by Jim Dalrymple II | Jun 10, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

There’s Star Trek‘s Data. And HAL 9000 from 2001: A Spacey Odyssey. Scarlett Johansson memorably voiced Samantha, an artificial intelligence assistant, in Her. And the Maschinenmensch from 1927’s Metropolis is one of the most enduring images in cinema, even if most people today haven’t actually seen the movie.

Humans have been inventing machines since time immemorial, but we are perhaps most fascinated by those machines built in our own image. A car or a copy machine or a coffee maker is an object, but an android with a voice or a face? That’s a protagonist.

Recent years have seen an explosion of AI technology. Thanks to tools like ChatGPT and Midjourney, smart and interactive bots that would’ve seemed like science fiction half a decade ago are now commonplace. They’re so common, in fact, that when a panelist at last month’s Inman on Tour Miami asked a room filled with real estate professionals who has used AI, virtually every hand went up.

But the proliferation of this technology has turned an abstract philosophical question into a practical one for numerous companies, including many operating in real estate: How human should our AI assistants actually be?

To answer this question, Inman reached out to multiple real estate technology companies that have built their own AI tools. And while company leaders subscribe to different philosophies, one thing was clear: AI technology is becoming more and more human. In fact, it’s becoming so real-seeming that increasingly, consumers are simply treating it like a person.

Blurring lines between humans and machines

Jindou Lee used to work in video game development, but today he’s the CEO of HappyCo, a company that develops property management technology. Last year, the company unveiled its JoyAI. The tool takes requests from tenants, then helps coordinate maintenance.

Lee has spent considerable time thinking about the humanity of the bot his company has built. And he told Inman that user interactions with JoyAI suggest a certain blurriness, where users sometimes don’t appear to know if they’re engaging with a piece of technology or an actual human being.

Jindou Lee.

“There are so many times where, you know, a resident would thank our AI bot,” he said. “They didn’t know if they were talking to a human or not.”

In response, HappyCo has designed some transparency into its tech. If a person asks JoyAI if it’s a human or a bot, it has the ability to answer honestly and reveal to users that it is, in fact, a digital assistant. But while Lee said that people do appreciate connections to actual humans, and no one wants to feel like they’re talking just to a computer, JoyAI users have tended to accept the machine.

“If it solves the problem, we found that people don’t really care,” he said. “If you’re a resident, you put in a ticket, you just want it to be fixed.”

A few years ago, when chatbots were more rudimentary, that might not have been the case. But today, as the technology advances, Lee expects more and more people to accept interactions with AI. And the line between humans and bots may not always be so clear.

“I think those lines,” he said, “will continue to blur.”

What’s in a name

As Kathleen Lappe and her team at DirectOffer developed their own voice assistant AI — which functions as a concierge in both the real estate and hospitality spaces — they wanted to find a name for the tech. Lappe recently told Inman the team discovered that the names Noah and Olivia were the two most common English names at the time, so they settled on the latter.

“We felt OLIVIA rolled off the mouth,” Lappe said, “And then we built an acronym after OLIVIA, so it just hit the right spot.”

OLIVIA’s avatar as featured on DirectOffer’s website. Credit: DirectOffer

In choosing OLIVIA — which also presents itself with a human face and is described internally as “her” — DirectOffer was following in the footsteps of many other companies that have consistently chosen female names for their artificial intelligence. Amazon, for example, has Alexa. Apple’s phones all come with Siri. And once upon a time, Microsoft built a bot named Cortana.

This preference for female names is common in real estate as well. Aside from OLIVIA, there’s DealMachine’s Alma, lead nurturing bot Gabbi.AI, and voice-based AI rent collector Colleen. There are exceptions, too, but the trend toward female names for AI assistants is clear.

In the case of OLIVIA, Lappe said that users simply tended to respond better to female names.

Kathleen Lappe

“In general, women don’t have a problem with women giving instructions to them,” Lappe said. “And men are more comfortable with women guiding them.”

Lee made a similar point, saying that in his company’s research, “People responded better to female names than male names” — hence “JoyAI.”

The trend toward female names for virtual assistants is so common that researchers have actually looked into the topic. A 2019 report from UNESCO, for example, argued that feminized voices are a relatively recent phenomenon and that they raise questions about potential gender biases in technology. But perhaps most critically, the report suggests that the naming and gendering of AI is further blurring the lines between real and simulated people.

“As emotive voice technology improves,” the report states, “the ability to distinguish between human and machine voices will decrease and, in time, probably disappear entirely.”

In a similar vein, a 2021 paper looked at this question and acknowledged that past investigations suggested female-voiced bots are common because they’re perceived as being warmer. But the researchers actually suggested there’s something deeper going on.

“We argue that people prefer female bots because they are perceived as more human than male bots,” the researchers found.

In other words, it’s not so much that people like women’s voices more. It’s that those voices are nudging them further into the gray zone between machine and human.

To anthropomorphize or not

While the bots generally seem to be racing toward personhood, not every company is trying to make them seem human. Michael Martin, CEO of real estate virtual assistant company Sidekick, said his company has taken a very different approach and intentionally chooses not to anthropomorphize their tech. Sidekick’s assistants are simply and fittingly called “Sidekicks.”

Michael Martin

“It reinforces this kind of false humanity of an AI that I think stokes fears of human replacement,” Martin told Inman of naming bots. “Which I think in real estate is particularly pronounced in many cases. I think it’s really important, as AI becomes more ubiquitous, that the human-computer interaction always remains clear.”

Martin has followed other companies’ moves to anthropomorphize AI and speculated that such choices are done to make the tools more relatable. But his vision for the future of the technology is something different. It’s a vision in which artificial intelligence becomes “more of a substrate” embedded in some other machine — say, a car or a fridge — than a friendly aide with a name or face. In this future, a bot might not actually need a name at all.

In the end, it may not be entirely an either-or between Martin’s vision and what other companies like DirectOffer are creating. But either way, it’s clear that going forward, technology will be increasingly able to do something that we’ve long associated with living beings: Act on its own.

“There’s a world very soon,” Martin said, “where two agents working together on a deal, that experience is better because both of them have a Sidekick, and those Sidekicks can interact without the agent needing to.”

Correction: DirectOffer’s OLIVIA is a voice assistant AI. This post originally mischaracterized it as a chatbot.

Email Jim Dalrymple II

by Darryl Davis | Jun 10, 2025 | Industry, News Feed

Lean on systems and support that take the busywork off your plate — like CRMs, done-for-you marketing, voicemail drops and smart follow-up templates, coach Darryl Davis writes.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Let’s not sugarcoat it: Getting into real estate right now is no walk in the park.

The market is unpredictable. Buyers are anxious. Sellers are skeptical. And your to-do list? It’s probably longer than your pipeline. But here’s the good news — this isn’t just a tough time to start in real estate. It’s also the perfect time to become the kind of agent who can weather anything.

Because skills sharpen under pressure. And resilience? That’s built one challenge at a time.

If you’ve had a rough week — or three — don’t sweat it. You’re not doing it wrong. You’re just in the phase where most agents give up. But the ones who stick it out? They’re the ones who end up unstoppable.

Here’s how to stay the course, even when it feels like the course is uphill in both directions:

1. Get in the game early (even if you trip)

You won’t master real estate by learning alone. Webinars, coaching and training are important — they give you the what and how. But the real magic happens when you take what you’ve learned and put it into action. Making the calls. Asking the questions. Showing up — awkward or unsure — but still showing up. Action builds clarity. Movement builds momentum. Just start.

2. Redefine rejection

That “no” you just heard? It wasn’t personal. It was practice. Every conversation, especially the ones that fall flat, teaches you something. And every agent you admire has a stack of “no thanks” under their belt. Keep going.

3. Find a guide, not just a guru

Look for someone who’s been where you are — and is willing to share the journey. Whether it’s a mentor, coach or peer, surrounding yourself with people who’ve navigated the chaos will remind you: It is survivable. (And sometimes even funny in hindsight.)

4. Make peace with the awkward phase

You will mess up an appointment. You will forget a form. You will get ghosted. It’s part of the deal. But every time you face it instead of folding? You’re one step closer to becoming the skilled, steady, in-demand agent you set out to be.

5. Use the tools that keep you moving

You don’t have to do this the hard way. Lean on systems and support that take the busywork off your plate — like CRMs, done-for-you marketing, voicemail drops and smart follow-up templates. Less time on admin equals more time building your business.

The truth is, there’s no magic wand in real estate. No shortcut. No perfect market. But there is a version of you that keeps going when others stop. That version? That’s who builds the career.

So, give yourself some grace. Let it be messy. Learn fast, fail forward, and remind yourself that every “bad day” in real estate is still moving you toward mastery — if you let it. You’ve got this.

by Kevelyn Guzman | Jun 10, 2025 | Industry, News Feed

One-size-fits-all answers just don’t cut it in this highly complex market. Start thinking bigger, and build the business of your dreams, Coldwell Banker Warburg’s Kevelyn Guzman writes.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Let’s stop playing small. You’re not just an agent. You’re not just helping someone buy or sell a home. You’re running a business — whether you’ve realized it or not.

Too often, I hear agents refer to themselves as if they’re filling a job: “I work at XYZ Brokerage.” But if that’s how you see yourself, you’re missing the bigger picture. You are your own brand. You’re the CEO of your own operation. You are your own marketing department, finance team, sales lead and strategic planner.

And while your brokerage should absolutely support your growth, it’s your name, your reputation and your income on the line. You’re not alone — but you are in charge.

5 ways to scale

The agents who get that? They don’t just survive. They scale. Here’s how:

1. Build structure like it’s your job — because it is

One of the biggest traps in this industry is the illusion of freedom. You can technically work when you want. But without structure, that freedom quickly turns into chaos.

Successful agents aren’t winging it. They’re managing their calendars, setting time blocks, building systems for lead follow-up, content creation, showings and client care. You don’t have to be a robot, but you do have to be disciplined.

You can’t outsource self-management. You are the COO of your day-to-day. The way you spend your time will either compound in your favor or work against you.

2. Know your brand — and build it like a business

Your brand is your most valuable asset. It’s how people remember you, talk about you and refer you. And yes, it starts with the visuals — your logo, colors, font and photos. These aren’t just “nice to have.” They anchor your brand identity. They make you recognizable across every platform, from listing presentations to Instagram stories.

But your brand is more than design. It’s your voice. It’s how you follow up. It’s how you show up in negotiations, at open houses and in your social presence. Whether you’re all business or you bring the humor, your brand should be intentional and consistent.

3. Treat your numbers like a CFO

No thriving business operates without a clear understanding of the numbers. And yet, too many agents are out here guessing. They don’t know how much they’re spending on marketing, what their average ROI is or what they need to make monthly to hit their annual goals.

That’s not a business — that’s gambling.

If you don’t already have a budget, make one. If you’re not tracking your leads and conversions, start. Know your best-performing marketing channel. Know how much you can spend to acquire a client and still stay profitable.

4. Learn when to delegate — and what to invest in

Here’s the truth: You can’t scale if you’re doing everything yourself. You may start as a solo operation, but you shouldn’t stay one.

If the brokerage you’re affiliated with does not offer transaction support or marketing assistance, then outsourcing this support is critical for your business. These aren’t vanity moves. They’re business decisions. Time is money. And if you’re spending your time on things that don’t grow your business, you’re stalling your potential.

The most successful agents I know are the ones who know when to delegate — and when to double down. They lean on their brokerage for support, plug into the network and bring in help when it makes financial sense.

5. Hustle is great. Vision is better

You can’t out-hustle a lack of strategy. And you can’t grow a business without a clear idea of what you want to build.

What kind of clients do you want to work with? What price points? Which neighborhoods? What does a “good year” look like — and how will you get there?

Hustle gets you started, but intention keeps you focused. This is where working with the right brokerage matters. You should have a leadership team helping you connect your day-to-day work to the bigger picture. You should feel like your goals are being championed, but also challenged.

Make sure your brokerage doesn’t just support agents, but partners with entrepreneurs. Does it offer coaching, masterminds, brand development and international connections? But at the end of the day, you should know where you’re going and shouldn’t be afraid to own it.

Act like the CEO of your business

You are the business. You’re the brand, the engine, the decision-maker. That doesn’t mean you have to do it alone — but it does mean no one will care about your growth more than you.

Treat this like a business and you’ll start thinking bigger. You’ll raise your standards, sharpen your focus and build something real. Whether you’re closing two deals a year or two a month, the same rule applies: Act like the CEO of your business, and watch everything shift.

Kevelyn Guzman serves as regional vice president at Coldwell Banker Warburg. Connect with her on Instagram and Linkedin.

by Ginger Wilcox | Jun 10, 2025 | Industry, News Feed

In a market with fewer clients and more competition, trust is the ultimate differentiator for real estate pros, Better Homes and Gardens President Ginger Wilcox writes.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Real estate runs on trust — but in today’s market, that trust is under pressure.

Clients are asking harder questions. They’re reading headlines about lawsuits, watching TikToks that question commission models, and feeling more cautious with every economic swing or news story. If you think a smile, a good listing presentation and a few social posts are enough to win their confidence, think again.

This market demands more.

Great agents don’t just earn trust. They build it deliberately, consistently and strategically. It’s not just a core value; it’s a business advantage. And when done right, trust isn’t just how you close deals. It’s how you grow a career that lasts.

Here’s what that looks like in practice:

Trust isn’t claimed — it’s proven

Forget the buzzwords. Clients don’t care if you say you’re “reliable” or “honest” — they care if you show up when it matters.

Trust gets built in the small moments:

- When you admit what you don’t know and get the right answer.

- When you give them insights or information that they don’t already know.

- When you pick up the phone for the hard conversation.

- When you protect their time, their money and their peace of mind.

If your actions aren’t creating clarity and confidence, you’re not building trust: You’re eroding it.

Trust is scalable — but only if you systematize it

Top-performing agents don’t rebuild trust from scratch with every client. They scale it by creating consistent experiences, clear expectations and repeatable systems that reinforce their value with every client they serve.

Ask yourself:

- Do your follow-up systems match the promises you made in the first conversation?

- Are you proactively resetting expectations when the market shifts mid-deal?

- Is your digital presence aligned with your real-world reputation?

Trust isn’t just about the one client in front of you — it’s about the next five that client will refer if you get it right.

Trust converts — but only if you stay top of mind

Most agents think of referrals as luck. They’re not. They’re the outcome of sustained trust.

The best agents turn satisfied clients into active advocates. That means showing up after the close — checking in, adding value, being a visible part of their life and community. Not with spammy drip campaigns, but with relevance and care.

Your past clients are the most powerful marketing engine you have. But they won’t activate it if they don’t remember what made you great.

Trust isn’t soft. It’s not vague. It’s not some warm, fuzzy feeling

It’s the foundation of your value. It’s why clients follow your advice, don’t question your worth and send you more business, ensuring your long-term success in this industry. It’s also one of the few things competitors can’t copy.

And in a market where there is more competition, fewer listings and clients are more cautious, trust is the ultimate differentiator.

Start treating it like the asset it is.

Ginger Wilcox is the President of Better Homes and Gardens Real Estate.

by Bernice Ross | Jun 10, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

In a market where flipping has started feeling like playing financial roulette, owner-occupying your first investment, otherwise known as house hacking, offers new investors a safer, smarter path to profit from their first real estate investment.

There was a time when flipping homes seemed like one of the fastest ways to build real estate wealth. Buy low, renovate fast and sell high — that was a formula that worked for millions of one- to four-unit investors.

Due to thinning margins, supply chain problems, too few contractors, plus higher interest rates, house flipping has now become challenging even for the most experienced flipper. Couple that with tariffs, inflation and a stagnant or deflating market, and this is an environment where you can easily end up with massive losses rather than profit.

What’s the hot new alternative? House hacking

House hacking is the strategy of living in your investment property and either renting out part of your existing home or creating additional units you can rent out to generate rental income. This approach reduces (and can even eliminate) your personal housing costs, build equity, while also simultaneously lowering your risk.

House hacking is one of the best alternatives for becoming a real estate investor and not getting crushed by what could easily happen if you were doing a flip.

House hacking your primary residence

“House hacking” combines the advantages of single-family homeownership with the income and wealth-building potential of owning a rental property.

Here are a few common house hacking strategies for single-family properties:

Garage conversions

Transform your detached or attached garage into a studio or one-bedroom rental.

Basement apartments

Finish out a lower level with its own entrance, bathroom and kitchenette. My in-laws had a huge unfinished basement that only had a laundry. They added a separate outside entrance, built a full kitchen, created a living area for viewing TV and a single bath for that area. They also added a second master suite for guests, including a steam shower that was accessible from the main house down the stairs.

ADU builds

If you’re in a market with high rents and lenient ADU laws, (Portland, Austin or parts of Southern California), building or converting even a modest ADU can add $1,200 to $2,500 per month to your income stream while also significantly increasing your resale value.

In addition, many cities now allow homeowners to build a small backyard cottage or over-garage apartment with minimal red tape.

Internal reconfiguration

Do you have a split-level house or home with a fourth or fifth bedroom with a private bath away from most of the house? If so, you can section off part of your home to create a rental with a private bath and separate entry, which is great for traveling nurses, students or Airbnb guests.

Practical steps to get started

Assess your property

Identify spaces within your home that can be rented out, such as spare bedrooms, basements or garages.

Understand financing options

Explore loans suitable for owner-occupied properties, like FHA or VA loans.

Check local regulations

Research zoning laws, rental regulations and tax implications in your area. Many areas have strict rules about short-term Airbnb-style rentals. This may vary given that you are living in the property, but it’s important to verify.

Prepare the space

Make sure that the rental area meets safety standards, is up to code if you make any improvements and is clean and appealing to potential tenants.

Market your rental

Use platforms like Airbnb or local rental listings to find tenants.

Owner occupying a 2- to 4-unit property

If you house hack your primary residence, chances are it will mean that you’re living in a nicer property than if you purchase a two- to four-unit building, where you may end up living in an apartment.

In other words, you’re not getting the dream home you see on HGTV, but you are trading those high mortgage payments for rental income that starts you on the path to building true real estate wealth.

Benefits of owning a 2- to 4-unit property where you reside include

- Built-in cash flow from Day 1.

- Simplicity in management (you’re already on-site)

- Favorable financing options as an owner-occupant.

- Better yet, lenders typically allow you to count a portion of the rental income from the other units toward your qualifying income. That means you can afford a larger purchase than you could with a single-family loan alone.

- When you’re purchasing as an owner-occupant, you may qualify for low- or no-down-payment loans (FHA: 3.5 percent; VA: 0 percent), an opportunity that doesn’t exist for investor-only loans, which typically require 15 percent to 25 percent down.

- Best of all, you may even be eligible for down payment assistance. According to DownPaymentResource.com, the average DPA benefit in 2024 was $18,000, money that in many cases can cover most, if not all, of your down payment and closing costs.

Add even more value by building additional units over time

Want to increase income without buying another property? Consider these value-boosting strategies:

- Convert a duplex to a triplex by finishing a basement.

- Add an ADU to the backyard of your two- to four-unit property.

- Upgrade the existing units to command higher rent.

- Split a large unit into two smaller apartments, if zoning allows.

With the national housing shortage and demand for rentals still sky-high, especially in starter markets, these upgrades can yield serious ROI.

10 powerful reasons your first real estate investment should be a property you live in

1. Significantly better financing terms

Owner-occupants qualify for much lower interest rates and better loan terms than traditional investors. FHA and VA loans allow low or even zero-down payments, something that investor loans almost never offer.

2. Buy with less cash upfront

Instead of coughing up 15 percent to 25 percent down on an investment property, you can get started with as little as 3.5 percent down on a duplex, triplex or fourplex if you live in one unit. It’s the easiest path for first-time homeowners to break into real estate investing.

3. Reduce your housing costs

Tenant rent can cover a large chunk (and sometimes all) of your mortgage, taxes and insurance. This drastically lowers your cost of living while you’re simultaneously building wealth through equity and appreciation.

4. Boost your buying power

Lenders often count projected rental income toward your qualifying income, especially on two- to four-unit properties. That means you may qualify for more property that is more expensive than your W-2 income alone would normally allow.

5. Gain built-in property management

When you live onsite, you can handle minor issues immediately, avoid property management fees and stay on top of maintenance. This saves money, time and headaches.

6. Set the standard for tenant behavior

Tenants tend to behave better when their landlord lives on the premises. Properties stay cleaner, lease violations drop and disputes get resolved quickly. Your presence creates built-in accountability.

7. Learn by doing (and earning)

Becoming a landlord will provide you with a real-world masterclass in real estate investing, especially if you’re managing a two- to four-unit building. You’ll learn how to screen tenants, manage maintenance and handle finances, all with less risk than traditional investing.

8. Double-dip on tax benefits

You may be able to deduct mortgage interest and property taxes as an owner-occupant while also claiming depreciation, repair costs and other deductions on the rental portion of your property. (Always check with your CPA for your unique tax situation.)

9. You have multiple exit strategies

Unlike pure rentals, owner-occupied two- to four-units offer flexible resale options. You can rent out all the units, refinance and move into your next investment property, do a straight sale of the property, or a 1031 Tax Deferred Exchange.

10. Build wealth faster

With lower expenses, higher cash flow, forced savings through amortization and real-time experience, living in your first real estate investment lets you scale faster. Whether you’re after financial freedom or long-term rental income, this strategy gets you there more quickly.

The best real estate investment may the one you can live in

In a market that is challenging even to the most experienced house flippers, living in your first real estate investment can provide the foundation for building lasting wealth through real estate investing. Best of all, you don’t need a lot of money to get started, just a mortgage, a plan and the willingness to live in a property where your name is on the mailbox.

by Matt Carter | Jun 9, 2025 | Industry, News Feed

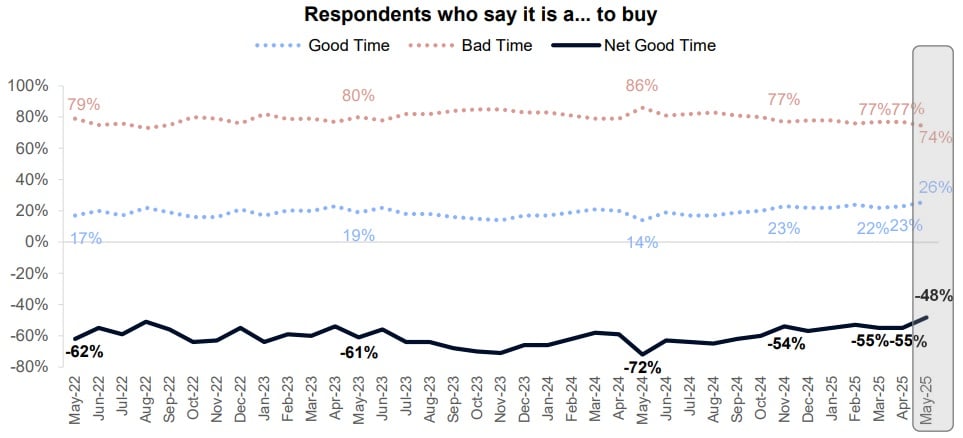

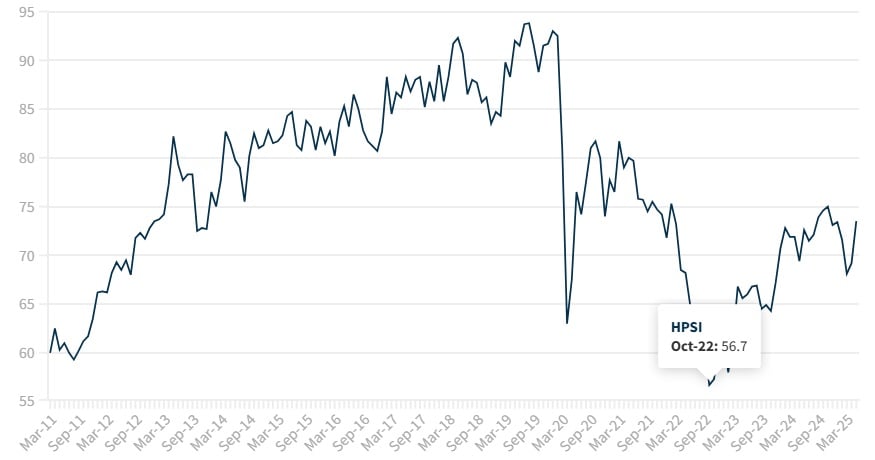

While just 26 percent of Americans said May was a good time to buy, that’s up from 23 percent in April and 14 percent a year ago, an all-time low in Fannie Mae survey.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Consumer sentiment about the housing market improved in May to the highest level since November as Americans became more optimistic about buying and selling conditions and the prospects for mortgage rates to come down in the year ahead.

Fannie Mae’s latest National Housing Survey, released Monday, showed five of six components of the mortgage giant’s Home Purchase Sentiment Index (HPSI) improved in May.

Consumer sentiment has been trending down this year, in part due to fears about the impact of the Trump administration’s tariff policies, but the economy continues to do better than surveys suggest, economists say.

Fannie Mae Home Purchase Sentiment Index

At 73.5, the HPSI was up 4.3 points from April to May, surpassing the previous 2025 high of 73.4 seen in January.

The HPSI — which hit an all-time low of 56.7 in October 2022 in records dating to 2011 — distills six questions from Fannie Mae’s monthly National Housing Survey into a number.

The latest survey, which was fielded from May 1 through May 20 to 1,345 household decision makers, found that while most Americans still think it’s not a good time to buy, sentiment is improving.

With Americans also less worried about losing their jobs in May, the only HPSI component that didn’t improve was household income.

While only 26 percent of household decision-makers said May was a good time to buy, that’s up from 23 percent in April and 14 percent a year ago — an all-time survey low.

With the share who said May was a bad time to buy falling from 77 percent in April to 74 percent in May, the net share of consumers who said it was a good time to buy increased by seven percentage points, to -48 percent.

More than two-thirds of consumers surveyed (68 percent) said they’d buy rather than rent if they were going to move, up from 65 percent in April.

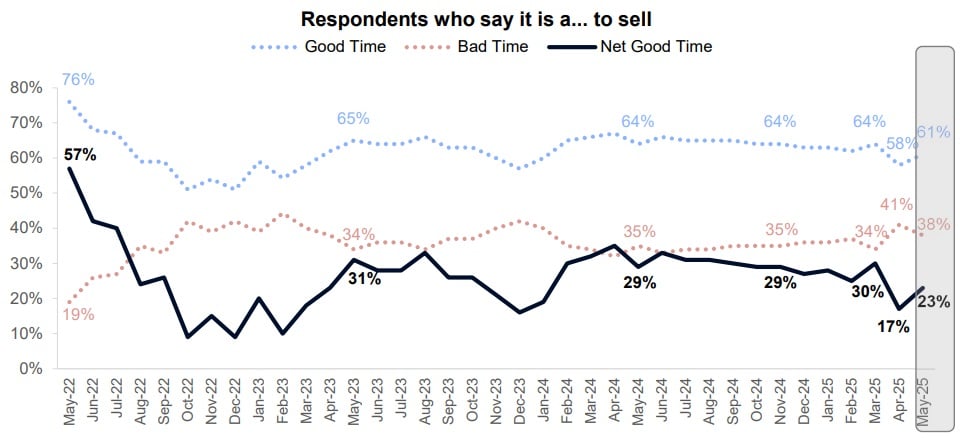

Most consumers (61 percent) said May was a good time to sell, up from 58 percent in April but down from 64 percent a year ago. With the share who said it was a bad time to sell falling from 41 percent in April to 38 percent in May, the net share of consumers who said May was a good time to sell increased by six percentage points, to 23 percent.

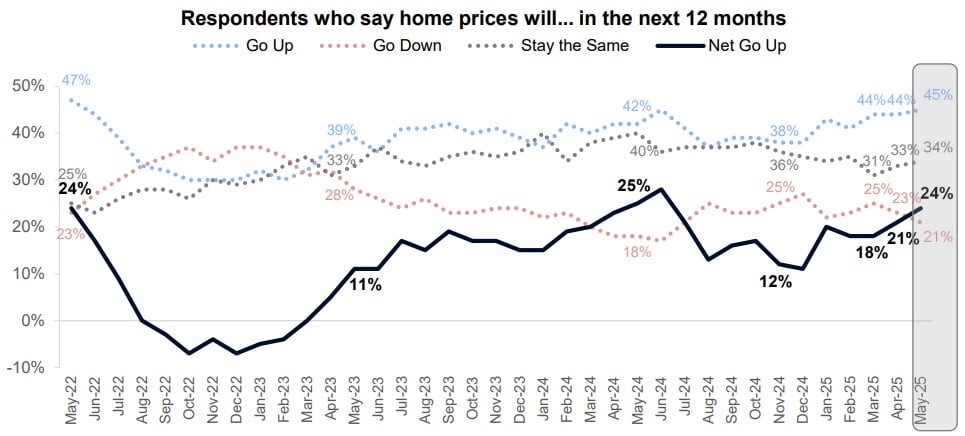

With more consumers convinced that prices are headed up in the next 12 months (45 percent) or that they’ll stay the same (34 percent), the net share of consumers who expect prices to go up rose three percentage points, to 24 percent.

While many would-be homebuyers are hoping prices come down, Fannie Mae’s HPSI treats expectations of price increases as a positive, since it shows consumers aren’t worried about prices crashing.

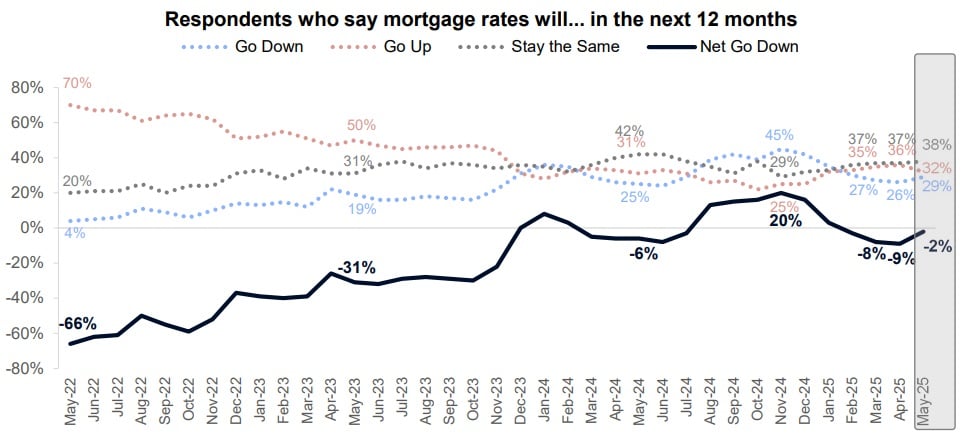

Most consumers surveyed in May said they expect mortgage rates to either stay the same over the next 12 months (38 percent) or go down (29 percent).

With the share who expect rates to go up falling from 36 percent in April to 32 percent in May, the net share expecting rates to go down improved by seven percentage points, to -2 percent.

Last month, Fannie Mae economists said they expect mortgage rates to come down by a full percentage point by the end of next year. Forecasters at the Mortgage Bankers Association have issued a more cautious take.

MBA forecasters predict mortgage rates will still be averaging 6.6 percent during Q4 2025 and 6.3 percent during Q4 2026.

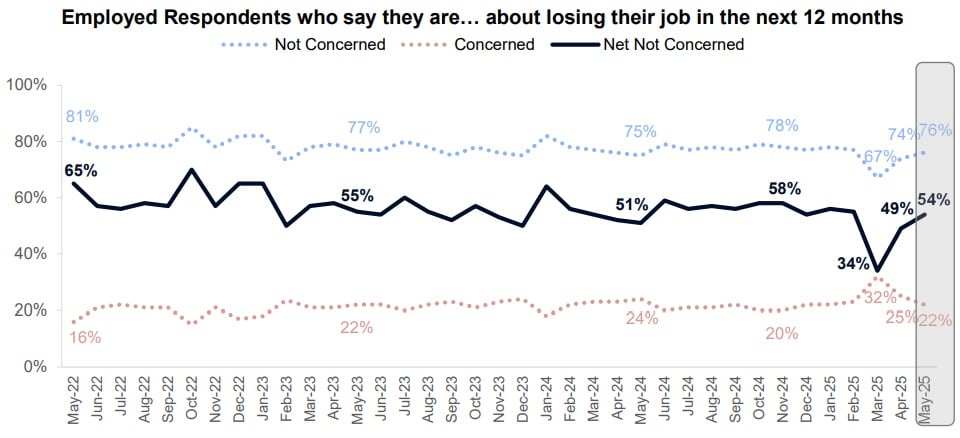

Only one in five employed respondents surveyed in May (22 percent) said they were worried about losing their job in the next 12 months, down from 25 percent in April and a 2025 high of 32 percent in March.

With 76 percent of employed consumers saying they weren’t concerned about losing their job, the net share who said they weren’t concerned about being unemployed increased by five percentage points, to 54 percent.

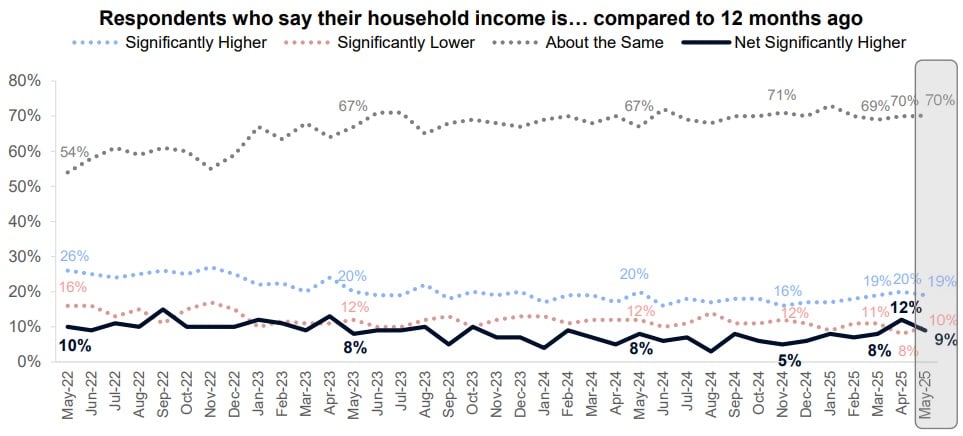

Most consumers surveyed in May (70 percent) said their household income is about the same as it was 12 months ago. But 10 percent said it was significantly lower, up from 8 percent in April, but down from 12 percent a year ago.

The net share of consumers who said their income was higher than 12 months ago fell three percentage points from April to May, to 9 percent.

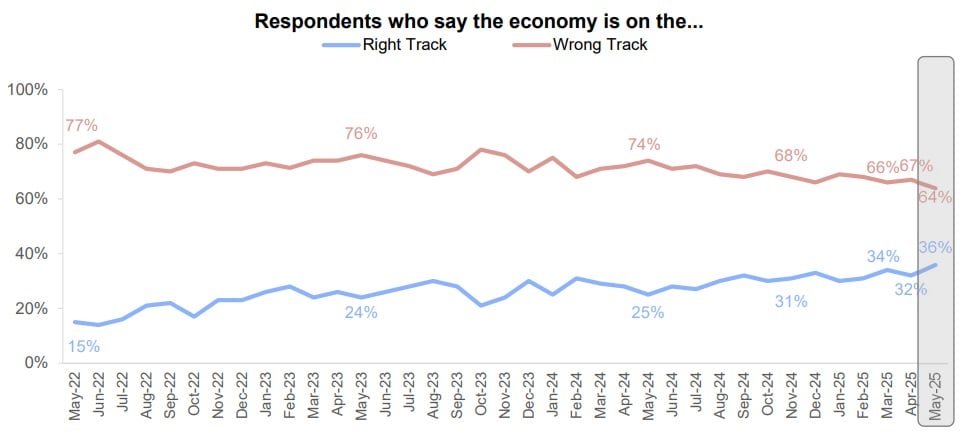

Although not factored into the HPSI, the National Housing Survey asks household decision-makers if they think the economy is on the right or the wrong track.

While most consumers thought the economy was on the wrong track in May (64 percent), that’s down from 67 percent in April and 74 percent a year ago.

Email Matt Carter