The company offered thousands of quick cash loans in exchange for 40-year exclusive listing agreements that a judge found violated the law and issued an injunction stopping the practice.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego.

Months after a judge ordered MV Realty to terminate long-term contracts with homeowners, the South Florida real estate brokerage has begun letting its clients out of the fraudulent contracts.

According to a report by the Tampa Bay Times, MV Realty has terminated thousands of its contracts, which trapped the firm’s clients into 40-year exclusive listing agreements with the brokerage.

Under the terms of the so-called “homeowner benefit agreements,” if clients listed their homes with another brokerage, MV Realty would place liens on their properties and charge them 3 percent of the property’s value to let them out of the contract.

The state of Florida sued the company in November 2022. In February, a judge ordered the firm to cancel its contracts within two weeks.

The state later said the company failed to comply with the court’s injunction until it recently began terminating the contracts, according to the Times.

MV Realty would work with homeowners who were in need of a quick cash loan. In exchange for money up front, MV Realty would lock its clients into the long-term contracts.

The state said the company violated the Florida Deceptive and Unfair Trade Practices Act through the enforcement of its contracts, and that more than 9,300 homeowners were affected.

“In my almost six and a half years with the office, this was one of the worst abuses that crossed my desk,” former acting attorney general John Guard said in a statement earlier this year. “The 9,303 Floridians who were subject to MV Realty’s unconscionable practices will have their properties unencumbered by this injunction and we will continue to hold MV Realty responsible for its abuses.”

The brokerage began facing legal trouble throughout the country as its notoriety spread and states began filing their own lawsuits to stop its conduct.

MV Realty lost its ability to transact real estate in Colorado. California blocked the company from enforcing its long-term contracts late last year.

Amid the mounting legal battles, the company initially filed for chapter 11 bankruptcy protection before withdrawing that request.

Your next professional move should be driven by vision and intention, not pressure, as you continue to develop your career, Coldwell Banker Affiliates’ Jason Waugh writes.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

During a career, there often comes a moment — not marked by burnout or dissatisfaction, but by a quieter, more persistent realization: You may be ready for something new. Perhaps your current role no longer challenges you, or the work that once felt fulfilling now feels routine. Maybe the industry is evolving faster than your current environment can accommodate.

These signals can be subtle. According to a recent Career.io study, real estate professionals report high job satisfaction, rating their job a 4.24 out of 5. Yet, paradoxically, the industry also ranks among the top three for burnout, with professionals changing roles approximately every 3.91 years, according to 2024 research published by PsychologyJobs.com.

This duality underscores the complexity of career decisions — you can be passionate about your work and still recognize the need for change.

So, how do you know when it’s time to make a move? I spent 30 years affiliated with my previous company before joining Coldwell Banker. Three decades. That transition wasn’t driven by dissatisfaction — it was the result of thoughtful reflection and strategic consideration.

In today’s dynamic real estate landscape — characterized by market recalibration, economic volatility and uncertainty, industry consolidation and rapid technological advancement — proactive decision-making is not just advantageous; it’s imperative.

Recently, I had the pleasure of meeting with Anywhere Real Estate’s Rising Star award winners. We discussed ways to advance their careers and navigate changes that may be inevitable. Here’s my framework of eight key questions to help guide career decisions.

Whether you’re contemplating a move or simply reassessing your path, these questions can provide clarity:

1. Are you clear on your purpose?

Time is one of our most valuable and limited resources. In your professional journey, it is essential to have a well-defined vision of how you allocate your time and with whom you choose to invest it.

Consider focusing not only on what you wish to achieve or acquire, but more importantly, on who you aspire to become. Aligning your actions with a clear sense of purpose will drive more meaningful and impactful outcomes.

2. What are your core strengths — and where do you need to grow?

Conduct an honest self-assessment. Identify your key competencies and areas for development. Too often, individuals change their external circumstances without first addressing the internal changes necessary for meaningful progress.

Then ask: Do you want to deepen your expertise or broaden your skill set? And, consider whether your current organization provides the environment and resources to support that development.

3. Have you engaged in meaningful career conversations within your company?

Before looking outward, look inward. Speak with your manager and cross-functional leaders. Explore potential opportunities within your current organization that align with your goals.

4. Do you understand your financials?

Evaluate the true cost of each transaction — both in time and money. Without a clear understanding of your financial metrics, it’s difficult to assess whether a new opportunity offers real value or just better marketing.

5. Are you speaking with the right people?

Don’t rely solely on recruiters. Engage with individuals across all levels of the organization you’re considering. Culture fit is critical — without it, even the most attractive compensation package can feel restrictive.

6. What’s holding you back?

Change is emotional. When I made my move, it felt like choosing between loyalty and betrayal. Acknowledge those feelings, but don’t let them paralyze your progress. Often, your peers will support your growth more than you expect.

7. Who will support you through the transition?

Transitions involve many moving parts — branding, licensing and onboarding. Have you met the team that will guide you through this process, or are you relying on promises from leadership?

8. Is this about FOMO?

With so much movement in the industry, it’s natural to feel as though you might be missing out. However, not every opportunity is the right one. The key is to evaluate alignment in timing and opportunity. If the timing is right but the opportunity is not, the outcome may be unfulfilling.

Conversely, if the opportunity is compelling, but the timing is not, it may still lead to disappointment. Sometimes, the wisest decision is to stay the course. After all, the grass tends to be greenest where we consistently water it.

Recruiting efforts will continue. The industry will keep evolving. But your next move should be driven by vision and intention, not pressure.

Take the time to reflect on where you want to be in two, five or 10 years. Whether you choose to stay, pivot internally or make a bold leap, ensure your decision is strategic, intentional and aligned with the professional you aspire to become.

Jason Waugh serves as president of Coldwell Banker Affiliates for Coldwell Banker Real Estate LLC.

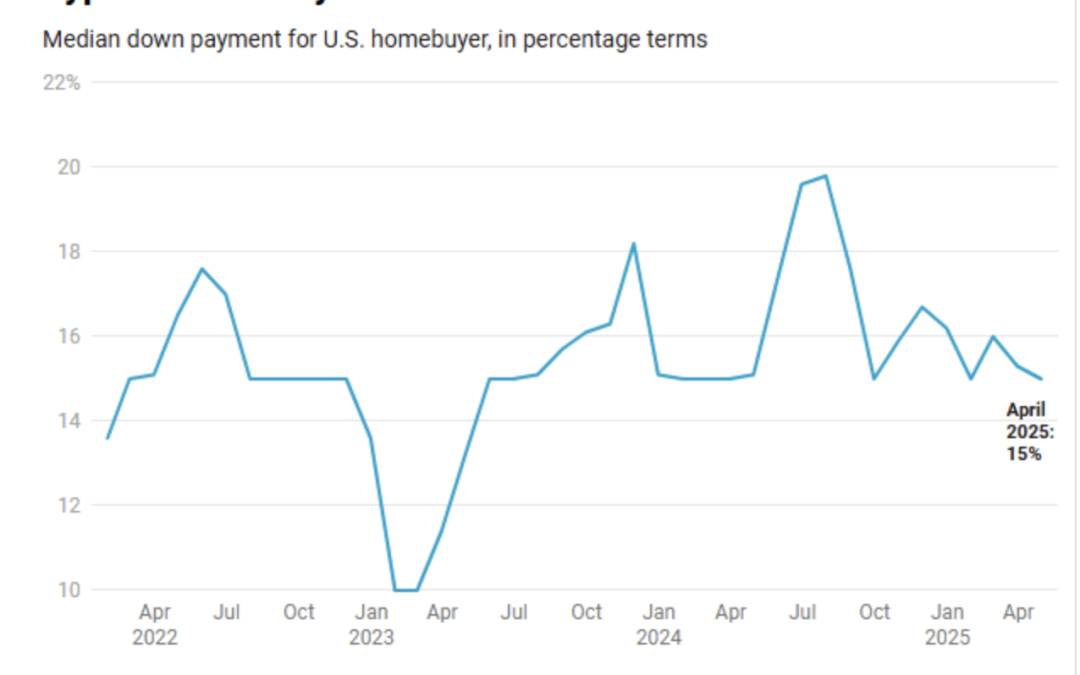

Down payments are declining even as home prices are rising because buyers are facing affordability challenges or opting to reserve more of their cash because of economic uncertainty, Redfin said.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The 1 percent drop, to $62,468, is subtle but significant, according to the report, which tracked county records in the 40 most populous metro areas in the U.S.

“The buyers who are moving forward today are being very careful with their finances because with housing costs near record highs, they’re typically spending a big portion of their paycheck to buy a home,” Redfin Premier agent Fernanda Kriese, who is based in Las Vegas, said in the report.

“I’m seeing an uptick in first-time buyers looking for starter homes,” Kriese added. “Combine that with concerns about layoffs and a potential recession, and people are doing things like cross-comparing mortgage origination fees, shopping around for lenders and looking into down-payment assistance.”

Credit: Redfin

In terms of percentage, the typical homebuyer today puts down 15 percent of the purchase price, nearly equal to the 15.1 percent they put down at this time last year, Redfin’s report noted. And the median down payment for American homebuyers has hovered around that number for about the last four years, briefly dipping around 10 percent in early 2023. Pre-pandemic, a 10 percent down payment was more frequent.

But dollar-amount down payments have not fallen on an annual basis since the summer of 2023 when home-sales prices were also falling, according to Redfin. During that period, down payments were declining because of falling home prices.

Now, home prices are rising, although they are doing so more slowly. As of April, home prices were up 1.4 percent year over year, compared to the 4 percent they were up by during the same period in 2024.

The reason down payments are falling by dollar amount is because not all homebuyers make a down payment — one-third pay in all cash. And those that are financing a home are most likely buying less expensive homes, which also means a smaller down payment in terms of dollars, but not necessarily percentage terms.

Redfin said that a higher share of homebuyers are also using FHA and VA loans, which allow for smaller down payments, somewhere between 0 percent to 3.5 percent. In April, 15.3 percent of mortgage home sales used an FHA loan, up from 14.2 percent the year before. The share of mortgage home sales using a VA loan was 7.2 percent in April, up from 6.4 percent the year before and the highest April level seen since 2020.

With homebuyer affordability remaining difficult because of roughly 7 percent mortgage rates, many buyers may be purchasing lower-priced homes than they might otherwise. Economic uncertainty in the U.S. right now may also be driving buyers to reserve more of their money in their bank accounts for extenuating circumstances.

Meanwhile, there are now more homesellers than homebuyers in the U.S., tipping the market to favor buyers, which has meant concessions and sellers willing to accept lower down payments. Unfortunately, lower down payments might also be a sign of a buyer with less secure financial standing, and a deal that’s more likely to fall through.

Stop trying to DIY your compliance or ignore difficult clients. According to coach Darryl Davis, keeping careful records, researching thoroughly and communicating regularly are your best bets for staying on the right side of the law.

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Let’s get something straight: In real estate, the legal landmines are everywhere. Even if you’ve dotted every “i” and crossed every “t,” you can still end up in a courtroom. That’s not fear-mongering — that’s the nature of the job.

But here’s the good news: You can dramatically reduce your risk by being intentional, informed and yes, maybe just a little bit paranoid (the healthy kind without the tinfoil hats).

5 ways to stay out of trouble

These five strategies aren’t just best practices — they’re essential armor for staying protected in today’s high-risk, post-settlement industry.

1. Document everything like your career depends on it, because it might

If it’s not in writing, it didn’t happen. Period.

Every phone call, showing or negotiation that even might matter later? Back it up with an email.

“Hi [Client Name], just confirming our conversation this morning where you said you wanted to hold off on submitting that offer.”

Boom. Timestamp. Proof. Protection.

I’ve told agents for years: Assume you’re going to get sued. Not because you’re doing anything wrong, but because that’s the nature of the beast. A solid paper trail isn’t just smart; it’s survival.

2. Stop confusing MLS rules with license law

One of the biggest mistakes agents make is assuming that MLS rules or association policies carry the same legal weight as your state’s license law. They don’t.

If someone claims something is “illegal,” don’t panic; ask for the source. “Show me the law” should be your default response. MLS policy violations and legal violations are two different animals. Don’t take the bait. Don’t get burned.

3. Your association is not a law firm, so stop treating it like one

Associations serve a purpose, but that purpose is not legal counsel. Their forms and opinions are designed to cover their own liability, not necessarily yours.

If you have a legal question, your first call should be your broker. Your second? The state’s licensing department or hotline (yes, you should have that number saved in your phone). It’s amazing how many lawsuits could be prevented if agents stopped asking the wrong people for legal advice.

After all, would you get parenting advice from someone who’s never had children? Probably not. Why, then, would you get legal advice from people who aren’t attorneys?

4. Stay educated because what you don’t know will hurt you

Real estate is an ever-changing industry. What was legal or standard a year ago could be a lawsuit today. If your education ends when you check off your CE credits, you’re falling behind. Every agent should block time off in their week just for training, reading and getting up to speed. Make this time a non-negotiable, because your career may depend on it.

Subscribe to trusted sources (like Inman News). Attend quality trainings. Join mastermind groups. And yes, read the fine print on your board’s updates. The agents who stay informed are the ones who stay in business — and out of court.

5. Over-communicate like a pro (Even when there’s nothing new to say)

If there’s one thing that drags agents into drama, it’s silence. When clients or cooperating agents don’t hear from you, they fill in the blanks — and usually not with anything flattering. In fact, the longer the silence continues, the worse the assumptions become. That’s not how to create a positive experience for your clients.

Here’s the rule: No update is still an update. Tell your clients, “Hey, still waiting to hear back; just wanted to keep you in the loop.” It builds trust. It calms nerves. And it gives you written proof you kept everyone informed.

If you want to stay out of court, you have to stop playing defense and start playing offense. That means being disciplined, detail-oriented and willing to slow down long enough to protect your future.

Do the boring stuff. Send the recap email. Make the extra call. Read the update from your state’s real estate commission. Because in this business, the agents who survive are the ones who prepare like it’s already hit the fan.

And when in doubt? Don’t guess. Ask your broker or attorney. That five-minute call could save you five years of regret.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

“You get what you pay for.”

It’s a common refrain when real estate agents and brokers who charge a typical commission refer to their counterparts who charge less — the implication being that a lower fee results in lower quality service.

But low-fee brokers with experienced, full-service agents exist and can offer consumers great value, according to a report from the Consumer Policy Center, a think tank founded earlier this year by Stephen Brobeck and other senior fellows.

The report, “Reducing Real Estate Commissions: Are Low-Fee Brokers a Viable Alternative for Home Sellers?,” is written by Brobeck and CPC fellow Wendy Gilch. They found that, for those willing to comparison shop, such brokers can indeed be a viable alternative and potentially offer “superior value” to “traditional” brokers in the sense that they provide quality work for less.

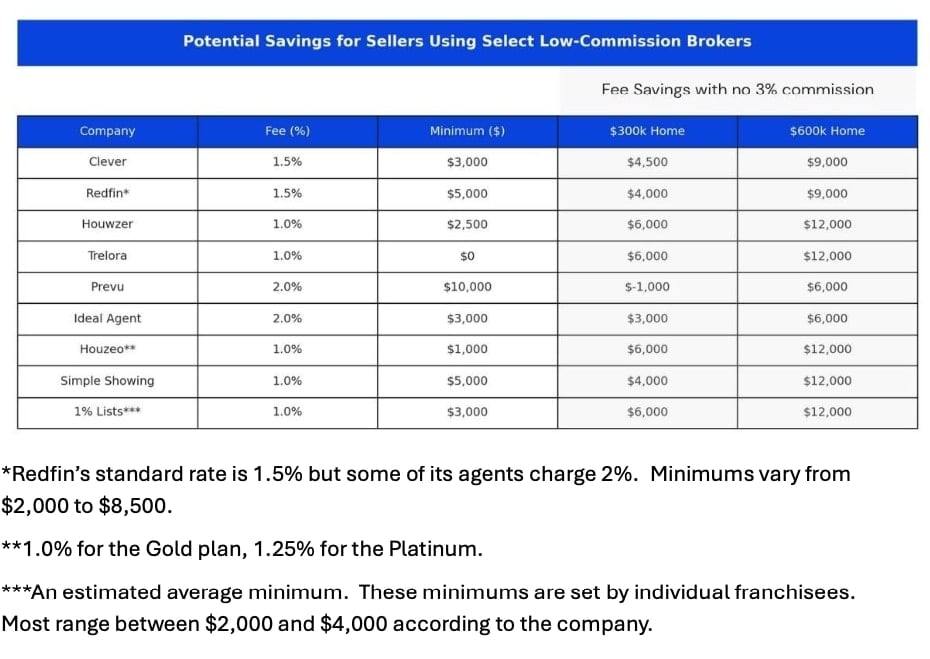

For instance, a seller who hires an agent that charges a 1.5 percent commission rather than a 3 percent commission will spend $6,000 less on the sale of a $400,000 home.

Stephen Brobeck

“Many low-commission brokers work with successful, full-time agents who are either employed by the brokers or by independent firms,” Brobeck said in a statement.

“There is every indication that, for significantly reduced fees, many low-commission agents provide the same quality of service offered by successful traditional agents.”

Source: Consumer Policy Center

Some in the real estate industry say that traditional brokers are more likely than low-commission brokers to sell homes for higher prices, thereby negating the savings of using a lower-fee broker, and point to data showing that for-sale-by-owner (FSBO) homes sell for lower prices than those sold by traditional agents, the report notes. But Brobeck and Gilch stress that such data doesn’t account for differences between the sellers.

“FSBO sellers have lower average incomes and less expensive homes so are more likely to try avoiding brokerage costs,” the report says.

“More importantly, there has been academic research on the issue of whether traditional listing agents secure higher sale prices than do low-fee agents, and the finding is that they do not. To quote one study: ‘We find no evidence that the use of a broker leads to higher average selling prices, or that it significantly alters average initial sale prices.’”

However, at least a couple of studies have found that using a traditional broker reduces time on market “by several days,” the report added.

For this report, Brobeck and Gilch considered 45 low-commission or flat-fee brokers and narrowed in on 15 “because of their visibility and success.”

Of the 15, nine are low-commission brokers, meaning they charge less than a typical 2.5 percent or 3 percent commission, typically between 1 and 2 percent, for “full, personal services”:

Clever

Houwzer (merged with Trelora, but they maintain separate public brands)

Houzeo (which also offers flat-fee services)

Ideal Agent

1% Lists

Prevu

Redfin

Simple Showing

Trelora

Six are flat-fee brokers, meaning they charge a specific dollar amount — usually between $100 and $1,000 — to list properties on local multiple listing services (MLSs) and listing sites such as Zillow and Realtor.com and also provide generic information on homeselling. They get paid regardless of whether a home sells.

Beycome

Circle One Realty

Cottage Street Realty

Flat Fee Group

FSBO.com

Houzeo (which also offers low-commission services)

Brobeck and Gilch found that, unlike “traditional” brokers, low-fee brokers almost universally clearly disclosed their fees and specific services online.

To compare the companies they considered information provided by the brokers themselves, assessments of the firms by other discount brokers, third-party reviews, and data on customer satisfaction related to customer comments and complaints, such as that found on Google, Trustpilot, Yelp, Pissed Consumers, Consumer Affairs, and the Better Business Bureau.

They also asked for agent recommendations from six of the low-commission companies (Clever, Redfin, Houwzer, Prevu, Ideal Agent, and Houzeo) and called those agents, posing as homesellers.

Flat-fee brokers

Regarding flat-brokers, the report notes they “offer the potential of huge cost savings” to the tune of thousands of dollars, though most do not offer personalized services. One exception was Cottage Street Realty, which offers experienced agents who provide personal service but don’t meet with sellers or see the listing in person.

Wendy Gilch

“The expansion of different types of flat-rate services has provided new opportunities to owners wishing to sell themselves,” Gilch said.

Likely referring to the waning use of the National Association of Realtors’ no-commingling rule, she added, “The fact that major MLSs and portals, such as Zillow, no longer segregate FSBOs from Realtor listings helps these sellers immeasurably.”

Regarding specific firms, however, the report said there were not enough available reviews to evaluate them.

“There is insufficient information about flat fee brokers to make reliable judgements about individual companies,” the report says.

The report suggests the sellers that might find flat-fee brokers most attractive would be those under no time pressure to sell who want to figure out what their property is worth and maybe find an unrepresented buyer to sell to with the help of an attorney or lower-cost agent; knowledgable sellers who can manage the sale themselves with the help of an attorney or title com[any; or sellers and buyers who know each other and can negotiate among themselves and close with the help of an attorney or title firm.

“To best utilize these lower-cost options, sellers must decide how much of the home pricing, listing, posting, showing, bidding, negotiating, and closing they wish to take on as responsibilities,” the report said.

“In most cases, at minimum they will need some assistance from an attorney or title company. If they decide to delegate these responsibilities to a licensed agent, they should carefully consider the qualifications, track record, and reputation of the candidates they consider. Sellers under no pressure to sell, those with some knowledge of brokerage practices, and those who themselves find a buyer will be most likely to find low- cost flat fee services to be attractive.

“Sellers under pressure to sell (and often to also buy), those unfamiliar with brokerage practices, and those who want to minimize their involvement in the sale are most likely to prefer their own loyal, fiduciary agent. The latter group constitutes a large majority of all sellers.”

Low-commission brokers

The report found that nearly all of the low-commission brokers studied offered full agent services, though they differed in their local availability, type, cost of services and who provides them.

For example, the report says, Clever, Redfin, and Ideal Agent offer their services throughout most of the country and each has at least 2,000 agents, while Houzeo is also a national company but has a limited number of low-commission agents. The remaining five brokers are regional.

“At all companies, sellers are assisted personally by licensed agents,” the report says.

“We believe that the most important factor, apart from cost, that sellers should consider in deciding whether to use a low-commission agent is the quality of the agent.”

The report emphasized the importance of sellers assessing their prospective agents and brokers.

“[A]ll low-commission brokers employ at least some competent, experienced agents, which emphasizes the importance of sellers doing their own assessment of recommended agents,” the report says.

“That assessment should include not only recent selling experience and client reviews, but also information about how well agents explain the sales process and how involved they will be in the sale. With this in mind, low-fee brokers do represent a viable alternative for home sellers.”

The report advised sellers to look for brokers that offer:

“Availability for full, in-person service including an initial meeting, home inspection, home showings, and the closing. Companies with agents within ten miles of the seller are preferable to those living 50 miles away.

Agents who have been hired because of their experience and good client reviews.

Agents whose performance is evaluated by their company using customer reviews.

Commissions that are 1.5 percent or lower with low minimums.

Good evaluations by sellers and by independent reviewers.”

Of the six companies from which Brobeck and Gilch requested an agent recommendation, they found that most such agents had had at least 10 sales the previous year, were positively reviewed by clients on Zillow or Realtor.com, and “in a phone conversation, convinced us they were a viable option.”

Asked why they only reached out to six of the companies, Brobeck told Inman, “We could not request assistance from companies operating outside the DC and Pittsburgh areas because all companies require inclusion of much information about the owner and the home, and we didn’t feel it was reasonable to ask others, besides Wendy and me, to do so given privacy issues and the possibility of their being subjected to aggressive phone and email marketings.”

The report singled out Clever, an online referral service with more than 15,000 partner agents, as unique among low-commission brokerages for explicitly only recommending agents with strong credentials, including that they must be full-time professionals with more than five years experience, be favorably reviewed by past sellers and possess “extensive local market knowledge” — criteria many agents at traditional brokerages would not meet.

Clever, the report added, is also available nationwide, charges a 1.5 percent commission with a low minimum sale price, offers sellers the ability to pick among experienced full-time agents, and has consistently positive client reviews.

“No other low-commission broker shares these characteristics,” the report said.

“Trelora, Houwser, 1% Lists, and Simple Showing all charge lower commissions but limit their services to certain local areas.”

The report notes that Clever partner agents pay a portion of the 1.5 percent commission to Clever and that one might question whether such an agent would work as hard for a 1 percent net commission as for a 1.5 or 2 percent net at a higher-cost brokerage.

“Three considerations — there is intense competition for clients, agents depend on referrals from satisfied clients, and Clever monitors the performance of its partner agents – suggest that this risk is worth taking when the savings is usually considerable,” the report says.

Asked whether anyone in the real estate industry helps finance the CPC or its research, Brobeck told Inman, “No! Financed entirely by the Fellows.” The CPC has a similar disclosure on its website.

The market has undeniably shifted from the extreme seller’s environment of the early pandemic. But in much of the U.S., buyers still face substantial inventory constraints, an Intel analysis shows.

This report is available exclusively to subscribers of Inman Intel, the data and research arm of Inman offering deep insights and market intelligence on the business of residential real estate and proptech. Subscribe today.

The U.S. housing market has entered a new era — one in which homebuyers in most parts of the country actually have more negotiating power than they had before the pandemic.

But the market is also deeply divided.

Broad swaths of the nation now provide far more options for buyers than they were used to even a decade ago. At the same time, the other half of the country remains substantially inventory-strapped, a scenario that supports high prices even as buyers and brokerages fight to wrest new listings from competitors.

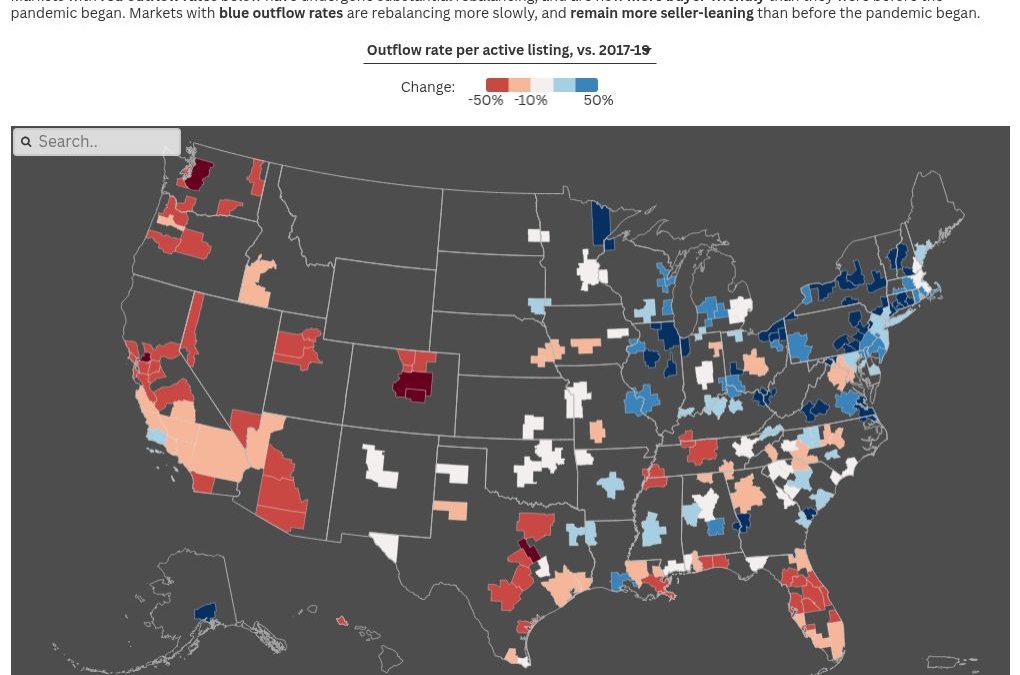

These two Americas follow distinct geographic patterns, an Intel analysis of Realtor.com data found.

And while much of the nation still faces severe supply challenges, Intel found that others are rebalancing for the wrong reasons — screeching to a halt as new supply remains depressed amid a listless sales environment.

Intel breaks down where the 150 largest metro areas in the U.S. stand on inventory in this week’s report.

Slow to adjust

To an extent, nearly every market has participated in the ongoing transaction downturn, and the Great Rebalancing of housing inventory that has accompanied it.

But while researching this piece, it became clear that the pandemic’s lasting imprint on local markets remains much deeper in some places than others.

Agents throughout much of the South and the West regions of the United States are seeing conditions where the typical buyer’s pleas to bring down prices now hold more weight.

That doesn’t mean these markets are suddenly buyer’s markets by the traditional definition, where it would take six months or longer for the current stock of inventory to sell in its entirety at present sales rates. Even before the pandemic, inventory had been getting relatively tight, pushing most places into firmly seller-market territory.

But those same places are significantly less seller-friendly today, and it’s weakened price growth in some places and brought prices down in others.

For brokerages, this is a double-edged sword. Lower prices directly cut into a broker or agent’s commissions. At the same time, today’s price levels remain unaffordable for many potential buyers at today’s mortgage rates, which puts a significant damper on sales.

On the other side of the country, agents in the Midwest and Northeast are likelier to see conditions that are rebalancing much more slowly.

Many of these markets remain stuck in an overheated situation, a sort of lingering phantom of the pandemic dynamic where razor-thin inventory is still hard to come by, even in the current depleted buyer pool.

Inside the Great Rebalancing

If roughly half the country is undergoing a significant rebalancing toward more buyer-friendly dynamics, what’s driving it?

There are two main answers, Intel found.

The most unusual path is the one taken by Texas and Florida. In these places, new inventory — including new construction and existing listings — is now coming online each month at a rate that rivals or even exceeds pre-pandemic norms.

These states appear to be benefiting from healthier conditions than what’s being seen in other rebalancing markets, including more inbound migration in recent years.

More new listings helps support more new transactions and demand. And while listings are recovering in most parts of the country, Texas and Florida have been at it for longer, and have reached healthier levels sooner.

Using listing outflow as a rough proxy for sales, transaction levels are also much closer to normal levels in many Texas and Florida markets, even as dynamics have shifted in a more buyer-friendly direction.

In the greater Dallas area, listings are moving off the market at levels that are 94 percent of where they were in a typical spring before the pandemic struck. Houston-area listing outflow is back above normal levels, and San Antonio is back right below its pre-pandemic outflow trend.

So in these places, decent sales volume and a buyer-friendly rebalancing have been able to coexist, offsetting the effect of softening prices for brokerages. But that hasn’t been typical of other parts of the rebalancing nation.

Examining San Diego, listing outflow remains stuck at only 58 percent of its typical levels, while new-listing levels are at 67 percent of normal.

The result is typical of many markets along the Pacific Coast and even deeper inland throughout the West: markets where low transaction levels, rather than robust supply growth, are now creating significantly more buyer-friendly conditions — to an extent that may even threaten price stability.

Here’s how some of America’s biggest population centers fit into four major classes of market.

Rebalanced in large part by healthy supply:

Texas cities: Austin, Dallas, Houston, San Antonio

Eastern seaboard: Tampa, Orlando, Charlotte

Western supply pockets: Denver, San Francisco

Rebalanced primarily by a plummet in demand:

California population centers: San Diego, Los Angeles, Riverside

Other Western cities: Phoenix, Portland, Seattle

Strong competition on decent supply:

Scattered large metros: Pittsburgh, Kansas City

Overheated on short supply:

Northeastern hubs: New York, Philadelphia, Baltimore, Boston

Midwestern metros: Chicago, Cleveland, Cincinnati, St. Louis