by Taylor Anderson | Jul 1, 2025 | Industry, News Feed

Celebrity agent Mauricio Umansky, who has targeted the National Association of Realtors’ dominance over agents and the rules governing real estate, heads back to court.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Celebrity broker and The Agency founder Mauricio Umansky has revived a simmering lawsuit that takes aim at rules created by the National Association of Realtors, arguing the rules help maintain unfair dominance over the nation’s multiple listing services.

The new lawsuit, filed in the U.S. District Court of Southern California, boils down to a few key arguments:

- Umansky alleges NAR controls competition in the residential real estate industry by controlling a large network of MLSs in the country.

- Namely, the Clear Cooperation Policy that requires listings to be placed on an MLS within one business day limits competition from companies seeking to offer private listings that are marketed outside the MLS.

- The policy stymied efforts by would-be competitors, like Umansky’s ThePLS.com, to give brokerages a new way to discreetly market homes for sale.

“The surge in consumer demand for pocket listings, and the rise of a listing network to market pocket listings effectively, was a competitive threat to the viability of the NAR-affiliated MLS system,” ThePLS.com wrote in its complaint, filed overnight on Tuesday. “These market changes also threatened NAR’s ability to control competition in the residential real estate brokerage industry.”

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

The federal antitrust lawsuit keeps pressure on NAR and its affiliated MLSs, and shows that the industry will remain engaged in a fierce debate over the rules — especially those governing private listings — that will guide the next chapter of the real estate industry.

Compass, the No. 1 largest brokerage by sales volume, last week filed a lawsuit against Zillow, the nation’s largest real estate portal by unique visitors. Compass is taking aim at updates to Zillow’s policies that require listings to be filed on the MLS and therefore on Zillow within one business day.

Compass is making the claim that Zillow is a monopoly and that its policy is anticompetitive because it prevents the company from growing its network of Private Exclusive listings, which are homes for sale and only accessible through a Compass agent. The network itself is marketed on Compass’ website, which is a violation of Zillow’s new standards.

The newly filed lawsuit keeps a target squarely on NAR and the Clear Cooperation Policy.

“Through the Clear Cooperation Policy, NAR and the MLS conspirators eliminated the possibility of a more competitive future in the market for residential real estate listing network services,” ThePLS.com wrote in the complaint. “A once-in-a-lifetime opportunity for competition in a monopolized market has been lost. NAR’s conduct has harmed competition and consumers, and is illegal.”

What is NAR saying?

The new filing actually represents the refiling of a case that Umansky and NAR fought over beginning in 2020, shortly after NAR adopted its Clear Cooperation Policy. NAR said that PLS had walked away from the negotiating table before filing its suit overnight, and it defended its Clear Cooperation Policy.

“NAR and PLS were in discussions to extend this agreement until PLS ceased to engage,” an NAR spokesperson said in a statement to Inman. “The Clear Cooperation Policy promotes transparency and competition in the real estate marketplace while still providing home sellers and their agents the option to list their property as an office exclusive.”

More context

After years of debate, NAR opted to keep Clear Cooperation in March, but at the same time rolled out a new policy to allow for the delayed marketing of a listing without violating the rule.

The update was an effort to balance criticisms of the policy, but it received mixed reviews among industry insiders.

ThePLS.com filed it’s first lawsuit against NAR in 2020, shortly after the trade organization first adopted the Clear Cooperation Policy.

NAR and ThePLS.com previously reached an agreement that dismissed the case but kept open the possibility of it being filed again at a later date.

“Where we landed is that we gave them a tolling agreement on the statute of limitations to give us time to figure out whether or not we were amenable to repealing the Clear Cooperation Policy,” former NAR outside legal counsel Ethan Glass said at a hearing in 2024.

Over the years, Umansky has challenged NAR in other ways as well.

Early last year, he was part of a team that launched the American Real Estate Association, a group that intends to compete with NAR.

“Right now I don’t feel like anybody is caring; we’re in a lot of trouble,” Umansky said at the time, arguing at another point, “We need better advocacy, we need better lobbying, we need to make sure we’re taken care of.”

Update: This post was updated after publication to add additional clarity.

Email Taylor Anderson

by Andrea V. Brambila | Jul 1, 2025 | Industry, News Feed

The rollout will be followed by the debut of BPP-powered local MLS sites and then a long-promised national consumer listing site to compete against Zillow, Realtor.com, Homes.com and Redfin.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The Broker Public Portal, a company formed by a large group of brokers and multiple listing services to launch the nation’s first national public-facing MLS website, has “soft” launched and added its 48th MLS investor.

TAKE THE INMAN INTEL SURVEY FOR JUNE

On June 30, the BPP went live with what CEO Dan Troup called a “soft launch” on BrokerData.com, which will be part of a three-phase launch program.

Dan Troup

“This is allowing us to test and demonstrate our technology in a production environment that anyone can look at,” Troup told Inman via email.

In October 2022, the National Broker Portal LLC, a joint venture owned 50-50 by Homesnap and the Broker Public Portal shut down, following CoStar’s purchase of Homesnap. CoStar subsequently sunset the Homesnap brand. At the time of their divorce, BPP said it would pivot to creating and providing a national listing data “superset” and forming multiple joint ventures with tech vendors that wish to use that data for their tech products.

According to Troup, the second phase of the BPP reboot “will be the launch of local market websites that are powered by our search solution but displayed on local MLS domains” while the third phase will be the debut of BPP’s national consumer-facing portal, which will replace Homesnap.com.

“Timing will be driven by our stakeholders and their value proposition to their members,” Troup said.

“We will launch as soon as our partners review the product and tell us to turn on their data.”

BPP’s investors are made up of 44 brokerages and 48 MLSs, the latter of which serve 1,047,000 agents combined, according to the company. The latest MLS investor to come on board is Cary, North Carolina-based Doorify MLS, which has nearly 15,000 agent and broker subscribers across 16 counties.

“Our investment in Broker Public Portal is a clear signal of Doorify MLS’s commitment to technology sovereignty in real estate,” said Matt Fowler, CEO of Doorify MLS, in a statement.

Matt Fowler

“By taking ownership in this broker- and MLS-controlled platform, we’re ensuring our industry retains vital control over its technology infrastructure and data. Our core mission is to provide consumers with the most comprehensive MLS search experience, directly connecting them with the local experts – their agents and brokers.

“This investment fortifies a platform truly built by the industry, for the industry, fostering genuine engagement between consumers and real estate professionals.”

Like every investor in BPP, Doorify MLS is limited to one share of the company. Each share, or unit, in the company costs $5,000.

“This has never changed,” Troup told Inman. “We are well-funded as a result of the our dissolution from Homesnap.”

“Every shareholder in BPP has the same rights and our governance has not changed – we are only funded by MLSs and Brokers. The investment from Doorify is in accordance with our governance and follows the same rules that previous shareholders are granted.

“The BPP is a crowdfunded effort that supports a national consumer MLS website to provide some competitiveness to the existing national portals.”

Whenever that national MLS website does launch, it will face a crowded field of well-established and well-funded rivals, including Zillow, Realtor.com, Homes.com and Redfin.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

by Jessica Souza | Jul 1, 2025 | Industry, News Feed

Your budget is your business plan in action, broker-owner and author Jessica Souza writes. Find out how to crunch the numbers and make them work as hard as you do.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Let’s be real — when you’re launching your real estate career, creating a business budget might feel a little … intimidating. Between licensing costs, marketing expenses and just trying to get your first deal closed, the idea of budgeting can feel like one more thing on an already overflowing to-do list.

But here’s what I want to tell every new (and honestly, not-so-new) agent: a business budget isn’t a restriction — it’s a roadmap. It’s what helps you make smart, confident decisions. It’s what gives you clarity in slow seasons and control in fast ones. And it’s what separates the agents who hustle paycheck to paycheck from the ones who actually build sustainable, scalable businesses.

I’ve seen both sides; I’ve lived both sides. And now, as a broker-owner coaching new agents every day, I’ve boiled the budgeting process down to five simple, doable steps that anyone can follow.

5 steps for building a business budget

Let’s break it down.

Step 1: Know your numbers (and separate your accounts)

First things first: You can’t manage what you don’t measure. Before you make a single budget decision, you need to know:

- How much is coming in (even if that’s $0 for now — this is about preparation)

- What your fixed and variable expenses are

- What your income goals are

Start by setting up separate business banking accounts. Even if you’re a one-person show, this is key. Having a separate account for your real estate income and expenses helps you stay organized, track your spending, and avoid those messy “Wait, was this dinner a business expense or date night?” moments.

