Join the movement at Inman Connect Las Vegas, July 30 – Aug. 1! Seize the moment to take charge of the next era in real estate. Through immersive experiences, innovative formats and an unparalleled lineup of speakers, this gathering becomes more than a conference — it becomes a collaborative force shaping the future of our industry. Secure your tickets now! Learn more.

As a valued member of the Inman community, we invite you to participate in the real estate industry’s most ambitious new monthly survey: the Inman Intel Index.

Each month, the Inman Intel Index survey takes the pulse of Inman’s readership to discover what’s top of mind for agents, mortgage professionals, proptech players and industry executives.

Please take a moment today to fill out the March survey. Most respondents complete it in under four minutes, and Inman will release the results in the coming weeks.

The insights gathered from your responses and your peers nationwide help illuminate industry sentiment on real estate’s most important topics. From the most recent lawsuit settlement and business development trends to AI and recruiting, the Inman Intel Index asks the most important questions every month.

Click through to add your answers to the March survey, and check back for analysis next month.

Most agents say they’ve heard from competitor brokerages in recent weeks. Intel explores what’s on their mind as they decide whether to stay — or bolt.

This report is available exclusively to subscribers of Inman Intel, the data and research arm of Inman offering deep insights and market intelligence on the business of residential real estate and proptech. Subscribe today.

The number of real estate agents is on a downward trend, and will likely decline further as market forces and industry shifts push newcomers and veterans alike to the brink.

Most brokerages, meanwhile, seem actively intent on growing their ranks with those who stay in the game.

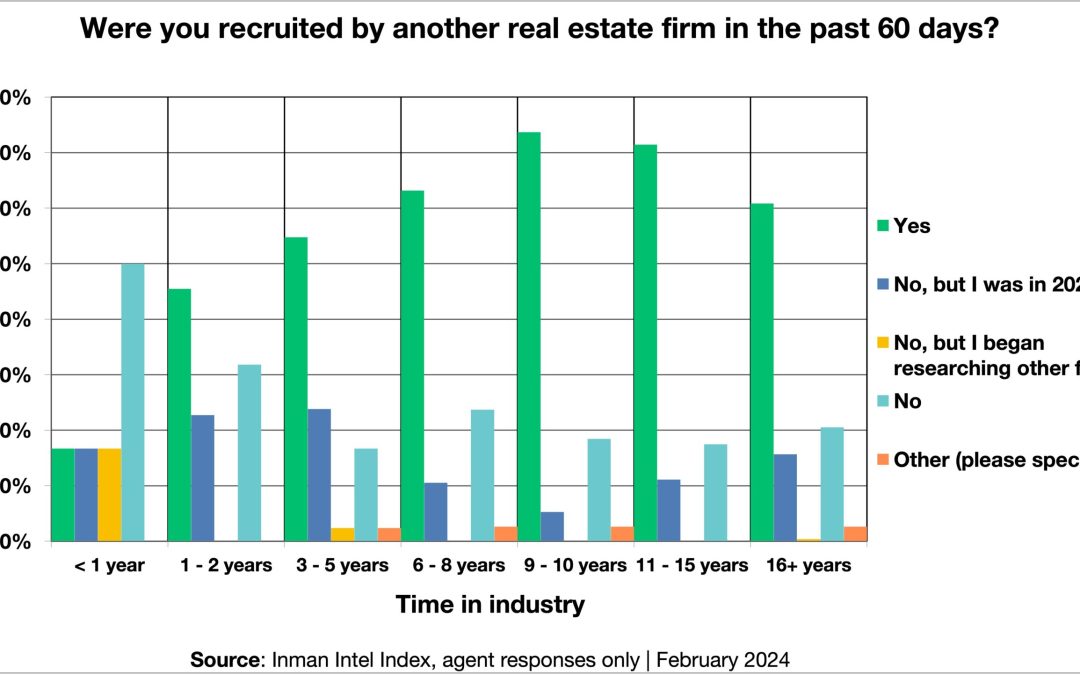

According to the latest Inman Intel Index industry survey, 6 out of 10 agent respondents said they were recruited by a competitor in the first 60 days of 2024. That same share rises to more than three-quarters of real estate agents when you look back to the start of last year.

While respondents alluded to how the constant recruitment push is an industry norm, at least in their experience, others indicated the pace is increasing.

Here is a sample of anonymous quotes from those who answered the question in February’s survey, which included 563 real estate agents among the 811 total respondents:

Recruitment efforts generally grew in tandem with tenure, track record, experience navigating previous downturns and industry knowledge.

The survey did show a pronounced drop in 2024 recruitment for the longest-tenured agents, a group that was nonetheless in line with other veteran agent cohorts going back 14 months.

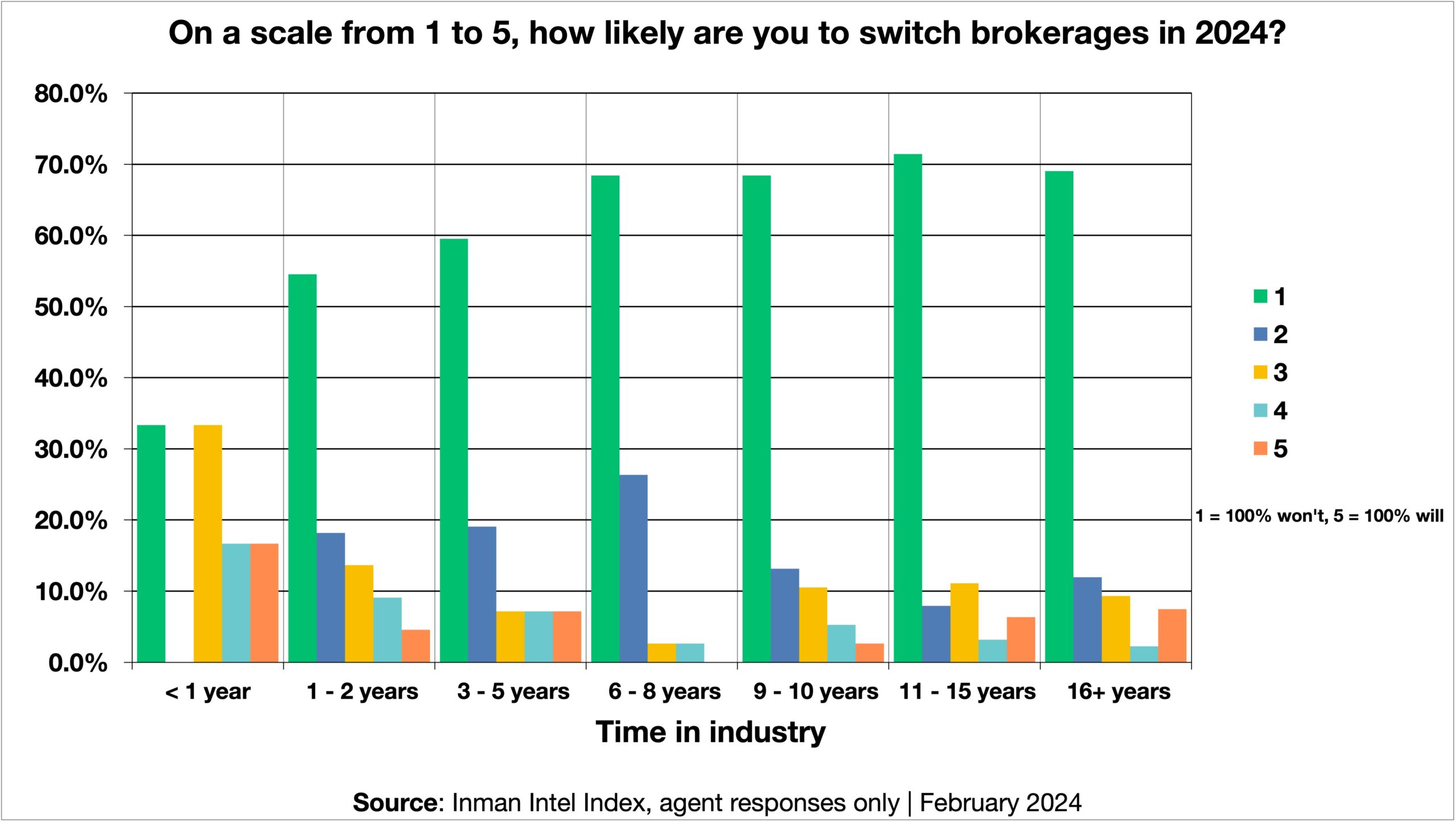

The share of agents who said they are likely to change brokerages in 2024 doubled month over month and is now approaching 10 percent. For broker-owners focused on the other side of this coin—retention—the Intel Index survey revealed emerging trends there, too.

Outside of the agents with less than one year in the industry, at least 55 percent of every other group ruled out a company change entirely. Conversely, no group outside of the newest agents had greater than 7.5 percent say they were 100 percent certain they were switching brokerages.

One segment of agents that stands out and may be of particular interest to those on offense and defense is the group with 1-2 years of industry experience.

While a slight majority sat on the most steadfast end of the scale, over one-quarter marked their likelihood of switching brokerages as a 3 or higher. This is the highest concentration among the tenure brackets.

Among those who have joined in the past 24 months, nearly one-third of respondents said that a “Better culture fit” would be their top motivator to switch.

Another 18 percent chose “Better commission/compensation structure.”

14 percent said improved consumer perception and recognition of the new brand would make the difference.

Also notable among a group that has only really experienced a housing downturn is it had the highest number of respondents who had changed brokerages in 2023.

The reasons behind their moves largely sync with what this same group said about their drivers for potentially changing this year, with a change of culture and better commission/compensation coming in first and second, respectively. “Better technology and training” also registered with some of those who relocated.

The Intel Index has seen an uptick in agents acknowledging a brokerage move last year, with February the second consecutive month with over 10 percent of agents saying they changed companies.

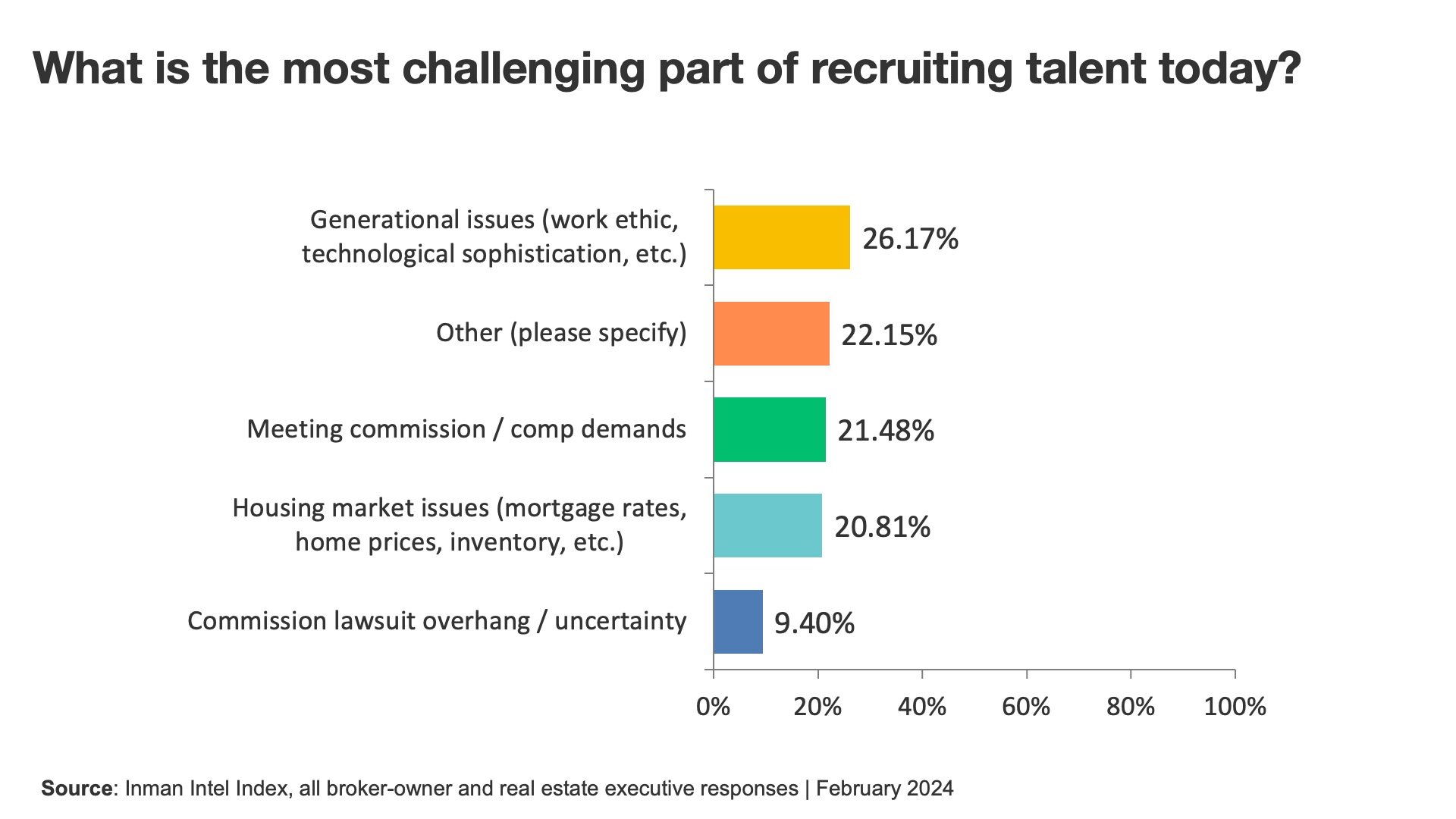

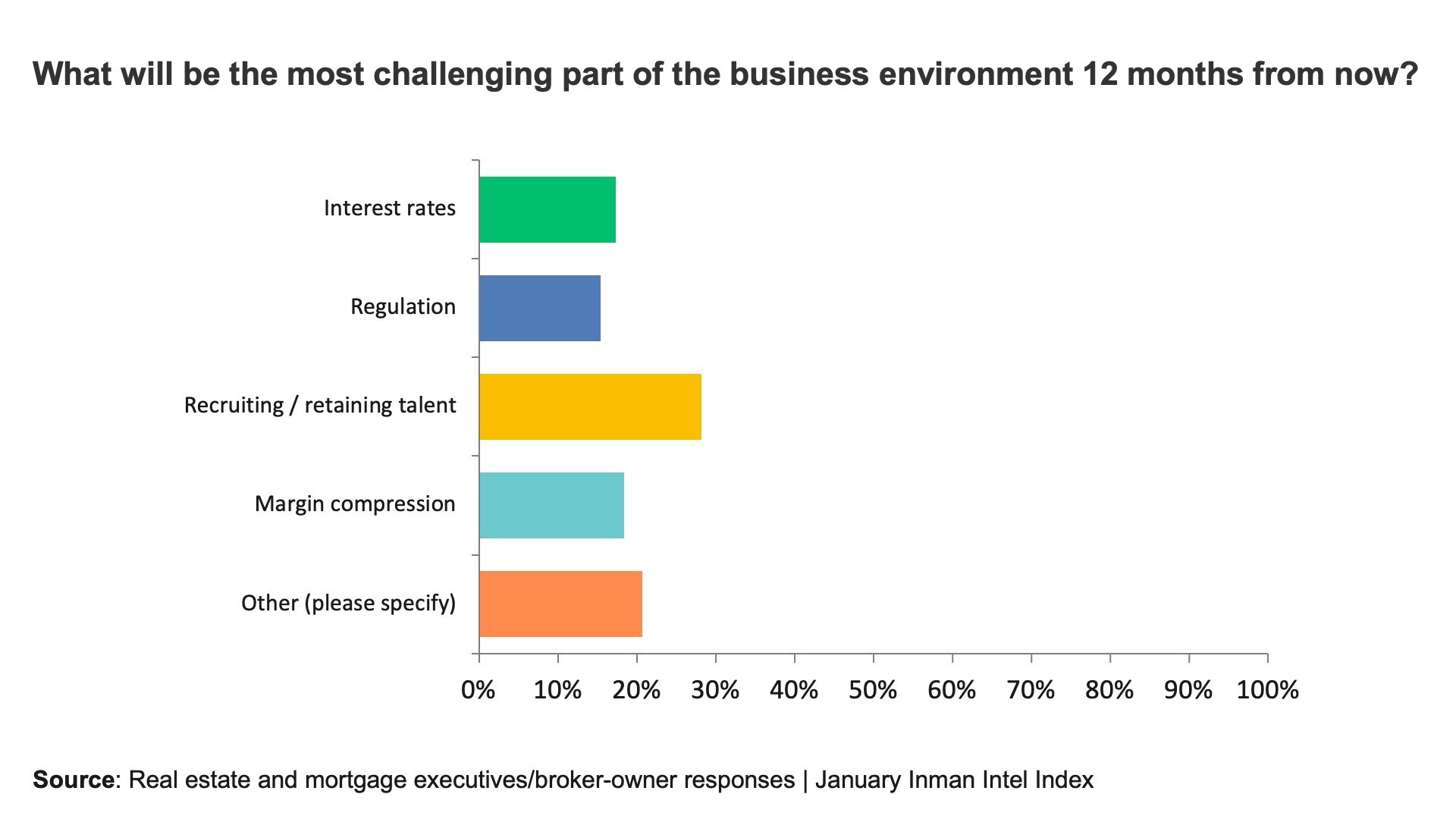

For broker-owners, recruiting and retention ranks well below their biggest business concern of the day. Nearly 30 percent said interest rates worry them most, a full 10 percentage points higher than keeping their talent or unearthing new stars.

But when asked specifically about recruiting talent, a plurality of owners and executives pointed to generational issues as the biggest pain point. Their answer choice pointed them toward issues that may confront them with younger and older agents, such as work ethic and technological sophistication.

Intel will explore these insights and more in April in a deeply reported series on the topic of recruiting. The series will be based on new, even more detailed questions that will be part of the March survey, as well as conversations with experts in the field.

Methodology notes: This month’s Inman Intel Index survey was conducted Feb. 20-March 3, 2024. The entire Inman reader community was invited to participate, and Intel received 811 responses. Respondents for this survey were directed to the SurveyMonkey platform, where they self-identified their profiles within the residential real estate market. Respondents were limited to one response per device, but there was no limitation to IP addresses. Once a profile (residential real estate agent, mortgage broker/banker, corporate executive/investor/proptech, or other) was selected, respondents answered a unique set of questions for that specific profile. Because the survey did not request demographic information for age, gender or geography, there was no data weighting. This survey will be conducted monthly, with both recurring and unique questions for each profile type.

This report is available exclusively to subscribers of Inman Intel, the data and research arm of Inman offering deep insights and market intelligence on the business of residential real estate and proptech. Subscribe today.

One of the most widely cited measures of U.S. home prices has come under fire in recent weeks after an upstart firm’s critique ignited a broader discussion on what data concepts the industry should track — and how.

A public post in late January by Parcl Labs captured the imagination of real estate data insiders when it called into question the S&P CoreLogic Case-Shiller Index, a monthly price tracker considered by many to be a go-to source for home price trends.

It’s not the first time such a widely referenced industry measuring stick has been scrutinized, and it won’t be the last.

To understand these arguments, Intel examines what Case-Shiller and similar models attempt to accomplish, how to interpret them, and what blind spots other data providers are increasingly jockeying to fill in.

Read more in the full report below.

Origin of a ‘gold standard’

For decades, real estate professionals have acknowledged many problems with simply tracking raw home prices.

One of the biggest issues? The group of homes that sell in one year might not look like the homes that sell in the next period. A sudden mortgage rate surge, for example, might drive more buyers to a lower price tier, without exerting as much downward pressure on home prices within the same tier.

That’s one of the problems that the Case-Shiller index was designed to solve.

Economists Karl Case, Robert Shiller, and Allan Weiss formulated this index in the late 1980s. It is based on the concept of “repeat sales.” Instead of tracking the prices of houses sold in a period, the index tracks the prices of individual houses over time.

It’s far from the only measure set up this way. The Loan Performance Home Price Index, another CoreLogic data series, uses the repeat-sales pricing technique, as does the Federal Housing Finance Agency House Price Index.

In a blog post discussing the relationship between appraisal values and home price movements, FHFA’s Justin Contat and Daniel Lane wrote, “The repeat-sales index is the industry gold standard since it is ‘constant-quality’ and suffers less than mean or median values from sampling differences.”

Case-Shiller’s National Home Price Index is more than a simple up-and-down gauge; over time, it has become a benchmark for both housing and the nation’s broader economy. The index, and its subset of multiple major metro areas, is a key tool used by policymakers and investors in their decisions.

While many point out one of its potential drawbacks — a two-month lag in the data — they also generally point to another time-based element for its popularity. A multi-decade time series with a rigorously tested methodology doesn’t come along every day.

“What Case and Shiller put together is really the gold standard for price changes in the housing market,” Edward Glaeser, a professor of economics at Harvard University, said in an interview for The New York Times obituary of Karl Case. “It has the beauty of being both transparent and reliable.”

Taking a swing at the king

On the last Tuesday of February, as on every month dating back years, the S&P CoreLogic Case-Shiller Indices were released. And like clockwork, they generated headlines seconds later.

But it was another headline, published a few weeks earlier, that made a splash in data and research circles when it called into question decades of accepted price-monitoring standards.

This bold-faced shot across the standard bearer’s bow came from a January article by Parcl Labs, one of a growing number of data providers that are challenging the institutional order that sets its clock to indicators like the Case-Shiller release.

A spokesperson for S&P Global declined to respond in detail to a request for comment on the post, directing Intel instead to the Case-Shiller methodology page.

Parcl Labs, riding a pandemic-era digital real estate mentality shift, offers investors the opportunity to bet on markets rather than physical property. It focuses on determining daily value and trend action. In doing so, Parcl argues it adds a novel layer of information in real estate pricing and analytics.

Parcl’s article, penned by co-founder Jason Lewris and Vice President of Strategy Lucy Ferguson, argued Case-Shiller “lacks utility for the modern housing market.”

Their list of issues with Case-Shiller was long and included the following:

Backward-looking data that is two months old. In recent years, more data providers have moved toward offering customers daily updating reports instead of quarterly or monthly ones. Parcl’s post argues that this trend leaves Case-Shiller — which releases with a two-month delay — further behind the curve than ever.

Utilizing only single-family repeat sales, but not even all of them, to measure home value change. In addition to excluding new construction homes, co-ops, and condominiums, the Case-Shiller methodology also negates any trades that occur within six months of one another. A study by Parcl in 2022 asserted that, due to these exclusions, the Case-Shiller 10-City Composite Home Price Index left out 42 percent of sales in the 10 largest metropolitan statistical areas.

Discounting older or low-turnover homes by the better part of 50 percent in some cases. While Case-Shiller does not necessarily exclude older homes or ones with significant gaps between sales, methodology weighting adjustments greatly alter their impact. Parcl concluded that, due to what is trading in San Francisco of late, most sales within that metro area’s index are being discounted and some as much as 45 percent.

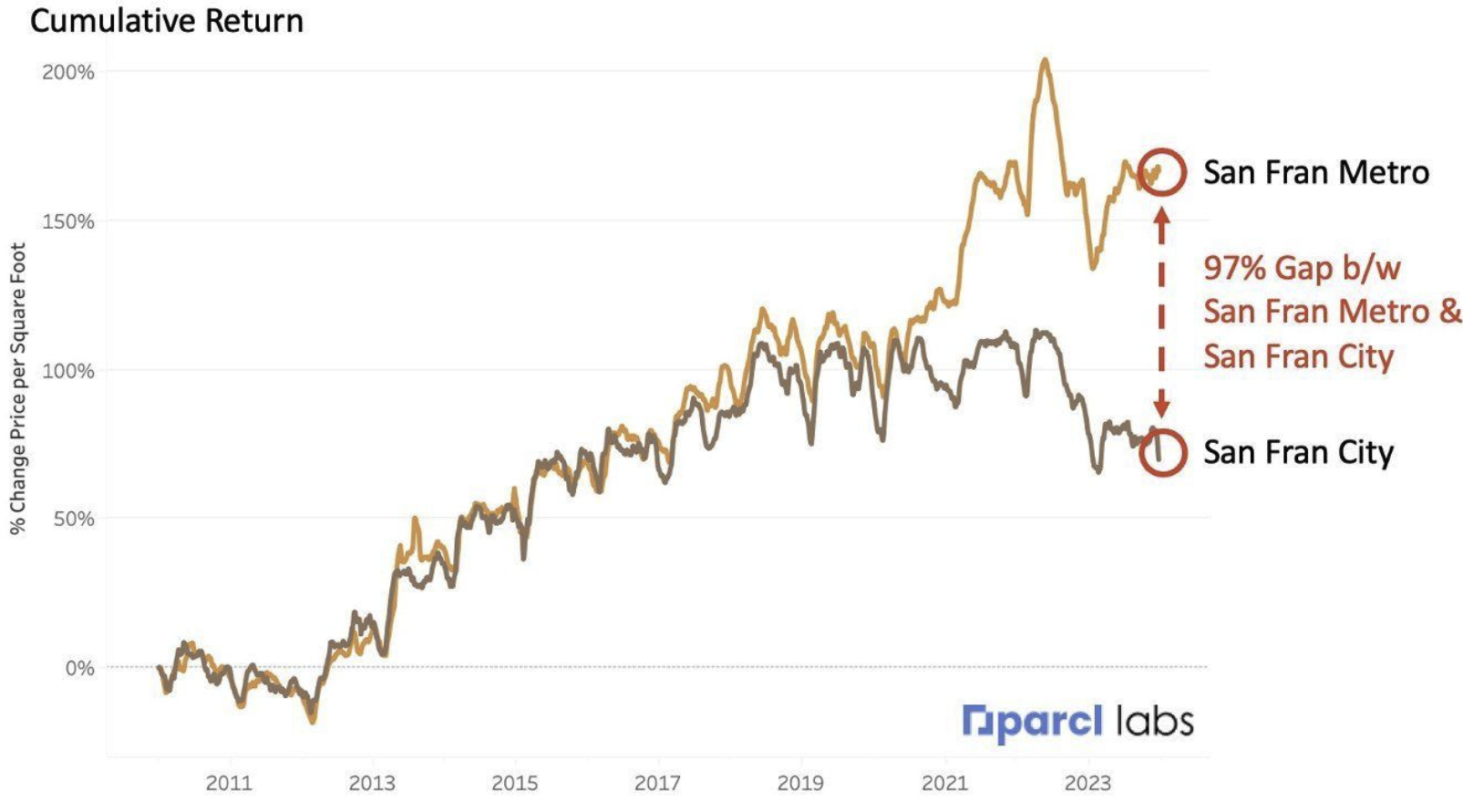

Using MSA boundaries in its 10- and 20-metro area indices paints with too broad a brush. People live in New York City, or Boston, or Chicago, but just like any other real estate, supply, demand, and value are localized dynamics. The following chart, for example, illustrates the performance delta between metro San Francisco and the city proper.

Chart by Parcl Labs

A single source of truth?

While believing Case-Shiller is an imperfect data source, Lewris still sees some utility in it for now: Namely, in helping the Parcl Labs team get smarter and understand specific market conditions or how most adherents use it.

Lewris wrote in a recent blog post that the Parcl team attempted to reconstruct the Case-Shiller methodology as best it could to help “predict” how it would behave in more recent weeks.

“This report gives us insight into how markets are evolving for single-family, repeated sales homes that fall outside the definition of home flipping,” Lewris wrote.

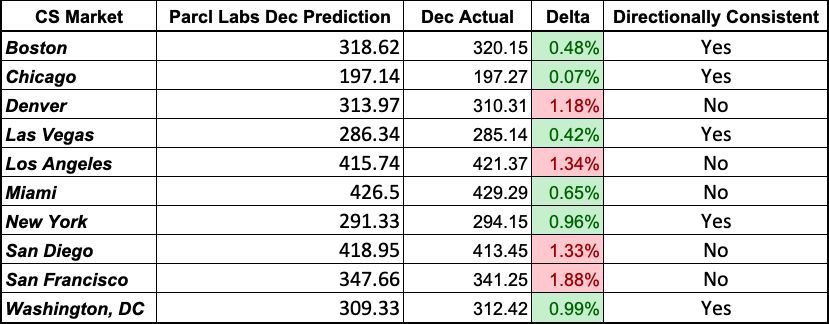

Each time the Case-Shiller is released, Parcl provides a post-mortem on how close it was to predicting the results. December’s was largely on par with most months, with Parcl’s estimates generally very close, even if they were off directionally.

Ultimately, though, Parcl Labs has about as bold a goal as any information provider in any industry: Its stated mission is to create a new global standard for residential real estate pricing and analytics, largely by creating a single source for home valuation.

This idea is both elegant in concept and daunting in practice. Instead of having multiple systems servers and access points, the idea is to create one system that integrates, interrogates, aggregates and disseminates data. Neither the concept nor the chase to produce such a data reservoir is new, and whether Parcl — or another upstart data provider — will persuade the industry it has cracked the code remains to be seen.

However, some experts believe having different sources that competently and efficiently offer different data products has worked well for decades. If something isn’t broken, they argue, there’s no need to fix it.

“We use the FHFA series, which is a repeat-sale model, and we like it. But Case-Shiller is proven, and I don’t think it’s broken,” said Ali Wolf, chief economist for Zonda. “Parcl is doing something new and different, and there’s a value to their data. But it doesn’t make Case-Shiller wrong or irrelevant.”

This report is available exclusively to subscribers of Inman Intel, the data and research arm of Inman offering deep insights and market intelligence on the business of residential real estate and proptech. Subscribe today.

Real estate and mortgage leaders wake up to challenges daily — often the same ones, over and over, in a Groundhog Day cycle of low inventory, high mortgage rates and, more recently, lawsuits threatening to upend old practices.

Wash, rinse, repeat.

But long-haul leaders have their eyes on the horizon, too, and new data suggest a future concern is growing out of today’s tumult.

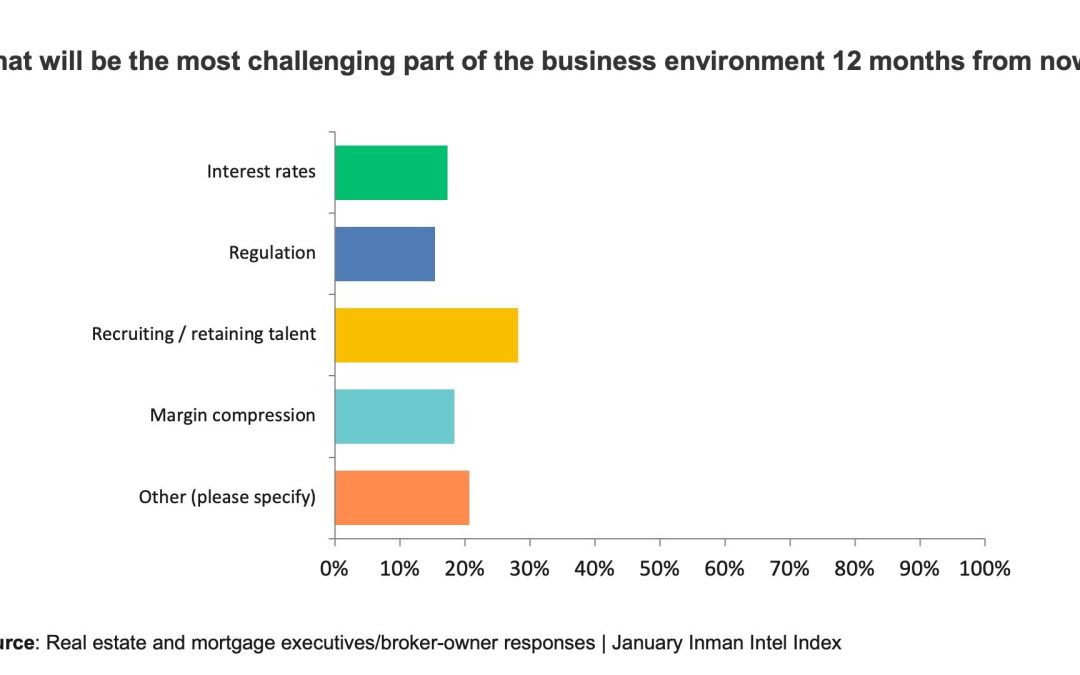

Approximately28 percent of brokerage leaders who responded to January’s Inman Intel Index predict “recruiting and retaining talent” will be the most challenging part of their business one year from now.

That mark was the highest measured by the Inman Intel Index, also known as the Triple-I, since this flagship survey was unveiled in September. The same response choice had not previously cracked 24 percent. January was also the first time “recruiting and retaining talent” led all concerns as brokerage leaders look to the year ahead.

For this reason, Intel is planning a deeply reported series on the topic of recruiting in the weeks to come. The series — which will run in early April — will be based on detailed questions that will be part of the March Triple-I and conversations with experts in the field.

But in the meantime, read the full report below to learn why so many real estate leaders see recruiting as a matter of such pivotal importance in the year to come.

One potentially cuts both ways: Housing headwinds keep shrinking the ranks of both agents and loan officers. Company owners are metaphorically defending the home front while having less talent to target outside their walls.

This is because, to some degree, the departures in both industries aren’t just rookies or poor fits. Several corporate leaders have discussed strong producers who did not have the wherewithal to ride out a generational downturn. This is the scenario that Compass CEO Robert Reffkin gave voice to in an interview with Brad Inman last month.

“Last year, I’ve never seen so many top agents question whether they should leave the business,” Reffkin said.

The National Association of Realtors is bracing for what could be its largest one-year membership drop ever, which would come on the heels of its first year-over-year decline since 2012. NAR Chief Economist Lawrence Yun highlighted in his most recent membership analysis that, despite a slower outflow than some expected, losses are far from over.

“Most state and local associations should anticipate further declines in membership over the next 24 months based on the lag effects of past housing cycles,” Yun wrote.

Some of the nation’s biggest brokerages acknowledged losses in their recent earnings call presentations.

EXp’s year-end agent count was also down 1.8 percent compared to the previous quarter, according to founder and CEO Glenn Sanford. During his investor call, Sanford said that Q4 was the “first time in history our agent count has declined quarter over quarter” — though he added that agent attrition appears mostly isolated among the least productive agents.

RE/MAX’s total agent count fell 6.1 percent in the United States last year and has continued falling at the start of this year, according to corporate spokespeople. Worldwide, it now counts 143,497 agents, the company said.

The fight to hold onto producers isn’t relegated to the real estate brokerage world, either. The mortgage world has been decimated by an extended period of high rates and lower home sales.

It isn’t 2007 and 2008 for mortgage originators, but approximately 50,000 nonbank mortgage brokers and bankers fell off payrolls in 2023, and layoff announcements haven’t slowed in 2024.

Consider just some of the headlines from the mortgage world in the first two months of the year:

Leveling up

On the other side of the spectrum, some real estate and mortgage brokerage firms are staffed with relative newbies who joined in the veritable gold rush created by the COVID-19 homebuying frenzy.

They thrived when mortgage money was all but free and inventory was looser, and maybe even began to establish themselves on social media as influencer.

But TikTok only goes so far when interest rates rise at the fastest pace in 40 years, or U.S. home sales were the fewest since 1995.

Some of the 22 percent of survey respondents who said “recruiting and retaining talent” was the hardest part of the present business environment cut to the quick on the topic.

Preparing for opportunity

At some point, when inventory replenishes, mortgage rates fall (enough), and household formation demand factors collide, the housing market will hit another upcycle.

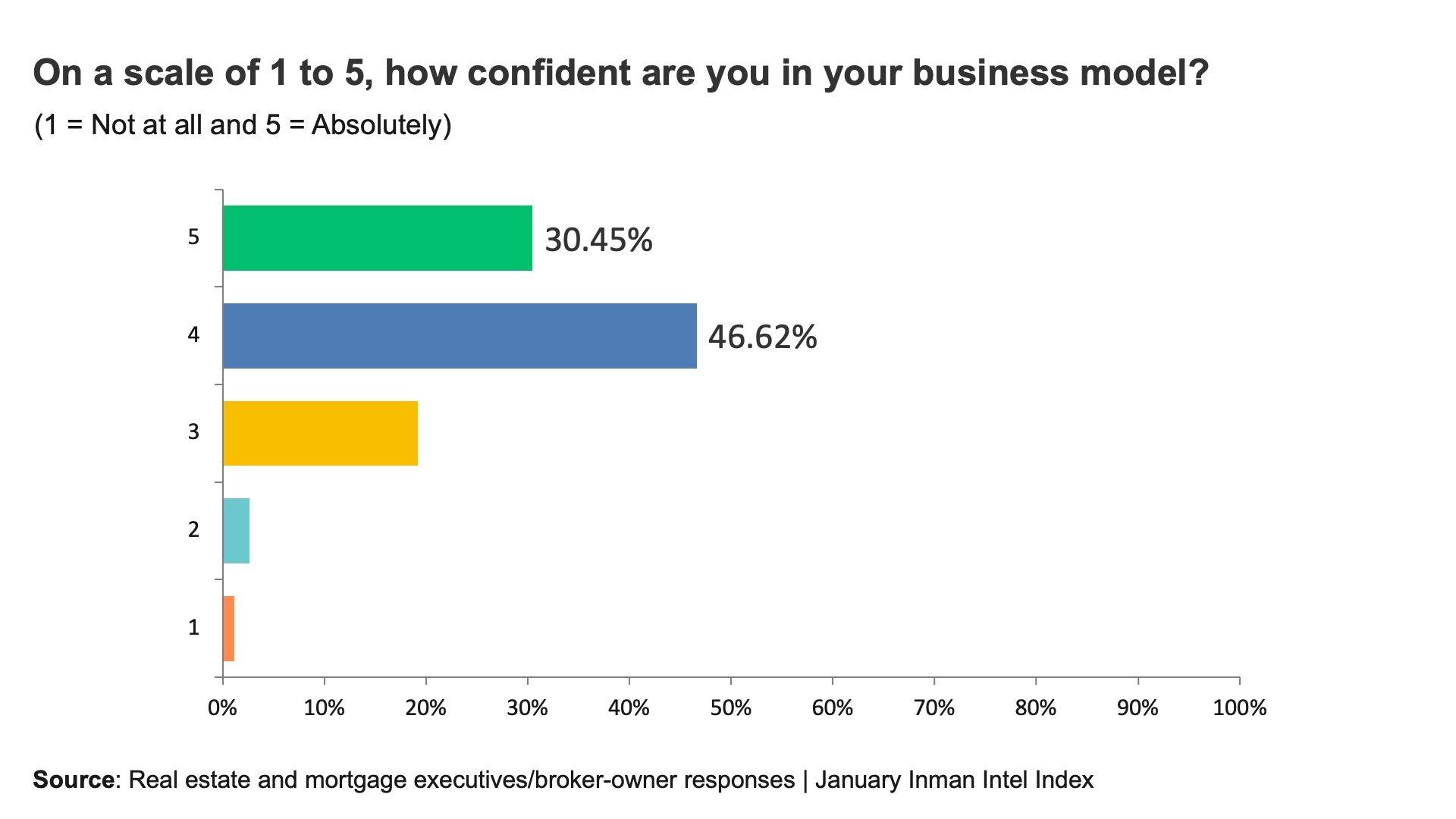

According to the January Triple-I, more than three-quarters of real estate and mortgage executives rated their confidence in their business model at a 4 or higher on a 5-point scale.

So it stands to reason that the survivors, the ones with a proven business plan, an inviting culture, and requisite technology, will be positioned to snatch market share from their rivals by winning the talent arms race.

Mortgage companies are in the thick of it now. Still, they will need underwriters, loan officers, secondary market specialists, support staff, marketing personnel, and more when the spigots turn back on. The worst position a mortgage company can be in following a downturn is being unable to deliver quality service and efficient underwriting and pre-approval for their clients and real estate referral partners.

For real estate brokerages, there there is likely to be fewer competitors 12 months from today. What is less certain, among many things, is what buyers agents will get paid and by whom. One piece of the recruitment pitch, then, could be having a clear pitch for the agent who may not feel they’re getting transparency or answers from their current brokerage.

One survey taker offered a take on today’s challenges that falls roughly in line with what others believe are the challenges coming down the pike.

“The lack of education most brokers provide their agents. They are so concerned about paying the highest splits, they can’t afford management to train and hold them accountable. The old mom and pop method is being replaced with I pay you top dollar stay up to speed on your own. In turn an agent doesn’t have a value proposition and commissions are dropping. No one is addressing this.”

Keep an eye out in early April for Intel’s full series on recruiting, where these questions will be explored in even greater detail.

Methodology notes: This month’s Inman Intel Index survey was conducted Jan. 21-31, 2024. The entire Inman reader community was invited to participate, and Intel received a total of 1,029 responses. Respondents for this survey were directed to the SurveyMonkey platform, where they self-identified their profiles within the residential real estate market. Respondents were limited to one response per device, but there was no limitation to IP addresses. Once a profile (residential real estate agent, mortgage broker/banker, corporate executive/investor/proptech, or other) was selected, respondents answered a unique set of questions for that specific profile. Because the survey did not request demographic information for age, gender, or geography, there was no data weighting. This survey will be conducted monthly, with both recurring and unique questions for each profile type.

Mark your calendars for the ultimate real estate experiences with Inman’s upcoming events! Dive into the future at Connect Miami, immerse in luxury at Luxury Connect, and converge with industry leaders at Inman Connect Las Vegas. Discover more and join the industry’s best at inman.com/events.

The Inman Intel Index survey, also known as the Triple-I, is now open. Now in its sixth month, the Triple-I gathers insights, outlooks and sentiment from the residential real estate world’s most engaged professionals.

This month, we’ve added a host of new questions that will tap into commissions, recruiting and shifting market dynamics. Answers from agents, mortgage professionals, proptech players and industry executives will be fleshed out in extensive coverage next month.

The insights gathered from you and your peers illuminate industry trends, from the state of the housing market to advances in technology like artificial intelligence.

Here are a few key findings unearthed by the Triple-I since September:

More than 8 out of 10 real estate company leaders invested in technology in 2023, and 75 percent said they would do so this year. (January)

One in 4 agents surveyed said they managed to grow their business revenues in 2023. (December)

Over 1 in 4agents who responded said a significant chunk of their clients had mentioned commission suits, 3x as many as in late October. (November)