by Matt Carter | Jun 27, 2025 | Industry, News Feed

Recission of a dozen regulatory policies is aimed at “slashing red tape that drives up costs and shuts families out of the market,” HUD Secretary Scott Turner said.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The Trump administration lifted “a pile of regulations” from FHA lenders Friday afternoon, eliminating a dozen policies governing flood risk management, inspections in disaster areas, appraisals, underwriter qualification and data collection.

The move is aimed at “slashing red tape that drives up costs and shuts families out of the market,” Department of Housing and Urban Development (HUD) Secretary Scott Turner said in an announcement.

TAKE THE INMAN INTEL SURVEY FOR JUNE

The policy recissions, published in a series of Mortgagee Letters, are effective immediately and will be incorporated into a future version of the Federal Housing Administration’s Single Family Housing Policy Handbook for lenders.

Builders constructing new homes in special flood hazard areas or FEMA-designated “coastal high hazard areas” will no longer be required to build homes at least two feet above the base flood elevation for their homes to qualify for FHA financing.

The new elevation standard, announced in November by the Biden administration, “would have limited the land available for development and increased the cost of construction for FHA-insured single family properties, thereby contributing to the insufficient supply of New Construction housing and rising home prices,” HUD said in rescinding it.

Lenders signing off on FHA loans in Presidentially Declared Major Disaster Areas (PDMDAs) will no longer be required to obtain mandatory damage inspection reports that identify and quantify any dwelling damage.

Instead, they “must exercise reasonable due diligence to determine if additional inspections or repairs are necessary,” HUD said.

Requiring inspections by FHA-approved appraisers in disaster areas regardless of whether any damage had occurred, “sometimes resulted in a lengthy waiting period” for mortgage approvals, and led to “unnecessary inspections, delayed loan closings, and postponed issuance of FHA insurance,” HUD maintains.

In scaling back the several requirements for appraisers, HUD said FHA “has historically imposed more extensive property appraisal protocols and more stringent procedures than those required for other mortgage lending purposes.”

Appraisers will no longer be required to confirm that the remaining economic life of a property is longer than the mortgage term. Fewer photos of properties will be required — they won’t be required to take photos of attics or crawl spaces, for example.

When analyzing the housing market in which a property is located, appraisers will still be required to determine if property values are increasing, stable or declining, but won’t have to assess whether the current trend appears to be changing.

“Current appraisal standards no longer support the need for certain FHA-specific protocols, rendering them outdated and misaligned with broader industry norms,” HUD said. “In addition, FHA’s internal collateral valuation technology and data capabilities have significantly improved, further reducing the necessity of these duplicative and antiquated appraisal requirements.”

HUD is also lowering the experience requirements for “Direct Endorsement” underwriters who have the authority to sign off on loans without prior FHA review or approval, and allowing lenders to employ them on a part-time basis.

“FHA recognizes that the financial landscape for smaller lending institutions has evolved significantly over the past decade, presenting both opportunities and challenges in sustaining growth and meeting customer needs,” HUD said of the change.

In eliminating a requirement that lenders collect information about the borrower’s language preference and any homeownership education and housing counseling they may have received, HUD said only 1.2 percent of FHA borrowers completed the form “in a manner that provided any potential benefit to them.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 27, 2025 | Industry, News Feed

Two closely watched surveys show Americans remain concerned that the U.S. is headed for the dual challenge of an economic slowdown and an increase in inflation.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Uncertainty over what tariffs the Trump administration will ultimately impose on U.S. trading partners continues to weigh on consumer confidence, according to two closely watched surveys.

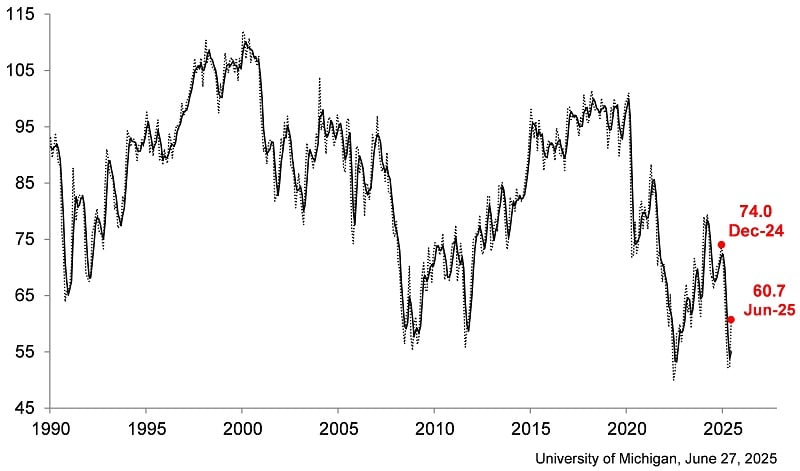

The latest reading from the University of Michigan surveys of consumers released Friday showed consumer sentiment improved for the first time in six months in June, rising 16 percent from May.

University of Michigan Index of Consumer Sentiment

But at 60.7 in June, the U of M Index of sentiment was down 18 percent from December 2024, and “consumer views are still broadly consistent with an economic slowdown and an increase in inflation to come,” survey director Joanne Hsu said in a statement.

Joanne Hsu

“Consumers continue to be concerned about the potential impact of tariffs, but at this time they do not appear to be connecting developments in the Middle East with the economy,” Hsu said.

While rising tensions with Iran initially sent oil prices up by 20 percent in June, they’ve since retreated after attacks on Iran by Israel and the U.S. did not escalate into an all-out war.

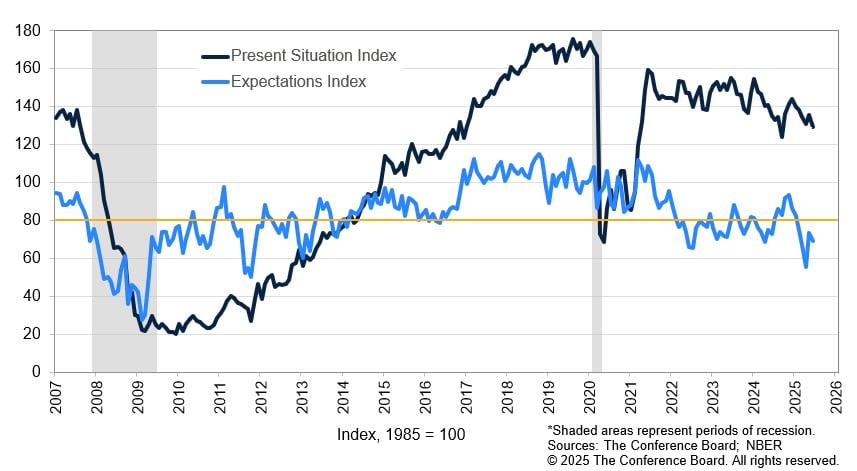

The Conference Board Consumer Confidence Index, released on June 24, retreated by 5.4 points in June, to 93. That index had previously posted its first gain in five months in May, rising 12.3 points.

Stephanie Guichard

“Tariffs remained on top of consumers’ minds and were frequently associated with concerns about their negative impacts on the economy and prices,” Conference Board Senior Economist Stephanie Guichard said in a statement. “Inflation and high prices were another important concern cited by consumers in June.”

Conference Board Present Situation and Expectations Indexes

The Conference Board’s Expectations Index, which is based on consumers’ outlook for income, business and labor market conditions, fell 4.6 points to 69, well below the threshold of 80 that often signals a recession ahead.

While many economists expect tariffs will have an inflationary impact on prices, they could also cause the economy to slow if consumers buy less and hiring slows.

Federal Reserve policymakers have signalled that while they expect to cut short-term interest rates twice later this year to keep unemployment in check, they’ve been waiting to see what impact tariffs have on prices.

The latest reading of the Federal Reserve’s preferred inflation gauge, the personal consumption expenditures (PCE) index, showed consumer spending shrank by $29.3 billion in May, and that the annual rate of inflation moved away from the Fed’s 2 percent goal, to 2.3 percent.

Ongoing negotiations have added to the uncertainty over tariffs, with the Trump administration pushing back many country-specific “reciprocal tariffs,” which were originally slated to go into effect in April, until July 9.

U.S. stock indexes hit new all-time records on Friday on news that the U.S. and China are close to reaching a trade deal, only to reverse course when President Trump said he was ending trade talks with Canada.

In the meantime, consumers are paying an average effective tariff rate of 15.8 percent on imported goods — the highest since 1936, according to a June 17 analysis by The Budget Lab at Yale.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Lillian Dickerson | Jun 27, 2025 | Industry, News Feed

Former mortgage loan originator Andrew Josephson claims the company failed to adequately pay him and other employees for time worked in an effort to cut costs and gain a leg up on competitors.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

A mortgage loan originator who previously worked for Zillow Home Loans has filed a class action lawsuit against the portal giant’s mortgage lending arm, alleging that it failed to adequately pay him and other employees for time worked in an effort to cut costs and gain a leg up on competitors.

Andrew Josephson | Credit: LinkedIn

The disgruntled former employee and lead plaintiff in the case is Andrew Josephson, who worked for Zillow Home Loans from 2023 to 2025, according to his LinkedIn profile. Josephson is now a product specialist at Federal First Lending and has worked in the past at Escrow.com and Network Capital.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Representatives for Zillow said they were unable to comment on pending litigation. Lawyers for Josephson did not immediately respond to Inman’s request for comment.

The complaint filed on Wednesday in Orange County, California, alleges that Zillow Home Loans failed to pay minimum wages and overtime, provide meal and other breaks, reimburse business expenses, provide accurate itemized wage statements, pay all wages within a timely period of Josephson’s separation from the company, and violated business and professional codes.

The suit further alleges that Zillow Home Loans intentionally created “an artificially lower cost of doing business in order to undercut their competitors and establish and/or gain a greater foothold in the marketplace.”

The plaintiffs are requesting a jury trial and damages to recover unpaid wages, non-reimbursed business expenses, benefits and attorneys’ fees and expenses. California citizens currently or previously employed by Zillow Home Loans, any time between June 25, 2021, and the date of class certification, who have similar grievances as those outlined by the lawsuit, may be included in the class of plaintiffs.

This is not the first time that Zillow or one of its entities has been on the receiving end of a lawsuit regarding wages. In 2019, business consultant Nicole Correa filed a class action suit against Zillow Group, alleging labor code violations, including a failure to pay overtime wages, and Zillow settled that suit in 2021 for a little over $342,000. In 2014, former inside sales consultant Ian Freeman also sued Zillow Group in a class action suit that alleged the company violated wage laws. Zillow settled the case in 2016 for $6 million.

Read Josephson’s full complaint here.

Email Lillian Dickerson

by Craig C. Rowe | Jun 27, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Inman Innovator Award-winning Solid Earth is a technology company that works with multiple listing services and associations to bolster workflow efficiencies, and part of that effort includes reducing the barriers to accessing data and tools often buried under multiple logins and outdated security measures.

To that end, the company has introduced Passkey authentication to all of its MLS clients, Inman learned in a June 26 statement. The new “password-free, phishing-resistant login” will be rolled out initially to thousands of members in the San Antonio Board of Realtors (SABOR).

“Passkeys are device-based credentials built on FIDO standards and backed by Apple, Google and Microsoft,” according to the statement. “They let users sign in using Face ID, Touch ID, or a device PIN, eliminating the need for passwords and reducing risk from phishing and credential reuse.”

It’s not at all uncommon for MLS platforms and industry data sources to be caught in hacks or phishing attempts, which puts all members at risk, especially those who rely on MLS software partnerships to run their business.

In 2023, Rapattoni suffered a ransomware attack that paralyzed servers hosting multiple listing services with hundreds of thousands of members. Those affected, among others, included Northwest Indiana Realtors Association, San Francisco Association of Realtors, BAREIS MLS, Pasadena Foothills Realtors, and CincyMLS.

It happened to MetroList in 2019 and to Georgia MLS in 2020, as well. It’s safe to say that the sophistication of such schemes has only evolved, making every tactic to prevent them all the more important.

“Our focus has always been on empowering members with intuitive, secure tools,” said Gilbert Gonzalez, CEO of the San Antonio Board of Realtors, in a statement. “Passkeys are a perfect fit, giving our members a seamless login experience while supporting our mission to lead with innovation.”

Solid Earth works with a number of technology-forward MLSs across the industry, such as BeachesMLS, Miami Realtors, and the Greater Baton Rouge Association of Realtors.

On top of its security tools, the company builds home search portals, company websites, member communication platforms and membership dashboards, among other custom offerings.

“Our mission is simple: to create one secure record for every real estate professional in the U.S. — making life easier for them and the MLSs that support them,” Rebecca Pearson, VP of Marketing and Communications at Solid Earth, said in the release. “Passkeys are a major leap forward in delivering on that promise.”

Email Craig C. Rowe

by OB Jacobi | Jun 27, 2025 | Industry, News Feed

MLSs are just too important to the health of the industry, and to the homebuying and selling process, to keep them under NAR’s control, Windermere co-President OB Jacobi writes.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Recent events surrounding private listing networks and the National Association of Realtors’ Clear Cooperation Policy (CCP) have made one thing clear to me: NAR needs to get out of the multiple listing service (MLS) business. That may sound bold — and it’s probably not a position the organization will welcome — but I believe much of the mess we’ve experienced in recent months could have been avoided if MLSs had the power to govern their own rules.

TAKE THE INMAN INTEL SURVEY FOR JUNE

Over 90 percent of the Multiple Listing Services around the country are Realtor-owned and operated and must follow overarching policies and rules set by NAR, such as CCP. By contrast, the Northwest Multiple Listing Service (NWMLS), which covers most of Washington State and parts of Oregon, is a broker-owned, not-for-profit organization that operates independently from NAR.

OB Jacobi

Its policies and rules are developed by committees, task forces and experts and reviewed by elected board members for the benefit of its 30,000+ members and their clients. And it is for this reason that the NWMLS was one of the only MLSs in the country not included in the NAR antitrust lawsuit or settlements.

The fallout of these lawsuits and the confusion NAR caused by modifying CCP earlier this year calls into question their fitness to dictate MLS rules. MLSs have become too complex for them all to have blanket rules, and they should be trusted to figure out what’s best for their memberships and their communities.

MLSs are too important to leave them under NAR’s control

This isn’t meant to be a bash on NAR — I genuinely believe they provide a great deal of value to our industry. But they should focus on their strengths: education, research, member benefits and, especially, advocacy. The value of NAR’s lobbying efforts in Washington, D.C., cannot be overstated.

But MLSs are just too important to the health of our industry — and to the homebuying and selling process — to keep them under NAR’s control. The more NAR tries to jerry-rig the MLS process, the more confusion they cause. And that confusion opens the door to anti-MLS brokerages pushing private listing networks that could set our industry back decades. Not to mention the lawsuits that follow when they don’t get their way.

NAR, I really do appreciate everything you do for our industry. But when it comes to managing MLS rules and policies, it’s time to relinquish control and focus on what you do best. That shift would be a true win-win for everyone.

OB Jacobi is the co-president of Windermere Real Estate.

by Inman | Jun 27, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Want to level up your business? Inman Access offers expert-led tutorials with insights, advice and ideas designed to help you build your skills every day.

Real estate coach and trainer Verl Workman shares innovative strategies to generate leads and convert them into loyal clients without breaking the bank. Don’t miss the chance to completely transform your lead generation game!

Elevate your skills and set yourself up for success in 2025. Watch the session above, plus get fresh content added weekly, with Inman Access.

Watch now.