Protip: Open a business checking and a tax savings account. Every time you get paid, transfer 20 percent to 30 percent into your tax account before you even blink. Future you (and your CPA) will be forever grateful.

Step 2: Build your baseline budget

Now that you’ve separated your accounts and tracked your basics, it’s time to build a budget that reflects what you actually need to run your business.

Here’s a list of common new agent startup and recurring costs:

Startup

- Licensing + exam fees

- Local, state, and national association dues

- MLS access

- Business cards, signage, lockboxes

- Headshots and initial marketing

Monthly/Quarterly

- Brokerage fees or splits

- CRM or lead generation platforms

- Social media scheduling tools (think Canva, Later)

- Website hosting or IDX feed

- Fuel, car maintenance, office supplies

- Continuing education

Now, set realistic monthly and quarterly budgets for these categories. Don’t overshoot your tools and tech. You don’t need everything at once. Start lean, then grow intentionally.

Remember: Just because it’s a write-off doesn’t mean it’s free.

Step 3: Plan for slow seasons and the ‘no check’ gap

Real estate is a feast-or-famine business if you’re not careful.

It’s easy to get a big commission check and feel like you’ve got money to burn. But smart agents — ones who last — know to treat every check like it’s part of a bigger puzzle.

Here’s how:

- Plan your personal budget around your lowest average month, not your best one

- Create a reserve fund for business expenses — ideally three to six months

- Remember: there’s often a 30-90 day lag between doing the work and getting paid

Start thinking like a CEO, not just a salesperson. Your business needs cash flow, cushion and clarity. Treat your commission as income to be managed, not a jackpot to be spent.

Step 4: Use tools that help you instead of confusing you

If you’re someone who breaks into a cold sweat at the thought of spreadsheets, you’re not alone. Good news: You don’t need to be a numbers nerd to build a great budget.

Here are a few tools I recommend:

- QuickBooks Online: Great for tracking expenses and mileage

- Wave: A free, beginner-friendly accounting platform

- Google Sheets: Customize your own tracker

But here’s the real key: Use it consistently. Block out 30 minutes once a week to check in on your numbers. Know what’s coming in, what’s going out and what needs adjusting. Budgeting isn’t a one-time setup; it’s a habit.

Step 5: Budget for growth, not just survival

This step is often missed, but it’s what makes the difference between staying stuck and scaling with intention.

Too many agents budget just to get by. But a great budget should include room to grow, even if the numbers are small at first.

Set aside funds for:

- Future marketing campaigns

- Coaching or training opportunities

- Upgrading your systems or software

- Celebrating wins (yes, budget for the celebratory coffee after a hard week)

I like to call this your “vision line” in the budget. It’s not required for survival, but it’s essential for momentum. You’re not just building a business to stay afloat. You’re building a life you’re excited to wake up to.

Your budget is your business plan in action

At the end of the day, a budget isn’t just about dollars. It’s about decisions. It’s about choosing where your energy (and your money) goes, so your business feels more aligned than chaotic.

If you’re a new agent reading this, wondering where to even begin, let me say this clearly:

You don’t have to be perfect. You just have to be willing. Willing to look at your numbers. Willing to learn. Willing to treat your business like it matters — because it does.

So open the spreadsheet. Separate your accounts. Build your baseline. And take the first step toward a business that doesn’t just survive — it soars.

I’m cheering you on. Every click, every dollar, every smart decision at a time.

Jessica Souza is a broker-owner and author. Connect with her on LinkedIn and Instagram.

by Matt Carter | Jul 1, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

After staying stuck in the high sixes for two months, mortgage rates are coming back down as investors seeking certainty pull money out of the stock market and move it into bonds and mortgage-backed securities that fund most home loans.

But there’s no guarantee that the downward move in mortgage rates is sustainable, economists say, and hopes that home sales will pick up may hinge more on additional inventory coming onto the market, which is expected to cool or reverse home price gains.

After popping in April over concerns that the Trump administration’s tariff policies could reignite inflation, mortgage rates have been trending down since May 21.

