Ready to step into brokerage leadership or step up your game? Broker Joseph Santini shares characteristics of great brokers to enhance your professional development.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

There are a lot of real estate brokers out there heading up many different models. There are broker-owners, brokers who oversee entire states, brokers who work for large brokerages and brokers who head up one-person companies. I think if a broker really knew what they were getting into prior to taking on this position, they may have thought twice about it, as the challenges are many, and the skills needed to be successful as a real estate broker are more than they appear to be.

Being a broker takes an unusual set of skills, as you have to be entrepreneurial enough to make money but also be able to serve the agents that you lead in a meaningful way. It is not easy to balance these two skill sets, and most people lean one way or the other, which may not be ideal for this position.

So, after doing this for a while and meeting brokers from all over the country, make that the world, I have come up with 10 characteristics that I have observed of great real estate brokers. Should you possess many of these traits, your office will be a success for sure.

How many do you possess, and which ones do you need to work on?

Great brokers are really good at hiring people, both staff and agents. Like sports coaches, they are master recruiters and can consistently bring in new extraordinary talent to their offices. They always surround themselves with the best staff.

They have the ability to keep all the balls in the air at the same time. They achieve consistent growth in all areas. They don’t slack off on one thing to excel in another. That’s why they have a great staff.

They are very eager to learn and get better. You can always find them reading a book or taking a class, even when they ran out of time hours ago. They are always seeking new information that will make them better.

They never stop working. Their brokerage is always top of mind, and they are always in total control of the direction it is taking. The best ones like to be in control, much like a top-producing agent.

They are easily accessible. They are easy to reach and fast to get you what you need. They do not procrastinate.

They are masters in time management. They are generous with time when needed and selfish with it when needed as well. This could be the most important characteristic of all, contributing to their success.

They are master delegators. They delegate everything that they can but watch everything from a distance as well. This gives them the time to do the most important things for the bottom line.

They are passionate about succeeding, and their agents like them. They are good people with good hearts.

They create a positive, productive business environment and structure for their agents to thrive in and find success.

They are master communicators. They keep the information flowing between the office, the staff and their agents. They stay in communication with all their agents all of the time so they can address issues as they come up.

So, there you have it. Like any position, there are certain traits and skills that are conducive to success. Many of these brokers have these characteristics within them naturally, and the best are always striving to get better at the skills that they do not possess.

Being a broker is a challenging job, but also one that you can get great satisfaction from, as you can play a role in the success of many people in many ways. The one thing that comes through very clearly about successful real estate brokers is that they really love what they do.

Joseph Santini is a managing broker at Coldwell Banker Realty in Boca Raton, Florida. Listen to his podcast or connect with him on LinkedIn.

Broker Joseph Santini offers 10 truths about real estate that will put you on the right track and save you some time on your path to success.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Real estate is an interesting business that has some key differences from other businesses. The one thing that stands out the most is the fact that it can be unclear exactly what you should be doing every day to make money and be successful in the real estate business.

Let’s take, for example, a stockbroker. He has a desk and a phone, and it’s very clear what he has to do all day: make calls and sell stocks. Real estate activities are not always clear, and agents often waste a lot of time on activities that don’t lead to a paycheck.

There are so many activities that you can fill up your day with, most of which don’t produce income, and the road to success is not very clear. There are also some misconceptions about the business for those looking in from the outside. In addition, many agents are not getting any direction from anyone, and you have a very reduced chance of succeeding in this business.

Like many occupations that require a license, the material you review to study for the real estate test really does not address the actual things you need to do to succeed in real estate. Hopefully, you will hang your license with a brokerage that will point you in the direction that you need to go and give you some education to find and speed up your path to success.

Read on to discover some myths about real estate, followed by the reality.

1. Myth: Real estate is an easy business and can be done part-time.

Reality: Real estate is one of the most time-intensive businesses in the world. To be successful, you will be very busy even doing it full-time. Anyone can do a deal or two, but real financial success will take time. All of your time.

2. Myth: You work for your broker and the company with which you hang your license.

Reality: You only work for yourself. This is your own business; you’re an entrepreneur, and your brokerage is your partner.

3. Myth: Once you get your license, people will be banging down your door to list their homes and asking you to write contracts for them to buy properties.

Reality: The hardest part of the real estate business is finding customers, especially sellers. The inability to find enough customers is what ends most people’s real estate careers. Nobody will be looking for you.

4. Myth: Your broker and everyone in the office will find you customers.

Reality: The only way to find customers is for you to do lead generation activities effectively on a consistent basis to find them yourself. Nobody is coming to save you and do this for you.

5. Myth: I can work whenever I want, and I will have a lot of time off.

Reality: Since it is your own business, you decide when, where and how much you work, but if you are not putting in a lot of time, usually much more than a regular 9-to-5 job, you won’t make the money that you are expecting.

6. Myth: It takes years and a lot of education to be successful in real estate.

Reality: Years in the business mean nothing. Someone can be in real estate for 10 years and have done 10 transactions, while another person may be two years in with 40 transactions. Anyone can decide to do the work, be effective, and see success rather quickly. Education helps, but you really need to just find people who want to buy and sell real estate. You will learn things on every deal that you do.

7. Myth: It doesn’t cost any money to be a real estate agent.

Reality: Real estate is one of the least expensive businesses to get into where you can make six figures, but like every business, you have to spend money to make money.

8. Myth: You need to know many people to succeed in real estate.

Reality: Knowing a lot of people will make your real estate career much easier, but for those of you who don’t know a lot of people, good lead generation activities will overcome this.

9. Myth: Successful agents can just coast when they get to a certain level of success.

Reality: It sure looks like that, doesn’t it? But in reality, those very successful agents that you see are working harder than most to keep their business where it is. Once they stop working and lead generation, their income will quickly drop to zero.

10. Myth: Real estate is not like other sales jobs, so you don’t have to be a salesperson.

Reality: Real estate is exactly like any other sales job, and it takes the same kind of drive, determination and assertiveness. People who enter the business with prior sales experience have a much better chance of succeeding. People coming from traditional non-sales jobs will have to be ready to learn some new things and be effective at them to succeed.

So, there you have it: 10 truths about real estate that will put you on the right track and save you some time on your path to success. When we know how the business works, we can then focus on what needs to be done.

The great thing about real estate is that anyone can jump in and find success, if they are willing to do the work and be effective.

Joseph Santini is a managing broker at Coldwell Banker Realty in Boca Raton, Florida. Connect with him on LinkedIn.

When I think about building a successful real estate investing (REI) team, I can’t help but draw parallels to my experience in the NFL. I played for nine seasons with four different teams, and during that time, I saw many coaches and players come and go. Everyone brought a slightly different skill set to the field, and together, we formed teams to accomplish some pretty remarkable things.

In many ways, putting together a top-notch REI team is no different from assembling a football team. Both require a clear vision, the right mix of talent, and a strategy to get everyone working together toward a common goal.

Just like in football, everything starts with a vision. As the coach of my REI team, it’s my job to set that vision and define our big goal. In football, that goal might be to win a game, while in real estate, it could be to flip a house for a solid profit.

Whatever the goal, it’s crucial to know exactly what you’re aiming for so you can assemble the right team to get the job done. If I want to flip a house, for example, I need to think about every single team member required to do so successfully. This starts with identifying the key players, much like deciding which positions I need to fill on the field.

For a house flip, my team might include:

Each role is crucial to the success of the project, just like a football team needs a quarterback to lead the offense, receivers to catch the ball, and an offensive line to block and protect.

If I can find all-stars for every role and get everyone on the same page, we’re set up for success. The trick is ensuring everyone works well together and that they’re all aligned with our mission.

Alignment and Incentives: Keeping Your Team on the Same Page

Getting everyone to perform at their best isn’t just about hiring the most talented individuals; it’s about creating alignment. In football, every player on the field knows their role and is motivated by a common goal: winning the game.

It’s the same in real estate investing. Everyone on your team needs to understand the big picture and their part in achieving it. This means aligning incentives so that each team member has a reason to perform well.

In real estate investing, alignment means making sure everyone is not only fairly compensated for their services, but also sees the potential for a long-term relationship and future deals. When people know that delivering exceptional results today could lead to more opportunities tomorrow, they’re naturally more invested in the team’s success.

Think about it: If the quarterback I hire throws a great game, helps us win, and shows leadership on the field, I’ll pay him more, give him more control, and likely offer him a job for many seasons to come.

The same principle applies to your REI team. If a contractor finishes a project ahead of schedule and under budget, or if an agent goes above and beyond to secure a great deal, you’re going to want to keep working with them.

Trust and Communication: The Foundation of Team Success

Trust and communication are the cornerstones of any great team.

In football, trust is built through countless hours of practice and open lines of communication, on and off the field. In real estate, it’s no different. Your team needs to trust that everyone is committed to the same goal and that there’s transparency in all dealings.

You build this trust by fostering an environment where communication flows freely. Make sure everyone feels comfortable sharing ideas, concerns, and updates. Just like a good quarterback has to communicate with his offensive line, you need to make sure your contractor knows exactly what’s expected, or your lender understands the full scope of the deal.

Adaptability and Flexibility: The Ability to Pivot When Necessary

No matter how well you plan, things will go wrong—both in football and real estate. Maybe a property needs more repairs than anticipated, or the market shifts suddenly.

In these moments, the ability to adapt is crucial. The best teams are those that can pivot and adjust their strategy when needed. This is why it’s essential to have team members who are not only experts in their fields, but are also flexible and solution-oriented.

In football, if the defense suddenly switches up their game plan, the offense has to adapt on the fly. The same goes for your REI team. You need people who can think on their feet and come up with creative solutions when the unexpected happens.

Leading Your Team to Victory

At the end of the day, building a successful REI team is all about bringing together the right mix of talent, ensuring everyone is aligned with your vision, fostering open communication, and staying adaptable in the face of challenges. Just like in football, your job as the coach is to set the strategy, put the best players in the right positions, and lead them to victory.

So think of your REI team like a football team: Find your all-stars, align their incentives with your goals, and keep everyone communicating and adapting. Do that, and you’ll be well on your way to a winning season in real estate investing.

Take control of your time and money with advice from an NFL pro.

Stop trading time for money—and let your money work for you—with Real Estate SideHustle, “a game-changer for anyone aiming to achieve financial freedom” (Christopher “Chip” Paucek, Former CEO of 2U and current Co-Founder of Pro Athlete Community).

Note By BiggerPockets: These are opinions written by the author and do not necessarily represent the opinions of BiggerPockets.

Whether it’s refining your business model, mastering new technologies, or discovering strategies to capitalize on the next market surge, Inman Connect New York will prepare you to take bold steps forward. The Next Chapter is about to begin. Be part of it. Join us and thousands of real estate leaders Jan. 22-24, 2025.

Declining mortgage rates and slowing home price appreciation have boosted affordability in many markets and made refinancing a tempting option for 2.5 million homeowners — many of whom are locking rates on refis at levels not seen in more than 2 years.

While that’s good news for mortgage lenders and real estate agents, the latest ICE Mortgage Monitor report from Intercontinental Exchange Inc. also shows the potential for a boom in homebuying and refinancing if mortgage rates keep falling as expected, with the Federal Reserve gearing up this month to shift its stance from fighting inflation to warding off a recession.

Optimal Blue data shows mortgage rates are already down 1.5 percentage points from the post-pandemic high of 7.83 percent registered in October 2023, and affordability is as good as it’s been in six months, ICE’s Andy Walden said.

Andy Walden

“Recent easing in mortgage rates brought some much-sought relief to prospective homebuyers,” Walden said in a statement. “Along with a general cooling in home price growth, rates falling below 6.5 percent made August the most affordable month for housing since February.”

While purchase mortgage demand picked up somewhat, the response has “muted in comparison to early 2023 and 2024 when rates fell to similar levels,” ICE Mortgage reported.

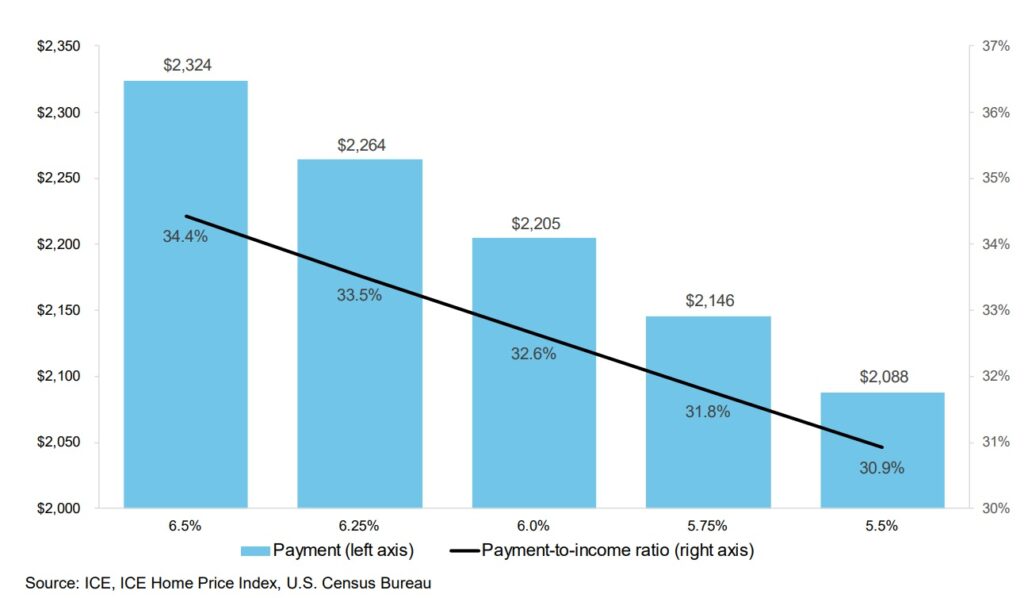

How falling mortgage rates could affect affordability

Monthly payment on average-priced home as percentage of income. Scenarios assume home prices and income hold steady as mortgage rates fall, and that buyers make a 20 percent down payment to finance their purchase with a 30-year fixed rate mortgage.

With mortgage rates at 6.5 percent, buying the average home still requires 34 percent of median income — about 10 percentage points higher than the historical average, Walden noted.

Each quarter point mortgage rate reduction reduces the mortgage payment required to purchase the average-priced home by around $60.

So if rates come down another percentage point, to 5.5 percent, payment-to-income ratio drops to 31 percent and homebuyers would be looking at a monthly payment of $2,088 instead of $2,324.

While forecasters at Fannie Mae and the Mortgage Bankers Association expect rates will continue to come down, they don’t anticipate rates on 30-year fixed-rate loans to dip below 6 percent until Q4 2025.

Mortgage rates are only part of the affordability problem. While home prices soared during the pandemic, they are now decelerating and even coming back down in some Sunbelt markets where inventories are growing.

Growing inventory and continuing soft demand slowed annual home price appreciation to 3.6 percent in July, down from 4.1 percent in June, ICE Mortgage estimates.

Looking at the nation’s 100 largest markets, ICE Mortgage sees affordability remaining a challenge in more than half, with the median income needed to make monthly mortgage payments still elevated by 10 percentage points from historical averages.

By that measure (payment-to-income ratio), affordability has returned to historical trendline in seven markets: Birmingham, Alabama; Des Moines, Iowa; McAllen, Texas; Cleveland and Toledo, Ohio; Memphis, Tennessee; and Baton Rouge, Louisiana.

Payment-to-income ratios are within 5 percentage points of historical averages in 22 other markets, ICE Mortgage estimates.

But elevated down payment and tight credit requirements may also be contributing to muted demand, the report warned.

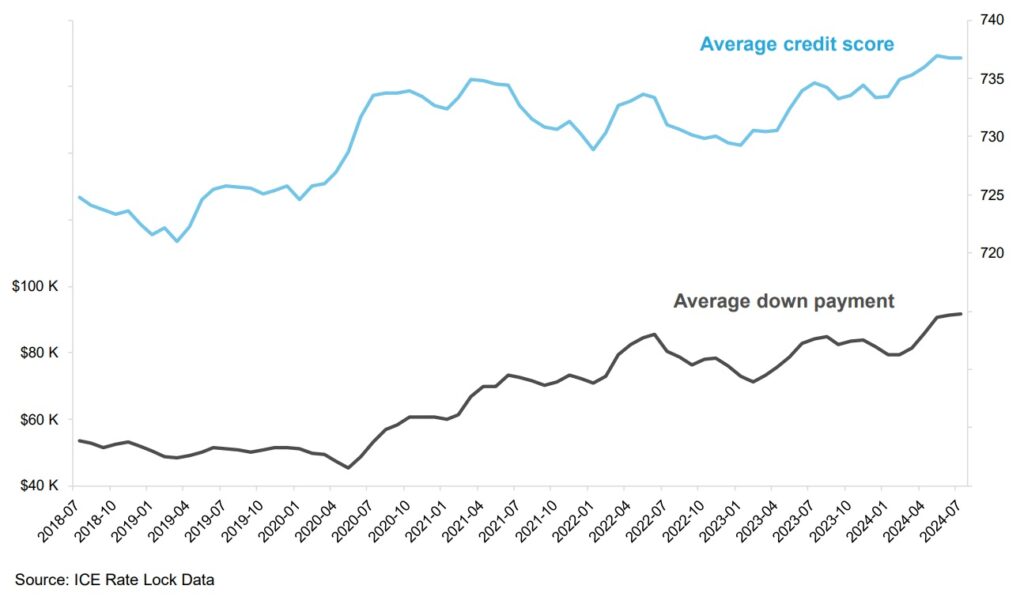

Homebuyers making record down payments

Homebuyers have better credit scores and are making bigger down payments than before the pandemic.

Homebuyers financing their purchases made down payments averaging $91,600 in July, a new record high. That’s up 9 percent from a year ago and 79 percent from July 2019 — the summer before the pandemic, when down payments averaged $51,100.

Would-be homebuyers are also facing tight lending requirements, with the average credit score for borrowers taking out purchase loans hitting a record 737 in May, according to ICE Market Trends data.

While homebuyers would welcome lower mortgage rates, they would also benefit recent homebuyers who took out loans when rates were higher.

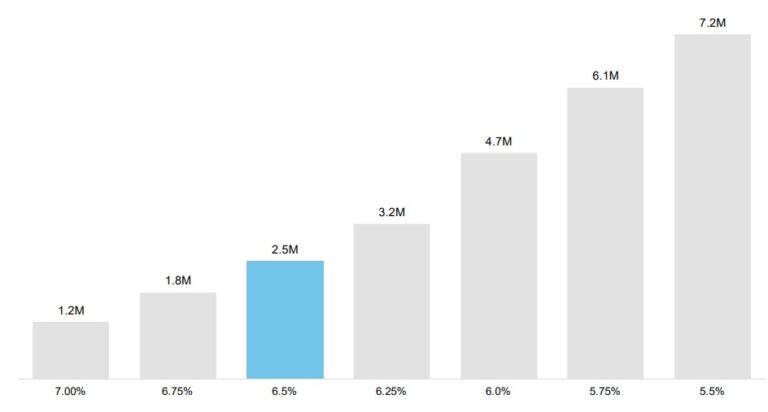

As of Aug. 22, 2.5 million homeowners were “in the money” for a refinance, meaning they could save money by refinancing at a lower rate.

Among that group, more than 60 percent took out their mortgages in the past two years, including 850,000 in 2023 and 560,000 this year. ICE Mortgage calculates that “highly qualified” candidates with credit scores of 720 or higher and at least 20 percent equity in their homes could save $264 a month by refinancing into a new loan that shaves at least 75 basis points off their current rate.

If rates fell by a full percentage point to 5.5 percent, nearly 7.2 million homeowners would be “in the money” for a refinance, and 2.7 million of those would be considered highly qualified, ICE Mortgage estimates.

If rates fell that far, two-thirds of mortgages originated in 2023 and more than 80 percent of loans taken out in 2024 would be in the money for a refinance.

That’s a potential headache for loan servicers who collect monthly mortgage payments for investors, who don’t want their mortgage servicing rights (MSR) portfolios shrink as clients refinance with another lender.

Loan servicers retained only one in five borrowers who refinanced during Q2 2024, down from 25 percent in Q1 and the second lowest retention rate in more than 17 years.

Servicers were “particularly successful in retaining refinancing borrowers who’d recently obtained their loans,” with retention as high as 41 percent among 2023 and 34 percent among 2022 vintage loans, ICE Mortgage noted.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Take a new, unconventional approach to one-on-ones that emphasizes the needs, preferences and goals of your agents, luxury consultant Chris Pollinger writes.

Whether it’s refining your business model, mastering new technologies, or discovering strategies to capitalize on the next market surge, Inman Connect New York will prepare you to take bold steps forward. The Next Chapter is about to begin. Be part of it. Join us and thousands of real estate leaders Jan. 22-24, 2025.

In real estate, where top talent operates independently, managing relationships with independent associates is an art form. Unlike traditional employees, these professionals bring unique motivations, work styles and expectations to the table. The conventional management playbook simply doesn’t apply.

So, how do you ensure that your one-on-one meetings with associates are not just productive but also foster a thriving partnership? Let’s explore some strategies that can make a real difference.

1. Tailor one-on-ones to independent contractor dynamics

First off, let’s throw out the idea that your associates are just like employees. They’re not. Independent associates have different motivations — be it financial freedom, control over their time or the ability to work how and when they want.

Your job is to align their goals with your business objectives, but without the heavy-handed oversight that comes with a traditional boss-employee relationship.

Make your one-on-ones more about collaboration and partnership. Approach these meetings with a mindset that you’re working alongside them, not above them. It’s about finding common ground where their aspirations and your business goals intersect.

2. Shift focus from performance to project management mindset

Let’s be real: Traditional performance reviews are a relic of the corporate world that don’t resonate with independent associates. What matters to them isn’t how well they conform to your processes but how effectively they deliver on driving more transactions.

Instead of approaching things from a performance review mindset, switch gears to a project-based approach. Discuss milestones, immediate goals and how their work ties into the broader vision. This project-focused approach not only respects their independence but also keeps everyone aligned and moving forward.

3. Understand their motivations

If you don’t know what drives your associates, you’re flying blind.

Is it the money?

The flexibility?

The chance to grow their own brand?

Start every relationship by digging into what makes them tick. When you understand their motivations, you can tailor your one-on-one conversations to make sure you’re not just meeting your business needs, but also fulfilling their personal and professional goals. This understanding creates a win-win scenario that’s hard to beat.

4. It’s about them, not you

One-on-ones are not your soapbox. They’re a platform to dig into what your associates need to succeed. Use this time to listen more than you speak.

What challenges are they facing? What support do they need? By focusing on their needs and challenges, you build trust and make them feel valued. And when people feel valued, they perform better. It’s that simple. This shift in focus can transform a transactional relationship into a true partnership.

5. Prioritize professional development

Independent associates thrive on opportunities for growth. Whether it’s expanding their skill set or growing their client base, they’re always looking for ways to level up. Use your one-on-ones to discuss opportunities for professional development or introduce them to networking events in your industry (like Inman Connect). Not only does this benefit them, but it also strengthens your relationship. You become more than just a boss or mentor — you become a key player in their growth story.

6. Manage people according to their strengths, core values and personality

One-size-fits-all management is a myth. Each of your associates has unique strengths, core values and personality traits that make them tick. Your job is to tailor your management style to fit them, not the other way around.

Use your one-on-ones to explore these aspects and adjust your approach accordingly. This personalized management can maximize their effectiveness and satisfaction, making them more likely to stick around and do great work.

7. Create a culture of transparent accountability

Accountability isn’t a one-way street. In your one-on-ones, don’t just focus on what your associates are doing; invite them to critique your processes and the partnership.

This two-way feedback can improve collaboration and make your associates feel like they have a stake in the game. When they feel heard and valued, they’re more likely to stay committed and deliver real results.

8. Emphasize flexibility and mutual respect

Remember that associates are not bound by the same rules as employees. Flexibility is key. Be open to adjusting meeting times or formats to suit their schedules. This shows that you respect their autonomy and value their contribution. Flexibility isn’t just about logistics; it’s about creating a working relationship built on mutual respect and understanding.

Bonus super secret: Encourage peer collaboration

To accelerate results, foster collaboration among your associates. Your associates aren’t just islands working in isolation — they’re part of your team.

Encourage them to share knowledge, resources or even co-manage projects. This can lead to more innovative solutions and a stronger sense of community within your team. Peer collaboration isn’t just good for morale; it’s also a smart business strategy that can drive better results.

In the end, managing independent associates is all about adapting to their unique dynamics and creating a partnership that benefits both parties. By focusing on collaboration, project management, understanding their motivations and offering flexibility, you can build strong, effective relationships that drive success.

Forget the old playbook — it’s time to embrace a new, unconventional approach to one-on-ones that puts your associates, and ultimately your business, in the best possible position to thrive.

Chris Pollinger, founder and managing partner of RE Luxe Leaders, is the strategic advisor to the elite in the business of luxury real estate. He is an advisor, national speaker, consultant and leadership coach. Learn more about their consulting, coaching and advisory programs at RELuxeLeaders.com