by Inman | May 23, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the power of the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Want to level up your business? Inman Access offers expert-led tutorials with insights, advice and ideas designed to help you build your skills every day.

Verl Workman, co-founder and CEO of Workman Success Systems, specializes in developing high-performing teams. In this edition of Inman Access, Workman shares his unique approach to developing leaders at every organizational level.

Elevate your skills and set yourself up for success in 2025. Watch the session above, plus get fresh content added weekly, with Inman Access.

Watch now.

This post was originally published on this site

by Lillian Dickerson | May 23, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

President Trump’s “One Big Beautiful Bill Act” was passed by the U.S. House of Representatives on Thursday morning, a legislative package that the National Association of Realtors said “included several major victories” for its members.

TAKE THE INMAN INTEL SURVEY FOR MAY

The sweeping bill included a series of tax cuts, border control measures, increased work requirements on Medicaid (which are expected to lead to millions of low-income individuals losing health insurance), rolled back green energy tax incentives and raised the debt limit by $4 trillion, among other measures. It was passed by a vote of 215-214.

The bill now heads to the Senate for consideration, where lawmakers are expected to weigh in on it after the Memorial Day holiday.

Two Republicans and all 212 House Democrats voted against the bill, which House Minority Leader Hakeem Jeffries called a “GOP Tax Scam” that represents “an assault on the economy, an assault on healthcare, an assault on nutritional assistance, an assault on tax fairness and an assault on fiscal responsibility.

“Some Republicans who initially opposed the bill were concerned that it would add to the federal debt, and called for bigger spending reductions — on top of cuts to Medicaid and food stamp programs included in the version bill passed by the House Thursday.

Democrats approached that issue from the other end, opposing the bill’s proposal to extend $4.5 trillion in tax breaks enacted in 2017.

The most recent analysis of the bill by the Congressional Budget Office, published May 20, estimated those tax cuts would increase the federal deficit by $3.8 trillion over the next decade, while cuts to services would produce $1 trillion in savings.

Moody’s Ratings on Monday became the last credit agency to strip the U.S. of its most favorable debt rating over concerns that Congress and “successive U.S. administrations” have failed to tackle annual budget deficits — an action that could lead to higher interest rates on government bonds and mortgages.

Real estate industry players responded positively to the bill’s passage in the House, in large part because it included several business-friendly measures and sought to provide tax relief for families and low-income households.

“We appreciate House leaders for taking this important step with this tax reform bill, which supports hardworking families and strengthens the real estate economy,” NAR Executive Vice President and Chief Advocacy Officer Shannon McGahn said in a statement. “With lower tax rates, SALT relief, and new incentives for small businesses and community development, this proposal brings real benefits to everyday Americans.”

Emily Cadik, CEO of the Affordable Housing Tax Credit Coalition also praised the bill in a statement.

“The housing credit provisions in the reconciliation legislation passed by the House of Representatives today are a welcome step toward the creation of over half a million additional affordable homes in the U.S. At a time when housing costs remain high, and safe, affordable homes remain out of reach in too many communities across the country, we applaud the House’s action toward resolving a crisis that continues to affect millions of Americans.”

Bob Broeksmit, president and CEO of the Mortgage Bankers Association, also highlighted positive outcomes for the industry through the bill in a statement on Thursday.

“We have worked diligently with Congressional leadership and committee members to preserve key elements of the 2017 Tax Cuts and Jobs Act. This includes the deduction for qualified residence interest, the up to $500,000 homeowner exclusion on the gain on the sale of a principle residence, Section 1031 like-kind exchanges, and the continued deductibility of business interest for real estate. We also support the bill’s expanded deduction for Qualified Business Income under a permanent Section 199A, needed improvements to the Low-Income Housing Tax Credit program, and a new round of Opportunity Zones.”

NAR’s advocacy team was pleased the bill addressed the association’s top five tax priorities: qualified business income deduction, State and Local Tax Deduction (SALT), individual tax rates, mortgage interest deduction, and business SALT and 1031 “like-kind” exchanges.

What follows are highlights of the bill, and if passed in the Senate and signed into law, how it may impact the real estate industry.

An increase in qualified business income deductions (Section 199A)

The new bill would make permanent the deduction for qualified business income, and raises it after December 31, 2025, from 20 percent to 23 percent. Since more than 90 percent of NAR members are classified as independent contractors or small business owners, they would benefit from the increased deduction.

