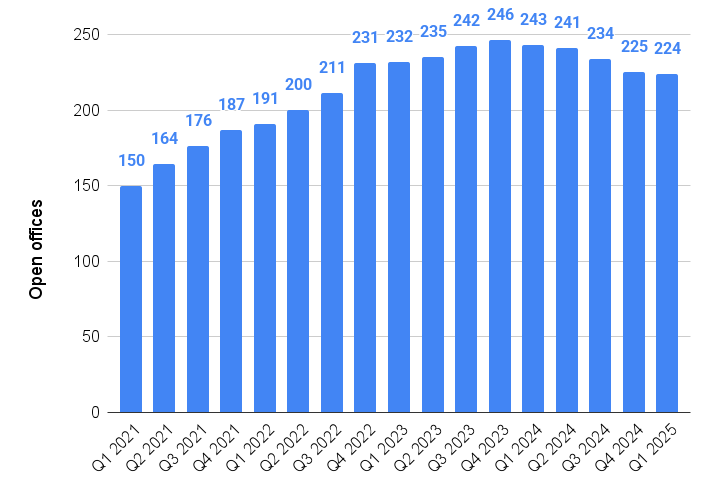

Since peaking at 246 offices in Q4 2023, RE/MAX’s mortgage franchising business has experienced declines for five consecutive quarters.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

New Motto Mortgage offices in Texas, Florida and Missouri could help RE/MAX’s mortgage franchising business get back into growth mode after five consecutive quarters of declining office counts.

Motto Mortgage DreamNest — already serving the metro Houston market and markets throughout Texas — will host a ribbon cutting ceremony Saturday, June 7, at its recently opened Cypress office.

Owner Frank Martin brings over 17 years of real estate construction and development experience to the new Motto Mortgage brokerage, where Christian Sanchez will serve as branch manager.

“We are thrilled to be open for business in Cypress, and we are looking forward to personally introducing ourselves to the community at our grand opening event,” Martin said in a statement Thursday. “Motto Mortgage DreamNest offers an advantageous alternative to the traditional mortgage bankers currently operating in the Greater Houston area.”

Motto Mortgage doesn’t make loans itself but provides technology, training and marketing tools to franchisors. Each Motto Mortgage franchise is independently owned, operated and licensed by mortgage brokers who work with multiple wholesale lenders to find the best deal for their clients.

After rapid growth during the pandemic — the number of open offices nearly doubled from 118 in Q1 2020 to 235 in Q2 2023 — Motto Mortgage’s open office count peaked at 246 in Q4 2023 and has been shrinking ever since.

Rising mortgage rates slowed the pace at which Motto Mortgage signs new franchise agreements, and some existing franchises have gone out of business or not been renewed. Franchisees sign seven-year agreements directly with Motto Franchising, and 2024 was the first full year Motto has had offices come up for renewal.

In reporting a $2 million net loss for the first quarter, parent company RE/MAX Holdings said there were 224 Motto Mortgage offices open as of March 31, down 8 percent from a year ago.

RE/MAX disclosed in its earnings report that it was providing short-term financial relief to 58 of those offices, which were “temporarily either not being billed and/or having associated revenue recognized.”

RE/MAX also provides third-party loan processing services to mortgage brokers through another subsidiary, wemlo, which it acquired in 2020.

Karri Callahan

“It’s obviously a tough environment for both the legacy Motto business as well as what we’re seeing in terms of the processing business from a wemlo perspective,” RE/MAX Holdings Chief Financial Officer Karri Callahan said on a May 2 call with investment analysts.

Callahan said the shrinking office count is the biggest driver in the decline in revenue generated by Motto Mortgage and wemlo, but “we really have seen some stabilization there on a sequential quarter basis, which is good to see.”

Company executives were also pleased with the engagement at last month’s Motto Mortgage Innovation and Loan Excellence (MILE) Summit in Orlando, which Callahan called “very, very positive.”

Nearly 300 awards were presented at the MILE Summit, including:

RE/MAX announced on March 31 that Motto Mortgage President and CEO Ward Morrison — who led the company during its explosive growth phase — is getting married and has decided to retire on June 15, but will continue to work for the company as a consultant for the rest of the year.

Erik Carlson

On the company’s earnings call, RE/MAX CEO Erik Carlson called Morrison “irreplaceable,” but said an active search is underway — internally and externally — for his successor.

“We have a great team in place at Motto and wemlo, and so that team is doing great things right now,” Carlson said. “Obviously, with the mortgage market, there’s a lot of great candidates out there. So we’ll look both within the walls and outside the walls, and we’ll have an announcement on that, I hope, before our next earnings call.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Promise that the government will maintain “implicit guarantees” of the companies’ obligations suggests that what Trump has in mind is monetization, not privatization.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

President Trump’s plans for mortgage giants Fannie Mae and Freddie Mac are generating more speculation following his promise that the government will maintain implicit guarantees of the companies’ obligations.

Like a similar post last week, Trump’s latest Truth Social post on “TAKING THESE AMAZING COMPANIES PUBLIC” initially sent shares in Fannie and Freddie soaring Wednesday morning.

That was before Trump’s pick to head Fannie and Freddie’s federal regulator, Bill Pulte, appeared on CNBC and poured some cold water on existing investors’ hopes of turning big profits on the deal.

