by Matt Carter | Apr 30, 2025 | Industry, News Feed

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

The nation’s largest mortgage lender is expanding its rivalry with Rocket Companies into the arena of loan servicing, but will have a lot of catching up to do with Rocket set to acquire the biggest servicer in the business, Mr. Cooper.

United Wholesale Mortgage (UWM) announced Wednesday that it’s signed a long-term agreement with ICE Mortgage Technology and will bring its loan servicing — the collection of monthly payments from borrowers — in-house.

Mat Ishbia

“This will mean a better experience for borrowers and a stronger, stickier relationship with their brokers, which we believe could result in more repeat business and referrals — the foundation for long-term growth and success,” UWM CEO Mat Ishbia said in a statement.

Rocket’s pending $9.4 billion acquisition of Mr. Cooper prompted UWM — which surpassed Rocket Mortgage as the nation’s largest mortgage lender in 2022 — to pull its mortgage subservicing contract with Mr. Cooper this month.

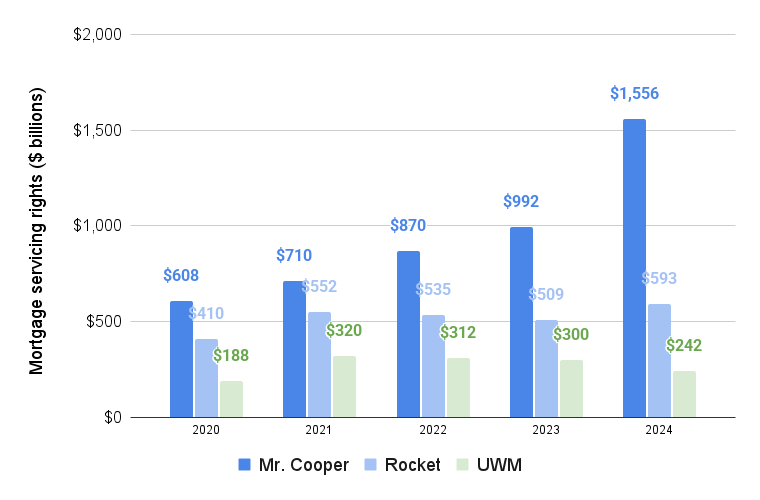

UWM, which famously won’t work with mortgage brokers who do business with Rocket, owned the servicing rights to 729,781 mortgages with a total outstanding balance of $242.4 billion at the end of the year — a business that generated $637 million in fee income in 2024.

UWM’s shrinking mortgage servicing portfolio

Mr. Cooper, Rocket Mortgage and UWM mortgage servicing rights (MSR) portfolios, including subservicing. Source: Company earnings reports.

Rocket and Mr. Cooper, by comparison, were together servicing (or subservicing) more than $2.15 trillion in mortgages at the end of the year — a combined portfolio nearly nine times larger than UWM’s.

Loan servicers collect monthly mortgage payments from borrowers on behalf of lenders or investors in mortgage-backed securities who own the loans. It’s an attractive business for many mortgage lenders, because the fees they can earn from loan servicing are a steady source of income that can even out ups and downs in home sales.

By maintaining close contact with borrowers, lenders who service their own loans are also in a better position to do repeat business with them when they’re ready to refinance or buy their next home.

Rocket claims that it “recaptures” 83 percent of its servicing clients when they’re ready to take out another loan. The Detroit-based lender’s client base is about to get a lot bigger, with Rocket setting its sights on acquiring not only Mr. Cooper but real estate brokerage Redfin for $1.75 billion.

Together, Rocket and Redfin attract 62 million visitors to their websites every month, while Rocket and Mr. Cooper’s combined client base of 9.5 million servicing customers represents opportunities for repeat business.

“Integrating Rocket’s originations-servicing recapture flywheel with Mr. Cooper’s servicing platform will drive down costs and improve the experience for the companies’ nearly 10 million combined clients,” company executives said in outlining the rationale for the deal.

Lenders who want to be in the loan servicing business can retain the mortgage servicing rights (MSRs) on the loans that they originate when they are bundled up into mortgage-backed securities (MBS) and sold to investors.

They can also acquire MSRs from other lenders who need the cash — or don’t want to be in the servicing business. Lenders who want to keep their MSRs but don’t want to service the loans can also contract with subservicers, as UWM has done in the past.

UWM’s MSR portfolio has been shrinking since 2021, as the Pontiac, Michigan-based lender sold servicing rights to raise money. As an example of one such deal, at the beginning of last year, UWM sold the MSRs on $70 billion in mortgages for $941.2 million.

Using tech to leverage economies of scale

Loan servicers benefit from economies of scale, as executives at Mr. Cooper have said of the company’s investment in AI and other technology to slash expenses. Two years ago, Mr. Cooper executives revealed the company was spending “several hundred million dollars a year” on call center operations, and expected to achieve $50 million in annual savings at the outset of a “multiyear” artificial intelligence project.

By partnering with ICE Mortgage Technology, UWM gets immediate access to what the companies claim is ICE’s “industry-leading MSP loan servicing system.”

UWM said it selected MSP “for the system’s powerful features, scalability and capacity to support outstanding customer service that fosters borrower retention, and the fact that ICE is an independent, neutral and proven technology provider.”

UWM will also employ ICE Servicing Digital, a homeowner portal with “retention and recapture features,” aimed at winning repeat business, and ICE Loss Mitigation, which helps homeowners facing hardship connect with assistance.

“While we are excited about the cost savings for UWM, we’re even more excited about the opportunity to help brokers deepen their relationships with borrowers by leveraging MSP,” Ishbia said.

Ben Jackson

ICE President Ben Jackson said in a statement that the company is “honored that UWM has entrusted us to supply the technology underpinning its new servicing strategy.”

It’s the second big tech partnership for UWM this month, following the announcement of a “strategic, industry-transformative agreement” to integrate Google Cloud AI and machine learning tools into UWM’s lending platform.

Interest rate risk

While mortgage servicing has been a profitable business for Mr. Cooper, it’s not without risks. Loan servicers are expected to help homeowners avoid foreclosure, a task that can prove demanding during economic downturns.

MSR portfolios are also sensitive to fluctuations in mortgage rates.

When interest rates go up, demand for purchase mortgages and refinancing often wanes. But MSRs become more valuable because borrowers are less likely to refinance and end up with another loan servicer.

When mortgage rates go down, loan servicers must often make adjustments to the fair value of their MSR portfolios, as borrowers are more likely to refinance and exit the portfolio.

Servicers who purchased MSRs during the pandemic era “have found themselves in the sweet spot, as mortgage holders remain reluctant to trade in low-priced loans,” outsourcing and advisory firm SitusAMC said in an analysis released Wednesday, “Mortgage Servicing Rights in 2025: Navigating Market Volatility.”

Mark Garland

The “million-dollar question” is where interest rates and mortgage origination volume will land over the next 12 to 18 months, SitusAMC executive Mark Garland said in a statement.

“Volume is everything,” Garland said. “Volume is going to be the issue that will keep people in the [loan servicing] business or drive them out.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 30, 2025 | Industry, News Feed

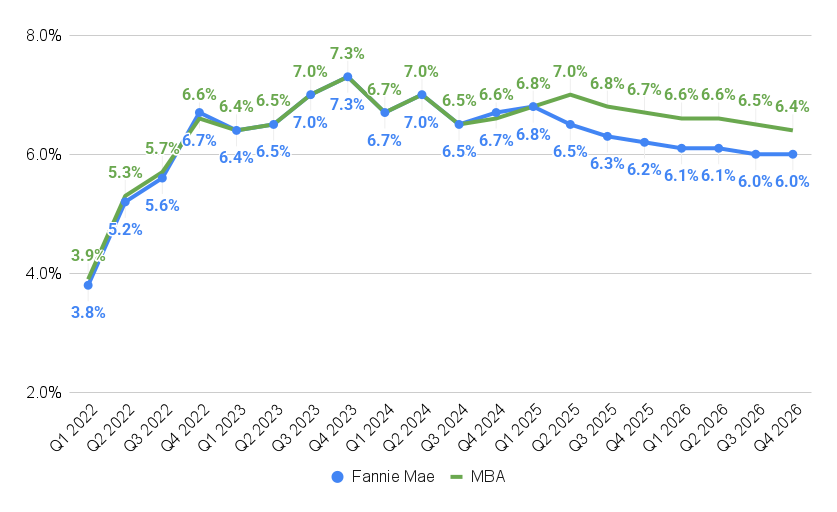

Slowing economy could also help bring mortgage rates down to Earth more rapidly, with the latest forecast predicting rates will drop to 6.2 percent by the end of this year and to 6 percent next year.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Incoming economic data has Fannie Mae economists expecting higher inflation and slower growth this year than they’d previously forecast in March.

The latest forecast envisions economic growth slowing to 0.5 percent this year, down from March’s forecast for 1.7 percent growth, and that annual inflation will rise to 3.5 percent by the fourth quarter.

TAKE THE INMAN INTEL INDEX SURVEY FOR APRIL

The commentary accompanying April’s forecast lacked the in-depth analysis Fannie Mae’s Economic and Strategic Research (ESR) Group provided in March and previous months.

But other economists and many consumers expect tariffs imposed or threatened by the Trump administration will push prices up and slow the economy down this year, heightening the probability of a recession.

Signs of a slowing economy could also help bring mortgage rates down to Earth more rapidly. Fannie Mae forecasters now expect mortgage rates to come down to 6.2 percent by the end of this year and 6.0 percent next year.

Mortgage rates expected to ease

Source: Fannie Mae and Mortgage Bankers Association forecasts, April 2025.

In March, forecasters at the mortgage giant weren’t expecting mortgage rates to hit 6.2 percent until the end of next year.

Economists at the Mortgage Bankers Association in an April 11 forecast projected mortgage rates will still be averaging 6.7 percent in Q4 2025 and 6.4 percent during Q4 2026.

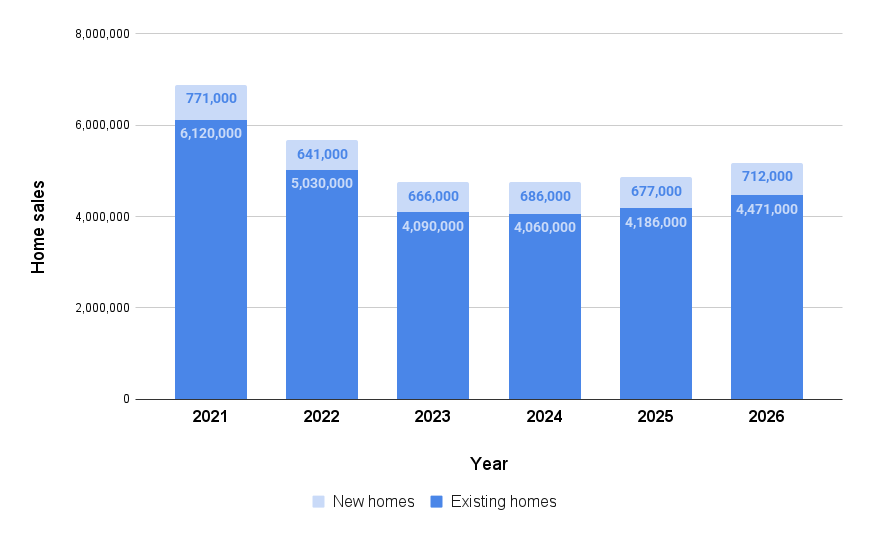

Home sales forecast revised down

Source: Fannie Mae housing forecast, April 2025.

Despite stronger than expected first quarter home sales, Fannie Mae economists revised their forecast for 2025 home sales to 4.86 million, down from 4.95 million in March.

While sales of existing homes are still expected to grow by 3 percent this year, to 4.186 million, Fannie Mae economists now expect sales of new homes will decline by 1 percent, to 677,0000.

A stronger rebound is still expected in 2026, with sales of new and existing homes expected to grow by 7 percent to 5.18 million and surpassing the 5 million mark for the first time since 2022.

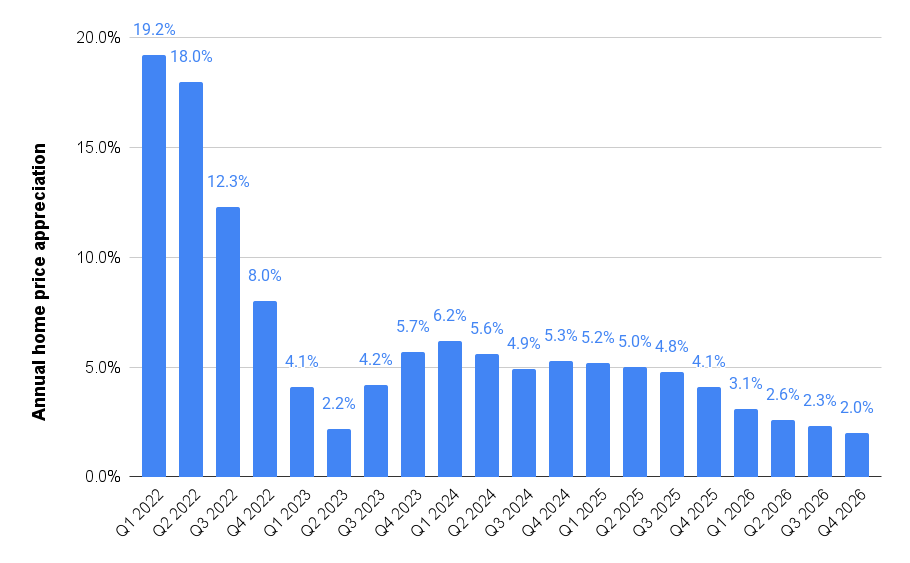

Hotter home price appreciation

Fannie Mae economists are also expecting hotter home price appreciation than in January, the last update of the quarterly forecast for that metric.

In January, Fannie Mae economists were expecting annual home price appreciation to cool to 3.5 percent by Q4 2025. The latest forecast is that home prices will be up 4.1 percent from a year ago in Q4 2025, before appreciation cools to 2 percent by Q4 2025.

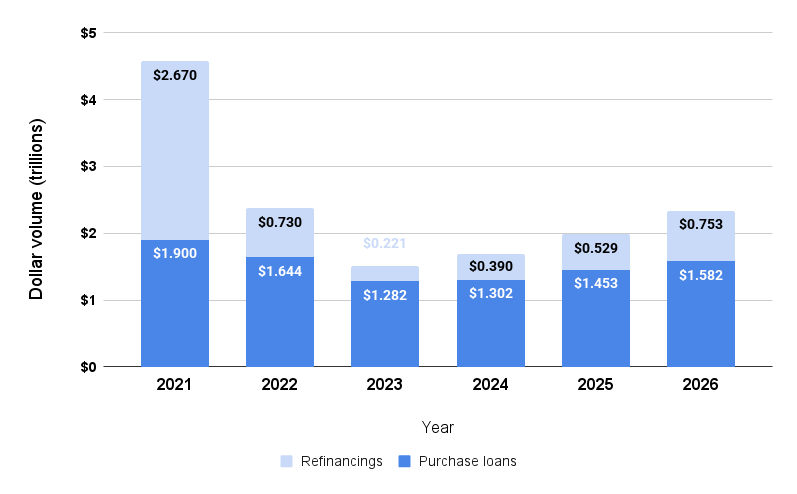

Higher prices spur mortgage originations

Higher home prices mean mortgage lenders could see 17 percent growth in 2025 lending by dollar volume, with refinancing expected to surge 36 percent to $529 billion, and purchase loans projected to hit $1.453 trillion, up 12 percent from 2024.

If mortgage rates keep trending down next year as projected, Fannie Mae economists expect refinancing to surge by 42 percent next year, to $753 billion, and purchase loan fundings to grow by 9 percent, to $1.582 trillion.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 29, 2025 | Industry, News Feed

Consumer confidence sank to a five-year low in April over concerns about tariffs, while trade deficit surged to an all-time high in March, and job postings shrank more than expected

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Mortgage rates are on the retreat this week as the latest data on the economy has investors who fund most home loans worried that tariffs will not only fuel inflation but lead to a recession.

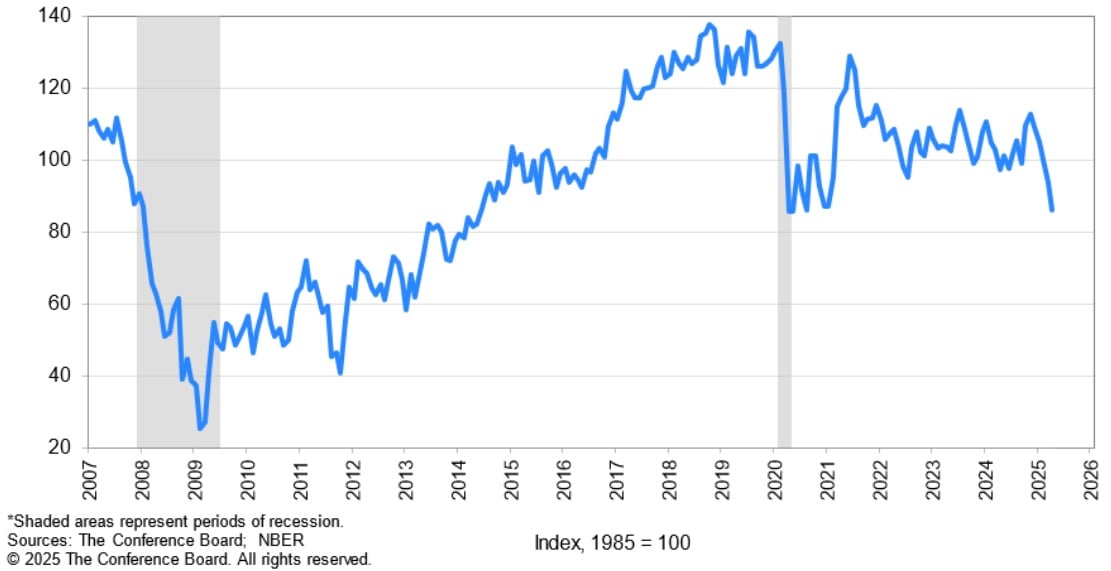

The Conference Board reported Tuesday that its Consumer Confidence Index dipped for the fifth consecutive month in April, to 86 — the lowest level since May 2020, the onset of the COVID pandemic.

Mark Zandi

TAKE THE INMAN INTEL INDEX SURVEY FOR APRIL

The U.S. trade deficit hit an all time high in March and job postings shrank more than forecasters were expecting, with a federal hiring freeze in place and uncertainty over the economy putting a chill on private sector hiring.

The 19-point drop in the Consumer Confidence Index over the past three months is “just shy of the recession threshold of 20,” Moody’s Analytics Chief Economist Mark Zandi posted on X. “Unless the trade war cools off very (very) soon, recession appears dead-ahead.”

Consumer confidence falters

“One positive note is that the slide in confidence was mostly due to weaker consumer expectations,” Zandi added. “Present assessments are holding up better. This suggests confidence could recover quickly with good news on the trade war, heading off a recession.”

In the latest back and forth on tariffs, President Trump signed an executive order Tuesday aimed at providing U.S. automakers some relief by “de-stacking” tariffs to avoid the cumulative effect of overlapping tariffs on other items like steel and aluminum.

The Conference Board reported that its Expectations Index, which tracks consumers’ short-term outlook for income, business and labor market conditions, fell 12.5 points to 54.4 — the lowest level since October 2011, and below a threshold of 80 that usually signals a recession ahead.

Stephanie Guichard

Consumers surveyed by the Conference Board through April 21 said they expect inflation will hit 7 percent in the next year, the most pessimistic reading since November 2022, when the U.S. was experiencing “extremely high inflation,” Conference Board economist Stephanie Guichard said, in a statement.

The decline in consumer confidence was shared across all political affiliations, and consumers “explicitly mentioned concerns about tariffs increasing prices and having negative impacts on the economy” in write-in responses, the Conference Board said.

Job openings trend down again

Employers were looking to fill 7.192 million job openings in March — a drop of 288,000 from February and 901,000 from a year ago, the Bureau of Labor Statistics reported Tuesday. Economists had expected job openings to hold steady at 7.5 million.

Federal government job openings fell by 36,000 in March, while “the surge in economic policy uncertainty in March, mostly relating to tariff policy,” was the primary driver of the 229,000 decline in private sector job openings, Pantheon Macroeconomics Chief U.S. Economist Samuel Tombs said in a note to clients.

Samuel Tombs

“In particular, openings in the transportation, warehousing and utilities sector dropped by a relatively large 59,000, as businesses geared up for lower levels of demand for goods,” Tombs said. “Meanwhile, healthcare job postings fell by 45,000 and now are back in line with their long-run level, relative to the number of jobs.”

Tariffs on some goods from China have been increased by as much as 170 percent this year, with most of that hike taking effect April 9.

The Trump administration’s threats to raise tariffs on China and other U.S. trading partners prompted a rush of imports in March that pushed the U.S. trade deficit to a record high of $162 billion, according to an advance reading published by the Census Bureau Tuesday.

Trade deficit widens

U.S. companies imported an all-time high of $342.7 billion in goods last month, up $16.3 billion from February.

Economists have forecast that economic growth slowed to an annual rate of 0.4 percent during the first quarter, down from 2.4 percent in the final three months of 2024. The Bureau of Economic Analysis is scheduled to release an estimate of Q1 gross domestic product (GDP) growth on Wednesday.

The latest advance economic indicators pushed the Atlanta Fed’s GDPNow forecasting model’s estimate of Q1 annual GDP growth down to -2.7 percent Tuesday, from -2.4 percent on April 24.

Mortgage rates retreat from 2025 high

At 6.76 percent on Monday, rates on 30-year fixed-rate mortgages were down four basis points from Friday and 29 basis points from a 2025 high of 7.05 percent registered Jan. 14, according to rate lock data tracked by Optimal Blue.

Yields on 10-year Treasury notes, a barometer for mortgage rates, fell five basis points Monday and another four basis points Tuesday.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 29, 2025 | Industry, News Feed

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Wells Fargo could soon be rid of a $1.95 trillion asset cap that’s limited the bank’s growth after the Consumer Financial Protection Bureau lifted a 2018 consent order aimed at resolving issues in mortgage and auto lending, the bank confirmed Monday.

It’s the 12th consent order closed by Wells Fargo’s regulators since 2019 and the sixth this year, leaving in place only two of the 14 consent orders drawn up by regulators recent years over concerns about the bank’s past business practices.

Charlie Scharf

“I am proud of the work done by our teams and remain confident that we will complete the work needed to close our other open consent orders,” Wells Fargo CEO Charlie Scharf said in a statement. “Wells Fargo is a different and stronger company today as we focus on creating long-term value for our customers, clients, communities and shareholders.”

The latest consent order to be lifted was tied to the CFPB’s issues with how some borrowers were charged for mortgage interest rate-lock extensions, and the bank’s administration of a mandatory insurance program on auto loans. The CFPB fined Wells Fargo $1 billion in that enforcement action and drew up a consent order outlining how the bank would remedy the issues.

Wells Fargo had previously announced in January that the CFPB had lifted a 2022 consent order related to a $3.7 billion settlement over the bank’s alleged mismanagement of mortgages, auto loans and deposit accounts.

The Federal Reserve Board in February lifted two 2011 consent orders tied to alleged deficiencies in mortgage loan servicing and mortgage lending practices at a former Wells Fargo subsidiary.

Wells Fargo’s progress in closing consent orders, along with the Trump administration’s push to loosen regulations, means an asset cap that has limited the bank’s growth could be lifted as soon as the second quarter, RBC Capital Markets analyst Gerard Cassidy told Reuters.

The CFPB under the Trump administration has dropped at least nine pending consumer lawsuits, and has also taken the unusual step of attempting to undo a fair lending settlement negotiated by the bureau before the November election.

But Scharf said that doesn’t mean regulators are more relaxed about lifting consent orders than they were during the Biden era.

“I [have been] very consistent in my belief that the regulators are objective when it comes to these things,” Scharf told investment analysts on the bank’s April 11 earnings call. “They’re very fact-based. They want to see us do the work. They want us to do their validation. And if we do that, they’ll close the orders. I don’t think the change in administration suggests that we need to do anything differently.”

But broader regulatory changes that are being discussed by the Trump administration for the banking industry as a whole, “would allow us to better support our customers,” Scharf said. “That means make more loans, take more deposits, and provide more liquidity to the markets, while still preserving robust regulatory oversight.”

If Wells Fargo’s asset cap is lifted, it could have more room on its books to originate and hold jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $806,500 conforming loan limit in most markets. Lenders who make such loans often hold them on their balance sheet, since they’re more difficult to bundle up and sell to investors.

Scharf said that while the asset cap remains in place, Wells Fargo will do what it has for the past several years, which is “focus on growing businesses where we don’t rely on our balance sheet,” like credit cards and wealth management services.

But once the asset cap is lifted, that will give Wells Fargo more leeway to expand its deposit base and fund more loans, he said.

“We are a different company today than when this new management team arrived,” Scharf said. “These recent closures reflect that we have completed much of the common risk and control infrastructure work across the company that is required by other orders.”

The fact that the consent orders are closed “doesn’t mean we’re going to stop doing the work,” he said. But Wells Fargo can operate more efficiently, “because now we have a much better understanding of the control environment and how to run it properly.”

While Scharf wouldn’t put a number on how much Wells Fargo might grow its deposit base and loan fundings when the asset cap is lifted, “it does give us more degrees of freedom in terms of how we run the place.”

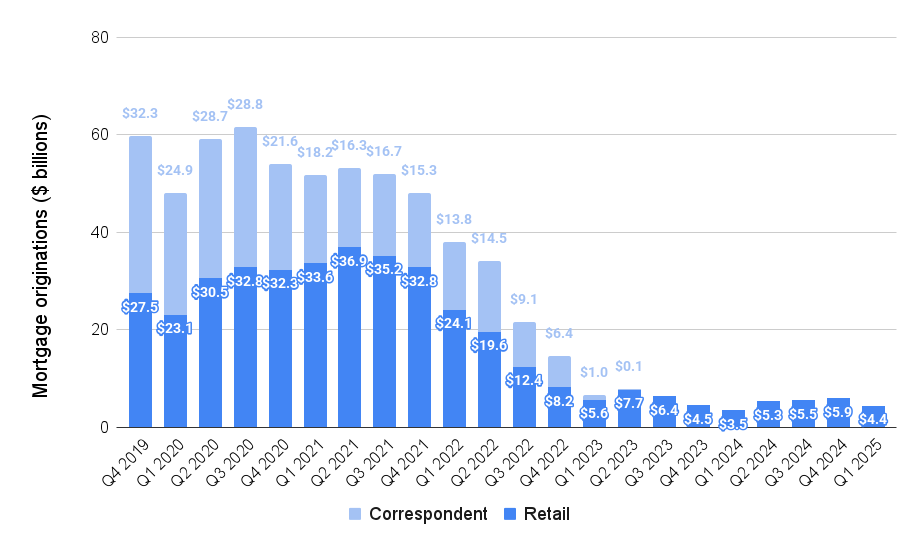

Wells Fargo’s dwindling appetite for mortgages

Once the nation’s largest mortgage lender, Wells Fargo was overtaken by direct lender Quicken Loans (now Rocket Mortgage) in 2017.

As rising mortgage rates put an end to the pandemic era refinancing boom, Wells Fargo’s mortgage volume also shrank as bank executives reassessed their appetite for risk as a buyer of mortgages from correspondent lenders.

In January 2023, Wells Fargo shut down the bank’s correspondent lending channel and announced a new strategic direction in home lending — a smaller, less complex business focused on the bank’s existing customers and minority communities.

With all of Wells Fargo’s mortgage business now coming through its retail channel, it originated just $20.2 billion in loans last year, less than a tenth of the $223 billion in mortgages originated during the 2020 refinancing boom.

In reporting a $4.9 billion first-quarter profit on April 11, the bank said it originated $4.4 billion in mortgage loans, up 26 percent from Q1 2024.

Growth in both purchase mortgages and refinancings helped drive the double-digit annual growth in home lending, and Wells Fargo continues to streamline the business with headcount down 47 percent, Wells Fargo Chief Financial Officer Mike Santomassimo said on the April 11 earnings call.

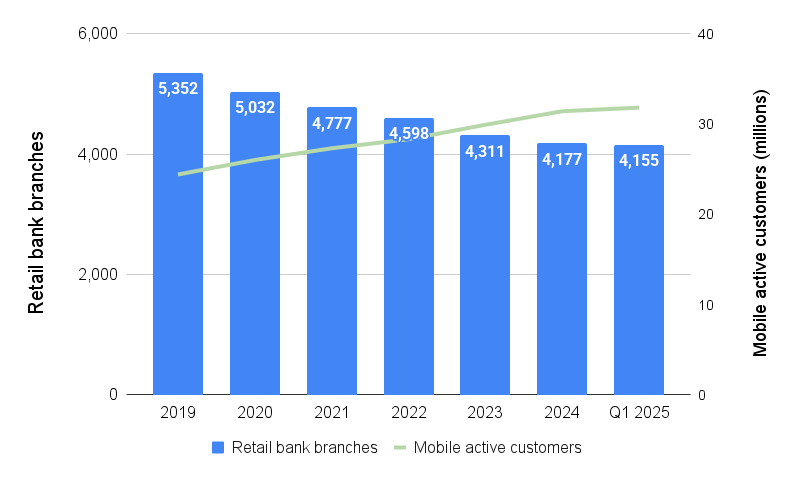

More customers, fewer branches

With 4,155 branches open as of March 31, Wells Fargo has trimmed its branch count by 22 percent from the 5,325 branches open at the end of 2019 on the eve of the pandemic.

Wells Fargo continues to shrink its brick-and-mortar operations, closing 22 branch offices during the first quarter.

But Wells Fargo also boosted its “mobile-active” customer count by 30 percent since 2019, to 31.8 million as of March 31. That growth continued in Q1, with the bank adding about 400,000 mobile-active customers — consumers and small business users who have logged into their accounts using a mobile device in the past 90 days.

While Wells Fargo is scaling back its brick-and-mortar presence, it is investing in refurbishing the branches that will stay open, accelerating the process in 2024 by completing 730 branch makeovers.

Scharf said Wells Fargo continued to invest in refurbishing its branches during the first quarter, and following the termination of a sales practices consent order over a year ago, has been taking “measured actions” to generate “modest growth” of metrics like net checking account growth and credit cards originated in branches.

“When we think about our consumer lending business, almost all of our businesses in our consumer lending segment are earning far below the ROTCEs (return on tangible common equity) that they should be earning for different reasons,” Sharf said.

Wells Fargo’s investments in building its credit card business, for example, are “front-loaded,” with modest returns as balances grow over time.

“But as long as the results play out on top of the models that we assumed, we know that’s just a matter of time until those returns increase significantly,” he said.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 25, 2025 | Industry, News Feed

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Three former Wells Fargo executives who were fined $18.5 million by the bank’s federal regulator in January for their alleged role in a 2016 scandal involving problematic sales practices are on track to settle those enforcement actions for just a fraction of that amount.

The Office of the Comptroller of the Currency (OCC) — under new leadership appointed by President Trump in February — announced Friday that it’s reached settlements with two of those executives totaling $150,000. The OCC won’t comment on the status of the case of the third executive, who is challenging a $10 million fine in court.

The OCC had previously levied a $7 million fine on former Wells Fargo Chief Auditor David Julian and a $1.5 million fine on his deputy, former Executive Audit Director Paul McLinko. Under the terms of the settlement, Julian will pay $100,000 and McLinko will pay $50,000, without admitting wrongdoing.

In a Jan. 14 decision, Acting Comptroller of the Currency Michael Hsu affirmed rulings by an administrative law judge, who in a 2022 hearing determined that Julian and McLinko had failed to plan and manage audit activity that would have detected the problematic sales practices that persisted at the bank for more than a decade.

“This case stems from one of the largest scandals in banking history,” Hsu said in his decision. “Under pressure to meet unreasonable sales goals, thousands of employees at Wells Fargo engaged in a collection of practices [that] included opening millions of unauthorized customer accounts, transferring funds without customer consent, lying to customers that certain products were available only as a package with other products, enrolling customers in online banking and bill-pay without their consent … and falsifying customers’ personal information.”

Hsu, who headed the OCC during the Biden administration, stepped down on Feb. 10 and was succeeded by Trump appointee Rodney Hood.

Julian and McLinko appealed Hsu’s decision the day after it was issued, with attorneys for McLinko calling it and other rulings against their client “arbitrary, capricious [and] an abuse of discretion,” and “infected by multiple prejudicial evidentiary and procedural errors.”

A March 13 scheduling order gave attorneys for Julian and McLinko until April 22 to file briefs with the U.S. Court of Appeals for the District of Columbia, with final briefs from all parties due on July 7. But on April 1, the court suspended the briefing schedule with no explanation.

A spokesperson for the OCC declined to comment on why it chose to settle with Julian and McLinko rather than defend its previous orders in court, saying it “does not comment on specific enforcement actions beyond what is published [on] our website.”

Attorneys for Julian and McLinko declined to comment on the record.

Julian and McLinko each signed consent orders saying that they agreed to settle with the OCC “to avoid the costs associated with future administrative and judicial proceedings” without admitting the allegations against them, or the findings and conclusions of the administrative law judge.

In the third case, Hsu on Jan. 14 ordered former Wells Fargo Community Bank Group Risk Officer Claudia Russ Anderson to pay a $10 million civil money penalty, agreeing with an administrative law judge’s finding that she “failed to institute effective controls to manage the risks” posed by the bank’s sales practices.

Anderson appealed the case the next day, and has until May 12 to file a brief with the U.S. Court of Appeals for the District of Columbia. The OCC declined to comment on the status of that case.

Having settled with Julian and McLinko, Anderson’s case is the last of 11 enforcement actions the OCC pursued against 11 former Wells Fargo executives related to the bank’s alleged systemic and widespread sales practices misconduct.

All told, the OCC has collected more than $43 million in fines from Wells Fargo executives to date. That’s on top of the $185 million in fines the bank agreed to pay the Consumer Financial Protection Bureau (CFPB), OCC, and City and County of Los Angeles in connection with the scandal in 2016.

Carrie Tolstedt, the former head of Wells Fargo’s Community Bank, was the only Wells Fargo employee to face criminal charges for her role in the cross-selling scandal.

Tolstedt was sentenced to 12 months of probation after pleading guilty in March 2023 to obstructing the government’s investigation into the bank’s sales practices.

While the OCC originally sought a $25 million civil penalty against Tolstedt in 2020, she eventually settled for $17 million.

Tolstedt, who also reached a $3 million settlement with the SEC, collected a $125 million retirement package from Wells Fargo, although the bank “clawed back” $67 million of that compensation, CNN reported at the time.

In February of last year, Tolstedt and her husband, Brad, sold a home in Phoenix for $7.8 million, then bought another home in August for $5.9 million, The Arizona Republic reported.

Other former Wells Fargo executives who paid fines to the OCC in the wake of the cross-selling scandal include:

- Former Chairman and CEO John Stumpf ($17.5 million)

- Former General Counsel James Strother ($3.5 million)

- Former Chief Administrative Officer Hope Hardison ($2.25 million)

- Former Chief Risk Officer Michael Loughlin ($1.25 million)

- Former Community Bank Group Finance Officer Matthew Raphaelson ($925,000)

- Former Head of Community Bank Deposit Products Group Kenneth Zimmerman ($400,000)

- Former Head of Community Bank Human Resources Tracy Kidd ($350,000)

In a separate case in 2021, Wells Fargo agreed to pay the OCC a $250 million fine over the bank’s practices for helping homeowners having trouble paying their mortgages.

In 2022, Wells Fargo agreed to pay $3.7 billion to settle allegations by the CFPB that it harmed millions of consumers over a period of several years through widespread mismanagement of mortgages, auto loans and deposit accounts.

Once the nation’s largest mortgage lender, Wells Fargo was overtaken by direct lender Rocket Mortgage (then known as Quicken Loans) in 2017. It’s no longer ranked among the nation’s top 10 mortgage lenders, but could be poised for a comeback this year as it makes progress in getting out from under a $1.95 trillion asset cap that’s limited the bank’s growth.

If the asset cap is lifted as the bank continues to close consent orders imposed by regulators, Wells Fargo could gain more capacity to originate jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $806,500 conforming loan limit and hold those loans on its books.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site