Raising state and local tax (SALT) deduction caps

The bill would raise the SALT deduction cap from $10,000 to $40,000 for households that earn less than $500,000. The marriage penalty would remain in place, meaning that whether filing as single or married, taxpayers would be able to deduct a maximum of $40,000 in state and local taxes. The income cap and deduction would each grow by 1 percent every year over a 10-year span.

Individual tax rates extension

Increased individual alternative minimum tax exemption rates that were set to expire at the end of this year would be permanently extended under the new bill and indexed for inflation, which could aid taxpayers with homebuyer affordability.

Preserving mortgage interest rate deduction

The bill would make permanent the current mortgage interest deduction level to the first $750,000 in home mortgage acquisition debt, what NAR calls “a key tax benefit for homeowners” that “support[s] housing market stability.”

Business SALT and Section 1031 like-kind exchanges

The bill would preserve Section 1031 “like-kind” exchanges, which allows the deferral of capital gains taxes when an investor directs a property’s sale proceeds into a new investment. It would not change anything for most businesses that deduct state and local taxes. Some limits introduced for state-level business SALT workarounds for high-income professionals will likely not impact real estate professionals, NAR noted.

Child tax credits

The new bill provision would eliminate the current expiration date of Dec. 31, 2025, for the double rate, or $2,000, per child tax credit, and make that tax credit permanent, rather than returning to pre-2017 levels of $1,000 per child. The provision also raises the child tax credit to $2,500 per child for tax years 2025 through 2028 and indexes it for inflation starting in 2029. The move would help families and potentially offset some of their housing costs.

Low-income housing tax credits

To support the development of affordable housing, the bill would restore the current 9 percent Low-Income Housing Tax Credit (LIHTC) to its 2021 level with an allocation increase of 12.5 percent. On the 4 percent LIHTC, the bill would lower the bond-financing threshold to 25 percent for projects that are financed by bonds that are issued before 2030. The bill would also designate tribal and rural areas as “Difficult Development Areas.”

Estate and gift tax threshold

The new bill would permanently extend the estate and lifetime gift tax exemption, which was set to expire at the end of the year, and raise it to $15 million for single filers and $30 million for those married filing jointly. NAR said that the provision would prevent a significant drop in the exemption rate and support generational wealth transfers.

The ‘Big 3’ business tax provisions

The bill would allow taxpayers to immediately expense 100 percent of any qualified property used in a trade or business for properties acquired between Jan. 20, 2025, and Jan. 1, 2030, instead of just 40 percent of the cost, according to existing law. It would also allow for the immediate expensing of properties used for manufacturing, refining, agriculture and other similar industries.

Similarly, taxpayers who previously had to deduct research and development over a five-year period would now be able to expense domestic research immediately.

The bill would also raise the cap on business interest expense deductibles for taxable years 2025 through 2029, with “adjusted taxable income” calculated without taking into account deductions for depreciation, amortization or depletion, which is more favorable to businesses.

Opportunity zones

The current designated opportunity zones (OZs) in the U.S., or areas of low-income that are eligible for qualified investments in exchange for tax benefits, are set to expire at the end of 2026. The provision on OZs in the new bill would launch a new round of OZs from 2027 to 2033, narrow the definition of OZs to census areas with a poverty rate of at least 20 percent or a median family income that does not exceed 70 percent of the area’s median income and require at least 33 percent of OZs be rural. Rural investments would also get enhanced tax benefits, like a 30 percent step-up in basis of 10 percent when investments are held for at least five years.

Ending new energy-efficient home credits

Currently, contractors can claim credits on homes built that meet Energy Star standards, with those that are considered Zero Energy Ready eligible for a $5,000 credit and those at low energy efficiency levels eligible for smaller credits. The program was set to expire at the end of 2032, but the new bill would accelerate that expiration date to the end of 2025.

Those homes that started construction before May 12, 2025, and are acquired by the end of 2026 would still qualify for the credit. However, on future projects, contractors would not receive credits for building energy-efficient homes.

