by Matt Carter | Jun 11, 2025 | Industry, News Feed

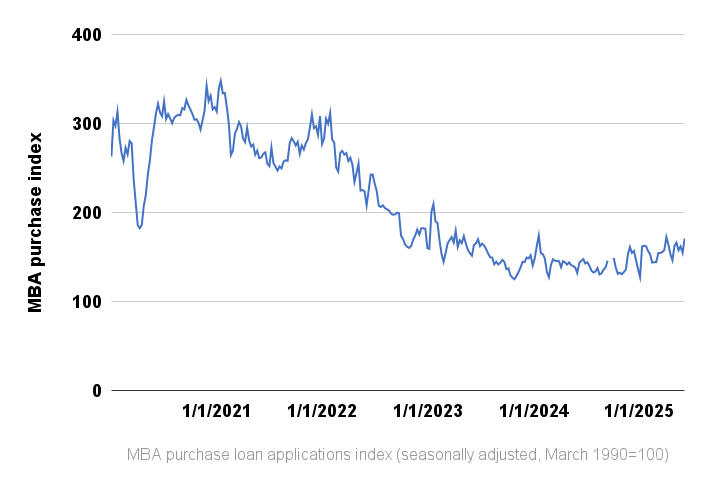

Purchase loan applications soared 10 percent last week to the highest level since April, even though rates have been stuck in the high sixes, the Mortgage Bankers Association reported Wednesday.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Mortgage rates aren’t coming down, but improving inventory in many markets helped drive up homebuyer demand for purchase loans to the second highest level of the year last week, the Mortgage Bankers Association reported Wednesday.

Demand for purchase mortgages was up by a seasonally adjusted 10 percent last week when compared to the week before, and 20 percent from a year ago. Requests to refinance were also up 16 percent week over week and 28 percent from a year ago, the MBA’s latest Weekly Mortgage Applications Survey found.

“Coming out of the Memorial Day holiday, mortgage applications increased to the highest level in over a month, driven by growth in both purchase and refinance applications,” MBA Deputy Chief Economist Joel Kan said in a statement.

Joel Kan

“Despite ongoing uncertainty surrounding the economy, homebuyers seem to be taking advantage of loosening housing inventory in certain markets,” Kan said.

Consumer sentiment about the housing market improved in May to the highest level since November, according to Fannie Mae’s monthly National Housing Survey.

While just 26 percent of Americans said May was a good time to buy, that’s up from 23 percent in April and 14 percent from a year ago, a survey low.

Mortgage rates stabilize

Rates for 30-year fixed-rate mortgages hit a 2025 low of 6.48 percent on April 4, according to lender data tracked by Optimal Blue.

Since climbing in early April over fears about the potential for tariffs to reignite inflation, rates for 30-year fixed-rate loans have been rangebound in the high sixes for the last 2 months.

Although inflation is nearing the Fed’s 2 percent goal, Fed policymakers are in a wait-and-see mode, while they assess the impacts of the Trump administration’s policies on tariffs, immigration, taxes and regulation. The job market is cooling off, but not quickly enough to alarm Fed policymakers.

The CME FedWatch tool, which tracks futures markets to predict the probability of future Fed moves, shows investors see no chance that the U.S. central bank will cut rates when policymakers meet next week.

But after an encouraging inflation report from the Bureau of Labor Statistics on Wednesday, futures markets tracked by the CME FedWatch tool priced in a 70 percent chance of a Sept. 17 rate cut, up from 62 percent on Tuesday.

Inflation moving in the right direction

The Consumer Price Index (CPI) showed the price of goods and services rose 2.35 percent from a year ago in May. While that’s up slightly from 2.31 percent in April, forecasters were expecting a bigger jump.

So far, tariffs are only having a “microscopic” impact on consumer prices, Pantheon Macroeconomics Chief U.S. Economist Samuel Tombs said in a note to clients. But he noted that it usually takes at least 3 months for retailers to pass cost increases on to consumers.

“Looking ahead, we continue to expect increases in prices for CPI core goods to gather momentum in June, then peak in July and remain above-trend for the rest of the year, assuming the current set of tariffs remain in place,” Tombs said.

The Federal Reserve’s preferred gauge of inflation, the personal consumption expenditures (PCE) index, showed the price of goods and services rose 2.1 percent in April from a year ago, the Bureau of Economic Analysis reported May 30.

The PCE index for May will be released on June 27.

Tombs said Pantheon Macroeconomics forecasters expect core PCE inflation, which excludes volatile food and energy prices, will climb to a peak of 3.25 percent around the end of the year.

Purchase loan demand rebounds

The MBA’s seasonally adjusted purchase loan index, which is benchmarked to March 1990, soared above 300 when mortgage rates plummeted to historic lows during the pandemic. But as inflation and mortgage rates surged in 2022, the index dropped below 200.

At 170.9 during the week ending June 6, the index is up 34 percent this year and approaching a 2025 high of 172.7 registered during the week ending April 4.

In addition to adjusting for seasonal factors — demand for homes usually peaks in the spring — last week’s index results included an adjustment for the Memorial Day holiday.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 11, 2025 | Industry, News Feed

Fort Wayne, Indiana-based Hallmark Home Mortgage is licensed in 18 states. Company founder and CEO Deborah Sturges is joining Fairway as a division manager.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Fairway Independent Mortgage Corp. will expand its presence in the Midwest with a deal to acquire “significant assets” of Indiana-based Hallmark Home Mortgage.

Hallmark will operate as a new division of Fairway, with CEO and founder Deborah Sturges joining Fairway with the title of president, Hallmark Home Mortgage, the companies announced Wednesday.

Deborah Sturges

“This strategic decision brings Fairway’s expanded product portfolio, enhanced technology, and deep support resources into Hallmark’s orbit,” Sturges said in a statement.

Terms of the deal were not disclosed.

Steve Jacobson

“Deborah and I worked together at Waterfield [Financial Corp.] decades ago and have remained industry acquaintances ever since,” Fairway founder and CEO Steve Jacobson said, in a statement. “Our shared values and our trust in each other make this partnership a natural fit. Our shared vision will make us even stronger together.”

Based in Fort Wayne, Indiana, Hallmark Home Mortgage is licensed in 18 states, sponsoring 45 mortgage loan originators who work out of 19 branch locations, according to Nationwide Mortgage Licensing System (NMLS) data.

In 2022, Hallmark hired former Finance of America divisional manager Marc Wadman to spearhead the lender’s expansion into Colorado, Georgia, Kansas, Louisiana, Missouri, South Carolina and Texas.

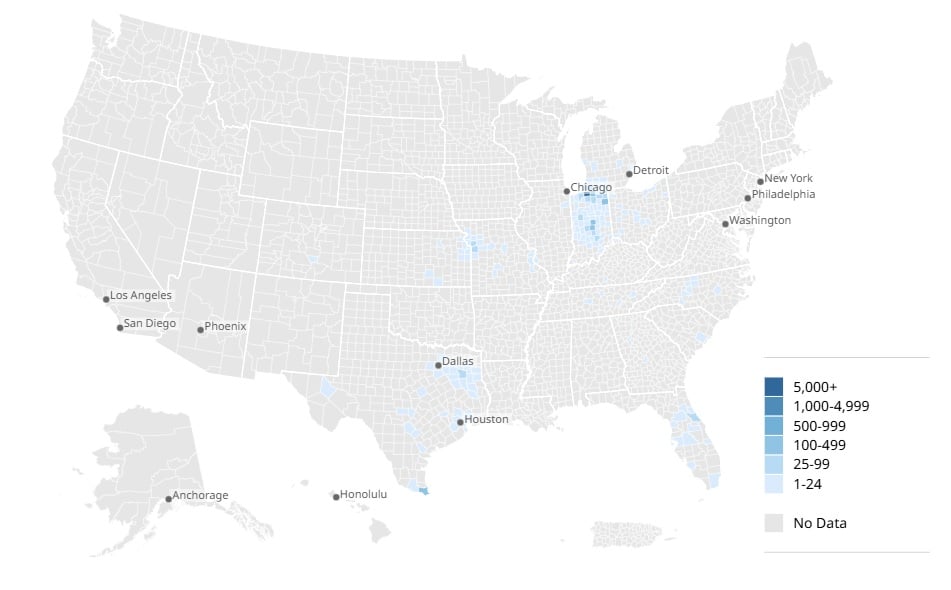

Hallmark mortgage originations by county

Source: iEmergent analysis of Home Mortgage Disclosure Act (HMDA) data.

Hallmark originated $591 million in mortgages last year, with most of that business in Indiana ($399 million), Texas ($88 million) and Missouri ($38 million), according to Home Mortgage Disclosure Act data tracked by iEmergent. Of the 2,640 loans Hallmark originated in 2024, 95 percent were purchase loans taken out by homebuyers

Based in Madison, Wisconsin, Fairway is licensed in all 50 states and sponsors 2,474 mortgage loan originators working out of 604 branch offices, according to NMLS data.

Fairway originated $23.7 billion in loans last year — 91 percent of them purchase loans — making the company the sixth-largest provider of loans to homebuyers, according to iEmergent data.

Fairway’s other trade names include 62PLUSHOMEBUYER.COM, CG HomeLoanPartners, Corporate Lending Group, MortgageBanc, Northpoint Mortgage and The Mortgage Reel. Fairway also owns the domain home.com, which redirects to the company’s homepage.

Last year, Fairway agreed to pay $10 million to settle allegations by federal regulators that the company engaged in redlining in the metro Birmingham, Alabama, market, which it entered in 2009 with the acquisition of MortgageBanc.

Fairway denied wrongdoing, saying regulators “did not identify any evidence of redlining or other discrimination,” and accused the government of acting in “bad faith” by characterizing Fairway’s actions as intentional, willful and reckless.

“Fairway vigorously defended itself against the government agencies’ allegations and continues to deny that the company engaged in any discriminatory behavior,” Fairway said in a statement in October.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 11, 2025 | Industry, News Feed

The Trump administration is seeking to cut 90 percent of the CFPB’s workforce, and has dismissed about 20 active enforcement cases and moved to vacate or weaken several finalized settlements.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The Consumer Financial Protection Bureau’s enforcement division will be under new leadership for the third time during the Trump administration after acting director Cara Petersen resigned Tuesday, saying in a farewell email that “the bureau’s current leadership has no intention to enforce the law in any meaningful way.”

The Trump administration is seeking to cut 90 percent of the CFPB’s workforce and has put the brakes on about 20 active enforcement cases, Bloomberg Law said in breaking the story of Petersen’s departure.

The New York Times, which also obtained Petersen’s farewell email, said she took over as the acting head of enforcement after her predecessor, Eric Halperin, resigned in February.

Petersen has worked at the CFPB since it was created in the wake of the 2007-2009 financial crash and Great Recession.

“I have served under every director and acting director in the bureau’s history and never before have I seen the ability to perform our core mission so under attack,” Petersen wrote to her colleagues.

“It has been devastating to see the Bureau’s enforcement function being dismantled through thoughtless reductions in staff, inexplicable dismissals of cases, and terminations of negotiated settlements that let wrongdoers off the hook.”

The CFPB did not respond to Bloomberg Law’s request for comment.

Under the leadership of acting Director Russell Vought and Chief Legal Officer Mark Paoletta, the CFPB has not only halted active enforcement cases, but moved to vacate or weaken several finalized settlements, Bloomberg Law reported.

The CFPB’s unprecedented attempt to undo a settlement in a fair lending case that the government reached with a Chicago mortgage broker last year would establish a “dangerous and destabilizing precedent” if granted, according to fair housing and consumer protection groups opposing the move in court. The judge in that case hasn’t ruled on the CFPB’s request.

Last month the CFPB knocked nearly $2 million off of a fine that international remittance company Wise had agreed to pay to resolve claims that it advertised inaccurate fees and failed to properly disclose exchange rates and other costs.

Although Wise is still on the hook to pay $450,000 to about 16,000 consumers who were allegedly overcharged, it will pay a revised fine of $45,000, rather than the $2.025 million that it had originally agreed to pay in a consent order.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 9, 2025 | Industry, News Feed

