by Matt Carter | Jun 4, 2025 | Industry, News Feed

While purchase loan demand was still up 18 percent last week from a year ago, some of that demand may not translate into sales, with Redfin reporting an unusual bump in cancelled purchase contracts.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

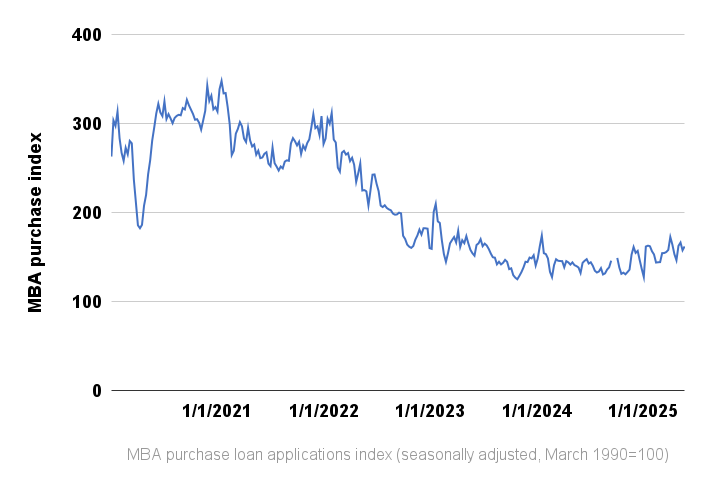

Last week’s dip in mortgage rates didn’t send homebuyers rushing to their lender, with purchase loan applications contracting by a seasonally adjusted 4 percent compared to the week before, according to a weekly survey of lenders by the Mortgage Bankers Association (MBA).

The latest MBA Weekly Mortgage Applications Survey, released Wednesday, found purchase loan demand was still up 18 percent from a year ago. However, some of that demand may not translate into sales, with Redfin reporting an unusual bump in cancelled purchase contracts in April.

The MBA survey showed requests to refinance were down 4 percent during the week ending May 30 when compared to the week before, but up 42 percent from a year ago.

Joel Kan

“Most mortgage rates moved lower last week, with the 30-year fixed rate declining to 6.92 percent and staying in the 6.8 percent to 7 percent range since April,” MBA Deputy Chief Economist Joel Kan said in a statement.

“Refinance activity fell across both conventional and government segments, and the overall average refinance loan size was the smallest since July 2024, as potential borrowers hold out for larger rate drops,” Kan said.

Redfin’s analysis of MLS pending-sales data showed 14 percent of homes that went under contract in April — about 56,000 properties — ended up not selling because their purchase agreements were cancelled.

That’s the second highest share of April cancellations in records dating back to 2017, Redfin said, after April 2020, when the pandemic put the brakes on many closings.

Redfin said purchase agreements are being cancelled at a higher rate than usual during the spring homebuying season due to economic and political uncertainty, a surge of inventory in many markets, and elevated home prices and mortgage rates.

Mortgage rates on the rebound

Since hitting a 2025 low of 6.48 percent on April 4, rates on 30-year fixed-rate conforming mortgages have rebounded above 6.8 percent for most of May, according to lender data tracked by Optimal Blue.

Inflation continued to move closer to the Federal Reserve’s 2 percent target in April, but central bank policymakers have been reluctant to cut short-term interest rates as they continue to assess the impacts of the Trump administration’s policies in areas including tariffs, immigration, taxes and regulation.

Purchase loan demand peaked in April

Even after adjusting for heightened demand during the spring homebuying season, purchase loan requests peaked in April, MBA data shows.

At 155 for the week ending May 30, the MBA’s seasonally adjusted purchase index was at its lowest reading since the week ending April 25. The index is now down 18 points from its 2025 high of 172.7 registered during the week ending April 4, but 27 points higher than a low for the year registered in January.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 4, 2025 | Industry, News Feed

Lifting of the asset cap could give the bank greater leeway to originate jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $806,500 conforming loan limit in most markets.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Wells Fargo has freed itself from a $1.95 trillion asset cap that limited its growth for nearly a decade, with the Federal Reserve Board certifying Tuesday that the bank has put “widespread consumer abuses and other compliance breakdowns” behind it and improved its governance and risk management program.

The Fed imposed the asset cap in 2018, in the wake of a series of scandals, including “cross-selling” practices in which bank customers were enrolled in new deposit and credit card accounts without their knowledge.

“Wells Fargo pursued a business strategy that prioritized its overall growth without ensuring appropriate management of all key risks,” federal regulators said in imposing the asset cap. “The firm did not have an effective firm-wide risk management framework in place that covered all key risks. This prevented the proper escalation of serious compliance breakdowns to the board of directors.”

Tuesday’s lifting of the asset cap “represents successful remediation to the required standard based on focused management leadership, strong board oversight, and strict supervision holding the firm accountable,” Federal Reserve Governor Michael Barr said in a statement. “All three will need to continue for the firm to have a sustainable approach.”

Wells Fargo CEO Charlie Scharf said Wells Fargo is “a different and far stronger company today because of the work we’ve done” to address past problems.

Since 2019, the bank has closed 14 consent orders imposed by regulators over its business practices.

Wells Fargo announced in January that the Consumer Financial Protection Bureau had lifted a 2022 consent order related to a $3.7 billion settlement over the bank’s alleged mismanagement of mortgages, auto loans and deposit accounts.

On May 29, Wells Fargo said it had closed a 2015 consent order with the Office of the Comptroller of the Currency, leaving only the 2018 consent order with the Federal Reserve Board in place.

Wells Fargo has “changed and simplified our business mix, and we have transformed the management team and how we run the company,” Scharf said in a statement Tuesday.

“We have been methodically investing in the company’s future while improving our financial results and profile. We are excited to continue to move forward with plans to further increase returns and growth in a deliberate manner supported by the processes and cultural changes we have made.”

Lifting of the asset cap could give the bank greater leeway to originate jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $806,500 conforming loan limit in most markets. Lenders who make such loans often hold them on their balance sheet, since they’re more difficult to bundle up and sell to investors.

Once the nation’s largest mortgage lender, Wells Fargo was overtaken by direct lender Quicken Loans (now Rocket Mortgage) in 2017 and fell out of the top 10 in the face of regulatory issues, a shrinking branch footprint and rising interest rates.

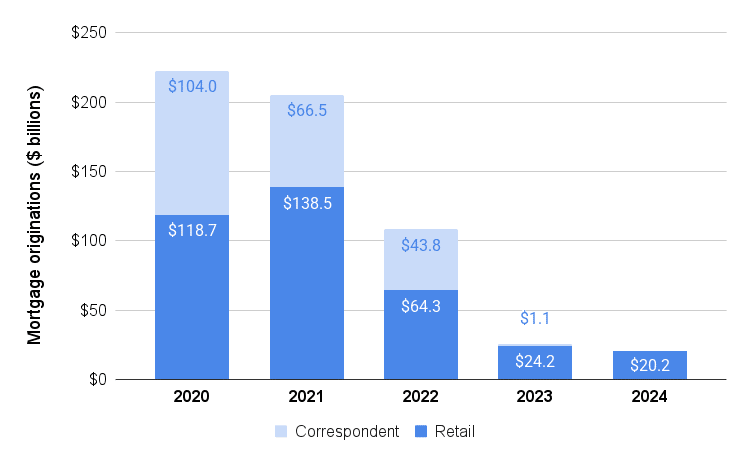

Wells Fargo mortgage originations, 2020-24

Source: Wells Fargo earnings reports.

When borrowers rushed to refinance during the pandemic, Wells Fargo originated $223 billion in mortgages in 2020 — more than 10 times as much business as it did last year ($20.2 billion).

Scharf has said Wells Fargo is “not interested in being extraordinarily large in the mortgage business, just for the sake of being in the mortgage business.”

But theoretically, technology like artificial intelligence employed by the nation’s biggest mortgage lenders — UWM and Rocket — could allow Wells Fargo to rapidly scale its mortgage business despite its reduced branch office footprint and staffing levels.

