by Lillian Dickerson | Jul 8, 2025 | Industry, News Feed

July is Luxury Month at Inman. We’ll take the temperature of the luxury market, talk to top producers in the ultra-luxury space and dive into the luxe trends of today — all culminating at Luxury Connect in San Diego, where we’ll announce this year’s Golden I Club honorees.

With almost exactly half of 2025 now in the books, its clear this is turning into a year of challenges. Global uncertainty spread, the economy rested on shaky ground, and political divisions have deepened — all of which are weighing on the minds of real estate professionals.

But amid all the challenges raining down on the housing market right now, one segment is still chugging along: luxury. In fact, in conversations with Inman, experts who specialize in the higher end of the market said that broader challenges notwithstanding, what they’re seeing right now looks more like resilience than collapse.

Mickey Alam Khan, CEO of full-service marketing agency Luxboro, was among those experts. He told Inman tariff policies have largely driven recent ups and downs in the economy, and will certainly impact the cost of construction materials and appliances, which will trickle down to the new development market. But otherwise, ultra-luxury buyers remain active.

Mickey Alam Khan

“So that impacts the future development of branded residences and new projects in that area,” Khan said. “That uncertainty is definitely hurting the overall market. When it comes to actual sales of luxury homes across the country, I feel that it’s the same situation as last year — the ultra-luxury market, or over $10 million, is always cash. So I think that market is as strong as ever, and ironically, it will grow stronger simply because of the swings and the volatility in the stock market.

“[Real estate] is becoming a more tangible asset of stored value,” he added.

Luxury real estate consistently outperformed the market at-large in 2024 and the first few months of 2025, adding to luxury agent optimism, Sotheby’s International Realty President and CEO Philip White told Inman, despite any other “noise” in the market right now.

“Luxury real estate agents must maintain unwavering focus on their business fundamentals rather than being swayed by daily market noise,” White said in an email to Inman. “Consistent client communication is paramount — ensuring buyers and sellers have current, accurate market intelligence positions agents as trusted advisors.”

Luxury trends

With interest rates still elevated, luxury buyers are heavily favoring cash transactions. There’s also little appetite for properties that require any kind of work, White said.

Philip White

“We’re observing a compelling dynamic where limited inventory of premier properties is driving competitive bidding for the most desirable locations,” White said in an email.

“Properties that have undergone strategic repricing to align with market comparables are moving successfully. There’s particularly strong demand for new construction and turnkey properties that require minimal renovation. Additionally, the vast majority of transactions are being completed as all-cash purchases. In fact, nearly 90 percent of our agents surveyed in the 2025 Mid-Year Luxury Outlook agent survey reported that the top transaction method for luxury property was cash.”

A wave of “smart luxury” buyers are also on the rise. According to Coldwell Banker Global Luxury’s 2025 Mid-Year Report, buyers who are seeking out perceived deals and investment opportunities want homes that have sat on the market.

With the value of the dollar weakened, more luxury buyers are being attracted to invest in U.S. real estate, Khan also pointed out, and even more are being compelled by President Trump’s “Gold Card” visa program, which creates a path to citizenship for individuals who invest $5 million in the U.S.

The program has received nearly 70,000 applicants, Commerce Secretary Howard Lutnick told the Financial Times, although it still faces legal challenges. Still, if those 70,000 applicants go through, it could mean a $350 billion investment in the country — much of which would likely be made in real estate.

“Where will that money go? It will go into buying either residential real estate or commercial real estate, investing in machinery, investing in talent,” Khan predicted. “But, I personally feel at least one-fifth of it will go into buying a home.”

Biggest deals of the year

There has been no shortage of big-ticket residential transactions so far this year, as investors have proven a continued penchant for luxury real estate.

The year’s priciest sales thus far have largely been concentrated in hot markets in South Florida and communities in and around Los Angeles. But other old-standbys like Manhattan, Honolulu and Aspen have seen their share of high-end deals too.

A three-home estate in Naples, Florida, marks the most expensive public sale of the first half of 2025 so far, with a jaw-dropping total sales price of $225 million. The property spans more than 15 acres and includes 800 feet of beach frontage. Michael McCumber of Gulf Coast International Properties represented the listing.

That sale was the only one thus far to surpass the $200 million mark — but there have also been several sales that have gone above and beyond $100 million, showing that ultra-high-net-worth individuals aren’t slowing down when it comes to buying the most elite luxury properties.

Stay tuned for a full list of the year’s top deals later in July.

Private listing networks

Few luxury brokerages have held back from weighing in on the private listings/office exclusives debate that has gripped the industry this year.

From staunch proponents of a client’s right to privately market their home (i.e. Compass, The Agency) to those who only support office exclusives in the rarest of circumstances (i.e. eXp Realty), brokerage opinions on the matter run the gamut.

