by Matt Carter | May 6, 2025 | Industry, News Feed

Executives put a positive spin on prospects for growth, with loan origination volume up 17 percent from a year ago to $32.4 billion and revenue up 5 percent to $613.4 million.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The nation’s biggest mortgage lender lost $240.7 million during the first quarter, as a dip in mortgage rates forced United Wholesale Mortgage to write down the fair value of its mortgage servicing rights by $388.6 million.

UWM executives put a positive spin on the big picture in reporting earnings Tuesday, noting that loan origination volume was up 17 percent from a year ago to $32.4 billion, as the company did brisk business with homeowners looking to refinance.

Executives at the Pontiac, Michigan-based wholesale lender said they expect to originate $38 billion to $45 billion in mortgages this quarter, with gain margin of 90 to 115 basis points. The upper range of that guidance would represent UWM’s first $40 billion quarter since Q4 2021.

Mat Ishbia

“We haven’t hit over $40 billion since the real boom times, and we are going to do that this quarter,” CEO Mat Ishbia predicted on the company’s earnings call.

“Where everyone else is kind of hovering, our investments have been working,” Ishbia told investment analysts. “Our broker channel is winning. And then on top of that, the technology stuff that’s going to come out in the second quarter … it’s going to blow your mind, and it’s just the beginning of what we’re doing.”

UWM refinanced $10.7 billion in mortgages during Q1, nearly double the $5.5 billion in refi volume that came in a year ago, helping drive 5 percent revenue growth, to $613.4 million.

While purchase loan originations were essentially flat at $21.7 billion, UWM’s investment in AI and other technologies will allow it to ramp up its business with little impact on expenses, Chief Financial Officer Rami Hasani said on a call with investment analysts.

UWM announced a strategic partnership with Google Cloud last month to integrate AI and data analytics capabilities into its lending platform.

Rami Hasani

“We believe our business is currently in a position to handle twice our 2024 origination volume with minimal impact to our fixed costs,” Hasani said on his first earnings call since succeeding Andrew Hubacker as CFO on April 1.

Shares in UWM closed down 15 percent Tuesday after touching a new 52-week low, as shareholders also digested details of a plan to increase UWM’s “float,” or the number of outstanding shares, by up to 80 million shares.

Ishbia said that under a plan scheduled to go into effect on June 17, he’ll continue to own around 80 percent of UWM’s shares a year from now, down from 87 percent today. He said the company will continue to pay a 10-cents-per-share quarterly dividend — payouts that also benefit him and his family as majority owners.

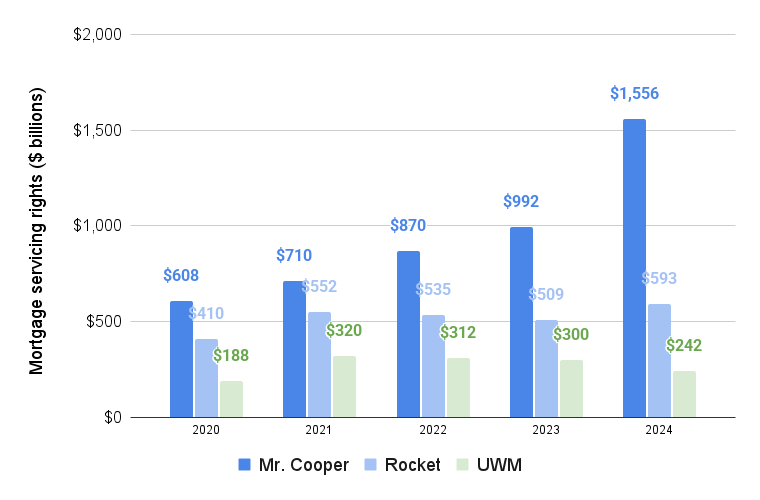

Plans by rival Rocket Companies to acquire the nation’s largest loan servicer, Mr. Cooper, prompted UWM to end its subservicing contract with Mr. Cooper and announce last month that it will bring mortgage servicing in-house.

Ishbia said the plan is to start onboarding loan servicing at the beginning of next year, and “hopefully have it all in house by the end of next year.”

For now, UWM’s mortgage servicing rights (MSR) portfolio continues to shrink as it sells servicing rights for cash. UWM’s MSR portfolio shrank by 11 percent during Q1 to $214.6 billion.

UWM’s shrinking mortgage servicing portfolio

Mr. Cooper, Rocket Mortgage and UWM mortgage servicing rights (MSR) portfolios, including subservicing. Source: Company earnings reports.

Loan servicers collect monthly mortgage payments from borrowers, passing the money along to lenders or investors in mortgage-backed securities who have purchased the loans.

Big mortgage lenders often like being in the loan servicing business because the fees they can earn are a steady source of income that can even out ups and downs in the housing market.

Lenders who service their own loans are well-positioned to “recapture” borrowers when they’re ready to refinance or buy their next home.

But the constantly fluctuating valuations of mortgage servicing rights (MSRs) can create accounting headaches.

When mortgage rates fall, MSRs become less valuable because borrowers are more likely to refinance and end up with another loan servicer. But when mortgage rates rise, so does the paper value of a servicer’s MSRs. MSR valuations can push profits, as measured by net earnings, deep into the red or the black.

“As we’ve discussed several times, we have zero control over MSR values, whether it goes up or down,” Ishbia said. “So it’s really not that relevant to me. But we did have an amazing quarter and we’re profitable on all the [other] measures we look at.”

Another metric — adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) — remained positive in Q1 at $57.8 million, down 43 percent from a year ago.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 5, 2025 | Industry, News Feed

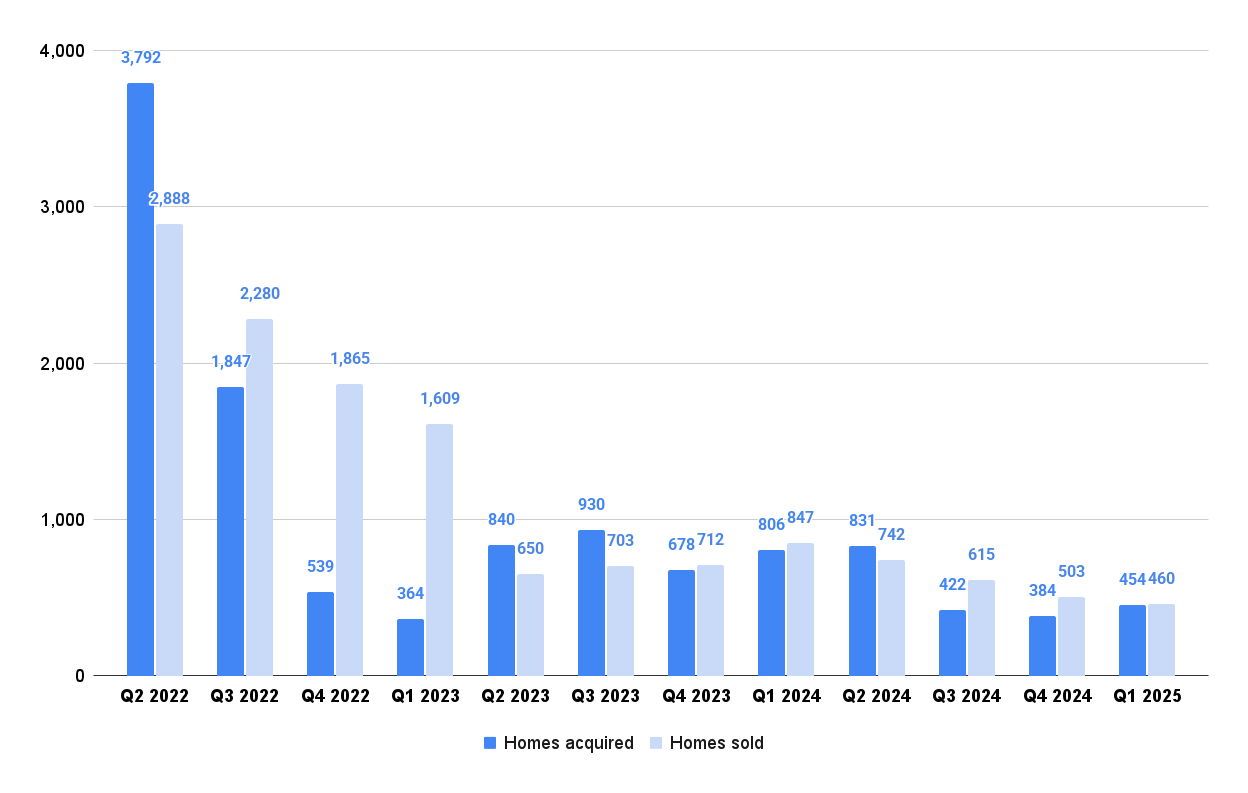

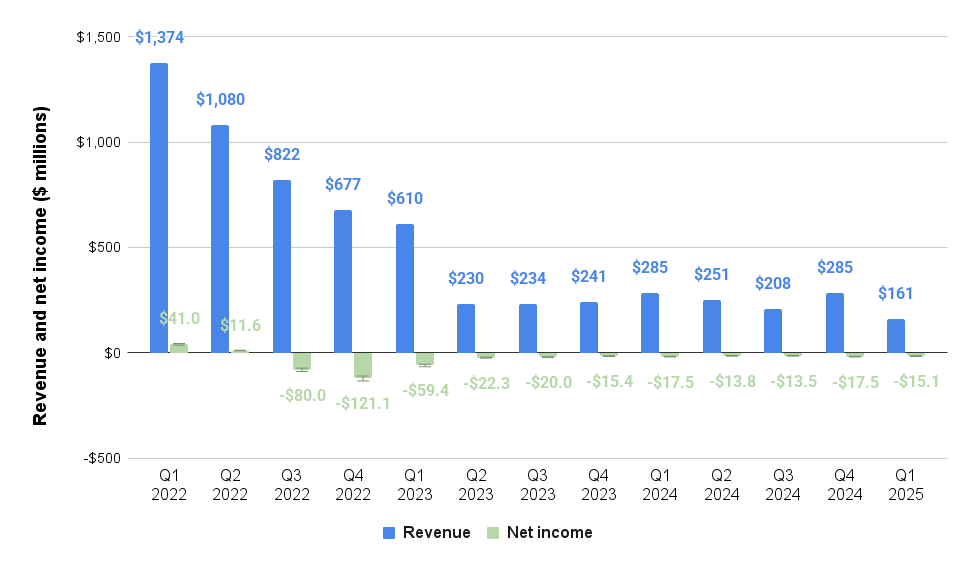

Offerpad’s $15.1 million Q1 net loss is down 14 percent from Q4 2024, with home acquisitions up 18 percent from the previous quarter to 454.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Cash offer and renovation platform Offerpad Solutions Inc. trimmed its first quarter loss by 14 percent while upping its home purchases, but brought in less revenue as it sold fewer homes.

Offerpad reported a $15.1 million Q1 net loss Monday, down from $17.5 million in Q4 2024, with home acquisitions up 18 percent from the previous quarter to 454.

With Q1 home sales down 9 percent from Q4, revenue shrank by 8 percent to $160.7 million.

Brian Bair

Offerpad CEO Brian Bair said the company’s cash offer program “performed as expected,” while “asset light” services like the company’s B-to-B Renovate business, Direct+ buyer program and Agent Partnership Program “contributed significantly to the top and bottom line.”

Offerpad’s Renovate business closed 209 projects in the first three months of the year, up 12 percent from Q4, generating record revenue of $5.3 million.

Bair announced a new partnership with Auction.com in which Offerpad’s Renovate service will become a preferred provider of renovation services for buyers on the platform.

“It’s a meaningful step forward as we help buyers transform properties into move-in-ready homes, expand our renovation business and deliver greater value to buyers, sellers and communities across the country,” Bair said.

Shares in Offerpad, which in the last 12 months have traded for as little 92 cents and as much as $7.88, closed at $1.03 before Monday’s earnings release, and were up 2 percent in after hours trading.

Offerpad was put on notice by the New York Stock Exchange last month that it could be delisted from the exchange because its market capitalization has dropped below $50 million.

With 27.38 million shares outstanding, Offerpad’s price per share would need to rebound to at least $1.83 for the company’s market capitalization to meet the $50 million threshold.

The company said at the time it was confident it would be able to submit a business plan detailing how it will get back into compliance with the stock exchange’s listing standards within 18 months.

Offerpad Q1 2025 acquisitions up, sales down

Offerpad acquired 454 homes during Q1, up 18 percent from Q4 but down 44 percent from a year ago.

Close to half of those acquisitions (42 percent) were driven by Offerpad’s Agent Partnership Program, up from 28 percent a year ago.

While Offerpad sold 43 fewer homes during Q1 2025 than it did in Q4 2024, gross profit per home sold was up 8 percent quarter over quarter to $22,800.

Offerpad finished the quarter with 671 homes in inventory, but said only 13 percent were owned for more than 180 days, down from 22 percent at the end of the year.

Company executives said they expect home sales to rebound to between 500 and 550 sales in Q2.

Offerpad trims losses and expenses as revenue drops

Although slower Q1 sales dented revenue, operating expenses for the quarter were down 39 percent from a year ago to $22 million, helping Offerpad trim $2.4 million from its Q4 loss.

Offerpad executives said they expect Q2 revenue of $160 million to $190 million, and “sequential improvement” in adjusted earnings before interest, taxes, depreciation and amortization (EBITDA).

At negative $7.8 million, Q1 EBITDA represented a 32 percent improvement from $11.5 million in Q4.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 5, 2025 | Industry, News Feed

Bellevue, Washington-based Evergreen hires Wells Fargo and Bank of America veteran Andrew Leff as head of national business development as it continues to expand beyond its roots as a regional independent mortgage bank.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Evergreen Home Loans continues to expand beyond its roots as a regional independent mortgage bank, hiring Wells Fargo and Bank of America veteran Andrew Leff as head of national business development.

Leff, who’s also held senior leadership positions at JPMorgan Chase and U.S. Bank, will be responsible for expanding Evergreen’s footprint through partnership-driven growth strategies including builder and affinity relationships, the lender announced Monday.

Robert Lipston

“Andrew’s reputation in the industry speaks for itself,” Evergreen executive Robert Lipston said in a statement. “He brings the experience, strategic vision, and leadership we need as we continue to grow our national presence. We’re thrilled to have him on board.”

Based in Bellevue, Washington, Evergreen in January announced an expansion into five Southeastern states — Florida, Georgia, North Carolina, South Carolina and Tennessee — with former Guild Mortgage executive John Porath overseeing its operations in those states.

The cash offer pioneer in March announced its entry into the New Mexico market with branches in Albuquerque and Carlsbad under the leadership of Area Manager Barry Abt.

Launched in 2021, Evergreen’s CashUp program has grown into a suite of products that also includes a buy-before-you-sell product, “StepUp,” and a rate-lock product for sellers, “Lock and List.”

Evergreen has fueled growth through partnerships with real estate agents and builders, a strategy that Leff has extensive experience with.

Leff was head of business development programs at Wells Fargo, managing builder, corporate affinity, relocation and wealth management partnership channels. During a 10-year stint at Bank of America, Leff was instrumental in building and scaling the bank’s national builder and affinity platforms, Evergreen said.

Andrew Leff

“I truly admired Evergreen’s people-first culture and entrepreneurial spirit,” Leff said in a statement. “I’m excited to help build on that foundation by creating scalable, value-driven partnerships that support both the business and the communities we serve.”

Evergreen sponsors 227 mortgage loan originators who work out of 51 branch locations in nine states — Arizona, California, Idaho, Montana, New Mexico, Nevada, Oregon, Texas and Washington — according to records maintained by the Nationwide Multistate Licensing System.

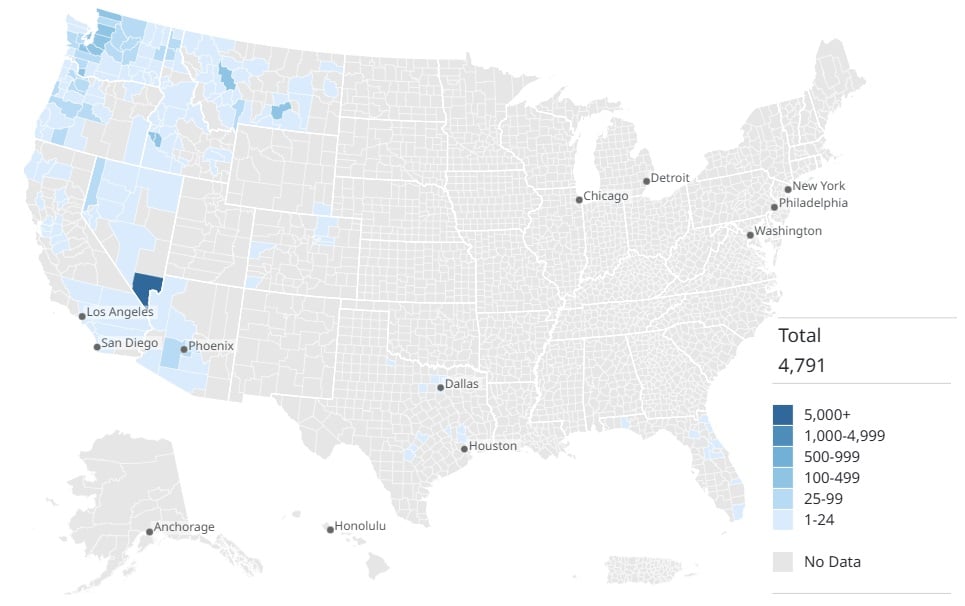

Evergreen Home Loans’ growing market presence

Evergreen Home Loans 2024 business by county. Source: iEmergent analysis of Home Mortgage Disclosure Act (HMDA) data.

Last year, Evergreen funded 4,791 mortgages totalling $1.92 billion, up 22 percent from 2023, according to an analysis of Home Mortgage Disclosure Act (HMDA) data by mortgage business intelligence provider iEmergent.

According to iEmergent data, purchase loans accounted for 85 percent of Evergreen’s business in 2024, most of which was done west of the Rocky Mountains, with a growing presence in Texas and Florida.

Evergreen on Monday was advertising 11 positions on its website, with openings for loan officers and funders, investor accounting manager and a branch marketing assistant.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 2, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The head of Fannie Mae and Federal Mac’s federal regulator, Bill Pulte, says he’s signed more than 80 orders revamping policies and procedures at the mortgage giants — only a handful of which have been made public.

Since being sworn in as director of the Federal Housing Financing Agency on March 14, Pulte has issued a raft of orders, decisions and waivers eliminating programs and practices intended to boost lending in minority communities, protect borrowers from unfair or deceptive practices, and assess risks associated with climate change.

The orders that have been made public are available only as pictures of the documents Pulte has published on his social media profile on X, often without comment. To date, Pulte has posted a dozen documents — including six orders, five decisions, and a waiver — implementing what in many cases are major policy changes at FHFA.

In an April 30 appearance on a business program on X, “From the Desk of Anthony Pompliano,” Pulte claimed he’s signed six or seven times that number of orders — he was not sure exactly how many.

“I’ve signed over 80 orders, or something like that,” Pulte told Pompliano. “I thought last I saw for sure was over 50, but somebody told me yesterday it’s now over 80. I don’t have an exact count, but that’s crazy to think about that. As a director of just federal housing, that you would have that many things that you could just — boom, boom, boom, get done.”

The FHFA, which has made no formal announcements of Pulte’s orders and has not made them available to the public, published 13 orders on its website during Trump’s first administration and 11 during the Biden administration.

Asked for copies of the additional orders Pulte says he’s signed, the FHFA provided the following statement: “U.S. Federal Housing FHFA is prioritizing efficiencies that eliminate wasteful and unnecessary red tape. We are laser-focused on finding smart solutions that make the American Dream a reality for Americans everywhere.”

Pulte, the grandson of PulteGroup Inc. founder William J. Pulte, angered some prominent Democrats by firing 14 members of Fannie and Freddie’s boards of directors and appointing himself the chair of both companies less than a week after he was confirmed.

Ten Democrats including Chuck Schumer, Cory Booker and Kirsten Gillibrand asked FHFA Inspector General Brian Tomney on April 15 to determine if the agency had complied with the law in gutting Fannie and Freddie’s boards, and to assess whether plans to downsize FHFA would compromise its ability to “fulfill its statutorily mandated functions.”

The next day, Senators Elizabeth Warren, Jack Reed and Lisa Blunt Rochester urged Tomney to “open an investigation into FHFA’s apparent noncompliance with federal laws and regulations,” claiming Pulte is prohibited by law from holding any position at Fannie Mae or Freddie Mac.

“Within a week of taking office, he removed a majority of the directors of Fannie and Freddie, installing himself, his business associates, and partisan loyalists in their place,” the April 16 letter to Tomney claimed. “He also removed Fannie’s entire audit committee. After these actions, the boards appear to lack anyone from an organization that has represented consumer or community interests, or has shown a career commitment to low-income housing.”

The FHFA’s recent appointments to Fannie Mae’s board include Mike Stucky — a former Pulte Group division president — and banker, investor and lawyer Omeed Malik. As chairman and CEO of Colombier Acquisition Corp., Malik is leading a plan to take GrabAGun, an online retailer of firearms and ammunition, public in a special purpose acquisition company (SPAC) merger.

Donald Trump Jr. — a partner in Malik’s venture capital firm 1789 Capital — will serve on GrabAGun’s board of directors, and Pulte announced in January that his family is an investor in the company.

Tomney declined both requests from lawmakers in separate letters on April 24, saying the FHFA was responding to those inquiries and committed to “continuing dialogue.”

“FHFA is best positioned to respond to your questions regarding the factual and legal basis for staffing decisions at FHFA and the changes made on the boards of the enterprises [Fannie Mae and Freddie Mac],” Tomney wrote in a response to the April 15 letter from Schumer, Booker, Gillibrand and other Democrats.

Both of Tomney’s letters to lawmakers were obtained by Politico.

Reading the tea leaves

Much of what’s known about the FHFA’s administration of Fannie and Freddie during the second Trump administration comes from Pulte’s posts on X, and media appearances on Fox News and other news outlets.

In the last week, Pulte has posted about meetings he’s had with top lending industry executives at loanDepot, Rithm Capital, Newrez and Annaly Capital.

On April 21, he posted, “We do not foresee any more executive leadership changes at Fannie Mae & Freddie Mac. Our focus will now turn to growth, making homes more affordable, rooting out mortgage fraud, & providing great career opportunity to those who make Fannie & Freddie great American Icons, again!”

In an April 9 appearance on Fox News, Pulte said there is an “ongoing investigation” into the issues that led to the firing of more than 100 Fannie Mae employees. He said FHFA discovered “multiple people were working two jobs” — including some who were located in China — and that some employees had received kickbacks for charitable donations.

In an 18-minute interview on “From the Desk of Anthony Pompliano” Wednesday, Pulte said the Trump administration is focused on bringing home prices down through deregulation.

by Matt Carter | Apr 30, 2025 | Industry, News Feed

Advance GDP reading suggests the economy shrank by 0.3 percent during Q1, as a rush by businesses to import goods before tariffs took hold and government spending cuts dented growth.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Mortgage rates got more room to come down Wednesday after two data releases suggested inflation eased in March and the economy shrank during the first quarter, boosting the odds that the Federal Reserve will cut rates in June.

The Federal Reserve’s preferred measure of inflation, the personal consumption expenditures (PCE) price index, showed prices rose 2.3 percent in March from a year ago, the Bureau of Economic Analysis reported. That’s closer to the Fed’s 2 percent goal than February’s PCE price index reading of 2.7 percent.

In a separate release, the bureau’s advance estimate of real gross domestic product (GDP) suggested that the economy shrank by 0.3 percent during Q1, thanks to a tariff-driven surge in imports and a decrease in government spending.

If that estimate holds, it would represent an abrupt turnaround from the 2.4 percent annual growth in real GDP during Q4 2024 and the first economic contraction since 2022.

A rush by businesses to import goods before tariffs took hold was a “huge drag” on net trade, economists at Pantheon Macroeconomics said in their latest U.S. Economic Monitor.

But the advance GDP report “probably greatly overstates the loss of momentum at the start of this year,” Pantheon economists Samuel Tombs and Oliver Allen wrote.

“That said, the April tariff shock has since worsened the picture dramatically,” Tombs and Allen said. “We think stagnation is the most likely outcome over the rest of this year, but a recession would become likely if the threatened additional reciprocal tariffs are imposed in full in July.”

Economy may have shrunk in Q1

The surge in imported goods, which were up more than 50 percent, dented growth by five percentage points, Mortgage Bankers Association Chief Economist Mike Fratantoni said in a statement.

“Clearly, businesses were rushing to get goods into the country and were willing to store them until they were needed for production,” Fratantoni said.

The U.S. trade deficit hit an all time high in March and job postings shrank more than forecasters were expecting, with a federal hiring freeze in place and uncertainty over the economy putting a chill on private sector hiring, according to reports released Tuesday.

Joel Kan

“Mortgage application activity, particularly for home purchases, continues to be subdued by broader economic uncertainty and signs of labor market weakness, dropping to the slowest pace since February,” MBA Deputy Chief Economist Joel Kan said of a drop in mortgage demand last week.

The MBA’s weekly survey of lenders showed applications for purchase mortgages were down by a seasonally adjusted 3 percent last week when compared to the week before, but still up 3 percent from a year ago. Requests to refinance were down 4 percent week over week but up 42 percent from a year ago.

At 6.70 percent on Tuesday, rates on 30-year fixed-rate mortgages were down 19 basis points from their April high of 6.89 percent and 35 basis points from a 2025 high of 7.05 percent registered on Jan. 14, according to rate lock data tracked by Optimal Blue.

Inflation trending down again

While the PCE price index is inching toward the Fed’s inflation goal of 2 percent, core inflation excluding food and energy costs also dropped to 2.6 percent, down from 3 percent in February.

Samuel Tombs

Real consumption rose more sharply from February to March than forecasters had expected, showing “households aren’t allowing their fears about the damage that tariffs will eventually bring weigh on their overall level of expenditure today,” Tombs said in a note to clients.

Surveys show consumer sentiment “became much gloomier in April,” Tombs said, but spending is unlikely to slow down until consumers have to pay higher prices for imported goods.

Pantheon economists are sticking with their forecast that the Fed will cut short-term interest rates three times this year, by a total of 75 basis points, beginning in June.

The CME FedWatch tool, which tracks futures markets to predict the likelihood of future Fed moves, on Wednesday put the odds of a June Fed rate cut at 67 percent, up from 65 percent on Tuesday and 59 percent on April 23.

Mike Fratantoni

“The quandary facing the Federal Reserve is that while the trend in the data is clearly showing a slowing economy, it also renewed upward pressure on inflation,” Fratantoni said. “We expect that the Fed will hold rates steady at its meeting next week and will indicate that it will continue to hold at this level until it becomes clear whether a recession or inflation is the bigger risk.”

In their latest forecast, Fannie Mae economists said they expect economic growth to slow to 0.5 percent this year, and that annual inflation will rise to 3.5 percent by the fourth quarter.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site