by Matt Carter | Jul 1, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

After staying stuck in the high sixes for two months, mortgage rates are coming back down as investors seeking certainty pull money out of the stock market and move it into bonds and mortgage-backed securities that fund most home loans.

But there’s no guarantee that the downward move in mortgage rates is sustainable, economists say, and hopes that home sales will pick up may hinge more on additional inventory coming onto the market, which is expected to cool or reverse home price gains.

After popping in April over concerns that the Trump administration’s tariff policies could reignite inflation, mortgage rates have been trending down since May 21.

At 6.67 percent Monday, lender data tracked by Optimal Blue shows rates on 30-year fixed-rate mortgages are down 25 basis points since May 21 and 38 basis points from the 2025 high of 7.05 percent registered on Jan. 14.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

A basis point is one hundredth of a percentage point. So rates have come down by 1/4 percentage point in the last five weeks — more than halfway to the 2025 low of 6.48 percent seen on April 4.

“The drop in rates is small but still helpful,” National Association of Realtors Chief Economist Lawrence Yun said in a statement to Inman.

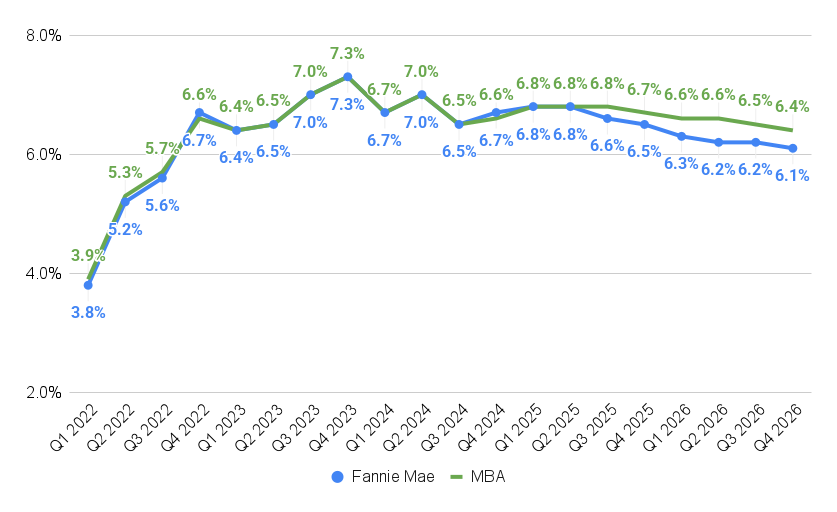

Mortgage rates trending down

Yun noted that 10-year Treasury yields — a barometer for mortgage rates — have made a similar downward move, and pointed out a few key reasons behind the trend.

Lawrence Yun

“First, there is an improved prospect of tariff negotiations,” Yun said. “Second, the likelihood of a Fed rate cut in September — or possibly even sooner — has increased, with two voting members publicly stating support for a July rate cut. Finally, actual inflation is calmer than forecasted in April and May, helped by decelerating shelter costs.”

Although the Trump administration has been putting the heat on Federal Reserve Chair Jerome Powell to lower short-term interest rates, mortgage rates are determined largely by investor demand for mortgage-backed securities (MBS).

When the prospects for economic growth look precarious, investors pile into MBS and government bonds seeking safe returns. More demand for bonds and MBS drives up their prices and brings down their yields.

But when inflation looks like a potential threat to their returns, investors will demand higher yields — driving up borrowing costs for homebuyers.

When the Fed cut short-term rates three times at the end of last year by a full percentage point, mortgage rates went up as investors weighed incoming data showing inflation moving away from the central bank’s 2 percent goal.

Where interest rates are headed next depends in large part on the outcome of ongoing tariff negotiations and Congress’ tax and spending policies, and forecasting mortgage rates can be a tricky business.

But in their latest forecast, economists at the Mortgage Bankers Association on June 20 predicted rates for 30-year fixed rate loans will end the year about where they are now — at 6.7 percent.

Mortgage rates forecast to stabilize

Source: Fannie Mae and Mortgage Bankers Association forecasts, June 2025.

The MBA sees mortgage rates coming down only gradually next year, to 6.4 percent by Q4.

Edward Seiler

A June 12 forecast by Fannie Mae economists was slightly more optimistic, predicting rates will drop to 6.5 percent by Q4 2025 and to 6.1 percent by the end of next year.

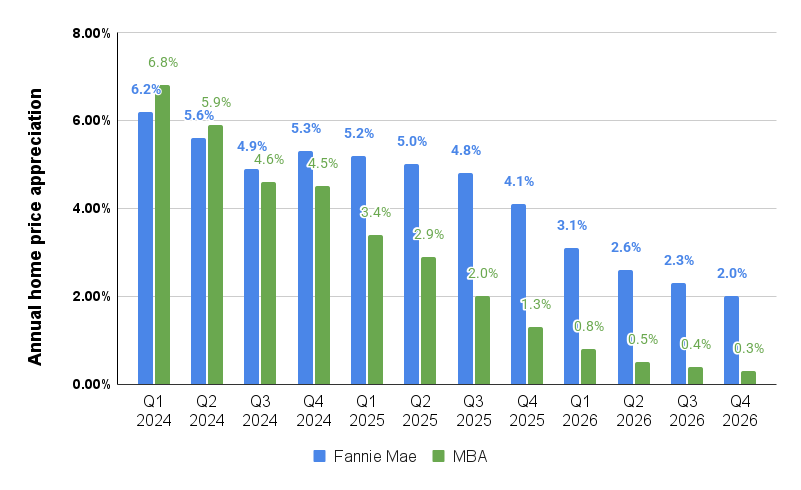

MBA economist Edward Seiler, the executive director of the Research Institute for Housing America (RIHA), told Inman that cooling home price appreciation is likely to have a bigger impact on affordability than mortgage rates.

Home price appreciation expected to cool

Source: Forecasts by Fannie Mae (April 2025) and Mortgage Bankers Association (June 2025).

Fannie Mae’s home price appreciation forecast is published quarterly, and hasn’t been updated since April.

MBA forecasters in June predicted that national home price appreciation will cool to 1.3 percent by the end of this year, and to 0.3 percent by Q4 2026.

Since the MBA’s forecast also predicts that inflation will swell to 3.2 percent by the end of next year, that implies national home price growth will be negative in real terms.

Price declines are expected in markets where inventory is coming online faster than houses are sold.

Among the 20 largest housing markets tracked by the S&P CoreLogic Case-Shiller Index, two saw year-over-year declines in April — Tampa (-2.2 percent) and Dallas (-0.2 percent).

Nicholas Godec

“The underlying market dynamics remain challenging but not dire,” S&P Down Jones Indices analyst Nicholas Godec said in a statement.

Elevated mortgage rates are keeping monthly payment burdens near generational highs, and the mortgage lock-in effect continues to constrain housing supply, he said.

The supply-demand imbalance “continues to provide a price floor, preventing the sharp [price] corrections that some had feared.”

It’s a market in transition, Godec said, where “local fundamentals matter more than national trends.”

Housing and mortgage experts polled by Fannie Mae in May saw Austin, Tampa, Dallas, Denver, Houston, Miami, Phoenix, Washington, D.C., and Atlanta as markets where home prices are most likely to underperform national home price appreciation over the next 12 months.

Among the 20 largest U.S. housing markets, Boston, New York, Philadelphia, Nashville and San Diego were viewed as places where prices are most likely to go up faster than the national average.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 30, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Mortgage giant Rocket Companies completed a reorganization of its capital structure Monday that will pave the way for the acquisition of tech-forward real estate brokerage Redfin — a deal it’s claimed could cut consumers’ transaction costs in half by compressing agent fees, mortgage gain-on-sale and title premiums.

The all-stock deal, valued at $1.75 billion when announced in March, went unchallenged by antitrust regulators and was approved by Redfin shareholders on June 4.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

In announcing the completion of its reorganization in a regulatory filing, Rocket said it reduced its classes of common stock from four to two in an “Up-C Collapse” that will improve its ability to use its common stock as acquisition currency for future deals.

That includes Rocket’s next big acquisition target, Mr. Cooper Group Inc., the nation’s biggest loan servicer, for stock valued at $9.4 billion.

Company executives have said acquiring Redfin will help subsidiary Rocket Mortgage capture 8 percent of the purchase loan market, and the Mr. Cooper deal will put Rocket in touch with more homeowners who might be ready to refinance.

Detroit-based Rocket wants to handle 20 percent of U.S. mortgage refinancings, and Rocket CEO Varun Krishna said last month that the company has invested about $500 million in AI and other technology that will help the company scale its business without a proportionate increase in expenses after the mergers.

