by Matt Carter | Jun 25, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Economists and investors expect Federal Reserve policymakers to continue to resist calls by the Trump administration to lower interest rates until they see more data on how tariffs and other policies are impacting inflation and employment.

Grilled by House and Senate lawmakers at separate hearings this week, Fed Chair Jerome Powell defended the central bank’s reluctance to resume cutting rates, saying the job market remains solid and that there’s no rush to make a decision.

After the Fed voted unanimously on June 18 to hold rates steady, Associated Press Reporter Chris Rugabar asked Powell if “cracks in the jobs market” and housing data “that have been pretty weak” could justify future rate cuts.

“I think if you look at the overall picture, what you’re seeing is 4.2 percent unemployment, and an economy that’s growing at a rate [that] appears to be 1-1/2, 2 percent — maybe a little better than that,” Powell said.

TAKE THE INMAN INTEL SURVEY FOR JUNE

While consumer sentiment has “come up off of very low levels,” it’s still depressed, Powell acknowledged.

“The housing market is a longer run problem, and also a short run problem,” Powell said. “Basically, we have a longer run shortage of housing, and we also have high [mortgage] rates right now. I think the best thing we can do for the housing market is to restore price stability in a sustainable way and create a strong labor market.”

Trump took to social media after the vote and urged the Federal Reserve Board to “override this Total and Complete Moron!” referring to Powell. “Maybe, just maybe, I’ll have to change my mind about firing him?”

Vice President J.D. Vance and Federal Housing Finance Agency Director Bill Pulte kept up the heat on Tuesday, with Vance saying he’d “love to hear an argument for why Powell cut rates 50 points right before an election but can’t do it now with inflation lower.”

Pulte claimed Powell’s interest rate policies “are not based on data but instead on Powell’s politicization of the Fed,” calling them “dangerous.”

On Wednesday — a few hours before ordering Fannie Mae and Freddie Mac to study allowing homebuyers to count crypto holdings as an asset — Pulte called on Powell to resign.

Trump told reporters Wednesday that he already has “three or four people” in mind who might replace Powell — although it’s unclear whether he will try to fire him.

Trump appointed Powell to lead the Fed during his first term, and his term is not set to end until May 2026.

One reason the Trump administration has grown impatient with Powell is that inflation has been nearing the Fed’s 2 percent goal. The personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred gauge of inflation, showed the price of goods and services rose 2.1 percent in April from a year ago, the Bureau of Economic Analysis reported last month.

But while the Fed can pull levers that give it direct control over short-term interest rates, mortgage rates are determined by investor demand for mortgage-backed securities (MBS), which fund most home loans.

As the Fed cut short-term interest rates by a full percentage point in its final three meetings of 2024, mortgage rates moved by about the same amount in the opposite direction, as incoming economic data suggested inflation was on the rise again.

The last time the Fed cut rates, mortgage rates went up

Powell has been saying for months that Fed policymakers need more time to assess the impacts of the Trump administration’s policies in areas including tariffs, immigration, taxes and regulation.

The “dot-plot” in the Fed’s latest Summary of Economic Projections shows members of the Federal Open Market Committee (FOMC) expect to cut the short-term federal funds rate just twice later this year, to between 3.75 percent and 4 percent.

“Lawmakers this week have been no more successful than journalists last week in getting Chair Powell to set out a more concrete timetable for the policy easing anticipated by a slender majority of [Fed policymakers] this year,” economists at Pantheon Macroeconomics said in their latest U.S. Economic Monitor.

The CME FedWatch Tool, which tracks futures markets to predict future Fed moves, shows investors think there’s only a 25 percent chance of a July rate cut. But bets placed by futures market investors as of June 25 put the odds of a September rate cut at 90 percent — up from 64 percent on June 18.

Fed policymakers will receive “substantial extra information” if they hold off until September to make a decision, Pantheon economists Samuel Tombs and Oliver Allen wrote Wednesday.

By September, “we think the FOMC will have seen a sequence of three weak labor market reports through August,” Tombs and Allen predicted, with the unemployment rate hitting 4.5 percent by August — 4 months sooner than currently projected by the Fed.

“That would represent a resounding call to ease policy, even before the full effect of the tariffs on inflation is visible in the data,” Pantheon forecasters wrote.

In the meantime, mortgage rates have been holding steady in the high sixes.

Mortgage rates stabilize

After hitting a 2025 low of 6.48 percent on April 4, rates on 30-year fixed-rate conforming mortgages have been rangebound between 6.75 and 7 percent in May and June, according to lender data tracked by Optimal Blue.

Weekly surveys of lenders by the Mortgage Bankers Association show that demand for purchase loans was up 12 percent last week from a year ago.

“Applications increased slightly overall driven by FHA refinances, but conventional applications saw declines over the week,” MBA Deputy Chief Economist Joel Kan said, in a statement. “The average loan size for purchase applications declined to $436,300, the lowest level since January 2025, driven by decreasing conventional purchase loan sizes.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 25, 2025 | Industry, News Feed

Head of Fannie Mae and Freddie Mac’s federal regulator says mortgage giants should consider what risk mitigation might be required when counting mortgage borrowers’ crypto holdings as an asset, “including adjustments for market volatility.”

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The head of Fannie Mae and Freddie Mac’s federal regulator has directed the mortgage giants to consider allowing borrowers to count cryptocurrency as an asset without having to convert their holdings into dollars.

In a post on the social media platform X Wednesday — Federal Housing Finance Agency Director Bill Pulte’s preferred channel for issuing official communications — Pulte said cryptocurrency is “an emerging asset class that may offer an opportunity to build wealth outside of the stock and bond markets.”

TAKE THE INMAN INTEL SURVEY FOR JUNE

Pulte is a crypto investor himself — in addition to millions of dollars in annual dividends from his stakes in Pulte Group and several heating and air conditioning companies, he listed $500,000 to $1 million in bitcoin among the assets he disclosed in a financial disclosure statement for executive branch personnel.

The order Pulte issued Wednesday directs both Fannie and Freddie “to prepare a proposal for consideration of cryptocurrency as an asset,” but only in cases where the assets are “evidenced and stored on a U.S.-regulated centralized exchange.”

Bill Pulte

Fannie and Freddie must also consider what risk mitigation might be required when counting mortgage borrowers’ crypto holdings as an asset, “including adjustments for market volatility and ensuring sufficient risk-based adjustments to the share of reserves comprised of cryptocurrency,” Pulte said.

The mortgage giants were instructed to submit any proposed policy changes regarding the treatment of crypto to their board of directors for approval — Pulte chairs both Fannie and Freddie’s boards — before submitting them to FHFA for review.

Commenting on Pulte’s proposal, Annapolis, Maryland based mortgage banker John Downs said asset reserves are not as much of a factor in obtaining loan approvals as they used to be.

“That prevents the crypto rug from truly impacting the borrowers ability to repay,” Downs wrote, alluding to the dramatic ups and downs in crypto valuations.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 25, 2025 | Industry, News Feed

The 2023 order, aimed at ensuring the collection of information about applicants’ race, ethnicity and gender, wasn’t scheduled to be lifted until 2028. Regulators say the bank has fulfilled its obligations.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

In its latest move to ease regulations, the Consumer Financial Protection Bureau (CFPB) has terminated a 2023 consent order with Bank of America aimed at addressing allegations that the lender reported false information about mortgage borrowers to federal regulators.

Bank of America was accused of failing to ask some mortgage applicants demographic questions about their race, ethnicity and gender as required by the Home Mortgage Disclosure Act (HMDA) — data that’s collected to uncover potential discriminatory lending patterns.

The CFPB claimed that in addition to failing to collect that demographic information from some borrowers, Bank of America falsely reported that the applicants had chosen not to respond.

Bank of America knew “that many loan officers receiving applications by phone were failing to collect the required data as early as 2013, but the bank turned a blind eye for years,” the CFPB alleged in announcing a $12 million settlement.

Under the terms of a Nov. 27, 2023, consent order, Bank of America also agreed to implement a compliance plan ensuring that it collected, recorded and reported required HMDA data used by the CFPB and other federal regulators to detect redlining.

While the consent order was to remain in effect for a minimum of five years — until late 2028, if no further reporting violations occurred — Office of Management and Budget Director Russell Vought on June 4 signed an order terminating it, saying Bank of America had fulfilled its obligations.

The CFPB did not publicize the action, which was first reported by Reuters this week. Bank of America declined Inman’s request for comment on the early termination of its consent order with the CFPB.

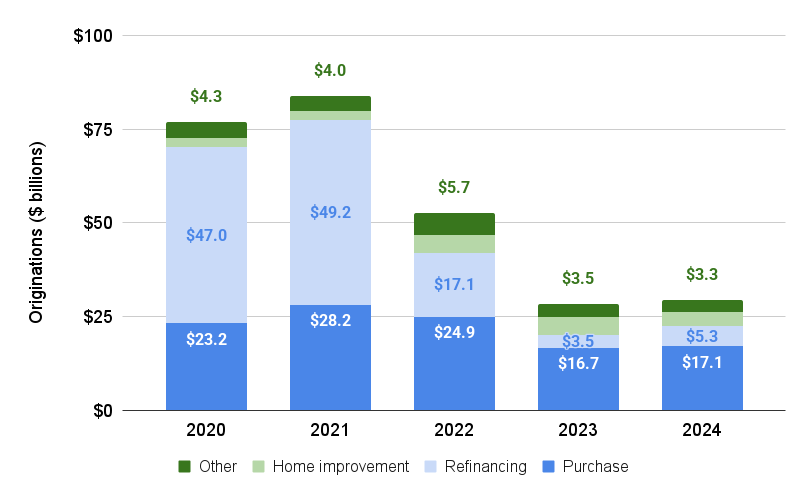

Bank of America mortgage originations, 2020-2024

Bank of America was the nation’s fifth-largest mortgage lender last year by dollar volume, with $29.5 billion in originations, according to an analysis of HMDA data by iEmergent.

Since the end of the pandemic-era refinancing boom fueled by low interest rates, most of the bank’s mortgage business has been with homebuyers, with $17.1 billion in purchase loans funded in 2024.

Regulatory rollback

Vought and his top deputy at OMB, Dan Bishop, are leading the Trump administration’s efforts to downsize the CFPB, with Vought serving a dual role as the bureau’s acting director.

The Trump administration, which is seeking to cut 90 percent of the CFPB’s workforce, has put about 20 active enforcement cases on hold and sought to vacate a number of settlements that the bureau reached under the Biden administration.

The acting director of the CFPB’s enforcement division, Cara Petersen, resigned on June 10, saying in a farewell email that “the bureau’s current leadership has no intention to enforce the law in any meaningful way.”

Two days later, U.S. District Judge Franklin Valderrama declined the CFPB’s motion to vacate a settlement it reached last year in a fair lending case involving Chicago mortgage broker Townstone Financial, saying that doing so “would erode public confidence in the finality of judgments.”

Russell Vought

Vought had claimed that an internal review of the case determined that the CFPB “abused its power” in pursuing the case against Townstone in order to “further the goal of mandating DEI in lending.”

Consumer groups that defended the Townstone settlement in court called the CFPB’s request to vacate it “unprecedented,” and argued that granting it would establish a “dangerous and destabilizing precedent.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Lillian Dickerson | Jun 25, 2025 | Industry, News Feed

A steady course is predicted for luxury real estate throughout the remainder of 2025, the firm’s mid-year luxury report said, creating “compelling opportunities for strategic homebuyers and sellers,” according to CEO Philip White.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Many Americans may feel shaken right now because of economic uncertainties and stock market volatility, but their confidence in luxury real estate as a safe haven remains firm.

Bradley Nelson | Sotheby’s International Realty

The conclusion comes from Sotheby’s International Realty’s 2025 Mid-Year Luxury Outlook, released on Wednesday, which pulled intel from Sotheby’s International Realty agents across the globe who specialize in transactions priced at US$10 million and above. Those insights are also paired in the report with data from investment bank UBS, J.P. Morgan, Moody’s, McKinsey and Company, Bain and Company, Cotality, the National Association of Realtors (NAR) and the National Association of Home Builders (NAHB).

“The luxury real estate landscape continues to evolve at an unprecedented pace, creating opportunities for homebuyers and sellers with the right market knowledge,” Sotheby’s International Realty Chief Marketing Officer Bradley Nelson said in a statement.

“Our global network of affiliated agents brings unparalleled expertise and market insights that only Sotheby’s International Realty can deliver. This report is designed to empower both homebuyers and sellers with the strategic intelligence needed to make informed real estate decisions throughout the remainder of the year.”

TAKE THE INMAN INTEL SURVEY FOR JUNE

Luxury real estate continued to outperform the market at large during 2024 and the first months of 2025, Sotheby’s Realty noted, with the top half of the wealthiest U.S. households benefiting from the greatest gains in real estate value, according to data from Realtor.com.

Philip White | Sotheby’s International Realty

As some buyers pull away from the market during economic uncertainty, it also creates opportunity for other buyers who are ready to pounce when there’s less competition, the report said. The economic landscape, as well as movement in key markets, rebuilding opportunities in disaster areas and more, will all have an impact on the luxury real estate market this year, Sotheby’s International Realty concluded. But a steady course is predicted as 2025 continues.

“Ultra-high-net-worth individuals continue to view real estate as an essential portfolio component,” Sotheby’s International Realty President and CEO Philip White said in a statement. “Even amid economic uncertainty, the resilience of the luxury housing market provides compelling opportunities for strategic homebuyers and sellers, and this report serves as a roadmap for navigating today’s complex luxury real estate landscape.”

Economic headwinds

Odeta Kushi | First American Deputy Chief Economist

“On one hand, sharp swings in equities can prompt some high-net-worth individuals to delay big purchases due to uncertainty,” Odeta Kushi, deputy chief economist of First American Financial Corp, said in Sotheby’s International Realty’s report. “On the other, real estate — especially in prime markets — might be seen as a safer, more tangible store of value.”

- Construction costs may be exacerbated by Trump administration tariffs, Kushi said, which could drive luxury homebuyers toward turnkey properties to avoid elevated construction costs.

- Real estate represents 18.7 percent of the top 10 percent of wealthiest households’ investment portfolios, according to an April 2025 Realtor.com report, which is down from 19.9 percent a year ago.

- The segment of $1 million homes in the U.S. continues to grow, and represents nearly 13 percent of recent existing-home sales, according to April 2025 data from NAR, suggesting affluent buyers see real estate as a safe harbor for their investments.

- A weaker dollar in response to trade wars could lead to more overseas real estate investor purchases in the U.S., as could President Trump’s proposed “Gold Card” visa program, which creates a path to citizenship for individuals who invest US$5 million in the country.

Key US markets

Kara Warrin | Golden Gate Sotheby’s International Realty

“Our luxury property market isn’t impacted by interest rates because 85 percent of transactions are with cash,” said Kara Warrin, an advisor with Golden Gate Sotheby’s International Realty in Marin County and San Francisco. “Our team sold more than US$65 million between October and December 2024, with an average sale price of US$6 million. The buyers tend to be local people who want something bigger and better and have the cash to pay for it.”

- Buyer confidence seems to be growing in San Francisco, driving momentum at Sotheby’s International Realty – San Francisco, where the firm closed several transactions over $20 million in 2024, breaking old records.

- Momentum picked up in the New York City luxury market after the election as a result of pent-up demand and more liquidity from stock market performance, local Sotheby’s Realty advisors say. Condos are especially in demand because of their fewer restrictions than co-ops.

- Low inventory and restrictions on new development in Aspen have led to sustained elevated prices in the luxury ski town.

Rebuilding after disaster

“The number of such damaging natural disasters is growing,” Sotheby’s International Realty’s report said. “According to data released in January 2025 by the National Centers for Environmental Information, part of the National Oceanic and Atmospheric Administration, in 2024, the U.S. alone suffered 27 natural disasters where the estimated damage exceeded US$1 billion.

This trend is having profound consequences for high-end property markets around the world, reinforcing the increasing importance of considering climate resilience when investing in luxury real estate.”

- 2024 was the fifth year straight in which insured global losses from natural disasters exceeded US$100 billion, marking sustained climatic disruption, according to a January 2025 Moody’s report. One-third of losses were attributed to hurricanes making landfall in the U.S.

- In the last five years, 23 percent of U.S. homeowners saw property damage or loss as a result of severe weather, and 65 percent are prepping homes for future weather events, according to a Bank of America Institute report from May 2025.

- Rebuilding after a disaster can slow the inventory recovery, potentially bumping up prices while inventory is still constrained, the report noted. Relocation to other areas after a disaster can shift demand and create more pressure on nearby markets.

- Low inventory in the Pacific Palisades in the wake of fires in January 2025 has led to the average list price for surviving homes to grow to US$9.7 million, significantly higher than historic norms. Many of those who are rebuilding are now incorporating fire-preservation features in homes to prepare for future wildfires.

Global highlights

Tammy Fahmi | Sotheby’s International Realty

“What’s driving today’s high-end market is the feeling a home delivers as much as its address,” said Tammy Fahmi, senior vice president of global servicing and strategy at Sotheby’s International Realty. “What we’re witnessing in luxury real estate isn’t just a trend — it’s a fundamental redefinition of value. This experiential revolution transcends cultural boundaries, with buyers willing to pay substantial premiums for properties that offer exceptional features that reflect their lifestyles.”

- With the Saudi Vision 2030 economic development initiative, executives and foreign companies coming into Saudi Arabia are driving luxury developments with high-end amenities. The Red Sea Project, just off Saudi Arabia’s west coast, is also expected to drive tourism to the region after it is unveiled around 2030.

- Demand for high-end properties in India has surged in the last two years, and the luxury real estate market is expected to reach a value of US$105 billion by 2030.

- Between 2012 and 2021, the highest-priced transaction in Puerto Rico rose from US$2 million to $30 million. The island has seen growth in the luxury goods market, with revenue from the industry set to reach US$533.44 million in 2025, according to Statista Market Insights.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Carl Medford | Jun 25, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

It is no secret that real estate agents have had a long-term love-hate relationship with Zillow since its online debut in 2006. Its advent, along with the other web-based portals that began to appear (Trulia, Realtor.com, Homes.com), inaugurated the transition of real estate information from the carefully guarded hands of real estate agents to the masses and fundamentally changed the industry.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Although there has always been significant tension between the online portals and real estate brokerages and their agents, the current war between Zillow and Compass has caused many to take a deeper look at Zillow and, as a result, has raised more than a few questions about some of Zillow’s practices.

A look at the war between Compass and Zillow

To begin, let’s take a quick look at the current issue with Compass. In a nutshell, Zillow takes listings from the various MLSs across the country and posts them on its website. It then captures leads (mostly buyers), which Zillow then turns around and sells to participating agents who pay (at a basic level) a monthly fee for a prescribed number of leads or (for a higher level of better “qualified” leads) a monthly fee and a subsequent referral fee for closed transactions.

The rub here for many real estate agents is that they believe the leads should belong to them because they (as listing agents) do all of the legwork up front to develop a relationship with a seller, pay the costs of marketing and servicing the listing, and so on.

Zillow’s contention has always been that listing agents and their brokers do not do a good enough job of online marketing, thus providing a foothold for companies such as Zillow and Realtor.com, which, by spending significant amounts to market those leads online, should reap the benefits.

Zillow and other online portals rely on MLSs to provide them with data feeds that, in turn, provide the flow of listings they need to continue their business model. Enter Compass, which, by setting up its own independent feed of off-market listings, is cutting off some of the potential flow of listings to Zillow, thus undermining Zillow’s business model.

Compass — and I’ve certainly commented on this in other posts — has been flying in the face of many other brokerages with their blatant opposition to NAR’s Clear Cooperation Policy.

In retaliation, Zillow is refusing to allow any listings that have been previously marketed on off-MLS sites for more than a day to come onto its site. Let me clearly state that I support NAR’s CCP and, as such, do not agree with any attempts to set up private listing portals. With that out of the way, Zillow’s action does raise a number of questions that will now be played out in the courts.

How Zillow’s brokerage status changes the picture

An important distinction to understand is that, unlike web-based portals such as Realtor.com, Homes.com and Trulia, Zillow is actually a broker in all 50 states. This means that Zillow operates by the same rules that govern brokers and their agents, a fact that separates Zillow from information-only portals.

One immediate question that arises from any given broker refusing to post any listing is the question of potential steering.

Although I am not an attorney or capable of dissecting the finer points of the conflict, the overall topic of Zillow brings up some other questions about Zillow’s long-term intent and how real estate agents can continue to navigate with this “elephant” in the room effectively.

At the heart of the issue is whether or not a portal is providing information or advice. If they are providing information, then they are acting as a web-based portal. If they provide advice, however, then they are entering into brokerage territory. There is no doubt that this is a finely nuanced discussion, and, at the end of the day, is fraught with legal implications.

Take, for example, the idea of posting school scores. If you are simply a web-based information portal, then you can link to sites such as Great Schools and display their results for any given property. As such, and with the correct disclaimer, information is being displayed with no advice or interpretation.

As a broker or agent, however, the rules are different. To stay clear of fair housing violations and to avoid any appearance of steering, brokerages and their agents can disclose the existence of sites that provide school scores and even provide their clients with links to those sites, but should not communicate the actual scores themselves.

Brokerages and real estate agents can do the following:

- Provide links or resources where buyers can research school performance themselves.

- Direct buyers to official sources for more detailed and up-to-date information (GreatSchools.org, Niche.com, state Department of Education websites).

Brokerages and their agents should avoid:

- Providing specific scores or data.

- Providing assessments or judgements (“this is a horrible school” or “that is a great school district”) can be considered to be steering and a violation of fair housing laws.

- Excluding or recommending neighborhoods based on school information.

To avoid any fair housing laws, Zillow and other brokerage sites, such as Redfin, follow strict guidelines to maintain a legal safety net:

- They present data from Great Schools “as-is,” not curated in any way.

- They provide disclaimers indicating the source of the data and encourage users to verify the information independently.

- They let users of their website draw their own conclusions.

- They ensure there is no editorializing or interpreting of the scores.

- They maintain a role closer to a search engine or web-based informational portal that provides them with more leeway than a licensed real estate agent offering guidance or advice.

Even though Zillow provides adequate legal disclaimers, there is still risk, and any brokerage displaying school scores opens itself up to potential violations in an indirect manner.

- When it comes to fair housing laws, impact matters. Whereas the intent may have been to simply provide information, if that data is used by a consumer to avoid certain properties or areas, then the heart of fair housing laws has been violated. If the school scores are posted on an information-only web portal, there is no issue. If they are posted on a brokerage site, however, it is different.

- If school scores can be demonstrated to steer certain demographic groups toward or away from any given area — even in a passive manner — this could then be challenged in court, especially if there’s a pattern of disparate impact.

- This is not a new issue: Consumer advocacy groups and HUD have complained about this practice, though, to date, no landmark case has held Zillow liable. Responding to concerns that have been raised about this practice, while Zillow has made changes to the way the information is being displayed, it chosen not to remove the data.

As you can hopefully see by now, the inherent nuances are the issue, which brings up the next potential issue.

Zillow’s ‘suggested offer prices’

I am going to guess that many agents simply do not know about this feature on Zillow’s site. Set approximately 50 percent of the way down the page of an active listing, this feature not only provides Zillow’s trademark Zestimate (along with its accuracy percentage over the past 10 years), but also outlines strategies a buyer can employ potentially to write a winning offer. Maybe it’s just me, but this looks like advice, not information.

As an example, a home listed at $1,098,000 shows a Zestimate of $1,075,400. Under the Explore offer strategies headline are four buttons: Strong, Competitive, Moderate and Weak.

- By pressing the Strong button, Zillow suggests that an offer of $1.09 million-plus has an over 90 percent chance of winning.

- Press the Competitive button, and Zillow suggests that by writing an offer between $1.07 million and $1.09 million, you now have a 70 percent to 90 percent chance of getting your offer accepted.

- Hit the Moderate button, and the numbers $1.07 million to $1.07 million are displayed, along with a 50 percent to 70 percent chance of getting your offer accepted.

- Finally, by using the Weak button, Zillow suggests that an offer between $1.01 million and $1.07 million has less than a 50 percent chance of winning.

While these numbers for the specific property I used are close to the list price, I have seen instances where the recommended numbers are dramatically lower than the list price.

Here are some important things to consider:

- With this feature, even though the numbers provided are automated, Zillow is providing advice, which puts it squarely in the category of a broker or real estate agent.

- It is using its Zestimate to provide the basis for recommendations, which, as has been demonstrated amply over the years, is not accurate enough to provide sound pricing advice.

- By providing advice as to a recommended offer price lower than the list price, it is acting in direct competition with the listing agent and the seller.

All of this poses some serious concerns and questions:

By offering pricing suggestions — even algorithmically — this can be construed as real estate advice, which is inherently a part of a real estate agent’s fiduciary role.

This can interfere with buyer-agent relationships if a buyer’s agent recommends a specific offer price, based on their market knowledge, conversations with the listing agent and condition of the property, and Zillow recommends a lower price. This could potentially:

- Undermine the agent’s ability to represent their client

- Create confusion and mistrust between agent and clients

- Significantly impact negotiation strategies

This can also introduce potential liability:

- By providing “advice,” Zillow could potentially be construed as establishing an agency relationship with a buyer.

- If buyers rely on Zillow’s “suggested pricing” and either lose out on a home by offering too little or, inversely, overpay, there could be potential legal risk and liability, especially if it could be proven that the data was flawed. (Since the data is based on the Zestimate, which does not provide information based on property condition, photos, etc., the chances for error are high.)

While Zillow attempts to mitigate concerns or liability by labeling its suggested prices as “an estimate,” including disclaimers such as “not a guarantee” and avoiding direct “you should offer this” language, they are still, in my opinion, skating on very thin ice.

ChatGPT provides the following assessment:

Zillow is skating a fine line by posting suggested offer prices. It’s not illegal, but it treads dangerously close to giving what amounts to licensed advice — especially since Zillow holds brokerage licenses.

They’re relying on:

-

- Automation, not personal guidance.

- Disclaimers to reduce liability.

- Their platform status, not direct agent representation.

As a result, this practice has drawn criticism from brokerages, real estate agents, legal analysts, consumer advocacy groups and industry watchdogs alike.

The irony here cannot be overstated: While we are in the midst of a battle over Clear Cooperation, with Zillow refusing to show listings on its portal that are not on the MLS, sellers, aware of the fact that Zillow’s Suggested Offer Prices may in fact be competing directly against their chances of a competitive price (to be fair, Zillow sometimes recommends higher than list price offers), may not want their listings (even though they are on the MLS) shown on Zillow.

What a tangled web we weave.

by Lillian Dickerson | Jun 25, 2025 | Industry, News Feed

Homebuyers continued to respond to market headwinds like high mortgage rates and economic uncertainty and failed to be drawn in by builder sales incentives.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

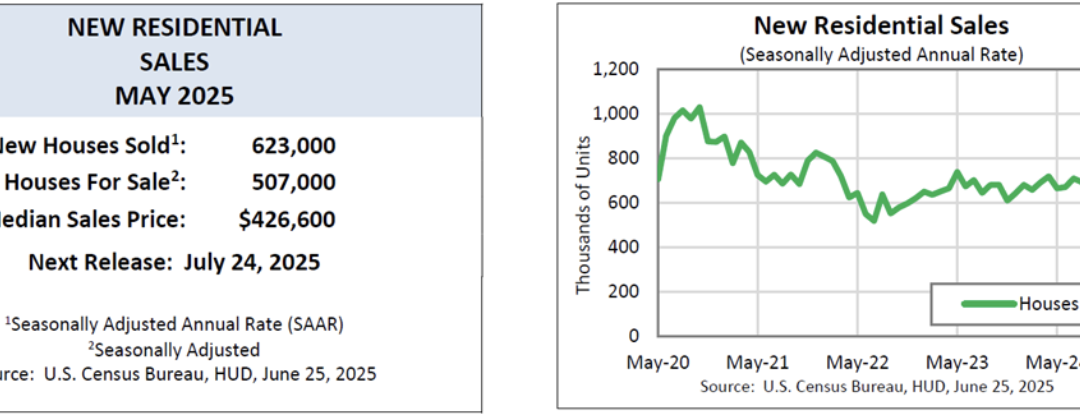

Sales of newly constructed single-family homes dropped 13.7 percent in May 2025 from the previous month, as homebuyers continued to respond to market headwinds like high mortgage rates and economic uncertainty and failed to be drawn in by builder sales incentives.

The seasonally adjusted annual rate of sales hit 623,000 in May, which was 6.3 percent below the May 2024 rate of 665,000, the U.S. Census Bureau and U.S. Department of Housing and Urban Development reported on Wednesday. The figure represented the most severe drop in new-home sales in nearly three years.

TAKE THE INMAN INTEL SURVEY FOR JUNE

The report comes on the heels of the Census Bureau and HUD’s report last week showing that housing starts slid by 10 percent in May to their lowest level since 2020.

“New home sales plunged in May,” Navy Federal Credit Union Chief Economist Heather Long said in a statement sent to Inman. “The spring and summer are shaping up to be very tough for the real estate market. Buyers are staying on the sidelines as they worry about uncertainty and high mortgage rates. New-home inventories edged up in May and remain at elevated levels. Buyers are waiting for deals and there just aren’t many of them right now.”

The seasonally adjusted inventory estimate for new homes was 507,000 at the end of May 2025, 1.4 percent above April 2025’s estimate and 8.1 percent above inventory levels in May 2024.

The figure represents 9.8 months of supply of new homes at the current sales rate, which is 18.1 percent above the April 2025 supply of 8.3 months, and 15.3 percent above May 2024 levels of 8.4 months.

In May 2025, the median sales price of new homes sold was $426,600, 3.7 percent above the median price in April and 3 percent higher than the median sales price in May 2024.

The average sales price for new homes sold in May 2025 was $522,200, 2.2 percent higher than April and 4.6 percent higher than the average in May 2024.

Email Lillian Dickerson