by Matt Carter | May 21, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

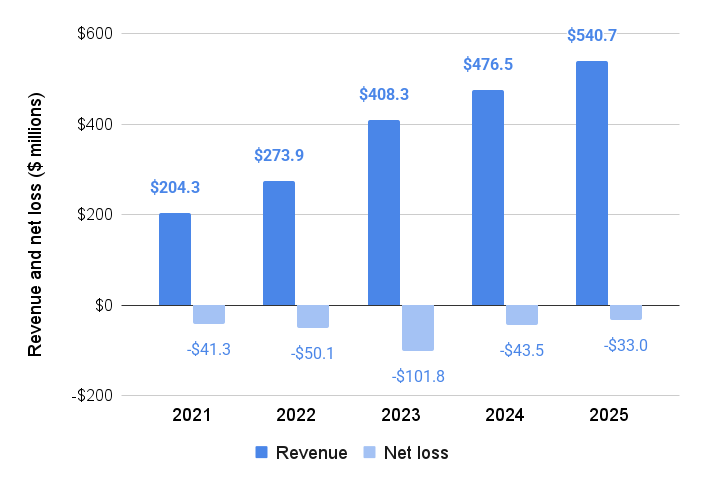

Cloud banking solutions provider nCino Inc. surprised investors with a sneak peek at its upcoming earnings report Tuesday, revealing that revenue and income exceeded the cautious guidance it provided last month.

Shares in nCino hit an all-time low on April 2, the day after the company reported an $18.6 million fourth quarter net loss despite growing revenue by 14 percent from a year ago, to $141.4 million.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

Company executives issued guidance for Q1 last month predicting:

- Total revenue of between $138.75 million and $140.75 million.

- Subscription revenue of between $121.75 million and $123.75 million.

- “Non-GAAP” operating income between $22.5 million and $24.5 million.

Preliminary financial results for the first quarter ended April 30, 2025, “exceed the top end of previously disclosed financial guidance ranges for total revenues, subscription revenues, and non-GAAP operating income,” the company announced Tuesday, without providing further details.

Ncino will report first quarter results after the market closes on May 28. Shares in nCino, which in the last 12 months have traded for as little as $18.75 and as much as $43.20, gained 4 percent Tuesday to close at $25.81.

Non-GAAP financial measures exclude factors like acquisition-related expenses and stock-based compensation. The company also provides GAAP measures that follow Generally Accepted Accounting Principles (GAAP) as required by securities regulators.

In a May 9 annual report to security holders, nCino said the company’s unrecognized compensation expenses related to non-vested stock-based compensation totaled $145.7 million as of Jan. 31. Those costs are expected to be recognized over the next three years, as shares granted to executives and employees vest.

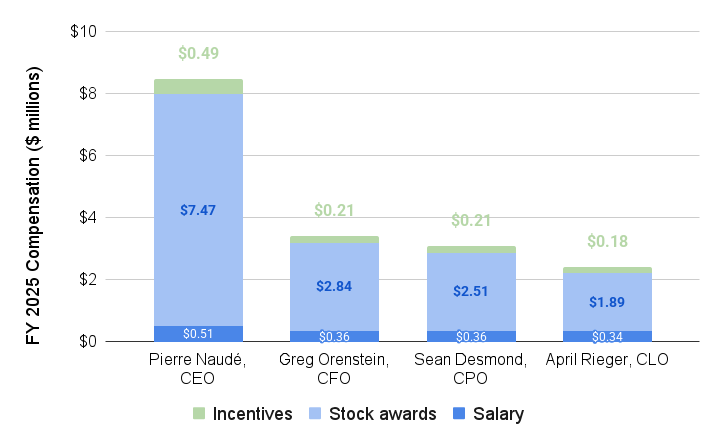

In notifying shareholders of the company’s upcoming annual meeting on June 18, nCino detailed past compensation of top executives including former CEO Pierre Naudé, and Chief Product Officer Sean Desmond, who succeeded Naudé as CEO on Feb. 1.

Stock awards to top executives

The company’s five top executives — Naudé, Desmond, Chief Financial Officer Greg Orenstein, Chief Legal Officer April Rieger and former president Josh Glover — have been granted $49.8 million in restricted stock awards over the last three years.

Naudé’s compensation has included $21.6 million in stock awards during that period, including $7.47 million in fiscal year 2025, which ended on Jan. 31.

Although Naudé, 66, is no longer CEO, he is still employed by the company as executive board chair. His son, Pierre W. Naudé, and daughter, Petra Sheaffer, are also nCino executives.

As senior manager, product management, the younger Naudé earned $360,000 last year, including restricted stock grants valued at $154,000.

Sheaffer was paid $506,000, including $299,000 in restricted stock grants, for her role as associate director, technical partner relationship manager.

Excluding the senior Naudé, the median annual compensation of all 1,832 nCino employees as of Jan. 31 was $112,179, meaning the CEO was paid 76 times as much, the company disclosed.

Ncino offers an employee stock purchase plan that lets rank-and-file workers buy shares in the company for 85 percent of their fair market value.

At launch in 2020, the program authorized the company to issue a total of up to 1.8 million shares for sale to participating employees, a number that automatically increases each year. As of Jan. 31, 5.48 million shares of nCino common stock remained available for employees to purchase.

NCino, which raised $268.4 million in a July 2020 initial public offering, on April 1 announced plans to repurchase up to $100 million of the company’s outstanding common stock.

Growing revenue in search of profits

Ncino revenue and net losses, fiscal years 2021-2025 ending Jan. 31. Source: NCino regulatory filing.

Since launching in 2011, Wilmington, North Carolina-based nCino has racked up $385.3 million in cumulative losses.

The company, whose clients include independent mortgage banks Synergy One Lending and Fairway Independent Mortgage Corp., has grown revenue in part through strategic acquisitions of SimpleNexus, DocFox, FullCircl, Integrated Lending Technologies (ILT), Visible Equity and FinSuite.

In some cases, nCino will issue restricted stock to key employees of companies that it acquires in an effort to incentivize them to stay.

Last year the company paid $74.3 million in cash to acquire DocFox. But it also issued 198,505 restricted stock units in nCino to certain DocFox employees valued at $6.1 million. The stock grants, which will vest over four years if the employees continue to work for nCino, were recorded as stock-based compensation after the acquisition.

On nCino’s April 1 earnings call, Desmond said nCino’s most recent acquisition — of Boston, Massachusetts-based integration technology provider Sandbox Banking for $52.5 million in February — is likely to be its last for now.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 20, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Surveys show consumers and real estate professionals are increasingly anxious about the economy. But many would-be homebuyers would actually welcome a recession as an opportunity if it leads to lower prices and rates, polling shows.

The University of Michigan Index of Consumer Sentiment slipped to 50.8 in May, its second lowest reading ever, and only 23 percent of Americans surveyed by Fannie Mae in April said it was a good time to buy.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

And now a majority of Americans shopping for homes on Realtor.com (63%) expect the economy will dip into a recession within a year, according to a survey Monday from the official search portal of the National Association of Realtors.

“Confidence in the economy has clearly taken a hit amid ongoing headlines around trade, tariffs and rate uncertainty,” Realtor.com Chief Economist Danielle Hale said in a statement.

But 30 percent of would-be homebuyers visiting Realtor.com in the first three months of the year said a recession would make them at least somewhat more likely to buy — nearly twice the share (16 percent) who said they’d be less likely to buy if the economy tanks.

Danielle Hale

“Well-prepared buyers who have been waiting on the sidelines are likely motivated by personal and lifestyle needs like growing families, new jobs, or retirements and these considerations can outweigh short term economic uncertainties,” Hale said.

Elevated mortgage rates and a surge in home prices have priced many buyers out of the market, and a recession could bring relief on both fronts. That helps explain why last fall, 36 percent of Americans polled by LendingTree said they were hoping the housing market would crash in 2025.

While it’s unlikely many Americans want to relive the pain of the 2007-2009 Great Recession — in which millions of Americans lost their homes to foreclosure — a milder economic downturn could unlock inventory in markets where listings are scarce.

The mortgage lock-in effect — which makes homeowners with low rates reluctant to trade up or down because they’d have a higher rate on their new mortgage — diminishes when mortgage rates fall.

During the first week in May, demand for purchase loans picked up for the second week in a row as mortgage rates stabilized and more listings came on the market. Lenders received 18 percent more purchase mortgage applications during the week ending May 9 than had the same time a year ago, surveys by the Mortgage Bankers Association (MBA) show.

Mike Fratantoni

“Despite the economic uncertainty, the increase in home inventory means there are additional properties to buy, unlike the last two years, and this supply is supporting more transactions,” MBA Chief Economist Mike Fratantoni said of the most recent survey results.

Nationwide, there were 31 percent more homes for sale in April than there were a year ago, according to Realtor.com data. The 959,251 active for-sale listings that homebuyers had to choose from last month marked a new post-pandemic high.

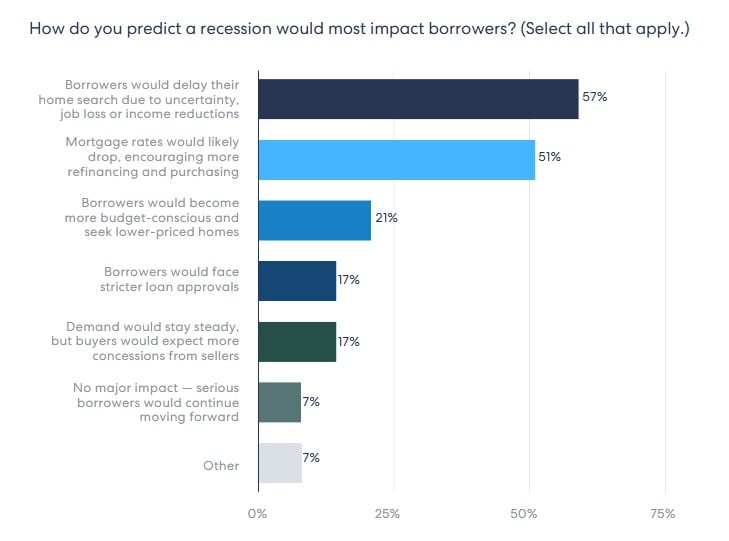

What loan originators are seeing

Most mortgage loan originators (63 percent) are also expecting a recession, and 57 percent think a recession would cause would-be homebuyers to delay their search due to uncertainty, job loss or income reductions, according to a recent survey by HomeLight.

But loan originators see a recession as a mixed bag, with slightly over half (51 percent) expecting that mortgage rates would also come down, leading to more homebuying and refinancing.

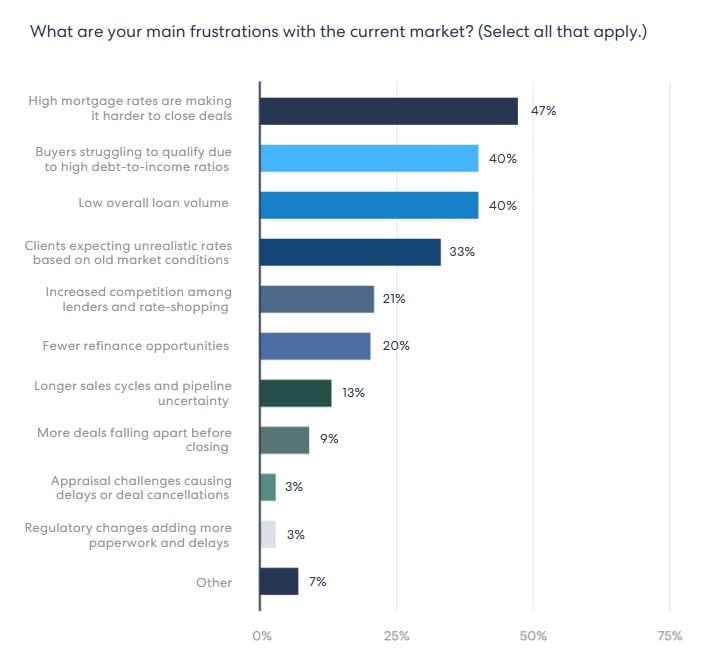

HomeLight’s Q2 2025 Lender Insights and Predictions survey, which was fielded between April 17 and 26, showed that loan originators expect that a recession would lead homebuyers to seek better deals and demand more seller concessions — and also have a harder time qualifying for a loan.

Seeing buyers struggling to qualify due to high debt-to-income ratios is already the second biggest frustration of loan originators, topped only by closings being derailed by elevated mortgage rates, HomeLight’s survey found.

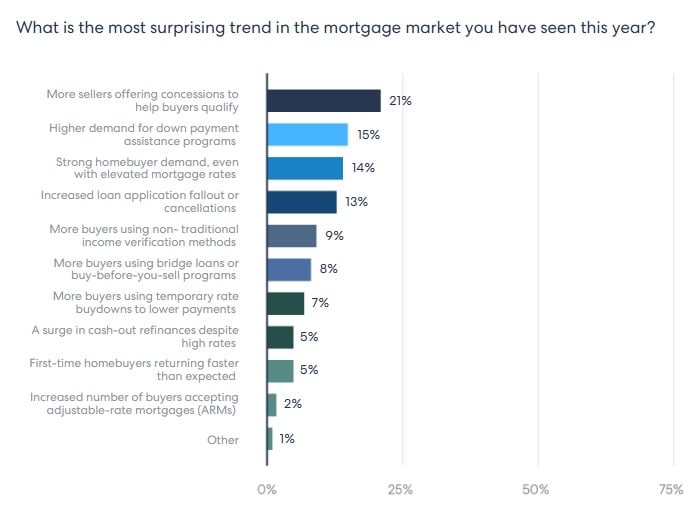

One in five loan originators (21 percent) said seller concessions are rising as a “surprising trend in the mortgage market” to help buyers qualify, and 15 percent said there’s more demand for down payment assistance programs.

Only 9 percent of loan officers surveyed by HomeLight say more deals are falling apart before closing, but that trend is on the rise.

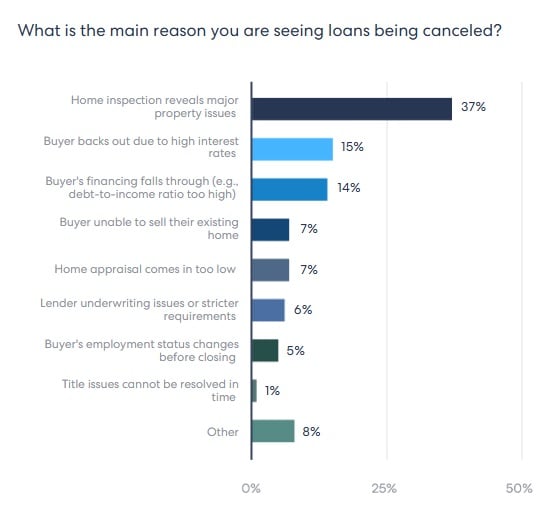

Home inspections are the main reason deals fall apart, 37 percent of loan originators said, followed by buyers getting cold feet over mortgage rates (15 percent) or seeing their financing fall through (14 percent).

Michelle Jacinto

“Buyer commitment is wishy-washy,” Michelle Jacinto, a branch manager at Direct Mortgage Loans LLC in Indiana, told HomeLight. “Any slight challenge, and they want to cancel. Anything from payments, cash to close, inspection items, or timeline changes.”

Devon Rowe, a mortgage advisor with Advantage Mortgage in Woodland, Washington, said buyers get nervous and news scares them.

A home inspection can “serve as a reason to back out of the contract, even when sellers are willing to do the repairs,” Rowe told HomeLight.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 19, 2025 | Industry, News Feed

Moody’s Ratings is the last credit agency to strip U.S. of most favorable debt rating over concerns that Congress and “successive U.S. administrations” have failed to tackle annual budget deficits, growing interest costs.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Mortgage rates surged Monday after Moody’s Ratings downgraded the U.S.’s credit rating over concerns that “successive U.S. administrations” and Congress have failed to tackle the nation’s annual budget deficits and growing interest costs.

With Republicans poised to extend tax cuts implemented during the first Trump administration — and with mandatory spending on Social Security, Medicare and interest payments on U.S. debt also expected to rise — Moody’s downgraded the U.S.’s long-term issuer and senior unsecured ratings to Aa1 from Aaa.

“This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns,” Moody’s analysts said.

TAKE THE INMAN INTEL SURVEY FOR MAY

The downgrade represented “a major symbolic move” since the other major rating agencies had already stripped the U.S. of its top credit rating, analysts at Deutsche Bank said in a note to clients.

The announcement — made minutes before bond markets closed Friday — helped drive rates on 30-year fixed-rate mortgages up seven basis points Monday, to 6.99 percent, according to data tracked by Mortgage News Daily.

Yields on 10-year Treasury notes, a barometer for mortgage rates, briefly touched a high of 4.56 percent Monday, up 17 basis points from Friday’s low of 4.39 percent.

Appearing on NBC’s Meet the Press on Sunday, Treasury Secretary Scott Bessent dismissed the downgrade by Moody’s and other agencies as a “lagging indicator,” and pointed the finger of blame at the Biden administration.

“We didn’t get here in the past 100 days — it’s the Biden administration and the spending that we have seen over the past four years,” Bessent told NBC’s Kristen Welker. “We inherited a 6.7 percent deficit relative to GDP — the highest when we weren’t in a recession or not in a war — and we are determined to bring the spending down and grow the economy.”

Welker pointed out that the first Trump administration added $8 trillion to the nation’s debt, which economists attribute to 2017 tax cuts and a surge in spending during the pandemic.

Bessent objected that the Trump administration handled “the rescue portion of COVID” while the Biden administration was responsible for “the recovery portion.”

Moody’s analysts said U.S. debt, which hit $36.2 trillion last year, has been rising sharply for more than a decade, as federal spending increased and tax cuts brought in less revenue.

They noted that most federal spending — 73 percent in 2024 — is on mandatory entitlement programs like Social Security, Medicare and interest on the U.S. debt, which has soared to more than $1 trillion annually.

“Without adjustments to taxation and spending, we expect budget flexibility to remain limited, with mandatory spending, including interest expense, projected to rise to around 78 percent of total spending by 2035,” Moody’s analysts said.

If the 2017 Tax Cuts and Jobs Act is extended — as Trump and Congressional Republicans are pushing for — that would add around $4 trillion to the federal fiscal primary (excluding interest payments) deficit over the next decade, Moody’s analysts concluded.

Just back from a trip to the Mideast, Bessent claimed countries in the region are poised to invest trillions of dollars in the U.S.

“Who cares?” Bessent said of the Moody’s downgrade. “Qatar doesn’t, Saudi [Arabia] doesn’t, UAE doesn’t — they’re all pushing money in. They’ve made 10-year investment plans. This administration, we’re doing peace deals, trade deals and tax deals.”

Federal deficit as a percentage of GDP

Economist Stephen Moore — a Project 2025 author who Trump tried to appoint to the Federal Reserve’s governing board in 2019 — lashed out at Moody’s Ratings in a Fox Business op-ed Monday.

Although Moody’s was the last of the credit rating agencies to downgrade the U.S.’s credit rating, Moore called the timing of the downgrade “particularly suspicious,” coming “just as Congress is voting on the Trump tax cut.”

“What Moody’s and other credit-rating agencies still can’t understand is that tax cuts like Ronald Reagan’s in 1981 and Trump’s 2017 bill grow the economy and, over time, lower the debt burden as a share of the nation’s wealth,” Moore wrote. “More people working and less people on welfare is a great way to lower debt spending. If we can get the growth rate up to 3 percent — which President Trump is aiming for — the debt burden starts to shrink.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 16, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A closely followed measure of consumer sentiment deteriorated for the fifth month in a row in May and is approaching an all-time low, but the economy continues to do better than it and other surveys might imply, economists say.

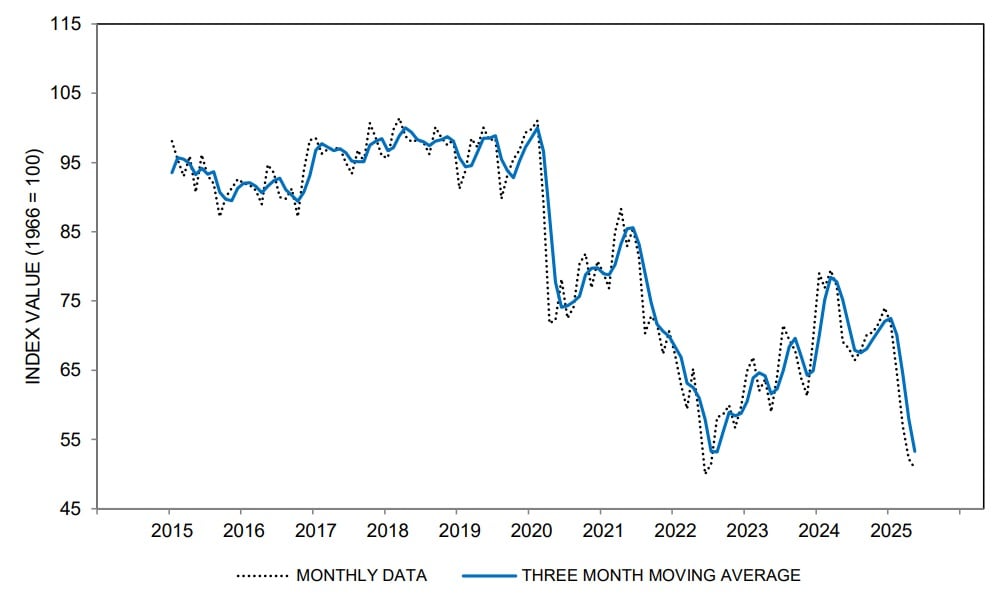

The University of Michigan Index of Consumer Sentiment slipped to 50.8 in May, down 3 percent from April and 26 percent from a year ago, according to preliminary data released Friday.

Joanne Hsu

Three-quarters of those surveyed cited tariffs as a cause for concern, and “uncertainty over trade policy continues to dominate consumers’ thinking about the economy,” survey director Joanne Hsu said in a statement.

The survey was fielded between April 22 and May 13, so many responses were gathered before the Trump administration announced a pause on some tariffs on goods from China on May 12.

UofM Index of Consumer Sentiment

The Consumer Sentiment Index hit an all-time low in records dating to 1978 in June 2022, when inflation as measured by the Consumer Price Index was hitting a post-pandemic high of 9.1 percent.

The Consumer Price Index for April, released Tuesday, showed prices were up 2.3 percent from a year ago last month, closer to the Fed’s 2 percent goal than the 3 percent annual inflation registered in January.

“The Michigan report continues to paint, at face value at least, a grim picture,” Pantheon Macroeconomics Senior U.S. Economist Oliver Allen said in a note to clients.

The Index of Consumer Expectations — which historically has been a better guide to growth in consumers’ real spending — was down 32 percent from a year ago in May, to 46.5 — the lowest reading since 1980, Allen noted.

It’s not just the prospect that tariffs will reignite inflation that has consumers worried. Confidence in the labor market “has taken a heavy blow, with the net share of households expecting higher unemployment remaining around its highest level since the global financial crisis,” Allen said.

There’s little doubt the economy is decelerating — an advance estimate of real gross domestic product (GDP) suggested that the economy shrank by 0.3 percent during the first quarter, thanks to a tariff-driven surge in imports and a decrease in government spending.

But forecasters at Pantheon Macroeconomics suspect consumer surveys — and the University of Michigan survey in particular — paint an “unduly negative” picture of consumer outlook.

Retail sales posted gains in March and April, and “most near-real indicators of consumers’ discretionary spending on services are holding up well,” he said.

Oliver Allen

“Our view is that consumers’ spending will soften as the wave of pre-tariff purchases unwinds, higher prices for imported goods take a bite out of real incomes, and policy uncertainty further undermines hiring and the labor market,” Allen concluded. “But we doubt consumption growth will slow nearly as sharply as the Michigan survey currently implies.”

Surveys by the Mortgage Bankers Association show demand for purchase mortgages has increased for two weeks in a row, as would-be homebuyers responded to growing inventories of listings in many markets and stabilizing interest rates.

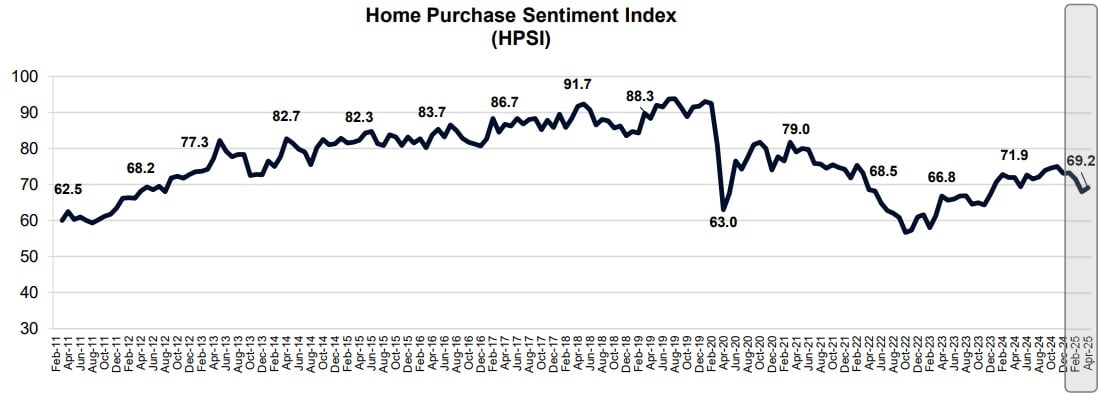

Fannie Mae’s latest monthly National Housing Survey, which polled 1,181 household decision makers between April 1 and April 18, found consumer sentiment toward housing was up slightly from March to April.

At 69.2, Fannie Mae’s Home Purchase Sentiment Index (HPSI) was up 1.1 points from March but down nearly three points from a year ago.

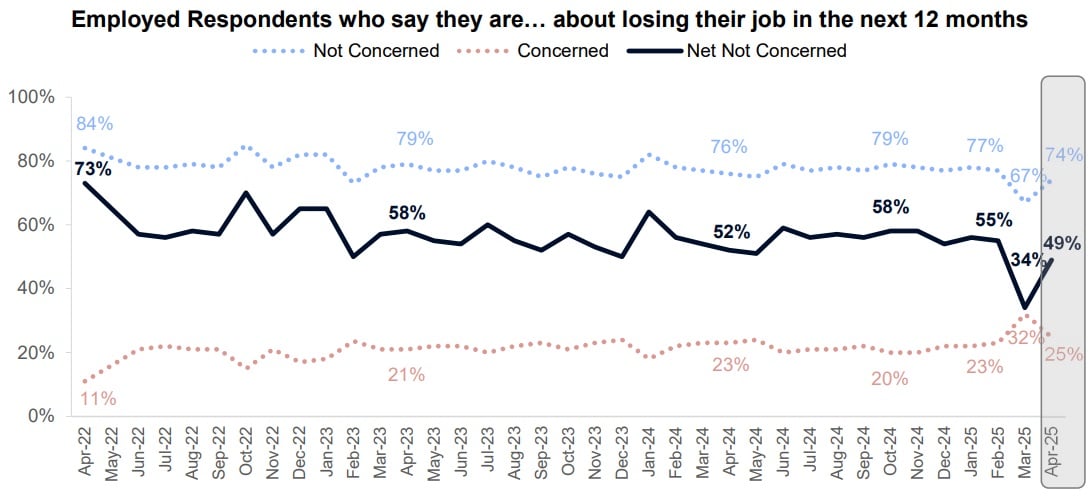

Three of the index’s six components improved: Americans were less concerned about losing their jobs than in March, more had seen their incomes increase, and more expected home prices to increase in the next year.

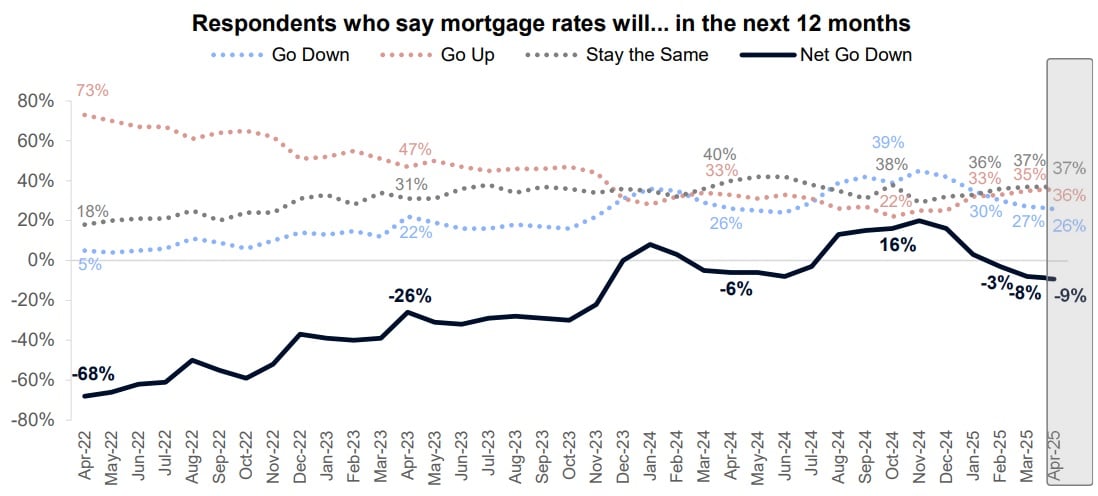

But consumers were more pessimistic about selling conditions and the prospect for mortgage rates to come down in the year ahead.

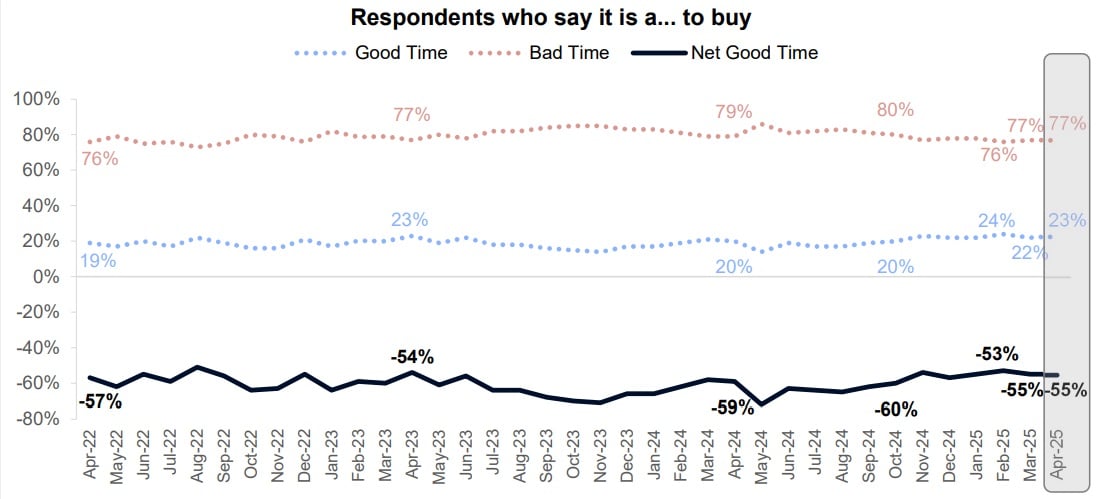

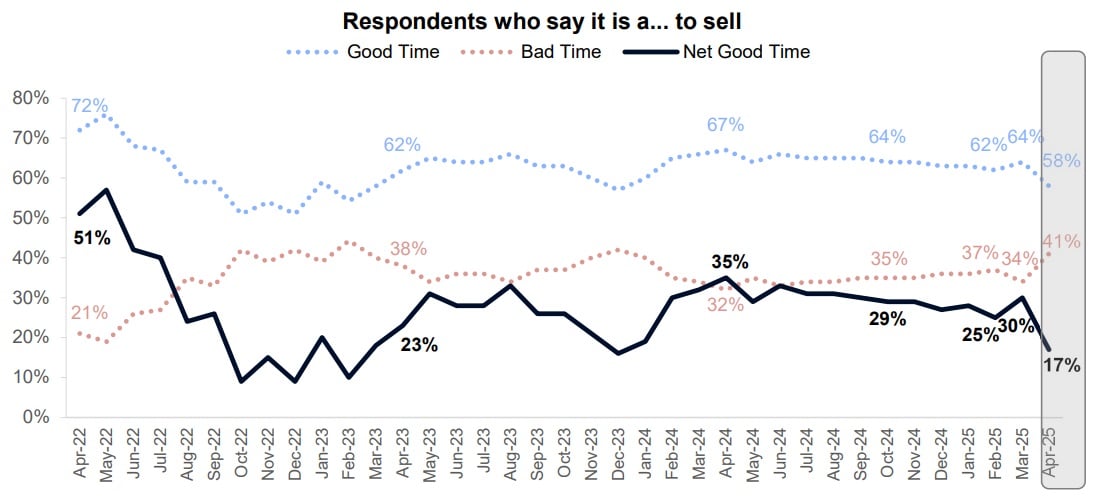

Only 23 percent of Americans surveyed in April said it was a good time to buy, but that was up from 22 percent in March. The share who said it was a bad time to buy (77 percent) remained unchanged.

The share of consumers who say they would buy a home if they were going to move was unchanged at 65 percent.

The share who said they would rent if they were going to move increased one percentage point from March to April, to 35 percent.

The percentage of household decision makers who said it was a good time to sell fell from 64 percent in March to 58 percent in April.

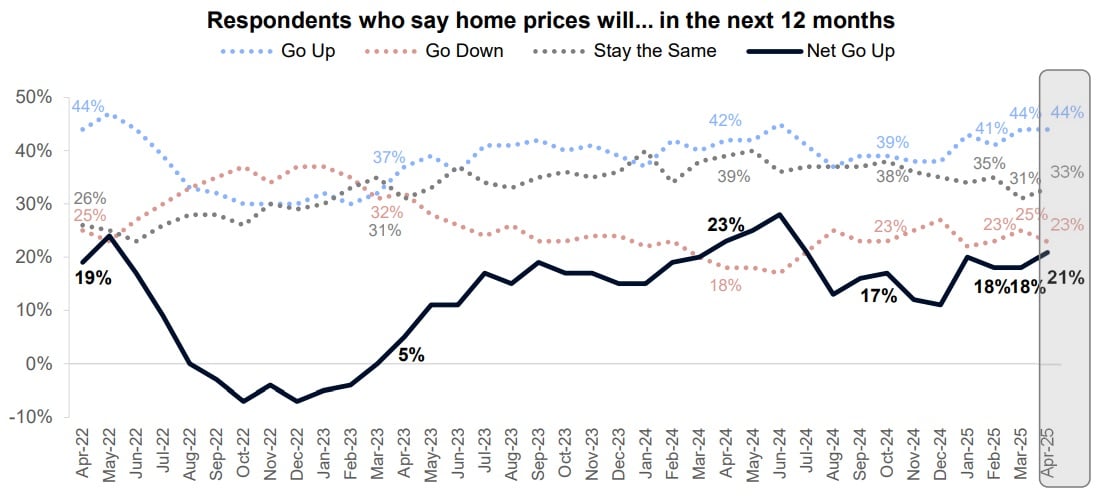

Only 23 percent of Americans surveyed in April thought home prices would go down in the next 12 months, compared to 25 percent in March.

While that would be bad news for would-be bargain hunters, it’s viewed as a positive for the HPSI as it reflects consumer confidence that housing markets aren’t on the verge of crashing.

About one in four households surveyed in April (26 percent) expect mortgage rates will come down in the next 12 months, about the same as March (27 percent) but down sharply from November, when 45 percent were expecting lower rates in the year ahead.

Only one in four employed Americans (25 percent) said they were concerned about losing their job in April, down from a spike in March to 32 percent.

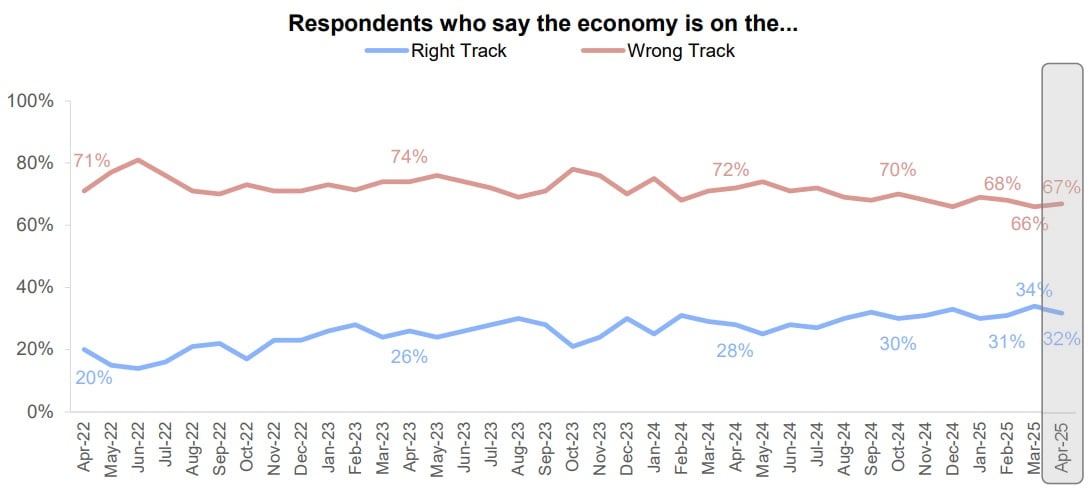

While not factored into the HPSI, only one in three households (32 percent) thought the economy was on the right track in April, down from 34 percent in March but up from 28 percent a year ago.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 16, 2025 | Industry, News Feed

Lawsuit seeks class action status to represent Redfin shareholders, claiming they need more information about financial advisor’s potential conflict of interest before June 4 merger vote.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Rocket Companies’ deal to acquire real estate brokerage Redfin has run into a potential snag in the form of a lawsuit filed on behalf of Redfin shareholders claiming they should be provided with more information on a potential conflict of interest on the part of the deal’s financial advisor.

The lawsuit seeks a court order preventing Redfin shareholders from voting on the merger until they’ve received more details on Redfin deal advisor Goldman Sachs’ dual role as a lender to Rocket.

Redfin shareholders are currently scheduled to vote on the deal on June 4. The window for antitrust regulators to weigh in with questions or objections to the deal closed on May 8. Reporting earnings that day, Rocket executives said they expected to close the deal as soon as this quarter, which ends June 30.

Attorneys representing Redfin shareholder Jason Morano filed a lawsuit the next day, seeking class action certification to represent shareholders they claim were left in the dark by a “materially incomplete and misleading” deal proxy statement.

The May 9 complaint seeks more information on the nature of the lending relationship between Goldman Sachs and Rocket, and how much Rocket has paid Goldman over the last two years.

Redfin’s deal advisor is the investment bank Goldman Sachs & Co. LLC. A Rocket SEC filing shows that Goldman Sachs Bank USA is one of several banks providing its subsidiary, Rocket Mortgage, with access to a $1.15 billion revolving credit facility.

Redfin’s May 5 proxy statement — a prospectus explaining the background and terms of the deal to investors — does disclose that “Goldman Sachs Investment Banking has an existing lending relationship with Rocket and/or its subsidiaries.”

But attorneys for Morano argue that disclosure is vague and lacks details that should have been provided to Redfin shareholders — such as how much of the $1.15 billion credit facility is provided by Goldman Sachs, and how much Rocket has paid the bank in interest and fees.

The lawsuit also seeks “key inputs” used to prepare a discounted cash flow analysis (DCF) used to support the valuation of Redfin and the board’s recommendation that shareholders approve the merger.

(Although structured as a merger, Redfin will be a wholly owned subsidiary of Rocket if the deal goes through.)

Rocket and Redfin did not respond to Inman’s requests for comment on the lawsuit.

Law firms often get involved in big mergers and acquisitions, sometimes winning settlements or better terms for shareholders.

Since Rocket announced its plans to acquire Redfin, at least seven law firms have publicized that they’re investigating the terms of the deal on behalf of Redfin shareholders: Halper Sadeh LLC; Ademi & Fruchter LLP; Kahn Swick & Foti LLC; Johnson Fistel LLP; Rowley Law PLLC; Brodsky & Smith and Monteverde & Associates PC.

Morano, who certified to the court that he owns 25 shares in Redfin purchased in March 2020, was previously the plaintiff in an unrelated 2022 lawsuit challenging Take-Two Interactive Software’s $12.7 billion acquisition of mobile games platform Zynga.

Attorneys for Morano urged the Seattle-based U.S. District Court, for the Western District of Washington to expedite the case by requiring opposition to their motion to be filed by May 14, and for a decision by May 15.

“With the shareholder vote a mere four weeks away, good cause and exigent circumstances exist warranting an order granting plaintiff’s requested relief of a shortened briefing schedule and an expedited hearing on plaintiff’s forthcoming motion for a preliminary injunction,” they said in a May 9 motion.

But Judge Richard A. Jones recused himself from the case on Thursday without holding a hearing, reassigning it to Judge Marsha J. Pechman.

Redfin recounts the long road to the deal

Challenges to mergers and acquisitions often seek to demonstrate that the company being acquired has been undervalued.

Redfin’s deal prospectus revealed that it has been in talks to be acquired since 2022, signing a non-disclosure agreement with Rocket in 2022 and with two other potential suitors in 2023.

Rocket submitted a non-binding proposal on Jan. 16 to acquire Rocket at an implied value of $10.45 per share — a 35 percent premium at the time.

Redfin’s board decided to hold out for a better offer, and on Jan. 30 entered into a confidentiality agreement with a fourth company interested in acquiring the brokerage.

Rocket upped its offer in an all-stock deal that valued Redfin at $12.50 per share, and a deal was signed on March 9.

In voting to approve the deal — and recommending that shareholders do the same — the board noted that Redfin had $812 billion in debt coming due over the next three years, including $74 million in October.

Redfin “had engaged in discussions with three other strategic parties that the Redfin board believed were most likely to have an interest in an acquisition of Redfin and would have the ability to consummate a transaction of this size and nature,” the prospectus stated. “No potentially interested counterparty other than Rocket submitted an offer.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site