by Craig C. Rowe | May 28, 2025 | Industry, News Feed

Pam O’Connor has joined the advisory board of Maverix Advisory Group, an industry consulting group working with proptech startups and growing brokerages.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Pam O’Connor has joined the advisory board of Maverix Advisory Group, an industry consulting group working with proptech startups and growing brokerages.

O’Connor retired in 2018 after serving as president and CEO of Leading Real Estate Companies of the World since its founding in 1997.

“I worked with Jeff [Kennedy] for almost a decade, and it’s been fun watching him grow Maverix over the past year. I’m excited to be involved and look forward to supporting the shared mission,” O’Connor said in a statement on her placement.

Maverix was launched by Jeff Kennedy, a longtime industry player, who most recently served as vice president of sales and partnerships for Leading Real Estate Companies of the World (LeadingRE). His new firm’s intent is to guide executives and real estate entrepreneurs on go-to-market strategies, product direction and relationship building, among other advisory services.

Kennedy was joined by Kevin Van Eck in February, who previously worked at @properties Christie’s International Real Estate. Kennedy expressed gratitude for O’Connor’s presence in the industry and at Leading RE.

“Pam is one of the most respected leaders in residential real estate,” said Kennedy in the statement. “She’s a visionary, and her ability to see around corners and build world-class organizations is second to none. We’re honored to have her involved as we continue to grow a top-tier advisory platform for our clients.”

At the time of her retirement, Paul Boomsma of Leading RE also praised O’Connor’s leadership.

“With incredible passion, talent and dedication, Pam has spent decades building programs that support the success of independent brokerages. Her influence across the industry is undeniable, and we are immeasurably thankful for her years of leadership.”

O’Connor is joining former MoxiWorks CEO York Baur on the Maverix board, which was created to provide additional guidance to its principals.

The Maverix client list includes Curbio, Final Offer, Rechat, Notable and Courted, among others.

Email Craig Rowe

This post was originally published on this site

by Lillian Dickerson | May 28, 2025 | Industry, News Feed

The former reality television stars known for the USA Network series “Chrisley Knows Best” had been serving multi-year sentences in prison for bank and tax fraud since the beginning of 2023.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Real estate entrepreneur and reality TV personality Todd Chrisley and his wife, Julie Chrisley, have been pardoned by President Trump.

The couple, who became famous for the USA Network reality TV show Chrisley Knows Best, were convicted in 2022 on charges of bank and tax fraud after it was discovered they conspired to defraud Atlanta-area banks out of more than $30 million in loans by submitting false documents, and committed nearly $500,000 in tax evasion while brandishing their lavish lifestyle on TV. The couple also failed to file tax returns and pay taxes for the years 2013 through 2016.

TAKE THE INMAN INTEL SURVEY FOR MAY

When the charade became too much to keep up, Todd Chrisley filed for bankruptcy and “walked away from more than $20 million of the fraudulently obtained loans,” the U.S. Attorney’s Office said in 2022 after the couple’s conviction.

President Trump announced his intentions to pardon the couple in a call with their daughter, Savannah Chrisley, a video of which was posted on social media by a White House aide on Tuesday. The president then signed their pardons on Wednesday, opening a pathway for them to be released from prison.

Todd Chrisley has been serving a 12-year sentence in Florida at the FPC Pensacola minimum-security men’s federal prison since January 2023, and was scheduled for release in April 2032. Julie has been serving a 7-year sentence at the FMC Lexington prison in Kentucky, and was scheduled to be released in January 2028. In addition to their prison sentences, the couple were also ordered to pay $17.8 million in restitution.

In the video posted online on Tuesday, Trump said to Savannah Chrisley, “Your parents are going to be free and clean and I hope that we can do it by tomorrow.”

“They’ve been given a pretty harsh treatment based on what I’m hearing,” Trump later added.

Savannah posted on Instagram on Wednesday a photo of the president with a pair of signed documents in the Oval Office and wrote, “God is still writing your story. He’s Not Late. He’s Not Distant. HE’S NOT DONE, & What is coming is MORE than you could’ve imagined.”

Attorney Alex Little, who is representing the Chrisleys, said in a statement on Tuesday that the pardon “corrects a deep injustice” in which the couple were “targeted because of their conservative values and high profile.”

The move was another example of President Trump pardoning those he views as his allies, friends, donors and supporters. This week, Trump also pardoned Scott Jenkins, a former Virginia sheriff who had been sentenced to prison for 10 years on fraud and bribery charges.

Last month, the president likewise signed a pardon for former nursing home executive Paul Walczak after Walczak’s mother, Elizabeth Fago, attended a $1 million-per-person fundraising dinner hosted by President Trump at Mar-a-Lago.

Walczak had pled guilty to tax crimes shortly after the 2024 election, and submitted a pardon application right around Inauguration Day. Prior to the pardon being signed, Walczak was on track to pay $4.4 million in restitution and serve an 18-month prison sentence.

Email Lillian Dickerson

This post was originally published on this site

by Matt Carter | May 28, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Mortgage giant Fannie Mae is turning to controversial Silicon Valley data analytics company Palantir Technologies to help it detect mortgage fraud, which the head of its federal regulator, Bill Pulte, claims is “rampant.”

Palantir’s “cutting edge AI technology” will help Fannie Mae find criminals who try to defraud it, increasing safety and soundness “by rooting out bad actors in our housing system,” Pulte said in announcing the partnership Wednesday.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

As President Trump’s appointee to lead the Federal Housing Finance Agency (FHFA), Pulte last month sent a criminal referral letter to the U.S. Department of Justice suggesting that New York Attorney General Letitia James had made misrepresentations about two properties she owns in order to receive better loan terms.

James — who won a $486 million civil fraud judgment against Trump that is under appeal — has denied the allegations, calling them baseless.

As FHFA director, Pulte appointed himself the chair of both Fannie Mae and its sister company, Freddie Mac, in March and has been highlighting mortgage fraud as an issue for the companies in recent public appearances.

Appearing on Donald Trump Jr.’s podcast, Triggered, last week, Pulte said he could not comment on James’ case.

Bill Pulte

“But I will say that people claiming that they live in certain states that they don’t live in, people claiming other representations that are maybe not necessarily true — these are very big concerns to the mortgage market,” Pulte said. “It doesn’t matter whether you’re a welder, a plumber, a politician, an attorney — if you commit mortgage fraud, you are a risk to the system.”

In his criminal referral, Pulte claimed James falsified records by stating that a Norfolk, Virginia, home she purchased with her niece was to be her principal residence, the New York Post reported. Separately, Pulte accused James of misrepresenting the number of units in her Brooklyn residence to obtain better loan terms.

“Occupancy fraud is a huge issue in the country where people are basically getting loans based on certain down payments and certain interest rates, based on saying that they live in one area and not another, as well as saying that they should qualify for loans that maybe they shouldn’t have,” Pulte told Trump Jr. “So, you know, just generally speaking, my thought is that mortgage fraud is rampant and we are doing everything we can. We’ve made a number of criminal referrals — not just [James] — and we will continue to prosecute.”

Letitia James

James has acknowledged a clerical error on a 2023 power of attorney form related to the purchase of the Virginia property, but denies wrongdoing.

“This investigation into me is nothing more than retribution,” James told the Post.

Palantir’s business booming under Trump

Palantir has a long history as a government contractor, providing services to a range of federal agencies including the IRS, the National Institutes of Health and the Department of Veterans Affairs that generated $1.2 billion in revenue last year. During the first quarter of 2025, new defense contracts helped the company grow revenue from federal contracts by 45 percent from a year ago, to $373 million.

But Palantir has come under greater scrutiny during the Trump administration as it wins business that raises privacy concerns, such as an Immigration and Customs Enforcement (ICE) contract to build a platform that tracks the movements of immigrants.

A senior IRS official told CNN last month that employees at the agencies are concerned that Palantir is sifting through taxpayer data to track down immigrants and deport them.

Silicon Valley investor Paul Graham has accused Palantir of “building the infrastructure of the police state,” and demanded that the company make a public commitment that it will not build tools that could be used by the government to violate citizens’ rights, NPR reported this month.

“Palantir designs and deploys artificial intelligence and machine learning technology used by government agencies and commercial clients,” Fannie Mae said in a press release Wednesday. “The company’s technology provides expansive monitoring for anomalous transactions, activities, and behaviors to help companies detect suspicious activity and trigger investigative action.”

While Palantir co-founder Peter Thiel is a Trump supporter and donor, CEO Alex Karp is a Democratic donor who supported Kamala Harris for president, CNN noted.

Alex Karp

“This partnership with Fannie Mae will set off a revolution in how we combat mortgage fraud in this country,” Karp said in a statement. “We are bringing the fight directly to anyone who attempts to defraud our mortgage system and exploit hardworking Americans.”

How Fannie and Freddie deal with fraud

Fannie and Freddie don’t make loans themselves but buy mortgages from lenders and bundle them up into mortgage-backed securities (MBS) that are sold to investors. MBS are the ultimate source of funding for most U.S. home loans, and homebuyers enjoy low rates largely because the mortgage giants guarantee payments to investors.

Fannie Mae and Freddie Mac have the right to demand that lenders buy back mortgages if it’s later discovered that borrowers, sellers, real estate agents, lenders or appraisers made significant “misstatements, misrepresentations, or omissions” in selling loans to them.

Fannie and Freddie will only require lenders to buy back loans with misrepresentations when they identify a common pattern of activity on three or more loans made by the same lender. But there’s no such exemption for instances of fraud.

Fannie Mae specifies that it can require lenders to repurchase any mortgage where fraud is established in court or its investigators find “clear and convincing evidence” that a lender or other party “knowingly executed or participated in a scheme” to defraud it.

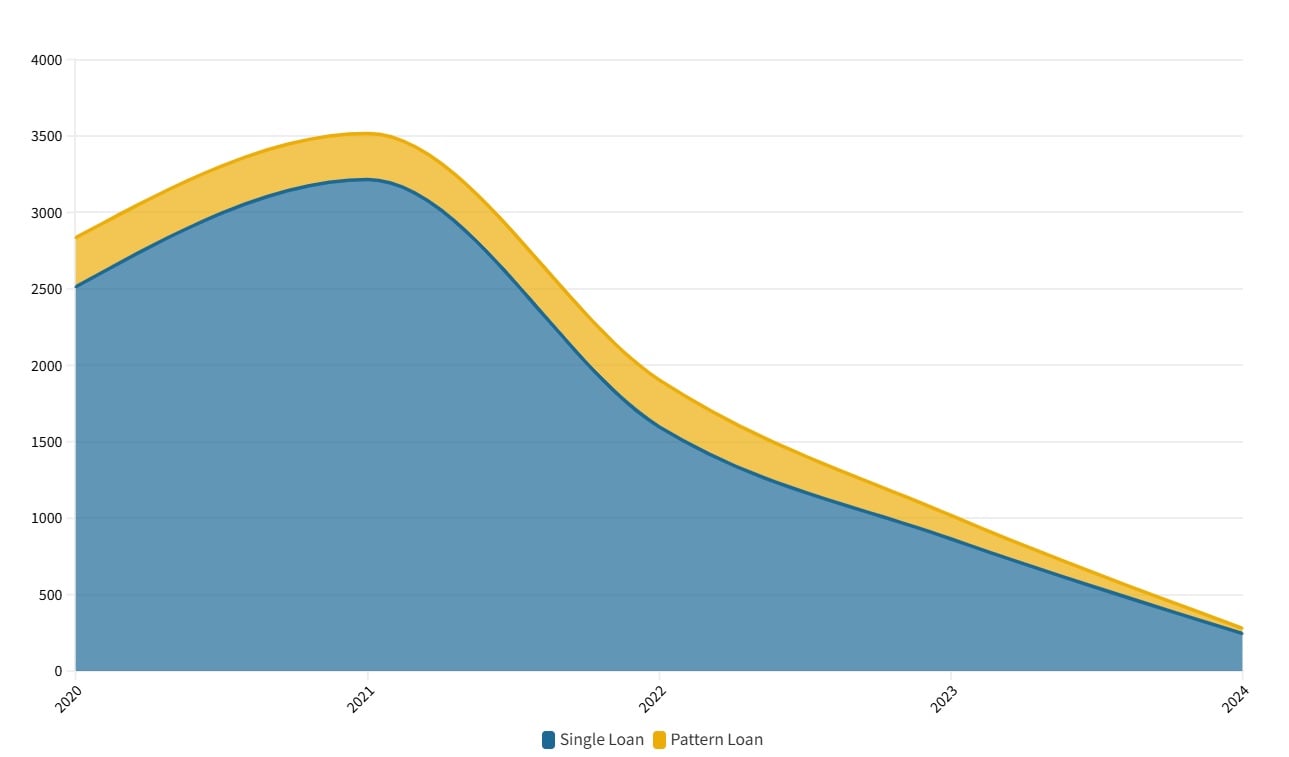

Fannie Mae fraud findings

Fraud findings on Fannie Mae-backed mortgages, 2020-2024. Source: Fannie Mae.

Mortgage fraud can go undetected for many years and is often discovered only when a borrower stops paying their loan.

So far, Fannie Mae’s Financial Crimes team has uncovered evidence of fraud in 3,517 single-family loans originated in 2021, including 3,215 single loans and 302 “pattern loans” — loans in which a common pattern of activity involving the same individual or company was discovered.

Through May 8, Fannie Mae investigators had uncovered evidence of fraud in only 280 loans originated last year — 245 single loans and 35 “pattern loans.”

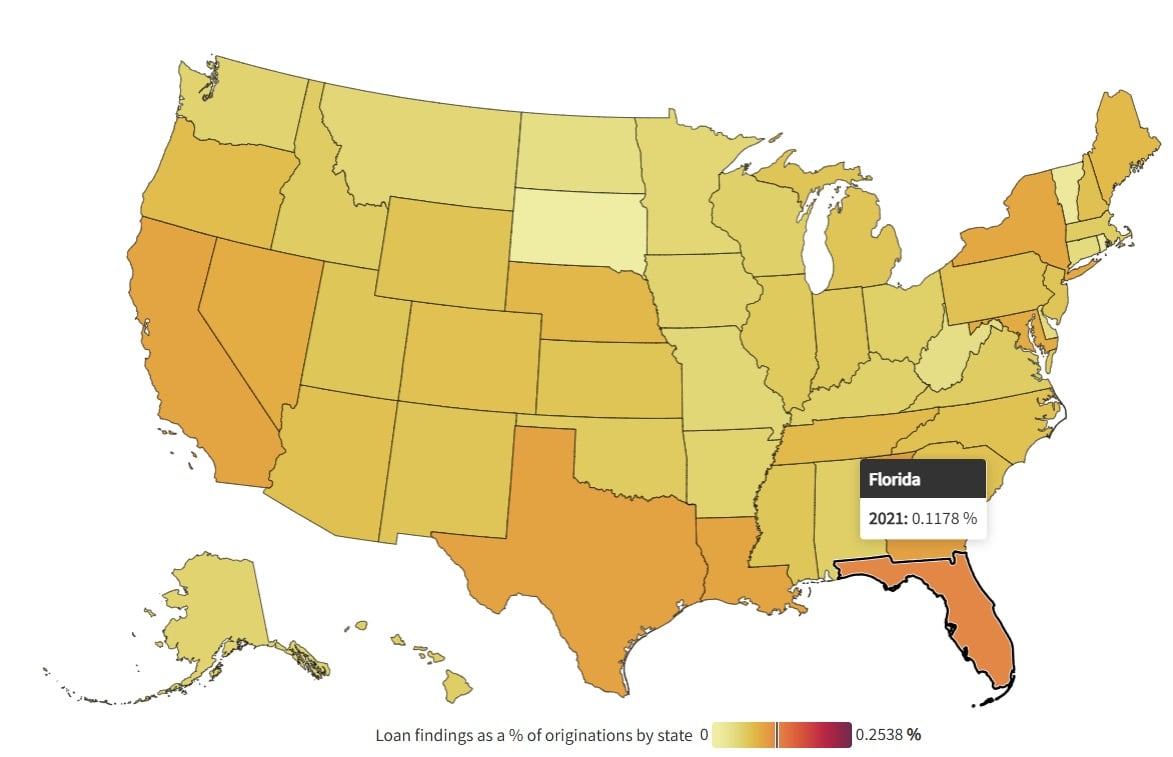

Loan fraud prevalence by state

Fraud as a percentage of Fannie Mae-backed loans originated in 2021 by state. Source: Fannie Mae.

With mortgage rates at historic lows, Fannie Mae in 2021 provided backing for 4.8 million single-family loans — 1.5 million purchase loans and 3.3 million refinancings.

In Florida, the state with the highest percentage of fraudulent loans, about 12 in 10,000 loans (0.12 percent) originated in 2021 were later found to have potential fraud issues.

In an October 2024 report, CoreLogic said about 1 in 123 mortgage applications lenders received in Q2 2024 showed indications of fraud, up 8 percent from a year ago. Fraud was more likely to show up in purchase applications (1 in 111) than in requests to refinance (1 in 171).

CoreLogic determined that New York, Florida, California, Connecticut and New Jersey are the states where lenders are at the highest risk for fraud.

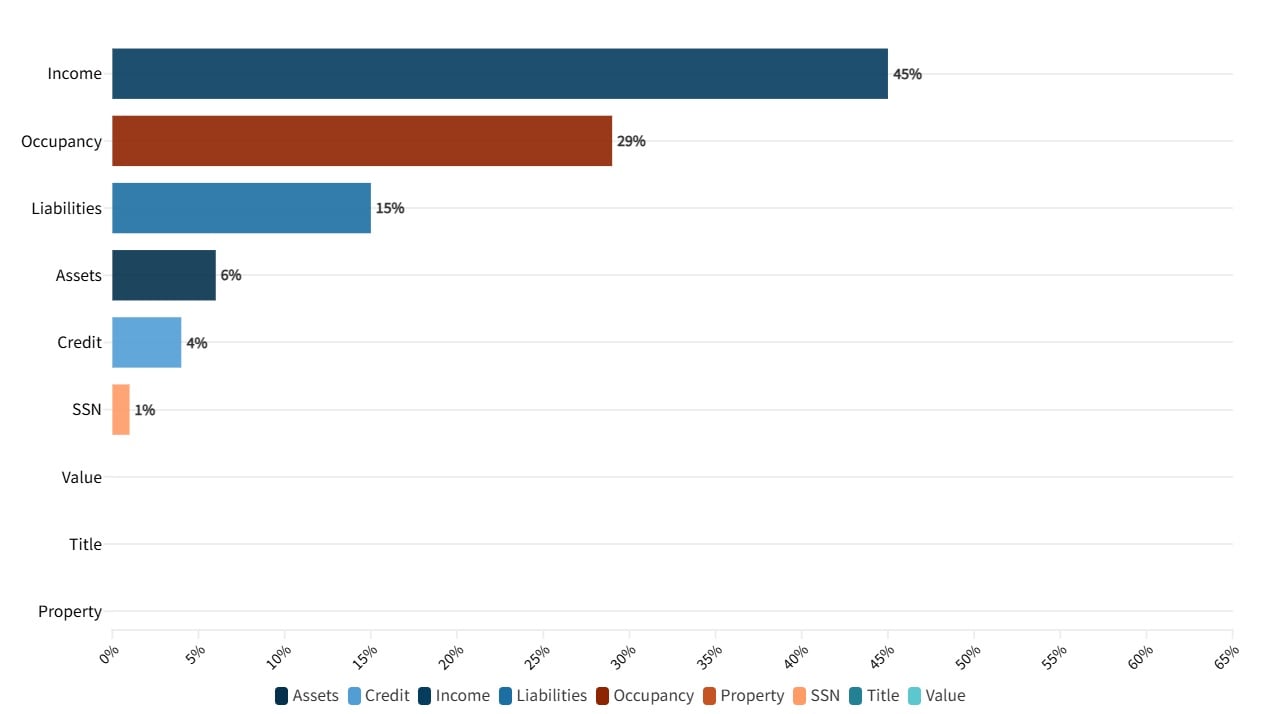

Most prevalent types of fraud

Types of fraud discovered on Fannie Mae-backed mortgages originated in 2024. Source: Fannie Mae.

Income misrepresentation was the most common type of fraud uncovered on loans backed by Fannie Mae last year (45 percent), followed by false occupancy claims (29 percent), understated liabilities (15 percent), overstated assets (6 percent), inflated credit (4 percent) and false social security numbers (1 percent).

Third-party mortgage brokers were blamed for much of the fraud that occurred in the subprime lending boom that preceded the 2007-2009 housing crash and Great Recession.

But mortgage brokers were involved in only about one in five Fannie Mae loans (19 percent) originated last year in which fraud is suspected, with third-party correspondent lenders involved with another 23 percent.

Most loans (58 percent) in which evidence of fraud was discovered were made by “non-third party” lenders like independent mortgage banks.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Summer Goralik | May 28, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

I’d been waiting for it — refreshing the docket more often than I care to admit. When Professor Tanya Monestier’s appeal brief finally dropped, challenging the court’s approval of the National Association of Realtors’ $418 million settlement, I opened it immediately.

Despite being exhausted and juggling more deadlines than I’d like to admit, I started reading this monster of a brief after 10 p.m. I didn’t even need coffee to stay focused. That’s a rarity when diving into dense legal writing after hours. Once I got going, I couldn’t put it down.

This wasn’t legal commentary. It read like a novel, with the kind of twist that changes everything. One moment, I was in a world where the biggest real estate settlement in modern history had been finalized. The next, I was staring at a legal reality that might not exist at all.

Reading Monestier’s argument felt like watching The Truman Show’s final scene, when Truman sails to the edge of the horizon, crashes into a wall and realizes everything around him has been a carefully controlled illusion.

“We accept the reality of the world with which we’re presented,” says Christof, the show’s omnipotent director.

That’s exactly what the real estate industry did and even many of its critics. We accepted the reality of the NAR settlement, believing it was valid, final and fair. But Monestier handed us a legal hammer and said: Tap that wall. And when you do, you’ll see the foundation might not just be cracked. It might be imaginary.

Optimist or idiot?

OK, I’ll admit it. Last November, I thought the court might actually reject the settlement or at least send it back for serious modification.

Not just because of the Department of Justice’s last-minute Statement of Interest, which flagged clear antitrust concerns, but because of the objections. Monestier’s, in particular, cut to the heart of class action fairness: The lack of meaningful injunctive relief, the workarounds already underway by some Realtors, the disproportionate attorney fees and the insultingly low payouts to harmed sellers.

Her filing was detailed, methodical and meticulously cited, supported by evidence showing how the supposed reforms were being undermined even before they took effect. I truly thought her objection might make a difference.

I was one of the optimists, one of the people who thought: Maybe this is the moment the system will actually pause and take a harder look. Between the objections and the DOJ’s Statement of Interest, it felt like there were serious issues worth addressing.

Was this finally one of those rare instances where the outcome might reflect reality? A moment when the court would pause, take a harder look and demand real changes before ushering in a new era of rules.

But that hope gave way to acceptance. The settlement was approved. The story moved on. And I, like so many others, moved on with it.

That is, until I read Monestier’s appeal.

Suddenly, the question of justice wasn’t settled. It was unsettled all over again. Her account didn’t just challenge the terms of the deal. It challenged the process itself.

Roll credits? Not quite. Turns out we were only halfway through the movie

Notably, Monestier describes how objectors were sidelined — and how the court instructed plaintiffs to ghostwrite the final approval order before the fairness hearing even occurred. (I’m still shaking my head at this one.)

She also explains how objections were struck not on the merits, but because most objectors, including Monestier herself, couldn’t travel across the country just to be heard, despite a court notice that said showing up wasn’t required.

If her account is accurate, justice wasn’t served. It almost feels staged.

And perhaps I shouldn’t be surprised. After all, I’ve spent years watching real estate fraud cases unfold. I’ve seen bad actors slip through the cracks while their victims are left picking up the pieces. I’ve had my belief in the system tested and defeated before.

But this one exposed something deeper: how quickly procedure can overpower principle when no one slows down to ask the right questions.

The legal foundation nobody checked

Although I’m not an attorney, here’s the legal crux that floored me: Monestier argues the entire settlement rests on injunctive relief that the plaintiffs didn’t even have standing to seek.

In plain terms, these were past sellers. They’re not at risk of being harmed again. There’s no concrete allegation that they’ll sell another home anytime soon, let alone use a broker — or more specifically, a Realtor.

What Monestier’s brief makes crystal clear is this: You can’t settle a claim for future harm unless the plaintiffs are actually likely to face that harm. That’s basic constitutional law. Article III requires it.

So how did this get approved?

How did millions of dollars change hands, how did sweeping headlines declare victory, and how did no one stop to ask the one question that could unravel the whole thing?

Pennies for pain

And then there’s the money.

According to Monestier’s analysis, the average payout for harmed sellers is roughly $16 to $17. Not enough to buy a pizza, as she memorably puts it. Maybe enough for a mediocre sandwich.

Meanwhile, plaintiffs’ counsel received $333 million in fees. That’s not a typo.

I’d seen this disparity before. The math has been floating around for months. I remember nearly choking on my cannoli (for real) while crunching the numbers the first time. And Monestier’s brief once again puts the whole picture into perspective. The class members, the actual sellers whose transactions gave rise to this case, received barely a fraction of what they lost. In some instances, as little as a 10th of a penny on the dollar.

What’s more, the core conduct at the center of the litigation wasn’t even prohibited. Sellers can still pay buyer-broker compensation. In fact, brokers can still engage in broker-to-broker compensation. These practices weren’t banned. They were simply moved off the MLS and into the shadows, where — let’s be honest — enforcement is murky.

2 truths and a shaky foundation

I won’t pretend the settlement didn’t bring some progress. The decoupling of commissions? That’s a step toward a more consumer-centric model, and one I support. But I’d be lying if I said the outcome was perfect or that it fully addressed the underlying issues that can’t be denied.

Sellers are still footing the bill for buyer-broker compensation, just through different channels. Buyers, meanwhile, are being handed agreements to sign, sometimes within seconds of meeting their agents. The incentives may be rearranged, but the power dynamics haven’t exactly been reset. There’s good and bad here, just like in any solution that tries to resolve two different sides of a lawsuit or a deeply divided story.

And I’ll be honest: The idea of unwinding the settlement scares me a little. The industry is already struggling to adapt. Reopening everything could create more chaos, more uncertainty. And it’s not just this case. There are other related settlements that still haven’t received final court approval. If Monestier’s appeal gains traction, it will have ripple effects far beyond Sitzer | Burnett.

But listen, fear of disruption isn’t a valid reason to ignore an appeal that raises serious questions. It’s not just about fairness. It’s about legality itself. What Monestier’s appeal forces us to confront is a deeper, more uncomfortable truth: What if this wasn’t just an imperfect deal? What if it never had a solid legal foundation in the first place?

If her arguments are correct, the settlement doesn’t just deserve criticism. It may not survive scrutiny. That’s not a technicality. That’s a collapse.

We can’t afford to build trust on top of shortcuts. Justice isn’t a speed run. And landmark settlements — especially the kind that promise reform across an entire industry — can’t rely on shaky standing, procedural sleight of hand or ghostwritten rulings. Not if we expect them to hold real value.

So, where do we go from here?

Don’t look at me. I have no clue. Perhaps you’ll turn to Rob Hahn, who — right on schedule — just delivered a lengthy post breaking it all down. The title says it all: “It Ain’t Over Till It’s Over: Analysis of Monestier’s 8th Circuit Brief.” Among many, one particularly memorable takeaway is worth quoting: “Tanya Monestier, an individual law prof, not a giant law firm with hundreds of lawyers, might singlehandedly plunge the industry back into chaos with this appeal.”

That said, I do know this: If you felt something was off, if you sensed the objections raised by Monestier or the concerns flagged by the DOJ were treated more like noise than legal red flags, you’re not alone.

Oh, and if you haven’t read Monestier’s appeal yet? You should.

Just don’t be surprised when you hit the wall and realize the horizon was never real. Because once you see the construct for what it truly is, the only thing left to do is step through the door.

And, as Truman says with a smile before leaving the illusion behind: “In case I don’t see ya, good afternoon, good evening and good night.”

Editor’s note: This story was updated with a quote from Rob Hahn.

NOTE: The opinions, suggestions, and recommendations contained in this discussion are based on Summer Goralik’s experience working for the California Department of Real Estate and as a real estate compliance consultant. They should not be considered legal advice or relied upon as such. You should consult with your brokerage and/or appropriate legal counsel in your jurisdiction for further clarification.

This post was originally published on this site

by Craig C. Rowe | May 28, 2025 | Industry, News Feed

Local Logic’s hyperlocal marketing data will help Rently users and their applicants know more about what surrounds an available rental.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Local Logic’s community-based marketing content is slated to assist property managers and leasing agents who use Rently, according to a recent company announcement.

“By integrating Local Logic’s proprietary location insights, covering everything from walkability and nearby schools to access to parks, transit, restaurants and more, Rently is enhancing the digital experience for renters while helping operators attract more qualified leads,” according to a May 19 statement.

Renters often make living decisions based on an apartment’s proximity to retail and lifestyle amenities, and Local Logic’s software surfaces such data and insights to add value to the sales efforts of real estate professionals. It provides 18 in-depth location scores and analytics on neighborhoods, parks, walkability and school rankings, among other local residency drivers.

The information is graphically presented alongside rental listing pages to enhance property appeal as well as cut down on information that needs to be provided directly by a leasing professional.

Last year, Local Logic released a series of APIs (application programming interfaces) and SDKs (software development kits) under the name NeighborhoodWrap. The tools allow marketers to enrich omnichannel marketing campaigns with tightly integrated local insights, the company’s primary value proposition.

Local Logic co-founder and CEO Vincent-Charles Hodder said in the release that the software partnership reflects its mission to “improve every real estate decision.”

“We’re excited to partner with Rently to give renters a better understanding of what life looks like around a listing, helping them move forward with confidence and helping operators convert interest into action,” he said.

Rently offers a range of automation benefits for rental property operators at all levels, including single-family portfolios.

Part of Rently’s experience is secure applicant self-touring, a feature they deployed in 2022. However, it goes beyond the specific apartment as it also assists people in navigating parking lots, interior walkways and property grounds to arrive at the exact doorstep scheduled for showing.

“After implementing Local Logic, we saw a noticeable boost in user engagement — prospective renters were more informed, more interested and ultimately scheduled more tours. It’s all about creating a smarter, more delightful journey with Rently,” Jared East, VP of Product at Rently, said in the statement.

Email Craig Rowe

This post was originally published on this site

by Chris Drayer | May 28, 2025 | Industry, News Feed

Just for fun, Chris Drayer crunches the numbers to see which countries are buyer opportunities, which are seller plays and which hold must-watch investment potential.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

As a real estate agent, you are constantly comparing apples to oranges to help your clients make the right decisions about real estate. Buy, sell or hold — and at what price?

Due to several world leaders saying that their countries were not for sale recently, it got me thinking. What if you could just buy a country, as if they were actual real estate properties? Rather than square foot, location and beds and baths, I started using metrics like population, GDP, landmass, and population growth trends.

TAKE THE INMAN INTEL SURVEY FOR MAY

After looking at the data, some of these “properties” look like fix and flip investments, while others seem like long-term holds.

Just for fun, let’s take a look at some of the world’s “real estate” from a global perspective. I picked a handful of countries that are in the news currently. The scope and scale of these properties vary wildly, and the outcome was surprising to me.

United States of America: The prime urban condo

- GDP: $29.17 trillion (2025)

- Population: ~341 million

- Landmass: 9.15 million km²

- Status: Buy

The U.S. is a luxury high-rise in the heart of downtown — stable, high-demand and constantly appreciating. With the world’s largest economy and strong population growth, it’s a proven performer. Yes, the HOA fees (read: politics and debt) are high, but it remains a top-tier property. You buy the U.S. not just for current value but long-term strength.

China: The massive mixed-use development

- GDP: $18.27 trillion

- Population: ~1.42 billion

- Landmass: 9.6 million km²

- Status: Hold (Watch closely)

Think of China as a sprawling, fast-growing complex on the edge of a booming city. The potential is undeniable, but construction cracks are showing — demographics are shifting, and debt is a growing concern. Keep this one on your radar, but don’t overleverage.

India – The fixer-upper with sky-high potential

- GDP: $3.89 trillion (nominal), rising fast

- Population: ~1.46 billion (now No. 1 globally)

- Landmass: 3.29 million km²

- Status: Strong buy

India is that undervalued neighborhood that suddenly gets a subway line. Rapid population growth, a tech-savvy workforce and democratic stability make India an incredible long-term play. Infrastructure and governance challenges persist, but the potential upside is massive.

Russia – The historic mansion in disrepair

- GDP: $2.18 trillion (nominal)

- Population: ~144 million (shrinking)

- Landmass: 16.38 million km²

- Status: Sell

Fun fact: Russia owns more land than any other “property” in the world. Your “bigger is always better” clients should tour this property. But it’s isolated, poorly maintained and geopolitically complicated. Sanctions, declining demographics and overdependence on energy exports make this a tough hold. It’s a majestic structure — but one that may be crumbling from within.

Canada – The beautiful suburban estate

- GDP: $2.21 trillion

- Population: ~40 million

- Landmass: 9.98 million km²

- Status: Buy

Canada is that pristine, well-kept estate in a quiet, safe neighborhood. It’s not flashy, but it’s attractive — politically stable, resource-rich and increasingly popular thanks to immigration. The growth isn’t explosive, but it’s steady. Think of it as the Toyota of global properties: clean, future-focused and reliable.

Greenland – The undeveloped acreage

- GDP: $3.24 billion (not ranked globally)

- Population: ~56,000

- Landmass: 2.16 million km²

- Status: Speculative buy

Greenland is that enormous plot of land on the edge of town that no one knows what to do with — yet. As climate change alters global trade routes and reveals untapped natural resources, Greenland could become a geopolitical hotspot. But for now, it’s a cold, lonely gamble.

Overall takeaways that shocked me

GDP: Showing the U.S. as the vastly dominant economic “property.” Greenland, as you would guess, is not even visible.

Population: The demographic weight of India and China is intense. Similarly, the insignificant population of Russia compared to China is incredible.

Landmass: Highlighting Russia’s and Canada’s vast size. Shocked to see that India was actually larger than Greenland.

Make a move: In truth, it’s not a complete picture, kind of like MLS listings that only had four pictures back in the day. But, if you had to choose based only on this data:

- Buy: India for growth, Canada for stability, U.S. for long-term power

- Hold: China, watch for shifting trends

- Sell: Russia, high risk and low upside

- Speculate: Greenland, for visionary investors only

The number game

My team members and I love to turn data into insight — whether we’re helping real estate professionals spot the next mover in their database or imagining the world’s nations as investment properties. It’s all about seeing patterns, predicting trends and making smarter decisions.

What’s happening with the world right now is engaging and impactful, and that is what analyzing data is all about. Because when you understand what’s happening beneath the surface of your database, you’re better positioned to launch the right conversation at exactly the right time.

Chris Drayer is co-founder of Revaluate, which segments consumers for marketers by propensity to move.

This post was originally published on this site