, commute, proximity to family, neighborhood amenities and so on. If no homes are available, then strap on your walking shoes, hit the streets, and knock on every door in that neighborhood that meets their criteria. You can also send out Golden Letters explaining your client’s need to live in that neighborhood. I am not advocating any brokerage practices or private networks that would violate the intent of the Clear Cooperation Policy: I am talking about buyer agents going out and actively looking for homes that might meet their client’s needs – properties that might otherwise not have gone on the market.

Times have changed, and if any given buyer’s agent wishes to succeed, they need to adapt to meet the new realities. Whereas markets in the past were significantly easier to navigate, actual work is required in the current market, and those who understand this and are willing to roll up their sleeves and dig in will be the ones who will ultimately build a successful business.

by Debra Trappen | Jun 5, 2025 | Industry, News Feed

Debra Trappen’s series continues with inspiration for getting back in touch with the work that lights you up and renews your motivation.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Welcome to Lead with Fire, A Soulful Series for Real Estate Game-Changers. This is more than business advice — “Lead with Fire” is a transformative series created for the soulful, visionary humans in the real estate industry who are done with the old playbook and ready to redefine success on their own terms.

The secret to success isn’t doing more; it’s staying lit up.

There was a moment when I realized the cost of playing it small was slowly killing me from the inside out.

I was doing work I loved. My values, passion and purpose all aligned — check, check, check. The problem? The people I was working with had a different agenda.

They didn’t want all of me. They wanted the “palatable” version. They wanted to dull my voice, shrink my presence, and rework my vision into something … safer. Directionless, yet controlling. Hollow, yet somehow demanding.

I fought it. I kept showing up. Kept trying to make it work. Until one morning, I realized I had slipped from flow into force.

I was exhausted — physically, mentally and spiritually. The drama drained me. The lack of vision, combined with vanilla feedback, drained me. The pressure to contort and conform drained me.

And then — a spark. The moment I made the decision to leave, the light returned. The fire that had dimmed came roaring back. My energy returned because I returned to myself.

Energy is everything

In a world obsessed with productivity, most people are taught to manage their time. When you’re building a life and business rooted in purpose, managing your energy is the real flex.

Your energy is sacred. It’s your fuel, your currency, your lifeforce. When you know what drains it and how to protect it, you unlock a new level of freedom and power.

Let’s get real about energy drains

Sometimes, it’s obvious. Late nights. Back-to-back meetings. Hustle without rest.

Other times, the most significant energy leaks are more subtle:

- Saying yes when your intuition says no

- Silencing your voice to keep the peace

- Over-giving and under-receiving

- Staying in places you’ve outgrown

- Holding back to make others comfortable

Energy management is about alignment, not avoidance. It’s doing what matters most to you.

Reignite your fire: Your energy rituals

Just as drains exist, so do boosters. Protecting your fire means having daily practices that nourish you and bring you back into alignment.

Consider weaving these into your day

- Boundaries that honor your bandwidth

- Quiet time that reconnects you to your inner wisdom

- Movement that energizes instead of depletes

- Creative time that lights you up from the inside

- Soulful conversations that make you feel seen

Reflections journal prompts

Let’s bring this to life. Take a few moments to reflect and journal on the following:

- What (or who) is draining my energy the most lately? Why am I still giving it my time, attention or power?

- What consistently replenishes me, even in a busy season? How can I create more space for that nourishment?

- Where have I been forcing instead of flowing? What would shift if I softened or surrendered?

- What boundaries would protect my energy and creativity right now? What am I available for — and what am I lovingly releasing?

- How do I want to feel at the end of each day — and what needs to change to honor that? Let that feeling guide your choices and your calendar.

It’s not just self-care — it’s self-leadership

When you protect your energy, you protect your vision. You protect your ability to show up, to lead, to create. You shift from surviving to shining. From pushing through to moving in flow.

Your fire-protection invitation

This week, create your own daily energy reset ritual. Something simple. Sacred. Repeatable.

- A few minutes of breathwork

- A morning walk without your tech

- A midday dance break or soaking in the sunshine

- An end-of-day journaling session to release the day

Let it be yours.

Let it be enough.

Let it bring you back to yourself.

Mantra to Lead with Fire:

“My energy is sacred. I choose flow over force and create from alignment, not exhaustion.”

Next up in the Lead with Fire series: How to show up online without selling out

What’s your time, energy and talent really worth? In our next post, we’ll explore the power of saying no, standing in your values and owning your worth — no apologies, no discounts.

Debra Trappen is the founder of the Red Threads Collective, a sacred community for women entrepreneurs. Connect with her on Instagram and LinkedIn.

by Matt Carter | Jun 4, 2025 | Industry, News Feed

While purchase loan demand was still up 18 percent last week from a year ago, some of that demand may not translate into sales, with Redfin reporting an unusual bump in cancelled purchase contracts.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

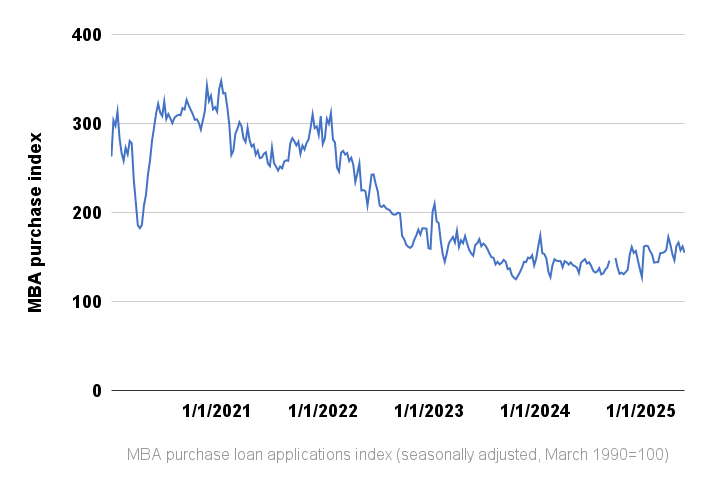

Last week’s dip in mortgage rates didn’t send homebuyers rushing to their lender, with purchase loan applications contracting by a seasonally adjusted 4 percent compared to the week before, according to a weekly survey of lenders by the Mortgage Bankers Association (MBA).

The latest MBA Weekly Mortgage Applications Survey, released Wednesday, found purchase loan demand was still up 18 percent from a year ago. However, some of that demand may not translate into sales, with Redfin reporting an unusual bump in cancelled purchase contracts in April.

The MBA survey showed requests to refinance were down 4 percent during the week ending May 30 when compared to the week before, but up 42 percent from a year ago.

Joel Kan

“Most mortgage rates moved lower last week, with the 30-year fixed rate declining to 6.92 percent and staying in the 6.8 percent to 7 percent range since April,” MBA Deputy Chief Economist Joel Kan said in a statement.

“Refinance activity fell across both conventional and government segments, and the overall average refinance loan size was the smallest since July 2024, as potential borrowers hold out for larger rate drops,” Kan said.

Redfin’s analysis of MLS pending-sales data showed 14 percent of homes that went under contract in April — about 56,000 properties — ended up not selling because their purchase agreements were cancelled.

That’s the second highest share of April cancellations in records dating back to 2017, Redfin said, after April 2020, when the pandemic put the brakes on many closings.

Redfin said purchase agreements are being cancelled at a higher rate than usual during the spring homebuying season due to economic and political uncertainty, a surge of inventory in many markets, and elevated home prices and mortgage rates.

Mortgage rates on the rebound

Since hitting a 2025 low of 6.48 percent on April 4, rates on 30-year fixed-rate conforming mortgages have rebounded above 6.8 percent for most of May, according to lender data tracked by Optimal Blue.

Inflation continued to move closer to the Federal Reserve’s 2 percent target in April, but central bank policymakers have been reluctant to cut short-term interest rates as they continue to assess the impacts of the Trump administration’s policies in areas including tariffs, immigration, taxes and regulation.

Purchase loan demand peaked in April

Even after adjusting for heightened demand during the spring homebuying season, purchase loan requests peaked in April, MBA data shows.

At 155 for the week ending May 30, the MBA’s seasonally adjusted purchase index was at its lowest reading since the week ending April 25. The index is now down 18 points from its 2025 high of 172.7 registered during the week ending April 4, but 27 points higher than a low for the year registered in January.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 4, 2025 | Industry, News Feed

Lifting of the asset cap could give the bank greater leeway to originate jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $806,500 conforming loan limit in most markets.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Wells Fargo has freed itself from a $1.95 trillion asset cap that limited its growth for nearly a decade, with the Federal Reserve Board certifying Tuesday that the bank has put “widespread consumer abuses and other compliance breakdowns” behind it and improved its governance and risk management program.

The Fed imposed the asset cap in 2018, in the wake of a series of scandals, including “cross-selling” practices in which bank customers were enrolled in new deposit and credit card accounts without their knowledge.

“Wells Fargo pursued a business strategy that prioritized its overall growth without ensuring appropriate management of all key risks,” federal regulators said in imposing the asset cap. “The firm did not have an effective firm-wide risk management framework in place that covered all key risks. This prevented the proper escalation of serious compliance breakdowns to the board of directors.”

Tuesday’s lifting of the asset cap “represents successful remediation to the required standard based on focused management leadership, strong board oversight, and strict supervision holding the firm accountable,” Federal Reserve Governor Michael Barr said in a statement. “All three will need to continue for the firm to have a sustainable approach.”

