by Matt Carter | May 14, 2025 | Industry, News Feed

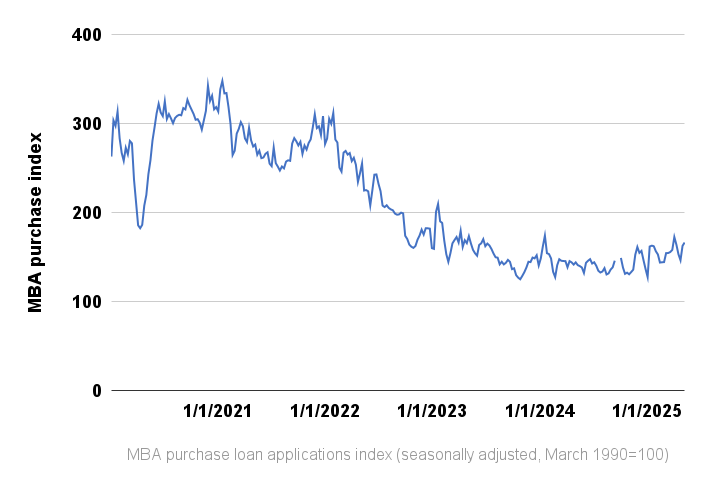

With more homes to choose from, purchase loan applications were up 18 percent from a year ago last week as buyers forged ahead despite economic uncertainty.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Homebuyers came out in force again last week as mortgage rates found some stability, with demand for purchase loans climbing for the second week in a row, according to a weekly survey of lenders by the Mortgage Bankers Association.

The MBA’s Weekly Mortgage Applications Survey showed purchase loan applications were up by a seasonally adjusted 2 percent last week when compared to the week before, and up 18 percent from a year ago.

“Last week saw steadier mortgage rates, as the [Federal Reserve] meeting played as predicted, and market movements led to a small two-basis point increase in the 30-year conforming rate to 6.86 percent,” MBA Chief Economist Mike Fratantoni said in a statement.

While refi applications were essentially unchanged from the week before, falling by 0.4 percent, requests to refinance were up 44 percent from a year ago.

Mike Fratantoni

“The news for the week was the growth in purchase applications,” Fratantoni said. “Despite the economic uncertainty, the increase in home inventory means there are additional properties to buy, unlike the last two years, and this supply is supporting more transactions.”

Nationwide, there were 31 percent more homes for sale in April than there were a year ago, according to Realtor.com data. The 959,251 active for-sale listings that homebuyers had to choose from last month surpassed April 2020 levels, marking a new post-pandemic high.

Federal Reserve policymakers let a key short-term interest rate stand last week and are no longer expected to start cutting rates in June due to uncertainties over the Trump administration’s future moves on tariffs, immigration, taxation and regulation.

Administration officials have rolled out new or revised tariff policies 55 times this year, according to a tariff tracker maintained by the law firm Reed Smith.

The Trump administration on Monday announced a 90-day pause on a “reciprocal tariff” on goods from China announced April 2, reducing the effective tariffs on many Chinese imports from 145 percent to 30 percent.

The news sent stock markets and mortgage rates higher, with investors less fearful of a recession but still wary of inflation.

Monday’s reduction of tariffs on Chinese imports, and a trade deal with the United Kingdom, leaves the overall average effective tariff rate on U.S. imports at 17.8 percent — the highest since 1934, according to an analysis by The Budget Lab at Yale.

The Consumer Price Index for April, released Tuesday, showed prices were up 2.3 percent from a year ago last month — closer to the Fed’s 2 percent goal than the 3 percent annual inflation registered in January.

Inflation headed in the right direction

But the April CPI report contained “early signs of tariffs pushing up goods prices, with much more to come,” forecasters at Pantheon Macroeconomics warned in their May 14 U.S. Economic Monitor.

The economic policy uncertainty generated by tariffs and a drop in consumer confidence “is forcing providers of discretionary services to reduce prices,” Pantheon economists noted. “The upward impact on inflation from the tariffs will build rapidly over the coming months, but we continue to think that services inflation will cool, providing some offset and enabling the Fed to ease policy in the second half of this year.”

The Federal Reserve’s preferred inflation gauge — the Personal Consumption Expenditures (PCE) Price Index — showed annual inflation falling from 2.7 percent in February to 2.3 percent in March. The PCE Price Index for April will be released May 30.

