Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

When you first get into real estate, your business is built on hustle. You say yes to every opportunity, every client, every ZIP code and every transaction that comes your way.

And honestly? That’s exactly what you should do when you’re starting out. You don’t have the luxury of being picky. At that stage, the name of the game is momentum. But once you’ve established a foundation, it’s time to shift gears.

At some point, if you want your business to grow and your brand to mean something, you need to stop being everything to everyone and start being something to someone. That’s where defining your target audience comes in.

And no, it doesn’t mean you have to turn away the clients who got you here.

Why picking a niche isn’t a limitation — it’s leverage

When agents hear the words “target audience,” many flinch. The first fear is usually: But I don’t want to lose all my business now. I get it. You’ve worked hard to build relationships, to serve your sphere and to become known as someone who can help anyone, anywhere. But here’s the truth: Defining a target audience doesn’t mean walking away from those opportunities.

It means getting laser-focused on your marketing, branding and outbound efforts without abandoning the systems that are already working for you.

Let me say that again: You can still work your sphere, follow up with referrals and answer the phone when past clients reach out. But in the market? In your messaging? You want to be known for something.

Because when you try to speak to everyone, you reach no one. The agent who specializes in a specific lifestyle, property type or community will be remembered long after the generalist is forgotten.

And when your business is aligned with your passion, your energy is different. Your conversations are easier. Your content flows. You show up more consistently and more authentically. And over time? That consistency builds trust and authority that a generalist brand can’t replicate.

Build a business that feeds your strengths

Let’s be real for a second — none of us got into this industry to “get by.” We came here because we wanted freedom. Freedom of time, freedom of income and freedom to build something we enjoy.

So let me ask: What part of the business gives you energy? What kinds of homes or clients light you up? What communities do you naturally gravitate toward? What lifestyle do you know like the back of your hand?

If you’re a golf fanatic, why aren’t you the go-to agent for golf course communities in your area? If you love the mountains, why not specialize in cabins, view properties or homes with acreage? When your passion matches your positioning, everything in your business becomes easier — and more enjoyable.

This doesn’t mean you stop working with other clients. It means you build a foundation that feeds your energy and attracts people who see you as the expert in something specific. And when you’re known for something? You’re not just getting more leads — you’re getting better leads.

You don’t have to choose between growth and loyalty

This is where I see agents get stuck. They know they need to specialize. They want to define a niche. But they’re afraid it means giving up the clients and relationships they’ve spent years building.

Let me clear this up right now: You don’t have to choose.

You can still send mailers to your sphere. You can still follow up on referrals. You can still serve past clients when they reach out. The difference is in where you direct your energy and how you present yourself to the market.

Think of your niche as the tip of the spear: It’s what leads your marketing, your content and your brand identity. It’s what helps people remember you, refer you and reach out to you. But everything behind that spear? That’s still your foundation. That’s your systems, your sphere, your database. You’re not replacing it. You’re focusing it.

In fact, the more specific your message becomes, the stronger your brand gets — and the easier it becomes to generate referrals, build trust and scale without burning out.

Average is invisible

In business, there’s one thing that’s clear: Average is invisible. If you’re blending in with the crowd, you’re not being noticed. You could be the most talented, hardworking person out there, but if you’re just like everyone else, your efforts will go unnoticed. This is why being “different” is so powerful.

The most successful businesses and leaders didn’t get there by being average. They stood out. Whether it’s a product, service or personal brand, it’s the unique, bold moves that get remembered. Think about it — when’s the last time you chose the average option over the standout one?

In real estate, this means carving out a niche, focusing on what you do best and bringing value in a way that nobody else can. When you’re different, people notice. When you’re average, they don’t even see you.

Embrace the truth

The truth is, the agents who grow the fastest and build the most meaningful businesses aren’t the ones chasing everything — they’re the ones who are clear on who they serve and why it matters.

So take a look at your business:

Are you speaking to a specific audience?

Are you building a brand that people can describe in a sentence?

Or are you still trying to be all things to all people — and burning out in the process?

Start small. Pick a community, a property type or a lifestyle you’re passionate about. Build your brand around that. You’ll be shocked at how much easier everything becomes when your energy and your audience are aligned.

Nick Schlekeway is the founder of Amherst Madison, a Boise, Idaho-based real estate brokerage. Connect with him on LinkedIn.

According to managing broker Spencer Krull, with mandatory buyer-broker agreements, it’s time for NAR to get rid of the “participation trophy” of procuring cause.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

With the National Association of Realtors (NAR) on the ropes, reeling from Clear Cooperation, agent dissatisfaction with the settlement, as well as the organization’s handling of its scandals, now is the perfect time to strike a blow to get rid of procuring cause.

What is procuring cause?

NAR’s Arbitration Guidelines in relation to Article 17 of the Realtor Code of Ethics define procuring cause as “the uninterrupted series of causal events which results in the successful transaction.”

According to the NAR settlement FAQ, as a legal concept, procuring cause predates both the organization and its code of ethics. With offers of compensation communicated off-MLS following the settlement, buyer agreements have become an important factor in how buyer brokers protect their compensation in the event of a contractual dispute.

With procuring cause, an agent works with a buyer, and if that buyer ends up using a different agent to write an offer, then the first agent can file a complaint with their local board and go after the second agent’s commission. Procuring cause is NAR’s equivalent of rewarding the kid who licks the lollipop to make sure no one else will want it.

Who’s really to blame?

You’d think that mandatory use of buyer-broker agreements would rid the industry of procuring cause actions, but as a managing broker, I still get calls from other managers saying their agent had a buyer agreement, that my agent stole them, and their agent is thinking of filing a procuring cause complaint.

Sure, there are unscrupulous listing or buyer agents who seduce a buyer away with the promise of a lower commission, or suddenly a buyer “remembers” their aunt is a real estate agent and has her submit the offer.

But the buyer is the one who breached the contract.

Even when an agent asks a buyer if they’ve signed an exclusive agreement with another agent, a lot of buyers answer, “I don’t know.”

They don’t know? Either the buyer was daydreaming of turning a third bedroom into a découpage studio, or the agent was daydreaming of using the commission to turn their own third bedroom into a découpage studio.

Still, many buyers and agents view the buyer-broker agreement as “just something we have to sign because of the NAR settlement.”

If every buyer’s agent took the client’s hands in theirs, stared into their eyes and said, “We’re exclusive; you can’t work with another agent for three months,” some buyers are still going to “step out” on their agent. The new agent isn’t the person who wronged the original agent; the buyer is.

Think of it like a bad divorce, and substitute “cheating spouse” with “cheating buyer.” The spurned husband doesn’t sue the pool guy (or gal); they sue the cheating spouse because the spouse is the one who signed and broke the agreement. (Bonus: At least the husband finally understands why they had the cleanest pool in the neighborhood!)

Time to go

Perhaps procuring cause served a purpose when cooperating commissions were still coupled with listings, but that time has passed, and it’s now time for NAR to take it off the books.

Buyer’s agents: It’s time to get better at articulating your value, explaining why you deserve the compensation you are asking for, and explaining the conditions of the buyer-broker agreement to the same degree you do with a listing.

Buyers: It’s time you understand you’re entering into an exclusive agreement creating a partnership with your agent to work together to get you a home. Oh, and you can’t just “break the contract,” the same way you can’t just break your cell phone contract.

Brokers: It’s time to have your agents’ backs by actively pursuing breached buyer-broker agreements the way you do with listings.

NAR: It’s time to stop giving out the participation trophy of procuring cause; the agents who get the deals across the goal line shouldn’t be penalized because a buyer cheated on their agent. In the post-settlement world, it’s time to dump procuring cause.

Spencer Krull is a managing broker with Side and works as a real estate expert witness and consultant for attorneys. Connect with Spencer on LinkedIn and Instagram.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A number of years ago it seemed like a good idea to pack ourselves and four of our young kids into a camper van conversion and hit the road for three weeks. We planned to drive from California’s San Francisco Bay Area up to Vancouver Island, Canada, do a loop across the Rocky Mountains into Northern Alberta and then meander back down through Idaho.

About three hours into the trip, we began to doubt our sanity. Not only did the kids not adapt well to the confines of the relatively small vehicle, but the tiny portable TV with a built-in VHS player we had thoughtfully provided in the rear belted out repeats of Disney movies until we all had them memorized.

After visiting numerous friends and relatives, we left Calgary, Alberta, with the goal of getting back to California, and our sanity, as quickly as possible. Eventful in many ways, the highlight of the trip came as we hit the Canada-U.S. border crossing at Eastport, Idaho.

While our two oldest children were Caucasian, the youngest two were African-American. As we drove up to the U.S. Customs checkpoint, I rolled down the window and greeted the customs officer. He asked the normal questions: “Where do you live?” “How long were you gone?” “Are you bringing anything back you need to declare?” and so on.

Then he asked if we were all U.S. citizens. I explained that I was American, my wife was Canadian, our Caucasian daughter was Canadian, our Caucasian son was both American and Canadian and our youngest daughter, who is African American, was a U.S. citizen.

It was clear the officer was having a difficult time tracking all of this, when suddenly, without warning, our youngest, a small-for-his-age African American four-year-old who was hiding behind my seat, stuck his small head out my window and waved at the officer. Taken aback, the official looked at me, at my son’s impish face, back at me and then stated, “I don’t even want to know; get out of here!”

And then, a number of years later, came 911. Everything changed. Casual document-free entry at the borders screamed to a halt. Shortly after, headed to Canada in a rush due to my father’s passing, my wife forgot to bring her green card.

While she had her passport and U.S. customs had a copy of her green card on file, on our return home, a U.S. customs official refused her access to the U.S. until, scant moments before our flight was to depart, they finally allowed her to board the plane, but only after paying a fine.

Fast forward to today, and things have changed even more: The numerous Canadian family members and friends scheduled to come down and visit us this year have all canceled their trips.

Change is inevitable

It has been said that change is the only certainty we face in life. The problem with change is that you seldom see it coming, but, once it occurs, there is no going back. Those carefree days at border crossings where you could enter with no ID are long gone. The possibility of any future trips with my young children is also gone.

It is true with relationships as well: I received a call out of the blue a couple of years ago from a niece. My younger brother had been walking through an airport on his way to visit a friend when, with no warning, a massive heart attack instantly ended his life. There is no going back; all we are left with are the memories.

We all tend to believe we have endless time to do the things in life that matter but, unfortunately, things change and, before we realize it, we are out of time. In the section of his book entitled Time Wealth, Sahil Bloom, author of The 5 Types of Wealth, makes some poignant remarks concerning time and the changes that happen in life, emphasizing, “It’s later than you think.”

“There are specific windows — much shorter than you care to imagine or admit — during which certain people and relationships will occupy your life. You may have only one more summer with all of your siblings, two more trips with that old group of friends, a few more years with your wise old aunt, a handful of encounters with that co-worker you love, or one more long walk with your parents. If you fail to appreciate or recognize these windows, they will quickly disappear.”

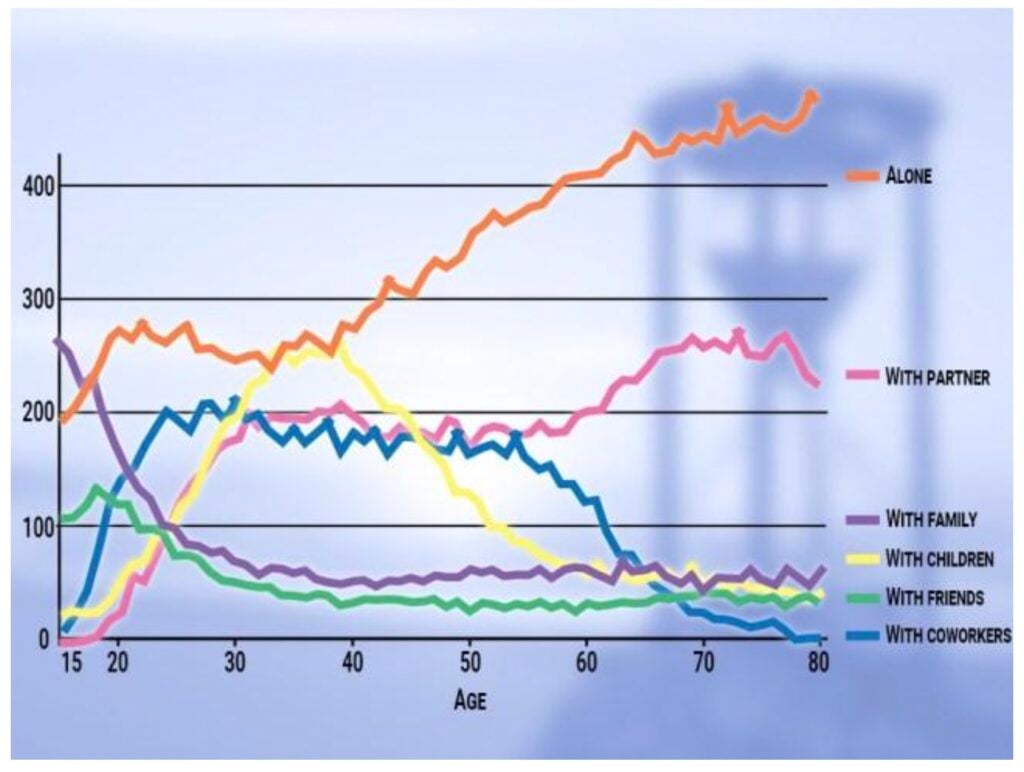

Most people believe they have a good idea where they spend their time. The graph below, however, based on the data from The American Time Use Study, puts things into shocking perspective.

The simple truth is this: Unless you make a conscious choice to spend your time where it really matters, the inevitable changes in your life will rule out many of your choices — and in many cases, much sooner than you think. Harry Chapin’s song “Cat’s in the Cradle” is a vivid reminder of this.

The irony of this song is that Chapin was killed in a car crash at age 38 when his son was only 9 years old. He not only never got to see his son grow up, but his career was cut short, and his son never had the opportunity to be like his dad as he might have been had he lived longer.

The choices we make now to actively manage the time we have remaining in a constructive way will set the stage for how we live the rest of our lives. — Carl Medford

You are more than your work

I recently heard of a woman in Canada whose retirement is scheduled to start in about 30 days. She is beside herself looking at the looming deadline, with no idea what she will do once this new chapter in her life begins.

She had poured herself into her job and, as the end is nearing, is discovering that she has no identity outside of her career. She had never taken the time to develop any hobbies or meaningful relationships, nor does she have a good relationship with her children, one of whom is homeless and whose whereabouts and condition is mostly unknown.

Making matters worse, her husband, recently semi-retired, has begun spending the majority of his free days on the golf course. Adding insult to injury has been the impending financial crisis in Canada, which has been dealing devastating blows to their retirement funds.

As her husband is gone most days, is unwilling to travel (other than to the links) and has developed a deeply negative frame of mind obsessing over the economy and their financial situation, she is left looking at what should have been a liberating time in her life as an impending nightmare. Instead of joyfully anticipating the days ahead, she is looking at them with dread.

A meaningful life needs to be planned. Unfortunately, many of us choose, instead, to live from moment to moment, letting the tyranny of the urgent get in the way of the truly important.

In a business such as real estate, there are no end of distractions that can come at us at all times of the day and without warning. It will take some serious thought, preparation and commitment to be able to bring your time in line with your future hopes, goals and aspirations. Here are 5 recommendations:

1. Take time to identify your life goals and priorities

Sit down with a pad of paper in a quiet place where you cannot be distracted, turn off your phone, and get away from your email and social media. You might even consider going on a retreat where you can have a chunk of undisturbed time to think.

Start asking yourself some deep questions.

What do you believe is truly important?

What do you want your life to look like in 10 years? Twenty years?

What types of relationships do you want to maintain or even develop as life moves onward?

What do you hope to accomplish after you have retired?

These are not the classic vision board items such as a nice car, trip to France or big house; none of those things will really matter if you end up with no friends, alienated family members and so on.

2. Analyze your current activities

Start with your days: Write down everything you do on a daily basis. Since days will differ, provide a list for every day of the week.

Interestingly, many people get to bedtime and have no idea how they spent their time that day. You should consider a period of time during which you have a pad of paper or journal with you constantly to record your times and activities as you go through the day.

On a separate page, list weekly recurring activities, monthly activities and then yearly events.

3. Categorize your activities

Once you have a good idea of where you are spending your time, split the various activities into categories and then rank them in order of importance. A model that has been used for years by many is the Eisenhower Matrix:

Dwight D. Eisenhower, a decorated military leader and the 34th U.S. President, served from 1953 to 1961. He was the Supreme Commander of the Allied Expeditionary Force in Europe during WWII and later oversaw the planning and execution of Operation Torch and the invasion of Normandy.

As president of the United States after President Harry Truman, he oversaw the construction of the Interstate Highway System, expanded Social Security, and took steps to integrate the military. He also signed the first significant civil rights bill since Reconstruction.

Considered one of the most significant world leaders of the past century, Eisenhower was known for saying: “I have two kinds of problems: the urgent and the important. The urgent are not important, and the important are never urgent.”

Faced with decisions that marked many turning points in his career, he used this matrix to manage his time so that the truly important things were accomplished while avoiding getting enmeshed in things that did not matter. It serves as a useful tool to help us prioritize everything we do.

4. Be willing to make some tough decisions

We have all heard the analogy of a person spending all of their time and resources climbing the ladder of success, only to reach the top and discover that the ladder was leaning against the wrong wall.

You may become the top producer in your state or build the largest real estate team on the planet and achieve all your financial dreams, but, after you retire, you will be forgotten as the next person climbs the ladder after you. Success is fleeting and, after you have died, that success will not matter one iota.

In Bloom’s case, living on the West Coast while his parents lived on the other side of the country, he describes how, after realizing the limited number of times he could reasonably expect to see his parents again, he chose to relocate to be close to his parents.

My wife and I made the same decision a number of years ago: Realizing we had spent the majority of our time with our older grandkids in the San Francisco Bay Area, we chose a concrete date at which time we would sell our Bay Area home and move two states away from our businesses to be closer to the younger grandkids.

It has not been easy, but the pandemic changed the rules of engagement, making it more possible to run a business remotely. We also fly in to interact with our teams and clients on a regular basis.

Ironically, it is the decisions we do not make that tend to produce the most regrets: The games we did not attend, the trips we did not make, the time we did not spend with loved ones and so on. In every case, once the opportunity is over, it is permanently in the rearview mirror of life; there is no going back.

5. It’s not too late

While you will never be able to do some things again, the future is open to you with opportunity. New friends. New hobbies. New goals, both for life and business. While some changes may need to be drastic — such as a move to the other side of the country to be closer to family — others can be small, incremental changes that will have a compound effect over time.

As an example, a simple decision to leave the office at 5 p.m. every day and spend dinner with your family instead of lingering into the evening hours can have a compounding effect on your family relationships. If you can manage that dinner with all hands present, allow no phones or TV, and instead, engage in productive conversations, so much the better.

You can also set aside time to pursue your passions. I am amazed at how many do not have hobbies or other meaningful activities; many simply default to reruns on TV.

My wife just decided to fulfill a lifelong dream to learn how to sail. She has taken the plunge and is loving every minute of it. She also started to paint with watercolors, and we have discovered amazing talent that had been hidden for years.

We are in a time of massive change in our industry. Real estate as we have known it is gone forever. Factor in a morphing market with higher interest rates, limited inventory and the potential of tariffs, and we are in a veritable perfect storm.

Now that the changes have occurred:

How will you navigate the way forward?

Will you let the current reality rob you of joy and passion, or will you embrace the change and chart a new course ahead?

Are you willing to pay the price required to hone your skills, hunker down and press into the new realities, or will you simply go with the flow of the past and let your business and dreams get swept out to sea?

There will always be tough decisions required when aligning your life and your business to goals that really matter. Those who dive in and commit are the ones who, as life progresses, live fully, knowing that they made the most of the opportunities they had as they came along. In the end, they are the ones who are truly successful.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The standard for real estate marketing can feel like déjà vu.

The same flyers, “just listed” templates and social posts — it feels like everyone has been doing the same thing in graphic design for real estate since 2016.

If you are “stuck in the same old strategy loop,” it’s time to shake things up — and rewrite the “rules” of real estate marketing and make your life easier.

Canva, aka the solution to Microsoft Publisher, has been on the design scene for quite some time, but it is easy to get stuck in a rut when using the tool that has become a standard go-to for many agents daily.

Social media advertising has changed and is becoming more organic. Fewer graphics and more natural-looking content are not only easier to produce, but they also look less cluttered to potential clients.

5 ways to rewrite the rules

Here are five ways to rewrite your old-school marketing playbook and use Canva and AI to save time and increase engagement with your audience.

1. Ditch or scale back the graphics

When it comes to content creation, a picture is worth a thousand words, and loading a beautiful photo with text, logos and tons of information creates a cluttered visual for your potential customers.

Not every piece of content needs to be branded with your face and phone number. This is a personal choice; just make sure your contact information is easy to find within the post’s caption.

How to do it:

Use Canva’s blank templates to resize photography to fit the social media platform it will host

Make sure to save the photography on your mobile phone’s camera roll for quick stories or posts on the fly

Create a template with your contact information and branding for end screens on Reels or the last “post” on an Instagram carousel. Let the rest of the content speak for itself

Example: Build a carousel of photos for a Facebook and Instagram post for a new listing. Use the caption for the call to action and your contact information. Mix up the use and order of the photos each time so that the audience may see different images each time you post about the listing.

Pro tip: Use ChatGPT to help you write a caption for each social media platform. Here is an example of a prompt that I like to use. Copy and paste the listing information from an MLS syndicated platform, and then add this prompt:

Write an SEO-optimized caption for [List your platform] for agent [who you are and your brokerage] with [contact and disclosure information]. Make it a “just listed” announcement and make sure to call attention to all the special features of the home. Find relevant hashtags, and keep this fun and light.

Pro tip: Invest in Canva Pro and build your brand inside Canva. Upload colors, logos and other elements you use all the time so they are there and ready to go. You should not be uploading this each time.

2. Make market updates fun and beautiful

Everyone wants to understand the market, but nobody wants to read a novel to get the information. Make a quick 30-second video where you explain the highlights, or go around your target market and take some great seasonal photos about your community.

All my favorite social media folks, like Katie Lance and Jimmy Burgess, will tell you (and show you) that video will get you great results, but if you are too camera-shy, use photography to your advantage.

How to do it:

Use Canva’s infographic or chart templates. Search “market update” or “infographic”

Add your MLS stats, or leverage a resource like your brokerage reports, and use this as one of your end screens or as a buried post in your carousel post

Copy and paste the data into ChatGPT and again give it the prompt to make you an SEO-optimized caption for the social media platform on which it will be featured

Pro tip: Create an SEO-optimized post on LinkedIn to provide a market report for the month and highlight your recent sales. This is a great way to track your portfolio and successes and show your audience that you are a professional salesperson who’s always ready to do business.

3. Make a simple flyer template with no photos

Years ago, when I began showing Canva to real estate agents in a marketing and design class, one gentleman stood up in front of the class, trying to vouch for me and my expertise, saying that I was “really good at making colored prints.”

This statement haunts me to this day. Agents, you are more than just the flyers. You are so much more.

Canva

The time agents, admins and assistants spend making flyers, hanging flyers and running them out to the property is just a time-waster, a tree-killer and a stress-booster.

Now, I recommend creating a simple flyer template using one QR code that goes to a live website with real-time updates, a full gallery, video and contact information for the agent.

It’s practical, it’s easy to generate if you need to make it before the photos are ready, and you can drop the code on stickers, business cards and other items that you have invested in and let them work instead of you working trying to size the photos into the right template and still having your client tell you they do not like the colors.

Pick a simple template (a postcard size is great), drop the code, the property address, your contact information, required disclosures, and rock and roll.

Use this template for all your listings, and keep things moving quickly.

Pro tip: Use this for quick direct mail to the neighborhood before an open house. The neighbors can hopefully send a few more folks your way, or they may see your great marketing and want to list with you as well.

4. Capture moments from your day, and turn them into a letter or a blog

One of the things I love about Canva is that it has some great ready-to-use templates for blog graphics or even a personal letter or postcard to your audience.

Don’t try to recreate the wheel. Use these templates to create meaningful and straightforward storytelling moments for your audience.

Blog post idea: Use Canva to make a graphic for your blog or even your LinkedIn article, and write about something that is not only an educational moment but also a milestone in your career. Try to keep it at around 250 words.

Direct mail letter: You can create your own stationery on Canva and then use it to send out a monthly letter to your sphere of influence. Make sure to sign a wet signature at the end of the letter if you can. A simple one-page letter can go a long way. Ditch the “just sold” postcards, and take a moment to make a meaningful connection with your audience. You can also turn this into a JPEG and post it on your social media as well, ensuring that the size is correct.

Canva

5. Make a 1-page business contact handout for each phase of the transaction

You must hustle, grind and work 24/7 to be the best real estate agent. This is one of the “oldest” rules in real estate, but honestly, it’s impossible to uphold, and it may be one of the biggest reasons we have such a high turnover rate in our industry.

Many phone calls, text messages and emails agents receive are from customers, other agents and vendors looking for information or instructions on the next steps.

Canva

You’re more than a salesperson — you’re a community guide, a trend spotter and a resource. A mini-mag shows your value, builds your brand and nurtures your list like no drip campaign can.

How to do it:

Create your guide and make sure it has your business hours, mailing address, preferred contact information, information on who to contact in an emergency and the contact information of all your favorite vendors you may recommend during the process. Also, on this flyer, list the “steps” to closing, so everyone can follow along. You will give this to your clients and the agents on the other side of the deal. They will use it, and you will get much use out of it, especially when you are working with new-to-real-estate clients or newbie agents.

Make a who-to-contact after-closing guide featuring information on utilities, local vendors, handymen, warranty information, etc. Give this out a week before closing. It will be a lifesaver in many cases.

Breaking the rules

You don’t need a marketing team, a graphic design degree, or hours and hours of graphic design each week for social media content and branding. You don’t have to do the same thing everyone else is doing. You don’t need to make extra work that is lost in seconds with the consumer.

Currently, scheduling the content is more important than pushing out over-polished, over-embellished content in the algorithm when considering ROI.

I would rather see agents push out a few personalized, natural-looking content posts than flood the feeds with graphic after graphic of announcements.

You need the right tools and the confidence to try something new and ignore the crowd. Canva gives you creative control and lets you express your brand personality, but it’s a tool to use, not a place to spend valuable hours that you could be spending with your loved ones and prospecting for new business.

Remember: This isn’t about being perfect — it’s about being consistent, memorable and creating content that works for you rather than you working to generate content constantly.

Rachael Hite is a seasoned housing counselor and thought leader in the real estate industry. Connect with her on Instagram and LinkedIn.

Sean Varin and Paul Marsh have been promoted to senior roles at Fathom Holdings and Fathom Holdings’ subsidiary, Encompass Lending Group. The duo will be responsible for stoking growth opportunities at both companies.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Fathom Holdings executives Sean Varin and Paul Marsh will take on new growth and mortgage roles within the company, according to an announcement on Tuesday.

Varin will transition from president of Encompass Lending Group (ELG) to Fathom Holdings SVP of strategic growth and partnerships, while Marsh will replace Varin at ELG.

Sean Varin

“Sean and Paul have been instrumental in the growth of Encompass Lending Group and exemplify the leadership qualities we value across Fathom Holdings,” Fathom Holdings CEO Marco Fregenal said in a prepared statement. “Sean’s vision for strategic integration and national program growth, combined with Paul’s passion and expertise in lending, will drive continued success across our brands. I’m excited to see what they will accomplish in these new roles.”

Varin will be responsible for expanding Fathom Holding’s national initiatives, including the Ambassador Program, Elevate Program, First Home Buyer Program, Consumer Credit Education Program and Hometown Heroes. His efforts, the announcement said, will be centered on strengthening collaboration between Fathom Holdings’ five brands and identifying future merger and acquisition opportunities.

“This is a huge moment — not just for me, but for all of us — as we work together to build something truly special,” Varin said of his promotion in a written statement. “The future is bright, and we’re just getting started!”

Paul Marsh

Meanwhile, Marsh will focus on strategic growth opportunities at ELG, Fathom’s mortgage origination company. Marsh co-founded ELG in 2008 and operated under E4:9 Holdings until April 2021, when Fathom acquired the Texas-based E4:9 Holdings for $26.75 million. Now that he’s back at the helm, Marsh will oversee ELG’s day-to-day operations and focus on “innovation, expansion, and delivering even greater value to both referral partners and clients.”

“This has been an incredible journey since day one,” he said. “It is truly an honor and privilege to lead this organization. We will continue to build on the great foundation that has been established with Sean’s leadership. I’m excited for the future!”

The appointments come as Fathom Holdings works through a tough period in the company’s history. During the fourth quarter of 2024, Fathom Holdings saw its revenue grow 24 percent year over year to $91.7 million as losses reached $6.2 million. The North Carolina-based company is at risk of being kicked off the Nasdaq due to its shares trading below $1.

Fathom notified investors on April 18 of Nasdaq’s delistment notice, and said it has until Oct. 13 to regain compliance with its bid price rule. If shares in Fathom close at $1 or higher for at least 10 consecutive business days, it will be considered back in compliance. If shares in Fathom remain below $1, it could qualify for another 180-day reprieve and regain compliance through a reverse stock split, a previous Inman article explained.

Executives put a positive spin on prospects for growth, with loan origination volume up 17 percent from a year ago to $32.4 billion and revenue up 5 percent to $613.4 million.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The nation’s biggest mortgage lender lost $240.7 million during the first quarter, as a dip in mortgage rates forced United Wholesale Mortgage to write down the fair value of its mortgage servicing rights by $388.6 million.

UWM executives put a positive spin on the big picture in reporting earnings Tuesday, noting that loan origination volume was up 17 percent from a year ago to $32.4 billion, as the company did brisk business with homeowners looking to refinance.

Executives at the Pontiac, Michigan-based wholesale lender said they expect to originate $38 billion to $45 billion in mortgages this quarter, with gain margin of 90 to 115 basis points. The upper range of that guidance would represent UWM’s first $40 billion quarter since Q4 2021.

Mat Ishbia

“We haven’t hit over $40 billion since the real boom times, and we are going to do that this quarter,” CEO Mat Ishbia predicted on the company’s earnings call.

“Where everyone else is kind of hovering, our investments have been working,” Ishbia told investment analysts. “Our broker channel is winning. And then on top of that, the technology stuff that’s going to come out in the second quarter … it’s going to blow your mind, and it’s just the beginning of what we’re doing.”

UWM refinanced $10.7 billion in mortgages during Q1, nearly double the $5.5 billion in refi volume that came in a year ago, helping drive 5 percent revenue growth, to $613.4 million.

While purchase loan originations were essentially flat at $21.7 billion, UWM’s investment in AI and other technologies will allow it to ramp up its business with little impact on expenses, Chief Financial Officer Rami Hasani said on a call with investment analysts.

UWM announced a strategic partnership with Google Cloud last month to integrate AI and data analytics capabilities into its lending platform.

Rami Hasani

“We believe our business is currently in a position to handle twice our 2024 origination volume with minimal impact to our fixed costs,” Hasani said on his first earnings call since succeeding Andrew Hubacker as CFO on April 1.

Shares in UWM closed down 15 percent Tuesday after touching a new 52-week low, as shareholders also digested details of a plan to increase UWM’s “float,” or the number of outstanding shares, by up to 80 million shares.

Ishbia said that under a plan scheduled to go into effect on June 17, he’ll continue to own around 80 percent of UWM’s shares a year from now, down from 87 percent today. He said the company will continue to pay a 10-cents-per-share quarterly dividend — payouts that also benefit him and his family as majority owners.

Plans by rival Rocket Companies to acquire the nation’s largest loan servicer, Mr. Cooper, prompted UWM to end its subservicing contract with Mr. Cooper and announce last month that it will bring mortgage servicing in-house.

Ishbia said the plan is to start onboarding loan servicing at the beginning of next year, and “hopefully have it all in house by the end of next year.”

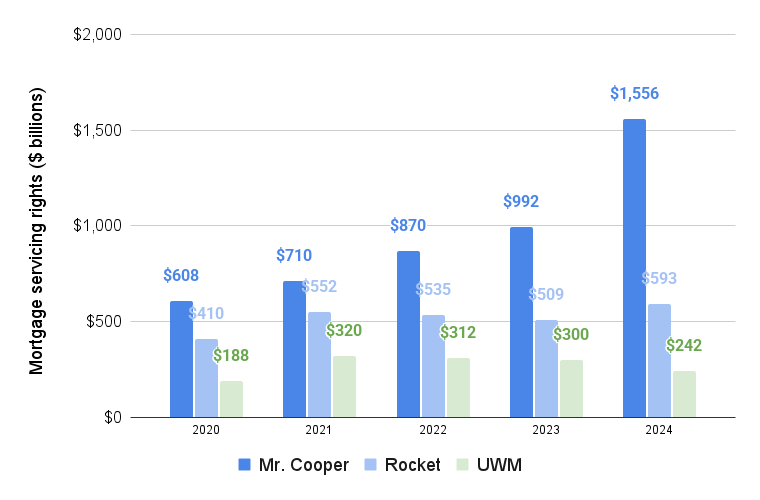

For now, UWM’s mortgage servicing rights (MSR) portfolio continues to shrink as it sells servicing rights for cash. UWM’s MSR portfolio shrank by 11 percent during Q1 to $214.6 billion.

UWM’s shrinking mortgage servicing portfolio

Mr. Cooper, Rocket Mortgage and UWM mortgage servicing rights (MSR) portfolios, including subservicing. Source: Company earnings reports.

Loan servicers collect monthly mortgage payments from borrowers, passing the money along to lenders or investors in mortgage-backed securities who have purchased the loans.

Big mortgage lenders often like being in the loan servicing business because the fees they can earn are a steady source of income that can even out ups and downs in the housing market.

Lenders who service their own loans are well-positioned to “recapture” borrowers when they’re ready to refinance or buy their next home.

But the constantly fluctuating valuations of mortgage servicing rights (MSRs) can create accounting headaches.

When mortgage rates fall, MSRs become less valuable because borrowers are more likely to refinance and end up with another loan servicer. But when mortgage rates rise, so does the paper value of a servicer’s MSRs. MSR valuations can push profits, as measured by net earnings, deep into the red or the black.

“As we’ve discussed several times, we have zero control over MSR values, whether it goes up or down,” Ishbia said. “So it’s really not that relevant to me. But we did have an amazing quarter and we’re profitable on all the [other] measures we look at.”

Another metric — adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) — remained positive in Q1 at $57.8 million, down 43 percent from a year ago.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.