Wells Fargo CEO Charlie Scharf said Wells Fargo is “a different and far stronger company today because of the work we’ve done” to address past problems.

Since 2019, the bank has closed 14 consent orders imposed by regulators over its business practices.

Wells Fargo announced in January that the Consumer Financial Protection Bureau had lifted a 2022 consent order related to a $3.7 billion settlement over the bank’s alleged mismanagement of mortgages, auto loans and deposit accounts.

On May 29, Wells Fargo said it had closed a 2015 consent order with the Office of the Comptroller of the Currency, leaving only the 2018 consent order with the Federal Reserve Board in place.

Wells Fargo has “changed and simplified our business mix, and we have transformed the management team and how we run the company,” Scharf said in a statement Tuesday.

“We have been methodically investing in the company’s future while improving our financial results and profile. We are excited to continue to move forward with plans to further increase returns and growth in a deliberate manner supported by the processes and cultural changes we have made.”

Lifting of the asset cap could give the bank greater leeway to originate jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $806,500 conforming loan limit in most markets. Lenders who make such loans often hold them on their balance sheet, since they’re more difficult to bundle up and sell to investors.

Once the nation’s largest mortgage lender, Wells Fargo was overtaken by direct lender Quicken Loans (now Rocket Mortgage) in 2017 and fell out of the top 10 in the face of regulatory issues, a shrinking branch footprint and rising interest rates.

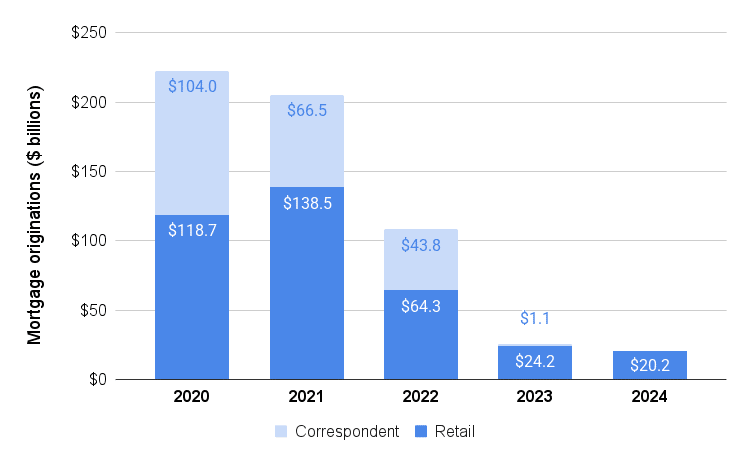

Wells Fargo mortgage originations, 2020-24

Source: Wells Fargo earnings reports.

When borrowers rushed to refinance during the pandemic, Wells Fargo originated $223 billion in mortgages in 2020 — more than 10 times as much business as it did last year ($20.2 billion).

Scharf has said Wells Fargo is “not interested in being extraordinarily large in the mortgage business, just for the sake of being in the mortgage business.”

But theoretically, technology like artificial intelligence employed by the nation’s biggest mortgage lenders — UWM and Rocket — could allow Wells Fargo to rapidly scale its mortgage business despite its reduced branch office footprint and staffing levels.

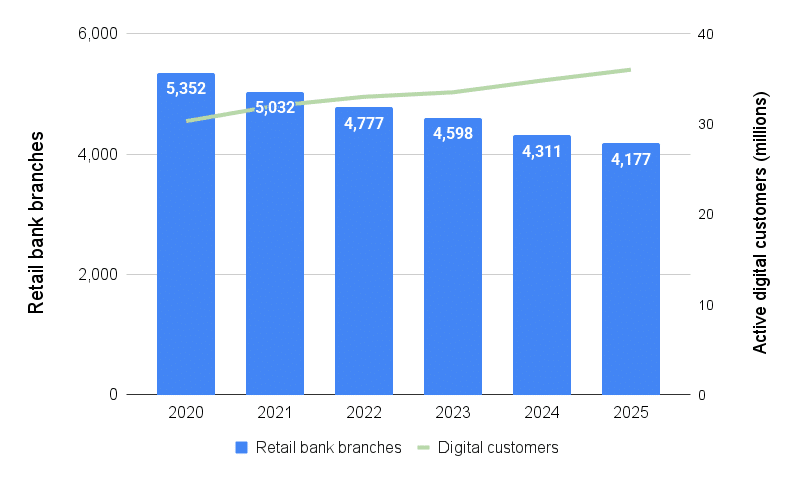

Wells Fargo closing branches, growing digital customer base

Retail bank branch and digital customer count at the beginning of the year. Source: Wells Fargo earnings reports.

Wells Fargo ended 2024 with 4,177 retail bank branches, down 22 percent from 5,352 at the beginning of 2020.

But a growing number of customers — 36 million at the beginning of the year — access the bank online or through mobile devices, up 19 percent since the beginning of 2020.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter