In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

A federal judge has put a temporary hold on the Trump administration’s move to fire all but 200 of the Consumer Financial Protection Bureau’s 1,700 employees, saying she has yet to weigh the merits of a lawsuit challenging the legality of dismantling the bureau.

Layoff notices went out Thursday to more than 1,500 CFPB employees, as an “approximately 200-person agency allows the bureau to fulfill its statutory duties and better aligns with the new leadership’s priorities and management philosophy,” CFPB Chief Legal Officer Mark Paoletta said in a court filing Friday.

Paoletta said employees who received layoff notices Thursday “are still CFPB employees for 60 days” and that the bureau “will continuously assess … workforce needs and assess and adapt and make appropriate changes to ensure compliance with statutory duties and account for changing circumstances.”

U.S. District Judge Amy Berman Jackson, who is presiding over the case that could determine the CFPB’s fate, issued a temporary restraining order Friday halting the layoffs, pending an April 28 evidentiary hearing.

“I’m willing to resolve it quickly, but I’m not going to let this RIF [reduction in force] go forward until I have,” Jackson said during a hearing, as reported by the Associated Press.

A union representing many of the CFPB’s staff sued Acting Director Russel Vought on Feb. 9, challenging what it characterized as the Trump administration’s “ongoing effort to dismantle the CFPB.” Consumer groups, including the National Consumer Law Center and the NAACP, joined the legal battle, and attorneys general of 13 states and the District of Columbia also filed an amicus brief seeking to forestall mass layoffs.

Jackson put layoffs of 1,200 CFPB workers on hold in a Feb. 19 temporary restraining order. But a three-judge panel from the U.S. Court of Appeals for the District of Columbia Circuit on April 11 ruled the Trump administration could lay off workers it had determined through a “particularized assessment” were not needed to perform duties mandated by Congress.

Trump administration details cuts

The CFPB provided that assessment to Jackson on Friday — the day after the layoff notices went out. In a five-page declaration, Paoletta detailed the cuts to be made in each of the bureau’s departments and why those workers were no longer needed.

Paoletta also submitted a memo that he sent to all CFPB staff on April 16, detailing the Trump administration’s supervision and enforcement priorities for the bureau.

Mark Paoletta

“The Bureau will focus its enforcement and supervision resources on pressing threats to consumers, particularly service members and their families, and veterans,” Paoletta said in the memo. “To focus on tangible harms to consumers, the bureau will shift resources away from enforcement and supervision that can be done by the states.”

Paoletta said in his court declaration Friday that the CFPB’s single biggest department, the supervision and enforcement division, will be cut from 487 employees to 50, as most of its workers no longer needed under the Trump administration’s new priorities, Paoletta said.

In his April 16 memo, Paoletta called for the supervision and enforcement division to “decrease the overall number of ‘events’ by 50 percent” with a focus on “conciliation, correction, and remediation of harms subject to consumers’ complaints” and “collaborative efforts with the supervised entities to resolve problems so that there are measurable benefits to consumers.”

The CFPB’s Operations Division of 323 employees performs duties “not required by statute” and will be cut to 30 employees, Paoletta said in his declaration.

The Research Monitoring and Regulations Division includes the Office of Service Members Affairs, the Office of Financial Protection for Older Americans, and the Office of the Private Education Loan Ombudsman.

While those offices perform duties mandated by Congress, Paoletta said he determined “that the statutory duties of each [office] could be performed by one person.” The division’s current staff of 230 employees will be reduced to 22.

Similarly, the CFPB Director’s Office includes the Office of Minority and Women’s Inclusion and the Office of Fair Lending and Equal Opportunity, which enforces the Truth in Lending Act (TILA) and Home Mortgage Disclosure Act (HMDA). Although those duties “are required by statute,” Paoletta said he determined “that the statutory functions of each of these offices could be performed by one person” and staffing in the Director’s Office will be cut from 86 employees to five.

The CFPB’s Consumer Response and Education Division of 149 employees will also be cut “substantially,” as the bureau “retains dozens of contractors to field consumer complaints,” Paoletta said.

Now that the Trump administration has provided a “particularized assessment” of why the employees it intends to fire are not needed to perform duties mandated by Congress, Judge Jackson will hear arguments to the contrary.

Lauren Saunders

“Congress created the CFPB to address the gaps that allowed nonbank mortgage lenders, student lenders, payday lenders and other nonbank companies to escape accountability,” Lauren Saunders, associate director of the National Consumer Law Center, said in a statement. “The CFPB cannot simply shirk the consumer protection responsibilities Congress gave it and expect states to enforce federal law.”

In his April 16 memo, Paolleta said the bureau will shift its focus away from nonbank lenders and “focus on the largest banks and depository institutions.”

“Nonbanks’ shoddy business practices were a significant driver of the financial crisis of 2007, causing millions of people to lose their homes, jobs and savings,” Saunders said. “By focusing solely on large banks, and ignoring the statutory mandate to supervise nonbanks and enforce the law across its entire jurisdiction, this Administration is clearing the way for unscrupulous companies to once again violate the law and take advantage of ordinary people.”

DOGE staffer allegedly drove layoff process

How rigorously the CFPB analyzed the duties of the workers to be fired is another area of contention.

A CFPB employee who was part of the “reduction in force” (RIF) team claimed in a court declaration Friday that the team was managed by a Department of Government Efficiency (DOGE) employee who “kept the team up for 36 hours straight to ensure that the notices would go out” Thursday and “was screaming at people he did not believe were working fast enough to ensure they could go out on this compressed timeline, calling them incompetent.”

The anonymous employee’s declaration — filed by attorneys representing the CFPB’s union employees — also claimed members of the team expressed concerns that “there was a court order requiring that they do a particularized assessment, but they were told that all that mattered was the numbers.”

“The direction to ignore the concern came from Mark Paoletta, who said that the numbers-based RIF should move forward, and that leadership would assume the risk,” the employee claimed.

The CFPB did not respond to Inman’s requests for comment.

Paoletta was appointed by President Trump in November as the Office of Management and Budget’s general counsel. In that role — which remains his full-time job — Paoletta was expected to “work closely” with DOGE “to cut the size of our bloated government bureaucracy, and root out wasteful and anti-American spending,” Trump said in an announcement.

After the November election, DOGE cheerleader Elon Musk posted on his social media platform, X, that the Trump administration should “Delete CFPB. There are too many duplicative regulatory agencies.”

Consumer groups and Democrats who support the CFPB have pointed out that Musk’s plans to provide a mobile payment service through X would be regulated by the CFPB.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Mortgage rates are climbing back toward 7 percent on fears that tariffs could reignite inflation, but Federal Reserve Chairman Jerome Powell warns policymakers would be challenged if unemployment also rises.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Homebuyer demand for mortgages sagged last week as mortgage rates climbed back toward 7 percent on fears that tariffs will fuel inflation, and Federal Reserve Chairman Jerome Powell warned Wednesday that policymakers are also concerned that more Americans will be unemployed.

Stagflation — high inflation coupled with stagnant economic growth and elevated unemployment — hasn’t been seen since the 1970s. But that’s a situation the Fed is contemplating now, Powell said after delivering an address to The Economic Club of Chicago.

“Most of the time when the economy is weak, inflation is low and unemployment is high — and both of those call for lower interest rates to support activity and vice versa,” Powell said. “Now the labor market is still strong, but the shock that we’re experiencing … [is generating fears of] higher unemployment and higher inflation. And you know, our tool only does one of those two things at the same time. So it’s a difficult place for central banks to be in in terms of what to do.”

Major stock indexes were down Wednesday as investors digested Powell’s remarks, with the tech-heavy Nasdaq index falling 3 percent.

But increased demand for Treasurys and mortgage-backed securities helped bring rates down slightly, with yields on 10-year Treasurys falling four basis points.

Applications for purchase mortgages fell by a seasonally adjusted 5 percent last week when compared to the week before as mortgage rates climbed, Mortgage Bankers Association (MBA) Chief Economist Mike Fratantoni said in a statement.

Mike Fratantoni

“Mortgage rates moved 20 basis points higher last week, abruptly slowing the pace of mortgage application activity,” Fratantoni said, noting requests to refinance were down even more sharply, falling 12 percent from the week before.

Looking back a year, the MBA’s weekly survey of lenders showed demand for purchase mortgages was still up 13 percent, and applications to refinance were up 68 percent.

Mortgage rates on the rebound

After retreating to a 2025 low of 6.48 percent on April 8, rates on 30-year fixed-rate conforming mortgages bounced back to 6.89 percent last week, according to rate lock data tracked by Optimal Blue.

Rates on jumbo mortgages exceeding Fannie Mae and Freddie Mac’s $806,500 conforming loan limit in most markets spiked to 7.34 percent Monday but have dropped back below 7 percent.

“Given the jump in rates, more borrowers are opting for the lower initial rates that come with an ARM [adjustable-rate mortgage],” Fratantoni said.

Close to one out of 10 mortgage applications (9.6 percent) that came in last week were for ARM loans — the highest since November 2023, the MBA said.

Because borrowers who need bigger loans are even more likely to opt for an ARM, close to one-fourth (24.6 percent) of loan requests by dollar volume were for ARM loans.

The average ARM loan request was for $1.06 million, compared to $346,000 for fixed-rate loans.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Congressional Democrats are questioning the legality of the Trump administration’s purge of Fannie Mae and Freddie Mac’s boards, in which the newly appointed head of their federal regulator — housing scion Bill Pulte — was installed as the chair of both companies.

In an April 15 letter to the inspector general who oversees Fannie and Freddie’s regulator, 10 prominent Senate Democrats also asked for more details on “abrupt and sizable” workforce reductions at the Federal Housing Finance Agency (FHFA) and the recent firing of more than 100 Fannie Mae employees accused of fraud.

The grandson of PulteGroup Inc. founder William J. Pulte, Pulte was confirmed by the Senate on March 13 as Trump’s nominee to lead the FHFA. Four days later, the FHFA sent 14 members of Fannie and Freddie’s boards packing and named Pulte the chair of both boards.

Elizabeth Warren

Senate Banking Committee ranking members Andy Kim and Elizabeth Warren on Tuesday asked FHFA Inspector General Brian Tomney to determine “whether or not FHFA leadership complied with all relevant federal laws, regulations and agency policies and procedures in its decision making.”

Brian Tomney

Tomney, who has served as the FHFA inspector general since 2022, wasn’t targeted in the Trump administration’s removal of at least 18 inspector generals, which some Democrats say were illegal.

The letter — also signed by Democrats Tina Smith, Chuck Schumer, Cory Booker, Raphael Warnock, Catherine Cortez Masto, Lisa Blunt Rochester and Kirsten Gillibrand — asked Tomney to assess if workforce reductions at the agency will affect its ability to fulfill its oversight role.

Rep. Maxine Waters, the top-ranking Democrat on the House Financial Services Committee, was even more blunt in an April 7 letter to Pulte himself, accusing him of having “broken the law by illegally appointing yourself as chairman” of Fannie and Freddie’s boards.

Maxine Waters

Waters slammed FHFA’s subsequent move to rein in Fannie and Freddie programs aimed at boosting lending in minority communities, saying it “will limit access to lending for first-time homebuyers and other borrowers who have been historically locked out of the market due to systemic and overt discrimination.”

The FHFA, which has been relying primarily on its own and Pulte’s X accounts for media communications, did not respond to Inman’s requests for comment.

Bill Pulte

In an April 9 appearance on Fox News, Pulte said there is an “ongoing investigation” into the issues that led to the firing of more than 100 Fannie Mae employees. He said FHFA discovered “multiple people were working two jobs” — including some who were located in China — and that some employees had received kickbacks for charitable donations.

Waters also took issue with FHFA appointing its general counsel, Clinton Jones, to serve on both Fannie and Freddie’s boards, and demanded that Pulte supply the “names, titles, qualifications, and all business and non-business affiliations” of the other new board members.

Clinton Jones

Jones joined the FHFA in 2019 during the first Trump administration, and was promoted to general counsel in February 2021 — shortly after Biden took office.

The other new additions to Fannie and Freddie’s boards last month included Mike Stucky, a former Pulte Group division president; Tri Pointe Homes Inc. executive Brandon Hamara; and Ralph “Cody” Kittle, a partner at private equity firm RenWave Kore.

Omeed Malik

More recently, on Monday Pulte announced on X that banker and investor Omeed Malik — recently dubbed “MAGA world’s premier financier” by New York Magazine — is joining Fannie Mae’s board of directors.

Another new Fannie Mae board pick — Christopher Stanley, a staffer from the Department of Government Efficiency (DOGE) — resigned the day after his March 17 appointment.

But Democrats said this week they have ongoing concerns about DOGE’s role in running the FHFA during the second Trump administration.

In their letter to the FHFA inspector general, Senate Democrats asked for details on what access DOGE officials have to FHFA, Fannie and Freddie data, and whether DOGE officials were involved in the decision to purge the company’s boards.

Waters and Senate Democrats also want to know more about news reports of staffing reductions at FHFA and Fannie Mae.

We exceeded DOGE’s expectations at U.S. Federal Housing (FHFA), with an over 25% reduction in the Agency’s active workforce. We’re consolidating divisions to focus on building more homes and strengthening safety and soundness.

“Fannie Mae and Freddie Mac play a critical role in our nation’s mortgage market and collectively guarantee roughly 50 percent of home loans,” Senate Democrats said. “Clarity in [their] operations is therefore essential to the stability of the housing finance system.”

David Dworkin

National Housing Conference CEO David Dworkin, a centrist advocate for affordable housing stakeholders, last month called Jones “a highly respected regulator and policy expert” whose appointment to the mortgage giants’ boards “was reassuring to many who expressed concern over which senior FHFA staff would be retained.”

And while Dworkin said he’s not aware of another instance of a regulator assuming the chairmanship of a regulated board, as a practical matter, “the FHFA Director has been the de facto board chair of both companies since they were put into conservatorship in 2008.”

More recently, Dworkin said the National Housing Conference is working with Pulte and Trump’s Housing Secretary, Scott Turner, to further the Trump administration’s stated goals of lowering the cost of housing and expanding housing supply.

In an April 13 column, Dworkin said he recently met with Turner to discuss ways Opportunity Zones can help build more affordable housing, and using AI to simplify housing choice vouchers.

“We’ve also gathered dozens of the most knowledgeable and influential housing experts to discuss how to effectively recapitalize and release Fannie Mae and Freddie Mac from 16 years of conservatorship,” Dworkin said, in light of a proposal to create a U.S. sovereign wealth fund and seed it with the Treasury Departments warrants for Fannie and Freddie stock.

Dworkin said that to understand Pulte’s April 8 assertion that FHFA is “turning around Fannie Mae and Freddie Mac, slowly but surely,” it’s important to understand “the degree of regulatory supervision that has micromanaged nearly every business decision” at the companies at every level.

“It’s a common refrain from lenders that they cannot get timely answers to some of the most routine questions,” Dworkin wrote. “As Pulte moves to ‘run these companies like a business,’ he is moving regulatory supervision to the top as he prepares the companies for release from conservatorship. It’s easy to mistake the missive as pejorative, but in fact, he understands that you can’t run a business unless you match an employee’s responsibility with the appropriate amount of authority and accountability.”

Together, Fannie and Freddie employ more than 16,000 workers and generated 2024 profits totaling $28.9 billion, boosting their combined net worth to $154.3 billion.

To succeed in meeting Trump administration’s goals, Dworkin said, Pulte and Turner”will have to be disruptors of what has not worked, but they must do so without being disruptive of what does. That won’t be easy, and will require broad consultation with stakeholders at every step of the way, while moving forward at a deliberate pace.”

“If we get it wrong, we could do damage that could take a generation to recover from,” he concluded.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Experts surveyed by Fannie Mae expect national home prices to grow by 3.4 percent in 2025. Median list prices in 69 markets were down by 10 percent or more from a year ago in March.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Housing experts surveyed by Fannie Mae expect national home price appreciation to cool this year as inventories continue to swell, with dozens of local markets already seeing double-digit annual declines in median list price.

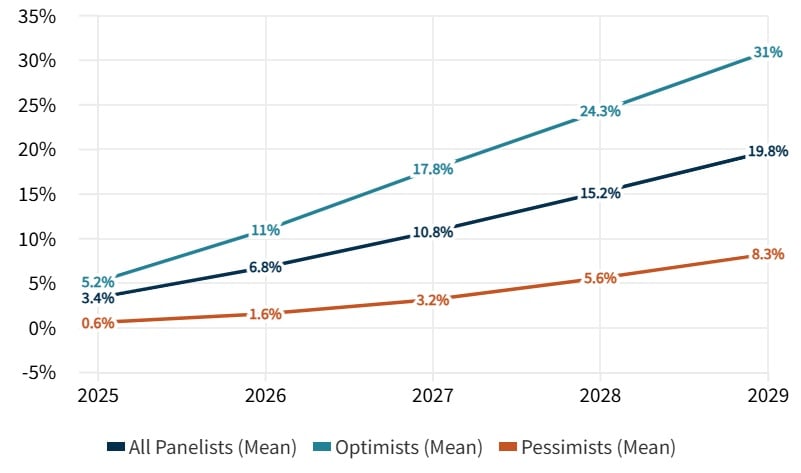

Fannie Mae’s latest Home Price Expectations Survey (HPES), released Tuesday, showed more than 100 housing and mortgage industry experts expect home price growth to slip to 3.4 percent in 2025, down from 5.8 percent last year.

The latest quarterly survey shows experts are less optimistic than they were in January, when they were forecasting 3.8 percent price appreciation in 2025.

The HPES panel expects price appreciation to continue to cool to 3.3 percent next year, down from the 3.6 percent forecast for 2026 issued in January.

But the most pessimistic quartile of survey panelists sees national home price appreciation flattening to 0.6 percent this year and remaining weak until 2028.

While prices could go up more sharply in some markets, they’re also expected to fall in some metros where listings come onto the market faster than buyers can snatch them up.

At the national level, there were 1.75 million new and existing homes on the market in February, up 15 percent from a year ago, according to data tracked by the National Association of Realtors and the U.S. Census Bureau.

Inventory of new and existing homes

The inventory of existing homes grew by 17 percent, to 1.24 million, according to NAR data, while the number of new single-family homes on the market grew by 7 percent, to 500,000, the Census Bureau reported.

Realtor.com was tracking 1.3 million listings in March, up 17 percent from a year ago.

The latest readings from the S&P CoreLogic Case-Shiller Indices showed national home prices were up 4.1 percent from a year ago in January, with Tampa the only market in the 20-City index to see prices slip over that period, by 1.5 percent.

Nicholas Godec

But the second half of the year “told a different story,” S&P Down Jones Indices’ Nicholas Godec said in a press release, with only four of 20 cities — New York, Chicago, Phoenix and Boston — managing to “eke out” price increases during that period.

San Francisco posted the largest six-month decline at 3.4 percent, followed by Tampa at 3.2 percent, Godec said.

Selma Hepp, chief economist at Cotality (formerly CoreLogic), said flattening home price changes over the last six months “suggest further price deceleration is ahead.”

Selma Hepp

“While this year’s cold winter and large natural disasters play a role in dampening demand, falling consumer sentiment suggests potential homebuyers are wary of the short-term economic outlook and future inflation,” Hepp said in a March 30 report.

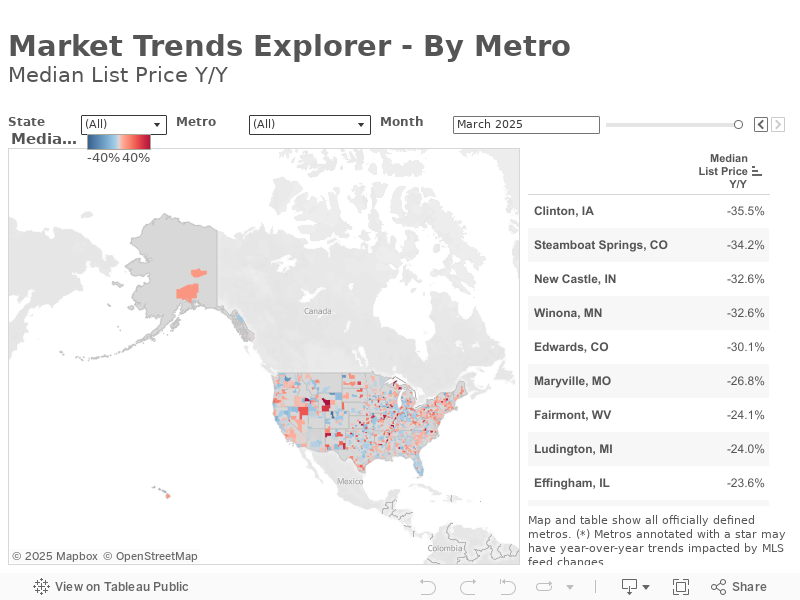

Home prices are driven by local supply and demand, and Realtor.com data shows median list prices in 69 metros were down by 10 percent or more from a year ago in March.

Median list price declines in 69 markets

Markets experiencing double-digit annual declines in median list price included Steamboat Springs, Colorado (-34.2 percent); Winona, Minnesota (-32.6 percent); Wenatchee, Washington (-22.1 percent); Flint, Michigan (-21.1 percent); Marion, Indiana (-19.7 percent); Enid, Oklahoma (-17.6 percent); Santa Fe, New Mexico (-14.5 percent); Ukiah, California (-13.7 percent); Dublin, Georgia (-13.4 percent); Montgomery, Alabama (-11.3 percent); Cedar Rapids, Iowa (-10.9 percent); Wausau, Wisconsin (-10.5 percent); and Boulder, Colorado (-10.2 percent).

“There are many ways to slice and dice housing data,” Realtor.com Chief Economist Danielle Hale said in her most recent weekly housing market update. “Through the lens of geography, our data reveals some commonalities.”

Danielle Hale

Realtor.com’s last Hottest Housing Markets report found that homes are selling more quickly in many markets in the Northeast and Midwest, and that a separate Down Payment Trends report showed buyers were putting more down on homes in the Northeast and Midwest and less in the South and West.

Last month, Fannie Mae economists said a pullback in mortgage rates should provide a “small boost” to home sales this year, in part because tariffs implemented by the Trump administration might inflate prices and slow economic growth. But tariffs announced this month have sent mortgage rates on the rebound, jeopardizing such forecasts.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Experts surveyed by Fannie Mae expect national home prices to grow by 3.4 percent in 2025. Median list prices in 69 markets were down by 10 percent or more from a year ago in March.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Housing experts surveyed by Fannie Mae expect national home price appreciation to cool this year as inventories continue to swell, with dozens of local markets already seeing double-digit annual declines in median list price.

Fannie Mae’s latest Home Price Expectations Survey (HPES), released Tuesday, showed more than 100 housing and mortgage industry experts expect home price growth to slip to 3.4 percent in 2025, down from 5.8 percent last year.

The latest quarterly survey shows experts are less optimistic than they were in January, when they were forecasting 3.8 percent price appreciation in 2025.

The HPES panel expects price appreciation to continue to cool to 3.3 percent next year, down from the 3.6 percent forecast for 2026 issued in January.

But the most pessimistic quartile of survey panelists sees national home price appreciation flattening to 0.6 percent this year and remaining weak until 2028.

While prices could go up more sharply in some markets, they’re also expected to fall in some metros where listings come onto the market faster than buyers can snatch them up.

At the national level, there were 1.75 million new and existing homes on the market in February, up 15 percent from a year ago, according to data tracked by the National Association of Realtors and the U.S. Census Bureau.

Inventory of new and existing homes

The inventory of existing homes grew by 17 percent, to 1.24 million, according to NAR data, while the number of new single-family homes on the market grew by 7 percent, to 500,000, the Census Bureau reported.

Realtor.com was tracking 1.3 million listings in March, up 17 percent from a year ago.

The latest readings from the S&P CoreLogic Case-Shiller Indices showed national home prices were up 4.1 percent from a year ago in January, with Tampa the only market in the 20-City index to see prices slip over that period, by 1.5 percent.

Nicholas Godec

But the second half of the year “told a different story,” S&P Down Jones Indices’ Nicholas Godec said in a press release, with only four of 20 cities — New York, Chicago, Phoenix and Boston — managing to “eke out” price increases during that period.

San Francisco posted the largest six-month decline at 3.4 percent, followed by Tampa at 3.2 percent, Godec said.

Selma Hepp, chief economist at Cotality (formerly CoreLogic), said flattening home price changes over the last six months “suggest further price deceleration is ahead.”

Selma Hepp

“While this year’s cold winter and large natural disasters play a role in dampening demand, falling consumer sentiment suggests potential homebuyers are wary of the short-term economic outlook and future inflation,” Hepp said in a March 30 report.

Home prices are driven by local supply and demand, and Realtor.com data shows median list prices in 69 metros were down by 10 percent or more from a year ago in March.

Median list price declines in 69 markets

Markets experiencing double-digit annual declines in median list price included Steamboat Springs, Colorado (-34.2 percent); Winona, Minnesota (-32.6 percent); Wenatchee, Washington (-22.1 percent); Flint, Michigan (-21.1 percent); Marion, Indiana (-19.7 percent); Enid, Oklahoma (-17.6 percent); Santa Fe, New Mexico (-14.5 percent); Ukiah, California (-13.7 percent); Dublin, Georgia (-13.4 percent); Montgomery, Alabama (-11.3 percent); Cedar Rapids, Iowa (-10.9 percent); Wausau, Wisconsin (-10.5 percent); and Boulder, Colorado (-10.2 percent).

“There are many ways to slice and dice housing data,” Realtor.com Chief Economist Danielle Hale said in her most recent weekly housing market update. “Through the lens of geography, our data reveals some commonalities.”

Danielle Hale

Realtor.com’s last Hottest Housing Markets report found that homes are selling more quickly in many markets in the Northeast and Midwest, and that a separate Down Payment Trends report showed buyers were putting more down on homes in the Northeast and Midwest and less in the South and West.

Last month, Fannie Mae economists said a pullback in mortgage rates should provide a “small boost” to home sales this year, in part because tariffs implemented by the Trump administration might inflate prices and slow economic growth. But tariffs announced this month have sent mortgage rates on the rebound, jeopardizing such forecasts.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.