Stephen Brobeck, senior fellow at the Consumer Policy Center, examines competing interests and competing policies to determine which will benefit consumers.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Although there are sellers who benefit by listing their properties privately, they represent only a small percentage of all homesellers. A large majority benefits the most by immediately listing their property on their local multiple listing service (MLS) so that the four major portals can quickly make the listing available to all potential buyers.

Moreover, there are effective measures these sellers can take if they are particularly concerned about privacy issues.

If a significant number of sellers agree to private listings, most are likely to have been encouraged by agents who their brokerages are urging to push private listings. There is some evidence, for example, that some Compass agents are being pressed to do so.

Consumers, who typically lack experience dealing with a complex and opaque industry, are susceptible to a sales pitch that may well promise a higher sale price and a faster sale, both of which are claimed by Compass.

Opposite truths?

However, most of the available evidence on this issue suggests that the opposite is true. Separate research by both Zillow and Bright MLS on large numbers of listings found that homes listed on MLSs sold for higher prices than those privately listed.

Research by Compass challenged this finding, but it was limited to the company’s listings and did not provide a satisfactory explanation of the methods, including sample sizes. All other factors being equal, why would a limited listing sell for a higher price than a broad listing?

On the buyer side, there is no debate. It is clearly in the interest of buyers to have access to full information about the largest number of properties available for sale, and not just because they would have more choices of properties. Some private listers are telling sellers that they do not have to provide information to buyers about sale price history and time on the market.

Let’s not forget this …

Furthermore, to the extent that large brokerages successfully list privately, buyers will feel that to obtain access to a large number of listings, they must work with these companies. A decision by many buyers to do so would disadvantage small and local brokerages.

There is a real possibility that determined private listing efforts by a few major companies could shrink meaningful consumer choice of brokers.

The new Zillow and Redfin policy of not listing publicly marketed properties to which they did not have initial access, may not weaken the determination of big private listers. However, it is likely to curb the enthusiasm of their agents who must explain to clients that a private listing may prevent a listing on the two portals.

I do not agree with some of the policies of the two portals, and I also recognize that their decision on private listings addresses a highly complex issue involving industry rules. Nevertheless, I still believe that their new policy will benefit consumers both individually and collectively.

Stephen Brobeck is a senior fellow at the Consumer Policy Center (CPC), a new consumer think tank. Since 1975, he has served as a board member then executive director and then senior fellow at the Consumer Federation of America (CFA). Since 1990, he has researched and commented on residential real estate brokerage issues.

I wrote an article explaining why I am investing in real estate investment trusts (REITs) instead of rental properties. In short, REITs are still discounted, and I expect their lower valuations to result in higher returns in the coming years.

Unfortunately, it would seem that many readers miss the point of investing in REITs due to misconceptions. I saw several people in the comment section claim that REITs should be less rewarding investments because:

You don’t enjoy the benefits of leverage.

They are not tax-efficient.

You are paying managers instead of getting your hands dirty.

But these statements are just plain wrong, and I am going to prove it.

The Studies Bear It Out

Studies show very clearly that REITs are more rewarding investments than private real estate in most cases, and there are good reasons for this. This may seem surprising to some of you, but it really shouldn’t be. Here are three examples.

Study 1

FTSE Equity REIT Index compared to NCREIF Property Index as an annual return percentage (1977-2010) – EPRA

Study 2

Private Equity Real Estate compared to Listed Equity REITs as net total return per year over 25 years – Cambridge Associates

Study 3

Performance of U.S. REITs and Private Real Estate Returns (1980-2019) – NAREIT

Three Misconceptions and Why They’re False

I will give you eight reasons why REITs should be more rewarding investments than private real estate in most cases. But before that, I will quickly correct the three misconceptions that I keep hearing over and over again:

Misconception 1: You don’t enjoy the benefits of leverage.

This is nothing more than a misunderstanding. Investors seem to think that just because you cannot take a mortgage to REITs, you won’t enjoy the benefits of leverage, but this is incorrect.

What they ignore is that REITs are already leveraged. You don’t need to take a mortgage because REITs take care of that for you.

When you buy shares of a REIT, you are providing the equity, and the REIT adds debt on top of it. As such, your $50,000 investment in the equity of a REIT may well represent $100,000 worth of properties.You just don’t see it because what’s traded in the stock market is the equity, not the total asset value, but the benefits are the same.

Misconception 2: They are not tax-efficient.

This misconception stems from the fact that REIT dividend payments are often classified as ordinary income. But this is very short-sighted because there are many other factors that improve their tax efficiency—to the point that I pay less taxes investing in REITs than in rentals:

REITs pay zero corporate taxes, so there is no double taxation.

REITs retain 30% to 40% of their cash flow for growth. All of that is fully tax-deferred.

A portion of the dividend income is commonly classified as “return of capital.” That’s tax-deferred as well.

The portion of the dividend income that’s taxed enjoys a 20% deduction.

REITs generate a larger portion of their total returns from growth because they focus on lower-yielding class A properties. The appreciation is fully tax-deferred.

Finally, if all that still isn’t enough, you can hold REITs in a tax-deferred account and pay zero taxes with great flexibility.

Beyond that, REITs also have enough scale to have in-house lawyers to fight off property tax increases and optimize their impact.

All in all, REITs can be very tax-efficient.

Misconception 3: You are paying managers instead of getting your hands dirty.

Yes, you are paying managers, but the management costs of REITs are still far lower than that of private rental properties because they enjoy huge economies of scale.

Taking the example of Realty Income (O), its annual management cost is just 0.28% of total assets.There are huge cost advantages when you own billions of dollars worth of real estate, and REIT investors benefit from this.

Now that we have these misconceptions out of the way, here are the eight reasons why REITs are typically more rewarding than rental properties:

Reason 1: REITs Enjoy Huge Economies of Scale

It goes far beyond just management cost. Real estate is a low-margin business, with low barriers to entry. Therefore, scale is a major advantage to lower costs and improve margins. REITs excel at this.

Take the example of AvalonBay Communities (AVB). The REIT owns nearly 100,000 apartment units, resulting in significant economies of scale at every level, from leasing to maintenance and everything else in between.

Let’s assume that AVB owns 500 apartment units in one specific market, and it strikes a deal with a local contractor to change 100 carpets each year. It will of course get a much better rate for each carpet than what you could get if you made a deal to change just one.

Another good example would be if you need to hire a lawyer to evict a tenant. AVB has in-house lawyers working for them, which greatly reduces the cost.

Such economies of scale apply everywhere, and it makes a big difference in the end.

Reason 2: REITs Can Grow Externally

Private real estate investors are mostly limited to rent increases to grow their cash flow over time. We call this “internal growth” in the REIT sector. But REITs can also supplement their internal growth with what we call “external growth,” which is when they raise more capital to reinvest it at a positive spread.

That’s how REITs like Realty Income have historically managed to grow their cash flow and dividends at 5%+ annually, even despite only enjoying annual 1% to 2% annual rent increases. The difference comes from external growth.

It sells shares in the public open market to raise equity and then adds debt on top of it and buys more properties. As long as it can raise capital at a cost that’s inferior to the cap rates of its new acquisitions, there is a positive spread that will expand its cash flow and dividend on a per-share basis. It is not dilutive. It is accretive and creates further value for shareholders.

Private real estate investors cannot do that because they don’t have access to the public equity markets, putting them at a significant disadvantage right off the bat.

Reason 3: REITs Can Develop Their Own Properties

Most private real estate investors will buy stabilized properties and rent them out. At most, they may do some light renovations in an attempt to increase the value and rent.

But REITs go far beyond that. They are very active in their investment approach and will commonly buy raw land, seek permits, and build their own properties to maximize value.

It is not uncommon for REITs like First Industrial (FR) to build new class A industrial properties at a 7%+ cap rate, but if it bought such stabilized assets, it would only get a 5% cap rate. That puts it at a huge advantage. Not only will it earn a higher yield from newer properties, but it will also create significant value by raising capital and developing these assets.

REITs can do this because of their scale. They can afford to hire the best talent and tend to have great relationships with city officials, tenants, and contractors.

Reason 4: REITs Can Earn Additional Profits by Monetizing Their Platform

REITs will commonly also earn additional profits by offering services to other investors, and you participate in these profits as a shareholder of the REIT.

Many REITs will manage capital for other investors and earn asset management fees. As an example, they may create joint ventures when acquiring properties and let other investors ride their investments, charging them fees for managing them, boosting the return that the REIT earns on its own capital. Healthcare Realty (HR) commonly does that.

Alternatively, the REIT may offer brokerage or property management services. Some are so active in developing properties that they have their own construction crew and offer construction services to earn additional profits. Naturally, this also boosts returns for REIT shareholders.

Reason 5: REITs Enjoy Stronger Bargaining Power With Their Tenants

REITs are large and well-diversified, and this puts them in a stronger position when negotiating with tenants. This is key to earning stronger returns over time because it commonly allows the REIT to achieve faster rent growth.

If you only own just one or a few properties, you will be reluctant to raise the rent out of fear that your tenant will move out. You are not well-diversified, so a vacancy would be very costly.

However, REITs can enforce rent increases because they know that they will be just fine if the tenant moves away.It won’t have a big impact on their bottom line, and they have the resources to quickly release the property at a minimal cost.

Reason 6: REITs Benefit from Off-Market Deals on a Much Larger Scale

Most often, when private real estate investors buy a property, they will do so via the brokerage market. The properties are advertised for sale, they are priced competitively, and you also end up paying high transaction costs.

Again, the scale of REITs gives them a major advantage, as they will commonly skip the brokerage market and structure their own off-market deals.

Some REITs, like Essential Properties Realty Trust (EPRT), will reach out to property owners via cold-calling efforts and offer to buy their real estate. They will then structure their ownleases with landlord-friendly terms and typically close the deal at a higher cap rate than what they would have gotten in a more competitive bidding environment.

Reason 7: REITs Have the Best Talent

I briefly mentioned this earlier, but it is worth mentioning it again: REITs can afford to hire the best real estate talent because of their large scale.

Even despite paying them handsomely, their management cost is still far lower as a percentage of assets than what it typically is for private properties. And there’s no doubt that better skills will result in better returns over time.

These people go to the top schools, gain the best private equity experience, and eventually dedicate their lives to working long hours for the benefit of REIT shareholders. You cannot compete with them, especially if you are just a part-time landlord.

Reason 8: REITs Avoid Disastrous Outcomes

Finally, another important reason why REITs outperform on average is that they avoid disastrous results for the most part. The distribution of results is much wider for private real estate owners.

Some will succeed. Others will lose it all. They are highly concentrated, leveraged private investments with liability risk and a social component. Not surprisingly, there are countless real estate investors filing for bankruptcy each year, and these disastrous results hurt the average performance of private real estate investors.

But REIT bankruptcies are extremely rare. There have only been a handful of them over the past few decades, and most of them were REITs that owned lower-quality malls.

This shouldn’t come as a surprise, given that most REITs use reasonable leverage, are well diversified, and own mostly Class A properties. It is really hardto then mess it up.

Final Thoughts

REITs are typically more rewarding than private real estate investments. Studies prove this, and there is a strong rationale as to why this would make sense. In fact, it would be surprising if it were the opposite, given all the advantages that REITs enjoy.

However, this doesn’t imply that private real estate is a poor investment; rather, it highlights the importance of not overlooking REITs and including them in your real estate portfolio.

Invest Smarter with PassivePockets

Access education, private investor forums, and sponsor & deal directories — so you can confidently find, vet, and invest in syndications.

Note By BiggerPockets: These are opinions written by the author and do not necessarily represent the opinions of BiggerPockets.

Publicly traded real estate software company reAlpha Tech Corp (AIRE) has shipped what it’s calling a “super app” that will provide a free solution for end-to-end homebuying representation.

Whether it’s refining your business model, mastering new technologies, or discovering strategies to capitalize on the next market surge, Inman Connect New York will prepare you to take bold steps forward. The Next Chapter is about to begin. Be part of it. Join us and thousands of real estate leaders Jan. 22-24, 2025.

Publicly traded real estate software company reAlpha Tech Corp (AIRE) has shipped what it’s calling a “super app” that will provide a free solution for end-to-end homebuying representation and services powered in part by an artificial intelligence called Claire.

In an Aug. 20 press release, reAlpha directly referenced new rules put in place as part of a settlement between the National Association of Realtors and a class of consumers seeking restitution for the way real estate commission payment has traditionally been structured.

The application will not charge a commission for its use by a homebuyer and includes human intervention and suport by a licensed sales professional, according to the release. It offers home search and onboard title and escrow services.

The application was called Claire at one time, but its new iteration reflects a deeper integration with the AI and a more comprehensive consumer-first experience in the mobile environment.

“This launch is timed to coincide with the real estate industry’s shift in light of the National Association of Realtors’ (NAR) recent settlement to eliminate the standard 6 percent sales commission when purchasing a home. These rule changes went into effect Aug. 17, and reAlpha believes such changes make its commission-free offering to be even more compelling for property buyers,” the release stated.

In summary, the application is a digital buyer services solution. Highlights include “commission-free homebuying,” the support of Claire, its AI real estate agent, and AI-based natural language home search and recommendations.

Claire offers 24/7 support for general app use, as well as insights on the market and answers to concerns on the homebuying process, including offer submission and negotiations. It can also review and distill transaction documents, the company said. This would include home inspection overview, settlement statements and more digestable analyses of contracts, addenda and other pertinent paperwork.

“At reAlpha, we know buying a home is the biggest and most important decision many people will ever make,” said Mike Logozzo, president and chief operating officer of reAlpha, in the release. “We believe in leveraging AI to create a more personalized and supportive homebuying experience. The reAlpha super app is designed to provide homebuyers with all the tools and support they may need to find their dream home, at a great price and with the best experience, all from their mobile device.”

The July 2024 acquisition of Hyperfast, a title company licensed in Florida, Virginia and Tennessee, will allow reAlpha to offer built-in title services, and, when more meaningful, custom homebuyinig needs arise, the company’s licensed agents can step in. The company also said in the release it plans to offer mortgage services and home insurance options as it assembles a portfolio of industry service providers.

An Inman report stated that the company sold a retail-grade fractional investing platform providing a wide range of users the ability to establish a stake in Airbnb homes and other STR opportunities. Its GenA product uses its AI to create marketing content for STR hosts, similar to what many tools in the residential sales space do for listing agents.

HAPPENING NOW! At Inman Connect Las Vegas, July 30-Aug. 1, 2024, the noise and misinformation will be banished, all your big questions will be answered, and new business opportunities will be revealed. JOIN US VIRTUALLY.

Brad Inman revealed that he’s embraced longevity in the past year, even enlisting the assistance of a Chinese healer.

One of Inman’s new morning routines includes eating more fruits and vegetables — and cockadoodledoo-ing at the sun, like a rooster.

As he demonstrated, to the audience at Inman Connect Las Vegas on Wednesday, he encouraged others to try it — but without much success, based on the quiet response.

Regardless of that sleepy reaction, Inman was excited to translate that same kind of morning energy to navigating the industry’s biggest hurdles today — and hoped the audience would join him for the ride.

“I’m going to try to be honest about what I see happening, but I also want to give you the hope, excitement and energy that I have when we get through this perfect storm,” Inman said.

Inman noted that, even though many of the factors plaguing the industry right now — high mortgage rates, low inventory, commission lawsuits, NAR leadership disruptions — are largely out of agents’ control, many may still have the tendency right now to be hard on themselves about navigating this “perfect storm.”

Inman guided the audience to pat themselves on the back for surviving the recent industry difficulties. This time, many took him up on the opportunity.

“You deserve it!” Inman declared.

“Life isn’t always perfect, even for those of us who are perpetually optimistic.”

Inman detailed how he went through his own perfect storm recently, facing a trifecta of setbacks, including some bad business news, the deaths of some close friends and dealing with a new health issue.

“At a moment when I thought everything was perfect, nothing would go wrong, I had foolishly persuaded myself, ‘this is so great,’” Inman told the audience.

One of Inman’s friends who had passed away was Jennifer Berman, a name well-known within the industry for her leadership, particularly in the luxury space, and her participation at Inman Connect events over the years.

“She was a force. She was a positive force, no matter the circumstances,” Inman said. “So let’s give a round of applause for all the generous contributions Jennifer Berman gave to the real estate industry.”

The three setbacks, though unpleasant, helped Inman learn how to tackle such unexpected challenges in the future. And he encouraged agents in the audience to bring these tactics to the challenges they’re facing in the industry now.

With his business setback, Inman was decisive. When he faced an unexpected health problem, he embraced self-care. And when his friends passed away suddenly, he took the time to be present — something he had neglected as a younger man.

“With my friends dying, I did something I didn’t do when I was younger,” Inman said. “I wasn’t present … This time, I leaned into my grief, and I really tried hard to be present.”

But perfect storms have touched down in other parts of the world today too, Inman noted, pointing to the recent volatility in U.S. politics.

“In three-and-a-half weeks, we’ve had three historic events happen in the political world,” Inman said.

Those events included the epic debate fail between President Biden and former President Trump, the assassination attempt on former President Trump and the decision by President Biden to pull out of the presidential race.

“So we are stricken with anxiety and it’s very, very difficult,” Inman said. “Someone was saying last night at dinner that it’s affecting homebuyers’ confidence to even buy a house.”

In real estate, the perfect storm that’s been brewing for months is comprised of a frozen market, driven by high rates, low supply and a lack of affordability; the class action commission lawsuits; and a lack of leadership.

“We had the commission lawsuits, and we also had, at a time when most needed, a lack of leadership,” Inman said. “The leaders that we may have depended on to guide us through were all being sued. And the lawyers put duct tape on all our CEOs. And then the mothership, the National Association of Realtors, had a series of scandals, and all kinds of changes in leadership.”

But Inman also noted that all of these challenges seem to be moving in the right direction. Rates show signs of dropping in the next few years, inventory is finally starting to grow with the construction of more homes and new zoning laws in select cities that allow for ADUs are opening up more affordable housing.

But Inman encouraged those in the audience and the industry at large to put their thinking caps on to come up with even more solutions.

“We have so many underutilized structures,” Inman said. “What if we devised a system to get all that land, all those buildings and just gave it to the public, and said ‘all you have to do is fix this house, clean it up, and go to town.’ What we need now is a huge initiative.”

“We have thought big in the past when it comes to affordable housing; we can do it again,” he added. “Let’s get NAR straightened out so that we can [use] their force to get this done.”

Inman also expressed admiration for Kevin Sears, NAR’s new president, who spoke at ICLV on Tuesday.

“Let’s talk about leadership,” Inman said. “I don’t know about you, but that Kevin Sears was impressive. He was here. He was present. I’ve gotten up here too many times and trashed NAR. I am rooting for the new CEO (who came from the newspaper business, which I think is great) and I am rooting for Kevin.”

On Thursday, Inman noted, Independent presidential candidate Robert F. Kennedy Jr. will speak at ICLV about real estate policy and more. Inman teased that Kennedy will lay out his own housing plan and that everyone in the audience should be thinking about their own ideas for creating housing solutions.

“Think big [and] act big,” Inman encouraged. “Because the goddamn problem is very big.”

Inman went on to share how he believes the class action lawsuits are going to result in the commission pie being less per agent. But, because the costs for consumers are going to be less as well, Inman surmised that that will translate into more transactions — and less experienced or eager agents will also likely drop out of the industry.

“For the eager, the opportunistic, the hardworking, the clever, there’s going to be a way to make even more money as a real estate agent,” he said.

The innovation to come out of all these challenges will be the “biggest win” for the industry, Inman added. And even though he now calls the portal wars the “potty wars,” he believes the competition between big players like Zillow and Homes.com will just make the process of looking for a home better for the consumer at the end of the day.

When it comes to AI, Inman also said that he expects that it will improve humankind “in ways that we cannot imagine,” and it will ultimately make buying and selling a house easier on consumers and seem like a more positive experience — something that will be good for agents, too.

In closing, Inman expressed his gratitude to the ICLV audience.

“I am just grateful for seeing people like you here, wanting to learn, connecting, and I know you’re going to come through the perfect storm,” he said.

Lending industry leaders surveyed by Fannie Mae see the lack of housing supply as the biggest risk factor in 2024, but most expect refinancing to pick up next year if rates continue to fall.

At Inman Connect Las Vegas, July 30-Aug. 1, 2024, the noise and misinformation will be banished, all your big questions will be answered, and new business opportunities will be revealed. Join us.

Nearly two out three mortgage lenders trimmed their workforces in 2023, but most lenders expect to either maintain or grow their payrolls this year, according to a survey of more than 200 senior executives by mortgage giant Fannie Mae.

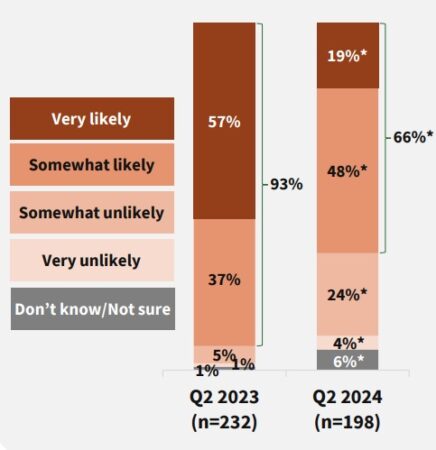

While the survey found two-thirds of mortgage industry executives think it’s likely the U.S. economy will tilt into a recession within the next two years, that’s down from 93 percent a year ago.

Lending industry leaders see the lack of housing supply as the biggest risk factor in 2024, but most (64 percent) expect a new mortgage refinance boom to kick off this year or next if rates continue to fall.

“After job cuts in 2023, and with lenders generally less pessimistic about the economy and the direction of the mortgage market, staff sizes appear to be normalizing” at the lowest level since 2014, Fannie Mae Chief Economist Doug Duncan wrote in summarizing the survey’s findings.

“Mortgage activity likely hit a post-pandemic floor following that era’s historically high mortgage purchase and refinance volumes,” Duncan wrote. “As a result, we believe some mortgage lenders are now preparing their workforces to meet potential growth in mortgage originations should the slow recovery of the housing market continue through the rest of this year and into 2025.”

Conducted in early May and released this month, Fannie Mae’s Mortgage Lender Sentiment Survey gathered perspectives from 215 senior executives at 198 lenders, including mortgage banks, depository institutions and credit unions.

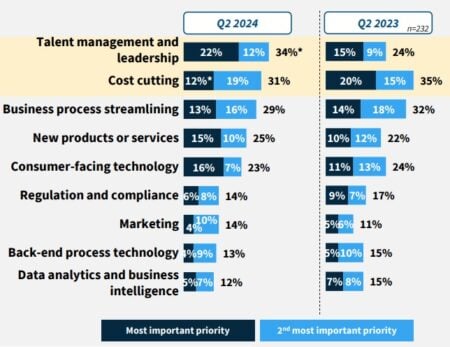

“Talent management and leadership” was the top priority for most executives, followed by cost-cutting and business process streamlining.

“Retention is top of mind,” an executive at one large institution told Fannie Mae. “We want to retain our LO (loan originations) team that is performing as well as continue to scout for new talent to join our organization. We are in growth mode for the foreseeable future.”

Fannie Mae defines large institutions as having more than $245 million in 2023 loan origination volume.

While 62 percent of mortgage executives said they cut their workforce last year, 54 percent said they expect 2024 staffing to stay about where it was last year, while 28 percent expect to staff up this year.

Last year, as mortgage rates were climbing past 7 percent to levels not seen in more than two decades, cost-cutting and business process streamlining were mortgage executives’ top two priorities.

An executive at a mid-sized institution with between $46 million and $245 million in originations said business process streamlining remains a top priority, with the lender migrating to a cloud-based system “to minimize new product introductions and streamline the process for employees and members seeking a loan.”

New products and services were a top priority for one in four executives surveyed, with a leader at a smaller institution (less than $46 million in originations) saying that “Traditional loan origination has decreased so much the last 18 months, we are looking at other types of ways to make money, be it new products or different services.”

Investments in consumer-facing technology — the top priority for lenders in 2019 — failed to crack the top three priorities for the third year in a row.

Lenders less certain of a recession in next 2 years

Mortgage execs think the odds of a recession in the next two years are better than even, but only 19 percent think a recession is “very likely,” down from 57 percent a year ago. Close to half of lending industry leaders (48 percent) still believe a recession is “somewhat likely.”

Scarce housing supply was the risk factor cited most often (64 percent) by mortgage executives, followed by mortgage rate changes (59 percent), household debt level (35 percent) and home prices (31 percent).

Fannie Mae economists, who last year were warning that Fed tightening would likely lead to a recession, backed away from that call in January.

In their June forecast, Fannie Mae’s highly regarded Economic and Strategic Research (ESR) Group forecast that purchase mortgage originations will grow by 14 percent next year, to $1.5 trillion, as 30-year fixed-rate loans will drop to 6.3 percent by the end of next year.

Fannie Mae economists are predicting even more dramatic growth in refinancing next year, with refi volume growing by 46 percent to $544 billion.

Two-thirds of mortgage executives surveyed by Fannie Mae are expecting a refi boom. While only 6 percent see that happening this year, 26 percent expect refinancing to pick up in the first half of next year, while 32 percent are planning on a refi boom kicking off in H2 2025.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.