by Taylor Anderson | Jun 17, 2025 | Industry, News Feed

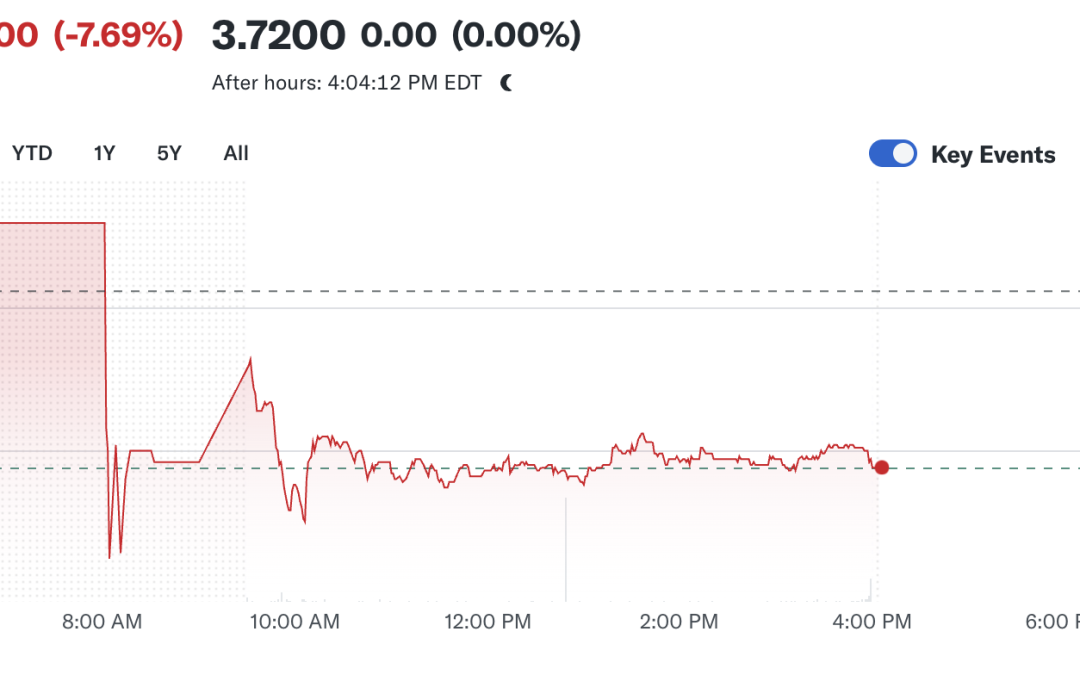

The company now expects to earn as much as 10 percent less this quarter than it expected in April, according to a new SEC filing. The company’s stock price fell sharply in early trading hours.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The slow real estate market is weighing on Anywhere Real Estate.

The company told investors in a filing with the Securities and Exchange Commission on Tuesday that it projects earnings to be as much as 10 percent lower in the second quarter than it expected in late April.

Six weeks ago, Anywhere told investors it expected its earnings before interest, taxes, depreciation and amortization (EBITDA) to be approximately the same as it was a year ago.

This week, however, the company revised that estimate downward and said it expected earnings from its brokerage and franchise businesses to fall between 3-10 percent.

The company said the downward revision was “largely due to softer homesale transaction volume than expected in the second quarter of 2025, driven by market and macroeconomic volatility,” according to the filing from Chief Financial Officer Charlotte Simonelli.

Anywhere Real Estate includes Better Homes and Gardens Real Estate, Century 21, Coldwell Banker, Corcoran, ERA Real Estate and Sotheby’s International Realty.

According to the National Association of Realtors, home sales in April were on pace for an annualized rate of 4 million homes sold this year.

The company reported a net loss of $78 million during the first quarter of the year.

Anywhere stock after the markets closed.

The revision led to a 7 percent drop in Anywhere’s stock value during early trading hours on Tuesday despite the company expressing a hint of optimism for a sales rebound.

While revenue is lagging in the second quarter, Anywhere said in the filing that it expects its earnings for the full year to be the same as it reported earlier this year.

That’s “based primarily upon our expectations for improving homesale transaction volume in the second half of 2025,” the company said.

Some of that second half performance is due to ongoing cost-cutting measures, which the company said were more heavily weighted toward the second half of the year.

The company said that it had cut costs by $14 million in the first quarter, and that it expected to cut costs by $100 million throughout the year.

Other savings would come from “additional cost management actions we intend to take.”

“Despite a historically challenging housing market, we continue to demonstrate strong financial performance and strategically invest in the business to propel us for future success faster,” CEO Ryan Schneider said at the time.

Email Taylor Anderson

by Taylor Anderson | Jun 17, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

President Donald Trump has an ear for real estate, and for a few minutes in January, Anthony Lamacchia got to bend it.

The industry that put Trump on the map has felt under attack in recent years, and a chance meeting that put the Massachusetts brokerage leader in front of the president earlier this year provided an opening for Trump to hear about it.

Lamacchia, CEO of Lamacchia Companies, told Inman exclusively that he received an invite alongside other business leaders to sit down with Trump at Trump International Golf Club West Palm Beach in January, two weeks before his inauguration for a second term in office.

At that meeting, Lamacchia told the incoming president that the Department of Justice under President Joe Biden appeared intent on punishing the real estate industry.

“I said, ‘Mr. President, are you aware that the Department of Justice has it out for real estate, organized real estate?’” Lamacchia told Inman. “He said, ‘I’m not. Tell me more.’”

Lamacchia said that for at least three minutes he talked “very substantially” with Trump about how the DOJ had backed out of a settlement agreement reached late in Trump’s first term.

The DOJ simultaneously announced a lawsuit and a settlement with the National Association of Realtors over various NAR rules in November 2020, after Trump lost his first re-election bid to former President Joe Biden. In July 2021, the DOJ withdrew from the settlement, and NAR tried for years fighting with the DOJ all the way to the Supreme Court.

At a meeting with 20 other business leaders, Lamacchia seized the opportunity to inform the president about one of real estate’s biggest headaches of late.

“He was not happy to hear it,” Lamacchia said. “He said, ‘Can you send me some information on that?’ So after the meeting, I sent an email to his assistant.”

Lamacchia spoke with Inman ahead of Inman Connect San Diego, where he’ll be speaking alongside other titans of real estate.

The following is a Q&A with Lamacchia, edited for clarity and brevity.

Inman: What do you expect the next three and a half, four years to be like under the Trump DOJ as it relates to real estate?

Lamacchia: I think it will be better. The prior DOJ, when Trump was in last time, was much more reasonable. And they made a deal with us.

I told Trump this. I met with Trump in January with 20 other business owners. I said, ‘Mr. President, are you aware that the Department of Justice has it out for real estate, organized real estate?’ He said, ‘I’m not. Tell me more.’ I said, ‘Your Department of Justice made a deal with NAR in November of 2020, signed the deal. There were a couple of industry changes that were agreed to, and Biden’s DOJ came in and undid the deal in June of 2021.’

And he was like, ‘Really?’ He was not happy to hear it. He said, ‘Can you send me some information on that? So after the meeting, I sent an email to his assistant and I never heard anything. But he was not happy to hear it.

I would think that this would be an industry that he would have an ear out for.

Frankly, I’ve been sitting around saying, when’s the shoe going to drop? Because I talked to him about it for three, probably three and a half minutes straight. Very substantively.

He was very interested. He asks very good questions. I mean, this guy, there’s no flies on him. And he said to me, ‘Why were you guys being investigated in the first place?’ And I said, ‘Well, the DOJ does an investigation in various industries every so many years. And with real estate, they do it about every decade.’ And then he goes, ‘Oh, antitrust?’

I said, yes. He goes, ‘OK, that makes sense.’ I said, ‘They negotiated for about a year, agreed to a couple of small changes. Your DOJ made the deal, finalized the deal in November of ‘20. Biden’s DOJ came in and undid the deal for the first time in history. A DOJ deal was undone.’ And he did not know. He was like, ‘Wow.’

That’s pretty incredible.

At the end, when I took a picture with him, he grabbed my arm and he goes, ‘OK, make sure to send that information.’ ‘OK, I will.’ He goes, ‘Don’t forget.’

I go, ‘Mr. President, I’m not going to forget.’

That’s interesting. I had no idea you met with him. Why did you not make it public?

I think just because it’s like everybody is so politically mental now. From where I sit, if Biden, if I had a chance to meet with Biden a year, two years, three years ago, I would have done it in a second.

But if I met with Biden, everybody would be like, ‘Oh, cool.’ You meet with Trump. It’s like, ‘Oh, you’re horrible.’ Listen, it was a business meeting.

On CCP, you’ve been clear all along. You said throughout you wanted CCP to stay, but that NAR was basically in a bind and needed to do something. What was the bind that they were in.

DOJ pressure. And then Robert Reffkin. I think he sort of self-perpetuated it. And hey, you know, good for him if that’s how he feels, but I think he’s wrong. And I also think the way that he went about it was terrible.

I mean, he’s criticizing NAR. You see the stupid post he did one weekend, put up a post about, this is NAR’s boardroom. What the hell does that have to do with the CCP policy?

But I think Robert Reffkin and the DOJ, although the DOJ never publicly came out and said they’re for or against CCP. But I think they pressured NAR. I don’t know that, just so you know. But I think they sort of put pressure on them.

Maybe I’m asking the wrong guy here, given where you already stand. But how is that pro-consumer in the DOJ’s eyes? Do you have any idea?

They don’t know what the fuck they’re talking about. You can quote me on that. They don’t know what the fuck they’re talking about. And here’s the thing. When I say the DOJ, I’m talking about the DOJ that we’ve seen for the last four years. I really can’t tell if this new DOJ is different yet. From what I’ve heard, they’re a bit more reasonable.

They’re a bit more business friendly. But when I say that comment, I’m referring more to the policies of the last four years. My attitude is the DOJ of the last four years has really gotten things wrong in our industry.

Do you feel like the industry itself, players in the industry are divided amongst each other right now? Does it feel like a divisive time or or not?

Yes, there’s no question. And part of it’s just grumpiness. There’s been a very big housing recession for three years now and people are just grumpy. And I don’t know if it’s a coincidence or if it was on purpose, but our industry also came under attack. You know, came under attack from frivolous lawsuits.

And it ended up being that, you know, we got hit with what I refer to as judicially sanctioned extortion. But even putting the case aside, there’s just other stuff.

It’s a divided industry. What are you doing? What are you standing for?

The biggest thing I want to see is interest rates come down. The biggest thing.

I do think that the Trump administration is making some progress that is going to lead to interest rates coming down. But is it happening as fast as we would all like or as fast as he promised? No. It’s hard to fix the system. But there are some roots of the economy that are screwed up.

And he’s obviously working to fix that. And I think it’s working. And I think we’re going to see rates come down later in the year.

Email Taylor Anderson

by Taylor Anderson | Jun 16, 2025 | Industry, News Feed

The company offered thousands of quick cash loans in exchange for 40-year exclusive listing agreements that a judge found violated the law and issued an injunction stopping the practice.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego.

Months after a judge ordered MV Realty to terminate long-term contracts with homeowners, the South Florida real estate brokerage has begun letting its clients out of the fraudulent contracts.

According to a report by the Tampa Bay Times, MV Realty has terminated thousands of its contracts, which trapped the firm’s clients into 40-year exclusive listing agreements with the brokerage.

Under the terms of the so-called “homeowner benefit agreements,” if clients listed their homes with another brokerage, MV Realty would place liens on their properties and charge them 3 percent of the property’s value to let them out of the contract.

The state of Florida sued the company in November 2022. In February, a judge ordered the firm to cancel its contracts within two weeks.

The state later said the company failed to comply with the court’s injunction until it recently began terminating the contracts, according to the Times.

MV Realty would work with homeowners who were in need of a quick cash loan. In exchange for money up front, MV Realty would lock its clients into the long-term contracts.

The state said the company violated the Florida Deceptive and Unfair Trade Practices Act through the enforcement of its contracts, and that more than 9,300 homeowners were affected.

“In my almost six and a half years with the office, this was one of the worst abuses that crossed my desk,” former acting attorney general John Guard said in a statement earlier this year. “The 9,303 Floridians who were subject to MV Realty’s unconscionable practices will have their properties unencumbered by this injunction and we will continue to hold MV Realty responsible for its abuses.”

The brokerage began facing legal trouble throughout the country as its notoriety spread and states began filing their own lawsuits to stop its conduct.

MV Realty lost its ability to transact real estate in Colorado. California blocked the company from enforcing its long-term contracts late last year.

Amid the mounting legal battles, the company initially filed for chapter 11 bankruptcy protection before withdrawing that request.

Email Taylor Anderson

by Taylor Anderson | Jun 12, 2025 | Industry, News Feed

After posting losses in 16 of the past 18 quarters, Opendoor implemented the latest in a string of layoffs on Wednesday, primarily on the iBuyer’s sales side, Inman has learned exclusively.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Opendoor let go of another 40 employees on Wednesday in what the company is describing as a targeted restructuring within its sales operation as it seeks to reverse an ongoing string of losses and build new revenue streams outside of buying and selling houses, Inman has learned exclusively.

According to an internal email obtained by Inman and a confirmation from the company, Opendoor said it implemented its latest round of staff reductions as part of a shift to become a “multi-product, multi-channel” company.

The layoffs were the latest in a series of restructuring and maneuvers aimed at finding a path toward profitability and growth after the company rose to become the largest, and one of the only remaining large-scale, iBuyers.

“Yesterday, Opendoor implemented a small, targeted restructuring, primarily within our sales organization,” an Opendoor spokesperson told Inman. “This change reflects our continued shift toward a unified go-to-market strategy — one that brings sales, marketing and industry channels into tighter alignment.”

The restructuring included transitioning 70 more employees into unspecified new roles, the company said.

The changes were only the latest sign that Opendoor was continuing to evolve after years of challenges to its primary model of buying homes, rehabbing them and selling them, ideally at a profit.

Notably, Opendoor has been talking more about generating revenue through a program involving referrals with agents and other “asset-light” revenue streams.

“By integrating these functions, we’re building a more sales-centric organization that better supports both our direct-to-consumer and partner agent strategies,” Opendoor said. “It’s a deliberate step toward creating a leaner, more asset-light business — one that can serve more customers and scale with discipline.”

The latest shift follows a trend for the iBuyer, which has posted collective net losses of nearly $2.8 billion in the 18 quarters since going public in its quest to buy homes and sell them at a profit.

Cutting toward profitability?

But while the company scaled to become the largest within the iBuying sector, it has consistently struggled to post a profit and has in recent years sought to evolve beyond the core iBuying concept.

Opendoor has posted a profit during just two of the past 18 quarters, according to the company’s earnings reports dating back to the fourth quarter of 2020, when the company went public.

In that same time, other companies that also had significant iBuying segments — perhaps most notably Zillow — abandoned the attempt to profit from iBuying at scale.

Meanwhile, Opendoor’s cash and cash equivalents has fallen 76 percent from its peak in early 2022, when it was using some of its $2.3 billion to ramp up its home-buying efforts amid a red-hot market.

At the end of the third quarter of this year, when Opendoor reported an $85 million loss, the company had $559 million cash and cash equivalents.

Amid the slowdown, the company has shifted its members of leadership and trimmed staff in multiple rounds.

In April 2023, Opendoor lopped off 560 positions, or 22 percent of its workforce, as it weathered a sharp downward shift in the market after several years of growth.

Last year, the company announced it had let go of about 300 employees “as part of a reorganization aimed at prioritizing strategic growth and driving long-term efficiencies,” according to its annual earnings report released in February. Those layoffs followed a $78 million loss in the third quarter of 2024.

The company finished 2024 with 1,470 employees, it said in its annual earnings report. 1,128 of those employees were in the U.S., the company said at the time.

During the first three months of this year, Opendoor laid off another 65 employees, which it said represented 5 percent of its workforce at the time. Those figures suggest the company had 1,300 employees.

That would mean that, after Wednesday’s layoff, Opendoor has approximately 1,195 employees, a figure the company declined to confirm on Thursday.

If the upheaval wasn’t enough, Opendoor is also working to engineer its way out of a threat of a different kind.

Just last week, Opendoor announced that it was planning to implement a stock maneuver in an attempt to stay publicly listed on the Nasdaq Composite after its stock fell well below the $1 per share minimum in April and stayed there. On Thursday, Opendoor’s stock closed at $0.60 per share.

Email Taylor Anderson

by Taylor Anderson | Jun 11, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

WeWork is finally WeProfitable again.

One year after restructuring its debt after declaring bankruptcy in November 2023, WeWork has regained profitability and is debt-free, the coworking company told Bisnow Tuesday.

The company became notorious for its shared working office spaces across the globe, ballooning to over 800 locations and reaching a market cap of nearly $10 billion in 2022 and a peak valuation of $47 billion.

The company renegotiated with creditors as a way to shed expensive and unprofitable leases and clear up its $4 billion in debt.

In April 2024, real estate tech company Yardi Systems announced that it had become the majority owner of WeWork and said it would guide it through its bankruptcy and into the future.

“We were burdened for many years with our portfolio that everybody knew about and saw,” WeWork Regional President for North America Luke Robinson told Bisnow.

Robinson told the news outlet that the company has now posted six-consecutive months of positive revenue before accounting for interest, taxes, depreciation and amortization, or EBITDA, a figure that indicates strong revenue but which doesn’t mean WeWork is turning a net profit.

It also confirmed to Inman that it now has 170 locations, which puts it among the largest coworking companies in the U.S. despite being far smaller than its 2019 peak.

In its previous heyday, the company gained fame both for its size, flashy office spaces and eccentric CEO Adam Neumann, who was behind the company’s rapid rise and its failure to successfully go public.

Under its new leadership, WeWork has also tweaked its approach at some locations, working directly with landlords to act as a property manager that leases space in buildings and shares revenues with the owners.

That’s alongside its more traditional approach of leasing space and then renting that space to people who need office space.

Several investors and landlords told Bisnow that WeWork’s leadership had shifted and regained trust in the industry, leaving the company an open pathway to rebuild and continue growing.

“When you have a firm where the pendulum has swung back and forth many times, when someone can provide trust and stability, that is a very precious commodity,” Cushman & Wakefield Chairman of Global Brokerage Bruce Mosler told Bisnow.

Email Taylor Anderson