It remains to be seen how and when the real estate industry may reach some sort of sustained status quo on this issue, and executives continue to weigh in — and call each other out. Compass, Corcoran Group and Douglas Elliman also all recently announced new platforms for their private listings.

And while any listing could theoretically be a private listing, the trend in practice is much more likely to concentrate at the higher end of the market. That’s because luxury homeowners are more likely to have wealth or notoriety that leads to privacy concerns, and thus an interest in selling without a traditional listing.

As a result, it’s already clear that the rise of private listings is poised to become one of the most consequential trends in the luxury space.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Darryl Davis | Jul 8, 2025 | Industry, News Feed

The real estate agents who rise to the top, coach Darryl Davis writes, are the ones who commit to daily growth, connection and service.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Here’s the truth most agents won’t say out loud: Feeling like an expert doesn’t come naturally. It’s built over time through small consistent actions that add up to big time confidence.

The good news? You don’t need 20 years of experience or a wall of awards to be seen as the go-to agent in your market. What you need is intention, plus the willingness to show up, stay curious, and yes, do the work.

Whether you’re brand new to the business or trying to get your groove back in a shifting market, here’s how to position yourself as a local expert even when you’re still finding your footing.

1. Know the numbers, know the neighborhoods

This is the foundation. Dive into your MLS. Study market reports. Tour listings — even the ones you’re not showing. Learn what’s moving, what’s sitting and what price points are turning heads. When someone asks, “How’s the market?” you’ll have real answers, not just vibes.

2. Become a student of the bigger picture

Understanding your local market is key. But pairing that with national trends, economic shifts and policy updates? That’s how you level up. Stay plugged into industry news. Follow experts you trust (like our friends here at Inman News). Learn the “why” behind the market movement; it gives your conversations more depth and authority.

3. Find (or create) your niche

You don’t have to serve everyone. In fact, focusing on a specific area — whether it’s first-time buyers, relocation clients or waterfront properties — can help you fast-track your credibility.

My mentor, Mac Levitt, knew everything there was to know about waterfront homes. He became the name agents and consumers alike would call with questions. You don’t need to know it all. Just aim to be the best in your lane.

4. Show up online (and offline)

Being an expert doesn’t mean hiding behind a feed full of just-sold graphics. It means showing up with useful, timely, human content on social, in person and in conversations. Think: quick market updates, helpful tips or one real estate convo a day. Visibility builds trust, and trust builds business.

5. Build your brain trust

Join local associations. Attend events. Connect with inspectors, lenders, attorneys, builders, appraisers and even journalists covering your beat. Learning from smart people sharpens your own expertise and puts you in the path of opportunity.

6. Teach what you know

This one’s a secret weapon. Write. Speak. Post. Host a first-time buyer webinar. Explain how appraisals work in a video. The act of teaching something forces you to understand it more deeply and positions you as the person others turn to for clarity.

7. Lead with curiosity, not ego

This one’s a classic: The best experts are also the best learners. If you don’t know something, ask. If you’re unsure, say so — but follow up with the answer. Clients don’t expect perfection. They expect honesty, confidence and someone who’s willing to go the extra mile to find the truth.

Bonus tip: Stop waiting to feel ‘ready’

Here’s the deal: Confidence isn’t a finish line. It’s a muscle. And you build it by doing the things that make you feel like a pro: studying, showing up, speaking out and staying connected. You don’t have to feel like the expert to act like one. The funny thing is that when you act like one long enough? You become one.

No matter where you are in your real estate journey — just starting out, starting over or leveling up — expert status isn’t something you wait for. It’s something you build. Start small. Stay curious. Keep showing up.

Because the agents who rise to the top of their markets aren’t always the loudest or the longest tenured: They’re the ones who commit to growth, connection and service. Every day.

by Josh Ries | Jul 8, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

When I started working online leads, I did what most agents were trained to do: Call fast, follow a script and jump straight into qualifying. I’d ask things like how soon they were looking to move, whether they were pre-approved or if they needed a lender. And depending on the script I was using that day, probably a few more questions I hadn’t earned the right to ask.

But it didn’t take long to realize something was off; it wasn’t working. Every call felt more like checking boxes than building real connection.

‘Did you earn it?’

After a while of not feeling right, I had lunch with two mentors (thanks, Jason Preuit and Donnie Owen). I complained about how no one would talk to me. Lead after lead, no one answered, and the ones who did barely stuck around.

One of them asked me a question I’ll never forget: “Did you earn it?”

I didn’t get it. I’d followed the training, used the scripts, called fast, asked the right questions. I’d never heard I needed to earn something first.

Then he explained that to get someone’s time, I had to give them a reason. Their time was just as valuable as mine, and I was treating the call like a transaction, not a relationship.

That hit hard!

Today’s consumers have been burned, hard-pitched, ghosted or pressured into bad decisions. You’re lucky if they gave you a real number.

