by Matt Carter | Apr 15, 2025 | Industry, News Feed

Omeed Malik, founder of investment bank Farvahar Partners and venture capital firm 1789 Capital, is a business partner and “close friend” of Donald Trump Jr.

In April, we’ll go deep on money and finance for a special theme month, by talking to leaders about where the mortgage market is heading and how technology and business strategies are evolving to suit the needs of buyers now. Inman’s Best of Finance returns for 2025, celebrating the leaders in this space. And subscribe to Mortgage Brief for weekly updates all year long.

Banker, investor and lawyer Omeed Malik — recently dubbed “MAGA world’s premier financier” by New York Magazine — is the latest addition to mortgage giant Fannie Mae’s board of directors, Federal Housing Finance Agency Director Bill Pulte announced on social media Monday.

Before founding the investment bank Farvahar Partners and venture capital firm 1789 Capital — where Donald Trump Jr. became a partner in November — Malik was managing director and global head of the hedge fund advisory business at Bank of America Merrill Lynch.

Pulte said Malik “brings great capital markets, legal and investment experience” to Fannie Mae’s board of directors.

As chairman and CEO of Colombier Acquisition Corp., Malik helped take PublicSquare — which touts itself as a marketplace for “patriotic businesses and consumers” — public in a 2023 SPAC merger with Colombier, a special purpose acquisition company.

Malik stepped down from PublicSquare’s board on Dec. 3 — the same day Trump Jr. joined it, along with Willie Langston, a partner at wealth management firm Corient and a former national finance chair for Ted Cruz’s presidential campaign.

Described as a “close friend” of Trump Jr. in a November New York Magazine profile, Malik on March 3 reposted a picture the president’s son published on X the day before — in which Trump Jr. thanked Malik for co-hosting a fundraiser for Vivek Ramaswamy’s bid to become Ohio’s next governor in the 2026 election.

Malik is also an investor in The Daily Caller, the conservative news outlet co-founded by Tucker Carlson. His addition to Fannie Mae’s board follows Pulte’s purge of 14 board members at the mortgage giant and its sister company Freddie Mac, in March.

Pulte — the grandson of homebuilder William J. Pulte, the founder of PulteGroup Inc. — appointed himself the chair of Fannie and Freddie’s boards less than a week after he was confirmed by the Senate as Trump’s choice to lead their federal regulator.

Board Chair Michael Heid was one of eight Fannie Mae board members removed by Pulte, who declared, “DEI is dead at Fannie Mae and Freddie Mac.”

Fannie Mae CEO Priscilla Almodovar was one of five board members who kept their seats. They’ve been joined by Pulte’s other appointments to Fannie Mae’s board: Mike Stucky, a former Pulte Group division president, and FHFA General Counsel Clinton Jones.

Jones, who joined the FHFA in 2019 and was promoted to general counsel in 2021, was also appointed to Freddie Mac’s board.

One of Pulte’s other picks — Christopher Stanley, a staffer from the Department of Government Efficiency (DOGE) — was appointed to Fannie Mae’s board on March 17 but resigned the next day.

Mike Stucky

Stucky, who, according to his LinkedIn profile, is a retired heating, ventilation and air conditioning (HVAC) executive, was appointed vice chair of Fannie Mae’s board on April 10, the company disclosed Monday in a regulatory filing.

The FHFA has determined that Fannie Mae’s board should have at least five and no more than 13 directors. With Malik’s addition, the board will have nine members.

In addition to Chair Lance Drummond, Pulte removed five other directors from Freddie Mac’s board, the company said in a March 17 regulatory filing. In addition to Pulte and Jones, new additions to Freddie Mac’s board included Brandon Hamara and Ralph “Cody” Kittle.

Hamara is the vice president of land acquisition at homebuilder Tri Pointe Homes Inc., a Nevada-based homebuilder that completed 6,460 homes last year. Kittle is a partner at RenWave Kore, a Greenwich, Connecticut-based private equity firm.

On March 24, Freddie Mac board member Grace Huebscher announced her resignation, and Pulte appointed Michael Parrott, CEO and founder of consulting firm 480th Company, as her replacement.

