by Matt Carter | May 16, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

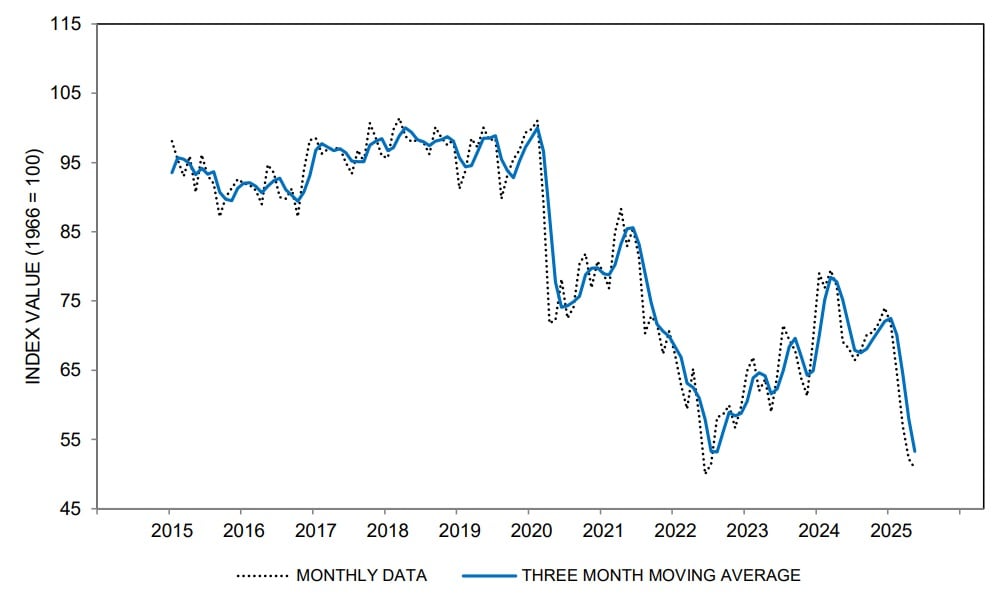

A closely followed measure of consumer sentiment deteriorated for the fifth month in a row in May and is approaching an all-time low, but the economy continues to do better than it and other surveys might imply, economists say.

The University of Michigan Index of Consumer Sentiment slipped to 50.8 in May, down 3 percent from April and 26 percent from a year ago, according to preliminary data released Friday.

Joanne Hsu

Three-quarters of those surveyed cited tariffs as a cause for concern, and “uncertainty over trade policy continues to dominate consumers’ thinking about the economy,” survey director Joanne Hsu said in a statement.

The survey was fielded between April 22 and May 13, so many responses were gathered before the Trump administration announced a pause on some tariffs on goods from China on May 12.

UofM Index of Consumer Sentiment

The Consumer Sentiment Index hit an all-time low in records dating to 1978 in June 2022, when inflation as measured by the Consumer Price Index was hitting a post-pandemic high of 9.1 percent.

The Consumer Price Index for April, released Tuesday, showed prices were up 2.3 percent from a year ago last month, closer to the Fed’s 2 percent goal than the 3 percent annual inflation registered in January.

“The Michigan report continues to paint, at face value at least, a grim picture,” Pantheon Macroeconomics Senior U.S. Economist Oliver Allen said in a note to clients.

The Index of Consumer Expectations — which historically has been a better guide to growth in consumers’ real spending — was down 32 percent from a year ago in May, to 46.5 — the lowest reading since 1980, Allen noted.

It’s not just the prospect that tariffs will reignite inflation that has consumers worried. Confidence in the labor market “has taken a heavy blow, with the net share of households expecting higher unemployment remaining around its highest level since the global financial crisis,” Allen said.

There’s little doubt the economy is decelerating — an advance estimate of real gross domestic product (GDP) suggested that the economy shrank by 0.3 percent during the first quarter, thanks to a tariff-driven surge in imports and a decrease in government spending.

But forecasters at Pantheon Macroeconomics suspect consumer surveys — and the University of Michigan survey in particular — paint an “unduly negative” picture of consumer outlook.

Retail sales posted gains in March and April, and “most near-real indicators of consumers’ discretionary spending on services are holding up well,” he said.

Oliver Allen

“Our view is that consumers’ spending will soften as the wave of pre-tariff purchases unwinds, higher prices for imported goods take a bite out of real incomes, and policy uncertainty further undermines hiring and the labor market,” Allen concluded. “But we doubt consumption growth will slow nearly as sharply as the Michigan survey currently implies.”

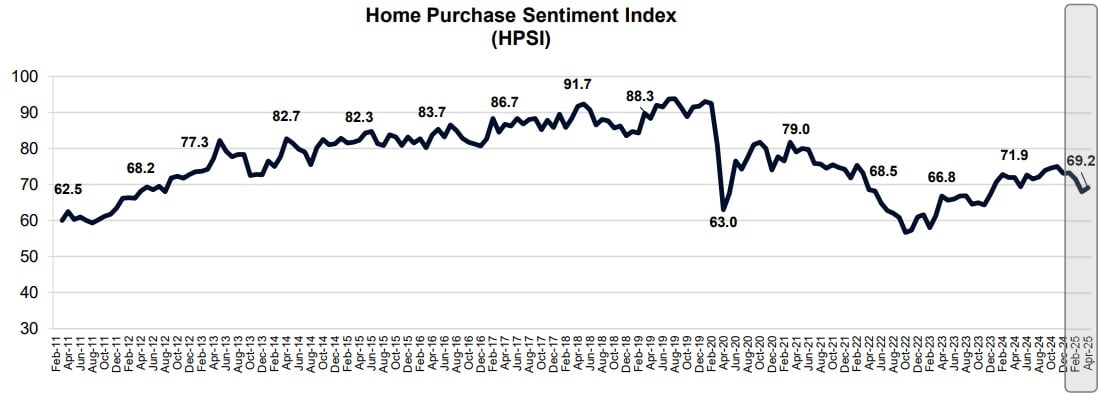

Surveys by the Mortgage Bankers Association show demand for purchase mortgages has increased for two weeks in a row, as would-be homebuyers responded to growing inventories of listings in many markets and stabilizing interest rates.

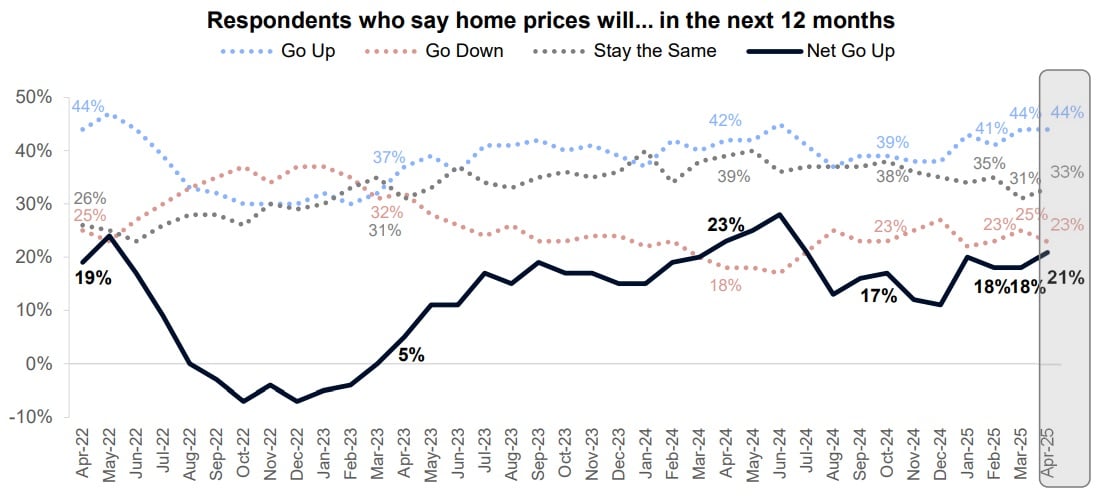

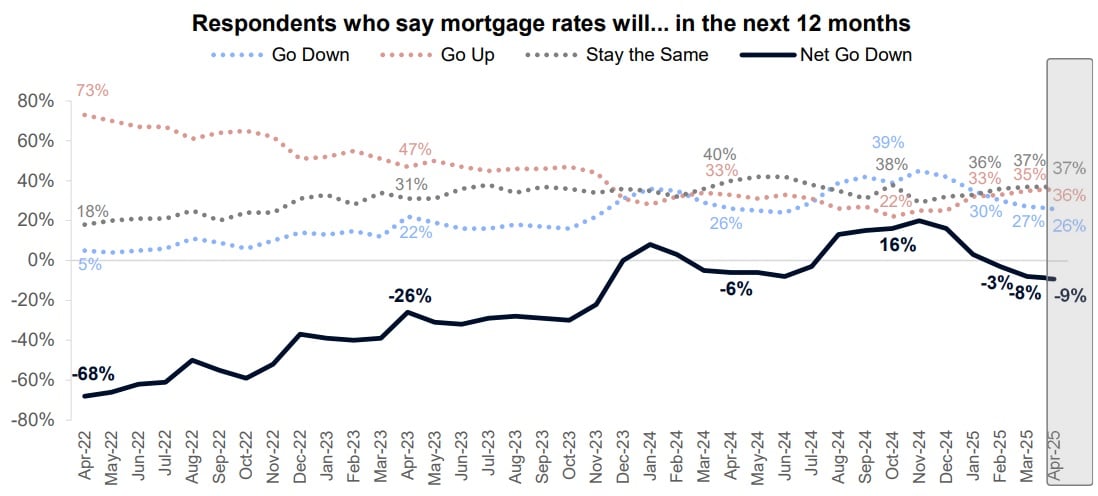

Fannie Mae’s latest monthly National Housing Survey, which polled 1,181 household decision makers between April 1 and April 18, found consumer sentiment toward housing was up slightly from March to April.

At 69.2, Fannie Mae’s Home Purchase Sentiment Index (HPSI) was up 1.1 points from March but down nearly three points from a year ago.

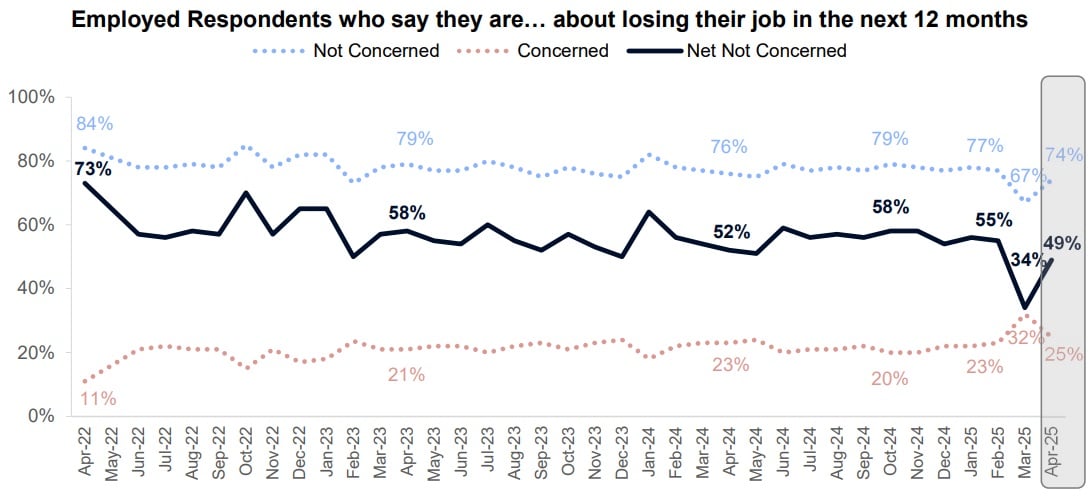

Three of the index’s six components improved: Americans were less concerned about losing their jobs than in March, more had seen their incomes increase, and more expected home prices to increase in the next year.

But consumers were more pessimistic about selling conditions and the prospect for mortgage rates to come down in the year ahead.

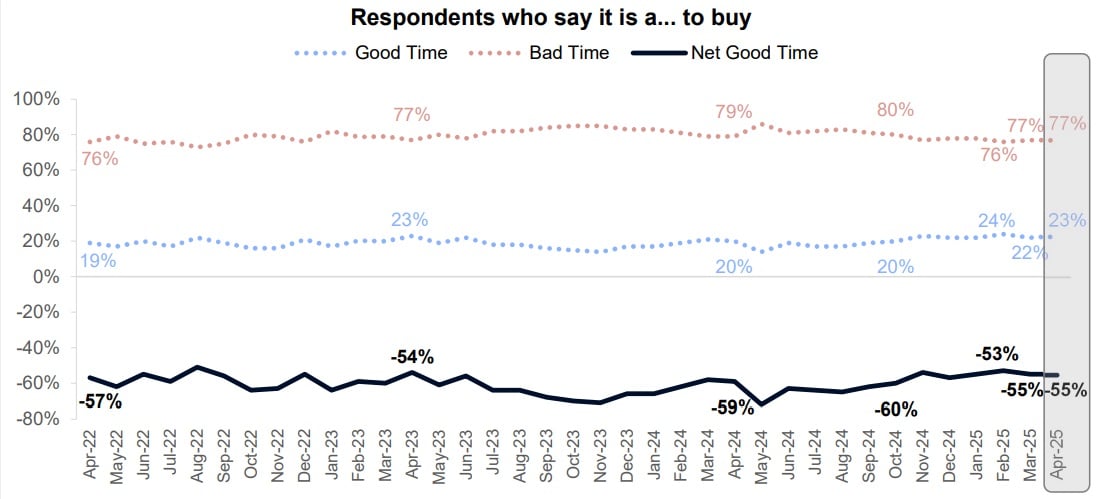

Only 23 percent of Americans surveyed in April said it was a good time to buy, but that was up from 22 percent in March. The share who said it was a bad time to buy (77 percent) remained unchanged.

The share of consumers who say they would buy a home if they were going to move was unchanged at 65 percent.

The share who said they would rent if they were going to move increased one percentage point from March to April, to 35 percent.

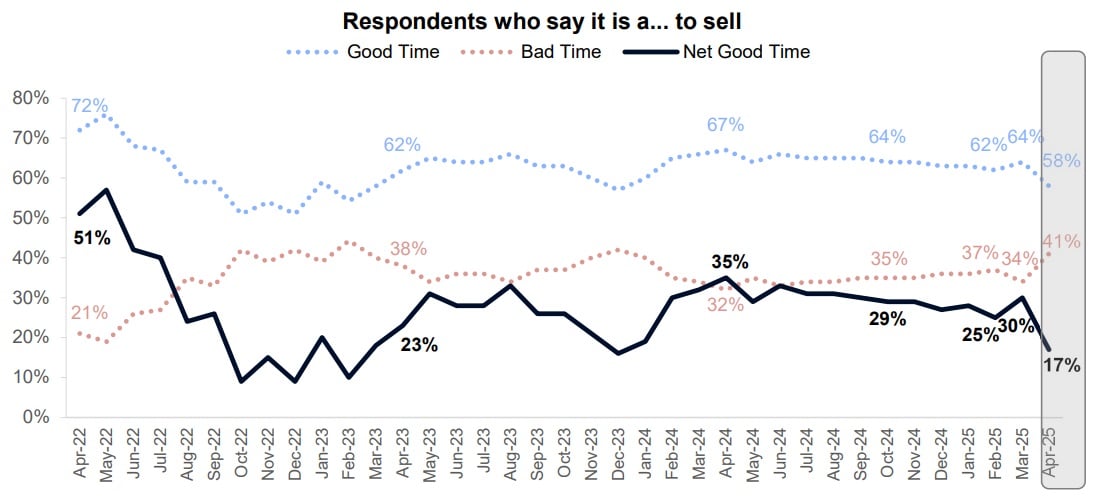

The percentage of household decision makers who said it was a good time to sell fell from 64 percent in March to 58 percent in April.

Only 23 percent of Americans surveyed in April thought home prices would go down in the next 12 months, compared to 25 percent in March.

While that would be bad news for would-be bargain hunters, it’s viewed as a positive for the HPSI as it reflects consumer confidence that housing markets aren’t on the verge of crashing.

About one in four households surveyed in April (26 percent) expect mortgage rates will come down in the next 12 months, about the same as March (27 percent) but down sharply from November, when 45 percent were expecting lower rates in the year ahead.

Only one in four employed Americans (25 percent) said they were concerned about losing their job in April, down from a spike in March to 32 percent.

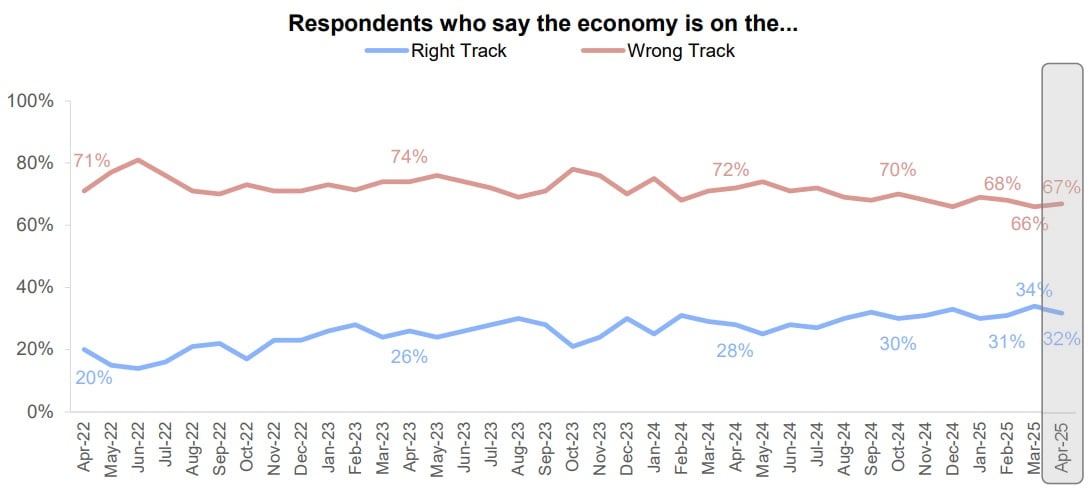

While not factored into the HPSI, only one in three households (32 percent) thought the economy was on the right track in April, down from 34 percent in March but up from 28 percent a year ago.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

This post was originally published on this site

by Jim Dalrymple II | May 16, 2025 | Industry, News Feed

A new Redfin report indicates that most consumers are still willing to pay for their real estate agents and that last year’s NAR rules have had minimal impacts on agent pay.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

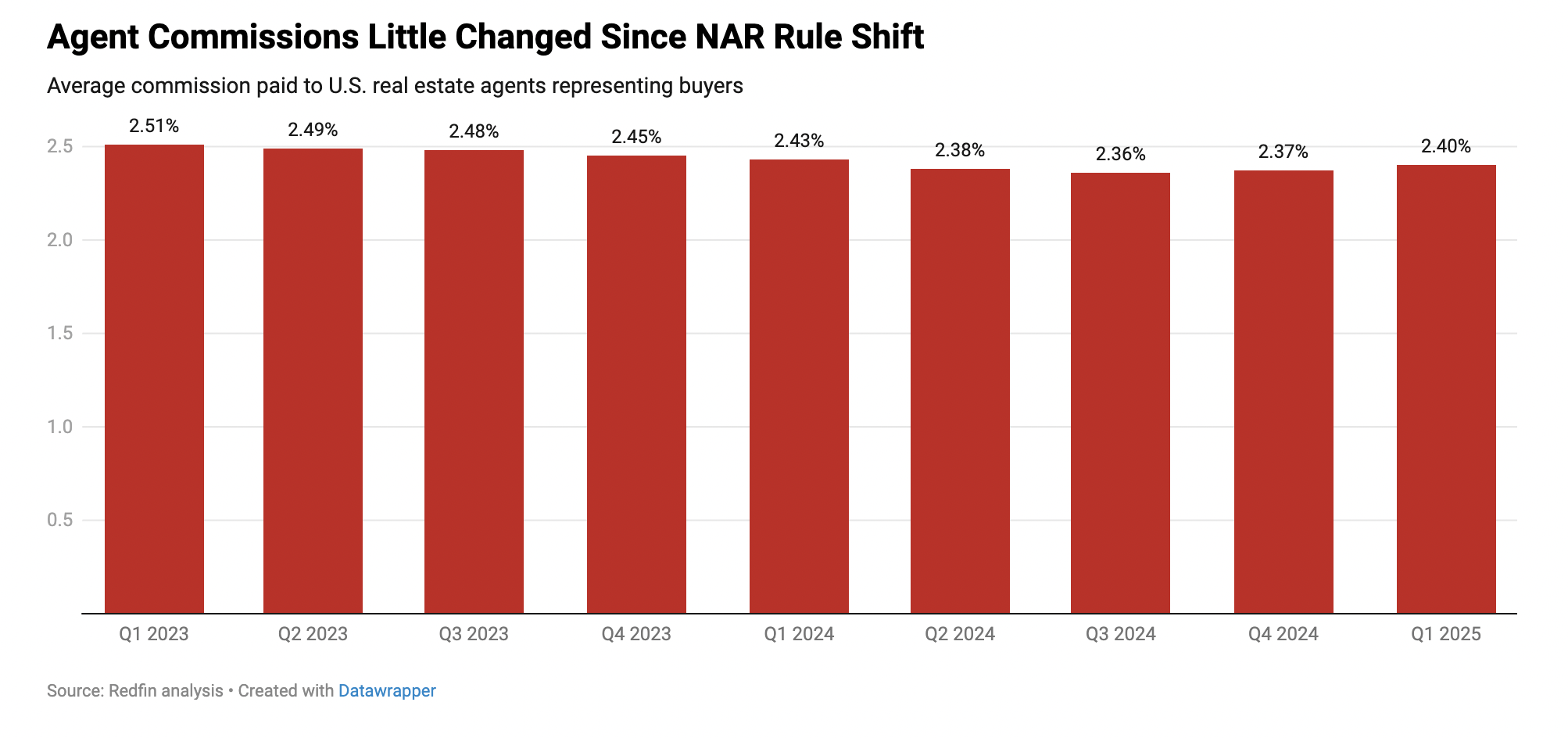

More than a year after the National Association of Realtors announced a landmark antitrust settlement, evidence continues to mount that agent commissions are mostly holding steady.

The latest data comes from Redfin, which on Friday reported that during the first quarter of 2025 buyers’ agents averaged commissions of 2.40 percent. Redfin’s report notes that the figure is actually a slight uptick compared to the final three months of 2024, and a bit of a dip from a year prior. But a graph of buyers’ agent commissions that Redfin included in its report illustrates how little commissions have changed over the past two years.

Credit: Redfin

Redfin’s report further notes that commissions have performed differently at different price points. For homes that sold for $1 million or more, buyers’ agent commissions have fallen relative to a year ago. But for homes that sold for less than $500,000, commissions in the first quarter of this year actually went up compared to the same time in 2024.

“Commissions are lower for high-priced homes because agents have more room to reduce their fees and still earn a healthy paycheck,” the report further notes.

The report includes less data on sellers’ agent commissions, but cites anecdotal reports from agents who say that sellers are also still willing to pay commissions.

Redfin ultimately attributes these trends to the fact that the “lion’s share of recent sellers — 45.9 percent — did not try to negotiate.” Additionally, the report found that buyers were less likely to negotiate their agents’ commission than sellers.

The report’s findings fall largely in line with those from recent Inman Intel Index survey data. Earlier this week, for example, Intel reported that 58 percent of agents surveyed in late April said that commission rates have remained unchanged or even increased since the new NAR rules went into effect last August. The rules were part of NAR’s settlement agreement in antitrust commission cases such as Sitzer | Burnett and Gibson. Among other things, they barred sellers’ agents from making offers of compensation to buyers’ agents in their multiple listing services.

Intel also found that only 6 percent of agent respondents in April said more than half of their buyers were trying to negotiate their compensation downward. Additionally, 11 percent of agents told Intel that they have seen an increase in their negotiated compensation rates since the new rules went into effect.

However, there are signs that change is coming, if slowly. Nearly 2 in 5 agent respondents to Intel, for example, said that their rates had declined since August, though only 1 in 20 agents described a “significant” decrease. And 36 percent of agents in April reported working with sellers who have taken a hard-line approach against covering the commission. Notably, this share has climbed from 26 percent in December.

Redfin’s report also comes on the heels of a new analysis from the Federal Reserve that found that requiring buyers’ agent agreements has no effect on commissions. Such agreements are also a component in NAR’s new rules.

All of these findings, however, come against the backdrop of a market that has cooled significantly over the past several years, thanks to higher mortgage rates. But if those market conditions were to change, at least some agents envision commissions evolving as well.

“Sellers don’t seem to have any issue paying a buyer’s agent commission,” Chaley McVay, a Redfin agent in Oregon, is quoted as saying in Redfin’s report. “But if we enter a seller’s market similar to that of 2021 and 2022 — with rampant bidding wars — sellers may be inclined to offer low or no commission to the buyer’s agent, forcing buyers to bridge the gap. And if that happens, first-time buyers will be hit hardest because many of them can already barely afford to buy a home.”

Email Jim Dalrymple II

This post was originally published on this site

by Marian McPherson | May 16, 2025 | Industry, News Feed

After a herky-jerky few years, the housing market is at a major tipping point, according to the National Association of Realtors’ May 2025 Housing and Affordability Report. The report, which is based on NAR and Realtor.com data, revealed the market needs at least 416,000 listings priced at or below $225,000 to make homeownership affordable to the typical middle-class household.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

After a herky-jerky few years, the housing market is at a major tipping point, according to the National Association of Realtors’ May 2025 Housing and Affordability Report.

The report, which is based on NAR and Realtor.com data, revealed the market needs at least 416,000 listings priced at or below $225,000 to make homeownership affordable to the typical middle-class household.

Currently, households earning annual incomes of $75,000 can only afford 21.2 percent of available housing — a slight improvement from March 2024 (20.8 percent), but far below pre-pandemic trends (49 percent). Households earning $100,000 are only doing slightly better, with them affording 37.1 percent of current listings, up from March 2024 (36.9 percent) but significantly down from March 2019 (64.7 percent).

Meanwhile, households making $50,000 have long struggled before the pandemic. Households in this income bracket can only afford 8.7 percent of listings, down from 9.4 percent in 2024. The market needs at least 367,000 listings priced at or below $175,000 to improve affordability, the report said.

Danielle Hale

“Shoppers see more homes for sale today than one year ago, and encouragingly, many of these homes have been added at moderate income price points,” Realtor.com Chief Economist Danielle Hale said in a written statement. “But as this report shows, we still don’t have an abundance of homes that are affordable to low- and moderate-income households, and the progress that we’ve seen is not happening everywhere. It’s been concentrated in the Midwest and the South.”

In NAR and Realtor.com’s study of the 100 largest metros, only four — Akron, Ohio; St. Louis, Missouri; Youngstown, Ohio; and Pittsburgh — are balanced, meaning home prices and local incomes are aligned, leading to a 15 percent or more increase in the availability of affordable homes.

Another 30 markets are closer to reaching balance, with the availability of affordable listings increasing at least 5 percent over the past year. Raleigh, North Carolina; Des Moines, Iowa; Grand Rapids, Michigan; Columbia, South Carolina; and Columbus, Ohio, have logged the greatest improvements from 2024, NAR said, thanks to favorable market conditions and legislators adopting housing policies that prioritize affordability.

Meanwhile, 44 percent of markets are “stuck in the middle,” where the average gap between what households can afford and what’s actually for sale is still more than 10 percentage points but less than 20 percentage points. Seattle; Washington, D.C.; Austin, Texas; Salt Lake City, and Denver are some of the key markets in a precarious situation, where the next few years will be key to determining whether they move toward balance or continue to fall behind.

The final 26 percent of markets have fallen behind, where the availability of affordable listings has either annually declined or remains more than 20 percentage points below what NAR considers a balanced market. Los Angeles; Oxnard, California; San Diego; New York City; and Spokane, Washington, are the top markets where affordability has crumbled, despite strong jobs and economic growth. In these cities, years of underbuilding and restrictive zoning laws have undercut any potential affordability improvements that come with a robust economy.

Nadia Evangelou

“It’s not just about economics — it’s about opportunity. When home prices outpace income growth by this much, it limits people’s ability to build equity, stay rooted in their communities, or move closer to jobs and schools. It becomes harder for teachers, nurses, police officers, and essential workers to live anywhere near where they work,” the report read. “What these metros need isn’t just more housing — it’s the right kind of housing, in the right places, and at prices that reflect the real lives of the people who call these areas home.”

Although some of the report’s findings are bleak, NAR Senior Economist and Director of Real Estate Research Nadia Evangelou said she’s still optimistic about the market’s ability to recover and yield more opportunities for homebuyers.

“Even in high-cost areas like San Francisco, we’re witnessing real progress,” she said in a written statement. “While the housing market remains far from balanced, current for-sale home listings better align with home buyers’ incomes compared to pre-COVID-19 levels — a clear reminder that improvement is possible.

“More homes are hitting the market, and it’s encouraging to see the greatest housing-supply gains among middle-income homebuyers,” she said.

Email Marian McPherson

This post was originally published on this site

by Richelle Hammiel | May 16, 2025 | Industry, News Feed

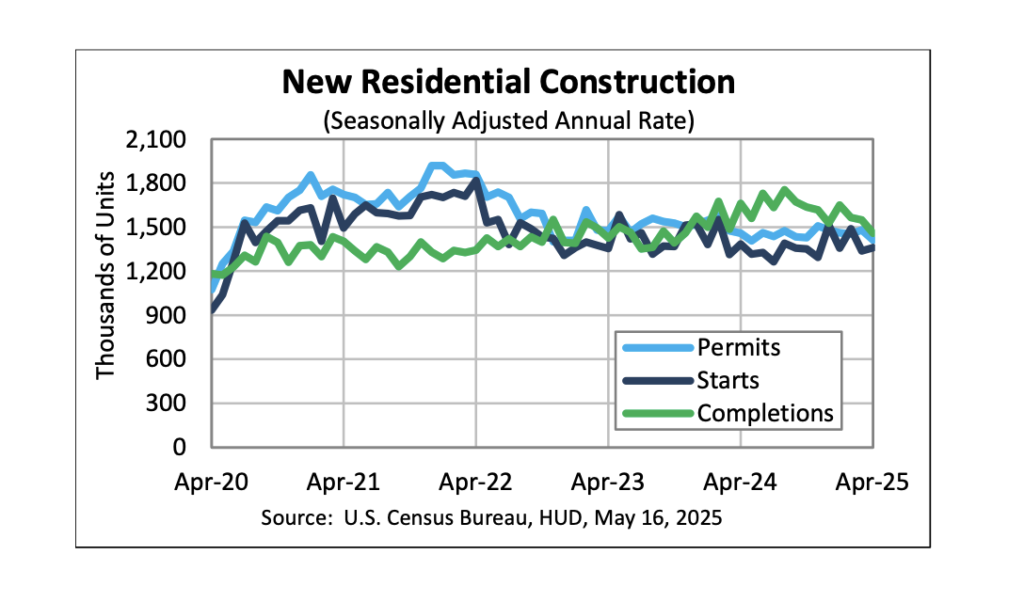

April’s housing data underscores a challenging landscape for new construction, particularly in the single-family segment, and the privately-owned segment isn’t far behind.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

April’s housing data underscores a challenging landscape for new construction, particularly in the single-family segment, and the privately-owned segment isn’t far behind.

Builders are navigating a complex mix of elevated costs, rising mortgage rates and waning consumer confidence, which is weighing heavily on the market.

Odeta Kushi | First American Deputy Chief Economist

“Builders’ growing pessimism is partially driven by the increase in mortgage rates in April, which impacts both builder and buyer financing costs,” First American Deputy Chief Economist Odeta Kushi said in a statement. “Residential construction costs are still more than 40 percent higher compared to pre-pandemic levels and skilled labor shortages persist.”

Policy instability is another source of strain. “Policy uncertainty also weighs heavily on builder sentiment, with 78 percent of builders reporting difficulties pricing their homes recently due to uncertainty around material prices,” Kushi noted, citing NAHB data. “The recent announcement that the United States and China will reduce tariffs for 90 days may offer temporary relief and brighten the outlook.”

This backdrop of uncertainty is reflected in the numbers, a new data report from the U.S. Census Bureau and the Department of Housing and Urban Development (HUD) indicated.

Source: U.S. Census Bureau and the Department of Housing and Urban Development (HUD)

Privately-owned housing starts in April rose modestly, up 1.6 percent from March to a seasonally adjusted annual rate of 1,361,000, though they remain 1.7 percent below the April 2024 level. Single-family starts dropped 2.1 percent to 927,000. Meanwhile, multifamily activity climbed from 371,000 to 420,000 from March to April.

Completions followed a similar pattern. Privately-owned housing completions fell 5.9 percent from the previous month to 1,458,000 and 12.3 percent year over year. Single-family completions declined 8 percent to 943,000, while multifamily completions edged up from 503,000 in March to 507,000 in April.

Permits — a forward-looking indicator of new builds — also declined. Permits for privately-owned housing units dropped 4.7 percent to 1,412,000, while single-family permits fell 5.1 percent to 922,000. Multifamily permits decreased from 445,000 units to 431,000.

“The April report was not a great one for single-family housing, with single-family starts, permits and completions all declining,” Kushi said. “The slower pace of single-family permits suggests a reduced rate of single-family groundbreaking in the upcoming months, due to higher inventory levels in key markets and ongoing challenges with costs and affordability.”

Builder sentiment has dropped accordingly. In May, it fell to the same level seen in November 2023, matching a trough not seen since December 2022. “This growing pessimism was broad-based across all NAHB Housing Market Index (HMI) components,” Kushi added.

Still, there may be some relief on the horizon. Kushi remains cautiously optimistic.

“The long-term housing shortage, builders’ ability to offer incentives, and potentially less restrictive monetary policy could be tailwinds,” she said.

Email Richelle Hammiel

This post was originally published on this site

by Andrea V. Brambila | May 16, 2025 | Industry, News Feed

The Federal Reserve analysis found that rising home prices are likely why commission rates fell in the past two decades, but found no impact on rates after buyer contracts were required in 15 states.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

One of the primary changes instituted by the National Association of Realtors’ nationwide antitrust settlement may end up having no effect on commission rates, according to an analysis by the Federal Reserve released this week.

The analysis, “Commissions and Omissions: Trends in Real Estate Broker Compensation,” examined commission rates advertised to buyers’ agents in a dataset of real estate listings from CoreLogic covering about half of properties listed nationwide from 1995 to 2023.

The researchers also used the CoreLogic House Price Index and average resale prices from CoreLogic Market Trends to look at the relationship between commissions and home prices and gathered data on buyer representation agreements and rebate bans from state legislative archives.

Buyer representation agreements lay out buyer and agent responsibilities, agency representation and agent compensation details. They are required by 15 states, before and independent of the NAR settlement, which requires buyer agents to sign agreements with buyers they are working with before showing them a home.

The study’s authors, Rupkatha Banerjee and Andrew Paciorek, found that commission rates have come down a bit nationally over the past two decades, from an average of about 3 percent in the late 1990s to about 2.7 percent in 2023. There also appears to be slightly more variation: In 2002, commissions largely clustered at 3 percent, while 20 years later, there was more of a spread, with more 2.5 percent and 2 percent rates.

“The highest bar is still at 3, suggesting that the industry norm of the 6 percent total commission paid to buyer and seller agents persists to some extent, at least under the usual assumption that the buyer and seller agents split commissions equally,” the researchers wrote.

“This persistence may be explained by steering and how poorly low-commission properties fare. Low commission listings stay on the market for longer and are less likely to sell,” they said, citing a 2019 study.

“Brokerage firms that offer low commissions are less likely to obtain cooperation from agents from larger firms, who make up the majority of the real estate market,” they added, citing a 2017 study.

“Thus, they are unable to compete with full-commission brokerage agencies.”

The researchers found that median home prices have nearly doubled since 1995 and that, when taking into account home prices, the downward trend in commission rates goes away.

“The variation in rates across metropolitan areas is negatively correlated with house prices, and we find that controlling for house prices in a panel regression eliminates the downward time trend,” the researchers wrote.

“Moreover, the magnitude of the correlation between house prices and commission rates implies that rising house prices could explain more than half of the aggregate trend.”

They theorized that the increase in home prices insulated agents from the effects of lower rates.

“When house prices are higher relative to consumer prices or prevailing incomes, real estate agents may be more willing to work for lower commission rates, since the higher selling price offsets the lower rate,” the researchers wrote.

The researchers also looked at commission rates in the years before and after buyer representation agreements and rebate bans were put in place in different state. They controlled for home prices to isolate the effects of the policies.

“Interestingly, we find no material or statistically significant effects of buyer representation agreement requirements or buyer rebate bans on advertised commission rates, suggesting that changes in these policies might not have a material effect,” the researchers wrote.

The researchers acknowledge that the NAR settlement includes a new provision not present in the states analyzed: The prohibition on advertising commission rates to buyers’ agents through the multiple listing service. This, they said, “could mitigate the issues of steering and collusion” and “lead to more substantial changes to business models and agent commissions going forward.”

Still, they noted that listing agents had found workarounds around the settlement’s prohibition and that NAR had added an option to delay marketing listings on top of its Clear Cooperation Policy (CCP), which requires listing brokers to submit a listing to the MLS within one business day of publicly marketing it.

“[P]ress reports suggest that sellers’ agents have found ways of sharing information on commission rate offers outside of the MLS,” they wrote.

“In addition, the NAR has relaxed its Clear Cooperation Policy, leaving more freedom for listing agents to forego or delay listing a property on the MLS in the first place. These sorts of adaptations make it difficult to predict the long-run effects of the settlement.”

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Dani Vanderboegh | May 16, 2025 | Industry, News Feed

Turn up the volume on your real estate success at Inman On Tour: Nashville! Connect with industry trailblazers and top-tier speakers to gain powerful insights, cutting-edge strategies, and invaluable connections. Elevate your business and achieve your boldest goals — all with Music City magic. Register now.

Every Friday, Inman Service Editor Dani Vanderboegh rounds up the most popular, most read, most critical stories of the week to give you a quick catchup on the big headlines you might have missed in the hustle and bustle of the workweek. Here’s this week’s Top 5 as chosen by our readers.

P.S. Don’t miss The Download, our weekly column that breaks down one of the week’s top stories and equips you with what you’ll need to meet next Monday head-on.

Credit: Compass, Beyond My Ken / Wikimedia Commons, and AJ Canaria Creative Works

The SERHANT. CEO jabbed at Compass’ launch this month of physical books of the brokerage’s exclusive listings in offices nationwide, likening it to old-school bookstores like Barnes & Noble.

CoStar CEO Andy Florance on Thursday said the “Boost” tool it rolled out on April 29 will now be available for brokers and homeowners who have been thwarted by Zillow’s private listing ban.

Gary Keller, co-founder of Keller Williams, took the stand on what was set to be the final day of arguments in the Sitzer | Burnett trial on Friday, Oct. 27.

Judge called Davis’ demand for arbitration “redundant, immaterial, impertinent, and scandalous,” but ruled the former CEO made reasonable attempts to arbitrate his case against Keller Williams.

Last week, Caballero set new world records after selling 7,722 homes in 2024 and inking $3.92 billion in volume. The agent, who works exclusively with builders in Texas, shared his tips with Inman.

The deal will give Lower greater reach, while also contributing to an “end-to-end homeownership” platform — increasingly the holy grail of real estate technology.

Email Editorial

This post was originally published on this site