Thanks to YouTube and social media, buyers and sellers recognize scripts instantly. What should be helpful sounds like an interrogation.

The real problem wasn’t speed. It was what we did with it

Speed wasn’t the problem; it was how we used it. We qualified too early and without value. We asked for commitment before earning trust.

I learned in a previous career that introducing anything adversarial too early kills momentum. And let’s be honest: The qualification process often feels adversarial, especially when it’s your opening move.

When I stopped trying to qualify fast and focused on earning attention, everything shifted. Conversations got easier. I started enjoying the work again.

Why qualifying too early kills trust

Agents are told to “strike while the iron is hot,” but no one explains what that actually means.

With online leads, qualifying too soon puts people on defense and creates friction before a relationship can form. This is especially true with top-of-funnel internet leads; most are months away from being ready.

While NAR offers conflicting data, we’ve found these leads typically convert 12 to 16 months after entering our system, and that window is growing. Buyers start earlier and move slower than they used to.

We found early qualification rarely led to real conversations or long-term engagement. So we flipped the script: Delay qualification and lead with value. That one change made all the difference. Now, we don’t qualify until the third call, often later.

Here’s the framework we use

Call 1: Initial contact (10 to 15 seconds)

Offer something useful, a market report or neighborhood update, or something already posted on social or our site. Confirm their contact info, and offer to text the link.

We end the call with:

“Thanks. Unless you need anything else from me?”

Then pause.

That line is the safety net. If the lead is lower in the funnel, like someone who signed up after seeing a property they want to see in person, they’ll tell you. That’s how we uncover urgency without forcing it.

Short. Helpful. No pressure.

Call 2: Follow-up (10 to 15 seconds, 5 to 7 days later)

Confirm they got the resource we sent after the first call. Ask if they have questions about it. End the call the same way.

Again: “Thanks. Unless you need anything else from me?”

Pause.

Same safety net.

This builds familiarity, shows we’re consistent, and proves we follow through.

Call 3: Qualify the lead (longer, if appropriate)

About a week before the third call, send something new to offer value, and create a reason to follow up.

If the rapport is there, begin qualifying. If not, hold back. You earn the right to ask deeper questions by showing up consistently and providing value first.

If you still haven’t earned the right after the third call, just repeat it. Send another resource, then check in.

No pressure, just keep building trust.

What earning it really means

What I’ve learned is that speed-to-lead isn’t about how fast you can qualify. It’s about how quickly you earn the right to keep the conversation going.

If your first touchpoint is focused on your needs, not theirs, don’t be surprised when they stop answering. People don’t want to be sold. They want help, and that starts with relevance, not pressure.

When we stopped trying to sort people and started serving them, everything changed: better conversations, more trust, more deals.

So yes, call fast. Follow up fast. Be present.

Speed gets you noticed, but trust gets you hired. And trust? You have to earn it.

Josh Ries is a real estate broker and a lead generation consultant. You can connect with him on TikTok and Instagram.

by Matt Carter | Jul 7, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Home prices have come down by at least a full percentage point in nearly one-third of the 100 largest U.S. housing markets even as many homebuyers stretch their finances to the limits to take out a mortgage.

Several markets have seen double-digit price declines from recent peaks, as price softening continues to spread from the Sunbelt into the Western U.S., ICE Mortgage Technology reported Monday.

While the inventory of homes for sale continues to grow at an accelerating pace, it remains to be seen whether softening home prices will keep some would-be sellers on the sidelines — as happened in late 2022 and early 2023, ICE reported.

ICE’s latest Mortgage Monitor Report suggested the market is on track to return to pre-pandemic inventory levels this fall, with listings already normalized in 39 of the 100 largest markets and 11 more on pace to get there by the end of the year.

Denver, where listings are up 100 percent from 2017-2019, has posted the biggest inventory gains, followed by Lakeland, Florida and Colorado Springs, Colorado (up 87 percent), Austin (up 69 percent) and Seattle (up 61 percent).

“California continues to be an area to watch closely, with the 10 largest markets seeing 42-75 percent inventory growth over the past 12 months,” ICE analysts noted. “While only three of its 10 largest markets (San Francisco, San Jose, and Stockton) have normalized, the remaining seven are on pace to do so by the end of this year, which could lead to softening price dynamics across the state.”

Swelling inventory and mortgage rates in the high sixes continues to cool home price growth, with early June data showing national home prices appreciated by just 0.3 percent on a seasonally adjusted annualized rate, ICE reported.

While home prices continue to climb in many Midwest and Northeast markets, 41 Sunbelt and Western markets saw prices drop on a seasonally adjusted basis in June.

Markets in Texas and Florida have seen double-digit price declines from peak levels, and parts of California, Arizona, Colorado, and Idaho have also seen prices come down more than 3 percent from recent highs.

“Thirty-one of the 100 largest markets in the U.S. have now seen prices dip by at least a full percentage point from their recent highs, suggesting the number of markets experiencing annual price declines may be poised to trend higher in coming months,” ICE analysts said.

Markets with biggest price declines from peak

- Austin, Texas (-19.7 percent)

- Cape Coral, Florida (-13.3 percent)

- North Port, Florida (-11.2 percent)

- San Francisco, California (-8.9 percent)

- Phoenix Arizona (-5.7 percent)

- San Antonio, Texas (-5.2 percent)

- Boise City, Idaho (-5.2 percent)

- Deltona, Florida (-4.0 percent)

- Stockton, California (-3.7 percent)

- Denver, Colorado (-3.6 percent)

- Tampa, Florida (-3.5 percent)

- Dallas, Texas (-3.2 percent)

- Palm Bay, Florida (-3.1 percent)

- Lakeland, Florida (-3.1 percent)

- Sacramento, California (-3.0 percent)

- San Jose, California (-2.9 percent)

- Provo, Utah (-2.8 percent)

- Miami, Florida (-2.3 percent)

- Colorado Springs, Colorado (-2.3 percent)

- Jacksonville, Florida (-2.2 percent)

- Oxnard, California (-1.9 percent)

- Orlando, Florida (-1.9 percent)

- Seattle, Washington (-1.9 percent)

- Portland, Oregon (-1.8 percent)

- Ogden, Utah (-1.6 percent)

- Los Angeles, California (-1.4 percent)

- Salt Lake City, Utah (-1.3 percent)

- San Diego, California (-1.3 percent)

- Bakersfield, California (-1.2 percent)

- Memphis, Tennessee (-1.2 percent)

- Riverside, California (-1.1 percent)

Seasonally adjusted price changes from local market post-pandemic peaks. Source: ICE Mortgage Monitor, July 2025.

While mortgage lenders are seeing an uptick in applications, underwriting standards remain tight and buyers face “significant affordability challenges,” ICE noted.

With average back-end debt-to-income ratios hitting 40 percent in May, borrowers needed an average credit score of 738, close to last year’s high.

“Loan amounts for purchase loans topped an average of more than $375,000 in May, and the average loan-to-value ratio topped 85 percent, so affordability is very stretched,” ICE reported.

To get their foot in the door, just over 5 percent of homebuyers are relying on adjustable-rate mortgages, and another 3 percent are opting for temporary interest rate buydowns.

More homeowners are underwater

While falling home prices could provide relief for homebuyers, they could also leave more homeowners underwater on their loan — owing more than their house is worth.

For now, ICE estimates that only about 538,000 homeowners are underwater, up from 339,000 a year ago.

But another 2.5 million homeowners have less than 10 percent equity in their home, up from 2 million a year ago.

If home prices fall by 10 percent, they’ll be underwater too — making it harder to avoid foreclosure if they have trouble making their mortgage payments.

“While the number of homeowners underwater on their mortgage is still relatively low, it’s beginning to grow in some markets, especially among mortgage holders who purchased more recently,” ICE noted.

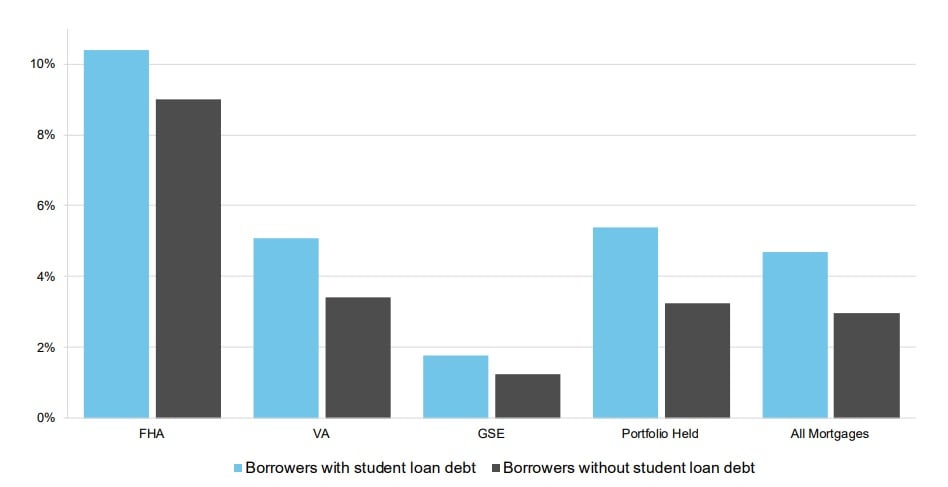

Buyers who made small down payments are most likely to have no equity, with close to 5 percent of VA mortgages and 2.6 percent of FHA loans underwater.

Only 3.2 percent of homeowners were delinquent on their mortgage payments in May, close to the all-time low.

Mortgage delinquencies by loan type

Source: ICE McDash and Tradelines powered by TransUnion.

