by Julie Brinkman | Jun 27, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Vacation rentals have a perception problem. Blamed for everything from driving up housing prices to changing the character of neighborhoods, homes that support local livelihoods often get a bad rap. And more often than not, those headlines are fueled by hotel lobbyists and government officials who are closely aligned with the hotel groups.

Putting politics aside, you need to read beyond the headlines and look at the facts; short-term rentals build and fuel local economies. Rooted deeply in the communities they serve, these hardworking homes are owned and managed by pillars of their communities, not by multinational hotel brands. These vacation rental hosts power small businesses, support working families and enable homeowners to stay in their homes. The impact is objectively measurable.

Vacation rentals make people, businesses and communities stronger

Unlike hotels, where profits are channeled to institutional investors, vacation rentals spread the wealth by opening up their community and neighborhood to travelers of all types. People who opt for these more personalized lodgings don’t just book a room; they shop at the local market, they meet the neighbors and they embed themselves in the communities they seek to explore.

Travelers who book these homes stay longer in communities and ultimately inject more economic benefit into those communities. In fact, these kinds of travelers spend 54 percent more per trip than hotel guests, according to a National Association of Realtors study. And the beneficiaries of these funds are not the multinational hotel chains; it’s the mom-and-pop stores, markets and experiences that these travelers access.

Another significant upside: Vacation rentals tend to be located in areas hotels have traditionally ignored; outside of massive tourist destinations, in small, quaint communities. This off-the-beaten-track approach affords the wandering traveler the ability to truly explore. And the economic upside is real. In fact, in Texas alone, vacation rental-related tourism has contributed over $6.1 billion.

Behind every vacation rental? Real jobs, real people

Income-generating domiciles don’t operate on autopilot; each home is unique. And behind every listing is a host of dynamic people, including cleaners, maintenance workers, property managers, gardeners and revenue planners.

These aren’t gig jobs. They’re micro-economies. We’ve seen entire small businesses grow from vacation rental demand. Property management alone has seen demand skyrocket, with thousands of small businesses springing up. Research confirms what anecdotal evidence has shown: Vacation rentals aren’t merely providing lodging; they’re infusing funds into areas where they’re needed most.

At the same time, vacation rentals are a financial lifeline for homeowners, who can use rental income to pay off mortgages, cover maintenance costs or build savings. This secondary source of income makes homeownership more affordable and sustainable, especially in high-cost housing markets.

Vacation rentals also create entrepreneurship opportunities — who doesn’t have a friend who bought a second home to rent out on a short-term basis? These stories abound across the globe.

In improving opportunities for local communities and residents, these accommodations have revolutionized how people travel and work. Digital nomads can log in remotely from anywhere, families can rent out whole houses rather than sharing hotel rooms, and solo travelers can live in local neighborhoods.

As people look for more authentic experiences that align with their values, rentals are also responding to the demand for unique, sustainable experiences. Hundreds of hosts now offer green options, improved accessibility for travelers with disabilities and stays that directly benefit local communities.

So why are cities cracking down?

Well-intentioned, poorly executed policy backed by well-funded hotel lobbyists.

New York City’s STR crackdown was championed to free up housing and lower rents. Instead, hotel prices soared, long-term rents stayed stubborn, locals lost income streams, and small businesses lost foot traffic.

This equation added up to economic hardships for the very locals that these laws were meant to protect.

NYC’s experience shows that simply banning the option does not stop housing crises; it just moves the problem elsewhere.

Excessive regulation threatens homeowners, reduces tax revenues, chases away tourists and stifles economic opportunities.

The Milken Institute illustrates that California presents a compelling case for how these kinds of rentals can add value to local economies. In Monterey County, they generate millions in lodging taxes, directly financing public services, infrastructure and development. This case study illustrates that a more targeted and data-driven policy is exponentially superior to blanket prohibition.

Cities should focus on regulation for the responsible management of STRs while ensuring housing stability. Smarter policy is the key to sustainable economic growth.

The path forward: A win-win for cities and communities

Vacation rentals are here to stay — travelers want them, homeowners need them, and local economies depend on them. The benefits are too significant to ignore, from job and entrepreneurship development to tax revenue and economic empowerment. With strategic policies, these homes can coexist alongside long-term housing and propel local economies forward. Instead of stifling them, cities should unlock their power for good.

Vacation rentals are already fueling the future of travel. Let’s see them as the economic drivers they are, enriching our communities as they generate income for homeowners.

Julie Brinkman, CEO of Beyond, proudly leads a global team dedicated to helping short-term rental hosts grow their revenue. Connect with her on LinkedIn.

by Julie Brinkman | Aug 21, 2024 | Industry, News Feed

Whether it’s refining your business model, mastering new technologies, or discovering strategies to capitalize on the next market surge, Inman Connect New York will prepare you to take bold steps forward. The Next Chapter is about to begin. Be part of it. Join us and thousands of real estate leaders Jan. 22-24, 2025.

Mortgage rates are likely to keep coming down this year and next, but it will take time for lower rates to translate into more sales, Fannie Mae economists said Wednesday.

Even with the recent pullback in mortgage rates, Fannie Mae forecasters now expect 2024 and 2025 home sales will come in slightly lower than they had forecast in July, as affordability “is unlikely to return to pre-pandemic levels anytime soon.”

Sales of existing homes were down 5.4 percent in June, to a weaker-than-expected annualized pace of 3.89 million, and 82 percent of Americans surveyed by Fannie Mae in July said it was a bad time to buy, economists at the mortgage giant noted in commentary accompanying their latest forecast.

TAKE THE INMAN INTEL INDEX SURVEY FOR AUGUST

“Active inventories of homes for sale have been rising throughout this year, but this increase has not been because of a robust rise in listings of homes added to the market,” Fannie Mae forecasters said. While new listings have risen modestly, “the main driver is the fact that these listings have not been met with any increase in actual home sales, and therefore total inventories are rising and the average time on the market is increasing.”

The recent pullback in mortgage rates has renewed interest in refinancing among some homeowners with high rates, but rates need to come down even more to motivate many would-be homebuyers.

Mark Palim

“On its face, the lower rate environment should be good for home sales by helping loosen the grip of the so-called ‘lock-in effect,’ in addition to aiding affordability more generally,” Fannie Mae Deputy Chief Economist Mark Palim said, in a statement. “However, high-frequency data, such as mortgage applications, home showing requests, and listings views, suggest that many potential homebuyers remain reluctant to make the jump.”

Economists with Fannie Mae’s Economic and Strategic Research (ESR) Group don’t see homebuying picking up “meaningfully until income growth begins to outpace home price growth and mortgage rates move closer to 6.0 percent.”

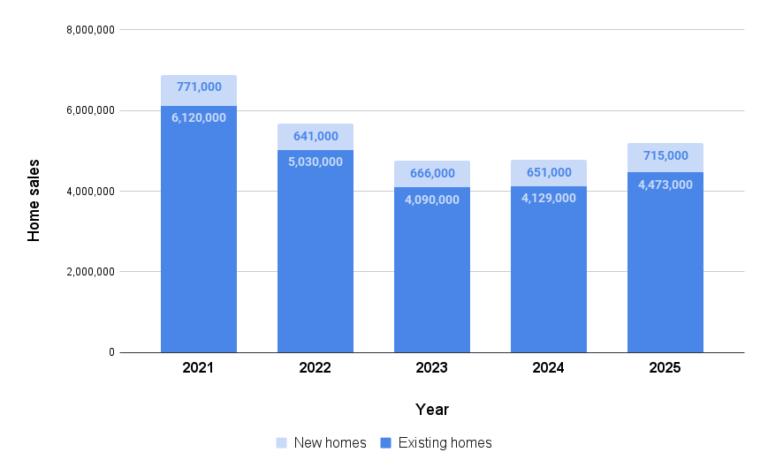

Home sales expected to grow by 8.5% in 2025

Source: Fannie Mae forecast, August 2024.

Fannie Mae economists now expect sales of new and existing homes will grow by just 0.5 percent this year, to 4.78 million, before surging by 8.5 percent in 2025 to 5.19 million.

That’s 27,000 fewer 2024 home sales than Fannie Mae had forecast in July, and 67,000 fewer 2025 home sales.

The pace of home sales — currently estimated at around 4.7 million a year, after adjusting for seasonal factors — is expected to rebound to 5.11 million next spring, and continue growing to 5.27 million in Q3 2025 and 5.43 million in Q4 2025.

Not only are mortgage rates expected to be lower by then, but national home price appreciation is slowing.

In July, Fannie Mae economists predicted national home price appreciation would cool to 6.1 percent by the end of this year and to 3 percent by Q4 2024. Prices could start to come down in Sunbelt markets where supply exceeds demand.

The Sunbelt had a “disproportionate in-migration wave following the pandemic” and saw a stronger construction boom in recent years, Fannie Mae economists noted in their latest forecast.

While the Sunbelt still has “comparatively less expensive homes than many Northeast and West Coast metros, the relative shift in affordability has been much more severe in recent years, so the normal pool of buyers are likely more stretched,” Fannie Mae economists said.

While inventories of for-sale listings are on the rise in Southern and Mountain West states, they’ve “hardly budged on average for the rest of the country,” Fannie Mae economists said.

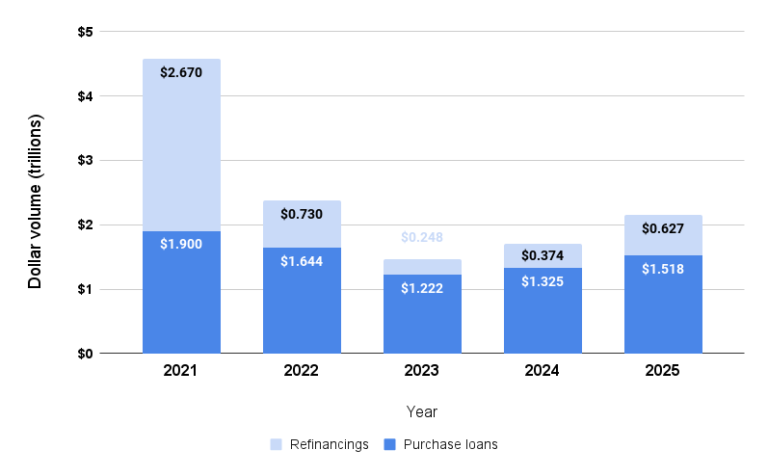

Purchase lending forecast to grow by 15% in 2025

Source: Fannie Mae forecast, August 2024.

Elevated home prices are one reason Fannie Mae economists expect purchase loan volume to grow by 8 percent this year, to $1.325 trillion. But that’s $31 billion less than July’s forecast, “given the somewhat weaker projected path for home sales.”

Purchase lending is expected to grow by another 15 percent next year, to $1.518 trillion, if the pace of sales ticks up in the second half of the year.

While mortgage lenders are expected to see even stronger growth in refinancing, it would be from a comparatively low baseline of $248 billion established in 2023.

Fannie Mae economists expect refinancing volume to grow by 51 percent this year, to $374 billion, and by another 68 percent in 2025, to $627 billion.

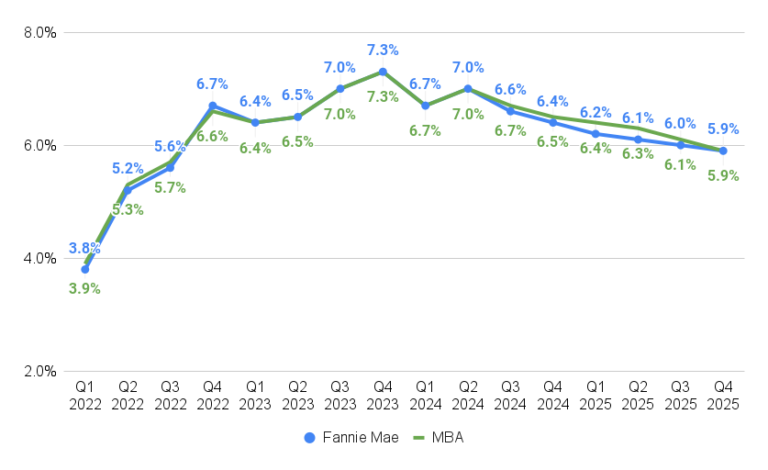

Mortgage rates expected to drop below 6%

Source: Fannie Mae and Mortgage Bankers Association forecasts, August 2024.

Economists at Fannie Mae and the Mortgage Bankers Association are aligned in their view that the Federal Reserve is on the verge of launching a rate-cutting campaign that will help bring rates on 30-year fixed-rate mortgages below 6 percent by Q4 2025.

With “inflation continuing to decelerate and labor markets softening to at least some extent, a period of rate cuts going forward is expected, but the magnitude and speed of such cuts is highly conditional on incoming data,” Fannie Mae economists said.

Last month, Fannie Mae predicted rates on 30-year fixed-rate mortgages would average 6.7 percent in Q4 2024 and 6.2 percent during Q4 2025. The latest forecast sees mortgage rates averaging 6.4 percent in Q4 2024 and 5.9 percent in Q4 2025.

Economists at the mortgage giant noted that while they continue to expect a soft landing as inflation cools, interest rates remain volatile. If bond market investors who fund most mortgages conclude that the Fed has waited too long to cut rates and the economy is headed for a recession, mortgage rates could come down further and faster.

“The recent jump in the unemployment rate to 4.3 percent helped drive a growth scare and related volatility in equity markets,” Fannie Mae economists said. “More recent data appear to have soothed many market fears of quickly deteriorating economic activity, though long-term interest rates remain significantly lower than a month ago as of this writing.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter