by Christy Murdock | May 8, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

From community involvement to agent celebrations, founder Gaetano Marra has built a real estate brokerage where fun is an important part of the business plan. The former schoolteacher’s self-named brokerage started out as an indie, then joined Better Homes and Gardens Real Estate in 2020, rising to become one of the company’s standouts within its first five years.

“After years of working in various roles within the real estate industry, I decided to pursue my dream of creating a brokerage that would not only reflect my values but also provide a service experience that went above and beyond expectations for both agents and clients,” Marra said.

The formula is working, according to Marra: “We’re growing by leaps and bounds! Last year, our business was up almost 50 percent year over year, while all of the major competitors in our market were down by double digits.”

With a 99 percent retention rate (and a “killer game room”), learn how this broker-owner is setting a new standard for fun, with an eye on bringing his brand of brokerage to the rest of the state.

Name: Gaetano Marra

Title: Broker/Owner

Location: Fairfield County, Connecticut

Brokerage name: Better Homes and Gardens Real Estate Gaetano Marra Homes

Rankings: Top 20 BHGRE company in U.S.

Team size: 150 agents

Transaction sides (2024): 750

Sales volume (2024): $245 million

Awards: In just five years with Better Homes and Gardens Real Estate, the company earned the Founders Circle designation, a distinction that places the firm among the top 20 of BHGRE companies across the country.

What are 3 things you’d like readers to know about you and your brokerage?

1. When I started my company, I wanted to build something different, something that was more than just a business. The goal was to create an office where both agents and clients could feel at home, where relationships were built on integrity, transparency and a shared focus on achieving the best possible outcomes.

I was very intentional about cultivating a culture where people feel valued, heard and understood.

2. Another important pillar of our success is its deep roots in the local community. All of us understand that a successful business must also be a responsible and engaged member of the community it serves.

The brokerage has made it a priority to support local organizations, sponsor events and participate in initiatives that benefit the Monroe area and beyond. We’re the title sponsor of a charity golf tournament, and we support a local high school sports program as an advertiser on their digital scoreboard.

We also have strong ties to Notre Dame Prep School, a high school that is part of my alma mater Sacred Heart University.

As part of a Connecticut state mandate that requires students to take a financial literacy course, I teach a real estate course in three area high schools. I teach students how to become a real estate agent, explain how they get paid and stress the significant impact owning a home can have on building personal and generational wealth.

We offer first-time homebuyer seminars. I also host a community-focused podcast called “The Expect Better Podcast,” where we focus on life, people, business, and relationships. We have guests from local businesses and nonprofit organizations and even well-known celebrities join to share their stories.

At the end of the day, the podcast — like our business — offers a great way to forge understandings and connections across the diverse landscape in which we live and work.

3. Our 150 agents work across three offices in Fairfield County, all located in the southwestern corner of Connecticut: Bridgeport, Monroe and Newtown. We’re a diverse group in age, experience and ethnicity, with a number of agents fluent in Spanish, Portuguese, French and Chinese.

Bridgeport is the most populous city in the state, with about 150,000 residents. The city is consistently ranked among the top 25 most ethnically and culturally diverse cities in the U.S. According to the 2020 five-year community survey, 48.2 percent of Bridgeport’s population speaks a different primary language at home other than English. We’re proud that our Bridgeport team reflects the community they serve.

A few miles north is Monroe, a bedroom community for people working in New York City, New Haven and Bridgeport, highly regarded for its award-winning schools, beautiful parks and sustained growth in local business and industry.

Newtown, a little farther north, offers a charming New England town experience with a focus on community, good schools and a relatively low crime rate, but it comes with a higher cost of living. More than a dozen Fortune 500 companies are based in Fairfield County.

Because of the nature of our service area, we work with clients at all price points, from first-time homebuyers to move-up and downsizing clients.

Tell us about a high point in your brokerage career

Learning that we had become one of BHGRE’s top 20 companies earlier this year was absolutely thrilling! I founded the brokerage in 2018 and then joined the brand in 2020 to help me grow the business, so reaching this level of success so quickly in the company’s history was definitely a high point.

This recognition is not mine alone, though. It’s a reflection of the hard work and dedication of every agent, every staff member, and every client who has trusted us with their real estate needs.

I have the absolute best agents and staff in the business, and no one will ever tell me differently. They are the ones behind all of this, and I am so lucky to be able to call each and every one of them family.

But we are not resting on our laurels; we are in the process of expanding our footprint. I like to say we will be painting the entire state of Connecticut green.

What makes a good leader?

My approach to running a real estate company is this: They say if you build it, they will come, but the more important question is, “Will they stay?” I’m proud to say we have a 99 percent retention rate among our agents.

I don’t recruit; both new and experienced agents come to us because of our company culture. Building that culture has been central to my leadership approach, and I love that we have a team that works hard so we can play hard together.

We have sales meetings and trainings once a month to support agents in building their businesses. Every month, the agent with the most production gets a special parking spot and their picture taken sitting in the Top Agent Throne, an ornate, high-backed chair covered in green velvet.

As a way of showcasing our hardworking agents, we have what’s called the Capper Club. When an agent hits their cap of $5 million in sales, they get a custom green jacket made by a local Italian tailor, who just happens to be my cousin. For every time they cap after that, they receive a jade pin to wear on their lapel.

We also have a fun social event like a cruise or axe throwing once a month. We have a full arcade and game room in the Monroe office, with a basketball hoop, poker table and Xbox.

You know what you’re going to get at our firm: A reliable company culture built around inclusiveness, collaboration and celebration.

Email Christy Murdock

This post was originally published on this site

by Lillian Dickerson | May 8, 2025 | Industry, News Feed

The Warburg Realty founder had been at his firm, which he sold to Coldwell Banker in 2021, for more than 30 years. Kevelyn Guzman took over leadership at the firm in 2024.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Nearly a year-and-a-half after handing over the reins of Coldwell Banker Warburg to Kevelyn Guzman, Frederick Warburg Peters has moved to Brown Harris Stevens.

Peters founded Warburg Realty in 1991, and has long been known as a spunky fixture of New York City real estate. The real estate vet sold his company to Coldwell Banker in 2021, and at the end of 2023, announced that he would be stepping into a president emeritus role at the brokerage the following year.

The Real Deal first reported the news based on an email sent out internally at Coldwell Banker Warburg on Thursday. Shortly thereafter, Brown Harris Stevens released a press statement about Peters’ move to the firm.

“The choice of Brown Harris Stevens was an easy one for me,” Peters said in a statement. “[BHS President] Hall Willkie has been a peer and a good friend for decades, and Bess Freedman has steered the company through the 21st century with great skill, modernizing the agent experience while maintaining the high standards of integrity and ethics for which BHS has always been known.”

Despite his move to an emeritus role at Coldwell Banker Warburg last year, Peters has consistently been an active agent since he started his real estate career in 1980. His lifetime transaction volume exceeds $1 billion.

Peters declined to elaborate further to Inman on his reasons for leaving Coldwell Banker Warburg.

Peters was a founding member of the Real Estate Board of New York’s Residential Division and currently serves on the Executive Committee of the Board of Governors. He has been the recipient of multiple REBNY awards over the course of his career, including the Henry Forster Memorial Award for lifetime achievement and contribution to the industry (1996), the Kenneth R. Gerrety Humanitarian Award for service (2010) and the Eileen Spinola Award for distinguished service (2023).

“Fred is synonymous with New York City real estate, and we are honored that he has chosen to continue his meteoric career with us at Brown Harris Stevens,” CEO Bess Freedman said in a statement. “His reputation and knowledge of the city, its buildings, and its people are beyond reproach. I look forward to working with him in this next chapter.”

Some of Peters’ latest deals have included the sale of a $6.3 million Park Ave co-op and the sale of a $5.6 million penthouse on East 74th Street, according to listing portal StreetEasy.

A spokesperson for Coldwell Banker Warburg said, “Coldwell Banker Warburg thanks its founder, Frederick Warburg Peters, for his leadership of not only the firm, but the New York real estate industry. The company wishes him happiness and success in his next chapter. Coldwell Banker Warburg continues to grow and thrive, with a bright future ahead.”

Peters will continue to write his regular column for Forbes as he moves to Brown Harris Stevens. He will be based out of the brokerage’s flagship office at 445 Park Avenue.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

This post was originally published on this site

by Matt Carter | May 8, 2025 | Industry, News Feed

Shares in Guild Holdings gain 10 percent as investors recognize $23.9 million net loss for the quarter was driven by a $70 million writedown in the fair value of Guild’s mortgage servicing rights portfolio.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

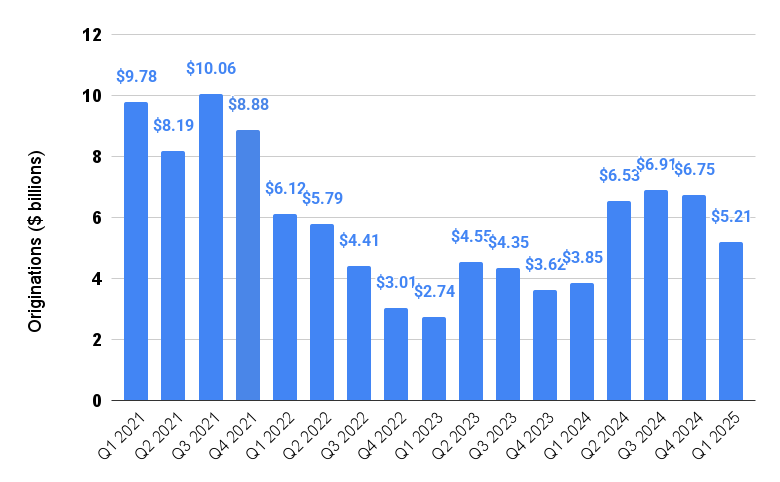

Shares in Guild Mortgage’s publicly traded parent company posted double-digit gains Thursday after the company reported first quarter mortgage originations were up 35 percent from a year ago, to $5.2 billion.

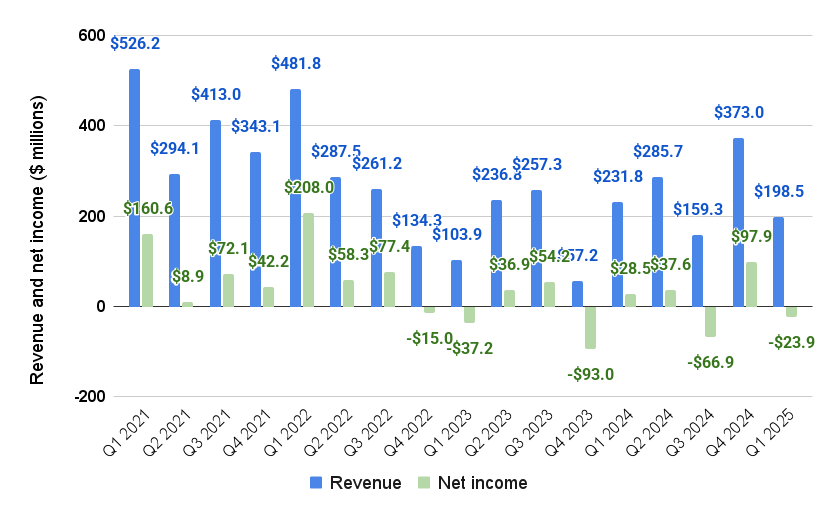

San Diego-based Guild Holdings Company posted a $23.9 million net loss for the quarter, but investors understood that the loss was driven by a $69.9 million writedown in the fair value of Guild’s mortgage servicing rights.

But investors liked the company’s year-over-year growth and higher profit margins, with gain-on-sale margins climbing to 376 basis points, up 59 basis points from Q4 and 12 basis points from a year ago.

Shares in Guild Holdings, which in the last 12 months have traded for as little as $11.21 and as much as $18.25, were up 10 percent Thursday after closing at $12.50 before Wednesday’s earnings announcement.

Guild is a bigger company than it was a year ago, sponsoring 2,728 mortgage loan originators working out of 708 branch locations, according to records maintained by the Nationwide Mortgage Licensing System and Registry (NMLS).

The lender’s growth has been fueled in part by deals like last year’s acquisition of Academy Mortgage Corp. — and First Centennial Mortgage, Cherry Creek Mortgage and Legacy Mortgage in 2023 — but also through organic recruiting efforts.

“These results showcase the benefits of our strategy to invest through market downturns, and we continue to grow at a faster rate than the broader industry,” CEO Terry Schmidt said on the company’s earnings call. “Our year-over-year growth in originations reflects not only the Academy acquisition we made in the first quarter of last year, but also the organic recruiting efforts we’ve completed throughout the past year.”

“These results showcase the benefits of our strategy to invest through market downturns, and we continue to grow at a faster rate than the broader industry,” CEO Terry Schmidt said on the company’s earnings call. “Our year-over-year growth in originations reflects not only the Academy acquisition we made in the first quarter of last year, but also the organic recruiting efforts we’ve completed throughout the past year.”

Guild executives said 88 percent of the $5.2 billion in mortgages originated by the company in the first three months of the year were purchase mortgages, compared to 71 percent for the industry as a whole.

David Neylan

“We have added scale … by successfully retaining loan officers who join via acquisitions, while also welcoming additional new loan officers through organic recruiting at a time when top producers are making a flight to quality,” Chief Operating Officer David Neylan said. “Second, our experience playbook and expertise with onboarding resulted in quickly achieving operational leverage as we grow. This can be attributed to discipline integration efforts from our seasoned teams across the country.”

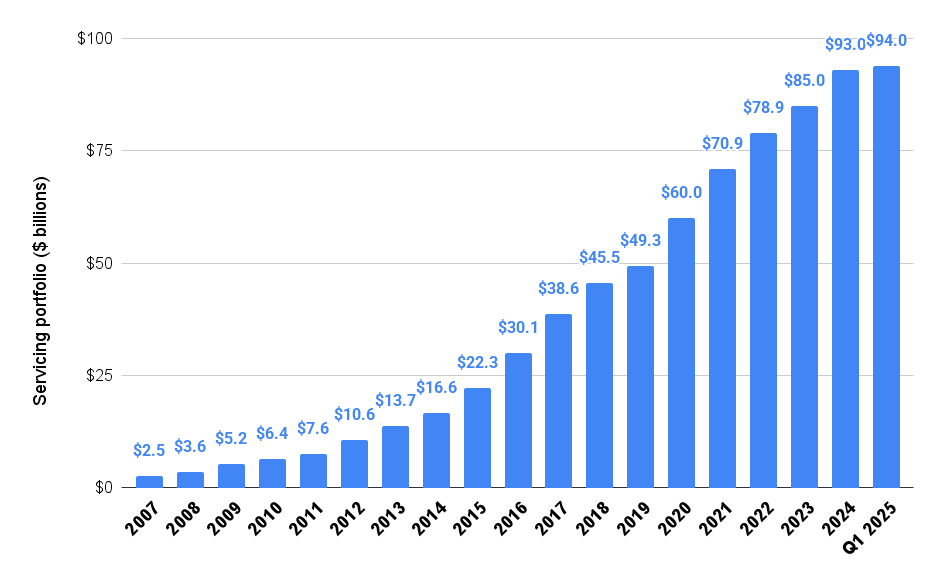

Guild’s mortgage servicing rights portfolio grew to $94 billion during the quarter, up $1 billion from the end of 2024 and nearly $8 billion from a year ago. The company kept the mortgage servicing rights (MSRs) for 60 percent of the loans it originated and sold to investors.

While fluctuations in MSR valuations can be an accounting headache, the loan servicing busines helped Guild “recapture” 31 percent of borrowers who sought to refinance during the quarter, and 26 percent of those who took out purchase loans.

“The loss in this year’s first quarter was primarily due to the downward valuation adjustment of MSRs of $70 million due to the period in interest rate declines,” Chief Financial Officer Desiree Kramer said. “Our servicing portfolio continues to be a valuable source for ongoing cash flow, future opportunities for loan recapture, and it reinforces our customer for life strategy.”

Guild’s $23.9 million loss for the quarter was a big swing from the previous quarter, when the lender posted a $97.7 million profit thanks to an $84.3 million lift from a positive MSR valuation adjustment.

MSR valuations fluctuate with mortgage rates, as a company’s loan servicing portfolio is worth less when mortgage rates decline because borrowers are more likely to refinance and end up with another servicer.

At $198.5 million, net revenue for the quarter was down 47 percent from Q4 and 14 percent from a year ago. But net revenue from Guild’s originations business was up 38 percent from a year ago, to $190.6 million.

“We have built a model designed to perform in every market cycle, and we have successfully navigated multiple cycles throughout our history,” Schmidt said. “Our consistent productivity improvements showcase the strength and deep experience as we continue to thrive, even as the broader market is experiencing prolonged volatility. We do not expect the current conditions to change in the short term, but we are all well positioned for success, even in today’s uncertain landscape.”

Asked whether Guild is on the hunt for acquisitions, Schmidt said “we’re always talking to a lot of suitors.”

The company is selective, “So it’s a long process. Sometimes we’re talking to people for six months, sometimes it’s two years.”

So far this year, organic growth has been stronger than M&A, but “we’re constantly doing both and our brand is extremely strong. There’s still a lot across the country that we can conquer and so we’re going to continue to work on growing the share.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Matt Carter | May 8, 2025 | Industry, News Feed

Shares in Guild Holdings gain 10 percent as investors recognize $23.9 million net loss for the quarter was driven by a $70 million writedown in the fair value of Guild’s mortgage servicing rights portfolio.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Shares in Guild Mortgage’s publicly traded parent company posted double-digit gains Thursday after the company reported first quarter mortgage originations were up 35 percent from a year ago, to $5.2 billion.

San Diego-based Guild Holdings Company posted a $23.9 million net loss for the quarter, but investors understood that the loss was driven by a $69.9 million writedown in the fair value of Guild’s mortgage servicing rights.

But investors liked the company’s year-over-year growth and higher profit margins, with gain-on-sale margins climbing to 376 basis points, up 59 basis points from Q4 and 12 basis points from a year ago.

Shares in Guild Holdings, which in the last 12 months have traded for as little as $11.21 and as much as $18.25, were up 10 percent Thursday after closing at $12.50 before Wednesday’s earnings announcement.

Guild is a bigger company than it was a year ago, sponsoring 2,728 mortgage loan originators working out of 708 branch locations, according to records maintained by the Nationwide Mortgage Licensing System and Registry (NMLS).

The lender’s growth has been fueled in part by deals like last year’s acquisition of Academy Mortgage Corp. — and First Centennial Mortgage, Cherry Creek Mortgage and Legacy Mortgage in 2023 — but also through organic recruiting efforts.

“These results showcase the benefits of our strategy to invest through market downturns, and we continue to grow at a faster rate than the broader industry,” CEO Terry Schmidt said on the company’s earnings call. “Our year-over-year growth in originations reflects not only the Academy acquisition we made in the first quarter of last year, but also the organic recruiting efforts we’ve completed throughout the past year.”

Guild executives said 88 percent of the $5.2 billion in mortgages originated by the company in the first three months of the year were purchase mortgages, compared to 71 percent for the industry as a whole.

David Neylan

“We have added scale … by successfully retaining loan officers who join via acquisitions, while also welcoming additional new loan officers through organic recruiting at a time when top producers are making a flight to quality,” Chief Operating Officer David Neylan said. “Second, our experience playbook and expertise with onboarding resulted in quickly achieving operational leverage as we grow. This can be attributed to discipline integration efforts from our seasoned teams across the country.”

Guild’s mortgage servicing rights portfolio grew to $94 billion during the quarter, up $1 billion from the end of 2024 and nearly $8 billion from a year ago. The company kept the mortgage servicing rights (MSRs) for 60 percent of the loans it originated and sold to investors.

While fluctuations in MSR valuations can be an accounting headache, the loan servicing busines helped Guild “recapture” 31 percent of borrowers who sought to refinance during the quarter, and 26 percent of those who took out purchase loans.

“The loss in this year’s first quarter was primarily due to the downward valuation adjustment of MSRs of $70 million due to the period in interest rate declines,” Chief Financial Officer Desiree Kramer said. “Our servicing portfolio continues to be a valuable source for ongoing cash flow, future opportunities for loan recapture, and it reinforces our customer for life strategy.”

Guild’s $23.9 million loss for the quarter was a big swing from the previous quarter, when the lender posted a $97.7 million profit thanks to an $84.3 million lift from a positive MSR valuation adjustment.

MSR valuations fluctuate with mortgage rates, as a company’s loan servicing portfolio is worth less when mortgage rates decline because borrowers are more likely to refinance and end up with another servicer.

At $198.5 million, net revenue for the quarter was down 47 percent from Q4 and 14 percent from a year ago. But net revenue from Guild’s originations business was up 38 percent from a year ago, to $190.6 million.

“We have built a model designed to perform in every market cycle, and we have successfully navigated multiple cycles throughout our history,” Schmidt said. “Our consistent productivity improvements showcase the strength and deep experience as we continue to thrive, even as the broader market is experiencing prolonged volatility. We do not expect the current conditions to change in the short term, but we are all well positioned for success, even in today’s uncertain landscape.”

Asked whether Guild is on the hunt for acquisitions, Schmidt said “we’re always talking to a lot of suitors.”

The company is selective, “So it’s a long process. Sometimes we’re talking to people for six months, sometimes it’s two years.”

So far this year, organic growth has been stronger than M&A, but “we’re constantly doing both and our brand is extremely strong. There’s still a lot across the country that we can conquer and so we’re going to continue to work on growing the share.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Jim Dalrymple II | May 8, 2025 | Industry, News Feed

Despite a slower housing market, the brokerage’s revenue grew 28.7 percent year over year in the first quarter while transactions rose 27.8 percent.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Compass may regularly polarize the real estate industry, but the company’s assertiveness has apparently not slowed down growth, with a new earnings report showing that it upped revenue, agent count, transactions and various other numbers in the first three months of 2025.

The report, published Thursday, shows that Compass’ revenue in the first quarter grew 28.7 percent year over year to $1.4 billion. The company’s number of principal agents also grew from 14,591 at the end of Q1 in 2024 to 20,656 at the same time this year.

Additionally, Compass agents closed 49,121 transactions during the first three months of 2025, which is up 27.8 percent compared to the first three months of last year.

Compass did still lose money, though the loss of $50.7 million was a significant improvement over the $132.9 million it lost in the first quarter of 2024. The report further notes that Compass was free cash flow positive in Q1, which is important in the brokerage’s case because CEO Robert Reffkin has repeatedly made positive free cash flow a goal.

Robert Reffkin

The report notes several times that Compass’ numbers outperformed the broader market, which saw transactions drop 2.1 percent. Reffkin hit on a similar theme, saying in the report that despite market volatility, his company “continued to widen the gap against the industry.” He also said that Compass has the highest number of top agents and teams.

“Looking ahead, while recent market trends have been somewhat mixed, we remain confident that our playbook and structural advantages position Compass to drive significant upside over time,” Reffkin added.

Compass’ new report further states that the brokerage now has a national market share of 6 percent.

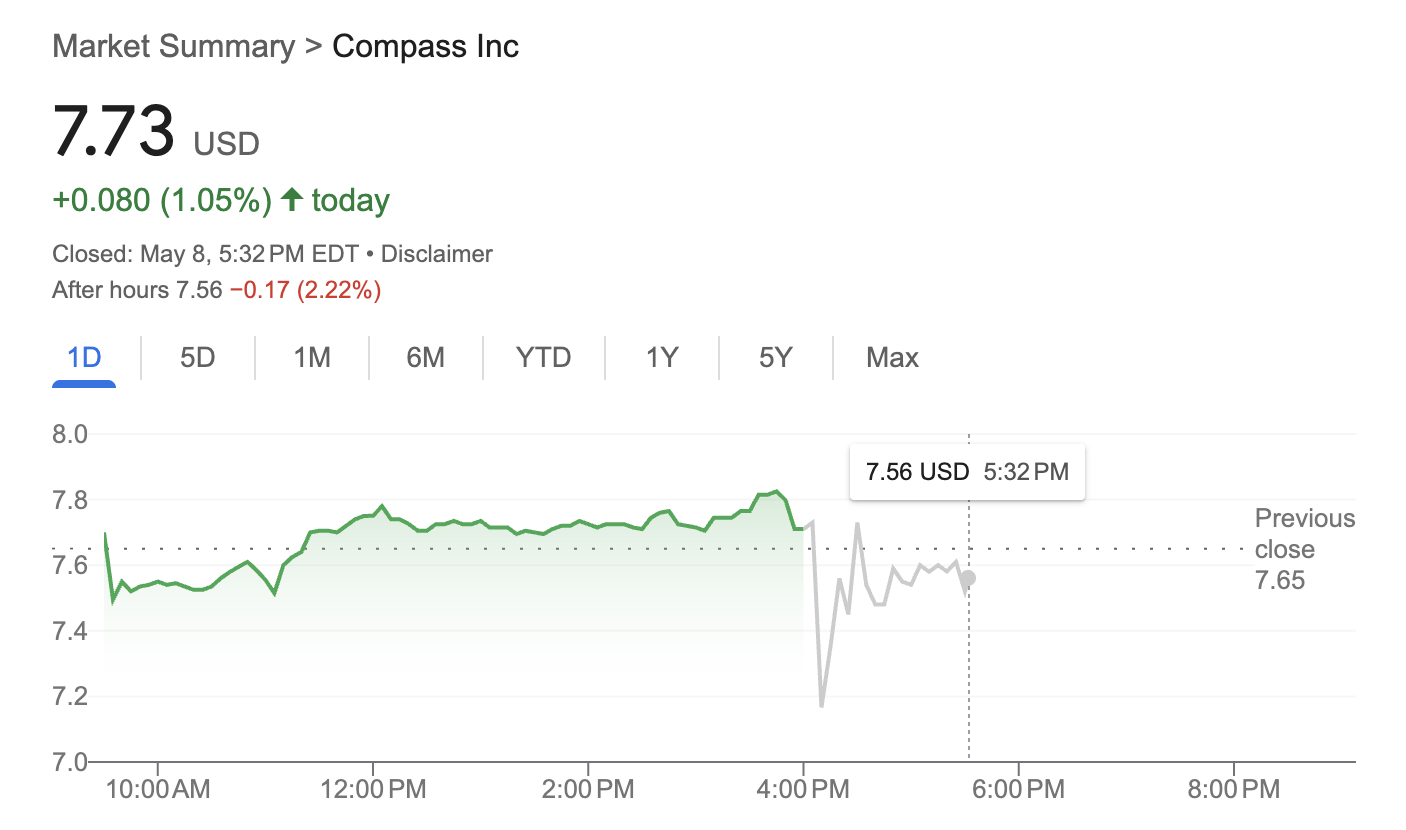

Heading into Thursday’s earnings, shares in Compass were trading in the mid to high $7 range. That was up for the day but down for the week. It also represents a significant improvement over one year ago, when shares in the brokerage were trading in the low $3 range.

Shares trended down slightly in after-hours trading following the publication of Thursday’s report.

Credit: Google

Compass had a market cap of about $4 billion as of Thursday afternoon.

Thursday’s earnings report arrives against the backdrop of an intense push by Compass in favor of private listings. Such listings are a key part of Compass’ “Three-Phase Marketing Strategy,” which sees properties marketed privately first, then marketed as “coming soon” second, and finally entered into a local multiple listing service in the third and last stage of the process.

Reffkin has vocally touted private listings, arguing among other things that homesellers should be able to market properties how they please. And though Reffkin has been the industry’s most vocal proponent of private listings, other brokerages have rolled out their own private listing networks as well.

At the same time, however, private listings have also drawn intense criticism from figures such as eXp Realty CEO Leo Pareja and NextHome CEO James Dwiggins. Moreover, Compass is currently in the beginning stages of a lawsuit with Northwest MLS in Washington state over the issue.

Heading into Thursday’s earnings, there was thus a question about whether Compass’ prominent role in the private listings debate might have some sort of impact on the brokerage’s bottom line or agent count numbers. So far, however, that does not appear to be the case.

Compass’ new earnings report touts the company’s Three-Phase Marketing Strategy, noting that “48.2 percent of homeowners who listed their home with Compass” outside of Washington used the program. That adds up to a total of 19,393 listings, the report notes.

Reffkin also discussed private listings during a call with analysts, saying that homeowners do not want the National Association of Realtors, MLSs or portals telling them how to market their homes. And he criticized MLSs and portals for increasing “friction” in order to discourage private listings. The comment was an apparent allusion to episodes such as the NWMLS situation and Zillow’s recent ban on private listings.

Reffkin also said that there is no downside for homesellers to use Compass’ Three-Phase Marketing Strategy.

“The worst thing that happens is a homeowner gets an offer and they have an opportunity to turn it down and go to the public sites,” Reffkin said. “That’s the downside, which means there is no downside.”

Reffkin later said that he expects to see private listings grow over the next year, and suggested industry incumbents have resisted private listings out of a sense of self interest.

“Agents aren’t stupid,” Reffkin said during the call. “If you need to fine them and ban them to keep them on your platform, there is something wrong with your platform.”

Update: This story was updated after publication with background, additional details from Compass’ earnings report, and commentary from executives’ call with analysts.

Email Jim Dalrymple II

This post was originally published on this site

by Lillian Dickerson | May 8, 2025 | Industry, News Feed

If passed into law, HB 3452 would require brokerages to market properties for sale on public platforms within one calendar day of entering into an agreement with a seller, unless the seller signed a disclosure and an opt-out form.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Heated debates over the National Association of Realtors’ Clear Cooperation Policy have continued even after the association announced its decision over a month ago to keep the policy while adding a new listing option for homesellers. However, Illinois lawmakers are now also adding their voices to the discussion — and may give the policy new weight, if a version of it is passed into law in the state.

House Bill 3452, proposed by Illinois State Representative Lilian Jiménez, would modify the Illinois Real Estate License Act of 2000 so that brokerages would be required to publicly advertise or market properties for sale or for rent on public platforms within one calendar day of entering into an agreement with the seller or landlord of the property, unless that seller or landlord signs a disclosure and marketing opt-out form provided by Illinois’ Department of Financial and Professional Regulation.

The bill was introduced in early February by Rep. Jiménez and has been in committee since March 21. Partners on the bill include the National Association of Hispanic Real Estate Professionals (NAHREP) and Zillow, according to Rep. Jiménez. She serves a district in Chicago where home prices have rapidly risen in recent years; she said one of her goals with the bill was to promote fair housing and buyer access to all homes that are for sale.

“There is a long history of redlining, block-busting and segregation in our communities, and I think the real estate industry, just like every other industry, needs to have a certain level of guardrails — which we can call regulation — but just means that the consumers’ interests are represented,” Jiménez told RealEstateNews.com.

Zillow has likewise made its own attempt at enforcing Clear Cooperation by rolling out new standards that penalize agents who violate the policy by banning their listings from the Zillow platform. Even so, some brokerages, most notably Compass, continue to lean into office exclusive listings. The brokerage recently announced that it would be providing physical books of its exclusive listings in Compass offices across the country.

Illinois Realtors has said that the bill is not on the association’s legislative agenda.

Jeff Baker, the association’s CEO, told RealEstateNews.com that he believes the bill “was less about Clear Cooperation and was more designed to codify a real estate portal’s business model into state law.”

“The bill was never assigned to a substantive committee for further consideration after its introduction,” Baker continued. “Illinois Realtors is committed to ensuring the Real Estate License Act remains a model for both consumer protection and maintaining a fair and level playing field for real estate practitioners.”

Chicago is a somewhat pocket listing-friendly city, as it happens. The city is under the purview of multiple listing service Midwest Real Estate Data (MRED), which has had a Private Listing Network (PLN) for almost 10 years.

Email Lillian Dickerson

This post was originally published on this site