While delinquency rates are low on portfolio loans made by private lenders and “GSE” loans backed by Fannie Mae and Freddie Mac, late payments on FHA and VA loans have been on the rise.

One issue among those borrowers is student loan debt. After pausing collections on defaulted student loans during the pandemic, the Department of Education resumed those efforts in May.

Nearly 30 percent of FHA borrowers and 20 percent of VA borrowers also have student loan debt.

Tim Bowler

“We’re seeing early signs of risk building within specific markets and within specific borrower populations, like borrowers with limited equity or who are behind on student loans,” ICE Mortgage Technology President Tim Bowler said, in a statement. “This is when proactive monitoring and data-driven risk management become essential. Identifying and engaging these borrowers early may prevent hardship later.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jul 7, 2025 | Industry, News Feed

Fannie Mae survey echoes polls by the University of Michigan and the Conference Board that found uncertainty over tariffs is weighing on consumer confidence.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

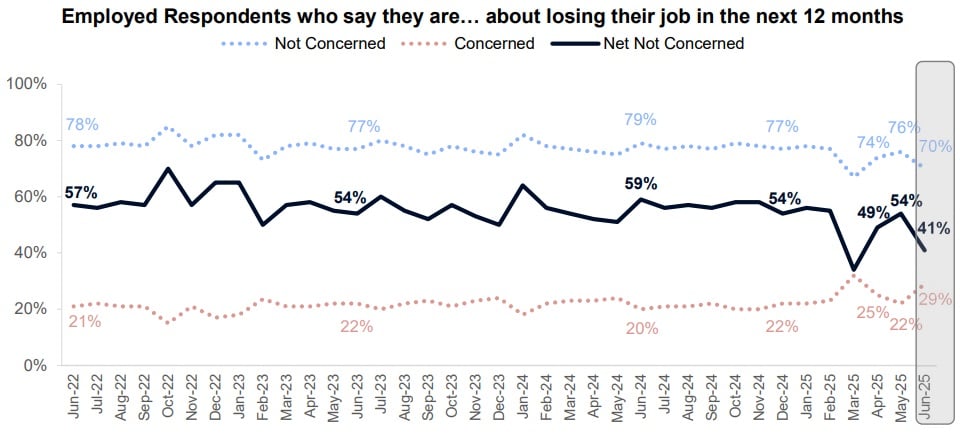

After hitting its highest level of the year in May, consumer sentiment toward housing deteriorated in June as Americans became more concerned about losing their jobs and less certain that mortgage rates will come down in the next year.

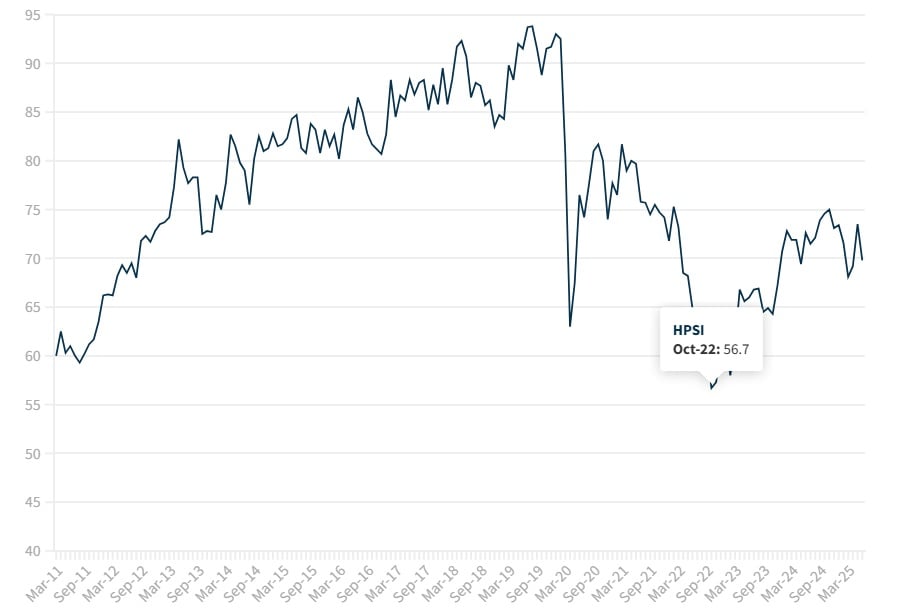

At 69.8, Fannie Mae’s Home Purchase Sentiment Index (HPSI) was down 3.7 points from May to June and 2.8 points from a year ago, the mortgage giant announced Monday.

The decline in Fannie Mae’s HPSI echoes consumer sentiment surveys conducted in June by the University of Michigan and the Conference Board, which showed uncertainty over tariffs weighing on consumer confidence. Consumers are currently paying an average effective tariff rate on imports of 15.8 percent — the highest since 1936, according to a June 17 analysis by The Budget Lab at Yale.

The Trump administration has delayed until Aug. 1 additional country-specific “reciprocal tariffs” that had already been postponed once to July 9. The White House said Monday that 14 countries were notified that they’ll face reciprocal tariffs next month, with additional notifications to go out in the days ahead, CNBC reported.

Goods from Japan and South Korea will be hit with a 25 percent import tax on Aug. 1, for instance, Trump informed the countries in letters shared on Truth Social.

“Tariffs remained on top of consumers’ minds and were frequently associated with concerns about their negative impacts on the economy and prices,” Conference Board Senior Economist Stephanie Guichard said in a statement. “Inflation and high prices were another important concern cited by consumers in June.”

Fannie Mae HPSI tracks consumer housing sentiment

Launched in 2011, Fannie Mae’s HPSI distills six questions from the mortgage giant’s monthly National Housing Survey into a single number.

The index plummeted in the spring of 2020 at the outset of the COVID-19 pandemic and hit an all-time low of 56.7 in October 2022, when home prices and mortgage rates were climbing.

At its current level, the HPSI is about where it was in the summer of 2012, when home purchase sentiment was rebounding from the 2007-2009 housing crash and Great Recession.

While “similar in spirit” to the University of Michigan and Conference Board surveys, the HPSI “is specifically devoted to the housing market,” and increases in the index “have been quite reliably followed by stronger housing markets,” Fannie Mae researchers said in an overview.

Five out of six HPSI components decreased in June. In addition to being more worried about losing their jobs and less convinced mortgage rates will fall, Americans were less certain that home prices will keep rising in the year ahead and that conditions are good for sellers.

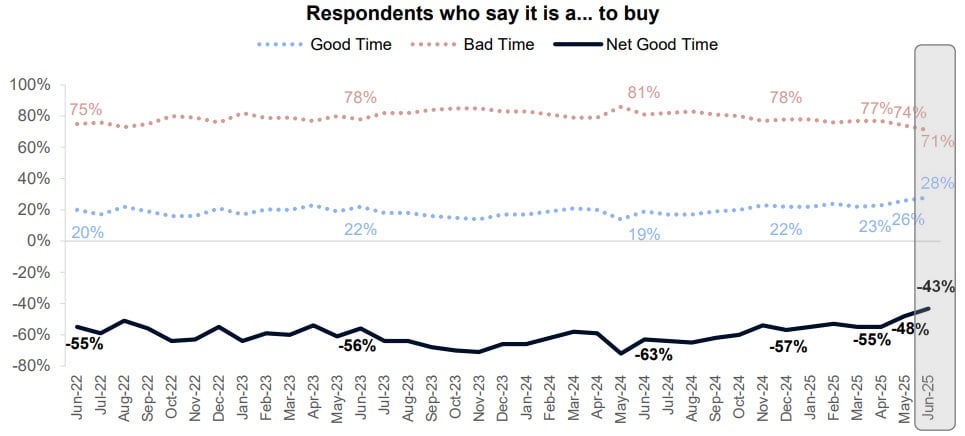

While just 28 percent of the 1,313 household financial decision makers surveyed by Fannie Mae between June 1 and June 17 said it was a good time to buy, that’s up two percentage points from May and nine percentage points from a year ago.

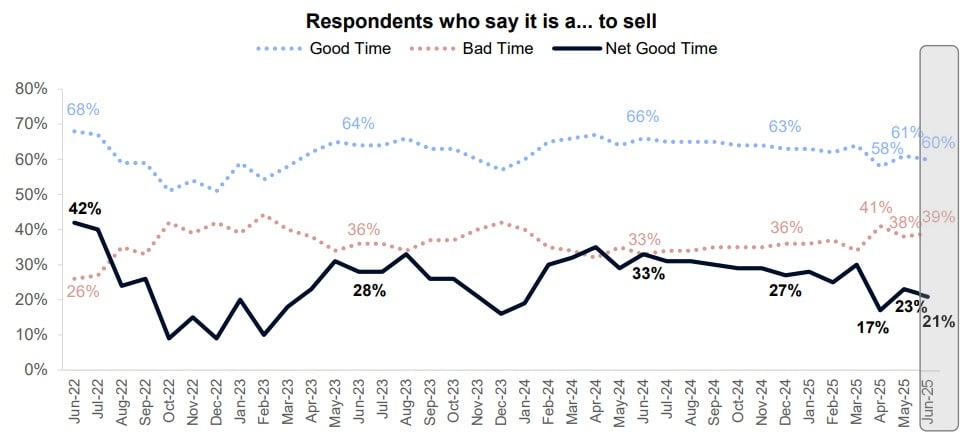

Although six in 10 Americans surveyed in June (60 percent) said it was a good time to sell, that’s down from 61 percent in May and 66 percent a year ago.