Futures markets tracked by the CME FedWatch tool show investors don’t expect the Fed to resume rate cuts until Sept. 17.

Mortgage rates stabilize

Rates on 30-year fixed-rate conforming mortgages have been edging up this month, but at 6.81 percent on Tuesday were still 20 basis points lower than a 2025 high of 7.05 percent registered on Jan. 14, according to rate lock data tracked by Optimal Blue.

Optimal Blue data shows rates on 30-year fixed-rate loans hit a 2025 low of 6.48 percent on April 4. Fannie Mae forecasters said last month they expect mortgage rates to come down to 6.2 percent by the end of this year and to 6 percent next year.

Purchase mortgage demand rises

At 166.5 as of May 9, the MBA’s seasonally adjusted purchase index showed homebuyer demand for mortgages was up 30 percent from a 2025 low of 127.7 registered on Jan. 3. The index was benchmarked at 100 in March 1990. Applications for purchase loans had previously picked up 11 percent during the week ending May 2.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 13, 2025 | Industry, News Feed

New Elevate program providing “concierge-level services” to agents is off to such a strong start that Fathom will temporarily suspend guidance while it reworks 2025 forecast.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Fathom Realty’s parent company trimmed its first quarter net loss to $5.6 million as growing agent and transaction count helped boost revenue by 32 percent from a year ago, to $93.1 million.

But the 5 percent decrease in Fathom Holdings Inc.’s net loss was “primarily due to a reduction in agent recruiting commissions,” the company said in reporting earnings Tuesday.

Fathom Realty’s agent network grew by 23 percent in the first three months of the year, to 14,715, and transactions were up 26 percent from a year ago, to 9,715.

Company executives said they expect to be profitable in Q2 by one metric — adjusted earnings before interest, taxes, depreciation and amortization (EBITDA).

“Although we expect 2025 to remain challenging for the real estate industry, we expect Fathom’s positive momentum to continue,” Fathom CEO Marco Fregenal said in a statement. “We are, in fact, currently expecting to be EBITDA positive in Q2 of 2025.”

Fathom’s adjusted EBITDA loss of $1.47 million in the first quarter was a slight improvement from $1.52 million a year ago.

Shares in Fathom Holdings, which in the last 12 months have traded for as little as 65 cents and as much as $3.37, gained 9 percent Tuesday before earnings were released, to 96 cents.

Fregenal said Fathom’s mission remains building “a best-in-class, technology-driven platform that empowers agents, streamlines transactions and delivers long-term value for our shareholders.”

Last month Fathom announced the Elevate program — an addition to Fathom Realty’s existing commission plans, offering a higher level of brokerage services in exchange for what the company considers to be a low split.

Fathom Realty, whose flat-fee and revenue-sharing commission models have helped the company grow its agent count, now offers agents the option of paying a 20 percent commission split in exchange for “concierge-level services,” including dedicated marketing support and lead generation.

Fregenal said the goal is to “ramp up the program to 100 new agents per month by Q4 of 2025.”

The Elevate program is off to such a strong start that Fathom “has elected to temporarily suspend guidance while it works with its newly formed strategy committee of the board of directors” to forecast 2025.

“We believe Elevate will enhance agent growth by helping agents increase their business as they become more productive,” Fregenal said. “More importantly, we anticipate the program will significantly enhance long-term profitability by increasing gross profit per transaction.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 13, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The Appraisal Institute, a professional association of real estate appraisers, is in turmoil following allegations that a top executive sexually harassed employees and that the association has been knowingly reporting inaccurate exam scores to state agencies.

Alissa Akins, the Appraisal Institute’s former director of education and publications, sued the association on March 28, alleging she was fired from her job in December in retaliation for exposing problems with the administration of licensing exams used by state regulators.

One of the Appraisal Institute staffers Akins accused of retaliating against her — Vice President Craig Steinley — is named in a May 8 wrongful termination lawsuit filed by former Appraisal Institute CEO Cynthia Chance, who accused Steinley of groping her and making lewd comments about her.

The Appraisal Institute “categorically and whole-heartedly denies that it has at any time engaged in fraudulent or retaliatory conduct,” in its administration of licensing exams or in its dealings with Akins.