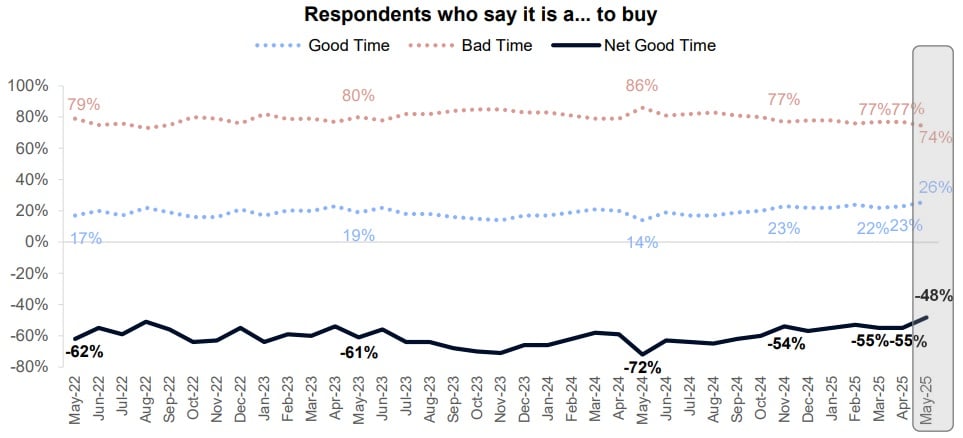

While just 26 percent of Americans said May was a good time to buy, that’s up from 23 percent in April and 14 percent a year ago, an all-time low in Fannie Mae survey.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Consumer sentiment about the housing market improved in May to the highest level since November as Americans became more optimistic about buying and selling conditions and the prospects for mortgage rates to come down in the year ahead.

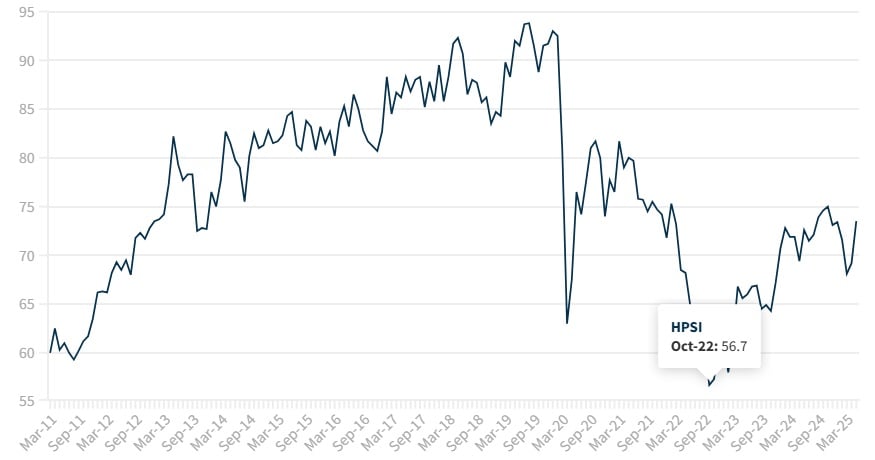

Fannie Mae’s latest National Housing Survey, released Monday, showed five of six components of the mortgage giant’s Home Purchase Sentiment Index (HPSI) improved in May.

Consumer sentiment has been trending down this year, in part due to fears about the impact of the Trump administration’s tariff policies, but the economy continues to do better than surveys suggest, economists say.

Fannie Mae Home Purchase Sentiment Index

At 73.5, the HPSI was up 4.3 points from April to May, surpassing the previous 2025 high of 73.4 seen in January.

The HPSI — which hit an all-time low of 56.7 in October 2022 in records dating to 2011 — distills six questions from Fannie Mae’s monthly National Housing Survey into a number.

The latest survey, which was fielded from May 1 through May 20 to 1,345 household decision makers, found that while most Americans still think it’s not a good time to buy, sentiment is improving.

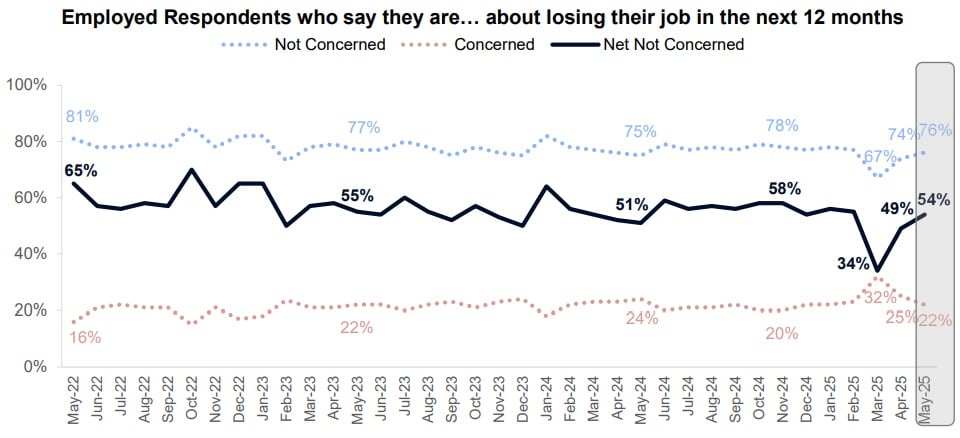

With Americans also less worried about losing their jobs in May, the only HPSI component that didn’t improve was household income.

