by Matt Carter | Apr 23, 2025 | Industry, News Feed

Economic uncertainty, rate volatility and mounting worries about the labor market are reducing the pool of potential buyers, putting a damper on the spring homebuying season.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Economic uncertainty and rate volatility continue to put a damper on the spring homebuying season, with demand for purchase mortgages dropping by a seasonally adjusted 7 percent last week compared to the week before, the Mortgage Bankers Association reported Wednesday.

The MBA’s Weekly Applications Survey showed requests to refinance were down 20 percent last week when compared to the week before, but up 43 percent from a year ago.

Joel Kan

“Overall mortgage application activity declined last week, as rates increased to their highest level in two months,” MBA Deputy Chief Economist Joel Kan said in a statement. “The 30-year fixed rate rose for the second straight week to 6.9 percent, an almost 30-basis-point increase over two weeks.”

It was the second consecutive weekly decline in purchase loan applications, which dropped by a seasonally adjusted 5 percent during the week ending April 11.

Mortgage rates on the rebound

At 6.83 percent on Tuesday, rates on 30-year fixed-rate mortgages were 35 basis points higher than a 2025 low of 6.48 percent registered on April 8, according to rate lock data tracked by Optimal Blue. But mortgage rates have a ways to go before retracing the 2025 high of 7.05 percent seen Jan. 14.

Mortgage rates sank to historic lows during the pandemic, with borrowers locking in rates under 3 percent during much of 2020 and 2021.

After soaring to a post-pandemic high of 7.83 percent in October 2023, rates for 30-year fixed-rate mortgages gradually descended to a 2024 low of 6.03 percent on Sept. 17 as investors anticipated the Fed would start cutting rates.

Forecasters at Pantheon Macroeconomics say tariffs imposed by the Trump administration are lifting manufacturers’ costs, but disinflation in the service sector is likely to prompt the Federal Reserve to resume cutting short-term interest rates in June.

“The bond market sell-off since April 2 has pushed up typical yields on mortgage-backed securities by about 35 basis points, which is already feeding through to rates offered to prospective homebuyers,” Pantheon economists said Wednesday in their latest U.S. Economic Monitor. “Meanwhile, mounting worries about the labor market, evident in the recent consumer surveys, will reduce the pool of potential homebuyers further, especially if the jobs market weakens over the next few months.”

Pantheon forecasters expect the Fed to cut rates three times this year, by a total of 75 basis points.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 23, 2025 | Industry, News Feed

Nation’s largest loan servicer turned an $88 million Q1 profit and remains on track to be acquired by Rocket in Q4, a deal that’s prompted UWM to cut ties to Mr. Cooper.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Loan servicing giant Mr. Cooper saw the pool of loans it collects payments on shrink for the first time in two years during the first quarter — a trend that could continue into Q2 following a decision by the nation’s largest lender to pull its business.

While net income was down 57 percent from Q4, to $88 million, Mr. Cooper executives said first quarter results released Wednesday demonstrate the company’s ability to deliver “consistent, recurring and predictable results.”

Mr. Cooper remains on track to be acquired by Rocket Companies during the fourth quarter, a deal that the companies claim will create the industry’s leading integrated homeownership platform, Mr. Cooper Chairman and CEO Jay Bray said.

Jay Bray

“By pooling our talent, data and technology, we are going to totally reimagine the homeownership journey from start to finish, and harness the transformative power of AI to bring our customers a truly amazing experience for our investors,” Bray said on a call with investment analysts.

TAKE THE INMAN INTEL INDEX SURVEY FOR APRIL

Mr. Cooper is the nation’s largest mortgage loan servicer, collecting monthly payments from 6.5 million homeowners on behalf of lenders and investors in mortgage-backed securities, a business that generated $214 million in pre-tax income in Q1.

But Mr. Cooper’s pending $9.4 billion acquisition by Rocket Companies has ruffled the feathers of United Wholesale Mortgage, which famously won’t do business with mortgage brokers who work with rival Rocket Mortgage.

Bray is slated to become president and CEO of Rocket Mortgage when the deal closes, reporting to Rocket Companies CEO Varun Krishna. Rocket also has its sights set on acquiring real estate brokerage Redfin for $1.75 billion, a deal it says could save consumers $20,000 per transaction by unifying home search, buying, selling, mortgage, title and loan servicing.

UWM — which surpassed Rocket Mortgage as the nation’s largest mortgage lender in 2022 — pulled its subservicing contract with Mr. Cooper this month, and will no longer sell mortgage servicing rights to the Dallas-based loan servicer, UWM confirmed to Inman.

At the end of last year, UWM owned the servicing rights on 692,908 mortgages totalling $225.8 billion, a business that generated $636.7 million in income last year. It’s not clear how many of those borrowers were subserviced by Mr. Cooper.

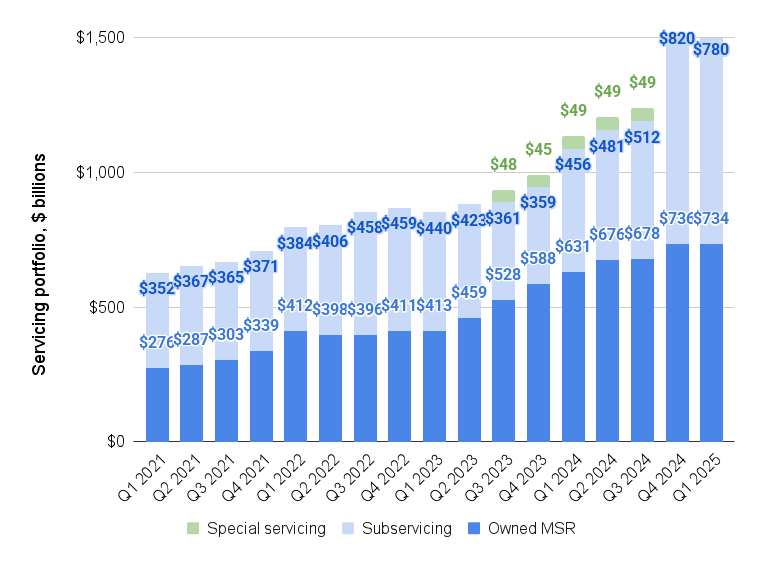

Aided by the $1.3 billion acquisition of Flagstar Bank’s servicing business last fall, Mr. Cooper ended the year with a $1.556 trillion mortgage servicing rights portfolio, up 57 percent from a year ago. That included $736 billion in owned mortgage servicing rights (owned MSRs) and $820 billion in subservicing Mr. Cooper performs for others.

Mr. Cooper’s $1.5T mortgage servicing portfolio

Even before UWM cut ties with Mr. Cooper, the loan servicer saw its subservicing portfolio shrink by $40 billion during the first quarter of 2024, to $780 billion.

Mr. Cooper President Mike Weinbach said the shrinkage was due to expected transfers of $60 billion in subservicing business that Mr. Cooper acquired from Flagstar to other servicers.

Mike Weinbach

“Outside of these de-boardings, our subservicing portfolio grew organically by 2 percent quarter over quarter,” Weinbach said on Wednesday’s earnings call. “We’re growing with our clients, which includes some of the strongest originators and investors in the industry.”

He said Mr. Cooper is in “advanced discussions with potential new clients and optimistic about winning new books of business.”

Mr. Cooper’s owned MSR portfolio also shrank by $2 billion during Q1, to $734 billion.

All told, Mr. Cooper was collecting payments on $1.514 trillion in loans as of March 31, down 3 percent from Q4 but up 33 percent from a year ago.

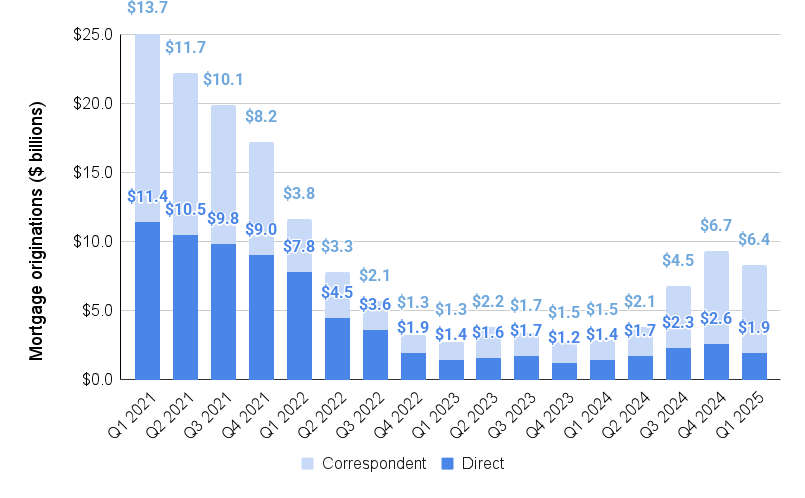

Mortgage originations down 10% from Q4 2024

Mortgage servicers are also in a good position to offer refinancing to borrowers, and Mr. Cooper funded 32,296 loans in the first quarter totaling $8.3 billion, down 10 percent from Q4 but up 186 percent from a year ago.

Most of the company’s mortgage originations ($6.4 billion) came through Mr. Cooper’s correspondent channel, which Weinbach said has benefited from “a number of investments and operational enhancements over the last 18 months.”

In the direct-to-consumer channel, Weinbach said Mr. Cooper enjoyed “very strong momentum” with cash-out refinancing, which made up 46 percent of the $1.9 billion in volume, and second liens, which accounted for another 21 percent of direct loans.

“During the quarter, we helped over 9,000 customers access equity in their homes, and helped nearly 2,000 customers reduce their monthly payments or purchase a new home,” Weinbach said.

Mr. Cooper sold its wholesale and non-delegated correspondent mortgage business to Ft. Lauderdale, Florida-based A&D Mortgage LLC, on April 1.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 22, 2025 | Industry, News Feed

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

The Trump administration’s attempt to undo a settlement in a fair lending case that the government reached with a Chicago mortgage broker just days before the November election is an “unprecedented” request that would establish a “dangerous and destabilizing precedent” if granted, according to fair housing and consumer protection groups opposing the move in court.

Under new leadership since the election, the Consumer Financial Protection Bureau has dropped at least nine pending consumer lawsuits, and the Trump administration is also embroiled in a court battle over its plans to fire all but 200 of the consumer watchdog’s 1,700 employees and hand many of its duties back to states.

But in seeking to vacate a settlement it reached with Townstone Financial Inc. and its owner, Barry Sturner, last year, the CFPB’s new leadership has taken the remarkable step of trying to undo an enforcement action the bureau achieved after more than four years of litigation.

TAKE THE INMAN INTEL INDEX SURVEY FOR APRIL

The motivation for undoing the settlement is not new information about the law or facts, as the CFPB claims, but boils down to a policy disagreement, 14 nonprofit fair housing and consumer protection groups alleged in an April 4 amicus brief opposing the move.

The “unprecedented relief” sought by the CFPB “would invite a host of similar docket clogging motions at the beginning of each new presidential administration, undermining public confidence in the finality of judicial orders and wasting the courts’ and agencies’ time rehashing old cases instead of addressing current controversies,” the groups said. “The parties point to no other case where a court anywhere in the country vacated a final judgment because incoming agency leadership disagreed with the decision to litigate the case leading to that judgment.”

The groups — including the National Fair Housing Alliance, the American Civil Liberties Union, the Consumer Federation of America and the National Consumer Law Center — were granted standing to file the amicus brief after the CFPB essentially switched sides in the case against Townstone.

Case filed during Trump’s first term

The CFPB sued Townstone in July 2020 — the final year of the first Trump administration, when the bureau was led by Trump appointee Kathy Kraninger.

Townstone was accused of broadcasting statements on an AM radio show and podcast that effectively discouraged Black residents from applying for loans.

In a 2016 episode, for example, Sturner allegedly said that between Friday and Monday, it’s “hoodlum weekend” on the South Side of Chicago, and that police are “the only ones between that turning into a real war zone and keeping it where it’s kind of at.”

The CFPB alleged that Black applicants accounted for only 1.4 percent of the 2,700 mortgage requests fielded by the mortgage broker in the Chicago market from 2014 to 2017, compared to 9.8 percent of applications taken by its competitors.

After more than four years of litigation, Townstone settled the case in November, agreeing to pay a $105,000 fine without admitting to or denying the allegations against it.

The proposed settlement was submitted for court approval on Nov. 1 — four days before the 2024 presidential election — and approved by the court on Nov. 7, two days after Trump was elected to a second term.

After Townstone paid the fine, the CFPB and attorneys for Townstone filed a motion to vacate the judgment, seeking not only a refund for Townstone but to revoke requirements that the company (or its successors) implement additional policies, procedures, education and training of employees to prevent discrimination for five years.

In their March 26 motion to vacate the settlement, attorneys for the CFPB claimed they’d uncovered evidence that Townstone was targeted “based on the political views of its owner,” and that that CFPB lawyers “misled their superior” — suggesting that Kraninger may have decided to proceed with the case based on incomplete or inaccurate information.

The CFPB also found fault with its investigators’ use of audio mining software to search Townstone’s radio show and podcasts, identifying 16 minutes out of nearly 79 hours of radio content that formed the heart of the case.

“CFPB abused its power, used radical ‘equity’ arguments to tag Townstone as racist with zero evidence, and spent years persecuting and extorting them – all to further the goal of mandating DEI in lending via their regulation by enforcement tactics,” CFPB Acting Director Russ Vought said in a March 26 press release.

But searching hours of publicly available audio programming for key terms is “certainly a more efficient use of government resources than having investigators listen to every episode in real time,” fair housing and consumer protection groups said in opposing the CFPB’s motion to vacate the settlement.

The information that CFPB lawyers were accused of omitting from a memo to Kraninger concerned case law that the attorneys may not have considered relevant, the groups said.

No ruling on First Amendment issues

While the CFPB maintained that the speech in question was not protected by the First Amendment because it was advertising, neither the trial court nor the appeals court weighed in on the First Amendment issues in the case.

Not in dispute is that Townstone employees made six “racially charged statements,” and that the case weighed on whether any or all of them would have discouraged a “reasonable [Black] person from making or pursuing” a mortgage loan, the consumer groups said in their amicus brief.

There are only six circumstances in which courts can undo a final judgement, the groups said, including “a mistake,” “newly discovered evidence,” and “fraud … misrepresentation, or misconduct.”

The CFPB is seeking to overturn the judgment under a catch-all provision, they said: “Any other reason that justifies relief.”

In an April 15 response, lawyers for the CFPB and Townstone said the bureau moved to vacate the settlement “not because of a change in leadership, but because it discovered that the Townstone case lacked any evidence of actual discrimination, lacked any actual consumers who complained about anything Townstone did, and was both brought and pursued because CFPB disliked Townstone’s speech.”

Vacating the settlement “will not open the floodgates to other efforts to vacate cases, unless those other efforts involve cases, such as this one, in which agencies have used baseless lawsuits to target individuals because of their speech,” CFPB lawyers said.

“Boiled down to its essence, CFPB’s case turned on an alleged statistical disparity in minority mortgage applications between Townstone and unknown (and unrevealed) ‘peer lenders’ and six statements that represented a mere 16 minutes out of 78 hours of total programming from Townstone’s radio show,” the CFPB now maintains.

“As the parties pointed out in their opening brief, a mere statistical disparity in applications is not actionable” under the Equal Credit Opportunity Act, CFPB lawyers said.

“The entire case was built on speech that CFPB lawyers did not like,” the CFPB now says. “That speech was not bigoted — it was, at worst, offensive.”

Even if it were, bigotry “is actionable only if it results in injury to a plaintiff; there must be a real link between the bigotry and an adverse … action,” CFPB attorneys said, citing a 2003 ruling by the Seventh Circuit Court of Appeals in Adams v. Wal-Mart Stores Inc.

At an April 8 hearing, U.S. District Court Judge Franklin Valderrama said he would consider the amicus brief filed by fair housing and consumer groups when deciding the CFPP’s motion to vacate the settlement and that the trial court “may set this matter for an in-person hearing following the review of the filings.”

Valderrama on March 26 granted Mark Paoletta and other attorneys representing the CFPB standing to appear before his court in Illinois, but minutes of the hearing noted that, “At this time, the case remains closed.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 21, 2025 | Industry, News Feed

Alliant National acquisition brings 700 independent title agents in 32 states to Dream Finders, which provided financing on 72 percent of the homes it built last year through subsidiary Jet HomeLoans.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Florida-based homebuilder Dream Finders Homes Inc. continues to build its presence in mortgage lending and title insurance through acquisitions, adding more than 700 independent title agents in 32 states with the acquisition of Alliant National Title Insurance Company Inc.

Alliant National President and CEO David Sinclair has joined Dream Finders along with the rest of his team, Dream Finders’ Chairman and CEO Patrick Zalupski said Monday. Terms of the deal, which closed on April 18, were not disclosed.

Patrick Zalupski

“This partnership creates significant value for both Alliant National and Dream Finders as a result of further vertical integration and additional service offerings to our stakeholders,” Zalupski said in a statement. “We are committed to investing towards the continued success of Alliant National’s platform and look forward to expanding our presence in the industry.”

TAKE THE INMAN INTEL INDEX SURVEY FOR APRIL

In announcing the deal in October, Dream Finders claimed Alliant National was the largest independent title underwriter in the country with no direct or affiliated operations.

David Sinclair

“Building on almost 20 years of serving independent title agents, we are thrilled to partner with Dream Finders Homes and envision an exciting future,” Sinclair said at the time. “The collaboration of an innovative builder, strong title agency, and the Alliant National underwriting team will promote our long-term success and growth into a national competitor.”

Dream Finders closed 8,583 new home sales last year, up 17 percent from the year before, providing financing and title services on most of those sales through its subsidiaries, Jet HomeLoans LLC and DF Title LLC.

Last month, Dream Finders announced that Jet HomeLoans had acquired Denver, Colorado-based Cherry Creek Mortgage. Based in Jacksonville, Florida, Jet HomeLoans sponsors 59 mortgage loan originators who work out of 10 branch locations, according to Nationwide Multistate Licensing System records.

Dream Finders went all-in on mortgage last year, acquiring the remaining 40 percent interest in its mortgage banking joint venture, Jet HomeLoans, for $9.3 million in July. It was the company’s sixth acquisition in five years.

Now a wholly owned subsidiary of Dream Finders, Jet HomeLoans originated 4,977 loans in 2024, up 56 percent from 3,189 the year before. The lender achieved a “capture rate” of 72 percent of all homes built by Dream Finders last year, up from 65 percent in 2023.

Jet HomeLoans made $4.98 billion in loans last year, an average of $441,230 per loan, with 40 percent of loans backed by government (FHA, VA and USDA) programs.

Dream Finders’ mortgage business generated $34.8 million in 2024 revenue — almost twice as much as title services revenue, which totalled $18.9 million last year. But title services revenue was up 95 percent from 2023, largely due to DF Title’s expansion of operations into the Texas market previously serviced by unconsolidated title joint ventures.

DF Title, which does business as Golden Dog Title & Trust, provides closing, escrow and title insurance services in Colorado, Florida, Georgia, North Carolina, South Carolina and Texas.

Dream Finders, which currently builds homes in 10 states, entered the Charleston and Greenville, South Carolina, and Nashville, Tennessee markets last year by acquiring the majority of the homebuilding assets of Crescent Homes. In January, Dream Finders entered the Atlanta, Georgia, market and expanded its footprint in Greenville with the acquisition of homebuilder Liberty Communities.

In reporting 2024 earnings in February, Dream Finders executives said they expect the Liberty Communities acquisition will help the company close on a projected 9,250 home sales this year, which would represent 8 percent growth.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 18, 2025 | Industry, News Feed

Offerpad’s market capitalization has dropped below $50 million for 30 consecutive trading days, and the New York Stock Exchange wants to know what it’s going to do about it.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Cash offer and renovation platform Offerpad Solutions Inc. has been put on notice by the New York Stock Exchange that it could be delisted from the exchange because its market capitalization has dropped below $50 million.

Offerpad informed investors on April 16 that it plans to submit a business plan within the next 45 days detailing how it will get back into compliance with the stock exchange’s listing standards within 18 months.

The April 10 compliance notification that Offerpad received from the New York Stock Exchange “has no immediate impact on the listing of the company’s Class A common stock,” the company said.

A spokesperson for Offerpad told Inman the notification is “a standard procedural matter” and that the company is confident in its ability to submit a compliance plan within the required timeframe.

“As we mentioned on our most recent earnings call, we have multiple pathways to success, and are actively executing on initiatives that support sustainable long-term growth,” Offerpad Chief of Staff and Vice President of Operations Cortney Read said in an email.

Over the past 12 months, shares in Offerpad have traded for as little as $1.36 and as much as $8.37. Friday’s closing price of $1.48 valued the company at $40.5 million.

TAKE THE INMAN INTEL INDEX SURVEY FOR APRIL

The compliance notification was triggered because Offerpad’s average global market capitalization fell below $50 million for 30 consecutive trading days.

With 27.38 million shares outstanding, Offerpad’s price per share would need to rebound to at least $1.83 for the company’s market capitalization to meet the $50 million threshold.

Assuming the New York Stock Exchange accepts its plan to regain compliance, Offerpad’s common stock will continue to be listed and traded on the exchange during the 18-month cure period.

Offerpad reported a $62.2 million 2024 net loss on Feb. 24 — a 47 percent improvement from the company’s $117 million in 2023 — and will release Q1 2025 earnings on May 5.

Rival iBuyer Opendoor is flirting with listing compliance issues on the Nasdaq exchange if its price per share remains below the exchange’s $1 minimum bid requirement.

Shares in Opendoor briefly dipped below $1 on April 1 and touched a 52-week low of $0.85 three days later, but bounced back to close at $1.09 on April 9. Shares in Opendoor were at $0.95 Friday, up 3 percent.

Shares in Fathom Realty’s parent company, Fathom Holdings, have also been trading below the $1 threshold since March 3, triggering a compliance warning from Nasdaq.

Fathom notified investors Friday that Nasdaq put it on notice on April 14 that it has until Oct. 13 to regain compliance with its bid price rule.

If shares in Fathom close at $1 or higher for at least 10 consecutive business days, it will be considered back in compliance. If shares in Fathom remain below $1, it could qualify for another 180-day reprieve and regain compliance through a reverse stock split, if necessary.

Fathom reported a $21.6 million 2024 net loss but finished the year with 14,300 agents — 2,505 more than it started with.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site