by Julie Brinkman | Jun 27, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Vacation rentals have a perception problem. Blamed for everything from driving up housing prices to changing the character of neighborhoods, homes that support local livelihoods often get a bad rap. And more often than not, those headlines are fueled by hotel lobbyists and government officials who are closely aligned with the hotel groups.

Putting politics aside, you need to read beyond the headlines and look at the facts; short-term rentals build and fuel local economies. Rooted deeply in the communities they serve, these hardworking homes are owned and managed by pillars of their communities, not by multinational hotel brands. These vacation rental hosts power small businesses, support working families and enable homeowners to stay in their homes. The impact is objectively measurable.

Vacation rentals make people, businesses and communities stronger

Unlike hotels, where profits are channeled to institutional investors, vacation rentals spread the wealth by opening up their community and neighborhood to travelers of all types. People who opt for these more personalized lodgings don’t just book a room; they shop at the local market, they meet the neighbors and they embed themselves in the communities they seek to explore.

Travelers who book these homes stay longer in communities and ultimately inject more economic benefit into those communities. In fact, these kinds of travelers spend 54 percent more per trip than hotel guests, according to a National Association of Realtors study. And the beneficiaries of these funds are not the multinational hotel chains; it’s the mom-and-pop stores, markets and experiences that these travelers access.

Another significant upside: Vacation rentals tend to be located in areas hotels have traditionally ignored; outside of massive tourist destinations, in small, quaint communities. This off-the-beaten-track approach affords the wandering traveler the ability to truly explore. And the economic upside is real. In fact, in Texas alone, vacation rental-related tourism has contributed over $6.1 billion.

Behind every vacation rental? Real jobs, real people

Income-generating domiciles don’t operate on autopilot; each home is unique. And behind every listing is a host of dynamic people, including cleaners, maintenance workers, property managers, gardeners and revenue planners.

These aren’t gig jobs. They’re micro-economies. We’ve seen entire small businesses grow from vacation rental demand. Property management alone has seen demand skyrocket, with thousands of small businesses springing up. Research confirms what anecdotal evidence has shown: Vacation rentals aren’t merely providing lodging; they’re infusing funds into areas where they’re needed most.

At the same time, vacation rentals are a financial lifeline for homeowners, who can use rental income to pay off mortgages, cover maintenance costs or build savings. This secondary source of income makes homeownership more affordable and sustainable, especially in high-cost housing markets.

Vacation rentals also create entrepreneurship opportunities — who doesn’t have a friend who bought a second home to rent out on a short-term basis? These stories abound across the globe.

In improving opportunities for local communities and residents, these accommodations have revolutionized how people travel and work. Digital nomads can log in remotely from anywhere, families can rent out whole houses rather than sharing hotel rooms, and solo travelers can live in local neighborhoods.

As people look for more authentic experiences that align with their values, rentals are also responding to the demand for unique, sustainable experiences. Hundreds of hosts now offer green options, improved accessibility for travelers with disabilities and stays that directly benefit local communities.

So why are cities cracking down?

Well-intentioned, poorly executed policy backed by well-funded hotel lobbyists.

New York City’s STR crackdown was championed to free up housing and lower rents. Instead, hotel prices soared, long-term rents stayed stubborn, locals lost income streams, and small businesses lost foot traffic.

This equation added up to economic hardships for the very locals that these laws were meant to protect.

NYC’s experience shows that simply banning the option does not stop housing crises; it just moves the problem elsewhere.

Excessive regulation threatens homeowners, reduces tax revenues, chases away tourists and stifles economic opportunities.

The Milken Institute illustrates that California presents a compelling case for how these kinds of rentals can add value to local economies. In Monterey County, they generate millions in lodging taxes, directly financing public services, infrastructure and development. This case study illustrates that a more targeted and data-driven policy is exponentially superior to blanket prohibition.

Cities should focus on regulation for the responsible management of STRs while ensuring housing stability. Smarter policy is the key to sustainable economic growth.

The path forward: A win-win for cities and communities

Vacation rentals are here to stay — travelers want them, homeowners need them, and local economies depend on them. The benefits are too significant to ignore, from job and entrepreneurship development to tax revenue and economic empowerment. With strategic policies, these homes can coexist alongside long-term housing and propel local economies forward. Instead of stifling them, cities should unlock their power for good.

Vacation rentals are already fueling the future of travel. Let’s see them as the economic drivers they are, enriching our communities as they generate income for homeowners.

Julie Brinkman, CEO of Beyond, proudly leads a global team dedicated to helping short-term rental hosts grow their revenue. Connect with her on LinkedIn.

by Matt Carter | Jun 26, 2025 | Industry, News Feed

Common Securitization Solutions (CSS) has rebranded as U.S. Fin Tech and will look to provide technology and business solutions to companies in addition to its owners.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A little-known joint venture of Fannie Mae and Freddie Mac that processes billions in mortgage-backed securities is getting a new name and an expanded mission — offering its services to other clients.

Common Securitization Solutions (CSS) is rebranding as U.S. Fin Tech, and will look to provide technology and business solutions to companies in addition to its owners.

TAKE THE INMAN INTEL SURVEY FOR JUNE

U.S. Financial Technology LLC, as CSS is now formally known, is a Delaware company co-owned by Fannie Mae and Freddie Mac and regulated by the U.S. Federal Housing Finance Agency (FHFA).

Tony Renzi

“We are excited to have a name that demonstrates that we are leading the United States and the world in financial services technology,” CEO Tony Renzi said in a statement Thursday. Renzi was appointed as CEO of CSS in 2019 and continues to lead the rebranded company.

Established as a joint venture of Fannie and Freddie in 2014, CSS operates the Common Securitization Platform (CSP), a conduit through which the mortgage giants issue and administer trillions of dollars in mortgage-backed securities (MBS) that launched in 2019.

CSS has been a fully virtual, geographically dispersed company since 2020, and boasts that its cloud-based platform provides “unrivaled layered security architecture and traceability capabilities” providing “business continuity with full disaster recovery and zero data loss within 4 hours.”

CSS “meets the challenges of the market, such as data management, processing, and speed of execution, to bridge the gap between the secondary mortgage market and investors,” the company says.

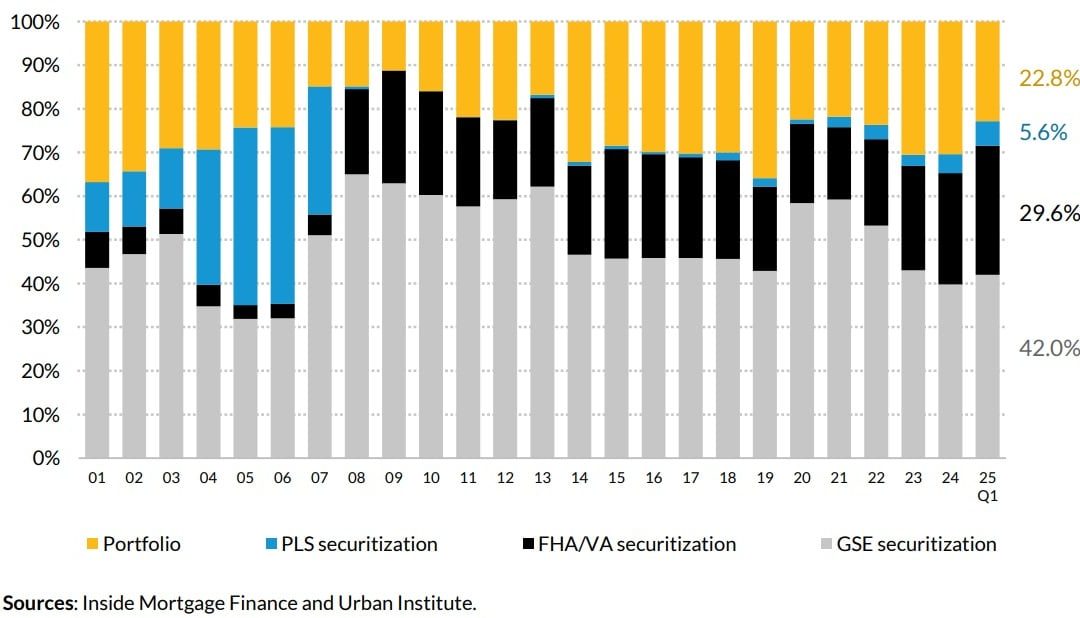

Mortgage funding sources, 2001-2025

Of the $355 billion in mortgages originated in the first quarter of 2025, Fannie and Freddie (the government-sponsored enterprises, or GSEs) packaged up 42 percent into MBS for sale to investors, according to data compiled by Inside Mortgage Finance and the Urban Institute.

Close to 30 percent of Q1 2025 originations were FHA and VA loan securitizations backed by Ginnie Mae, while 23 percent were made by lenders who kept them in their portfolios.

Securitizations of private-label securities (PLS) lacking the backing of Fannie Mae, Freddie Mac and Ginnie Mae were up 24 percent from a year ago, to $20 billion, but accounted for just under 6 percent of first-lien mortgage originations in Q1 2025.

PLS securitizations boomed at the turn of the century when lenders used them to finance subprime mortgages, but vanished for close to a decade after the 2007-2009 housing crash and Great Recession.

Fannie and Freddie were placed in government conservatorship in 2008 as their losses mounted, and the Trump administration is studying ways to restructure them.

Bill Pulte

Bill Pulte, Trump’s pick to run Fannie and Freddie’s regulator, has said the president is interested in taking the companies public, and might “sell a small piece” in the process.

“We created U.S. Fin Tech to demonstrate the incredible ingenuity of American technology under President Trump’s leadership,” Pulte said in a statement.

Pulte on Wednesday directed the mortgage giants to consider allowing borrowers to count cryptocurrency as an asset without having to convert their holdings into dollars.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Andrea V. Brambila | Jun 26, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Real estate trade groups, brokerages and landlords in New York City are taking their case against a broker fee law to a higher court and the city is fighting back.

On June 24, the City of New York responded to a lawsuit filed by the Real Estate Board of New York (REBNY), the New York State Association of Realtors, and seven real estate companies against the Fairness in Apartment Rental Expenses (FARE) Act, which requires rental property owners to cover broker fees when they enlist a broker to help them lease a unit.

TAKE THE INMAN INTEL SURVEY FOR JUNE

The trade groups and companies allege the legislation violates the First Amendment and the New York State Constitution, and was pre-empted by state law. The suit also claims the FARE Act violates the Contracts Clause of the U.S. Constitution since brokers and landlords can’t execute existing listing agreements that require brokers to negotiate and receive compensation from tenants.

In its answer to the suit, the city denies the allegations.

“Defendants City of New York and Commissioner [Vilda Vera] Mayuga have not violated any rights, privileges or immunities under the Constitution or laws of the United States or the State of New York or any political subdivision thereof, nor have defendants violated any act of Congress providing for the protection of civil rights,” attorneys for the city wrote.

They also pointed out that three of the four claims in the suit were dismissed by the court on June 10. Regarding the remaining claim, that the FARE Act violates the Constitution’s contracts clause, the city alleged that the plaintiffs lack standing to bring the claim.

“The only Plaintiff who has pled facts alleging that it has exclusive contracts impacted by the FARE Act is Bond New York,” the filing states, later adding that the court may lack the jurisdiction “over REBNY and Bond New York’s Contract Clause claim due to lack of standing and/or mootness.”

Meanwhile, the plaintiffs appealed the dismissal of the aforementioned claims on June 12 to the U.S. Court of Appeals for the Second Circuit. In a June 26 filing, they asked the higher court to decide “[w]hether the District Court erred in concluding that Plaintiffs failed to demonstrate a likelihood of success on the merits of their free speech claims,” among other questions.

Neither party has submitted appellate briefs yet. But in granting the city’s motion to dismiss in regards to most of the RENBY suit’s claims, District Court Judge Ronnie Abrams suggested that the plaintiffs were looking for a judicial solution to a political problem.

“In enacting the FARE Act, the City Council made clear that it sought to address a specific harm: the detrimental impact on housing mobility caused by the practice of imposing brokers’ fees on tenants,” Abrams wrote.

“Although the Act is not primarily intended to target speech and has only a relatively minimal impact on existing contracts, Plaintiffs have sought to enjoin its enforcement on the basis that it violates the First Amendment and the Contracts Clause.

“In their telling, the Act will wreak havoc on the City’s residential rental market, cause rents to rise, put brokers out of work, and make it exponentially more difficult for New Yorkers to rent apartments.”

Abrams stressed she did not believe it was the court’s job to decide which of these contrasting views was correct.

“Plaintiffs’ discontentment with the Act, however, stems not from its effects on their constitutional rights, but from a fundamental disagreement with its underlying policy,” she continued.

“The law is clear, though, that ‘[w]hether the legislation is wise or unwise as a matter of policy is a question with which [the Court cannot be] concerned.’ Thus, although some of Plaintiffs’ prophecies may prove true, Plaintiffs remedy is through the political process, not in court.”

Read NYC’s answer to REBNY’s suit (re-load page if document is not visible):

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

by Jeff Tucker | Jun 26, 2025 | Industry, News Feed

Windermere Economist Jeff Tucker looks at recent economic indicators, including some surprising upside despite a disappointing spring market.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

In this exclusive series on Inman, Windermere’s Principal Economist Jeff Tucker illuminates the latest stats, reports and numbers to know this week.

Number to know: 4.03M existing-home sales

I’ll be starting this month by checking in on one of the most important numbers for the real estate industry: existing-home sales. They actually surprised slightly to the upside in May, when closed sales ran at an annualized rate of 4.03 million. That is ever so slightly higher than April’s figure and ever so slightly lower than in May of 2024, but in both cases it’s less than a percentage point difference — let’s just call it roughly flat.

And “flat” pretty much sums up existing-home sales for the past couple of years: Outside of some seasonal outperformance this past Q4, we’ve just been bouncing around an annual sales rate of about 4 million.

Zooming out to the past 30 years puts that in perspective: 4 million existing-home sales puts us right around the lowest lows of home sales in the Great Recession. This lack of turnover is being driven by affordability challenges for buyers and the lock-in effect for sellers, as well as the aging of the U.S. homeowner population: Older folks just don’t move and sell as much as younger households.

But that doesn’t mean no one is trying to sell. The month of May ended with over a million active listings on the market, according to Realtor.com’s data, bringing the market very close to pre-pandemic inventory norms. In fact, the National Association of Realtors reported that when they measure inventory in terms of months of supply, it actually exceeds its May 2019 level.

Number to know: pending sales 3%

Pending sales ticked up by just under 3 percent in May, year-over-year. That’s an early indication we may see some modest year-over-year gains for closed sales in June, though the market is still looking quite sluggish.

Turning to the macroeconomy, we got another good, surprisingly cool CPI inflation report for the month of May. The annualized monthly growth rate of prices was almost exactly 1 percent, and the year-over-year change in CPI from last May was only 2.35 percent. This metric has been inching down closer and closer to the Fed’s goal of a 2 percent inflation rate, which is part of its dual mandate along with pursuing “maximum employment.”

Number to know: Mortgage rates 6.75%-7%

Finally, it’s another pretty quiet month for mortgage rates, which are once again stuck in a range between 6.75 percent and 7 percent. It’s been a busy news month, but mortgage rates mostly took it in stride, drifting down slightly in the past couple of weeks to end up basically where they were at this time last month.

The Federal Reserve declined to change its overnight Federal Funds Rate at its June meeting, but there is growing pressure to resume cutting rates soon, if inflation remains as muted as it has been this spring. Personally, I still think the Fed will wait until clearer signs of labor market deterioration before cutting; moreover, a growth slowdown is probably what bond traders need to see before long-term yields like mortgage rates fall substantially.

Jeff Tucker is the Principal Economist for Windermere Real Estate in Seattle, Washington. Connect with him on X or Facebook.

by Chris Morrison | Jun 26, 2025 | Industry, News Feed

Sharing knowledge, lifting others and celebrating victories creates an inviting foundation for unparalleled growth, new Inman contributor Chris Morrison writes.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

In an industry where tradition often supersedes innovation, we have seen something remarkable, where top-producing agents are making bold moves, departing institutional firms for a boutique luxury brand that barely existed only a few years ago.

TAKE THE INMAN INTEL SURVEY FOR JUNE

When building out your own team or bolstering your individual presence, we are sharing some valuable lessons. These are principles that can guide you on your journey, and we hope you find similar success.

The ingredients

Every final product begins with a great recipe. And while the ingredients may seem simple, how they come together can be magical.

- Be selective with your people

- Invest in technology that solves real problems

- Create a genuine culture of collaboration

- Lead and inspire; don’t just manage

- Maintain consistent, high-quality branding across all platforms

1. Be selective: Quality over quantity

For decades, the luxury real estate brokerage and team model has operated on a faulty premise: Recruit as many agents as possible, provide basic tools and hope for the best. Most brokerages and teams boast about having one or two top performers while carrying underperforming agents. It’s a flawed model that creates internal competition rather than collaboration, ultimately diluting a brand’s reputation.

Build something different by being extraordinarily selective. An agent with the wrong standards can irreparably damage your culture and reputation. When building your team, remember: quality over quantity.

We’re obsessed with quality over quantity. Our agent recruitment method is intentional, focusing on agents who not only meet the initial criteria but also align with our values.

Each agent on our team is a “hitter” — influential innovators and relationship builders who understand that real estate is about more than transactions; it’s about transformative experiences. They have integrity, consistently exceed expectations and are dedicated to preserving an extraordinary standard that benefits everyone.

This disciplined focus allowed us to grow to a billion dollars in sales within just 18 months. When building your team, remember that selective recruitment creates a foundation for exponential growth.

2. Technology with a purpose

The industry is saturated with flashy tech solutions that solve problems no one has. The key is to start by identifying the actual friction points agents experience every day — and then invest in or develop tools to solve those specific challenges.

For example, we use technology to identify 500 to 1,500 real estate professionals who have sold homes near a specific property and send a beautifully designed, targeted email campaign. This replaces the need for generic blasts to irrelevant agents and increases the likelihood of connecting with the right buyer pool. The result? Innovative outreach that respects both time and inboxes.

Technology should always reduce friction, not create more of it. Successful adoption doesn’t just come from having the right tools, but also from investing time in onboarding, training and ongoing refinement.

3. Culture as a competitive advantage

Instill a culture of integrity and mutual support where collaboration surpasses internal competition and where agents actively work alongside other agents, sharing insights, strategies and opportunities.

Maintain transparency and open communication about the team’s direction, including challenges and opportunities.

Hold frequent team meetings to share the latest listings, deals and best practices. And most importantly, always look to celebrate successes!

4. Lead and inspire

Recognizing the individual strength of each agent and providing personalized support help with retention. Articulate your clear vision for the firm, and ensure that each agent understands how they fit in that vision. If an agent requires professional development, then invest in their success. Above all else, exhibit the standards and work ethic you expect from others.

5. Build and maintain consistent, high-quality branding across all platforms

Presentation is everything, especially in marketing properties for sale. By developing marketing templates and aligning brand guidelines across your team, you create a strong and consistent brand. Invest in professional photography and curating your social media presence. Lastly, but not least, engage your clients in exclusive appreciation experiences, such as private property tours.

Your future team

Long-term success in our industry is measured by the relationships you build and the excellence you uphold. Sharing knowledge, lifting others and celebrating victories creates an inviting foundation for unparalleled growth. By thoughtfully combining these ingredients, you will craft an environment where your exceptional team can prosper.

Chris Morrison is the founding partner of RETSY, Arizona’s fastest-growing luxury real estate firm, headquartered in Scottsdale. Connect with Chris and his team on Instagram and LinkedIn.

by Christy Murdock | Jun 26, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Although he’s built a successful independent brokerage, you won’t find Sean Frank recommending that path to others. “With so many models competing in so many ways, it’s a challenge to create something very competitive from scratch. The honest reality is that I would not recommend starting a brokerage to most people. There are much better ways to spend time.”

One of the ways Frank’s brokerage, Mainframe Real Estate, differentiates itself is through its proprietary software development, “providing an all-in-one software that allows high-productivity agents to be extremely efficient and organized.” The emphasis on tech stems from Frank’s early experiences in the industry. “Technology in real estate is still lacking today, but it was horrendous at the time,” he said. “I had a passion for technology and wanted to create phenomenal tech for agents, and that was the driving factor for me [starting a brokerage].”

Name: Sean Frank

Title: CEO

Experience: 23 years

Location: Orlando, Florida

Brokerage name: Mainframe Real Estate

Rankings: Top 1 percent of brokerages in Central Florida

Team size: 53

Transaction sides: 670 (2024)

Sales volume: $270 million (2024)

How did you get your start in real estate?

I got my real estate license when I was 18 so that I could find a professional job while I was in college. The deeper I got into real estate over the years, the more experience I gained, and it became my career path in life. I wish I could say that I had some big dream to get into real estate, but it was much more happenstance.

What do you wish more people knew about working in real estate?

Real estate is not an easy business. It’s not the glitz and glam that it appears to be on social media. With a low barrier to entry, the industry is riddled with amateurs and unprofessional people. I wish consumers understood the huge gap in experience in the industry and what it could cost them.

For agents, even if they achieve great success in real estate sales, it’s at the costly sacrifice of their personal life. Agents always have to keep up sales momentum, and it can feel like being trapped on a hamster wheel. I warn people all the time not to get into real estate, but many people are naive to the reality, though they may not still be young.

What’s something you know now that you wish you knew when you started?

Before starting a brokerage, I wish I knew what it really took. Yes, it requires being nice and likable, but it’s about systems and processes more than anything. Growing a business is creating a monster. The bigger it gets, the more money and time it consumes. It’s not something someone can imagine before they are in it themselves.

These words could never convey the extreme amount of energy it took to get it off the ground. And then it’s a trap — you have to keep going and you can’t turn back. I have no regrets, but I completely underestimated what it would take to grow a successful company.

Tell us about a high point in your brokerage career

Learning to delegate and being able to afford to was a game-changer for my career. It took years of hard work and performing many roles in my company, but eventually, we grew to a point where I could begin offloading the work that I was doing. It allowed me to expand my mind and alleviate stress. Even more than a career accomplishment, it was a huge achievement for my personal life.

What’s your top prediction for next year?

I think the next 12 months of real estate will be a continuation of what we have seen over the last 12: a slowing market with more inventory and fewer buyers. Agents who have not been in the business more than five years don’t understand that the COVID-era market was a fantasy and that the swings of the market can be painful, and everyone needs to be prepared for them.

Tell us about an epic fail you’ve experienced since you’ve been a broker

The hardest part of leading a company is hiring and firing. The biggest mistake I made, especially in the early phases of the company, was not thoroughly interviewing people for positions. Hiring someone is a relationship, and ideally, it should last for as long as possible. But if somebody is underperforming and bringing down the team, they need to go.

The wrong employee is the most expensive person on staff because they are keeping the company from its highest potential. Learning how to hire properly can save unspeakable time, money and headaches.

What makes a good leader?

More than anything, a good leader is empathic. People want to know they are cared for and that their opinions matter. They want to believe they can give feedback, and it will be heard. Even if a leader can’t give everything that is asked of them, they can listen, learn and do their best. Culture is the most important aspect of any company, and it starts with a trusting and welcoming environment where everyone feels valued.

What’s one thing you wish every agent knew?

Relationships matter in this business more than anything. I see agents constantly trying to outshine other people on social media. They watch other agents “perform” and want to be like them. Nobody wants to pick up the phone and create deeper relationships anymore. Everyone is looking for a CRM or AI to build or maintain their relationships, but they will never replace authenticity.

The best part of this business is the relationships we build, so dive deep into them and watch the rewards that are created both personally and financially.