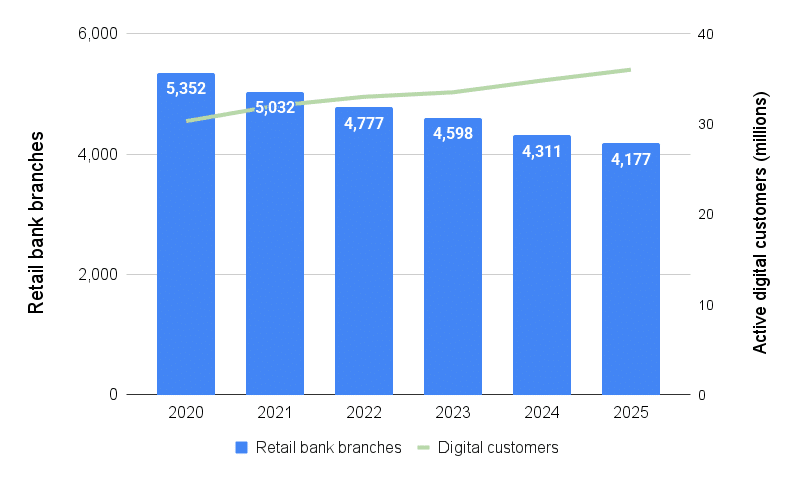

Wells Fargo closing branches, growing digital customer base

Retail bank branch and digital customer count at the beginning of the year. Source: Wells Fargo earnings reports.

Wells Fargo ended 2024 with 4,177 retail bank branches, down 22 percent from 5,352 at the beginning of 2020.

But a growing number of customers — 36 million at the beginning of the year — access the bank online or through mobile devices, up 19 percent since the beginning of 2020.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 4, 2025 | Industry, News Feed

With antitrust regulators declining to weigh in, $1.75 billion deal to marry a tech-focused mortgage lender to real estate brokerage could close by the end of the month.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Redfin shareholders on Wednesday signed off on the company’s agreement to be acquired by mortgage lending giant Rocket Companies, clearing the way for the deal to close this month.

The $1.75 billion merger agreement was approved by Redfin shareholders at a special meeting Wednesday, according to preliminary voting results.

The window for antitrust regulators to weigh in with questions or objections to the deal closed on May 8. In reporting first quarter earnings, Rocket executives said they expected to close the deal as soon as this quarter, which ends June 30.

Five Senate Democrats on Wednesday condemned Rocket’s plans to acquire Redfin and Mr. Cooper, and asked why antitrust regulators at the Department of Justice and Federal Trade Commission declined to challenge the Redfin merger.

“At a time when families already face a housing affordability crisis, these deals would combine the second-largest mortgage originator, the largest mortgage servicer, and the third-most-visited real estate brokerage website in the United States, into a massive, vertically integrated conglomerate that may reduce choice and raise prices for American families in the housing market,” Senate Democrats including Elizabeth Warren, Bernie Sanders and Cory Booker wrote regulators.

“Instead of competing for new customers by offering better products and services, Rocket is attempting to acquire two already massive companies to create a single, vertically integrated conglomerate,” the lawmakers claimed. “Rocket’s proposed acquisitions of Redfin and Mr. Cooper create the potential for Rocket to steer homebuyers to its own products, hike prices based on private data, and block competition.”

In a pitch to investors in March, Rocket executives said that by handling every aspect of homebuying and selling — from home search to mortgage financing and title and closing — transaction costs on the median priced home will drop from $40,000 to $20,000.

Redfin shareholders had filed four lawsuits complaining that shareholders were entitled to more information about the deal. Attorneys for Redfin shareholder Jason Morano, for example, sought class action certification to represent shareholders they claimed were left in the dark by a “materially incomplete and misleading” deal proxy statement.

Morano’s May 9 complaint sought a court order preventing Redfin shareholders from voting on the merger until they’ve received more details on Redfin deal advisor Goldman Sachs’ dual role as a lender to Rocket.

In a May 29 proxy statement, Redfin executives said all four lawsuits “are without merit, that no supplemental disclosures are required under applicable law, and that the requested additional disclosures are immaterial.”

Rocket, which also has its sights set on acquiring the nation’s biggest loan servicer, Mr. Cooper, says acquiring Redfin will help it achieve its goal of capturing 8 percent of the purchase loan market, and the $9.4 billion Mr. Cooper deal will put Rocket in touch with more homeowners who might be ready to refinance.

Rocket wants to handle 20 percent of U.S. mortgage refinancings, and Rocket CEO Varun Krishna said last month that the company has invested about $500 million in AI and other technology that will help the company scale its business without a proportionate increase in expenses after the mergers.

Rocket announced this week that it plans to issue $4 billion in debt and use the proceeds to retire notes held by Mr. Cooper subsidiary Nationstar Mortgage Holdings Inc.

Editor’s note: This story has been updated to include criticism of Rocket’s plans to acquire Redfin and Mr. Cooper by Senate Democrats.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 3, 2025 | Industry, News Feed

Although Rocket’s plans to acquire Mr. Cooper and Redfin are structured as all-stock deals, assuming their debts will leave Rocket more highly leveraged, Fitch analysts said of possible debt rating downgrade.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Rocket Companies will make the most of the company’s credit rating to issue $4 billion in debt and use the proceeds to retire notes held by a subsidiary of the nation’s largest mortgage servicer, Mr. Cooper, which Rocket plans to acquire this year.