While only 26 percent of household decision-makers said May was a good time to buy, that’s up from 23 percent in April and 14 percent a year ago — an all-time survey low.

With the share who said May was a bad time to buy falling from 77 percent in April to 74 percent in May, the net share of consumers who said it was a good time to buy increased by seven percentage points, to -48 percent.

More than two-thirds of consumers surveyed (68 percent) said they’d buy rather than rent if they were going to move, up from 65 percent in April.

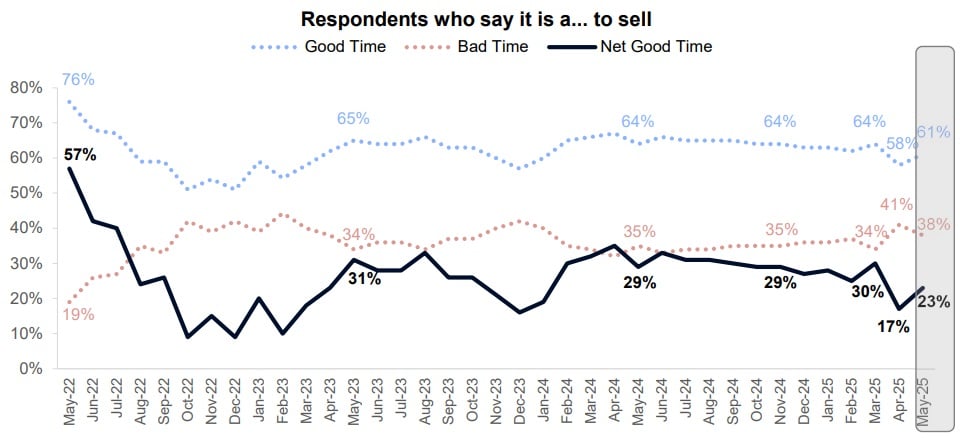

Most consumers (61 percent) said May was a good time to sell, up from 58 percent in April but down from 64 percent a year ago. With the share who said it was a bad time to sell falling from 41 percent in April to 38 percent in May, the net share of consumers who said May was a good time to sell increased by six percentage points, to 23 percent.

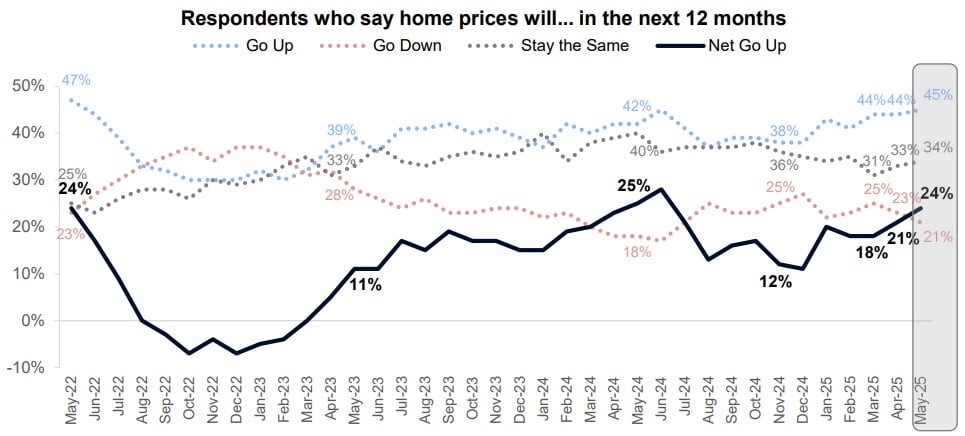

With more consumers convinced that prices are headed up in the next 12 months (45 percent) or that they’ll stay the same (34 percent), the net share of consumers who expect prices to go up rose three percentage points, to 24 percent.

While many would-be homebuyers are hoping prices come down, Fannie Mae’s HPSI treats expectations of price increases as a positive, since it shows consumers aren’t worried about prices crashing.

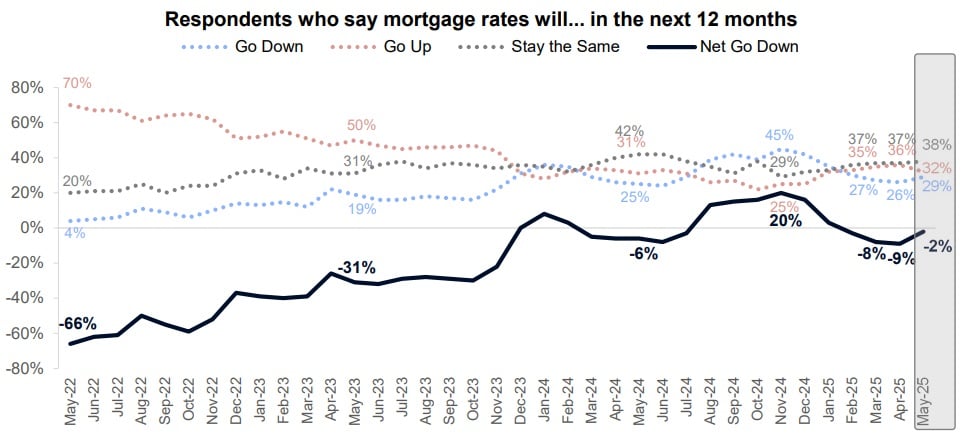

Most consumers surveyed in May said they expect mortgage rates to either stay the same over the next 12 months (38 percent) or go down (29 percent).

With the share who expect rates to go up falling from 36 percent in April to 32 percent in May, the net share expecting rates to go down improved by seven percentage points, to -2 percent.

Last month, Fannie Mae economists said they expect mortgage rates to come down by a full percentage point by the end of next year. Forecasters at the Mortgage Bankers Association have issued a more cautious take.

MBA forecasters predict mortgage rates will still be averaging 6.6 percent during Q4 2025 and 6.3 percent during Q4 2026.

Only one in five employed respondents surveyed in May (22 percent) said they were worried about losing their job in the next 12 months, down from 25 percent in April and a 2025 high of 32 percent in March.

With 76 percent of employed consumers saying they weren’t concerned about losing their job, the net share who said they weren’t concerned about being unemployed increased by five percentage points, to 54 percent.

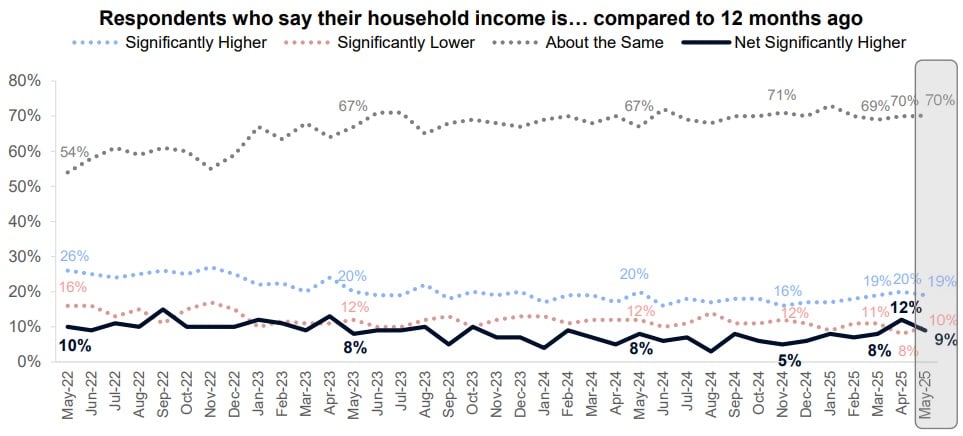

Most consumers surveyed in May (70 percent) said their household income is about the same as it was 12 months ago. But 10 percent said it was significantly lower, up from 8 percent in April, but down from 12 percent a year ago.

The net share of consumers who said their income was higher than 12 months ago fell three percentage points from April to May, to 9 percent.