Email Lillian Dickerson

This post was originally published on this site

by Richelle Hammiel | May 23, 2025 | Industry, News Feed

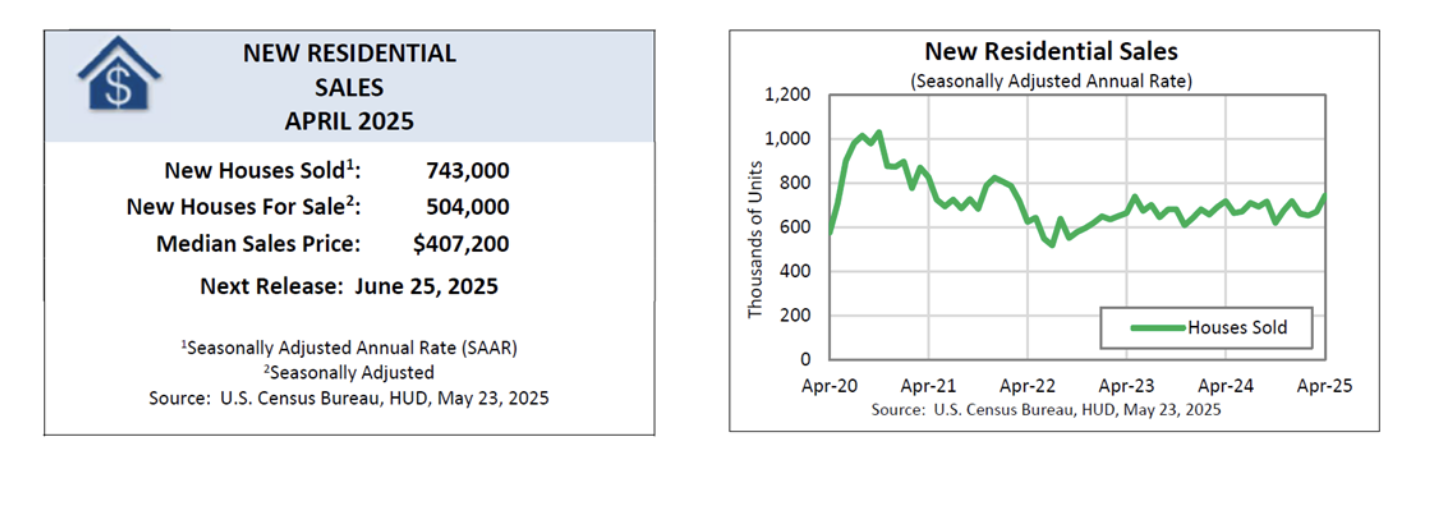

Sales of newly built single-family homes rose in April, pointing to continued buyer engagement during the spring homebuying season, the latest data from the U.S. Census Bureau and Department of Housing and Urban Development (HUD) suggests. New residential sales increased 10.9 percent from March to a seasonally adjusted rate of 743,000 units. That’s also a 3.3 percent boost over the April 2024 pace of 719,000 units.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Sales of newly built single-family homes rose in April, pointing to continued buyer interest during the spring homebuying season, the latest data from the U.S. Census Bureau and Department of Housing and Urban Development (HUD) suggests.

However, a few growing concerns, namely rising cancellation rates, softening builder sentiment and affordability challenges, could weigh on future momentum.

New residential sales increased 10.9 percent from March to a seasonally adjusted rate of 743,000 units. That’s also a 3.3 percent boost over the April 2024 pace of 719,000 units.

TAKE THE INMAN INTEL SURVEY FOR MAY

“Builders are off to a better spring than expected, despite higher mortgage rates in April,” First American Deputy Chief Economist Odeta Kushi said in a statement. “New-home sales in April beat consensus expectations and jumped approximately 11 percent above the March seasonally adjusted rate, even beating last April’s seasonally adjusted pace by 3.3 percent.”

The median sales price for new homes sold in April was $407,200, up 2 percent from March but down 2 percent year over year. The average sales price reached $518,400, up 3.7 percent month over month and 3.6 percent year over year.

“While the median sales price of a new home ticked up slightly on a month-over-month basis, prices are down 2 percent from a year ago,” Kushi added.

Odeta Kushi | First American Deputy Chief Economist

“Generally, new-home prices have been trending lower since prices peaked in 2022. This is in part an indication that builders are increasingly leaning on price incentives to support demand, but it’s also indicative of a shift in sales being concentrated at lower price points. For example, one year ago, 46 percent of new-home sales were priced below $400,000, whereas in April of this year that share increased to 49 percent.”

However, not all signs point to smooth sailing.

“While today’s report appears optimistic at first glance, there are underlying concerns,” Kushi warned. “The new-home sales report does not adjust figures to account for cancellations of sales contracts. Redfin recently highlighted a rise in home sales cancellations due to affordability challenges and heightened economic uncertainty. This trend suggests that sales figures might be overestimated.”

On top of that, builder sentiment is showing signs of strain, with builder sentiment dropping to its lowest level since November 2023. Expectations for single-family sales over the next six months have also declined to their lowest point since November 2023.

By the end of April, there were an estimated 504,000 new homes for sale, down slightly by 0.6 percent from March, but up 8.6 percent from April 2024. This figure represents 8.1 months of supply at the current sales rate.

“Despite the demand waiting on the sidelines and builders’ ability to offer incentives to attract buyers, the outlook remains clouded by uncertainty,” Kushi said.

Email Richelle Hammiel

This post was originally published on this site

by Andrea V. Brambila | May 23, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Howard Hanna Real Estate Services CEO Howard “Hoby” Hanna told Inman his decision on Wednesday to send a missive to the National Association of Realtors and more than 70 MLSs informing them that his brokerage no longer considers NAR’s Clear Cooperation Policy binding was all about choice and innovation.

Inman immediately reached out for a phone interview to find out more and the conversation touched on nationwide and local MLS policies, antitrust risk, Zillow’s new private listing rule, possible fines for Howard Hanna brokers, the catalysts behind the CCP, fair housing, and how Howard Hanna’s parent company, Hanna Holdings, will handle CCP compliance by market.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

“This is not about private or exclusive listing but more about trade associations mandating policies upon the industry that eliminate innovation creativity and unique marketing strategies that provide consumer choice regarding how their home is marketed,” Hanna told Inman in an email.

This interview has been edited for length and clarity.

Inman: Will you be having a dialogue with the MLSs that ask for it?

Hoby Hanna: Yeah. What I really think is MLSs should make their own rules in regards to participation that affect their members and have a voice, and not just take a policy that was written up top across the whole country and say, “This is how you have to do business,” and then makes all of us complicit in that form of business if we belong to the MLS.

To me that looks like antitrust, and that looks like we’re all having to do something if we want to participate. I think there should be individual participation rules.

Even in regards to this Zillow policy, Zillow is a broker in almost every MLS. They’re a participant like everybody else. One thing was when they said, “Well, you couldn’t display it on your website without [it] being on Zillow.” Well, that’s a far reach. Then you come back and say, “You can’t market it [on] anything, even if a seller requires it or that listing is banned for life.” It seems like that, in itself, is a pretty far reach and taking away consumer choice.

I’ve even said to some MLS executives, some of them should turn around and say to Zillow, “You can’t be a participant here and have our feed if you’re putting these stipulations on our members’ ability for seller choice.” If Zillow wants to say you can’t be on Zillow, but then they shouldn’t get the IDX feeds that they get everywhere.

The MLSs that said, “We have to follow NAR’s policy,” did they say, “We have to follow the policy, so we will levy fines or suspend members”?

They have not said that. I’m not even sure how they would collect the fines. But their answers were pretty straightforward: “We have our policies. They’re in conjunction with NAR and we expect that if you’re going to be a member here, that you participate to those policies and procedures.”

So what will Hanna Holdings do if its brokers are suspended because they don’t follow the policy, or if they levy fines? Are you going to pay the fines?

We won’t pay the fines. We don’t think our agents should pay the fines if the seller has choice. I’m saying that each MLS should have its own individual policies, and then we, as a broker and our separate franchises and in separate markets, will decide in those markets if we agree with those policies and how we’ll participate.

But if it’s just an adoption of Clear Cooperation, and they want to then turn around and fine on those policies and we have contracts that sellers don’t want to be privy to those policies, and they still want to fine us, we won’t pay the fines. For them, what does that lead to, if we don’t pay the fines? Then, okay, they’re going to say we can’t participate in the MLS? Well, is that really what they want to do? They want to have less inventory in the MLS? Do they want to destroy the MLS?

We could still put everything on our website and say to cooperative brokers, “You guys can come in, look at the homes here, and we’ll still cooperate with you,” because the MLS doesn’t offer cooperation anymore. There’s no offer of compensation; that’s been taken away. Cooperation is no longer offered as per the rulings and NAR settlement, we can’t offer cooperation. You have to find it. You can’t put it in the MLS to find out what it is.

It’s going to be your brokers, your franchisees, they’re going to get a notice saying, “You’re gonna have to pay this fine because you violated this policy,” so are you going to-

They’re going to have to decide individually what their reaction is at a franchise level. At a corporate level, we will decide when we talk to those different MLS executives and they say, “We’ve created our own participation policy, and this is what it is.”

We’ll decide, “Okay, that seems fair to us. That seems logical. You’ve given solutions that aren’t just to the 24-hour rule of Clear Cooperation. You’ve addressed seller choice.” So then we’ll decide individually, “Yes, that seems good to us, so we’ll be a member in good standing and abide by that,” and if there are fines in that case, we’ll pay the fines.

But just somebody blindly adopting NAR’s policy and saying we all have to abide by it, that we just can’t continue to do. That’s what got the industry in its last antitrust case.

It all stems back to MLSs specifically following rules that were mandated by NAR and then no brokers ever took a stance like this, saying, “We disagree with that. We’re separating ourselves from this. We’re giving our sellers and ourselves choice.”

We want to separate ourselves from the edicts of organized real estate.

So if your brokers decide to pay the fines, then that’s fine with you? If they make their agents pay, that’s fine with you?

Yes, they’ll make their overall decision. But as a holding company, we’re making it clear that we do not believe that Clear Cooperation as it exists is in the best interest of the industry or in the best interest of Howard Hanna being an innovative, technology-based leading broker.

We don’t think it captures seller choice if seller choice is disclosed. We do a pretty good job of making sure they understand their options. We think that just everybody blindly [following the policy] just puts too much exposure on future litigation.

You mentioned in the letter that CCP was adopted in response to fear that brokers were pursuing novel marketing strategies and taking advantage of new technologies. Why would NAR fear that?

Well, remember, it wasn’t just NAR. It was NAR’s MLS advisory board. A lot of the people that make up [that board], they’re not the leading brokerage firms in the country. There were people who were worried about Compass’s exclusive listing model. They were worried about programs like our Find It First, which allowed people to come search [listings before they were posted in the MLS]. They were worried about new entrants that said, “I don’t need an MLS.”

It’s just there was so much technology happening and plenty of people got scared of the status quo being disrupted.

So you’re saying it’s not NAR that’s fearing these new strategies, it’s the people on the MLS advisory board and committee?

Which, therefore, NAR sanctioned it, supported it, and said, “We are pushing this down to that three-legged stool,” saying you have to operate with this new rule.

And why would NAR do that?

I don’t know. In 2020, I never understood why they passed Clear Cooperation.

Well, I was there in the meetings at the time, and the big thing seemed to be fair housing.

I heard that too, and I looked at people and said, for example, if Howard Hanna left the MLS and our seller said to us, “We don’t need MLS. We think you guys do a great job, and you’ve got a website, and you’ve agreed to put our listing on HowardHanna.com” and let’s say we agreed to put it on Zillow and Realtor.com. Let’s just say that was our business model. Would that be a violation of fair housing?

And if there’s logic in that, if a seller wants to sell their own home, why don’t they have to put their house on Zillow, or put their house in a multi-list? These multi-lists and Zillow aren’t public utilities. Why does a builder not have to put the house in the multi-list? Are they violating fair housing? I just think that’s like one of those scare tactics.

If you could prove to me that HowardHanna.com doesn’t allow people of color or minorities or those affected by fair housing to look at our website — that doesn’t make sense to me. Maybe I’m wrong. Does that make sense to you that you have to be in the MLS to offer fair housing?

I think the idea at the time was, if you put it in the MLS, it goes out to not just HowardHanna.com but it goes out to all these other brokerage websites. It goes out to all the brokers and agents in the market. And so the maximum number of people will be able to see the listing, and not just the people that know to go to HowardHanna.com or the people that know a Howard Hanna broker or agent.

Ok, but under that same logic, if you’re a homebuilder, they don’t have to be in the MLS, and they don’t share their listings together. They choose if they’re going to put their listings online or partner with Zillow or give a feed.

My argument isn’t about holding all your listings off. It’s not about a three-phase marketing plan. It’s about if a seller wants to have choice, or you can create innovation or somebody in the industry could come up with a better way to display, share, promulgate their business, or somebody doesn’t want to have their house on the market in 24 hours.

It’s these unintended consequences. It’s not about not sharing inventory. It’s just, don’t put such stipulations and rules on it. I don’t think it’s a violation of fair housing. If the government wants to, [it can] say, “We think there should be a public utility, and whether you’re an individual homeowner or builder, developer, Realtor, everybody has to put their listing for sale on the public utility for everybody to see.”

We’re taking this position to distance ourselves a little bit from this organized real estate mandating what everybody else does. We actually think other people should take a hard look.

Do you know if any other brokerages have sent similar letters to NAR or MLSs?

I do not, and I didn’t talk to any brokers prior to doing this. This was our choice and our decision. We haven’t consulted, asked, gone into a coalition. We just said this is where we, as an independent business, feel we need to be.

At the end of the letter, it says Hanna Holdings and its affiliates and franchisees will determine, on a market to market by market basis, whether to require the listing brokers to submit listings on an MLS within one business day of marketing. How will Hanna Holdings determine whether to require that?

We will leave it up independently to our local markets and our franchisees, after discussion with MLSs, and let them make [the decision] but we’re not mandating that they have to operate in that sense. Sort of like we don’t mandate that you have to be a member of the National Association of Realtors to work at Hanna Holdings or any of its subsidiaries.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Dani Vanderboegh | May 23, 2025 | Industry, News Feed

Turn up the volume on your real estate success at Inman On Tour: Nashville! Connect with industry trailblazers and top-tier speakers to gain powerful insights, cutting-edge strategies, and invaluable connections. Elevate your business and achieve your boldest goals — all with Music City magic. Register now.

Every Friday, Inman Service Editor Dani Vanderboegh rounds up the most popular, most read, most critical stories of the week to give you a quick catchup on the big headlines you might have missed in the hustle and bustle of the workweek. Here’s this week’s Top 5 as chosen by our readers.

P.S. Don’t miss The Download, our weekly column that breaks down one of the week’s top stories and equips you with what you’ll need to meet next Monday head-on.

Illustration

The Federal Reserve analysis found that rising home prices are likely why commission rates fell in the past two decades, but found no impact on rates after buyer contracts were required in 15 states.

Zillow will send warnings about non-compliant listings beginning May 28, but enforcement won’t start until June 30. Agents will receive two warnings before their third non-compliant listing is blocked, executives said.

Credit: Compass and Nick Frandjian

The “Million Dollar Listing LA” star took to Instagram to criticize Compass Chief Evangelist Leonard Steinberg’s recent critique regarding how women in real estate are depicted on reality TV shows.

eXp Realty Credit: Jim Dalrymple

Kirsten Childress alleged she was drugged and sexually assaulted following a private event during eXp Shareholder Summit in May 2023. She is the sixth woman to make similar allegations in court.

Craig C. Rowe; Canva

Lone Wolf began notifying customers of the popular customer relationship manager software’s imminent shutdown “a few weeks ago,” Lone Wolf CEO Jimmy Kelly told Inman exclusively.

Email Editorial

This post was originally published on this site

by Andrea V. Brambila | May 23, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

This story will be followed later today with an interview with Howard Hanna Real Estate Services CEO Howard “Hoby” Hanna IV. Check back in a little bit.

Howard Hanna Real Estate Services is drawing a line in the sand.

On Wednesday evening, company CEO Howard “Hoby” Hanna IV sent a letter to the National Association of Realtors and more than 70 multiple listing services the brokerage belongs to, informing them it will no longer consider itself bound by the organization’s Clear Cooperation Policy, Inman has learned exclusively.

TAKE THE INMAN INTEL SURVEY FOR MAY

The policy requires brokers to submit listings to the Realtor-affiliated MLSs they belong to within one business day of marketing to the public. After months of consideration and vigorous debate across the industry, NAR chose in March to keep the policy as-is while adding a new delayed marketing option for sellers.

But it wasn’t enough. In the letter, Hanna describes Clear Cooperation as “bad policy” that Hanna Holdings — Howard Hanna’s parent company — never agreed to and voted against when it was adopted in 2020. “It deters innovation in the industry by restricting how Realtors market homes,” he wrote in the letter.

“Indeed, it was adopted in response to a fear that brokers were pursuing novel marketing strategies and taking advantage of new technologies. Stamping down on that innovation harms brokerages and it harms their customers.”

NAR, the letter continues, should not dictate how brokerages conduct business.

“Hanna Holdings does not consider the Clear Cooperation Policy binding and, accordingly, no Hanna Holdings affiliate or franchisee will adhere to the policy as a matter of course,” Hanna wrote.

“Instead, Hanna Holdings and its affiliates and franchisees will determine on a market-by-market basis whether to require their listing brokers to submit listings on a multiple listing service within one business day of marketing the property to the public.

“It will make these decisions based on its own business interests and independent of NAR and of any other brokerage.”

In a statement, a NAR spokesperson told Inman, “Clear Cooperation remains a mandatory policy, and MLSs are responsible for enforcing MLS policies. By joining a Realtor association-owned MLS, participants and subscribers agree to comply with the MLS rules and regulations.”

NAR did not respond to questions asking whether there will be any consequences for the company or its brokers if they don’t follow the policy, whether NAR will be taking any action as a result of the letter, whether any other brokerages have informed NAR they won’t follow the mandate, whether NAR had responded to Hanna’s letter and when NAR planned to respond.

Hanna told Inman in a phone interview that he called NAR CEO Nykia Wright before sending her and NAR’s chief legal counsel the letter and said it was “a very cordial call.”

“I said, ‘I just felt that [it was] probably better to make you aware of the situation, rather than just getting a blind letter,’ and she appreciated the call ahead of time, but we haven’t heard anything back,” Hanna said.

He said some MLS executives, such as those at West Penn MLS in Pennsylvania, Bright MLS in the Mid-Atlantic region and MLS Now in Ohio, had responded that they “want to have some dialogue,” while others, such as the Charlottesville Area Association of Realtors MLS in Virginia and a small MLS in North Carolina, had said “that they have to do whatever NAR tells them.”

Hanna told Inman that that doesn’t make sense to him.

“We have to make independent decisions, not just follow suit,” he said. “That’s what gets industries in trouble.”

Looming large in Hanna’s mind is that Howard Hanna was one of more than 90 large brokerages that were not covered under NAR’s $418 million settlement of multiple commission-related antitrust lawsuits nationwide last year, which meant that the company had to fight, and then settle, litigation it otherwise would not have.

Hanna believes MLSs should make their own participation rules rather than adopting a nationwide policy from NAR that mandates a particular way of doing business.

“[That] makes all of us complicit in that form of business if we belong to MLS,” he said. “To me, that looks like antitrust, and that looks like we’re all having to do something if we want to participate. I think there should be individual participation rules.”

None of the MLSs who said they had to follow NAR’s rules had thus far threatened fines, according to Hanna. But MLSs across the country have instituted hefty fines, some in the thousands of dollars, for violations of the CCP.

“We won’t pay the fines,” Hanna said. “We don’t think our agents should pay the fines if a seller has choice.

“What does that lead to, if we don’t pay the fines, then, okay, they’re going to say we can’t participate in the MLS? Well, is that really what they want to do? They want to have less inventory in the MLS? Do they want to destroy the MLS?”

Hanna has previously said his company was considering leaving the MLS due to NAR’s mandatory MLS policies.

“We could still put everything on our website and say to cooperative brokers, you guys can come in, look at the homes here, and we’ll still cooperate with you,” Hanna said.

The company would leave it up to its brokers whether to follow the CCP and whether to pay the fines or require their agents to pay the fines if they choose not to, according to Hanna.

“They make their overall decision,” Hanna said.

“But as a holding company, we’re making it clear that we do not believe that Clear Cooperation as it exists is in the best interest of the industry or in the best interest of Howard Hanna being an innovative, technology-based leading broker.

“We don’t think it captures seller choice if seller choice is disclosed. We do a pretty good job of making sure they understand their options. And we think that just everybody blindly [following the policy] just puts too much exposure on future litigation.”

Read the letter (re-load page if document is not visible):

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site