Rocket said Tuesday it plans to issue $2 billion in senior unsecured notes due in 2030 and another $2 billion due in 2033.

After the Mr. Cooper acquisition closes, Rocket will use part of the proceeds to pay off $1.95 billion in notes owed by Mr. Cooper subsidiary Nationstar Mortgage Holdings Inc. that are due in 2026, 2027 and 2028.

The remaining proceeds may be used “at the company’s discretion” to pay off, purchase or amend additional Nationstar notes that will be due in 2029, 2030, 2031 and 2032.

Mr. Cooper had $11.3 billion in outstanding debt as of March 31, including $4.95 billion in unsecured senior notes at interest rates ranging from 5 percent to 7.125 percent. Due dates for the notes are spread out over six years, from 2026 to 2032.

Rocket’s plans to acquire not only Mr. Cooper but real estate brokerage Redfin attracted the attention of analysts at Fitch Ratings, who in March warned that they may downgrade debt issued by subsidiary Rocket Mortgage to junk bond status.

In placing Rocket Mortgage’s issuer default rating on “rating watch negative,” Fitch analysts said Rocket has a “strong liquidity profile,” but will probably have to keep borrowing in order to fund loans and acquire mortgage servicing rights after it closes the deals to acquire Mr. Cooper and Redfin.

Fitch analysts said they will weigh a downgrade on Rocket Mortgage’s long-term issuer default rating (IDR) to “‘BB+’ from ‘BBB-,’” which would make it more costly for Rocket to borrow money.

Although both the Mr. Cooper and Redfin acquisitions are structured as all-stock deals, assuming Mr. Cooper and Redfin’s debt obligations will leave Rocket more highly leveraged.

Fitch estimates that the Mr. Cooper deal will more than double Rocket’s corporate leverage ratio, from 0.6x to 1.4x after the deal closes.

Mr. Cooper’s corporate leverage ratio was 2.1x at the end of last year, and Fitch analysts said they expect to upgrade the company’s BB issuer rating.

At the time the deals were announced, the all-stock transactions valued Mr. Cooper at $9.4 billion, while Redfin was valued at $1.75 billion.

In reporting first-quarter earnings, Rocket executives said they expect the Redfin deal to close as soon as this quarter, which ends June 30, and that the Mr. Cooper acquisition remains on track to close by the end of the year.

Speaking at an investment conference in May, Rocket CEO Varun Krishna said over the past several years, Rocket has invested about $500 million in AI and other technology that will help the company scale its business without a proportionate increase in expenses after the merger.

He said Rocket’s acquisition of Redfin will help it achieve its goal of capturing 8 percent of the purchase loan market, and the Mr. Cooper deal will put Rocket in touch with more homeowners who might be ready to refinance.

Rocket wants to handle 20 percent of U.S. mortgage refinancings. After acquiring Mr. Cooper, Rocket will be collecting payments on $2.1 trillion in mortgage loans — about one in six U.S. mortgages. When those homeowners are ready to refinance, Rocket will have a leg up on “recapturing” their business, Krishna said.

“Having a relationship at the top of the funnel and with real estate agents allows you to build a stronger organic purchase business,” Krishna said of the Redfin deal. “Having a servicing book allows you to build an organic servicing recapture business.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | May 30, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Inflation continued to move closer to the Federal Reserve’s 2 percent target in April, but central bank policymakers are expected to resist calls by the Trump administration to cut interest rates as they continue to assess the impacts of the administration’s policies in areas including tariffs, immigration, taxes and regulation.

The personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred gauge of inflation, showed the price of goods and services rose 2.1 percent in April from a year ago, the Bureau of Economic Analysis reported Friday.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

It was the second month in a row that the annual increase in the PCE price index moved in the right direction. The core PCE price index, which excludes volatile food and energy costs and is seen as a better indicator of inflation trends, showed costs were up 2.5 percent from a year ago — the lowest reading in 4 years.

Inflation moving toward Fed’s goal

Before the latest inflation numbers were released, Federal Housing Finance Agency Director Bill Pulte urged Fed policymakers to cut rates when they meet next on June 17.

Bill Pulte

“First and foremost, inflation is lower than it was the last time they cut,” Pulte said Thursday in an appearance on Bloomberg’s The Close. “President Trump has been very successful at reducing inflation, and so therefore it just only makes sense that if inflation was higher and they did cuts, then why can’t they do cuts now?”

While the Fed has tight control over short-term interest rates, mortgage rates are largely determined by investor demand for mortgage-backed securities (MBS), the ultimate source of funding for most home loans.

As the Fed cut short-term interest rates by a full percentage point at the end of last year, mortgage rates moved in the other direction, as economic data coming in last fall showed inflation moving away from the Federal Reserve’s 2 percent target.

But Trump himself remains fixated on the Fed, calling Federal Reserve Chair Jerome Powell “a FOOL, who doesn’t have a clue” in a May 8 Truth Social post after Fed policymakers voted unanimously to keep the short-term federal funds rate at 4.25 percent to 4.5 percent.

At a press conference following the meeting, Powell said the job market remains “solid,” but tariffs implemented and threatened by the Trump administration could reignite inflation. “The new administration is in the process of implementing substantial policy changes in four distinct areas: trade, immigration, fiscal policy and regulation.”

Tariff increases announced so far have been “significantly larger than anticipated,” the Fed chair said, and if implemented, “are likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment.”

Forecasters at Pantheon Macroeconomics are seeing early signs that tariffs are having an impact on prices, with core PCE inflation up 0.3 percent from March to April, Pantheon Senior U.S. Economist Oliver Allen said in a note to clients Friday.

Oliver Allen

“Much bigger increases in core goods inflation probably loom as the costs of the new tariffs are eventually passed on,” Allen said. “Accordingly, we still think core PCE inflation will peak later this year between 3 percent and 3.5 percent, if the current mix of tariffs remains in place.”

The CME FedWatch tool, which tracks futures markets to predict the probability of future Fed moves, shows investors don’t expect the Fed to cut short-term rates until September. But bets placed by investors on Friday indicate a 72 percent chance of a September rate cut, up from 66 percent on Thursday and 60 percent on May 23.

When the European Central Bank continued to cut rates in April while the Federal Reserve continued to take a wait-and-see stance, Trump complained that Powell “is always TOO LATE AND WRONG” and said his “termination cannot come fast enough!”

In a May 22 order, the Supreme Court made it clear that Trump can’t fire Powell without cause — the constitutionality of for-cause removal protections for members of the Federal Reserve’s Board of Governors are not in dispute.

Powell met with Trump at the White House Thursday “to discuss economic developments” including growth, employment and inflation, the Fed disclosed after the meeting.

“Chair Powell did not discuss his expectations for monetary policy, except to stress that the path of policy will depend entirely on incoming economic information and what that means for the outlook,” the Fed said in a statement. Fed policymakers will base their decisions “solely on careful, objective, and non-political analysis.”

Mortgage rates on the rebound

Since hitting a 2025 low of 6.48 percent on April 4, rates on 30-year fixed-rate conforming mortgages have been trending back up and flirting with January highs, according to lender data tracked by Optimal Blue.

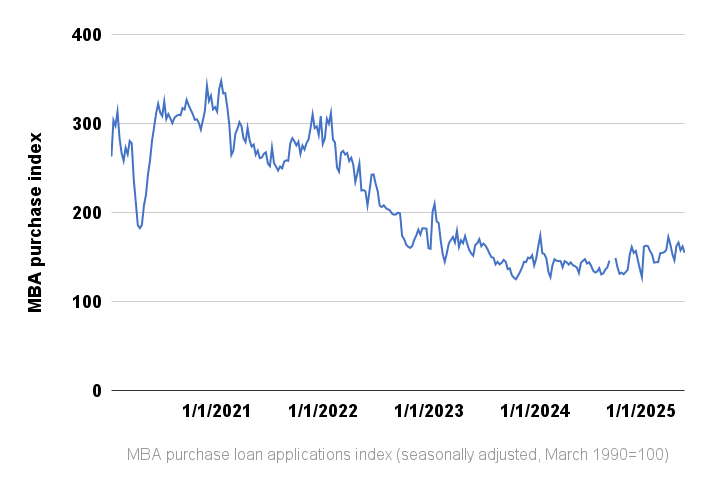

A weekly survey of lenders by the Mortgage Bankers Association shows demand for mortgages has slipped in recent weeks, but is stronger than it was a year ago.

Joel Kan

Thanks to more homes coming onto the market, applications for purchase loans were up by a seasonally adjusted 3 percent last week compared to the week before, and 18 percent higher than a year ago, MBA Deputy Chief Economist Joel Kan said.

With mortgage rates returning to the highest level since January, applications to refinance were down 7 percent week over week, but up 37 percent from a year ago.

“Purchase applications were up over the week and continue to run ahead of last year’s pace as increased housing inventory in many markets has been supporting some transaction volume, despite the economic uncertainty,” Kan said in a statement.

After hitting a 2025 high of 172.7 during the week ending April 4 as mortgage rates were touching lows for the year, the MBA’s seasonally adjusted purchase index retreated to 146.6 during the week ending April 25.

At 162.1 during the week ending May 23, the MBA purchase index is up 28 percent from its 2025 low of 127.7 registered during the first week in January.

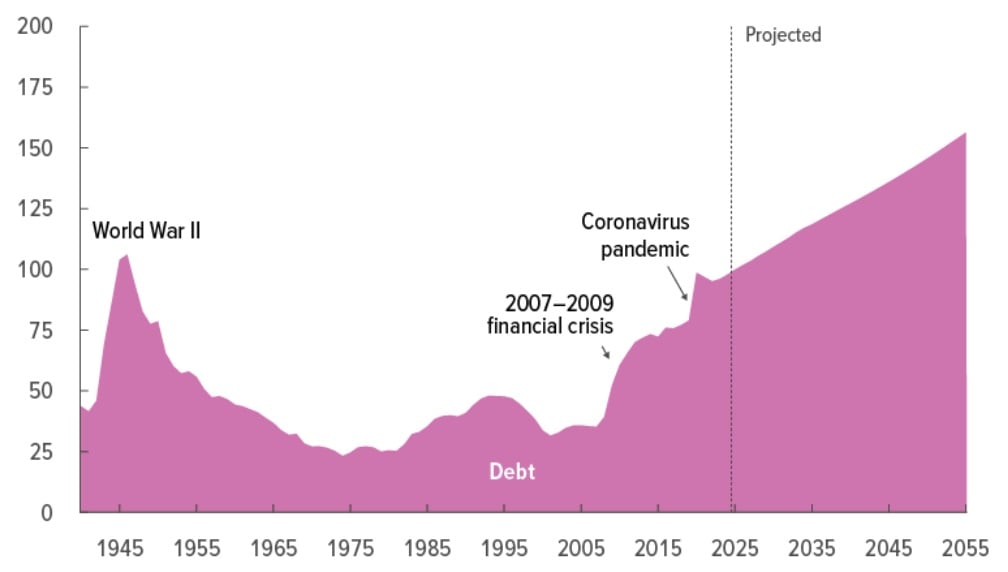

While the potential for tariffs to reignite inflation is an immediate concern for investors that has helped drive up mortgage rates, the potential for tax cuts proposed in Trump’s “big beautiful bill” to drive up federal debt is also on their long-term horizon.

On May 16, Moody’s Ratings became the last of the big rating agencies to downgrade the U.S.’s credit rating, over concerns that “successive U.S. administrations” and Congress have failed to tackle the nation’s annual budget deficits and growing interest costs.

CBO projects record government debt by 2029

The Congressional Budget Office in March projected that federal debt as a percentage of gross domestic product (GDP) will hit record levels in 2029 and continue to rise.

Trump has complained that dire projections of how extending tax cuts granted by the 2017 Tax Cuts and Jobs Act will impact deficits underestimates the boost in revenue the federal government might see if the U.S. economy grows at a faster clip.

Trump revisited that debate on Friday, calling growth projections by the Congressional Budget Office “ridiculous and unpatriotic.”

Trump advisor Peter Navarro provided more insight into Trump’s thinking Wednesday in an opinion piece for The Hill.

Navarro said that investor demands for higher yields on 10-year Treasurys — a key barometer for mortgage rates — “reflects fear, not facts.”

Peter Navarro

Bond investors, he said, “are pricing in a future where the government borrows trillions more with no offsetting revenues. They believe the tax cuts are not paid for.”

But Navarro claimed, “Trumpnomics and the Trump tariffs will put America on a sounder fiscal footing than any policy proposal in decades. That’s the complete information our financial markets should be working from – and bond investors should yield to that wisdom.”

Yields on 10-year Treasurys were essentially unchanged Friday at 4.41 percent, despite the encouraging April inflation numbers.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site