In a March 10 investor presentation, Rocket executives said that by handling every aspect of homebuying and selling — from home search to mortgage financing and title and closing — they aim to cut transaction costs on the median priced home from $40,000 to $20,000.

“For far too long, the homeownership process has been outdated and disconnected,” Krishna told investment analysts in March. “Home search, brokerage, mortgage, title, closing, servicing, all exist in separate ecosystems, forcing consumers to piece together a complex and frustrating journey.”

Redfin shareholders will receive 0.7926 shares of Rocket common stock for each share of Redfin they own. Shares in Rocket closed at $14.18 Monday, up from $9.51 per share before the deal was announced.

Redfin will remain headquartered in Seattle, with CEO Glenn Kelman continuing to lead the business and reporting to Krishna.

“Rocket’s and Redfin’s approaches to lending and brokerage service have always just been two halves of one vision to make the whole home-buying process magical,” Kelman blogged in March.

In reporting first-quarter earnings in May, Rocket executives said the Mr. Cooper acquisition remains on track to close by the end of the year.

Rocket announced on June 3 that it would issue $4 billion in debt and use the proceeds to retire notes held by Mr. Cooper subsidiary Nationstar Mortgage Holdings Inc.

Editor’s note: This story has been updated to clarify that Rocket Companies announced an “Up-C Collapse” reorganization Monday to pave the way for its closing of deals to acquire Redfin and Mr. Cooper.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Taylor Anderson | Jun 30, 2025 | Industry, News Feed

Zillow attorneys pushed back at Compass’ request for a broad and expedited discovery, and on the brokerage’s private listing network. ‘Compass would erect new barriers for buyers by making listings exclusive to each broker.’

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Compass faces no real harm from Zillow’s updated policy banning publicly marketed private listings from its platform, the portal said in a new legal filing on Monday.

In response to filings in Compass’ antitrust lawsuit challenging Zillow’s private listings policy, the nation’s largest real estate portal said that Compass waited until near the deadline to go to court and was seeking to “turn back the industry-wide status quo of transparency and liquidity.”

TAKE THE INMAN INTEL SURVEY FOR JUNE

“Zillow provides maximum transparency and has become a trusted resource for millions of users, who are able to use Zillow to find buyer agents who represent their best interests rather than relying on listing agents whose duty is to the seller,” the company wrote in its filing.

It was Zillow’s first response in court to the lawsuit Compass filed a week ago. On Friday, Compass also asked the judge overseeing the case to file a preliminary injunction on Zillow’s updated listing access standards, which require listings to be filed on the MLS and therefore on Zillow within one business day of any public marketing.

The policy seemed to take aim at Compass’ 3-Phased Marketing Strategy, the first of which includes putting a listing on the brokerage’s private listing network without going onto the MLS. The first phase of a Compass listing under the strategy is known as a Private Exclusive.

“Put plainly,” Compass wrote in its complaint, “Zillow has granted itself the power to ban every Compass Private Exclusive listing from going to Zillow because of the way in which Compass markets and executes its Private Exclusive listing strategy internally and externally.”

In its lawsuit, Compass argued that its Private Exclusives were considered “office exclusives,” or exempt listings where the seller directs their agent not to widely disseminate a listing publicly.

According to NAR: “The office exclusive listing shall be filed with the MLS but not disseminated to other MLS Participants and Subscribers.”

A spokesperson for NAR declined to comment on whether Compass’ Private Exclusives were considered office exclusives under that definition.

“NAR is not a party to this lawsuit and has no comment,” the spokesperson said.

According to Zillow’s updated policy, a listing within a brokerage’s private listings network would violate the policy if that network is itself publicly marketed on the brokerage’s website.

“Compass would erect new barriers for buyers by making listings exclusive to each broker — resulting in reduced transparency, less market liquidity, and a more frustrating and less efficient experience for buyers and sellers,” Zillow wrote in its filing.

“Likewise, other entities that display for-sale listings to prospective buyers, including Compass, remain free to display such listings from any source, including the MLS, regardless of whether Zillow would display them,” it continued.

The legal filing was made in opposition to Compass’ request for expedited discovery.

Compass attorneys are hoping to receive from Zillow any communication between Zillow, Redfin, eXp and other brokerages, along with unspecified documents about what it calls the Zillow Ban, documents outlining Zillow’s interactions with certain MLSs, and more.

It also wants data about Zillow’s users and traffic, and documents related to competition in the real estate portal market.

In its filing, Zillow wrote that the request was unreasonable.

“Compass’s requests seek potentially hundreds of thousands of documents (if not more) and terabytes of highly confidential data,” the attorneys wrote. “Compass, without seeking leave, has also indicated that it will seek fact depositions and expert discovery.”

Email Taylor Anderson

by Matt Carter | Jun 30, 2025 | Industry, News Feed

Payment options, including Automated Clearing House (ACH), card payments, pinless debit and real-time disbursements, simplify loan servicing, improve cash flow management for lenders.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Cloud-based mortgage customer relationship management (CRM) tool Mortgage Automator now boasts a suite of payment processing options provided by Usio Inc., including Automated Clearing House (ACH), card payments, pinless debit and real-time disbursements.

San Antonio, Texas-based Usio — which provides payment solutions to merchants, billers, banks, service bureaus, integrated software vendors and card issuers — announced Monday that integration with Mortgage Automator went live in June.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

Launched in 2013 as a document-generating tool for a small private lender in Toronto, Canada, Mortgage Automator has evolved into a full-fledged originations, servicing and investor management tool with automation

Mortgage Automator became available in the U.S. in 2019 and continues to evolve, offering integrations with CoreLogic, DocuSign, Doss Docs, Hubspot, Lightning Docs, OSC Insurance Services, PrivateLenderLaw.com and Twilio, among others.

Pavel Tchourliaev

“Our mission has always been to provide private lenders with the most powerful and intuitive software solutions,” Mortgage Automator CEO Pavel Tchourliaev said in a statement. “Partnering with Usio allows us to further enhance our platform by offering integrated payment processing that simplifies loan servicing and improves cash flow management for our clients.”

Founded in 1998 as Billserv.com, Usio is a publicly traded fintech company with a $39 million market capitalization.

Usio entered the payment facilitation business with the 2017 acquisition of Singular Payments LLC, launching its “PayFac-in-a-Box” platform the following year to partner with app and software developers in the legal, healthcare, property management, utilities and insurance verticals.

Usio’s 202 acquisition of Information Management Solutions LLC (IMS) put it in the electronic and paper billing business in 2020, and it now serves hundreds of customers in industry verticals including financial institutions and utilities.

Competitors include Fiserv Inc., Elavon Inc., WorldPay, Stripe and Block Inc. (formerly known as Square).

Usio Chief Revenue Officer Greg Carter said the company is excited to partner with Mortgage Automator “and help modernize how private lenders manage payments.”

Greg Carter

“Embedding our payment technology into Mortgage Automator’s platform gives lenders the tools they need to operate more efficiently, reduce friction, and deliver a better experience for their borrowers,” Carter said in a statement. “This is another example of how software vendors in all industries can benefit from the implementation of our unique PayFac-in-a-box technology.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Taylor Anderson | Jun 30, 2025 | Industry, News Feed

The nation’s largest real estate portal began enforcing its ban on private listings on Monday, 10 weeks after announcing its new standards. Here’s what you need to know now.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Zillow’s ban on private listings took effect on Monday, the latest development in an ongoing battle that will determine the future landscape for marketing and home search in the U.S.

The ban set up a test for sellers: You can market your home off the multiple listing service as long as you’re comfortable with your listing also not showing up on the biggest real estate portal in the country.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Zillow Group, which, along with subsidiaries like Trulia, collectively attract 227 million users each month, took the latest step toward its stated goal of providing consumers with broad and transparent access to as many listings as possible.

The months leading up to the day of reckoning were filled with legal battles and questions about the definition of private listings themselves as agents, brokers and their clients continued to navigate a tumultuous time in the industry.

Here’s what you need to know about the new state of affairs on Zillow.

What listings are impacted?

The updated policy bans listings that aren’t added to the MLS within 24 hours of being publicly marketed.

“What’s not allowed under the listing access standards,” Zillow wrote, is “publicly marketing that off-MLS listings are available if a buyer is willing to work with an agent or brokerage.”

The portal also clarified that listings within a brokerage’s private listing network would be prohibited if the network itself is marketed to consumers on a public-facing website.

Zillow Group said the ban does not apply to Delayed Marketing Exempt Listings — a type of listing status created via recent changes to the National Association of Realtors’ Clear Cooperation Policy — as long as they’re submitted to an MLS within one day of public marketing.

“Coming soon” and office exclusives also comply with Zillow’s listing access standard as long as listing brokers are adhering to NAR’s guidance for each listing status. That guidance says that office exclusives are required to be submitted to the MLS, but aren’t widely distributed to other subscribers.

Zillow said that for sale by owner (FSBO) listings, rental listings and new construction listings sold by the builder are also permitted.

The ban arrives amid growing industry focus on private listings, with Compass leading the charge in creating a network of such properties.

Though different industry players have debated just exactly which listings might ultimately fall under the terms of the ban, Zillow has already begun warning agents that their listings are not in compliance.

Compass Private Exclusives

Zillow and Compass are also currently locked in a lawsuit over the nature of the ban. In its complaint that initiated the suit, Compass argues that Private Exclusives — or listings marketed exclusively via Compass’ platform — “that are referenced in advertisements on Compass.com mentioning the number of Private Exclusive listings available in a city or specific geography, or similarly returned in response to a search result on Compass.com, will trigger the Zillow Ban.”

“Put plainly,” the complaint adds, “Zillow has granted itself the power to ban every Compass Private Exclusive listing from going to Zillow because of the way in which Compass markets and executes its Private Exclusive listing strategy internally and externally.”

Zillow didn’t respond to a request for comment about whether Compass’ Private Exclusive network is specifically banned by its updated policy.

How many listings are impacted?

Compass notes on its website and seller disclosure form that Private Exclusives aren’t initially listed on the MLS, which it says could reduce the number of potential buyers who see the listing, reduce the number of showings, reduce the number of offers and reduce the final sale price for the property.

Still, the company says, nearly half of its clients in the first three months of this year chose to start with a private listing. Most of them, 94 percent, ultimately moved on to list the home on the MLS, the company says.

For Compass, the first three months of 2025 included 19,393 listings that started as Private Exclusives.

Compass’ Private Exclusives network was an expansion of existing options for more tailored private home sales for celebrities, judges or politicians, for example.

That was before Zillow announced the update to its listing access policy.

It’s difficult to say how many listings throughout the country would be in violation of Zillow’s updated policy, though the number would likely represent only a small percentage of all listings.

‘The life of the listing’

Zillow said that listings that violate its policy are banned for the “life of the listing.” That refers to the time a home is being sold by a broker who did not follow Zillow Group’s listing access standard, resulting in that listing being banned from Zillow and Trulia’s sites.

However, if the seller terminates the listing agreement with that broker and signs a new agreement with a broker who follows the listing access standard, Zillow and Trulia will lift the ban and display the listing.

What else?

Compass filed a federal antitrust lawsuit against Zillow last week and later asked the judge in the case to stop Zillow from enforcing its updated policy.

A ruling on that latter request isn’t expected until later this summer or in the fall, putting in place a question about how many sellers will ultimately decide to go with a private listing.

Meanwhile, Homes.com has said it would continue to show all listings despite the moves by Redfin and Zillow. Realtor.com hasn’t revealed any plans for a ban.

Email Taylor Anderson

by Darryl Davis | Jun 30, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Back in high school, all I wanted was to be on stage. Not the kind of stage where I’m training agents or speaking at events (although that is my life now). I mean acting and performing on the Great White Way of Broadway.

Acting was the dream. So, when I got into real estate at 19, it wasn’t out of a deep love for square footage. It was a strategy: Real estate would pay the bills while I auditioned in New York City.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Then something unexpected happened. I started doing really well. Like, really well. Real estate went from part-time hustle to full-time career, and eventually, I phased out of acting completely. I remember telling myself, “You know what? One day, I’ll make enough to produce my own show.”

Well … I didn’t quite become a Broadway producer. But I did get close. I’ve had the incredible opportunity to invest in Broadway through one of the best in the business — Ken Davenport, a two-time Tony Award-winning producer behind hits like Kinky Boots, Godspell, Oh Mary! and Othello. (By the way, he has an incredible new show called Joy – check it out!)

My first investment was in his revival of Gypsy (yep, that Gypsy, with Audra McDonald starring in the revival) — and even though I wasn’t the one calling the shots, being part of that world gave me a front-row seat to what it takes to put on a successful production.

Let me tell you something: It’s a lot like running a real estate business.

Here are five producer-style principles that every real estate agent can borrow from Broadway to put on a show-stopping business.

1. It’s not about being the star. It’s about assembling the right cast and crew

Sure, the lead gets the spotlight, but no Broadway show survives without a solid ensemble, a killer director and a behind-the-scenes crew that keeps the whole thing running. Same goes for real estate.

You might be the one with your face on the sign and your name on the business card, but you can’t do this alone — not if you want to scale up your business (and stay sane).

Your crew might include your mortgage broker, your home inspector, your stager, your transaction coordinator, your photographer and your go-to handyman. Every one of them plays a role in making you look good — and in making sure your clients have a smooth ride.

And when you surround yourself with people who are not only competent, but also care about your clients the way you do? That’s when the magic happens.

2. You’ve got to take risks, but smart ones

Nobody puts millions into a Broadway show unless they believe in the story. And yet, even with belief, talent and the best marketing, you still don’t know if it’s going to be a hit or a flop. That’s part of the thrill and part of the gamble.

Real estate is no different. Every listing is a bit of a risk. Every marketing campaign, every shift in your farming strategy, every door you knock or prospecting call you make — it’s a leap of faith. But the key is to take informed risks.

Track your numbers. Test new ideas in small batches. Know your audience. Invest in yourself and your business like a producer does: with heart and a spreadsheet.

3. You’re building an experience, not just a product

People don’t go to Broadway just to watch a show — they go to feel something. They want the emotion, the story, the energy, the escape. They want the full package: the lights, the music, the atmosphere, the wow moment when the curtain rises.

Real estate is no different.

You’re not just helping someone buy or sell a property. You’re guiding them through one of the biggest emotional and financial moments of their life. That means how you show up matters. How you communicate, how you listen, how you make them feel during the process — those things stick with people far longer than the final price on a contract.

Members of our coaching program have started to shift their mindset this way. One shared how they stopped focusing solely on the transaction itself and started focusing on the experience — surprising clients with handwritten notes, giving thoughtful closing gifts, even staging welcome-home photo shoots. The result? More referrals, more repeat business and more clients saying, “You were the best part of this whole process.”

It’s not about the paperwork. It’s about the performance. And when you treat each client like an audience member whose experience matters, you’ll always get a standing ovation.

4. You have to believe in the project because not everyone else will

On Broadway, there are times when it’s not the show that’s in question — it’s the people behind it. Actors get passed over, producers get told “It’ll never work,” and directors are second-guessed at every turn. But the ones who make it? They believe in their talent, their voice, their purpose, even when others don’t.

The same goes for real estate. You’re going to have moments when a listing doesn’t sell, a client ghosts you, or someone questions your worth as an agent.

You’ll face markets that feel impossible and buyers or sellers who think they know better than you do. But here’s the thing — you don’t need to believe in every property, but you do need to believe in yourself. You need to believe that your guidance makes a difference. That your knowledge helps buyers build wealth and helps sellers move on to their next level in life.

You’re not just opening doors to houses; you’re opening doors to new eras in people’s lives.

When you believe in the contribution you make to others, in the heart you bring to this business, that’s what will carry you through the tough days. Not the price tag on a listing. Not the outcome of a transaction. But the impact you have along the way.

5. Your reputation offstage matters just as much as your performance

In Broadway, a producer’s name carries weight. If they’re known for putting on quality shows and treating people right, investors line up, actors want to work with them, and audiences trust the brand. But the moment a producer gets a bad reputation behind the scenes — being difficult, shady or cutting corners — it catches up to them fast.

It’s the same exact thing in real estate. You can crush it on listing appointments, stage homes like a rockstar and negotiate like a boss. But if other agents dread working with you, or clients feel like you’re only in it for yourself, your long-term success takes a hit. Word travels. Fast.

One of our coaching members shared that a big chunk of their business started coming from other agents — agents they had worked with on deals in the past who remembered them as professional, respectful and fantastic to work with. Those agents chose to refer their friends and family to someone they technically competed with. When that starts happening, you know you’re doing it right.

Your reputation is your real brand. Make sure it shines, even when the spotlight’s not on you. Especially when the spotlight’s not on you! As Charles Marshall said in his book Shattering the Glass Slipper, “Integrity is doing the right thing, even when no one is watching.”

So yeah, I never did star in a Broadway show, but I still found my stage. I coach and train real estate professionals across the country, helping them become the “producers” of their own careers. I may not be listing and selling anymore, but I still invest in real estate — and I see the business from both sides of the curtain.

And, just like Broadway, success in real estate is about more than just knowing your lines. It’s about casting the right team, believing in your vision, taking smart risks, building unforgettable experiences and protecting your reputation like it is opening night.

Now, go out there and break a leg