Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Even as markets muddle through uncertain waters today, high-net-worth clientele remain attracted to luxury real estate as an investment.

But this year, luxury buyers have proven to be more selective and ready to take a hard-line approach to their homebuying goals with an eye on cash deals, according to Coldwell Banker Global Luxury’s 2025 Mid-Year Report released on Wednesday.

The report analyzed market data from 120 markets in the U.S. and surveyed responses from more than 200 Coldwell Banker Luxury Property Specialists to predict luxury trends over the next six, 12 and 24 months.

Michael Altneu | Coldwell Banker Global Luxury

Out of those Coldwell Banker luxury agents surveyed, 68 percent said their clients are at least maintaining, if not increasing, their exposure to real estate. Many are also opting out of financing at a growing rate, with 51 percent of luxury agents reporting an increase in all-cash transactions.

The findings add up to a luxury real estate market in a period of adjustment, said Coldwell Banker Global Luxury Vice President Michael Altneu.

“So far in 2025, we’re seeing a luxury real estate market that isn’t fully bullish or bearish — but rather recalibrating,” Altneu said in a statement. “Affluent homebuyers still see real estate as a safe haven to grow and protect their wealth, but as the market balances and more inventory comes online, they can also be more choosy than in recent years. Practical considerations including home affordability, tax strategy, estate planning and long-term investment potential are taking precedence over aesthetics, flashy amenities or location. This could market the return of what we call ‘smart luxury’ — a mindset shift where discernment and strategic decision-making take priority.”

Different classes of luxury buyers are responding to market fluctuations in contrasting ways, Altneu added in the firm’s report. The “aspirational affluent” are reacting to financial market volatility by pulling back from real estate while the ultra-wealthy are digging their heels into the most high-end real estate assets, Altneu said, “driven in part by a desire to diversify out of equities and into real estate, which is seen as a safer, more stable asset class.”

Looking at the months ahead, luxury real estate agents can expect wealth strategy, “smart luxury,” move-up buyers, the ultra-wealthy and aspirationally wealthy divide, and cash purchases to increasingly impact the market.

Real estate remains a stable wealth strategy

Despite economic headwinds including high home prices and mortgage rates, a volatile stock market, Trump administration tariffs and more, many luxury buyers remain of the opinion that real estate is a stable investment, Coldwell Banker’s report shows.

Jessica Lautz | NAR Deputy Chief Economist

The nearly 7 in 10 luxury agents who said their clients are either upholding or growing their exposure to real estate shows the level of confidence high-net-worth individuals place on real property as an investment. Nearly 60 percent of luxury agents said they feel somewhat or extremely confident about the health of the market today.

At the opposite end of the spectrum, only about 11 percent of luxury agents said their clients are decreasing their real estate assets in favor of other investments.

“Real estate can be a place to park money, and when the world feels uncertain, we often see an interest in home and real estate purchases,” National Association of Realtors Deputy Chief Economist Jessica Lautz said in the report. “With the recent volatility in the stock market, the affluent may be looking to diversify their assets and invest in real estate since they view it as a more secure asset.”

The ‘smart luxury’ movement

Carla Rayman Kidd | Coldwell Banker

Luxury buyers today are much more keen on buying homes that are completely aligned with their ideal property features or condition — and a lot less willing to compromise on those properties that don’t fall into these categories, Coldwell Banker said in the report.

Those high standards might also be contributing to growing inventory, the report noted. Since 2023, inventory of single-family luxury homes is up 40.4 percent and inventory of attached luxury homes is up 42.6 percent. Rising inventory levels are also serving as a feedback loop of sorts, the report said, with buyers becoming more selective as more inventory becomes available.

Those “smart buyers” that Altneu mentioned are also waiting for a perceived deal.

“Many luxury buyers are trying to get a ‘deal’ on a home that may have been sitting on the market for a longer period of time — trying to take advantage of the current economic conditions of the world,” Coldwell Banker luxury agent Carla Rayman Kidd of Sarasota, Florida, said in the report.

Move-up buyers moving on in

Georgie Smigel | Coldwell Banker

With home prices continuing to climb, homeowners are gaining new levels of equity and graduating into luxury buyers, the luxury report found. The number of million-dollar homes is also increasing as a result. In the last year, almost 300,000 homes sold above the $1 million mark, up from 275,000 homes the previous year, according to data from Realtor.com.

“Prices have increased, forcing move-up buyers to now become luxury homebuyers — especially if they want a newer home,” Georgie Smigel of Coldwell Banker Realty in Cranberry Township, Pennsylvania, said in the report.

For every 1 percent increase in home prices, about $350 billion in home equity is generated, according to NAR data cited in Coldwell Banker’s report. “That means a gain of nearly $1.3 trillion in home value appreciation at a time when the stock market is undergoing a correction,” NAR Chief Economist Lawrence Yun said during NAR’s quarterly Real Estate Forecast Summit in March.

The aspirational and ultra-wealthy buyer divide

Winston Chesterfield | Barton Consulting

While many agents with ultra-luxury buyers (those in the top 5 percent of the market) reported an increase in transactions, those with lower-tier luxury buyers reported more hesitancy as financial market remain in an uncertain place.

Ultra-high-net-worth buyers tend to be “more globally minded, with larger investments exposed to geopolitical shifts,” Barton Consulting founder Winston Chesterfield said. “High-net-worth buyers, on the other hand, are often more focused on immediate, practical concerns — like interest rates, inflation, and taxes. They’re thinking in terms of their own financial world, not the global one.”

However, looking at the data, Coldwell Banker Global Luxury found no significant performance gap between the top 5 percent and top 10 percent of the market during the first five months of 2025 compared to the same period the year prior. “When comparing the top-performing tier to the broader luxury market, differences have been marginal — except in a handful of powerhouse markets,” the report stated, pointing to top-tier sales in Los Angeles, New York City, Miami, Palm Beach and Aspen.

Cash is king

Jade Mills | Coldwell Banker

Luxury buyers are known for their use of cash in transactions to avoid those pesky interest rates that have remained elevated in recent years. And according to Coldwell Banker’s report, that isn’t changing this year.

A massive 96 percent of Coldwell Banker luxury agents reported that buyers are either maintaining or increasing their use of cash purchases.

“Ultra-high-net-worth individuals aren’t just buying one property — they’re building real estate portfolios,” Jade Mills, president of Jade Mills Estates and International Ambassador of the Coldwell Banker Global Luxury program, said in the report. “These buyers are paying all-cash specifically because they want hard assets independent of market swings. When you’re dealing with generational wealth, real estate becomes a cornerstone strategy, not just a lifestyle purchase.”

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

The next time you’re questioning your effort and your impact, coach Darryl Davis writes, look at the ripple effect of all you do and the lives you touch.

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

In the hustle of daily life, it’s easy to lose sight of just how powerful and essential you are as a real estate professional. Are you feeling undervalued, overwhelmed or disconnected from the bigger impact of your work? Maybe you wake up, check your emails, return calls, set up listings, negotiate deals and hustle to make things happen for your clients, but it feels like you aren’t making a difference.

Let me remind you of something — what you do is bigger than just you. It’s bigger than just one home sale or one closed transaction. What you do sends ripples through the world, affecting dozens — no, hundreds — of lives with just a single deal.

The chain reaction of a single transaction

Let’s break it down.

When a house goes on the market, the impact begins immediately. The moment you take that listing or help a buyer find their dream home, an entire network of professionals jumps into action. Photographers, videographers and stagers help showcase the property. The MLS system processes the listing, and the people working behind the scenes at the MLS ensure it’s up and running smoothly.

Then comes the appraiser, the home inspector and the contractors making necessary repairs. That’s just the beginning.

Now think about the painters freshening up a home, the landscapers boosting curb appeal, the house cleaners ensuring everything shines. Movers step in to transport families to their next chapter.

Loan officers, underwriters, title companies, attorneys and insurance agents all play their roles, each earning a living from that one transaction. Every single person involved supports their family with the income they earn, thanks to the ripple effect of your work.

The ripple expands further

The marketing teams designing brochures and ads. The sign company crafting the For Sale sign. The surveyor ensuring boundaries are set. If the home was staged with rented furniture, that’s another business benefiting.

Once the home sells, utility companies gain a new customer, local restaurants welcome a new family and storage facilities provide solutions for transitions. The city and county clerk’s office process paperwork, generating revenue for public services. Even the neighbors are affected — new faces in the community mean new relationships, new stories and new beginnings.

And let’s not forget the emotional and social impact.

You’re not just selling a house. You’re helping a family find a home where memories will be made, where children will take their first steps, where celebrations will happen and where lives will be lived.

You’re guiding sellers through a transition, whether it’s upgrading, downsizing or moving forward after a major life change. Every decision, every negotiation and every conversation carry weight beyond the immediate sale. It shapes futures.

Real estate as a force for good

Every real estate transaction you touch is a ripple that spreads outward, changing lives in ways you may never even see. And that’s why what you do matters so much.

I get it — some days are tough. Deals fall through, clients get difficult, the market shifts. It’s easy to get caught up in your own challenges, focusing on the to-do lists, the numbers and the commission checks. But when you remember the bigger picture, when you recognize how many people are impacted by your success, it changes the game.

Your work isn’t just about you — it’s about the hundreds of people who rely on you, directly and indirectly.

So, the next time you’re feeling frustrated, the next time you’re questioning whether all the effort is worth it, take a step back. See the bigger impact. Feel the ripple effect of what you do and let that energy push you forward to your next level.

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Pulse is a recurring column where we ask for readers’ takes on varying topics in a weekly survey and report back with our findings.

With political and economic uncertainty in the air and in the midst of a multi-year down market cycle, finding qualified buyer leads is job one for many agents. Whether they come from your broker, from your sphere of influence or from paid channels, it’s not easy to find buyers who have all their ducks in a row financially and logistically.

So let us know: How are you getting buyer leads in today’s market? Once you get them, how are you converting them? Do you hold buyer consultations or otherwise qualify your buyers before you start showing them homes? Do you create content, focus on past clients and referrals, or are you paying for leads? Share your secrets below:

We’ll compile a list of the top responses and post them on Inman next Tuesday.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The U.S. bombing of nuclear sites in Iran that quickly sent the country to the brink of another broad conflict in the Middle East has added one more issue for those mired in a sluggish real estate market to worry about.

Of course real estate professionals never count on world conflicts to influence their bottom line, and war is a tragedy first and foremost for those directly in harm’s way. But the situation in Iran has the potential to ripple through global economies — impacting, among many others, real estate professionals and the people they serve.

With that in mind, we sought to make sense of what happens to housing when conflict breaks out, as well as what has happened to home sales historically during times of war involving — directly or indirectly — the U.S.

The result of this effort suggests that so far, economists haven’t seen responses in the relevant markets that might further hurt home sales.

Matthew Gardner | Gardner Economics

“Right now there is caution,” Matthew Gardner, an economist with Gardner Economics, said. “But we haven’t seen any kind of panic, whatsoever.”

Those signs of panic would likely first appear in oil, stocks and bonds.

In this case, economists have quickly turned their attention to the conflict’s impact on oil prices.

Oil is a direct and indirect source of inflation in the economy, so a conflict that leads to even the threat of Iran closing the Strait of Hormuz, a choke point in the Persian Gulf where roughly 20 percent of the world’s oil supply flows, was thought to send oil prices higher. The possibility that Iran would close the strait has been widely discussed during the conflict.

“That could have led the Fed to delay cutting rates even longer, and potentially you could see mortgage rates spiking,” Gardner said. “But that one thing didn’t happen.”

If oil prices rise, it could push up the consumer price index, making it even less likely for the Federal Reserve to cut the federal funds rate, which has an indirect effect on mortgage rates.

Instead, oil futures fell during the first hours of trading after the U.S. strikes on Iran and were down 8.6 percent as of mid-day Tuesday.

Oil prices as of mid-day on Tuesday, June 24, 2025

Economists next watch for volatility in equity markets. Had there been a sell-off in the stock market that drove down share values, investors and other potential homebuyers may have had less wealth with which to buy a home, Gardner said. That could have had an even bigger impact on the luxury market.

“But we didn’t see that,” Gardner said. “So far, so good.”

The third thing Gardner said he’s keeping an eye on is whether there are indications that global investors are moving money into the U.S. via real estate or the bond market.

“You could actually see money coming in, potentially, to the U.S. because it’s considered to be a global safe haven. Also it’s the global currency,” Gardner said. “That has the potential to actually lower mortgage rates.”

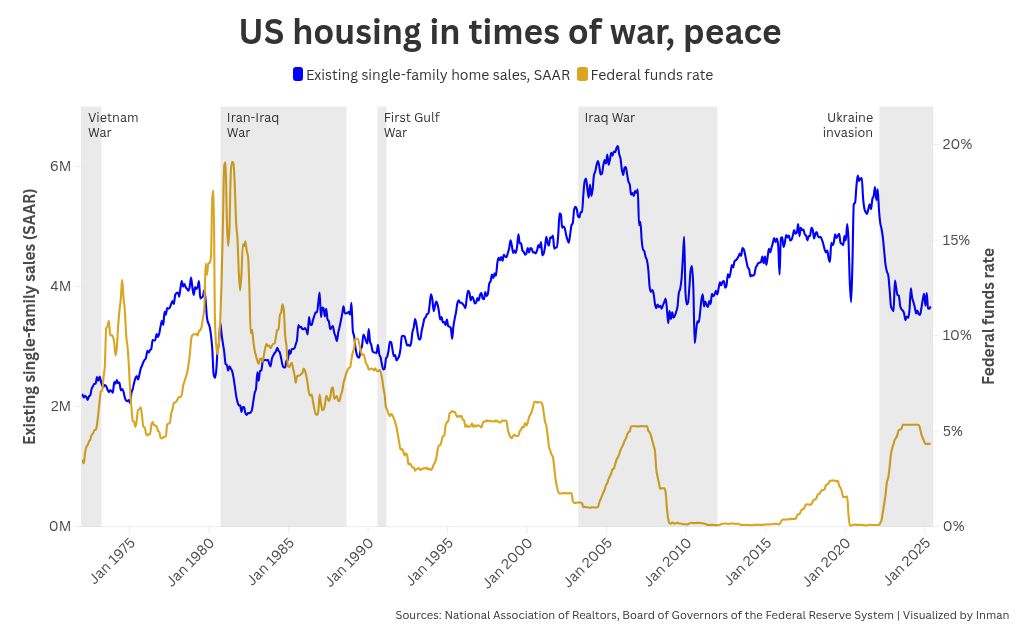

War, peace and interest rates

Inman analyzed the data for existing single-family home sales dating back to January 1965 to try and understand the impact of war involving the U.S. and the housing market.

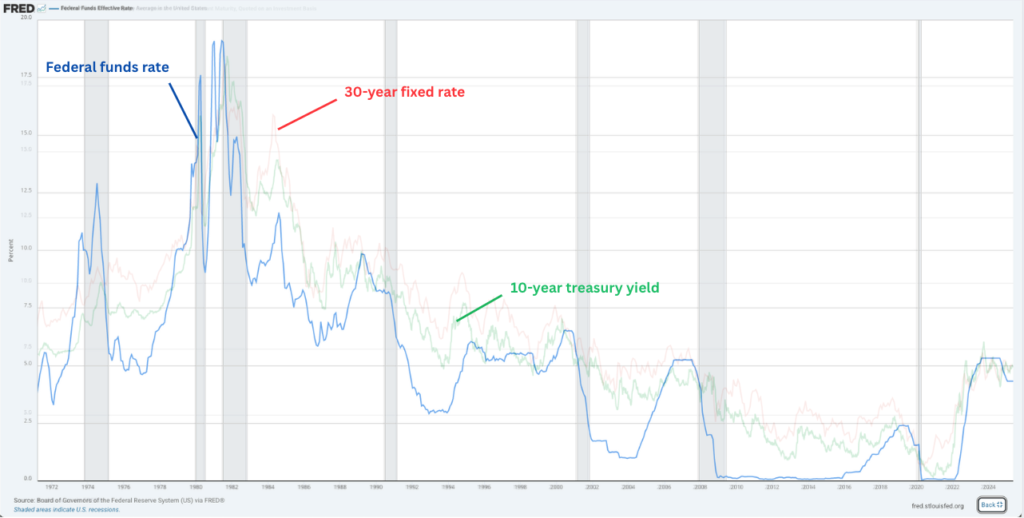

And while there are some trends in home sales that appear to generally track global conflicts, they also appear to more closely track the 30-year fixed rate, federal funds rate and 10-year treasury yield.

While this is not a comprehensive analysis of all factors — for instance, recessions and mortgage rates — it does paint an interesting picture.

The graph above shows that decades ago, home sales fell sharply as the Federal Reserve quickly raised the federal funds rate to combat quickly rising inflation. That happened to coincide with the Iran-Iraq War, when home sales fell before beginning to climb in mid-1982.

Operation Desert Shield began Aug. 2, 1990. The following day, mortgage rates were 9.84 percent. Rates jumped to 10.29 percent within three weeks and remained above 10 percent for much of the operation before beginning a long descent.

Home sales followed suit, with a sharp — and brief — decline and then rebound.

10-year Treasury Yield, the federal funds and 30-year fixed mortgage rates. FRED

In the case of Operation Desert Storm, which lasted for about six weeks in early 1991, rates fell.

Later, sales dipped sharply following the September 11 attack on the World Trade Center and invasion of Afghanistan before continuing a climb during the early years of the U.S. war with Iraq.

Sales continued to climb toward the apex of the housing bubble that burst in September 2005, preceding through the Great Recession.

The takeaway is that home sales more closely track things like mortgage rates than wars, though there are conditions caused by war that can impact rates and sales.

And while the Federal Reserve is currently walking a tight rope between taming inflation and keeping rates high for so long it causes a recession, Gardner said it wasn’t a recession specifically that had economists worried about the housing market.

“Some could argue that if it becomes bigger,” Gardner said, “and involves more of the Gulf states, we could see more of an economic global slowdown.”

Data editor Daniel Houston contributed to this story.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Ben Franklin is credited with saying, “In this world, nothing can be said to be certain, except death and taxes.” Depending on your income bracket and what happens with Trump’s “Big Beautiful Bill,” taxes might no longer be a certainty. Death, on the other hand …

With apologies to Mr. Franklin, I’d like to add one other certainty to the list: Uncertainty.

As I write this, Iran, Israel and (in a limited capacity) the United States are in a shooting war, which adds to potential uncertainties with oil shocks, a higher 10-year Treasury Bond, wavering consumer confidence, a lull in building starts and continued uncivil “civil” discourse. Our clients may be, understandably, on edge.

Yet, to quote from the National Association of Realtors’ Code of Ethics, “Under all is the land.” Sellers got to sell, buyers got to buy (fish got to swim, birds got to fly) and, based on history, real estate is still the safest investment out there.

So, how does an agent go about advising and guiding clients in these turbulent times? The same way we do it on a day-to-day basis. We constantly deal with turbulence. We walked our clients through the catastrophe of the 2008 economic meltdown.

On an ongoing basis, we deal with life-altering events: California agents help clients deal with the effects of wildfires, floods and earthquakes. In the Midwest and plains states, there are tornadoes, rain storms and freezing temperatures. Florida and the East Coast face hurricanes, and in New York City alone, there are the perennial disasters of the Knicks, Mets and Jets (wait till next year!).

Our clients already come to us for advice on the real estate market because they trust us. We’ve already helped them with one of the biggest (if not the biggest) investments of their lives, we guided them through the mortgage process, the vagaries of the insurance market, and they continue to come to us for advice on vendors, restaurants, and whether to remodel, refinance or sell.

But how can we advise clients on real estate when there are so many uncertainties flying around? By swatting them down, one small swipe at a time. Here are five tips to help.

Start big, go small

You don’t have to be an expert economist to sound like one. Break down economic information into digestible bites for your clients, starting with the national housing statistics from NAR, then move down to your state and county figures (available from your state Association) and finally narrow down to your local market (MLS).

Whether you are working with buyers or sellers, the conversation can go something like this: “Nationally, we’re looking at an average increase of X percent for days on market. On the state level, it’s actually lower at Y percent, but for our area, we’ve seen an even smaller shift of Z percent over the past three months, which means [insert your take here].”

If you’re already framing things this way, bravo. But if you’re reading this thinking “My clients don’t care about the national averages,” remember that a lot of agenting is perception. By going from national to local, you’re showing your clients that you consider a broad range of statistics to shape your view of the local market — something your competitors might not do, which bumps up your credibility.

Understand what’s affecting the numbers

If you normally check your email during the economic forecast of your local or state meetings, it’s time to pay attention. National and local forecasts are not always correct; however, their broad overview not only helps you frame economic factors for your clients, but it also gives you a basis to compare figures.

Not a numbers person? You don’t need to bench 250 pounds of economics; you can get results from doing 10-pound curls through entertaining and informative podcasts like Marketplace or watching the UCLA Anderson School forecast, which are incredibly digestible.

You don’t need to do it alone (and you shouldn’t)

If you are a residential agent, talk to residential income agents, or (shudder) commercial agents (I promise, they may be gruff, but offer to buy them a coffee and they soften up). Get their perspectives on the market, and find out what their clients are saying. Don’t stop there; talk to agents from different parts of the state, other states and even other parts of the country. Learn how they’re having these conversations with their clients and adapt what you like to make it effective for your clients.

And don’t just listen to groups — individuals are often influenced by groupthink and are more apt to share what they are really feeling in a one-on-one conversation, as evinced by this short and interesting video.

Don’t be afraid to say ‘I don’t know’

For whatever reason, so many agents hate saying “I don’t know,” and I have to admit I don’t know why. Quick question: I just said “I don’t know.” Do you have a lower opinion of me?

Ask your eye doctor what that weird mole on your back is, and they’ll probably say, “I don’t know.” (They may also say, “Please don’t do this in public.”) That said, they’ll probably follow up with, “Here’s the name of a specialist who will know.”

We say “I don’t know” all the time when it comes to a question about plumbing, electric and HVAC systems, but for some reason, when it comes to questions about the market, the reflex is to give an (often uninformed) answer. Maybe we’re afraid they’ll talk to another agent … who can also give them an uninformed answer. Whatever the reason, stop!

Learn to channel your inner doctor and say, “I don’t know, but let’s call X and see what they’re hearing.” Develop a broad range of experts: lenders, attorneys, CPAs, heck, even other agents. Swap information, learn from their expertise and demonstrate your expertise, and soon enough, you’ll be viewed as an expert. (Oh, and by the way, get that mole looked at.)