Steinley’s attorney told The New York Times that he “wholly denies any allegations of any unwanted touching or harassment. It simply did not occur.”

The New York Times‘ Debra Kamin — whose 2023 exposé of allegations of sexual harassment at the National Association of Realtors led to the resignation of NAR President Kenny Parcell — last week published details from interviews with 12 women “who said they have had uncomfortable interactions with Mr. Steinley.”

Kamin, who interviewed more than 20 appraisers and former Appraisal Institute staff members, obtained a confidential legal settlement in which the association paid $412,000 to settle a sexual harassment claim by former Chief Financial Officer Beata Swacha.

The Appraisal Institute has “fielded similar complaints from at least seven other women that have swirled within the group over the last decade,” Kamin reported.

After The New York Times story went live, more than 200 people signed a Change.org petition “urging the board of directors to take immediate action to remove Craig Steinley from his position.”

On Monday, Appraisal Institute President Paula Konikoff posted on LinkedIn that Steinley had “decided to step away from his public [Appraisal Institute] officer appearances, effective immediately.”

Steinley informed the board that he was acting “out of consideration for and in the interest of not being a distraction to the important and ongoing work of the organization and will cooperate with any investigatory effort.”

Steinley’s attorney, Craig Capilla, told Kamin Monday that Steinley “has not resigned. This is still an ongoing issue. I don’t think final decisions have been made.”

The Appraisal Institute did not respond to Inman’s request for comment on the allegations against it, nor on Steinley’s current employment status. A statement by Konikoff on the allegations detailed by The New York Times features prominently on the association’s homepage.

Konikoff’s statement formally acknowledges “those who participated in the article and the seriousness of what they said.”

“Let me be clear: The Appraisal Institute is committed to a safe and respectful environment for all our employees and members, and nothing short of that is OK,” Konikoff wrote. “We have policies that prohibit — and are there to ensure — we promptly address any reports of discrimination, harassment or retaliation.”

The Appraisal Institute maintains that allegations it ignored Akins’ warnings about its examination processes or retaliated against her “are not true, and we will fight this lawsuit in court.”

In her March 28 complaint, Akins said that after being hired in February 2024, she discovered that due to inconsistent updates of minimum passing scores that vary by state, the Appraisal Institute had in some years mistakenly passed students who failed, and in other years failed students who passed.

A rescoring of a random sample of 300 Appraisal Institute exams found at least 17 percent had been scored incorrectly — raising the possibility that hundreds of people were wrongly certified as appraisers — or were told they’d flunked exams they’d actually passed, Kamin reported.

The Appraisal Institute “knowingly reporting inaccurate exam scores to state agencies” as far back as 2020, Akins’ suit alleged.

When Akins discovered the issue and put forward a plan to correct it, the Appraisal Institute “refused to take action or make any of the suggested improvements,” her lawsuit claims. So Akins “demanded that her signature be removed from the certificates evidencing successful completion of a course, including passing the course exam.”

Akins claims in her suit that she was told if she did not resign, Steinley “will make it hell for you as long as you stay” and that she was fired when she refused.

In seeking to dismiss Akins’ lawsuit in a May 2 filing, attorneys for the Appraisal Institute said her complaint “fails to state any claim upon which relief may be granted,” and that even if proven, her allegations “are inadequate to allege fraud.”

Tackling appraisal bias

Increasing diversity in the appraisal profession is one of the goals the Biden administration outlined in launching an initiative to combat appraisal bias in 2022.

The initiative was sparked in part by media reports of Black families receiving higher appraisal values after removing indications of their race, and evidence of a wealth gap created in part by a history of bias in home appraisals.

As the Appraisal Institute’s president in 2023, Steinley testified at a public hearing that bias in real estate appraisal “can be unintentional. To mitigate bias, appraisers should be aware of the potential for bias and base opinions on rigorous analysis and research. Best practice relies on multiple data sources and techniques to enhance credibility of the opinion of value.”

The Appraisal Institute has participated in an Appraiser Diversity Initiative with Fannie Mae, Freddie Mac, and the National Urban League, and offers scholarships, workshops and other resources to those interested in becoming appraisers.

But under the leadership of Trump appointee Bill Pulte, Fannie and Freddie have been told to discontinue Equitable Housing Finance Plans that included initiatives to combat appraisal bias and promote greater diversity in the appraisal field.