At 6.67 percent Monday, lender data tracked by Optimal Blue shows rates on 30-year fixed-rate mortgages are down 25 basis points since May 21 and 38 basis points from the 2025 high of 7.05 percent registered on Jan. 14.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

A basis point is one hundredth of a percentage point. So rates have come down by 1/4 percentage point in the last five weeks — more than halfway to the 2025 low of 6.48 percent seen on April 4.

“The drop in rates is small but still helpful,” National Association of Realtors Chief Economist Lawrence Yun said in a statement to Inman.

Mortgage rates trending down

Yun noted that 10-year Treasury yields — a barometer for mortgage rates — have made a similar downward move, and pointed out a few key reasons behind the trend.

Lawrence Yun

“First, there is an improved prospect of tariff negotiations,” Yun said. “Second, the likelihood of a Fed rate cut in September — or possibly even sooner — has increased, with two voting members publicly stating support for a July rate cut. Finally, actual inflation is calmer than forecasted in April and May, helped by decelerating shelter costs.”

Although the Trump administration has been putting the heat on Federal Reserve Chair Jerome Powell to lower short-term interest rates, mortgage rates are determined largely by investor demand for mortgage-backed securities (MBS).

When the prospects for economic growth look precarious, investors pile into MBS and government bonds seeking safe returns. More demand for bonds and MBS drives up their prices and brings down their yields.

But when inflation looks like a potential threat to their returns, investors will demand higher yields — driving up borrowing costs for homebuyers.

When the Fed cut short-term rates three times at the end of last year by a full percentage point, mortgage rates went up as investors weighed incoming data showing inflation moving away from the central bank’s 2 percent goal.

Where interest rates are headed next depends in large part on the outcome of ongoing tariff negotiations and Congress’ tax and spending policies, and forecasting mortgage rates can be a tricky business.

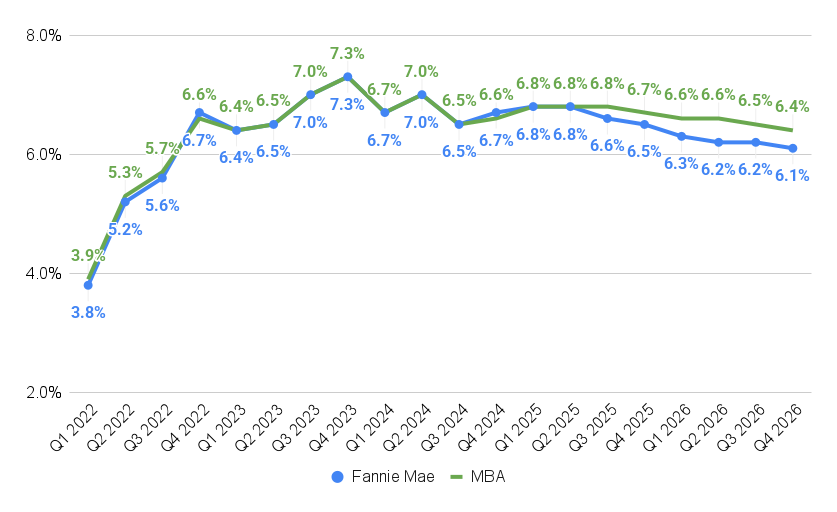

But in their latest forecast, economists at the Mortgage Bankers Association on June 20 predicted rates for 30-year fixed rate loans will end the year about where they are now — at 6.7 percent.

Mortgage rates forecast to stabilize

Source: Fannie Mae and Mortgage Bankers Association forecasts, June 2025.

The MBA sees mortgage rates coming down only gradually next year, to 6.4 percent by Q4.

Edward Seiler

A June 12 forecast by Fannie Mae economists was slightly more optimistic, predicting rates will drop to 6.5 percent by Q4 2025 and to 6.1 percent by the end of next year.

MBA economist Edward Seiler, the executive director of the Research Institute for Housing America (RIHA), told Inman that cooling home price appreciation is likely to have a bigger impact on affordability than mortgage rates.

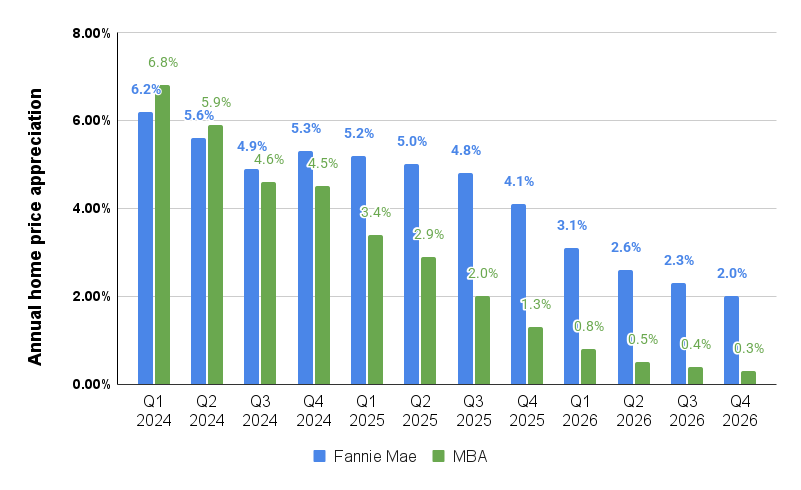

Home price appreciation expected to cool

Source: Forecasts by Fannie Mae (April 2025) and Mortgage Bankers Association (June 2025).

Fannie Mae’s home price appreciation forecast is published quarterly, and hasn’t been updated since April.

MBA forecasters in June predicted that national home price appreciation will cool to 1.3 percent by the end of this year, and to 0.3 percent by Q4 2026.

Since the MBA’s forecast also predicts that inflation will swell to 3.2 percent by the end of next year, that implies national home price growth will be negative in real terms.

Price declines are expected in markets where inventory is coming online faster than houses are sold.

Among the 20 largest housing markets tracked by the S&P CoreLogic Case-Shiller Index, two saw year-over-year declines in April — Tampa (-2.2 percent) and Dallas (-0.2 percent).

Nicholas Godec

“The underlying market dynamics remain challenging but not dire,” S&P Down Jones Indices analyst Nicholas Godec said in a statement.

Elevated mortgage rates are keeping monthly payment burdens near generational highs, and the mortgage lock-in effect continues to constrain housing supply, he said.

The supply-demand imbalance “continues to provide a price floor, preventing the sharp [price] corrections that some had feared.”

It’s a market in transition, Godec said, where “local fundamentals matter more than national trends.”

Housing and mortgage experts polled by Fannie Mae in May saw Austin, Tampa, Dallas, Denver, Houston, Miami, Phoenix, Washington, D.C., and Atlanta as markets where home prices are most likely to underperform national home price appreciation over the next 12 months.

Among the 20 largest U.S. housing markets, Boston, New York, Philadelphia, Nashville and San Diego were viewed as places where prices are most likely to go up faster than the national average.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 30, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Mortgage giant Rocket Companies completed a reorganization of its capital structure Monday that will pave the way for the acquisition of tech-forward real estate brokerage Redfin — a deal it’s claimed could cut consumers’ transaction costs in half by compressing agent fees, mortgage gain-on-sale and title premiums.

The all-stock deal, valued at $1.75 billion when announced in March, went unchallenged by antitrust regulators and was approved by Redfin shareholders on June 4.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

In announcing the completion of its reorganization in a regulatory filing, Rocket said it reduced its classes of common stock from four to two in an “Up-C Collapse” that will improve its ability to use its common stock as acquisition currency for future deals.

That includes Rocket’s next big acquisition target, Mr. Cooper Group Inc., the nation’s biggest loan servicer, for stock valued at $9.4 billion.

Company executives have said acquiring Redfin will help subsidiary Rocket Mortgage capture 8 percent of the purchase loan market, and the Mr. Cooper deal will put Rocket in touch with more homeowners who might be ready to refinance.

Detroit-based Rocket wants to handle 20 percent of U.S. mortgage refinancings, and Rocket CEO Varun Krishna said last month that the company has invested about $500 million in AI and other technology that will help the company scale its business without a proportionate increase in expenses after the mergers.

In a March 10 investor presentation, Rocket executives said that by handling every aspect of homebuying and selling — from home search to mortgage financing and title and closing — they aim to cut transaction costs on the median priced home from $40,000 to $20,000.

“For far too long, the homeownership process has been outdated and disconnected,” Krishna told investment analysts in March. “Home search, brokerage, mortgage, title, closing, servicing, all exist in separate ecosystems, forcing consumers to piece together a complex and frustrating journey.”

Redfin shareholders will receive 0.7926 shares of Rocket common stock for each share of Redfin they own. Shares in Rocket closed at $14.18 Monday, up from $9.51 per share before the deal was announced.

Redfin will remain headquartered in Seattle, with CEO Glenn Kelman continuing to lead the business and reporting to Krishna.

“Rocket’s and Redfin’s approaches to lending and brokerage service have always just been two halves of one vision to make the whole home-buying process magical,” Kelman blogged in March.

In reporting first-quarter earnings in May, Rocket executives said the Mr. Cooper acquisition remains on track to close by the end of the year.

Rocket announced on June 3 that it would issue $4 billion in debt and use the proceeds to retire notes held by Mr. Cooper subsidiary Nationstar Mortgage Holdings Inc.

Editor’s note: This story has been updated to clarify that Rocket Companies announced an “Up-C Collapse” reorganization Monday to pave the way for its closing of deals to acquire Redfin and Mr. Cooper.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Taylor Anderson | Jun 30, 2025 | Industry, News Feed

Zillow attorneys pushed back at Compass’ request for a broad and expedited discovery, and on the brokerage’s private listing network. ‘Compass would erect new barriers for buyers by making listings exclusive to each broker.’

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Compass faces no real harm from Zillow’s updated policy banning publicly marketed private listings from its platform, the portal said in a new legal filing on Monday.

In response to filings in Compass’ antitrust lawsuit challenging Zillow’s private listings policy, the nation’s largest real estate portal said that Compass waited until near the deadline to go to court and was seeking to “turn back the industry-wide status quo of transparency and liquidity.”

TAKE THE INMAN INTEL SURVEY FOR JUNE

“Zillow provides maximum transparency and has become a trusted resource for millions of users, who are able to use Zillow to find buyer agents who represent their best interests rather than relying on listing agents whose duty is to the seller,” the company wrote in its filing.

It was Zillow’s first response in court to the lawsuit Compass filed a week ago. On Friday, Compass also asked the judge overseeing the case to file a preliminary injunction on Zillow’s updated listing access standards, which require listings to be filed on the MLS and therefore on Zillow within one business day of any public marketing.

The policy seemed to take aim at Compass’ 3-Phased Marketing Strategy, the first of which includes putting a listing on the brokerage’s private listing network without going onto the MLS. The first phase of a Compass listing under the strategy is known as a Private Exclusive.

“Put plainly,” Compass wrote in its complaint, “Zillow has granted itself the power to ban every Compass Private Exclusive listing from going to Zillow because of the way in which Compass markets and executes its Private Exclusive listing strategy internally and externally.”

In its lawsuit, Compass argued that its Private Exclusives were considered “office exclusives,” or exempt listings where the seller directs their agent not to widely disseminate a listing publicly.

According to NAR: “The office exclusive listing shall be filed with the MLS but not disseminated to other MLS Participants and Subscribers.”

A spokesperson for NAR declined to comment on whether Compass’ Private Exclusives were considered office exclusives under that definition.

“NAR is not a party to this lawsuit and has no comment,” the spokesperson said.

According to Zillow’s updated policy, a listing within a brokerage’s private listings network would violate the policy if that network is itself publicly marketed on the brokerage’s website.

“Compass would erect new barriers for buyers by making listings exclusive to each broker — resulting in reduced transparency, less market liquidity, and a more frustrating and less efficient experience for buyers and sellers,” Zillow wrote in its filing.

“Likewise, other entities that display for-sale listings to prospective buyers, including Compass, remain free to display such listings from any source, including the MLS, regardless of whether Zillow would display them,” it continued.

The legal filing was made in opposition to Compass’ request for expedited discovery.

Compass attorneys are hoping to receive from Zillow any communication between Zillow, Redfin, eXp and other brokerages, along with unspecified documents about what it calls the Zillow Ban, documents outlining Zillow’s interactions with certain MLSs, and more.

It also wants data about Zillow’s users and traffic, and documents related to competition in the real estate portal market.

In its filing, Zillow wrote that the request was unreasonable.

“Compass’s requests seek potentially hundreds of thousands of documents (if not more) and terabytes of highly confidential data,” the attorneys wrote. “Compass, without seeking leave, has also indicated that it will seek fact depositions and expert discovery.”

Email Taylor Anderson