You don’t need to have all the answers, but you need to be present

Our clients trust us. There’s a lot of uncertainty these days from seismic shifts in how our government works, to civil unrest, to natural disasters, to international conflicts. We don’t have any say, sway or impact over these things, but “under all is the land.” And your clients are looking to you to help them make sense of what’s happening, not just with the market, but with their home.

Your clients don’t need you to have all the answers; they just need to know that you’re there for them and that you’re willing (and able) to help them navigate these rough seas. Your clients need to feel like you’re all in on this journey with them, and you need to be ready for the task.

Spencer Krull is a managing broker with Side, and also works as a real estate expert witness and consultant for attorneys.

By promoting family-friendly amenities, Victoria Kennedy writes, you can make your marketing more irresistible to moms and dads who are ready to become homeowners.

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

There’s little question that price will always be a factor in real estate. However, if you’re trying to attract families to your listing, or if you frequently work with families as a buyer’s agent, cost doesn’t always drive their decision to put down a bid. For many homebuyers who have (or intend to have) children, planting roots in a neighborhood that features family-friendly amenities takes precedence over price.

This presents a major opportunity. Research shows that younger families are moving into the suburbs in record numbers. According to 2024research from the Economic Innovation Group, twice the number of families have relocated into more rural areas than before the pandemic. In other words, your suburban or rural market may have more interest from families seeking properties that aren’t in congested cities.

What exactly can you do to appeal to all these families looking for the type of real estate your market offers? Try including some of these features within your marketing.

Community gathering spaces

Highlight indoor and outdoor areas that are accessible to all homeowners. These can be a huge draw for parents with kids.

Pools and well-designed playgrounds catch the attention of families looking to find the ideal place to call home. In terms of indoor spaces, a community fitness facility and room for events show families that the community has anticipated their needs. Some people like the idea of hosting gatherings in spaces other than their homes. Consequently, it’s convenient for them if they have a neighborhood space at their disposal.

Walkable areas

Far too many children are nature-deficient, spending less time outside than they should. And being cooped up can have long-term ramifications. As noted in recent research, nature deficiency can lead to cognitive, social and behavioral issues. Therefore, parents seeking real estate may want walkable areas.

An example of walkability could be extra-wide streets or sidewalks. Even if a listing’s neighborhood doesn’t have those features, it may still be appealing if it’s close to trails or paths. That way, families can get the exercise they need.

Be sure to consider communities that are friendly to bike riders as well. People for Biking research shows thatbicycling is trending across the United States. Highlight bike racks set up throughout a development to encourage families to bike together.

Sustainable features

Young families are into the practice of sustainability. For instance, younger drivers are opting for electric vehicles more frequently than older drivers, according toPew Research. With this in mind, highlight homes and neighborhoods that feature electric vehicle charging stations.

There are other ways to show that a neighborhood has been planned with sustainability in mind. Landscaping that includes native plants that aren’t hard on the environment and don’t use a lot of fossil fuels to maintain offers responsible curb appeal.

Another eco-friendly feature is solar-powered exterior lights. The less reliant lights are on the electric grid, the better. Be sure that you’re letting potential homebuyers know about sustainable offerings in all your listings’ marketing materials.

Safety updates

Parents want to raise their children in safe communities. Consequently, do all you can to highlight safety features. Recently repaired or redone sidewalks and common spaces are a good place to start. Well-lit neighborhoods and safety enhancements, such as street lamps or community entrance spotlights, are good features to point out to potential buyers.

Business and education accessibility

Offering easy access to the community may be a differentiator for a neighborhood. For example, you may want to emphasize proximity to local businesses, eateries, stores and schools. Many planned communities feature on-site places to dine and shop. If you’re able to include those types of establishments within your pitch, you may increase desire and demand from first-time and young homebuyers with growing families.

Every time you add a family to your market, you’re adding more diversity to the fabric of the neighborhoods you serve, while boosting your revenue streams. Families can be finicky about where they decide to plant roots. By focusing on promoting family-friendly amenities, you can make your service more irresistible to moms and dads who are ready to become homeowners.