Last year, The Appraisal Foundation, which is responsible for setting standards and qualifications for real estate appraisers, reached an agreement with the Department of Housing and Urban Development aimed at opening up the field to more Black people and people of color.

While HUD officials called the agreement “groundbreaking” and “historic,” The Appraisal Foundation emphasized that it had already undertaken more than a dozen steps outlined in the agreement.

In March, under the leadership of Trump appointee Scott Turner, HUD informed FHA lenders that they’ll no longer be required to follow procedures enacted last year to better protect borrowers against discriminatory appraisals.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 13, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The Trump administration will withdraw its nomination of attorney Jonathan McKernan to head the Consumer Financial Protection Bureau, as CFPB acting director Russell Vought presses forward with what Democratic lawmakers claim are efforts to dismantle the bureau.

In the latest development, Vought on Monday rescinded dozens of CFPB policy and regulatory guidance documents dating back to 2011 — including some issued during the first Trump administration — on topics including disclosure of consumer complaint data, fair lending, overdraft fees and mortgage loan servicing.

In notice published in the Federal Register on Monday, the CFPB outlined 67 guidance documents to be withdrawn pending further review, including eight policy statements, seven interpretive rules, 13 advisory opinions and 39 circulars and bulletins.

In some cases, the CFPB now claims its guidance relied on interpretations that were inconsistent with lawmakers’ intentions, or imposed compliance burdens without providing opportunities for notice and comment.

But even in cases where the bureau’s guidance is consistent with the law and provided opportunities for the public to weigh in, it’s now the bureau’s policy “to avoid issuing guidance except where necessary and where compliance burdens would be reduced rather than increased.”

While Monday’s recissions are not necessarily final — the bureau “will continue reviewing all guidance documents to determine whether they should ultimately be retained” — they won’t be enforced while the review is ongoing.

“Americans deserve an open and fair regulatory process that imposes new obligations on the public only when consistent with applicable law and after an agency follows appropriate procedures,” the CFPB said in a notice signed by Vought.

The American Bankers Association (ABA) welcomed the move, saying the CFPB has sometimes been too casual about issuing guidance that should have been subject to the more formal rulemaking process.

“While banks welcome guidance that helps them understand and comply with the law, too often in the past the CFPB has characterized something as guidance that is actually a rule Congress requires to go through the notice-and-comment process,” ABA President and CEO Rob Nichols said in a statement. “In the most egregious cases, the guidance announces expectations that exceed the CFPB’s statutory authority.”

As director of the White House Office of Management and Budget (OMB), Vought is leading the Trump administration’s efforts to downsize the CFPB.

With Elon Musk expected to step away from his unofficial role in running the Department of Government Efficiency (DOGE), it will be up to Vought to “lock in” many of DOGE’s cost-cutting efforts throughout the federal government, through avenues including the 2025 budget, eliminating job protections for high-level federal workers, and impounding funds appropriated by Congress, The Wall Street Journal reported Sunday.

Last month, U.S. District Judge Amy Berman Jackson put a temporary hold on the Trump administration’s move to fire all but 200 of the CFPB’s 1,700 employees, saying she has yet to weigh the merits of a lawsuit challenging the legality of dismantling the bureau.

Attorneys representing the CFPB’s union employees claimed that a DOGE employee who managed the bureau’s “reduction in force” (RIF) team failed to properly prepare a particularized assessment of why the employees it intends to fire are not needed to perform duties mandated by Congress.

That employee, a 25-year-old software engineer assigned to the CFPB in March, owns shares in a number of companies that are regulated by the bureau and was warned by ethics lawyers not to participate in any actions that could benefit him personally, ProPublica reported last week. Neither the employee or the CFPB responded to ProPublica’s requests for comment.

With oral arguments on the CFPB’s appeal of Berman’s order scheduled to be heard on May 16, more than 200 House and Senate Democrats signed an amicus brief Friday urging that Berman’s Jackson’s order be upheld.

“Without an act of Congress abolishing the CFPB or authorizing the President to do so, [Vought has] no power to shutter the bureau,” Democratic lawmakers said.

More than two dozen state attorneys general have signed a similar amicus brief.

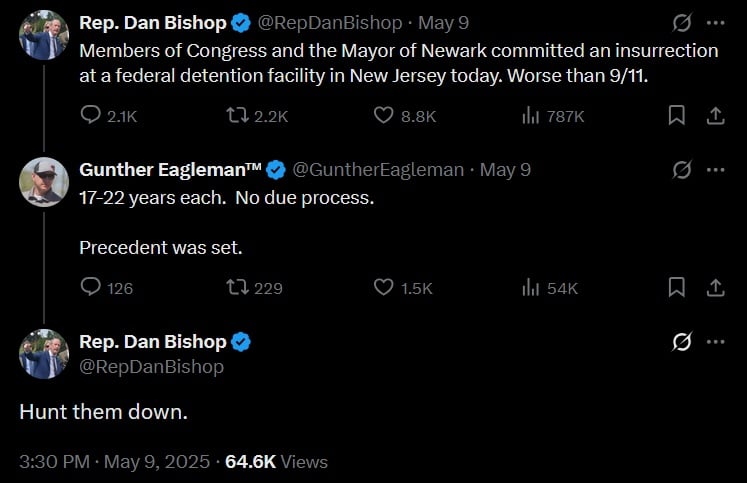

Three of the lawmakers who signed the amicus brief — Representatives Bonnie Watson Coleman, Rob Menendez and LaMonica McIver — made headlines Friday after inspecting an Immigration and Customs Enforcement (ICE) facility in Newark, New Jersey.

While the lawmakers said they were exercising their right to conduct a congressional oversight visit of the newly-opened, privately operated immigration detention facility, the visit generated controversy when Newark Mayor Ras Baraka was arrested on trespassing charges.

On Friday, Vought’s top deputy at the OMB, Dan Bishop, suggested that those lawmakers and Baraka had “committed an insurrection” and urged law enforcement to “Hunt them down.”

Source: May 9, 2025 post by OMB Deputy Director Dan Bishop on the social media platform X.

Baraka told the New York Times that a security guard allowed him to enter the property through a locked gate, but said he was not allowed inside the facility while the three House Democrats were touring it.

“If I was on that property, I was invited there,” Baraka told the Times.

When the three Democratic lawmakers emerged, Baraka was arrested in what the Times described as “a brief but volatile clash that involved a team of masked federal agents wearing military fatigues and the three lawmakers.”

A spokeswoman for the Department of Homeland Security told CNN that members of Congress who were at the scene could face charges for “assaulting our ICE enforcement officers.”

Watson Coleman rejected the DHS’s claim in a press release that she and Menendez, “stormed the gate and broke into the detention facility.”

“The author of that press release was so unfamiliar with the facts on the ground that they didn’t even correctly count the number of Representatives present,” Watson Coleman told CNN.

With the fate of the CFPB apparently up to be determined in court, the Trump administration’s pick to lead the bureau, Jonathan McKernan, is set to be nominated to serve in a different role — undersecretary of domestic finance at the Treasury Department.

McKernan’s nomination to lead the CFPB was endorsed on March 6 by the Senate Banking Committee in a 13-11 party line vote, but had not yet been voted on by the full Senate.

In the meantime, the former FDIC board member has has been working as an advisor at the Treasury Department, where he has become “an integral part” of Treasury Secretary Scott Bessent’s senior team.

“His continued service at Treasury will ensure that his experience and expertise are best put to advancing the President’s America First agenda,” the Treasury Department said in a press release Friday.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 13, 2025 | News Feed

How Title Companies Help Protect Your Purchase

Buying a home in Texas is exciting, but it also comes with a lot of moving pieces—paperwork, deadlines, money transfers, and legal ownership details that most buyers never see. That behind-the-scenes work is exactly where a title company earns its keep. From verifying the seller’s legal right to transfer the property to coordinating the closing process, the title company role is to help make sure you get clear, marketable ownership—and that your funds and documents are handled correctly.

Just as important, title insurance helps protect you from certain past problems tied to the property’s ownership history. In a state as large and diverse as Texas—where homes may sit on land with decades of records, multiple owners, mineral interests, and old liens—title work isn’t just a formality. It’s a key layer of protection for one of the biggest purchases most people will ever make.

What a Title Company Does (and Why It Matters in Texas)

In Texas, title companies play a central role in real estate closings. While practices vary by region, many Texas transactions use a title company to research the property’s title, issue title insurance, and facilitate the closing process by coordinating documents, funds, and recording.

The core title company role in a typical transaction

- Title search and examination: Reviewing public records to confirm the chain of ownership and identify issues like liens, judgments, unpaid property taxes, or ownership disputes.

- Clearing “clouds” on title: Working with the seller, lenders, attorneys (when involved), and county offices to resolve problems before closing.

- Escrow and settlement services: Holding earnest money and closing funds, preparing the settlement statement, and disbursing proceeds at closing.

- Coordinating signing: Managing the final signing appointment and ensuring all documents are executed correctly.

- Recording: Filing the deed and any lender documents with the county to make the transfer official in public records.

Texas has 254 counties, and recording systems, turnaround times, and local customs can vary. A detail-oriented title team helps keep everything aligned so you don’t get surprised right before closing day.

Step-by-Step: How the Closing Process Works with a Title Company

For first-time buyers, closing can feel like a blur of initials and wire instructions. Here’s a simplified look at how the closing process commonly unfolds in Texas when a title company is involved. Your exact timeline may shift based on lender requirements, inspection negotiations, or appraisal timing.

Step 1: Open title and order the title search

Once the contract is executed, the title company “opens” the order and begins researching the property. They’ll pull records from county offices and other databases to verify ownership and uncover issues that must be addressed before the property can be transferred.

Step 2: Earnest money is deposited

In many Texas contracts, the buyer submits earnest money within a short period after signing. The title company typically holds these funds in escrow until closing (or until the contract is terminated under the terms of the agreement).

Step 3: Review the title commitment

The title company issues a title commitment, which is essentially a promise to issue title insurance—provided certain requirements are met. It lists:

- Who currently owns the property

- Requirements to close (for example: payoff an existing mortgage, release a lien, correct a name mismatch)

- Exceptions (items that will remain on title, such as recorded easements or HOA restrictions)

Green flag: Requirements are clear and solvable, and exceptions match what you’d expect for the neighborhood (like typical utility easements).

Red flag: Unreleased liens, unclear ownership, missing probate documentation, or exceptions that don’t fit the property (for example, an easement that appears to cut through the middle of the lot).

Step 4: Coordinate lender conditions (if financing)

If you’re using a mortgage, your lender will send closing instructions and loan documents to the title company. The title company then helps coordinate the signing, confirms funding requirements, and ensures the lender’s lien is properly recorded after closing.

Step 5: Final numbers and signing appointment

As closing approaches, the title company prepares the settlement statement (often called the Closing Disclosure for buyer-side lender transactions). This document summarizes purchase price, closing costs, prorations (like property taxes), and who pays what.

At the signing, you’ll typically sign the deed paperwork (seller) and loan documents (buyer, if financed). Texas closings may happen in person, and in some cases with remote notarization depending on the parties and documentation.

Step 6: Funding and recording

After documents are signed and the lender releases funds (if applicable), the title company disburses money to the seller, pays off liens, pays agents, and records the deed with the county. Recording is the final step that makes the ownership change official in public records.

What Is Title Insurance, and Why Do Buyers Need It?

Title insurance protects against certain problems connected to the property’s title—often issues that happened in the past and may not be obvious during a standard home inspection. Unlike homeowners insurance (which protects against future events like fire or storm damage), title insurance focuses on past events that could affect your legal ownership.

In Texas, the cost of title insurance is regulated, meaning the basic premium is set by the state. You can still comparison shop for service, communication, and fees for other line items, but the core title insurance rate is standardized.

Common issues title insurance can help cover

- Forged or fraudulent documents in the chain of title

- Undisclosed heirs or ownership claims that surface after closing

- Errors in public records or recording mistakes

- Liens not properly released (for example, an old payoff that never got recorded as satisfied)

- Clerical mistakes that affect ownership, such as misspelled names or incorrect legal descriptions

Title insurance doesn’t replace due diligence, and it doesn’t cover every scenario. But it can be a powerful backstop for risks that are hard for an average buyer to detect.

Owner’s Policy vs. Lender’s Policy: What’s the Difference?

When people hear “title insurance,” they often assume it automatically protects them. In reality, there are two main policies, and they protect different parties.

Lender’s title insurance

If you take out a mortgage, your lender will require a lender’s policy. This protects the lender’s financial interest in the property up to the loan amount. It does not fully protect the buyer’s equity.

Owner’s title insurance

An owner’s policy protects you, the buyer, and your ownership rights—typically up to the purchase price. It’s usually a one-time premium paid at closing, and it stays in effect as long as you or your heirs have an interest in the property.

Quick pros and cons for buyers

- Owner’s policy pros: Protects your ownership claim, can cover legal defense costs for covered claims, provides long-term peace of mind.

- Owner’s policy cons: Adds to upfront closing costs, and coverage is subject to the policy’s terms, exclusions, and exceptions.

For many Texas buyers, the owner’s policy is a common and practical safeguard—especially in fast-moving markets where you may not have much time to investigate deeper history beyond the standard contract timelines.

Texas-Specific Title Issues Buyers Should Understand

Every state has its quirks. In Texas, a few recurring themes come up often enough that buyers should know what to watch for when reviewing the title commitment and survey.

Property tax prorations and exemptions

Texas property taxes are a major component of monthly housing costs, and tax bills can change when a home sells—especially if the prior owner had a homestead exemption or other exemptions. The title company helps prorate taxes between buyer and seller at closing based on the contract terms, but your future bill may still rise if exemptions reset or valuations change.

Tip: Ask your agent or lender to walk you through estimated taxes with and without exemptions so you can budget realistically.

HOAs and deed restrictions

Many Texas neighborhoods—especially in metro areas like Dallas-Fort Worth, Houston, Austin, San Antonio, and growing suburbs—have HOA requirements and recorded restrictions. Title commitments often list these as exceptions. They aren’t necessarily “bad,” but you should understand what they allow and prohibit before closing.

Easements and access rights

Utility easements are common and usually expected. But larger easements (drainage, shared driveways, access paths) can affect how you use the yard or whether you can build additions. Reviewing the survey alongside the title commitment helps connect the paperwork to the real-world property.

Mineral rights and prior reservations

In parts of Texas, mineral rights may have been severed from surface ownership long ago. Title work may show prior reservations or exceptions related to minerals. This doesn’t always impact day-to-day living, but it’s worth understanding because it can affect future use and, in some cases, surface access rights depending on what’s recorded.

How to Read a Title Commitment Without Feeling Overwhelmed

A title commitment can look intimidating, but you don’t have to be a lawyer to ask smart questions. Focus on three sections: ownership, requirements, and exceptions.

What to look for

- Names: Do the owner names match the contract? Are there multiple owners who must sign?

- Requirements: Are there liens to be paid off? Missing releases? Probate steps?

- Exceptions: Are there easements, restrictions, or boundary items that could affect your plans?

Common mistake: Ignoring the exceptions section. Many buyers sign and move on, only to learn later that a utility easement limits where they can put a pool or addition.

Green flag: The title officer or closer is willing to explain what each item means in plain language and tells you which items are routine versus unusual.

Choosing a Title Company in Texas: Practical Tips

In Texas, the title insurance premium itself is set, so the difference often comes down to service quality, responsiveness, and how smoothly the closing process is managed.

Questions to ask

- How quickly do you issue the title commitment after the order is opened?

- Who will be my day-to-day contact, and how do you communicate updates?

- How do you handle wire verification and fraud prevention?

- Can you explain fees beyond the title insurance premium (settlement, courier, recording, HOA docs, etc.)?

Red flags

- Slow responses as deadlines approach

- Unclear wiring instructions or last-minute changes without verification steps

- Fee estimates that change dramatically without explanation

Green flags

- Clear timelines, proactive updates, and easy-to-read statements

- Strong security practices for funds transfer

- Willingness to coordinate smoothly with your lender, agent, and any attorneys involved

Bottom Line: Title Work Is Quiet Protection You’ll Be Glad You Have

Most homebuyers won’t think about the title company role once the keys are in hand—and that’s often a sign that everything went right. But the work happening behind the scenes matters: confirming ownership, resolving liens, coordinating escrow, and guiding the closing process so your purchase is properly recorded.

Just as importantly, title insurance is a long-term safeguard against certain hidden risks in a property’s past. In a Texas market that can move quickly—especially during spring and early summer when buyer activity typically rises—having a dependable title team and the right coverage can help you close with confidence and protect what you’re building.