Freddie Mac now has 10 board members, including interim CEO Mike Hutchins, who took on that role after Pulte fired Freddie Mac CEO Diana Reid and Head of Human Resources Dionne Wallace Oakley last month.

Appointed as CEO in September, Reid was the first woman to lead Freddie Mac. With Almodovar having served as Fannie Mae’s CEO since 2022, both mortgage giants were briefly led by women for the first time in history.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 14, 2025 | Industry, News Feed

Investors bid up mortgage lender’s share price by 21 percent as company says deal with investor investor SB Northstar LP will improve its balance sheet and better position it for growth and a return to profitability.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Investors in tech-driven mortgage lender Better Home & Finance are cheering its plans to restructure more than half a billion dollars in debt, which the company said Monday will improve its balance sheet and position the company to grow and return to profitability.

Better will retire $534 million in convertible notes held by investor SB Northstar LP in exchange for $110 million in cash and $155 million in new notes at a 6 percent interest rate due in 2028. The notes that are being retired carried a 1 percent rate and were due in 2028.

Vishal Garg

“This transaction will create approximately $265 million of positive pre-tax equity value for the company and its shareholders, as well as create a path to long-term value creation for our equity holders,” Better CEO Vishal Garg said in a statement. “We continue to invest in building the leading AI platform in the mortgage industry, and fulfilling our mission of making homeownership cheaper, faster and easier, and just plain better for all Americans.”

Shares in Better, which in the last 12 months have changed hands for as much as $30 and as little as $7.71, initially jumped 27 percent Monday on news of the debt restructuring, which is expected to close by April 28. After briefly climbing above $13 from Friday’s close of $10.28, shares in Better gave up some of those gains but closed up 21 percent at $12.40.

Better’s board of directors in January approved a $25 million share repurchase program, a strategy that often signals company executives think their shares are undervalued.

Better, which did a booming business in refinancing during the pandemic when mortgage rates hit historic lows, struggled when interest rates rebounded and has racked up $1.9 billion in losses since its inception.

The New York-based lender inched toward profitability in 2024 as growth in home equity and refinancing helped the company grow funded loan volume for the first time in three years even as it slashed expenses.

Better finished 2024 with 1,250 employees — down 88 percent team from a Q4 2021 peak of 10,400 — but claimed its adoption of AI will fuel more profitable growth, with loan fulfillment costs that are 35 percent lower than the industry average of $9,000 per loan.

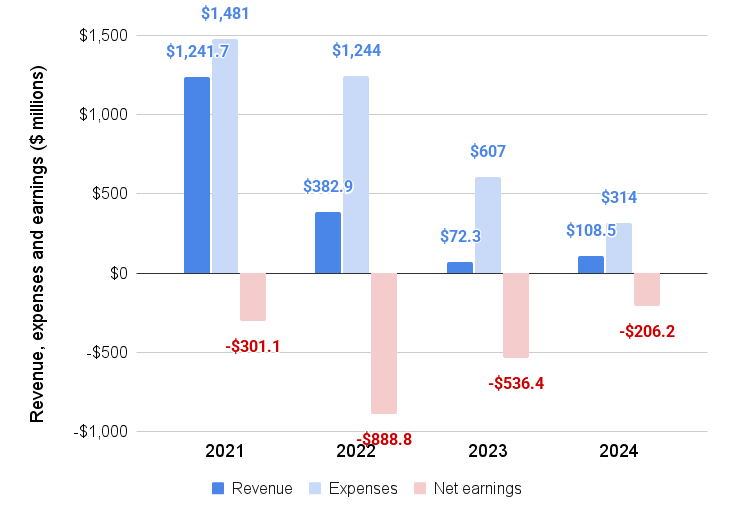

Revenue, expenses, earnings moving in right direction

Source: Better Home & Finance Holding Company earnings reports.

Better’s automated “One Day Mortgage” product represented 73 percent of all direct-to-consumer lending in Q4, helping the company achieve loan fulfillment costs it says are 35 percent lower than the industry average of $9,000 per loan.

While Better racked up a $206 million 2024 net loss, that was an improvement from $536 million in 2023 and $888.8 million in 2022.

Purchase mortgage lending accounted for nearly 74 percent of Better’s business last year, even though business from homebuyers was down 3 percent year from 2023, to $2.65 billion.

At $479 million, 2024 home equity funding volume was up 86 percent from a year ago, while refinancing volume grew by 56 percent, to $463 million.

But Better is losing one of its biggest partners this year, Detroit-based Ally Financial Inc., which announced in January that it was laying off hundreds of employees and getting out of the mortgage business.

Ally originated $1 billion in mortgages in 2023 through its partnership with Better and is also an investor in the company, which went public in a 2023 special purpose acquisition company (SPAC) merger.

While Better once relied on its business-to-business (B2B) partnerships for nearly half of its business, the partner channel accounted for only 19 percent of Q4 2024 loan volume.

Better executives have said they plan to grow the company’s partner channel by offering its technology through co-branded or white-label solutions.

In November, Better announced a partnership with NEO Home Loans to use Better’s Tinman technology stack to power local loan officers.

Better hired NEO Home Loans executives Ryan Grant and Danny Horanyi to lead the “NEO Powered by Better” partnership and build out a distributed retail channel.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Apr 11, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Fears of a tariff-fueled trade war are dragging consumer sentiment down to near all-time lows, while inflation worries continue to drive up mortgage rates as investors who back most home loans demand higher yields.

The University of Michigan Index of Consumer Sentiment fell 11 percent from March to April and is down 31 percent from December, according to preliminary data released Friday.

At 50.8 in April, the Index of Consumer Sentiment is in territory not seen since the height of the pandemic, when it hit an all-time low of 50 in June 2022.

“Consumers report multiple warning signs that raise the risk of recession,” survey Director Joanne Hsu said in a statement. Consumer expectations for business conditions, personal finances, incomes, inflation and labor markets “all continued to deteriorate this month.”

Consumer sentiment near all-time low

The index — benchmarked at 100 back in 1966 — is now lower than at any point during the Great Recession of 2007-2009, when it dropped into the mid-50s. Before that, the Index of Consumer Sentiment’s lowest reading was 51.7, registered in 1980 when the nation was in the grips of a recession and grappling with double-digit inflation.

“Consumers have spiraled from anxious to petrified,” Pantheon Macroeconomics Chief U.S. Economist Samuel Tombs said in a note to clients.

Samuel Tombs

But many real-time indicators of consumers’ spending show no sign of a slowdown, Tombs said, and forecasters at Pantheon Macroeconomics “remain comfortable with our base case that households’ real spending stagnates in Q2 and Q3, rather than drops outright.”

Consumers surveyed by the University of Michigan between March 25 and April 8 said they expect inflation will climb to 6.7 percent in the year ahead — the highest reading since 1981.

“People probably are even more downbeat now,” Tombs said, given that some responses were collected before the April 2 tariff announcement and the plunge in stock prices that followed.

While Democrats are more pessimistic than Republicans about the economy and the prospect of higher inflation, sentiment among all three political groups (Democrats, Republicans and Independents) has deteriorated this year.

Joanne Hsu

That demonstrates declines in national estimates “are not being driven by disproportionate declines among Democrats alone following the election of a Republican president,” Hsu said in a separate report.

Consumer Price Index data released Thursday showed inflation dropped closer to the Federal Reserve’s 2 percent target for the second month in a row in March.

But tariff-driven price increases aren’t likely to show up in the data until May, and Federal Reserve policymakers say they expect tariffs implemented by the Trump administration so far could have an inflationary impact on prices while also slowing economic growth.

John Williams

New York Fed President John Williams said Friday that he expects the combination of reduced immigration, tariffs and uncertainty will slow annual U.S. economic growth to less than 1 percent and drive unemployment up from 4.2 percent to as high as 5 percent over the next year.

“I expect increased tariffs to boost inflation this year to somewhere between 3-1/2 and 4 percent,” Williams said in prepared remarks to the Puerto Rico Chamber of Commerce.

Alberto Musalem

Addressing the Arkansas Bankers Association on Friday, St. Louis Fed President Alberto Musalem said declining consumer confidence, higher prices and lower real incomes associated with tariffs, and diminished wealth resulting from lower equity prices are all “notable actual or potential headwinds.”

Musalem noted that even before the recent tariff announcements, “surveys indicated consumer confidence had declined, which poses downside risk to household spending and the overall pace of economic activity going forward.”

Susan Collins

Susan Collins, president of the Federal Reserve Bank of Boston, told Yahoo Finance she expects tariffs will slow economic growth and push inflation well above 3 percent this year, which might mean the Fed waits longer to cut interest rates this year.

Williams, Musalem and Collins are all voting members of the Fed’s rate-setting policy team, the Federal Open Market Committee, which meets next on May 6-7. Futures markets tracked by the CME FedWatch tool show investors don’t expect the Fed to cut rates until June and that the odds of a June rate cut have dropped from 94 percent on April 4 to 76 percent Friday.

Worries about the impacts of tariffs have hammered the stock market, which initially helped bring mortgage rates and yields on government bonds down as investors moved money out of stocks and into bonds in a flight to safety.

But in recent days, bond yields and mortgage rates have been headed back up, as the Trump administration moved forward with a 145 percent tariff on goods from China and a 10 percent baseline tariff that applied to most other U.S. trading partners.

China — America’s third-largest trading partner — has vowed to fight tariffs “until the end,” initially ratcheting up retaliatory duties on U.S. goods to 84 percent and then to 125 percent on Friday.

Mortgage rates bounce back

After retreating to a 2025 low of 6.48 percent on April 8, rates on 30-year fixed-rate conforming mortgages bounced back to 6.82 percent this week, according to rate lock data tracked by Optimal Blue. Rates on jumbo mortgages exceeding Fannie Mae and Freddie Mac’s $806,500 conforming loan limit in most markets hit 6.93 percent Wednesday.

Yields on 10-year Treasurys — a barometer for mortgage rates that Treasury Secretary Scott Bessent has said is also a key metric for the Trump administration — have also climbed from a 2025 low of 3.89 percent on April 4 to 4.49 percent a week later.

In announcing a 90-day pause on country-specific “reciprocal” tariffs on dozens of U.S. trading partners on April 9, Trump indicated that he’d been watching bond yields rise, noting “people were getting a little queasy.”

“The Treasury market freaked everyone out this week,” when yields climbed even as the stock market tanked — the opposite of the usual flight to safety reaction, Wall Street Journal columnist Jon Sindreu noted Friday.

Sindreu explored several theories that have been floated for the lack of demand for government bonds that’s been pushing rates up.

A leading theory is that hedge funds that buy bonds and sell futures contracts against them have been forced to unwind such “Treasury cash-futures basis trades” by selling government bonds — an issue that sent rates soaring in March 2020.

Others have speculated that China has been paring down its $800 billion in U.S. debt holdings — a move “that would have caused far more havoc than actually occurred,” Sindreau concluded.

To Sindreau, the simplest explanation is that investors are worried that a trade war will upend global trade, which is making them “less confident in holding U.S. financial assets. The ultimate outlet for this is the dollar, which keeps plummeting against major developed currencies, and may have much lower to go.”

Optimal Blue data lags by a day, but rates tracked by Mortgage News Daily (MND) showed rates on 30-year fixed-rate conforming mortgages climbing again Friday by 10 basis points. Most U.S. home loans are funded by mortgage-backed securities (MBS) that are viewed by investors as comparable to 10-year Treasury notes.

“As with much of this week’s drama, today’s move didn’t have one distinct motivation,” MND Chief Operating Officer Matthew Graham wrote. “The weakness speaks to a broad shift in the outlook for U.S. Treasury demand. Digging any deeper would require esoteric explanations of underlying market structures. The bottom line is that investors are rattled by rapid changes in policy, as well as uncertainty about how those changes will ultimately settle and impact the market.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | Sep 10, 2024 | Industry, News Feed

Whether it’s refining your business model, mastering new technologies, or discovering strategies to capitalize on the next market surge, Inman Connect New York will prepare you to take bold steps forward. The Next Chapter is about to begin. Be part of it. Join us and thousands of real estate leaders Jan. 22-24, 2025.

At long last, the commission lawsuits saga appears to be entering a new chapter. The big names have settled, new rules have rolled out, and while unknowns remain, the big question of yesteryear — Will the industry bend? — has been answered (the answer was yes).

But that doesn’t mean the fight over real estate rules is over. Enter Clear Cooperation.

Clear Cooperation is a National Association of Realtors policy that requires agents to put their listings into their NAR-affiliated multiple listing service. The policy’s goal was to crack down on “pocket listings,” which are properties that get marketed privately, but it has been polarizing from the get-go. Some heralded it as a way to improve equal access to housing, but others have criticized it as legally dubious or an example of micromanaging.

The policy was somewhat eclipsed as a headline-grabber during the height of commission lawsuit litigation. But later this week, an NAR committee will return to the policy to begin considering whether it needs to change — or even end entirely.

It remains to be seen what may come of this meeting. But Clear Cooperation remains a central focus of federal regulators, it’s still polarizing in the industry, and with other antitrust litigation moving into the rearview mirror, it may represent the next and biggest frontier in the fight over the future of real estate. In other words, it is quickly becoming an issue du jour when it comes to questions over how agents live, work and get paid.

What exactly is happening now?

The upcoming NAR meeting will take place in Chicago on Thursday and Friday and will include the organization’s Emerging Issues Advisory Board, which is a subgroup of NAR’s MLS Committee. The board includes 23 members who work as brokers, MLS executives and in technology, among other things. The meeting is closed to the public, but the board can invite interested parties to submit comment.

The meeting could lead to a variety of outcomes. The board could, for example, opt to send the issue to the MLS Committee to take some sort of action or to another governing body within NAR. It could also choose to continue gathering information, including but not exclusively during its upcoming NAR NXT conference, which will take place in Boston.

The board meeting consequently does not guarantee any particular outcome but is effectively a first step if change of some sort were to eventually take place.

In anticipation of the meeting, the WAV Group conducted a survey on Clear Cooperation in recent days. The survey elicited 670 responses from members of brokerages, MLS leadership and MLS staff. According to a statement on the survey, 28 percent of respondents recommended keeping the rule as-is, while “the majority want to change or remove the policy.”

“Interest in removing the policy completely or making it optional and reworking it differed between MLSs and brokerages,” the WAV Group further reported. “Fifty-one percent of brokerage respondents recommended removing the policy. Forty percent of MLS respondents suggested making the policy optional and/or reworking the policy, the predominant answer for MLS leaders and staff.”

A history of polarization

This week’s meeting comes nearly five years after NAR adopted Clear Cooperation via overwhelming support from the organization’s board. The rule specifically states that “within one (1) business day of marketing a property to the public, the listing broker must submit the listing to the MLS for cooperation with other MLS participants.”

However, despite the broad support from NAR’s board, Clear Cooperation has been polarizing. Some industry heavyweights, such as Chicago area-based MLS Midwest Real Estate Data (MRED) and Bright MLS, publicly backed the policy in 2019. Redfin CEO Glenn Kelman was also a prominent voice in favor of cracking down on pocket listings and passing Clear Cooperation.

But other industry figures did not support the rule. They included the Austin Board of Realtors (ABoR) MLS, as well as prominent brokers such as Mauricio Umansky and Gary Gold — the latter of whom argued against a pocket listing ban by saying agents should not be “treated like children.”

Much of the debate in 2019 centered on issues of privacy versus equitable access to housing. On the one hand, agents such as Gold argued that homesellers were entitled to keep their homes and identities out of the public eye. They also argued that agents should be allowed to market properties as they see fit.

However, others argued that by keeping listings private, some consumers — especially minorities and those without powerful social networks — were effectively blocked from considering certain homes or neighborhoods. Proponents also argued that consumers generally benefit from having all listings available to them in one place.

One of the other lingering questions surrounding clear cooperation is whether or not the policy is actually effective. So far, the results appear mixed.

Two years after NAR approved Clear Cooperation, for instance, Inman reported that pocket listings remained common despite Clear Cooperation. Redfin found similar results, revealing in December 2021 that 43 percent of agents felt pocket listings had actually become more common in the wake of Clear Cooperation’s adoption. Nearly two years later, in 2023, Redfin Senior Director of Operation Joe Rath told Inman Clear Cooperation could be backfiring.

Last week, Inman reached out to Jonathan Miller — president and CEO of Miller Samuel, Inc. — who tracks pocket listings in Los Angeles. Miller has found that such listings do appear to be trending downward as a share of overall listings.

Credit: Jonathan Miller

However, when asked about the cause of this downward trend, Miller pointed to a softer market and L.A.’s so-called “mansion tax.” Which is to say, it’s unclear what relationship the waning of pocket listings in Los Angeles has to Clear Cooperation specifically.

A key part of the industry’s ongoing legal saga

Clear Cooperation was somewhat overshadowed recently by NAR’s now-defunct Participation Rule, which required sellers’ agents to offer compensation to buyers’ agents. That rule was a centerpiece of numerous commission lawsuits. That litigation and the subsequent settlements led to new NAR policies and the end of the Participation Rule.

However, one of the looming unknowns in the broader commission saga has been the U.S. Department of Justice — and the DOJ is very much interested in Clear Cooperation.

The DOJ is currently locked in a legal battle with NAR that began in 2020 with a lawsuit and simultaneously announced settlement. The DOJ later backed out of the settlement and resumed its investigation, focusing on both the Participation Rule and Clear Cooperation. This legal battle is now potentially headed for the U.S. Supreme Court. Critically, the Participation Rule is now gone but Clear Cooperation is not, setting the stage for further wrangling over the issue.

Clear Cooperation is also the subject of other legal action. Private listing networks The PLS.com and Top Agent Network (TAN) have both sued over the policy. Last month, a court set a Nov. 3 trial date in TAN’s case. Clear Cooperation is additionally a part of Homie’s lawsuit against NAR.

Battle lines are drawn

A number of key players have weighed in on the issue recently.

Robert Reffkin

One of the most prominent is Compass CEO Robert Reffkin, who used his company’s most recent earnings call to describe the policy as “anti-homeowner” and a “killer of value.” Reffkin also argued Clear Cooperation is ultimately doomed, pointing to litigation over the issue.

Last week at a RISMedia event, Reffkin reiterated criticism of Clear Cooperation, describing the policy as “forced cooperation” and urging NAR to repeal it.

Compass additionally told Inman that it is one of “nearly 70 brokerages” that are calling for the repeal of Clear Cooperation.

Inman reached out to a sampling of companies and individuals that may oppose Clear Cooperation, but those that responded declined to comment on the record. However, part of the argument against the rule appears to be that it hampers innovation and that it opens up the industry to further major and disruptive litigation.

The WAV Group survey identified similar issues, noting in a statement that “brokers interested in removing the policy were most concerned about getting named in another round of litigation.” The survey also found that support for removing Clear Cooperation was higher among larger brokerages.

Leo Pareja

But not everyone wants to jettison Clear Cooperation. For instance, eXp Realty CEO Leo Pareja also appeared at the RISMedia event and said he disagrees with Reffkin.

“I fundamentally believe in organized real estate and how it functions in North America,” Pareja said. “We have a complete, accurate, liquid marketplace, which is the beauty of the MLSs.”

When Inman reached out to eXp about the comments, the company provided a statement from Holly Mabery, senior vice president of broker operations, who said “a centralized platform like the MLS” will ensure “a comprehensive and robust marketplace.”

In an email to Inman last week, Consumer Federation of America Senior Fellow Stephen Brobeck spoke out in favor of Clear Cooperation.

Stephen Brobeck

“In most instances, it does not benefit sellers or buyers for a broker to only promote listings within their own agency,” Brobeck said. “Sellers are likely to receive a lower sale price, and buyer choice is restricted to a limited group of properties.”

Brian Boero, CEO of real estate branding and strategy company 1000Watt, also weighed in via a blog post on Friday. Boero expressed support for the policy, arguing that Clear Cooperation “should stand, and be fought for.” But his commentary was also notable for breaking down battle lines in the debate. Companies such as Zillow, he argued for example, “have created big consumer audiences around MLS data and earn significant parts of their revenue by referring leads to buyer agents.” According to Boero, they have an incentive to preserve Clear Cooperation.

On the other hand, whether brokerages benefit or suffer from the rule depends on their structure, Boero said.

Brian Boero

“A brokerage like Compass has concentrated market share in several key areas,” he argued. “Keeping more listings private will create more in-house deals for them. Other big brokerages, especially those that are virtual, like eXp, have broad market share — lots of agents spread relatively thinly. In-house networks aren’t as powerful for them, and they are therefore more likely to support leaving [Clear Cooperation] in place.

Boero also wrote that MLSs may support Clear Cooperation because “they do not want yet another piece pulled from their Jenga tower.”

Time will tell if pressure to change Clear Cooperation ends up amounting to anything. But Boero’s analysis highlights the way the issue intersects with different parts of the industry in different ways. And that means pressure to change is unlikely to abate any time soon.

Email Jim Dalrymple II

by Matt Carter | Aug 12, 2024 | Industry, News Feed

Despite an ever-changing housing market, second homeownership is still attainable for buyers looking for a home to make lasting memories with their loved ones — thanks to a variety of financing options, stabilizing interest rates and the new model of LLC co-ownership. As a real estate agent, you can play a crucial role in educating your clients about these opportunities and providing them with the right resources.

Second home hidden expenses

When shopping for an ideal second home, it’s essential for buyers to look beyond the property’s list price and monthly mortgage payments. Owning a second home comes with additional financial responsibilities. Help your clients budget for:

- Home furnishings and essentials

- Homeowners insurance

- Property taxes

- Utilities

- Maintenance and upkeep

- HOA dues

Exploring financing options

There are several options for financing a second home or vacation property, each with unique benefits and considerations:

- Conventional mortgage loan: This is a good choice if your clients have limited assets and prefer not to use equity from their primary residence. Note that second-home mortgages often have more stringent requirements.

- Cash or cryptocurrency: Paying with cash allows for a mortgage-free purchase or a sizable down payment, reducing the amount financed and lowering monthly payments.

- Home equity line of credit (HELOC): Clients can use the equity in their primary residence to open a revolving line of credit for their second home. HELOCs typically offer lower variable interest rates but can impact credit scores due to large equity access.

- Home equity loan: This is similar to a HELOC but offers a fixed interest rate and a lump sum payout. Repayment occurs in monthly installments, like a conventional mortgage.

- Cash-out refinance: Refinancing the primary mortgage for more than the remaining principal amount allows clients to use the extra cash for a second home. This option is beneficial if current interest rates are lower than those on the existing mortgage.

Key differences in second home mortgages

While financing a second home shares many steps with a primary home mortgage, there are crucial differences your clients should know about.

- Loan limitations: FHA and VA loans are exclusive to primary residences. Clients will need a conventional loan for a second home purchase.

- Larger down payment: At a minimum down payment on a second home generally starts at 10 percent, depending on your credit score, and is typically 25 percent or more.

- Higher credit score requirements: A minimum credit score of 640 is usually required, though higher down payments can offset lower credit scores.

- Higher interest rates: Second home loans often have higher interest rates due to increased lender risk. Clients should be prepared for this when planning their budget.

Defining the second home

The classification of a second home as a “vacation home” versus an “investment property” significantly impacts loan requirements. Vacation homes generally face more relaxed requirements.

Once your clients find the perfect second home, the pre-approval and financing process begins. Pre-approval might take longer due to stricter criteria, but the overall process from offer acceptance to closing typically takes 30 to 45 days.

Financing options for co-ownership

Co-ownership enables multiple individuals to purchase property together and share usage rights. Because each party is only responsible for a portion of the full purchase price, co-ownership can be a practical way to purchase and own an asset like a vacation home that might be too expensive on your own.

Financing options for co-ownership overlap with the options available for buying a whole home, but requirements may be different for this alternative type of ownership.

Pacaso’s competitive integrated financing

Together with our banking partners, Pacaso offers flexible ways to own a luxury vacation home, with integrated financing options, including rates as low as 5 percent and zero down at closing. The approval process is straightforward and fast, and can be completed in a few days to a week once all documents are provided. Explore Pacaso homes that qualify for special financing today.

By understanding these aspects of financing, you can better educate your clients and help them make informed decisions, ensuring a smooth and successful buying experience.