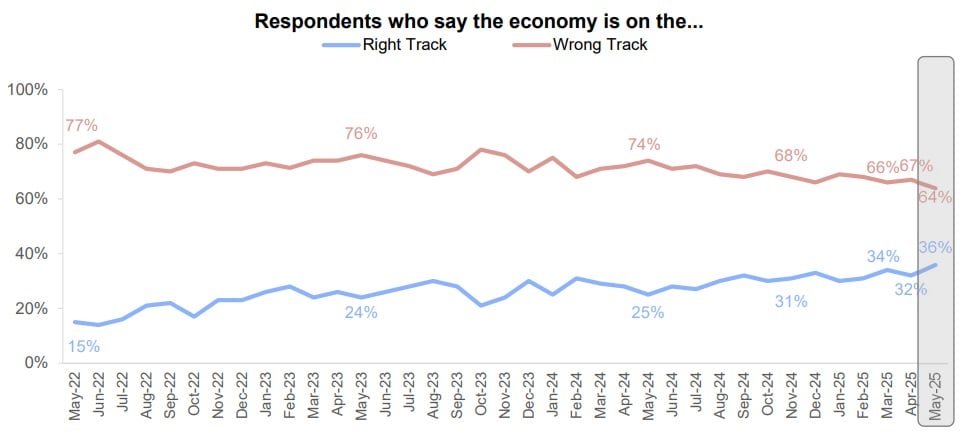

Although not factored into the HPSI, the National Housing Survey asks household decision-makers if they think the economy is on the right or the wrong track.

While most consumers thought the economy was on the wrong track in May (64 percent), that’s down from 67 percent in April and 74 percent a year ago.

Email Matt Carter

by Matt Carter | Jun 6, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Senate Democrats have questions and concerns about the Trump administration’s plans to restructure mortgage giants Fannie Mae and Freddie Mac — and are asking their federal regulator to put any action to privatize them or take them public on hold.

In a letter to Federal Housing Finance Agency (FHFA) Director Bill Pulte Thursday, lawmakers asked for assurances that changes in the works at Fannie and Freddie won’t “put investor profits over the homes of millions of Americans” and drive mortgage rates up.

READ INMAN’S FEDERAL HOUSING FINANCE AGENCY FAQ

“As FHFA Director, you have a duty to ensure the safety and soundness of [Fannie and Freddie], and a decision of this magnitude cannot be made on a whim without Congressional consultation and approval,” lawmakers said.

The five-page letter — signed by 14 Senate Democrats, including ranking Banking Committee member Elizabeth Warren and Senate Minority Leader Chuck Schumer — sought more information about the status of plans to reorganize Fannie and Freddie by June 18, 2025.

An FHFA spokesperson said in a statement to Inman that the agency is “studying how, if the President elects to take Fannie and Freddie public, it can be done in the safest and soundest manner, which includes keeping them in conservatorship. In any scenario, we will ensure the MBS [mortgage-backed securities] market is safe and sound and that there is no upward pressure on rates.”

Fannie and Freddie were placed in government conservatorship in 2008 under financial strains generated by the 2007-2009 housing crash and the Great Recession. The companies don’t make loans themselves, but play a vital role in keeping mortgage rates down by guaranteeing that MBS investors who fund most U.S. home loans get paid even when homeowners have trouble making their loan payments.

While Trump took steps during his first administration to release the mortgage giants from the government’s control, disagreements over how the companies would be structured have kept the “government-sponsored entities,” or GSEs, in limbo.

Advocates of privatizing Fannie and Freddie have always expected that it would entail the government divesting itself of its ownership in the companies and releasing them from conservatorship. The Trump administration has hinted at a different path that could involve taking the companies public while maintaining the FHFA’s tight control over their business.

Restructuring Fannie and Freddie without privatizing them might keep mortgage rates from climbing, but could also leave taxpayers on the hook if the companies run into trouble again.

In a May 28 appearance on CNBC, Pulte noted that in one recent social media post, Trump “very explicitly says that he wants to take them public. He did not say that he wants to privatize them.”

Treasury Secretary Scott Bessent has acknowledged that the government might even put its considerable stake in the companies in a sovereign wealth fund. In theory, Fannie and Freddie could generate revenue for the government.

“The reason they’re talking about this is they need the cash in order to make their tax cuts and their budget reconciliation bill work,” Whalen Global Advisors LLC Chairman Christopher Whalen told Yahoo Finance on May 22.

Shares in Fannie and Freddie gained more than 40 percent after Trump first posted to social media on May 21 that the companies “are doing very well, throwing off a lot of CASH, and the time would seem to be right” to take them public.

But Fannie and Freddie shares have since given up some of those gains, as it dawned on investors that the Trump administration might be more intent on tapping the companies as a source of revenue than privatizing them.

After Trump posted to Truth Social on May 27 that the government intended to maintain an implicit guarantee of Fannie and Freddie’s obligations, some Fannie and Freddie investors got cold feet and sold their shares.

A June 3 Bloomberg News story that confirmed the mortgage giants might remain in conservatorship — and perhaps be used to generate revenue to pare down the deficit — accelerated the selloff in Fannie and Freddie.

Ackman’s case for forgiveness

If the Trump administration wants to use Fannie and Freddie to generate revenue instead of privatizing them, that might come at the expense of existing investors, whose shares have traded on an over-the-counter exchange since being delisted by the New York Stock Exchange in 2010.

That includes billionaire Bill Ackman’s hedge fund management company, Pershing Square Capital Management, which holds significant stakes in both companies.

The worst-case scenario for existing investors is that the government converts its senior preferred shares in the companies into common stock, massively diluting the value of existing stockholders’ shares.

In a lengthy June 3 post on X, Ackman called the “notion that the Trump administration would act in a manner to wipe out [existing Fannie and Freddie] investors for an uncertain and likely suboptimal outcome … extremely unlikely.”

Ackman argues that the government would come out ahead if it simply cancelled the $348.2 billion Fannie and Freddie would currently be required to pay to buy back their preferred shares under terms established in 2008.

Cancelling Fannie and Freddie’s balance sheet liabilities would not be a gift to existing shareholders, Ackman maintains, because the mortgage giants never got credit for $301 billion in payments they made to the government when the Treasury was sweeping all of their profits into government coffers.

If the government instead tried to convert its preferred shares into common stock, Fannie and Freddie would have difficulty raising money from the private sector, Ackman argued — and face a flood of lawsuits from existing investors that would delay their exit from conservatorship.

Ackman complained that the media “often depicts Pershing Square as having wealthy investors,” but noted that the company manages funds on behalf of thousands of small shareholders as well as pension funds and others that invest on behalf of retirees and other small investors.

“While the press and some politicians attempt to portray the [potential release of Fannie and Freddie] from conservatorship as a windfall for the rich, the vast majority of the value created here will go to small investors,” Ackman claimed.

Depending on what the Trump administration has in mind for the mortgage giants, it may not be required to obtain Congressional approval.

Moody’s Chief Economist Mark Zandi said Monday that the most likely outcome is that the Trump administration keeps Fannie and Freddie in conservatorship so mortgage rates don’t go up.

Zandi said he’d like to see Fannie and Freddie chartered as government corporations with an explicit guarantee, which would help keep mortgage rates low.

Real estate industry groups like the National Association of Realtors and the Mortgage Bankers Association have proposed a “utility-style” model for Fannie and Freddie that would provide an explicit guarantee while limiting their risks and profits.

But because Congress would have to pass legislation approving such a model, there’s virutally no chance of that happening, Zandi said.

Trump has a tight grip on Fannie and Freddie

The Trump administration gained tight control over Fannie and Freddie after Pulte, grandson of PulteGroup founder William J. Pulte, fired 14 board members and made himself the chair of both companies in March.

Pulte has issued dozens of orders out of the public eye, eliminating programs and policies intended to boost lending in minority communities, protect borrowers from unfair or deceptive practices, and assess risks associated with climate change.

New appointees to the mortgage giants’ boards include banker and investor Omeed Malik — dubbed “MAGA world’s premier financier” and a “close friend” of Donald Trump Jr. by New York Magazine — as well as former Pulte Group division president Mike Stucky and Brandon Hamara Hamara, vice president of land acquisition at homebuilder Tri Pointe Homes Inc.

Senate Democrats have questioned the legality of Pulte’s Fannie and Freddie board purges and his right to serve as chair of the companies.

In their June 5 letter to Pulte, lawmakers wanted to know what the timeline was for privatizing or restructuring Fannie and Freddie, and whether the FHFA has met with Ackman or any other GSE shareholders.

“To our knowledge, neither FHFA nor the Administration have produced a study on the impact that releasing [Fannie and Freddie from conservatorship] would have on safety and soundness, mortgage rates, or the housing market and financial system more broadly,” Senate Democrats said.

The Trump administration “has also not released any information indicating whether the [GSEs] financial positions would make it feasible to take them public, including by relisting their common and preferred stock, or what taking them public would entail,” lawmakers complained.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter