by Latham Jenkins | Jun 27, 2025 | Industry, News Feed

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Selling real estate — especially high-end, luxury real estate — demands more than just showcasing a beautiful home; it requires an unforgettable storytelling narrative. I have mastered the art of transforming property showings into immersive, lifestyle-driven experiences that have captivated some of my wealthiest buyers.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

But storytelling isn’t just for luxury sales; it’s a strategy any agent can use to create stronger, more compelling sales experiences.

Curate an experience, not just a tour

Luxury buyers aren’t just purchasing a home; they’re investing in a lifestyle. Instead of a standard walk-through, put together moments that highlight the unique qualities of the property. For example, I’ve set up a cocktail bar in the wilderness during a sunset showing, allowing potential buyers to witness a stunning display of wildlife, which helped me craft an emotional connection to the land.

Tip: Identify a property’s most compelling features — sunset views, cozy fireplaces, a spacious backyard — and structure your showing to highlight those aspects. For a starter home, consider staging an inviting breakfast nook or a special room or outdoor space that highlights the property.

Master the art of storytelling

There’s a story behind every property. As an agent, you must take the time to understand, articulate, and even do your own research on the history, features, and places surrounding the environment that will add value to the potential buyer beyond the square footage and amenities. Wealthy buyers often have an appreciation for heritage, exclusivity, and uniqueness.

Tip: Research a property’s past and its surrounding area. Highlight elements that make it one-of-a-kind, whether it’s historical significance, architectural craftsmanship, or a rare natural setting. Share stories about the neighborhood’s history, or even local shops or places that will help potential buyers envision their lives beyond just the four walls of a house.

Timing is everything

In my experience, luxury showings must align with nature, weather, and the season. A property might have breathtaking views at sunset, but those same views could be underwhelming on a cloudy day. I’ve carefully planned showings around the property’s most picturesque moments, from watching elk bugle at dusk to snowmobiling into a winter retreat.

Tip: Scout the property at different times of day and seasons to determine the best viewing experience. Consider sunrise for dramatic lighting, fall for vibrant foliage, or winter for cozy, fireside settings. For an open house, plan showings during the best natural light hours—typically mid-morning or golden hour in the evening. If a property shines in the spring, showcase it then, rather than in the dead of winter when the yard looks dull.

Transform showings into exclusive adventures

For high-net-worth buyers, exclusivity is superior. A showing should feel like an invitation into a world few have access to. I have taken buyers on snowmobile rides to remote properties, arranged fireside chats with ranch managers and even rowed clients across rivers to reach secluded estates.

Tip: Consider what unique activities can be incorporated into the showing. Could it be a private chef-prepared meal on the property? A horseback ride to a scenic overlook? The goal is to immerse buyers in the lifestyle they’d experience if they owned the property.

You don’t need a private ranch to create an experience. Consider hosting a neighborhood walking tour for potential buyers, providing a guide to local amenities, or setting up a coffee bar at your next open house.

Be prepared for the unexpected

Flexibility is key, especially with luxury showings. I’ve encountered unexpected challenges — from avalanche-blocked paths to unpredictable wildlife — but by being an expert in my area and having experience in crafting different solutions, I’ve ensured those kinds of experiences remain seamless and positive for my clients.

Tip: Have contingency plans for weather, transportation, and logistics. Luxury buyers expect perfection, so be able to pivot quickly. If a storm rolls in during a showing, have an umbrella ready. If a buyer is concerned about traffic noise, schedule their visit at a quieter time of day. Being prepared for small details builds trust with your clients.

Balance marketing with authenticity

At the core of luxury real estate sales is authenticity. Buyers at this level can recognize sales tactics instantly, so the experience must feel genuine rather than contrived. I always focus on allowing clients to naturally experience a property rather than delivering a hard sell. I’ve stopped trying to just get the sale and put emphasis on the storytelling.

Tip: Whether you’re selling a $20 million estate or a $250,000 starter home, let buyers explore freely. Offer insights and highlight key features, but don’t overwhelm them with sales pitches. Ask them questions about their lifestyle and help them see how the home fits into their future.

Selling high-end, luxury real estate is more than transactions—it’s about creating unforgettable moments that allow buyers to envision their lives in the property. By curating experiences, mastering storytelling, and delivering exclusivity, agents can elevate their approach and resonate with their clientele.

For real estate professionals at any level, the key is simple: Don’t just sell houses. Sell experiences. Whether you’re working with first-time homebuyers or seasoned investors, storytelling helps build emotional connections, create lasting impressions, and ultimately, close deals.

by Matt Carter | Jun 27, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

As chief economist for NewHomeSource, Ali Wolf manages and analyzes content for Zonda, runs special research projects and strategizes with the nation’s largest homebuilders.

As a featured speaker at Inman Connect San Diego, she’ll provide insights into economic factors, buyer behavior, and how market shifts are impacting consumers.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Wolf took the time to talk to Inman in advance of her July 31 Connect appearance. While mortgage rates and affordability present challenges for homebuyers, she said, uncertainty can be the biggest issue for many — and that’s something real estate agents can help their clients cope with. This interview has been edited for clarity and brevity.

Inman: I’m guessing you probably have a lot of data that you’re looking at. Everybody’s got their own local market, but talking just about the national market, is there anything that you’ve seen recently that stands out?

Ali Wolf: The one thing that I feel most comfortable saying about the national market is that across almost every geographic area, across almost every price point, we are in a housing market today that lacks any sense of urgency. There’s people that maybe want to buy, or can buy, that are just choosing not to. The consumer is fully steering the market today, and their uncertainty about broader things in their lives is resulting in a lot of uncertainty in the housing market.

In the past, rent versus own was kind of a coin toss. It depended on how much you could put down, and interest rates. What is happening now, almost everywhere across the country, is that renting is the obvious choice if you just look at the monthly housing cost. So it’s becoming a market where the dynamics look a lot more complicated and a lot more messy than what they have in the past.

How can real estate agents help their clients get some clarity?

There are going to be certain buyers that will be priced out. But those that could still potentially buy, they’re going to say, “Hey, if I rent, it’s $1,500 a month. If I buy, it’s $1,800 a month. I don’t want to buy because I don’t want to pay that extra money.”

Not everyone should buy, but this is where our industry should say, “What else happens when you buy a home? Well, now you’re starting to invest in yourself. Now you’re paying down your mortgage, now you’re setting yourself for retirement in the future. You’re no longer worried about what your rent increase is going to be, because you’ve now locked in the largest share of your monthly budget.”

If you look at renters versus homeowners, owners have nearly 40 times the wealth of renters. So there’s going to be the immediate objection, which is, “Why would I buy?” But then there is the logic of why you might still want to.

The advice from a lot of real estate and financial professionals is “Don’t try to time the market.” But what would you say to a buyer is thinking, “Well, maybe next year will be a better time to buy.”

People try to time the market when, at the end of the day, it’s time in market that matters. You want to be invested, and paying off that investment as soon as you can, versus trying to save 3 percent or 5 percent on the home price. That is not going to matter 10 years from now. But what you’ve invested in yourself over that time becomes more valuable.

I also would say that you can try to time the market, but you have no idea what’s going to happen in 3 years. Home prices could go down but interest rates go up. You could see interest rates go down but home prices go up. I just think there are too many unknowns.

When you look at consumer sentiment surveys, there’s a lot of uncertainty about what tariffs will mean for the economy. Unemployment has been creeping up, and consumer sentiment has been pretty dismal this year.

Let’s go back to trying to time the market. Let’s say next year, home prices start to come down and interest rates start to come down, but then everyone that’s trying to time the market time tries to come into the market at the same time. So now you’re competing with more people.

But then there’s an extra layer with tariffs, if they go through as discussed, tariffs are taxes. Taxes mean higher costs. Homebuilders, for example, are still building on some supplies that they bought pre tariffs, so their costs are not as bad. If you wait, maybe the building material costs go up, and so a builder maybe wants to lower their price, but they can’t. And then where are you?

Many existing homeowners are feeling the mortgage lock-in effect — they don’t want to sell because they don’t want to give up the low rate on their existing mortgage — and there are affordability issues in many markets. What needs to happen to bring home sales back?

The lock-in effect is one reason why we’ve seen the new home market do better, because builders can basically solve for it (by offering interest-rate buydowns and other incentives). New homes and resale homes are selling at about the same price, and new homes are offering a lot of incentives. So when given the same choice that consumers had in the past, new or resale, more people are saying a new home makes more sense.

I think time heals all wounds. Over time, the mortgage lock-in effect becomes less dramatic. If I bought a house when I was single, and I locked in a 3 percent interest rate, and then I get married and now I have two incomes, I may be in a position to move.

To see a meaningful rebound in the market, though, I think one of the most important things is consumer confidence. I think stability is the most important factor. People can adjust to higher interest rates. They can compromise on where they want to live, on certain aspects of their home. What they can’t adjust to is constant uncertainty and volatility. That will push people to the sidelines.

Obviously if interest rates came down, if home prices came down, if supply went up, if wages went up, those are all factors that could also help with the housing market.

Any predictions on the likelihood of those things happening?

You will not hear me on record forecasting mortgage rates today. There are so many moving parts.

I think the one that seems most likely is that we do see more supply. We’re already seeing that. Now, more supply can be a little bit challenging, because it can result in pricing coming down. But if we’re talking about how do we get some balance in the market, I do think more supply and a little bit of a downward pressure on pricing actually can be helpful to keeping the market moving in.

We calculate that at least 4 million homes will be sold in 2025, even as the housing market feels slow, even as the housing market feels bumpy.

That’s 4 million sales that are up for grabs. So it really becomes how do you capture your share? The pie is smaller, but if you can capture a little bit more of the share, you can still have a thriving business even in a bumpy market.

Email Matt Carter

by Jimmy Burgess | Jun 27, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Sometimes a success story comes along that inspires us and reminds us why we’re in this business. Taley Hunt’s is exactly that. Her story is a case study in grit, consistency and “leading with value” that catapulted a brand new mom from zero to more than 400 transactions in her first five years.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Hunt arrived in Columbia, South Carolina, in 2019 with no sphere, no budget and no roadmap. What she did have was a $41,000 higher-ed salary she wanted to replace, a baby on the way, and a willingness to “go in blind and messy until something clicked.”

“People keep telling new agents to ‘hustle,’” Hunt told me. “For me, that just meant taking whatever tiny thing I had, whether it was one client, one inspection, one model-home visit or whatever else I had, and turning it into content that let the world know I was in the game.”

That decision produced 28 closings her first year (with a newborn baby), 86 the next, 145 the next and — by early June of this year — she had 110 homes closed or pending on the board. Her team is tracking toward 200 sides and more than $1 million GCI this year, with virtually no paid leads.

Below is the exact framework she follows — a seven-point system any agent can model, no matter how modest the starting point.

She shows — then shows again

Hunt has built much of her success through social media and her authenticity on the platforms. Her first viral post was as raw as it gets: She wedged her newborn’s rocker between a monitor and a stack of listing agreements, snapped the scene and captioned it:

“Writing my first offer while my assistant naps.”

She never stopped. Day after day, she gave her followers a front-row seat to the building of her business. These posts have included:

- Selfies at model homes (“Touring new construction—come with me”)

- An eight-month-pregnant belly in a spec house

- A two-minute car video after an inspection (“Here’s what we found and how we’ll negotiate it”)

“I didn’t wait until I ‘deserved’ to post,” she says. “I documented everything — previewing homes no one asked me to preview, searching the MLS for six hours — because that shows you’re active in the market, not just posing in front of a sold sign.”

Why it works

When you are looking for your ideal audience, the fastest path to success is showing up as your most authentic self. Hunt’s success breaks down to three key components.

- Relatability: Clients saw a real mom juggling real life, not a flawless billboard.

- Visibility: Every Story went to Instagram, Facebook and TikTok. As she put it, “I try to double-dip everything.”

- Searchability: Hunt Googled “questions first-time buyers ask,” answered them on video and created evergreen SEO content that still circulates.

She always turns 1 deal into 2 … or 3

Hunt’s very first buyer came from a Facebook group where an out-of-state agent needed a Columbia referral partner. She snagged it, executed flawlessly and — before closing — asked that buyer a simple question:

“Who else do you know who might be buying this year?”

Sixty days later, she closed her first referral from that first client. “That was my lightbulb moment,” she says, “realizing every transaction is a tree with more fruit — you just have to water it.”

Hunt has built what she calls her “3-R flywheel,” a relationship-driven strategy that fuels consistent business without cold calls or heavy ad spend. The first “R” stands for relationships. She stays close to past clients through personal texts, interactive Instagram polls and behind-the-scenes Reels that keep her top of mind in a way that feels natural.

From there, her second “R” stands for referrals. She plants a simple but powerful seed at closing: “Can I count on you to introduce me to one person I can help this year?” That one ask, followed by a handwritten thank-you note, helped drive 32 percent of her sales in 2024.

Finally, her last “R” stands for reputation. By tagging vendors, lenders and referring agents in her social posts and Reels, she shines a light on others in a way that earns reshares and multiplies her reach.

She practices database discipline: DTD2 + weekly value emails

Hunt is fanatical about DTD2, a tagging schedule popularized by The CORE Training. Week 1 of every quarter? Call (or, in her case, text) everyone whose last name starts with A or W. Week 2: B & X, and so on. Result: Four personal touches per contact per year, baked into the calendar.

“I text; I don’t call,” she emphasizes. “Nobody wants surprise calls anymore. A quick check-in text feels respectful.”

She also does a weekly newsletter to her database every Friday. That Friday newsletter has a 48 percent open rate. The newsletter has three key components: Local life (farmer’s markets, festivals, 5Ks, etc.), a market snapshot (clear and simple updates on the market) and ICYMI (links to her top Reels so they stay relevant with the algorithm).

“I’m not trying to convert via email,” she says. “I’m staying relevant. If they see my name weekly and hear from me quarterly, we’re golden.”

She hosts client appreciation events regularly

She hosted her first client event in Year 2. It was a photo with Santa event, and 15 families showed up. “It wasn’t the turnout,” she notes. “It was the triple touch: invite, reminder, thank-you.”

Today, her team runs five signature events, all co-sponsored by lenders, inspectors and insurance reps. These include a spring egg hunt (300 attendees in March), a summer movie day (buys out the theater), a fall festival (food trucks, inflatables and vendor booths), Thanksgiving pie pickup (apple or pumpkin as options), and Santa photo and toy drive (her favorite and a great way to end the year).

If you’re a new agent or someone who has never hosted a client event, you may be feeling overwhelmed hearing all she does for client appreciation events. But she encouraged agents to “Start with one annual anchor event. As you master the process, layer in a second, then a third.”

She’s a digital farmer — for other Realtors

Out-of-state agents are her second farm. She nurtures them exactly like a neighborhood. She’s built an email list of agents in other markets, and she consistently adds agents to that list. Her approach to digitally farming for agent referrals includes:

- A monthly value email: “Steal my six highest-converting postcards.”

- Posting daily in group searches: She types “Columbia, SC agent?” into national Facebook groups twice a day to snag live referrals.

- Handwritten notes: She sends 10-15 cards weekly to top producers in feeder markets (Atlanta, Nashville, Dallas, Houston and Memphis): “I love paying 30 percent for buyers headed to Columbia. Here’s my cell.”

Forty percent of her 2025 pipeline now originates from agent referrals. Every closing triggers a public Reel thanking the referring agent and reiterating that 30 percent split. “I make the agent the hero,” she laughs, “because heroes get sequels.”

She posts with purpose: The ‘little help’ strategy

Scroll her feed and you’ll spot templated “buyer-need” graphics like:

- “VA buyer, $450K, needs 3/2 near Fort Jackson — know anyone?”

- “Investor hunting duplex under $300K in Cayce — DM me.”

Each ends with two clear calls to action: Share or direct message me. One spring listing that she was able to track came straight from an owner whose neighbor shared the post.

She also stated that sneak-peek posts of “coming soon” listings, which she shoots green-screen style in front of a map, spark the same fear of missing out and occasionally turn into double-ended deals.

She’s found that leverage beats burnout

When you’re barreling toward 200 sides, leverage isn’t optional. Once Hunt realized this, she hired showing assistants at $25 per hour to help out with buyers. She now leans on a transaction coordinator and automates everything she can. But she still answers her own Instagram DMs.

“That’s my trust channel,” she says. “People feel like they know me; I’m not handing that off.”

Her advice to rookies is equally direct: “Start documenting now — even if you’re juggling a stroller and a Supra key. Ask every client for the intro to the next one. Systematize your follow-up, and celebrate gratitude loudly.”

She tells new agents what she’d tell her year-one self: “The things you struggle with today will be what you help someone else through tomorrow. Keep going. Winners are the ones who don’t stop when everyone else would.”

Four years ago, her stretch goal was matching her husband’s Army salary. She surpassed it tenfold this spring. “I couldn’t have dreamed this big,” Hunt admits. “Authenticity did the heavy lifting. I just kept showing up.”

Taley Hunt can be found on Instagram and on Facebook.

Jimmy Burgess is the Chief Coaching Officer for HomeServices of America and President of Berkshire Hathaway HomeServices. Connect with him on Instagram and LinkedIn.

by Julie Brinkman | Jun 27, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Vacation rentals have a perception problem. Blamed for everything from driving up housing prices to changing the character of neighborhoods, homes that support local livelihoods often get a bad rap. And more often than not, those headlines are fueled by hotel lobbyists and government officials who are closely aligned with the hotel groups.

Putting politics aside, you need to read beyond the headlines and look at the facts; short-term rentals build and fuel local economies. Rooted deeply in the communities they serve, these hardworking homes are owned and managed by pillars of their communities, not by multinational hotel brands. These vacation rental hosts power small businesses, support working families and enable homeowners to stay in their homes. The impact is objectively measurable.

Vacation rentals make people, businesses and communities stronger

Unlike hotels, where profits are channeled to institutional investors, vacation rentals spread the wealth by opening up their community and neighborhood to travelers of all types. People who opt for these more personalized lodgings don’t just book a room; they shop at the local market, they meet the neighbors and they embed themselves in the communities they seek to explore.

Travelers who book these homes stay longer in communities and ultimately inject more economic benefit into those communities. In fact, these kinds of travelers spend 54 percent more per trip than hotel guests, according to a National Association of Realtors study. And the beneficiaries of these funds are not the multinational hotel chains; it’s the mom-and-pop stores, markets and experiences that these travelers access.

Another significant upside: Vacation rentals tend to be located in areas hotels have traditionally ignored; outside of massive tourist destinations, in small, quaint communities. This off-the-beaten-track approach affords the wandering traveler the ability to truly explore. And the economic upside is real. In fact, in Texas alone, vacation rental-related tourism has contributed over $6.1 billion.

Behind every vacation rental? Real jobs, real people

Income-generating domiciles don’t operate on autopilot; each home is unique. And behind every listing is a host of dynamic people, including cleaners, maintenance workers, property managers, gardeners and revenue planners.

These aren’t gig jobs. They’re micro-economies. We’ve seen entire small businesses grow from vacation rental demand. Property management alone has seen demand skyrocket, with thousands of small businesses springing up. Research confirms what anecdotal evidence has shown: Vacation rentals aren’t merely providing lodging; they’re infusing funds into areas where they’re needed most.

At the same time, vacation rentals are a financial lifeline for homeowners, who can use rental income to pay off mortgages, cover maintenance costs or build savings. This secondary source of income makes homeownership more affordable and sustainable, especially in high-cost housing markets.

Vacation rentals also create entrepreneurship opportunities — who doesn’t have a friend who bought a second home to rent out on a short-term basis? These stories abound across the globe.

In improving opportunities for local communities and residents, these accommodations have revolutionized how people travel and work. Digital nomads can log in remotely from anywhere, families can rent out whole houses rather than sharing hotel rooms, and solo travelers can live in local neighborhoods.

As people look for more authentic experiences that align with their values, rentals are also responding to the demand for unique, sustainable experiences. Hundreds of hosts now offer green options, improved accessibility for travelers with disabilities and stays that directly benefit local communities.

So why are cities cracking down?

Well-intentioned, poorly executed policy backed by well-funded hotel lobbyists.

New York City’s STR crackdown was championed to free up housing and lower rents. Instead, hotel prices soared, long-term rents stayed stubborn, locals lost income streams, and small businesses lost foot traffic.

This equation added up to economic hardships for the very locals that these laws were meant to protect.

NYC’s experience shows that simply banning the option does not stop housing crises; it just moves the problem elsewhere.

Excessive regulation threatens homeowners, reduces tax revenues, chases away tourists and stifles economic opportunities.

The Milken Institute illustrates that California presents a compelling case for how these kinds of rentals can add value to local economies. In Monterey County, they generate millions in lodging taxes, directly financing public services, infrastructure and development. This case study illustrates that a more targeted and data-driven policy is exponentially superior to blanket prohibition.

Cities should focus on regulation for the responsible management of STRs while ensuring housing stability. Smarter policy is the key to sustainable economic growth.

The path forward: A win-win for cities and communities

Vacation rentals are here to stay — travelers want them, homeowners need them, and local economies depend on them. The benefits are too significant to ignore, from job and entrepreneurship development to tax revenue and economic empowerment. With strategic policies, these homes can coexist alongside long-term housing and propel local economies forward. Instead of stifling them, cities should unlock their power for good.

Vacation rentals are already fueling the future of travel. Let’s see them as the economic drivers they are, enriching our communities as they generate income for homeowners.

Julie Brinkman, CEO of Beyond, proudly leads a global team dedicated to helping short-term rental hosts grow their revenue. Connect with her on LinkedIn.

by Matt Carter | Jun 26, 2025 | Industry, News Feed

Common Securitization Solutions (CSS) has rebranded as U.S. Fin Tech and will look to provide technology and business solutions to companies in addition to its owners.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A little-known joint venture of Fannie Mae and Freddie Mac that processes billions in mortgage-backed securities is getting a new name and an expanded mission — offering its services to other clients.

Common Securitization Solutions (CSS) is rebranding as U.S. Fin Tech, and will look to provide technology and business solutions to companies in addition to its owners.

TAKE THE INMAN INTEL SURVEY FOR JUNE

U.S. Financial Technology LLC, as CSS is now formally known, is a Delaware company co-owned by Fannie Mae and Freddie Mac and regulated by the U.S. Federal Housing Finance Agency (FHFA).

Tony Renzi

“We are excited to have a name that demonstrates that we are leading the United States and the world in financial services technology,” CEO Tony Renzi said in a statement Thursday. Renzi was appointed as CEO of CSS in 2019 and continues to lead the rebranded company.

Established as a joint venture of Fannie and Freddie in 2014, CSS operates the Common Securitization Platform (CSP), a conduit through which the mortgage giants issue and administer trillions of dollars in mortgage-backed securities (MBS) that launched in 2019.

CSS has been a fully virtual, geographically dispersed company since 2020, and boasts that its cloud-based platform provides “unrivaled layered security architecture and traceability capabilities” providing “business continuity with full disaster recovery and zero data loss within 4 hours.”

CSS “meets the challenges of the market, such as data management, processing, and speed of execution, to bridge the gap between the secondary mortgage market and investors,” the company says.

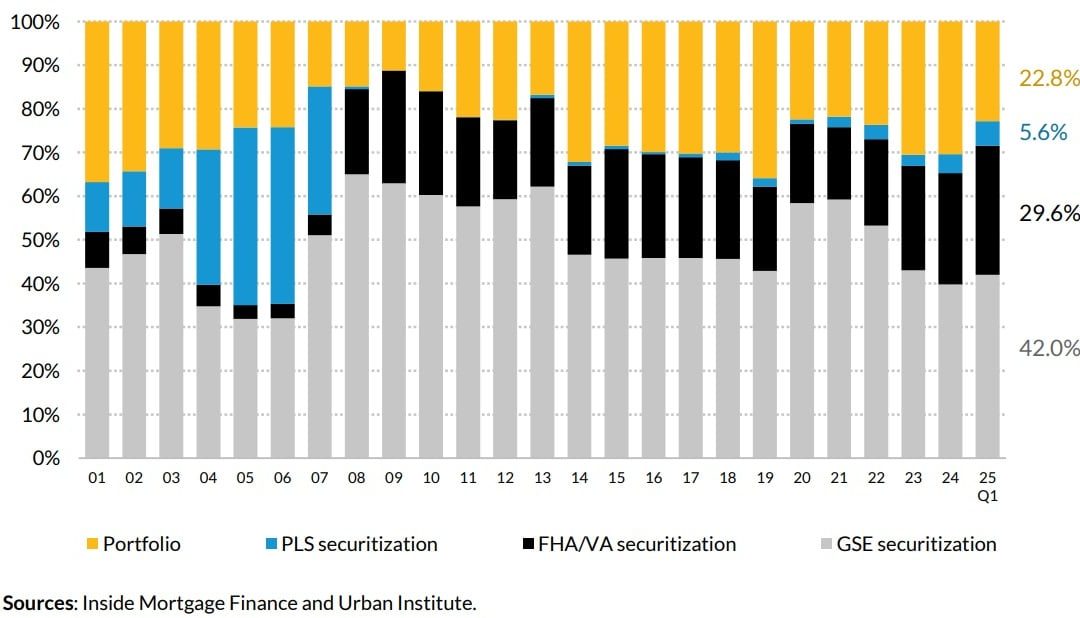

Mortgage funding sources, 2001-2025

Of the $355 billion in mortgages originated in the first quarter of 2025, Fannie and Freddie (the government-sponsored enterprises, or GSEs) packaged up 42 percent into MBS for sale to investors, according to data compiled by Inside Mortgage Finance and the Urban Institute.

Close to 30 percent of Q1 2025 originations were FHA and VA loan securitizations backed by Ginnie Mae, while 23 percent were made by lenders who kept them in their portfolios.

Securitizations of private-label securities (PLS) lacking the backing of Fannie Mae, Freddie Mac and Ginnie Mae were up 24 percent from a year ago, to $20 billion, but accounted for just under 6 percent of first-lien mortgage originations in Q1 2025.

PLS securitizations boomed at the turn of the century when lenders used them to finance subprime mortgages, but vanished for close to a decade after the 2007-2009 housing crash and Great Recession.

Fannie and Freddie were placed in government conservatorship in 2008 as their losses mounted, and the Trump administration is studying ways to restructure them.

Bill Pulte

Bill Pulte, Trump’s pick to run Fannie and Freddie’s regulator, has said the president is interested in taking the companies public, and might “sell a small piece” in the process.

“We created U.S. Fin Tech to demonstrate the incredible ingenuity of American technology under President Trump’s leadership,” Pulte said in a statement.

Pulte on Wednesday directed the mortgage giants to consider allowing borrowers to count cryptocurrency as an asset without having to convert their holdings into dollars.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Andrea V. Brambila | Jun 26, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Real estate trade groups, brokerages and landlords in New York City are taking their case against a broker fee law to a higher court and the city is fighting back.

On June 24, the City of New York responded to a lawsuit filed by the Real Estate Board of New York (REBNY), the New York State Association of Realtors, and seven real estate companies against the Fairness in Apartment Rental Expenses (FARE) Act, which requires rental property owners to cover broker fees when they enlist a broker to help them lease a unit.

TAKE THE INMAN INTEL SURVEY FOR JUNE

The trade groups and companies allege the legislation violates the First Amendment and the New York State Constitution, and was pre-empted by state law. The suit also claims the FARE Act violates the Contracts Clause of the U.S. Constitution since brokers and landlords can’t execute existing listing agreements that require brokers to negotiate and receive compensation from tenants.

In its answer to the suit, the city denies the allegations.

“Defendants City of New York and Commissioner [Vilda Vera] Mayuga have not violated any rights, privileges or immunities under the Constitution or laws of the United States or the State of New York or any political subdivision thereof, nor have defendants violated any act of Congress providing for the protection of civil rights,” attorneys for the city wrote.

They also pointed out that three of the four claims in the suit were dismissed by the court on June 10. Regarding the remaining claim, that the FARE Act violates the Constitution’s contracts clause, the city alleged that the plaintiffs lack standing to bring the claim.

“The only Plaintiff who has pled facts alleging that it has exclusive contracts impacted by the FARE Act is Bond New York,” the filing states, later adding that the court may lack the jurisdiction “over REBNY and Bond New York’s Contract Clause claim due to lack of standing and/or mootness.”

Meanwhile, the plaintiffs appealed the dismissal of the aforementioned claims on June 12 to the U.S. Court of Appeals for the Second Circuit. In a June 26 filing, they asked the higher court to decide “[w]hether the District Court erred in concluding that Plaintiffs failed to demonstrate a likelihood of success on the merits of their free speech claims,” among other questions.

Neither party has submitted appellate briefs yet. But in granting the city’s motion to dismiss in regards to most of the RENBY suit’s claims, District Court Judge Ronnie Abrams suggested that the plaintiffs were looking for a judicial solution to a political problem.

“In enacting the FARE Act, the City Council made clear that it sought to address a specific harm: the detrimental impact on housing mobility caused by the practice of imposing brokers’ fees on tenants,” Abrams wrote.

“Although the Act is not primarily intended to target speech and has only a relatively minimal impact on existing contracts, Plaintiffs have sought to enjoin its enforcement on the basis that it violates the First Amendment and the Contracts Clause.

“In their telling, the Act will wreak havoc on the City’s residential rental market, cause rents to rise, put brokers out of work, and make it exponentially more difficult for New Yorkers to rent apartments.”

Abrams stressed she did not believe it was the court’s job to decide which of these contrasting views was correct.

“Plaintiffs’ discontentment with the Act, however, stems not from its effects on their constitutional rights, but from a fundamental disagreement with its underlying policy,” she continued.

“The law is clear, though, that ‘[w]hether the legislation is wise or unwise as a matter of policy is a question with which [the Court cannot be] concerned.’ Thus, although some of Plaintiffs’ prophecies may prove true, Plaintiffs remedy is through the political process, not in court.”

Read NYC’s answer to REBNY’s suit (re-load page if document is not visible):

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter