Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The U.S. bombing of nuclear sites in Iran that quickly sent the country to the brink of another broad conflict in the Middle East has added one more issue for those mired in a sluggish real estate market to worry about.

Of course real estate professionals never count on world conflicts to influence their bottom line, and war is a tragedy first and foremost for those directly in harm’s way. But the situation in Iran has the potential to ripple through global economies — impacting, among many others, real estate professionals and the people they serve.

With that in mind, we sought to make sense of what happens to housing when conflict breaks out, as well as what has happened to home sales historically during times of war involving — directly or indirectly — the U.S.

The result of this effort suggests that so far, economists haven’t seen responses in the relevant markets that might further hurt home sales.

Matthew Gardner | Gardner Economics

“Right now there is caution,” Matthew Gardner, an economist with Gardner Economics, said. “But we haven’t seen any kind of panic, whatsoever.”

Those signs of panic would likely first appear in oil, stocks and bonds.

In this case, economists have quickly turned their attention to the conflict’s impact on oil prices.

Oil is a direct and indirect source of inflation in the economy, so a conflict that leads to even the threat of Iran closing the Strait of Hormuz, a choke point in the Persian Gulf where roughly 20 percent of the world’s oil supply flows, was thought to send oil prices higher. The possibility that Iran would close the strait has been widely discussed during the conflict.

“That could have led the Fed to delay cutting rates even longer, and potentially you could see mortgage rates spiking,” Gardner said. “But that one thing didn’t happen.”

If oil prices rise, it could push up the consumer price index, making it even less likely for the Federal Reserve to cut the federal funds rate, which has an indirect effect on mortgage rates.

Instead, oil futures fell during the first hours of trading after the U.S. strikes on Iran and were down 8.6 percent as of mid-day Tuesday.

Oil prices as of mid-day on Tuesday, June 24, 2025

Economists next watch for volatility in equity markets. Had there been a sell-off in the stock market that drove down share values, investors and other potential homebuyers may have had less wealth with which to buy a home, Gardner said. That could have had an even bigger impact on the luxury market.

“But we didn’t see that,” Gardner said. “So far, so good.”

The third thing Gardner said he’s keeping an eye on is whether there are indications that global investors are moving money into the U.S. via real estate or the bond market.

“You could actually see money coming in, potentially, to the U.S. because it’s considered to be a global safe haven. Also it’s the global currency,” Gardner said. “That has the potential to actually lower mortgage rates.”

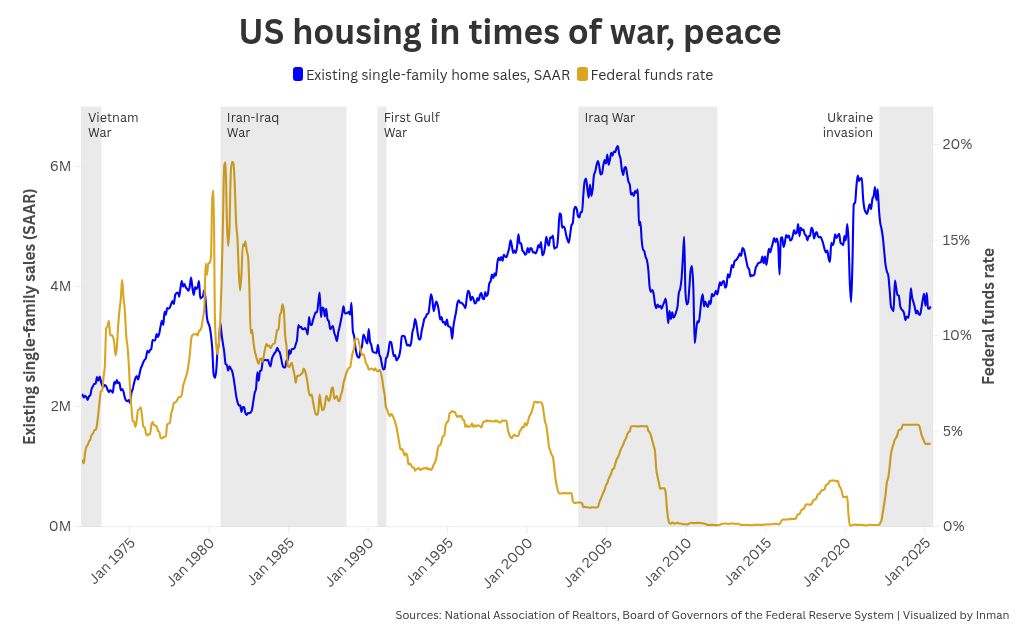

War, peace and interest rates

Inman analyzed the data for existing single-family home sales dating back to January 1965 to try and understand the impact of war involving the U.S. and the housing market.

And while there are some trends in home sales that appear to generally track global conflicts, they also appear to more closely track the 30-year fixed rate, federal funds rate and 10-year treasury yield.

While this is not a comprehensive analysis of all factors — for instance, recessions and mortgage rates — it does paint an interesting picture.

The graph above shows that decades ago, home sales fell sharply as the Federal Reserve quickly raised the federal funds rate to combat quickly rising inflation. That happened to coincide with the Iran-Iraq War, when home sales fell before beginning to climb in mid-1982.

Operation Desert Shield began Aug. 2, 1990. The following day, mortgage rates were 9.84 percent. Rates jumped to 10.29 percent within three weeks and remained above 10 percent for much of the operation before beginning a long descent.

Home sales followed suit, with a sharp — and brief — decline and then rebound.

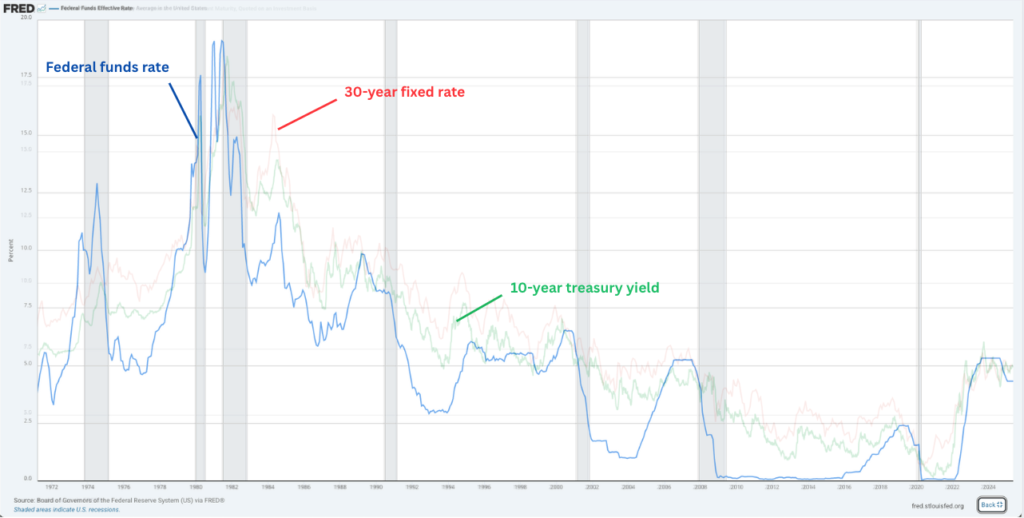

10-year Treasury Yield, the federal funds and 30-year fixed mortgage rates. FRED

In the case of Operation Desert Storm, which lasted for about six weeks in early 1991, rates fell.

Later, sales dipped sharply following the September 11 attack on the World Trade Center and invasion of Afghanistan before continuing a climb during the early years of the U.S. war with Iraq.

Sales continued to climb toward the apex of the housing bubble that burst in September 2005, preceding through the Great Recession.

The takeaway is that home sales more closely track things like mortgage rates than wars, though there are conditions caused by war that can impact rates and sales.

And while the Federal Reserve is currently walking a tight rope between taming inflation and keeping rates high for so long it causes a recession, Gardner said it wasn’t a recession specifically that had economists worried about the housing market.

“Some could argue that if it becomes bigger,” Gardner said, “and involves more of the Gulf states, we could see more of an economic global slowdown.”

Data editor Daniel Houston contributed to this story.

Amid fighting over the federal funds rate, NAR says home sales were 0.7 percent lower in May than a year ago as inventory rose to a 4.6-month supply

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Existing-home sales ticked up slightly from April to May but fell to a pace that’s even lower than the same time last year, according to new data released by the National Association of Realtors on Monday.

Existing-home sales dropped 0.7 percent compared to May 2024, to a seasonally adjusted annual rate of 4.03 million. Sales were 0.8 percent higher in the month than in April, NAR noted.

Inventory was 20.3 percent higher in May compared to a year earlier, NAR said, as the number of homes for sale rose to 1.54 million — or a 4.6-month supply.

“The relatively subdued sales are largely due to persistently high mortgage rates. Lower interest rates will attract more buyers and sellers to the housing market,” NAR Chief Economist Lawrence Yun said. “Increasing participation in the housing market will increase the mobility of the workforce and drive economic growth.”

It’s not clear just when mortgage rates might fall or what might cause them to drop.

President Donald Trump and Federal Housing Finance Administration Chairman Bill Pulte have been publicly calling on Federal Reserve Chair Jerome Powell to either cut rates or resign from his post before his term ends next year.

But it’s not clear that a drop in the federal funds rate, which can indirectly impact the rates for car loans and credit cards, would lead mortgage rates to fall from their current rate of 6.81 percent on average for a 30-year fixed. That’s up from 4 percent a decade ago, and from a record-low of 2.65 percent in January 2021.

Amid the ongoing high-rate environment, and with consumer sentiment low — just 26 percent of Americans believed May was a good time to buy a home — sales remained sluggish in much of the country in May.

The lower sales environment has dogged economists and real estate insiders who expected home sales to be higher this year than last, when sales fell to the lowest point in nearly 30 years.

Anywhere Real Estate dropped its earnings estimate for the second quarter of this year by up to 10 percent, saying a slower-than-expected sales environment has cut into its earnings.

NAR said in December that it expected mortgage rates to fall to 6 percent this year, a forecast that has proved increasingly difficult to get right. The trade group now says stubbornly high rates are weighing on the market.

“If mortgage rates decrease in the second half of this year, expect home sales across the country to increase due to strong income growth, healthy inventory, and a record-high number of jobs,” Yun said.

The sales of existing single-family homes rose 1.1 percent from April to May, while sales were down 2.7 percent for condos and co-ops.

Some markets were particularly strong, even when compared to last year, while others were sluggish.

Home sales were up 4.2 percent in the Northeast compared to a year ago, and prices rose 7.1 percent, NAR said.

Meanwhile, sales fell 6.7 percent in the western U.S. compared to a year ago while prices ticked up 0.5 percent.

Sales rose 1 percent in the Midwest and fell 0.5 percent in the South, NAR said.

Existing-home prices rose by 1.3 percent from a year ago, hitting $422,800 in May. That marked nearly two straight years of home price increases.

The chair of the Federal Housing Finance Agency, Fannie and Freddie has spent the past day calling on Powell to step down, saying he’s responsible for high home prices.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools, and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The chair of the Federal Housing Finance Agency (FHFA) is in an outright war against Jerome Powell, chair of the Federal Reserve, saying he is responsible for housing unaffordability and demanding that he resign.

Bill Pulte took to the social media platform X as well as national cable TV to call for Powell’s resignation in the days after the Federal Reserve opted to hold rates steady — a decision it made earlier this week. Pulte blamed Powell for keeping interest rates high.

“Jerome Powell is a main reason for the Housing Supply Crisis in this Country,” Pulte wrote Thursday in one of several X posts on the topic. “By improperly keeping interest rates high, Jerome Powell is trapping homeowners in low-rate mortgages and choking off existing home sale — directly fueling the housing supply crisis. He must lower rates.”

Pulte and President Donald Trump have both been putting pressure on Powell — who was appointed to the chair position in 2018 during Trump’s first term in office — to lower the federal funds rate. The federal funds rate can indirectly impact mortgage rates, automobile loans and credit card rates.

Powell’s term ends in May 2026. Pulte took to Fox News to spread his message on Friday morning, saying that Powell should either lower rates before the end of his term or resign.

“Peoples’ mortgage affordability has been crushed in the last four years,” Pulte said. “People have to pay double what they had to pay compared to President Trump’s first term in order to buy a home.”

Pulte said that Powell was “one of if not the biggest reason for the housing supply crisis that we have in this country.”

“It’s hurting Americans right now. Nobody wants to sell their existing homes,” he said. We need to get that inventory churning in this country again.”

Pulte didn’t answer when asked if he had heard from Powell since calling for his resignation.

Trump took to his Truth Social platform to share Pulte’s message.

“Too Late—Powell is the WORST. A real dummy, who’s costing America $Billion!” Trump wrote. In a separate message he wrote that the federal funds rate should be 2.5 points lower than it is.

The Federal Reserve began quickly raising the federal funds rate in March 2022 to combat high inflation and an overheated labor market. It stopped raising the rate in August 2023 and implemented a brief series of cuts in September 2024 but has not cut them since Trump’s second inauguration.

The board has continued to express caution, saying it was waiting to see the impact of Trump’s tariff policy before moving to lower rates.

Powell said this week that he expects a “meaningful amount of inflation” to arrive in the coming months.

“We have to take that into account,” Powell said.

“Increases in tariffs this year are likely to push up prices and weigh on economic activity,” Powell said. “The effects on inflation could be short-lived, reflecting a one-time shift in the price level. It’s also possible that the inflationary effects could be more persistent.”

A renter outside Portland, Oregon, sued Compass this week, saying its agents contacted her despite her phone being on the National Do Not Call Registry and multiple requests to stop calling.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A renter outside Portland became the latest to target a major real estate brokerage with a lawsuit over telemarketing practices this week when she filed suit against Compass and one of its offices over unwanted calls and texts.

Jessica Murch said the company and its brokers and agents violated the Telephone Consumer Protection Act of 1991 when they called her with questions about listing the home she lives in with Compass.

Murch, who said she doesn’t own the home, said she received at least four calls and five texts she says she didn’t consent to from brokers and agents at Compass.

Murch became the latest consumer to file suit against a major real estate company this spring when she sued Compass in U.S. District Court for Oregon on Tuesday.

Last August, Murch said she clearly asked the Compass broker to not call or email her again after the initial contact.

About two weeks later, Murch said she received another call from a different Compass agent asking if she was interested in listing her house and relocating.

“The Plaintiff stated that she thought that she was pretty clear that she no longer wanted to receive calls from Compass and didn’t want to talk to Compass, and reiterated her internal do not call request.”

Murch continued getting calls into 2025, she said, up until two weeks before filing her lawsuit.

“Telemarketing calls are intrusive,” Murch said in her complaint. “A great many people object to these calls, which interfere with their lives, tie up their phone lines, and cause confusion and disruption on phone records.”

Compass declined to comment, saying it doesn’t comment on pending litigation.

“Plaintiff and the Class have been harmed by the acts of Defendants because their privacy has been violated and they were annoyed and harassed. In addition, the calls occupied their telephone lines, storage space, battery life, wear and tear, and bandwidth, rendering them unavailable for legitimate communication, including while showering, getting ready for work, driving, working, and performing other critical tasks.”

Murch proposed a class that includes anyone who received multiple calls or texts from Compass or its agents if their numbers had been on the National Do Not Call Registry for at least a month before the contacts began.

She is requesting damages of between $500 to $1,500 per call or text.

Murch’s lawsuit was filed just days after a New York homeowner sued Keller Williams. The homeowner in that case made similar allegations against the franchiser.

A New York homeowner claims text messages sent by an associate broker at Keller Williams amounted to an “invasion of her privacy” and a violation of the Telephone Consumer Protection Act.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A New York homeowner is suing Keller Williams after one of its agents sent unsolicited text messages advertising her services, according to a new lawsuit filed last week.

Sydney Thayer filed her class action lawsuit against the franchiser in the U.S. District Court for the Western District of New York on June 12, saying the texts were a violation of the Telephone Consumer Protection Act.

Thayer, who lives in Rochester, New York, said she received texts on her phone between April 2024 and March despite her number being on the National Do Not Call Registry.

Screenshots included in the complaint show that an associate broker told Thayer she received her information from Zillow and asked if Thayer was interested in her real estate services.

“Defendant’s unsolicited text messages caused Plaintiff actual harm, including invasion of her privacy, aggravation, annoyance, intrusion on seclusion, trespass, and conversion,” Thayer wrote in her complaint. “Defendant’s text messages also inconvenienced Plaintiff and caused disruption to her daily life.”

The New York resident is seeking $1,500 in damages for each call that is found to have violated the TCPA, as well as an injunction preventing the practice.

A spokesman for Keller Williams acknowledged the lawsuit and said it was looking into the matter.

“We’re aware of the lawsuit alleging a TCPA violation by a real estate agent affiliated with one of our independently owned franchisees, and we are reviewing the matter,” said Darryl Frost, a Keller Williams spokesperson.

The new lawsuit is only the latest in a series of complaints targeting the company’s telemarketing tactics.

In January 2023, Keller Williams Realty agreed to pay $40 million to settle a class action lawsuit that alleged the franchisor’s agents made unsolicited, pre-recorded calls to consumers without their consent, including calls to consumers on the National Do Not Call Registry.

Months after that settlement, Keller Williams was hit with another, similar class action suit filed by a Las Vegas resident.

A slate of attorneys sued the company in 2019 for similar conduct.