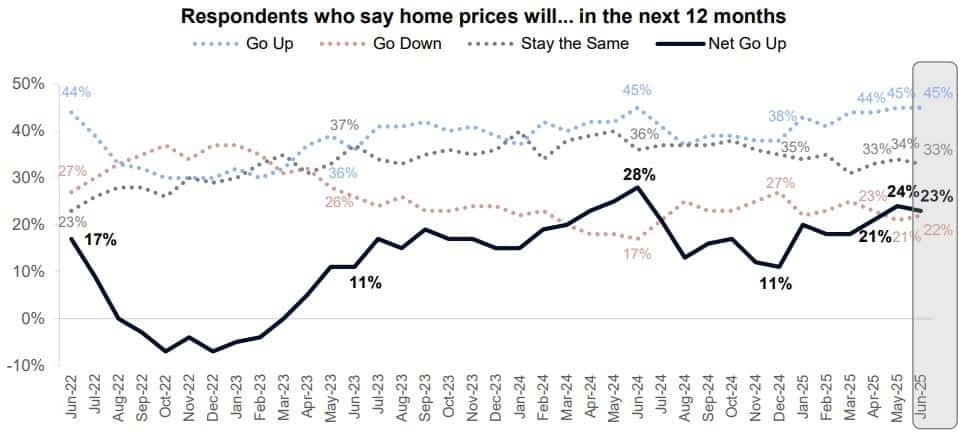

The share of survey respondents who expect home prices will go up in the next 12 months was unchanged in June at 45 percent.

But the share who said they expect home prices to go down — 22 percent — was up one percentage point from May and five percentage points from a year ago.

Although falling home prices might help boost sales, Fannie Mae’s HPSI treats a decline in home price expectations as a negative for consumer housing sentiment.

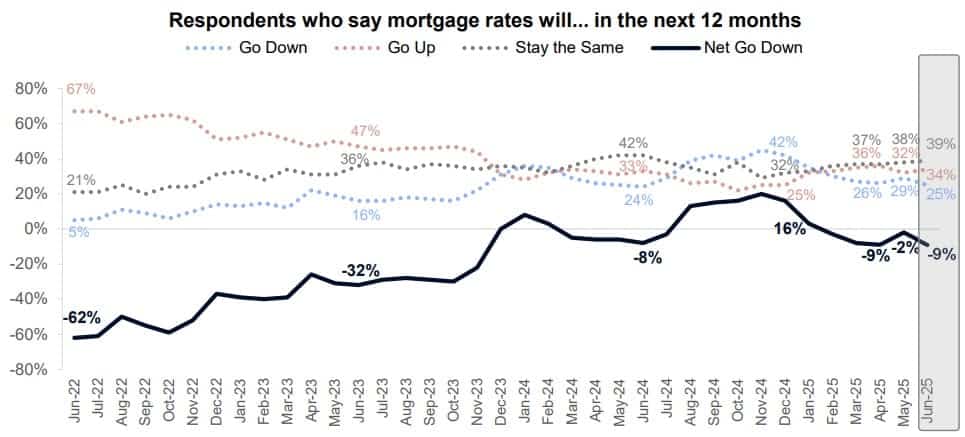

While close to one in three Americans (29 percent) surveyed in May said they expected mortgage rates to come down in the year ahead, that share dropped to 25 percent in June.

The Federal Reserve is expected to hold short-term interest rates steady until September, as policymakers assess the impact of the Trump administration’s tariffs, tax cuts, deregulation and deportations.

Fannie Mae economists last month predicted mortgage rates will drop to 6.5 percent by Q4 2025 and to 6.1 percent by the end of next year. Forecasters at the Mortgage Bankers Association have a more cautious outlook, predicting rates for 30-year fixed rate loans will end the year at 6.7 percent and drop to 6.4 percent by the end of next year.

Although only 29 percent of Americans polled in June said they were concerned about losing their jobs, that’s up from 22 percent in May and 20 percent a year ago.

At 4.1 percent, the unemployment rate in June was down slightly from 4.2 percent in May. But 7 million Americans were out of work, an increase of 1 million from June 2023.

Although not factored into the HPSI, 67 percent of household decision makers surveyed in June said they thought the economy was on the wrong track, up from 64 percent in May.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Leo Pareja | Jul 7, 2025 | Industry, News Feed

In an Inman Exclusive, Leo Pareja, CEO of eXp Realty, writes that exposure sells homes, while shielding listings hurts sellers, limits buyers and undermines trust.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Leadership isn’t about saying what’s easy. It’s about doing what’s right, especially when the stakes are high. Throughout my journey from selling nearly 4,000 homes to leading the No. 1 brokerage in the country by transaction count, one truth has always guided me: Silence in moments of chaos is complicity.

That often means speaking up when staying quiet would be easier. But the cost of silence is always greater than the criticism that comes with courage.

Since the NAR settlement first hit our radar in March of last year, I’ve led eXp through one guiding principle: Do what’s best for the consumer. It’s why we decided not to participate in broker-to-broker compensation moving forward.

It’s how we developed a straightforward, consumer-centric buyer agency, listing agency and most recently, seller disclosure documents. All open-sourced and shared freely with the entire industry. At a time when real estate is under a microscope, we’ve chosen to double down on putting the consumer first.

Recently, Compass filed a lawsuit against Zillow. While eXp is not named as a defendant, Compass accused us of being a “co-conspirator.” That’s a serious claim. One we categorically reject.

EXp charts its own course. We collaborate where it benefits consumers. We do not conspire. We do believe that the decision by Compass to forego sharing its listings with local MLSs is bad for consumers, and we will continue to stand against anything that hides listings, limits access or restricts opportunity.

Let’s talk about what this is really about: Compass wants to control inventory. They’re not hiding that motivation.

Take their “Three Phase Marketing” model. On paper, it’s positioned as “consumer choice.” In reality? It’s about controlling listing exposure. In Q1 of 2025, Compass reported that 48.2 percent of its listings entered this funnel. Nearly half of their homes were shielded from the broader market at the outset. No matter what language you wrap it in, that’s steering.

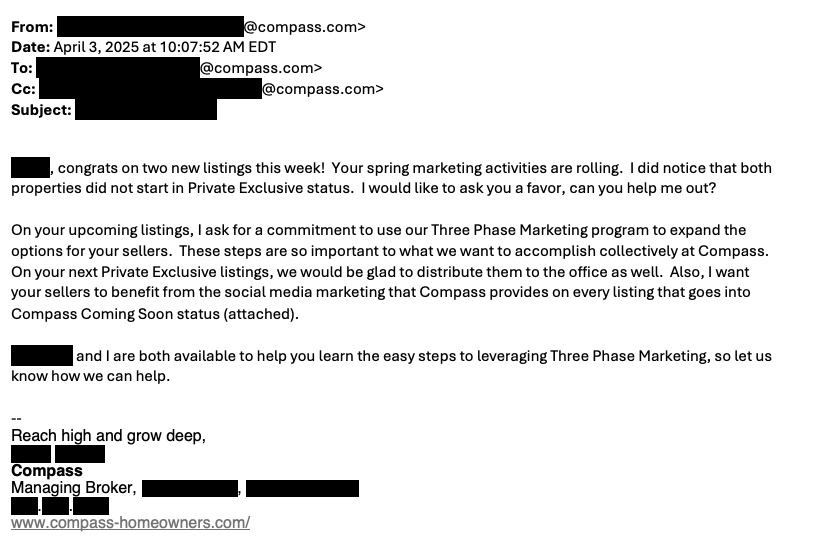

Below is a direct excerpt from an internal Compass email, sent by a managing broker to a former Compass agent (identifying info withheld, originals retained):

Let’s be clear: This isn’t about helping sellers or offering consumers more options. It’s about rigging the game, keeping inventory out of sight to create artificial scarcity, confusing the public and boosting agent commissions. That email doesn’t talk about the seller’s goals. It doesn’t mention fair housing or inclusive access. It’s about funneling deals inside a closed loop.

That’s not a marketing strategy. It’s market manipulation, plain and simple. And the consumer is the one being played.

Last week, Compass went a step further and declared it won’t comply with participation rules. Compass wants full access to display local MLS listings through IDX while keeping their own listings gated behind Compass.com. That’s not consumer advocacy. That’s bait-and-switch.

On a recent podcast with Ricky Carruth, Compass’s President of Growth, Rory Golod, confirmed this entire strategy is designed to win more listings and close more deals. Not once did he mention consumer value. Not once did he talk about transparency. He said the quiet part out loud, on repeat.

And Compass CEO Robert Reffkin? He already spoiled the plot of Compass’s end game when he said in a Q2 2024 earnings call:

“The foundation of every entity’s success in real estate is access to inventory. The source of success for all players in the industry whether MLSs, aggregators, buyer agents or listing agents is access to inventory.”

Access is power. And Compass wants to be the only one holding the keys.

But here’s the twist. They admit that 94 percent of their “exclusive” listings end up on the MLS anyway. If “exclusivity” was really serving the seller, why does nearly every listing eventually go public?

Because the data tells the truth: Exposure sells homes. Shielding listings hurts sellers, limits buyers and undermines trust. Period.

Let’s call this what it is: “Seller choice” is being weaponized, used as a Trojan horse by Compass to fragment the market, reduce transparency and create artificial scarcity that prioritizes agent interests over consumer needs. That’s not leadership; it’s exploitation.

We’re not here to play that game. At eXp, we believe in an open, transparent marketplace. We’ll keep building tools that serve the public, sharing resources that elevate everyone, and calling out the noise when it distracts from what really matters.

Because the future of real estate deserves truth, not spin.