“I would point you to his tweet,” Pulte said. “He very explicitly says that he wants to take them public. He did not say that he wants to privatize them.”

Fannie and Freddie have been in government conservatorship since 2008, when the government took a large stake in the companies to keep them afloat during the 2007-2009 housing crash and Great Recession.

While presidents including Barack Obama have made releasing Fannie and Freddie from conservatorship a goal, the two big questions have been:

How to restructure Fannie and Freddie without sending mortgage rates soaring

How to protect taxpayers if the companies run into trouble again

By providing assurances that the government will still provide implicit guarantees to Fannie and Freddie if they run into trouble again, Trump seemed to be addressing the first concern — that mortgage rates could go up if Fannie and Freddie were privatized.

Fannie and Freddie don’t make loans themselves, but provide guarantees to investors who buy mortgage-backed securities (MBS) that fund most U.S. home loans. Those guarantees mean investors are willing to accept yields that aren’t much better than what they’d get if they invested in 10-year Treasurys.

But if the government would still act as a backstop for the mortgage giants, it’s not clear how taxpayers would be any better protected than they are today.

“Interestingly, the President has not said anything that he wants to end conservatorship,” Pulte said. “We’re studying actually, potentially keeping it in conservatorship and taking it public.”

Fannie and Freddie are already publicly traded on an over-the-counter market. Investors who own the companies’ common stock — including billionaire Bill Ackman — are hoping the government will buy them out.

The government could invest its stake in Fannie and Freddie into a sovereign wealth fund, and raise cash by issuing preferred shares that pay dividends. That plan could also give MBS investors confidence that the U.S. stands behind the companies’ guarantees.

Pulte did not have a clear answer for CNBC’s Sara Eisen when she asked, “Why would you want to take the companies public? How does it help homeowners?”

Pulte did say that one reason Trump has more leeway to control Fannie and Freddie’s fate is a 2021 Supreme Court decision that expanded the president’s power to fire the mortgage giants’ regulator, the Federal Housing Finance Agency (FHFA), without cause.

After Trump appointed Pulte FHFA director in March, Pulte fired 14 members of Fannie and Freddie’s boards and appointed himself the chair of both companies’ boards.

“So President Trump now has control over Federal Housing Finance Agency as well as U.S. Treasury, and this opens up all kinds of ideas,” Pulte said. “So, whether the president decides to sell a small piece or what have you — that’s entirely up to the president. But I think the opportunities are endless.”

Peter Schiff, chief economist for Euro Pacific Asset Management, said that Trump’s assurance that the government’s implicit guarantees would remain in place amounts to an explicit promise.

“Of all the policy mistakes Trump has made as President, taking Fannie and Freddie public with explicit government guarantees would be the worst so far,” Schiff posted on X.

An explicit guarantee would allow Fannie and Freddie “to make as much money as possible by engaging in the most risky behavior possible, leaving the taxpayers left holding the bag when those risks inevitably result in another bankruptcy,” Schiff wrote. “Private profits and public losses are not capitalism. It’s the worst form of cronyism.”

Real estate industry groups like the National Association of Realtors and the Mortgage Bankers Association have proposed a “utility-style” model for Fannie and Freddie that would provide an explicit guarantee, but limit their risks and profits.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Mortgage giant Fannie Mae is turning to controversial Silicon Valley data analytics company Palantir Technologies to help it detect mortgage fraud, which the head of its federal regulator, Bill Pulte, claims is “rampant.”

Palantir’s “cutting edge AI technology” will help Fannie Mae find criminals who try to defraud it, increasing safety and soundness “by rooting out bad actors in our housing system,” Pulte said in announcing the partnership Wednesday.

As President Trump’s appointee to lead the Federal Housing Finance Agency (FHFA), Pulte last month sent a criminal referral letter to the U.S. Department of Justice suggesting that New York Attorney General Letitia James had made misrepresentations about two properties she owns in order to receive better loan terms.

James — who won a $486 million civil fraud judgment against Trump that is under appeal — has denied the allegations, calling them baseless.

As FHFA director, Pulte appointed himself the chair of both Fannie Mae and its sister company, Freddie Mac, in March and has been highlighting mortgage fraud as an issue for the companies in recent public appearances.

Appearing on Donald Trump Jr.’s podcast, Triggered, last week, Pulte said he could not comment on James’ case.

Bill Pulte

“But I will say that people claiming that they live in certain states that they don’t live in, people claiming other representations that are maybe not necessarily true — these are very big concerns to the mortgage market,” Pulte said. “It doesn’t matter whether you’re a welder, a plumber, a politician, an attorney — if you commit mortgage fraud, you are a risk to the system.”

In his criminal referral, Pulte claimed James falsified records by stating that a Norfolk, Virginia, home she purchased with her niece was to be her principal residence, the New York Post reported. Separately, Pulte accused James of misrepresenting the number of units in her Brooklyn residence to obtain better loan terms.

“Occupancy fraud is a huge issue in the country where people are basically getting loans based on certain down payments and certain interest rates, based on saying that they live in one area and not another, as well as saying that they should qualify for loans that maybe they shouldn’t have,” Pulte told Trump Jr. “So, you know, just generally speaking, my thought is that mortgage fraud is rampant and we are doing everything we can. We’ve made a number of criminal referrals — not just [James] — and we will continue to prosecute.”

Letitia James

James has acknowledged a clerical error on a 2023 power of attorney form related to the purchase of the Virginia property, but denies wrongdoing.

“This investigation into me is nothing more than retribution,” James told the Post.

Palantir’s business booming under Trump

Palantir has a long history as a government contractor, providing services to a range of federal agencies including the IRS, the National Institutes of Health and the Department of Veterans Affairs that generated $1.2 billion in revenue last year. During the first quarter of 2025, new defense contracts helped the company grow revenue from federal contracts by 45 percent from a year ago, to $373 million.

But Palantir has come under greater scrutiny during the Trump administration as it wins business that raises privacy concerns, such as an Immigration and Customs Enforcement (ICE) contract to build a platform that tracks the movements of immigrants.

A senior IRS official told CNN last month that employees at the agencies are concerned that Palantir is sifting through taxpayer data to track down immigrants and deport them.

Silicon Valley investor Paul Graham has accused Palantir of “building the infrastructure of the police state,” and demanded that the company make a public commitment that it will not build tools that could be used by the government to violate citizens’ rights, NPR reported this month.

“Palantir designs and deploys artificial intelligence and machine learning technology used by government agencies and commercial clients,” Fannie Mae said in a press release Wednesday. “The company’s technology provides expansive monitoring for anomalous transactions, activities, and behaviors to help companies detect suspicious activity and trigger investigative action.”

While Palantir co-founder Peter Thiel is a Trump supporter and donor, CEO Alex Karp is a Democratic donor who supported Kamala Harris for president, CNN noted.

Alex Karp

“This partnership with Fannie Mae will set off a revolution in how we combat mortgage fraud in this country,” Karp said in a statement. “We are bringing the fight directly to anyone who attempts to defraud our mortgage system and exploit hardworking Americans.”

How Fannie and Freddie deal with fraud

Fannie and Freddie don’t make loans themselves but buy mortgages from lenders and bundle them up into mortgage-backed securities (MBS) that are sold to investors. MBS are the ultimate source of funding for most U.S. home loans, and homebuyers enjoy low rates largely because the mortgage giants guarantee payments to investors.

Fannie Mae and Freddie Mac have the right to demand that lenders buy back mortgages if it’s later discovered that borrowers, sellers, real estate agents, lenders or appraisers made significant “misstatements, misrepresentations, or omissions” in selling loans to them.

Fannie and Freddie will only require lenders to buy back loans with misrepresentations when they identify a common pattern of activity on three or more loans made by the same lender. But there’s no such exemption for instances of fraud.

Fannie Mae specifies that it can require lenders to repurchase any mortgage where fraud is established in court or its investigators find “clear and convincing evidence” that a lender or other party “knowingly executed or participated in a scheme” to defraud it.

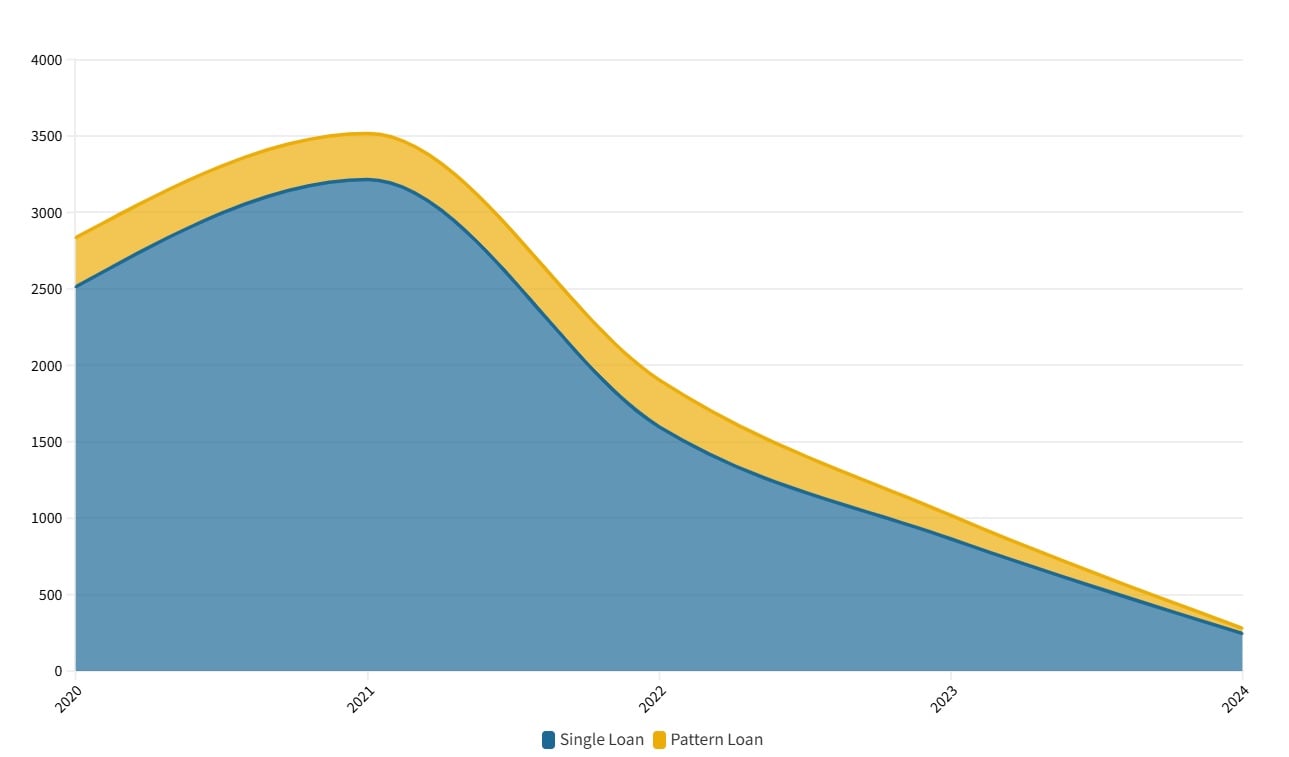

Fannie Mae fraud findings

Fraud findings on Fannie Mae-backed mortgages, 2020-2024. Source: Fannie Mae.

Mortgage fraud can go undetected for many years and is often discovered only when a borrower stops paying their loan.

So far, Fannie Mae’s Financial Crimes team has uncovered evidence of fraud in 3,517 single-family loans originated in 2021, including 3,215 single loans and 302 “pattern loans” — loans in which a common pattern of activity involving the same individual or company was discovered.

Through May 8, Fannie Mae investigators had uncovered evidence of fraud in only 280 loans originated last year — 245 single loans and 35 “pattern loans.”

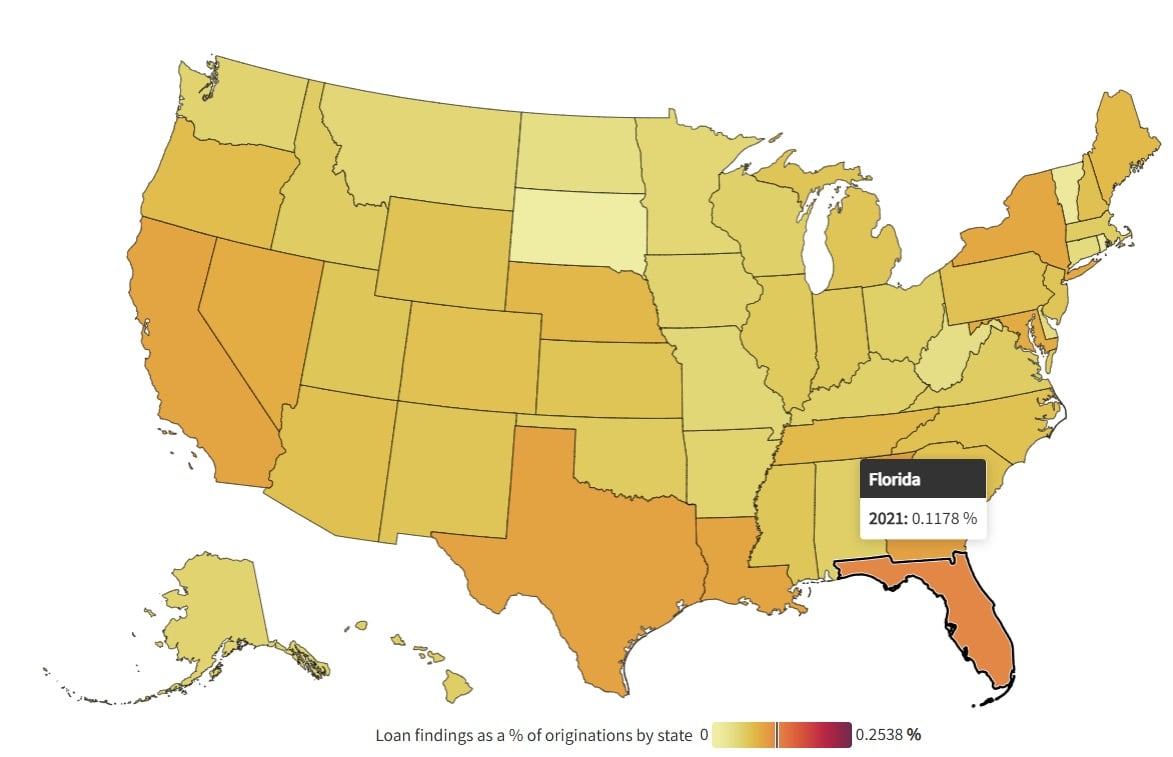

Loan fraud prevalence by state

Fraud as a percentage of Fannie Mae-backed loans originated in 2021 by state. Source: Fannie Mae.

With mortgage rates at historic lows, Fannie Mae in 2021 provided backing for 4.8 million single-family loans — 1.5 million purchase loans and 3.3 million refinancings.

In Florida, the state with the highest percentage of fraudulent loans, about 12 in 10,000 loans (0.12 percent) originated in 2021 were later found to have potential fraud issues.

In an October 2024 report, CoreLogic said about 1 in 123 mortgage applications lenders received in Q2 2024 showed indications of fraud, up 8 percent from a year ago. Fraud was more likely to show up in purchase applications (1 in 111) than in requests to refinance (1 in 171).

CoreLogic determined that New York, Florida, California, Connecticut and New Jersey are the states where lenders are at the highest risk for fraud.

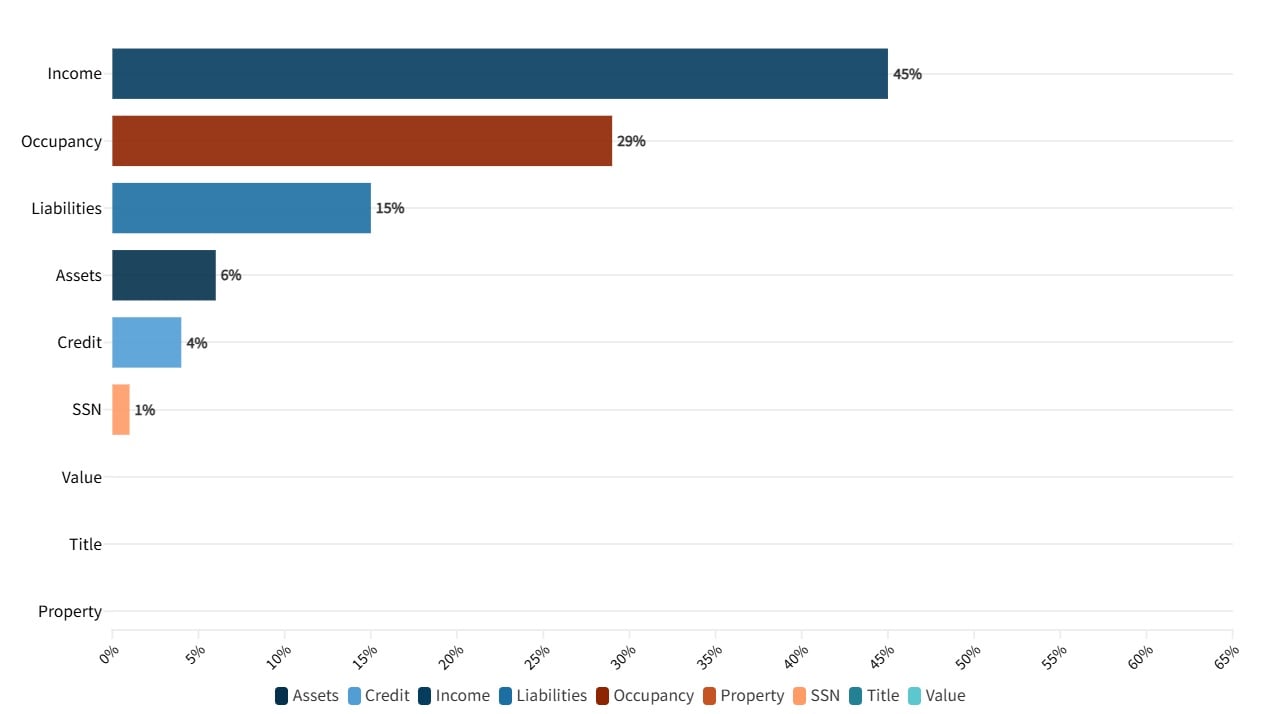

Most prevalent types of fraud

Types of fraud discovered on Fannie Mae-backed mortgages originated in 2024. Source: Fannie Mae.

Income misrepresentation was the most common type of fraud uncovered on loans backed by Fannie Mae last year (45 percent), followed by false occupancy claims (29 percent), understated liabilities (15 percent), overstated assets (6 percent), inflated credit (4 percent) and false social security numbers (1 percent).

Third-party mortgage brokers were blamed for much of the fraud that occurred in the subprime lending boom that preceded the 2007-2009 housing crash and Great Recession.

But mortgage brokers were involved in only about one in five Fannie Mae loans (19 percent) originated last year in which fraud is suspected, with third-party correspondent lenders involved with another 23 percent.

Most loans (58 percent) in which evidence of fraud was discovered were made by “non-third party” lenders like independent mortgage banks.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Shares in mortgage giants Fannie Mae and Freddie Mac soared Thursday after President Trump posted on his social media platform, Truth Social, that he’s giving “very serious consideration” to “bringing [both companies] public.”

Fannie and Freddie are already publicly traded on an over-the-counter market. But investors interpreted Trump’s comments to mean that the federal government will soon put forward a plan to restructure the companies — perhaps generating a windfall for the government and existing investors in the process.

There’s been talk that the government could invest its stake in Fannie and Freddie into a sovereign wealth fund that would provide investors who fund most home loans reassurance about continued government backing.

Treasury Secretary Scott Bessent has endorsed the idea of creating a U.S. sovereign wealth fund, and acknowledged in March that the government’s stakes in Fannie and Freddie — which the Congressional Budget Office estimates are worth about $270 billion — is one of a number of government assets that could fund it.

One way the Trump administration could monetize its stake in Fannie and Freddie would be to buy out public common shareholders — including billionaire Bill Ackman — and then issue preferred shares that pay dividends, Whalen Global Advisors LLC Chairman Christopher Whalen told Yahoo Finance.

That plan would leave the U.S. as the sole voting shareholder of Fannie and Freddie, and “give Treasury all the cash they need,” Whalen said.

“I think it’s very likely, because they need the money,” Whalen Global Advisors chairman Chris Whalen says on a potential public offering of Fannie Mae & Freddie Mac. pic.twitter.com/rgnC8dJwrq

“The reason they’re talking about this is they need the cash in order to make their tax cuts and their budget reconciliation bill work,” Whalen said.

An industry veteran, whose past experience includes senior research positions at Kroll Bond Rating Agency and Carrington Holding Co., Whalen has connections at Fannie Mae and Freddie Mac.

Trump said he’ll be speaking to Bessent, Secretary of Commerce Howard Lutnick, and Bill Pulte, whom he appointed to oversee Fannie and Freddie’s federal regulator, “making a decision in the near future.” “Fannie Mae and Freddie Mac are doing very well, throwing off a lot of CASH, and the time would seem to be right,” Trump posted Wednesday.

Hoping for a plan like the one laid out by Whalen, investors bid common shares in Fannie Mae and Freddie Mac up by more than 40 percent Thursday, to new 52-week highs. Preferred shares in Fannie and Freddie, which were delisted in 2010 but still trade over the counter, posted more modest double-digit gains.

The grandson of PulteGroup Inc. founder William J. Pulte, Bill Pulte in March appointed himself the chairman of Fannie Mae and Freddie Mac’s boards in a purge in which 14 board members were removed from their positions.

Banker, investor and lawyer Omeed Malik — dubbed “MAGA world’s premier financier” and a “close friend” of Donald Trump Jr. by New York Magazine — joined Fannie Mae’s board in April.

Democrats, including Sen. Elizabeth Warren, questioned the legality of Pulte’s purge of Fannie and Freddie’s boards. They’ve been keeping an eye on the administration’s plans for the mortgage giants, and some are wary of plans to create a sovereign wealth fund and the Trump family’s crypto investments.

The challenge for presidents who have tried to release Fannie and Freddie from conservatorship in the past — including Barack Obama and Trump in his first term — is how to restructure the companies to not only shield taxpayers from risk, but protect homebuyers from paying higher mortgage rates.

“My fundamental concern is that without a well-defined vision, exit from conservatorship could cause havoc in financial markets and in the U.S. housing market,” the Urban Institute’s Laurie Goodman wrote in an April analysis. “And I do not believe there is any consensus on what this vision should be.”

Fannie and Freddie have been in government conservatorship since 2008, when the Bush administration determined they needed to be bailed out, with the government taking a large stake in the companies to keep them afloat during the 2007-2009 housing crash and Great Recession.

During Trump’s first term as president, his administration laid the groundwork for releasing Fannie and Freddie from government conservatorship but were, ultimately, unable to finish the jobs.

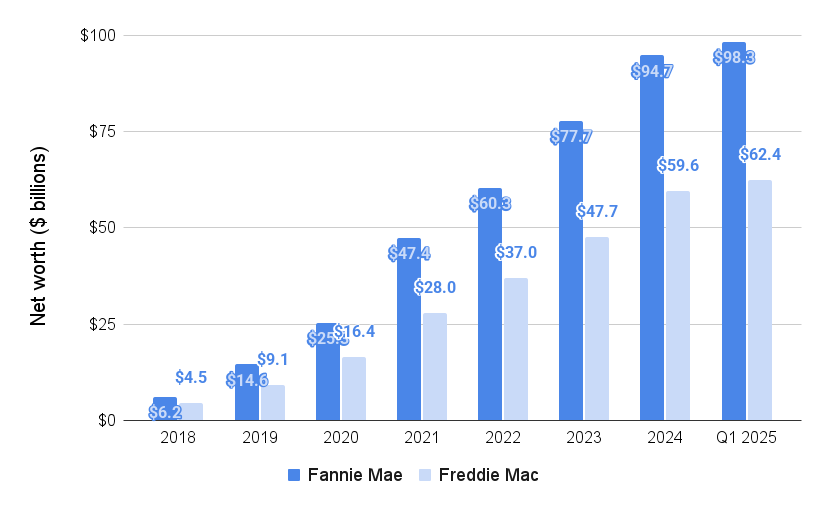

One important step taken was the first Trump administration’s decision in 2019 to discontinue the Treasury’s “sweeps” of Fannie and Freddie’s profits, which allowed the companies to begin rebuilding their net worths, which totalled $161 billion as of March 31.

Goodman estimates that Fannie and Freddie are about $132 billion short of the net worths they would need to meet the capital requirements Congress has mandated for privatization — a problem the Trump administration wouldn’t have to deal with if it buys out common shareholders, as proposed by Whalen.

Fannie and Freddie don’t make loans themselves, but protect investors who buy mortgage-backed securities (MBS) from losses. The guarantees Fannie and Freddie provide to MBS investors make mortgages a safe bet for institutional investors who are willing to accept modest returns that keep borrowing costs low.

Together, the companies were guaranteeing payments to investors on $6.74 trillion in single-family mortgages as of March 31. When times are tough, defaults on those loans can take a heavy toll on Fannie and Freddie’s bottom lines.

But in good times, the companies generate big profits that have helped them repay a $191 billion taxpayer bailout. The guarantee fees that the companies charge lenders helped the companies generate combined 2024 profits of $28.9 billion.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

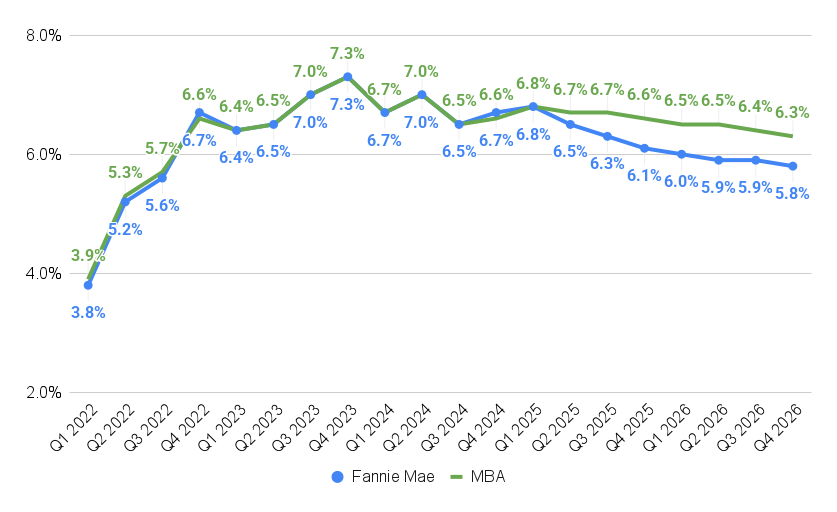

While Fannie Mae economists see mortgage rates coming down by a full percentage point, forecasters at the Mortgage Bankers Association have issued a more cautious take.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

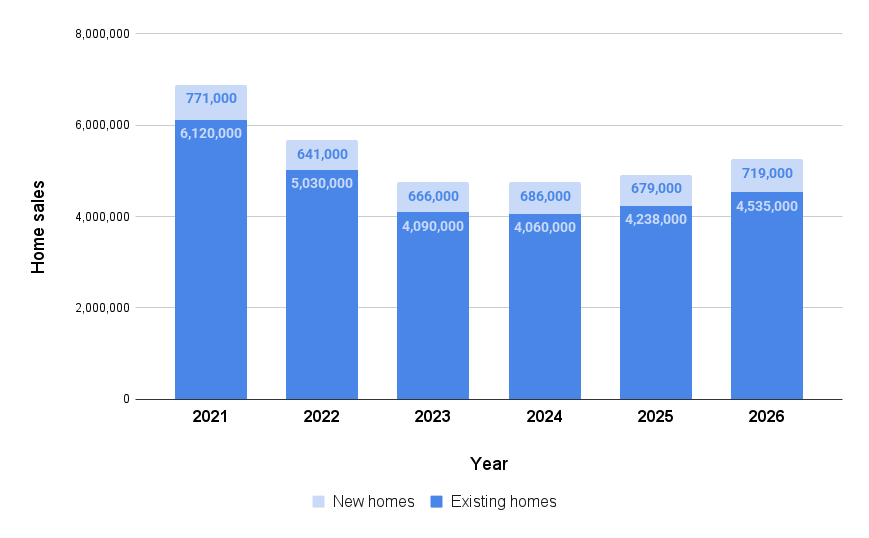

With mortgage rates looking like they could come down a little faster this year and next, Fannie Mae economists think home sales could bounce back by 3.6 percent this year, to 4.92 million homes.

That’s 54,000 more home sales than Fannie Mae was forecasting in April, when economists at the mortgage giant were expecting mortgage rates to still be at 6.2 percent at the end of this year and 6 percent next year.

Fannie Mae’s latest forecast, released Wednesday, projects rates on 30-year fixed-rate mortgages will drop to 6.1 percent by the end of this year and to 5.8 percent by the end of next year.

With sales of new homes projected to shrink by 1 percent this year, to 679,000, the projected bounce in home sales would be driven entirely by 4.4 percent growth in sales of existing homes, to 4.24 million.

Fannie Mae’s Economic and Strategic Research (ESR) Group is forecasting even stronger 2026 growth, with total sales expected to surge by 6.8 percent to 5.25 million.

If that forecast pans out, it would be the first time since 2022 that sales of new and existing homes surpassed five million.

Next year’s gains are also projected to be driven by 7 percent growth in existing home sales, to 4.53 million, with new home sales also forecast to grow by 5.9 percent, to 719,000.

While Fannie Mae economists see mortgage rates coming down by a full percentage point from Q1 2025 levels, forecasters at the Mortgage Bankers Association issued a more cautious take on May 16.

MBA economists think rates will still be averaging 6.6 percent during Q4 2025 and 6.3 percent during Q4 2026.

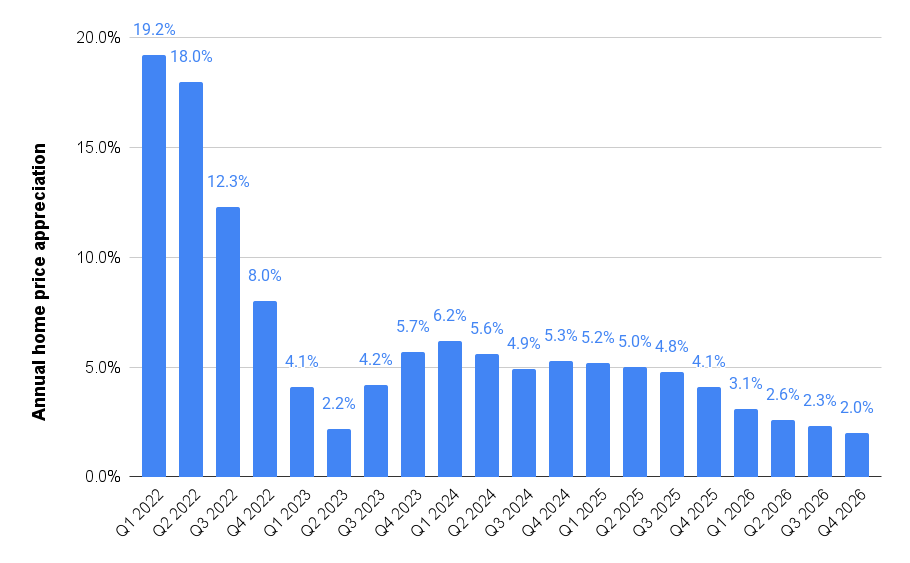

Fannie Mae economists update their home price appreciation forecast four times a year — in the first month of each quarter — rather than monthly.

In January, Fannie Mae economists were expecting annual home price appreciation to cool to 3.5 percent by Q4 2025.

In updating their home price appreciation forecast in April, forecasters at the mortgage giant predicted that home prices will be up 4.1 percent from a year ago in Q4 2025, before appreciation cools to 2 percent by Q4 2026.

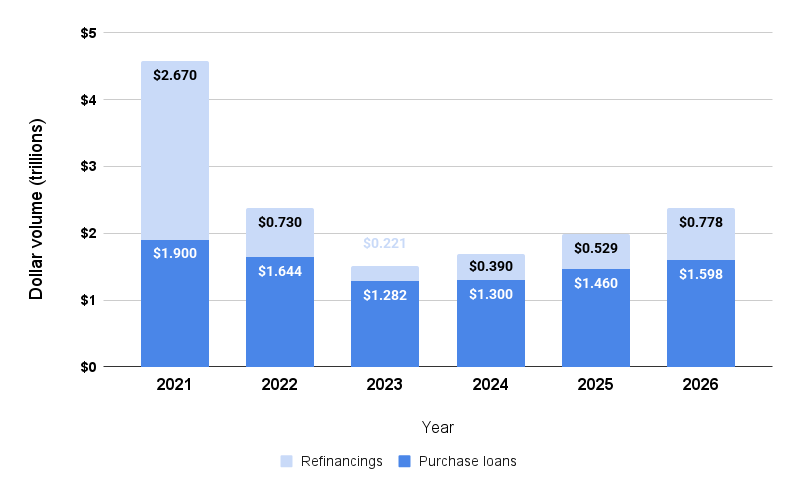

With home sales and home prices both expected to post gains, Fannie Mae economists expect mortgage originations to grow by 17.7 percent this year, to $2 trillion.

While refinancing is projected to grow by 35.6 percent this year, to $529 billion, lenders are on track to do almost three times as much purchase mortgage business.

Fannie Mae economists expect purchase loan volume will grow by 12.3 percent this year, to $1.46 trillion.

Additional easing of mortgage rates next year is expected to boost 2026 refinancing by 47.1 percent, to $778 billion, and purchase lending by 9.5 percent, to $1.6 trillion.

Next year’s projected $2.38 trillion in total mortgage volume would represent 58 percent growth from a 2023 trough of $1.5 trillion.

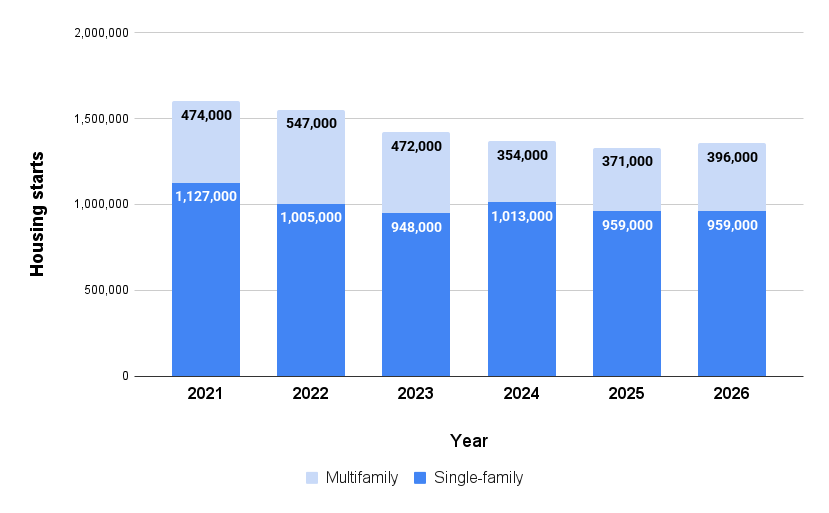

With inventories of new homes for sale on the rise in some markets, Fannie Mae economists expect single-family home starts will shrink by 5.3 percent this year, to 959,000, even as multifamily home starts grow by 4.8 percent to 371,000.

Next year, single-family home starts are expected to be flat at 959,000, with 6.7 percent growth in multifamily home starts, to 396,000.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.