by Lillian Dickerson | Jun 17, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

In 2023, Compass launched the first iteration of its artificial intelligence tool, Compass AI. At that time, the tool, which is housed within Compass’ tech platform, could generate content for agents, including for social media posts, listing descriptions, emails and more.

Now, agents will have the ability to simply speak prompts to Compass AI, and the improved tool will be able to do things like create follow-ups, develop marketing collateral, send client invitations to Compass One (the firm’s public-facing platform), create custom listing presentations, build transaction timelines, update and organize client contacts and more.

“So this represents a really big acceleration of [the platform,]” Rory Golod, president of growth and West regions at Compass, told Inman.

“This allows, effectively all of the administrative work that comes with a day-to-day for an agent to be done by AI,” Golod continued. “So what I think you’ll see [are] massive productivity gains, but also massive increases in ease.”

When Compass founder Robert Reffkin announced the updates during Compass’ annual retreat on June 3, agents gave Reffkin a standing ovation for two minutes, Golod said.

The latest version of Compass AI is currently being beta tested by select agents, and will roll out across the company later this year.

Inman spoke with Golod about the new tool and how it will improve agent efficiency. Here’s what he had to say, edited for brevity and clarity.

Inman: Could you clarify what’s new about this rendition of Compass AI?

Rory Golod: What we launched a few years ago was kind of like that first iteration, where it was really about creating content or giving advice. This is now a whole workload, this is actually, do actual work for me. This is like a true digital assistant, an AI assistant, because now I’m able to tell the system: create this, email the client, send this, put this together. Do all the stuff, whereas, the first version was, write a listing description, create a social media post, which was great at the time. That was a big deal. But the world’s evolved and so this is just far more expansive now. This is more about like, ‘Hey, Compass AI: do work for me.’

That’s something that agents have been really wanting to do for quite some time.

In this latest rendition of Compass AI, the tool will be able to track buyer behavior and tell agents which of their past clients are most likely to sell soon. That sounds similar to Compass’ ‘Likely-to-Sell’ tool that has been around since 2020. Does this mean that ‘Likely-to-Sell’ is going to be sunsetted?

None of our tools are going to go away. All it is, is it’s just going to make it easier. It will take ‘Likely-to-Sell’ and put it on steroids.

Imagine being able to ask for likely to sell based on all different types of factors. Right now it’s based on looking at their address and the comps around it, but what about, I want to see the 10 clients that have been the most active looking at listings online right now. Who of my clients doesn’t have an agent in New York? Who of my clients are looking at listings outside of New York state right now? Who of my clients have been on a collection [of listings] and commented on the collection or shared it with a friend or a spouse?

It’s infinite what it can do, so ‘Likely-to-Sell’ will be a big part of it. But now with [Compass] AI, we can go even bigger and bigger.

At the Compass retreat earlier this month, Robert Reffkin said there will be some tasks that Compass AI will just complete in the background without an agent prompting them at all. Could you clarify what those tasks are?

Right now, a lot of that will be the intermediate steps to creating all of this, and setting these things up and building out folders and all sorts of things that can just happen. Setting appointments, reminders, coordinating schedules, so much of that can just happen.

And then being able to automate steps through a transaction. When you’re doing a transaction with a client, you’re going through the transaction, there’s a full checklist of tasks and all those things. Now, they’ll have the ability to have all this be able to effectively be automated. So the agent is the one being updated — not the agent having to do the updating. That’s part of what makes this really, really exciting.

Definitely. At this point, what features do you think agents are most excited about?

I think it’s just the totality of the fact that they can just run the workflow. That [Compass AI promo] video is a minute-and-a-half, but that probably represents what would have been maybe a few hours of work. And even just the intelligence of the system, for it to be able to respond back and say, ‘Oh great, I’ll add this client. Are they a buyer? Are they a seller?’ You hear little things like that, and you’re like, ‘Oh wow, it’s smart. It knows what to ask.’ So I think that’s kind of one of the things that’s got people really excited.

How do you think Compass AI stands apart from other AI tools launched by brokerages over the past few yearss?

There’s no shortcuts in building technology. If we took over 10 years and $1.5 billion to build this platform, and we invest over $100 million per year in R&D, with some of the best engineering talent in the country, I don’t know how other companies that just don’t have anywhere near the financial resources to invest will be able to make that investment or are ever going to be able to build anything that’s comparable.

I think what happens is, a lot of the stuff we see are things that demo really well and look really good, but don’t actually work. And I think you can measure it by agent adoption and usage. You can show off great technology very easily but can you get people to actually use it? Does it work? Is it fully integrated? Does it do enough?

The challenge that I think exists, which is an opportunity for us with AI, is agents want to be able to ask it to do anything. If you give someone a car and you tell them they can go drive, but it only goes up to 40 miles per hour, it’s not going to be super effective, right? They want to be able to drive fast, slow, go long distances, whatever it is. So I think one of the things that really sets us apart is, because we have this platform, there are so many different workflows that this can quickly do. We don’t need to go get another piece of technology from another company to try to fit into what we’re doing for each one of these workflows. All these workflows exist. They all exist in Compass and all the data in the interactions and the interconnection exists.

If you’re creating a collection for a client, and then you want Compass AI to then write a beautiful email to your client with certain things in it, and then send that email, Compass AI can do that because it’s connected to your email. It’s connected to your CRM, it’s connected to the listing system. It’s all in one place.

But if you’re using another company’s tools, it’s not connected to your email, it’s not connected to your listing system, and so it ends up being really difficult and ultimately disappointing. So I haven’t seen another brokerage that’s been able to build technology that even comes close to the things that Compass has built. And I think that’s been kind of proven out in the market.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Lillian Dickerson | Jun 16, 2025 | Industry, News Feed

Down payments are declining even as home prices are rising because buyers are facing affordability challenges or opting to reserve more of their cash because of economic uncertainty, Redfin said.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

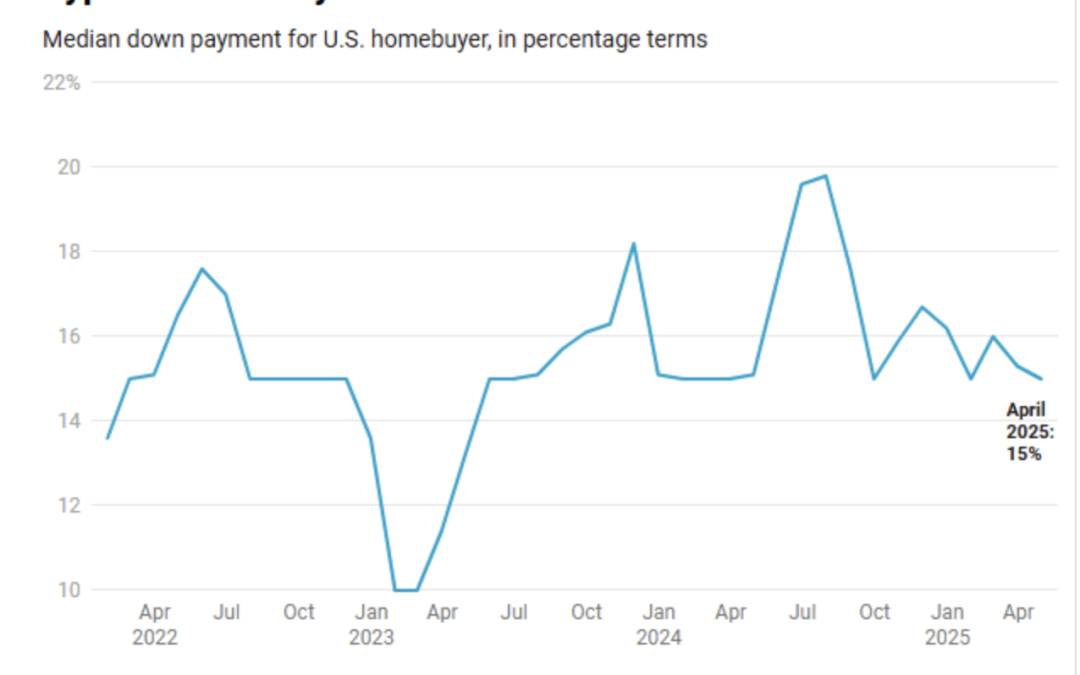

The median U.S. homebuyer’s down payment has fallen for the first time in nearly two years, according to data released Monday by Redfin.

The 1 percent drop, to $62,468, is subtle but significant, according to the report, which tracked county records in the 40 most populous metro areas in the U.S.

“The buyers who are moving forward today are being very careful with their finances because with housing costs near record highs, they’re typically spending a big portion of their paycheck to buy a home,” Redfin Premier agent Fernanda Kriese, who is based in Las Vegas, said in the report.

“I’m seeing an uptick in first-time buyers looking for starter homes,” Kriese added. “Combine that with concerns about layoffs and a potential recession, and people are doing things like cross-comparing mortgage origination fees, shopping around for lenders and looking into down-payment assistance.”

In terms of percentage, the typical homebuyer today puts down 15 percent of the purchase price, nearly equal to the 15.1 percent they put down at this time last year, Redfin’s report noted. And the median down payment for American homebuyers has hovered around that number for about the last four years, briefly dipping around 10 percent in early 2023. Pre-pandemic, a 10 percent down payment was more frequent.

But dollar-amount down payments have not fallen on an annual basis since the summer of 2023 when home-sales prices were also falling, according to Redfin. During that period, down payments were declining because of falling home prices.

Now, home prices are rising, although they are doing so more slowly. As of April, home prices were up 1.4 percent year over year, compared to the 4 percent they were up by during the same period in 2024.

The reason down payments are falling by dollar amount is because not all homebuyers make a down payment — one-third pay in all cash. And those that are financing a home are most likely buying less expensive homes, which also means a smaller down payment in terms of dollars, but not necessarily percentage terms.

Redfin said that a higher share of homebuyers are also using FHA and VA loans, which allow for smaller down payments, somewhere between 0 percent to 3.5 percent. In April, 15.3 percent of mortgage home sales used an FHA loan, up from 14.2 percent the year before. The share of mortgage home sales using a VA loan was 7.2 percent in April, up from 6.4 percent the year before and the highest April level seen since 2020.

With homebuyer affordability remaining difficult because of roughly 7 percent mortgage rates, many buyers may be purchasing lower-priced homes than they might otherwise. Economic uncertainty in the U.S. right now may also be driving buyers to reserve more of their money in their bank accounts for extenuating circumstances.

Meanwhile, there are now more homesellers than homebuyers in the U.S., tipping the market to favor buyers, which has meant concessions and sellers willing to accept lower down payments. Unfortunately, lower down payments might also be a sign of a buyer with less secure financial standing, and a deal that’s more likely to fall through.

Email Lillian Dickerson

by Lillian Dickerson | Jun 11, 2025 | Industry, News Feed

The new allegation of aggravated sexual abuse by force, threat or intoxicant against Oren and Alon brings the total number of counts against the brothers collectively up to 10.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A third indictment was filed against former luxury brokers Tal and Oren Alexander and their brother, private security executive Alon Alexander, in the federal sex-trafficking case against them on Tuesday, which brings the total number of counts against the brothers up to 10.

The brothers now face one count of conspiracy to commit sex-trafficking; five counts of sex-trafficking by force, fraud or coercion; one count of sex-trafficking of a minor by force, fraud or coercion; two counts of inducement to travel to engage in unlawful sexual activity; and the new count of aggravated sexual abuse by force, threat or intoxicant.

The count added to the superseding indictment alleges that Alon and Oren used force to administer a “drug, intoxicant or other substance” to a seventh female victim who was unaware that she was being intoxicated in order to control her and cause her to engage in sexual acts while “on a Bahamian flagged cruise ship which departed from and arrived in the United States.” The previous indictment against them had identified six victims, one of whom was a minor.

The new indictment further states that as a result of the alleged offenses in the new count against them, Oren and Alon are to forfeit any real and personal property that was used or intended for use to commit the offense, “including but not limited to a sum of money in United States currency representing the amount of proceeds traceable to the commission of said offenses.”

The Alexander brothers were arrested on conspiracy to commit sex trafficking and sex trafficking charges in Miami in December 2024. A superseding indictment submitted by prosecutors in May added six new charges against them.

All three brothers have denied the charges against them.

A lawyer representing Alon told Inman in an emailed statement that, “The government continues to move backwards — the latest charge changes absolutely nothing and is merely a reheated version of the same case in an effort to keep the media firestorm going against the brothers.”

Another lawyer for Alon pointed Inman to a polygraph test that he passed in January while denying had ever had sex with a woman he knew had been given drugs.

Lawyers representing Oren and Tal did not immediately respond to Inman’s request for comment for this story, but after the superseding indictment was filed in May, attorneys for Tal said the new indictment “changes nothing,” and that it was “a reheated version of the same case — and still does not include conduct that amounts to federal sex trafficking.”

At that time, a lawyer for Oren told Inman that, “These new accusations, like the previous ones, are meritless, and reflect a failed prosecutorial effort to salvage a factually and legally unfounded case built on readily disprovable claims.”

Oren and Alon, as well as family friend Ohad Fisherman, also face state rape charges in Florida. Oren has been charged with three counts of sexual battery and Alon and Fisherman have been charged each with one count of sexual battery.

Several civil lawsuits submitted by dozens of women are also outstanding against the Alexander brothers in New York State and elsewhere. The majority of the lawsuits were filed in New York under an extension of a city law that allowed alleged victims of gender-motivated violence to sue their supposed perpetrators, no matter how long ago the alleged act of violence occurred. Victims were allowed to file lawsuits through the end of February 2025.

The brothers are currently being held in Brooklyn’s Metropolitan Detention Center.

Update: This story was updated after publishing with a comment from a lawyer representing Alon Alexander.

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

by Lillian Dickerson | Jun 4, 2025 | Industry, News Feed

The federal law enforcement agency withdrew objections to a fourth proposed settlement between plaintiffs and MLS PIN Tuesday, but cautioned that the MLS was not immune to future legal action.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The U.S. Department of Justice (DOJ) has withdrawn its objection to the settlement between plaintiffs and MLS Property Information Network (PIN) in the homeseller commission lawsuit known as Nosalek, according to a response the DOJ filed in the case on Tuesday.

The move by the government agency follows homeseller plaintiffs and defendant MLS PIN submitting a fourth amended settlement agreement last week, which stipulates that offers of cooperative compensation will be prohibited on MLS PIN’s platform (something other MLSs did in the settlement of commission lawsuit case Sitzer | Burnett) and raises the proposed settlement fund from $3 million to $3.95 million, the same amount it would have cost MLS PIN to join NAR’s settlement in Sitzer | Burnett.

The DOJ’s response specified that it was not taking any position on whether or not the proposed settlement was “fair, reasonable, and adequate” so that the court could approve it without influence from the agency. The DOJ also reiterated that it believes “blanket, upfront offers” of buyer broker compensation from homesellers or their agents are anticompetitive in practice and lead to inflated home prices.

Furthermore, even though the parties reached a proposed settlement, it does not mean that they are shielded from “future enforcement actions” by the government, the filing stated. And, if MLS PIN indeed follows the terms of the settlement, that action in itself would not be a defense, should the government decide to take legal action against the MLS in the future.

“Because the proposed settlement was reached between private litigants in a private class action suit, such settlement does not preclude any future enforcement actions by the United States,” the DOJ’s response said. “Nor would compliance with the proposed settlement or new MLS PIN rules implementing that settlement afford a defense to any such enforcement actions.”

If such a warning by the DOJ is true in the Nosalek case, it may also apply to settlements arranged with parties involved in other commission lawsuit cases with approved settlements — which should keep major industry players on their toes.

A preliminary settlement approval hearing is scheduled for June 10 in Massachusetts federal court.

Other defendants in the Nosalek case, including HomeServices of America, Keller Williams, Anywhere and RE/MAX, have all now been granted final approval of their settlements.

Email Lillian Dickerson

by Lillian Dickerson | Jun 2, 2025 | Industry, News Feed

Rental demand for ultra-luxury properties in the beach market is down as much as 75 percent this year, according to local brokers, due to economic volatility and poor spring weather.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Demand for summer rentals in the Hamptons is down significantly this year as seasonal renters confront the reality of an uncertain economy.

Overall, rental demand is down about 30 percent from the same period in previous years, Judi Desiderio of William Raveis Real Estate told CNBC. Demand is down even further for ultra-luxury properties, according to Hamptons brokers, who say business is down between 50 percent to 75 percent from what is typical for this time of year.

TAKE THE INMAN INTEL SURVEY FOR MAY

“People are holding onto their money,” Enzo Morabito of the Enzo Morabito Team at Douglas Elliman told the news outlet. “They don’t like uncertainty.”

It’s possible that some would-be summer vacationers have also been deterred by gloomy, cold weather in May and are holding out as long as possible to see if forecasts turn around in July or August, brokers said, or are hoping that discounts may pop up later in the season.

But sustained economic uncertainty, largely set off by quickly changing tariff policies and ensuing stock market volatility, is likely one of the biggest factors causing luxury renters and even some buyers to hesitate putting their money into real estate right now, brokers said. The hesitation is a far cry from the relative enthusiasm shown by renters after the 2024 presidential election, as markets responded favorably to the outcome. But since April and the announced tariffs, that early interest has failed to materialize in the form of booked rentals.

Multiple waterfront and other luxury properties that Morabito typically represents as summer rentals remain available for the summer, even though they’re usually booked by March or April, the broker said.

More vacant rentals at this point in the season may turn into deals for renters, however. Already, some luxury rentals have seen price cuts of 10 percent to 20 percent, according to local agents. Some homeowners are also allowing for shorter rental periods than they might have otherwise, including one- or two-week stays.

“I believe this year there was so much ‘dark noise’ out there financially, and geopolitically, and the weather was not conducive to thinking of summertime,” Desiderio told CNBC. “There’s no doubt that by the time July 1 is upon us, all of the rentals will be taken this year.”

Hamptons home sales were also down year over year in the first quarter, though not as dramatically compared to the vacation rental market. Sales were down about 12 percent year over year in Q1 2025, while the median sale price rose 13 percent to $2 million.

The Hamptons market tends to follow Manhattan trends, brokers said, which means a recent two-month boost in luxury sales in the city may be good news for the luxury beach market.

“I just had two Canadians put a bid on an $18 million house, sight unseen,” Morabito confirmed to CNBC. “When Manhattan comes alive, we always follow.”

Get Inman’s Luxury Lens Newsletter delivered right to your inbox. A weekly deep dive into the biggest news in the world of high-end real estate delivered every Friday. Click here to subscribe.

Email Lillian Dickerson

This post was originally published on this site