Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The U.S. bombing of nuclear sites in Iran that quickly sent the country to the brink of another broad conflict in the Middle East has added one more issue for those mired in a sluggish real estate market to worry about.

Of course real estate professionals never count on world conflicts to influence their bottom line, and war is a tragedy first and foremost for those directly in harm’s way. But the situation in Iran has the potential to ripple through global economies — impacting, among many others, real estate professionals and the people they serve.

With that in mind, we sought to make sense of what happens to housing when conflict breaks out, as well as what has happened to home sales historically during times of war involving — directly or indirectly — the U.S.

The result of this effort suggests that so far, economists haven’t seen responses in the relevant markets that might further hurt home sales.

Matthew Gardner | Gardner Economics

“Right now there is caution,” Matthew Gardner, an economist with Gardner Economics, said. “But we haven’t seen any kind of panic, whatsoever.”

Those signs of panic would likely first appear in oil, stocks and bonds.

In this case, economists have quickly turned their attention to the conflict’s impact on oil prices.

Oil is a direct and indirect source of inflation in the economy, so a conflict that leads to even the threat of Iran closing the Strait of Hormuz, a choke point in the Persian Gulf where roughly 20 percent of the world’s oil supply flows, was thought to send oil prices higher. The possibility that Iran would close the strait has been widely discussed during the conflict.

“That could have led the Fed to delay cutting rates even longer, and potentially you could see mortgage rates spiking,” Gardner said. “But that one thing didn’t happen.”

If oil prices rise, it could push up the consumer price index, making it even less likely for the Federal Reserve to cut the federal funds rate, which has an indirect effect on mortgage rates.

Instead, oil futures fell during the first hours of trading after the U.S. strikes on Iran and were down 8.6 percent as of mid-day Tuesday.

Oil prices as of mid-day on Tuesday, June 24, 2025

Economists next watch for volatility in equity markets. Had there been a sell-off in the stock market that drove down share values, investors and other potential homebuyers may have had less wealth with which to buy a home, Gardner said. That could have had an even bigger impact on the luxury market.

“But we didn’t see that,” Gardner said. “So far, so good.”

The third thing Gardner said he’s keeping an eye on is whether there are indications that global investors are moving money into the U.S. via real estate or the bond market.

“You could actually see money coming in, potentially, to the U.S. because it’s considered to be a global safe haven. Also it’s the global currency,” Gardner said. “That has the potential to actually lower mortgage rates.”

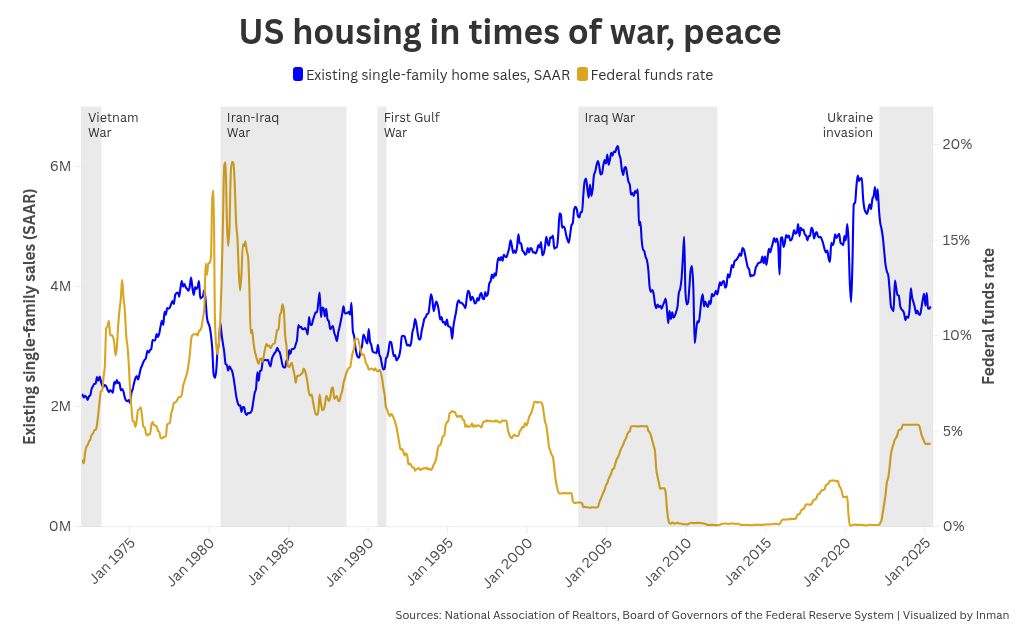

War, peace and interest rates

Inman analyzed the data for existing single-family home sales dating back to January 1965 to try and understand the impact of war involving the U.S. and the housing market.

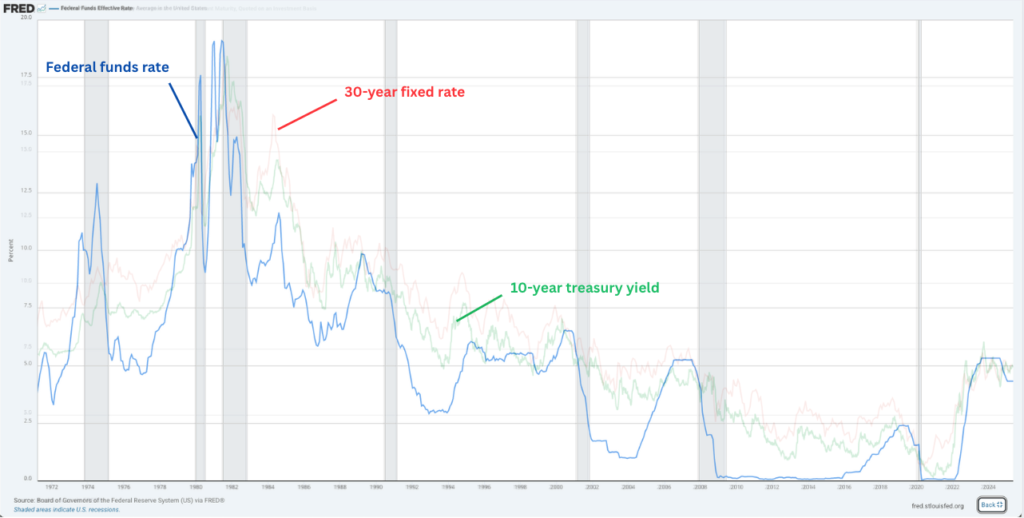

And while there are some trends in home sales that appear to generally track global conflicts, they also appear to more closely track the 30-year fixed rate, federal funds rate and 10-year treasury yield.

While this is not a comprehensive analysis of all factors — for instance, recessions and mortgage rates — it does paint an interesting picture.

The graph above shows that decades ago, home sales fell sharply as the Federal Reserve quickly raised the federal funds rate to combat quickly rising inflation. That happened to coincide with the Iran-Iraq War, when home sales fell before beginning to climb in mid-1982.

Operation Desert Shield began Aug. 2, 1990. The following day, mortgage rates were 9.84 percent. Rates jumped to 10.29 percent within three weeks and remained above 10 percent for much of the operation before beginning a long descent.

Home sales followed suit, with a sharp — and brief — decline and then rebound.

10-year Treasury Yield, the federal funds and 30-year fixed mortgage rates. FRED

In the case of Operation Desert Storm, which lasted for about six weeks in early 1991, rates fell.

Later, sales dipped sharply following the September 11 attack on the World Trade Center and invasion of Afghanistan before continuing a climb during the early years of the U.S. war with Iraq.

Sales continued to climb toward the apex of the housing bubble that burst in September 2005, preceding through the Great Recession.

The takeaway is that home sales more closely track things like mortgage rates than wars, though there are conditions caused by war that can impact rates and sales.

And while the Federal Reserve is currently walking a tight rope between taming inflation and keeping rates high for so long it causes a recession, Gardner said it wasn’t a recession specifically that had economists worried about the housing market.

“Some could argue that if it becomes bigger,” Gardner said, “and involves more of the Gulf states, we could see more of an economic global slowdown.”

Data editor Daniel Houston contributed to this story.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Ben Franklin is credited with saying, “In this world, nothing can be said to be certain, except death and taxes.” Depending on your income bracket and what happens with Trump’s “Big Beautiful Bill,” taxes might no longer be a certainty. Death, on the other hand …

With apologies to Mr. Franklin, I’d like to add one other certainty to the list: Uncertainty.

As I write this, Iran, Israel and (in a limited capacity) the United States are in a shooting war, which adds to potential uncertainties with oil shocks, a higher 10-year Treasury Bond, wavering consumer confidence, a lull in building starts and continued uncivil “civil” discourse. Our clients may be, understandably, on edge.

Yet, to quote from the National Association of Realtors’ Code of Ethics, “Under all is the land.” Sellers got to sell, buyers got to buy (fish got to swim, birds got to fly) and, based on history, real estate is still the safest investment out there.

So, how does an agent go about advising and guiding clients in these turbulent times? The same way we do it on a day-to-day basis. We constantly deal with turbulence. We walked our clients through the catastrophe of the 2008 economic meltdown.

On an ongoing basis, we deal with life-altering events: California agents help clients deal with the effects of wildfires, floods and earthquakes. In the Midwest and plains states, there are tornadoes, rain storms and freezing temperatures. Florida and the East Coast face hurricanes, and in New York City alone, there are the perennial disasters of the Knicks, Mets and Jets (wait till next year!).

Our clients already come to us for advice on the real estate market because they trust us. We’ve already helped them with one of the biggest (if not the biggest) investments of their lives, we guided them through the mortgage process, the vagaries of the insurance market, and they continue to come to us for advice on vendors, restaurants, and whether to remodel, refinance or sell.

But how can we advise clients on real estate when there are so many uncertainties flying around? By swatting them down, one small swipe at a time. Here are five tips to help.

Start big, go small

You don’t have to be an expert economist to sound like one. Break down economic information into digestible bites for your clients, starting with the national housing statistics from NAR, then move down to your state and county figures (available from your state Association) and finally narrow down to your local market (MLS).

Whether you are working with buyers or sellers, the conversation can go something like this: “Nationally, we’re looking at an average increase of X percent for days on market. On the state level, it’s actually lower at Y percent, but for our area, we’ve seen an even smaller shift of Z percent over the past three months, which means [insert your take here].”

If you’re already framing things this way, bravo. But if you’re reading this thinking “My clients don’t care about the national averages,” remember that a lot of agenting is perception. By going from national to local, you’re showing your clients that you consider a broad range of statistics to shape your view of the local market — something your competitors might not do, which bumps up your credibility.

Understand what’s affecting the numbers

If you normally check your email during the economic forecast of your local or state meetings, it’s time to pay attention. National and local forecasts are not always correct; however, their broad overview not only helps you frame economic factors for your clients, but it also gives you a basis to compare figures.

Not a numbers person? You don’t need to bench 250 pounds of economics; you can get results from doing 10-pound curls through entertaining and informative podcasts like Marketplace or watching the UCLA Anderson School forecast, which are incredibly digestible.

You don’t need to do it alone (and you shouldn’t)

If you are a residential agent, talk to residential income agents, or (shudder) commercial agents (I promise, they may be gruff, but offer to buy them a coffee and they soften up). Get their perspectives on the market, and find out what their clients are saying. Don’t stop there; talk to agents from different parts of the state, other states and even other parts of the country. Learn how they’re having these conversations with their clients and adapt what you like to make it effective for your clients.

And don’t just listen to groups — individuals are often influenced by groupthink and are more apt to share what they are really feeling in a one-on-one conversation, as evinced by this short and interesting video.

Don’t be afraid to say ‘I don’t know’

For whatever reason, so many agents hate saying “I don’t know,” and I have to admit I don’t know why. Quick question: I just said “I don’t know.” Do you have a lower opinion of me?

Ask your eye doctor what that weird mole on your back is, and they’ll probably say, “I don’t know.” (They may also say, “Please don’t do this in public.”) That said, they’ll probably follow up with, “Here’s the name of a specialist who will know.”

We say “I don’t know” all the time when it comes to a question about plumbing, electric and HVAC systems, but for some reason, when it comes to questions about the market, the reflex is to give an (often uninformed) answer. Maybe we’re afraid they’ll talk to another agent … who can also give them an uninformed answer. Whatever the reason, stop!

Learn to channel your inner doctor and say, “I don’t know, but let’s call X and see what they’re hearing.” Develop a broad range of experts: lenders, attorneys, CPAs, heck, even other agents. Swap information, learn from their expertise and demonstrate your expertise, and soon enough, you’ll be viewed as an expert. (Oh, and by the way, get that mole looked at.)

You don’t need to have all the answers, but you need to be present

Our clients trust us. There’s a lot of uncertainty these days from seismic shifts in how our government works, to civil unrest, to natural disasters, to international conflicts. We don’t have any say, sway or impact over these things, but “under all is the land.” And your clients are looking to you to help them make sense of what’s happening, not just with the market, but with their home.

Your clients don’t need you to have all the answers; they just need to know that you’re there for them and that you’re willing (and able) to help them navigate these rough seas. Your clients need to feel like you’re all in on this journey with them, and you need to be ready for the task.

Spencer Krull is a managing broker with Side, and also works as a real estate expert witness and consultant for attorneys.

By promoting family-friendly amenities, Victoria Kennedy writes, you can make your marketing more irresistible to moms and dads who are ready to become homeowners.

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

There’s little question that price will always be a factor in real estate. However, if you’re trying to attract families to your listing, or if you frequently work with families as a buyer’s agent, cost doesn’t always drive their decision to put down a bid. For many homebuyers who have (or intend to have) children, planting roots in a neighborhood that features family-friendly amenities takes precedence over price.

This presents a major opportunity. Research shows that younger families are moving into the suburbs in record numbers. According to 2024research from the Economic Innovation Group, twice the number of families have relocated into more rural areas than before the pandemic. In other words, your suburban or rural market may have more interest from families seeking properties that aren’t in congested cities.

What exactly can you do to appeal to all these families looking for the type of real estate your market offers? Try including some of these features within your marketing.

Community gathering spaces

Highlight indoor and outdoor areas that are accessible to all homeowners. These can be a huge draw for parents with kids.

Pools and well-designed playgrounds catch the attention of families looking to find the ideal place to call home. In terms of indoor spaces, a community fitness facility and room for events show families that the community has anticipated their needs. Some people like the idea of hosting gatherings in spaces other than their homes. Consequently, it’s convenient for them if they have a neighborhood space at their disposal.

Walkable areas

Far too many children are nature-deficient, spending less time outside than they should. And being cooped up can have long-term ramifications. As noted in recent research, nature deficiency can lead to cognitive, social and behavioral issues. Therefore, parents seeking real estate may want walkable areas.

An example of walkability could be extra-wide streets or sidewalks. Even if a listing’s neighborhood doesn’t have those features, it may still be appealing if it’s close to trails or paths. That way, families can get the exercise they need.

Be sure to consider communities that are friendly to bike riders as well. People for Biking research shows thatbicycling is trending across the United States. Highlight bike racks set up throughout a development to encourage families to bike together.

Sustainable features

Young families are into the practice of sustainability. For instance, younger drivers are opting for electric vehicles more frequently than older drivers, according toPew Research. With this in mind, highlight homes and neighborhoods that feature electric vehicle charging stations.

There are other ways to show that a neighborhood has been planned with sustainability in mind. Landscaping that includes native plants that aren’t hard on the environment and don’t use a lot of fossil fuels to maintain offers responsible curb appeal.

Another eco-friendly feature is solar-powered exterior lights. The less reliant lights are on the electric grid, the better. Be sure that you’re letting potential homebuyers know about sustainable offerings in all your listings’ marketing materials.

Safety updates

Parents want to raise their children in safe communities. Consequently, do all you can to highlight safety features. Recently repaired or redone sidewalks and common spaces are a good place to start. Well-lit neighborhoods and safety enhancements, such as street lamps or community entrance spotlights, are good features to point out to potential buyers.

Business and education accessibility

Offering easy access to the community may be a differentiator for a neighborhood. For example, you may want to emphasize proximity to local businesses, eateries, stores and schools. Many planned communities feature on-site places to dine and shop. If you’re able to include those types of establishments within your pitch, you may increase desire and demand from first-time and young homebuyers with growing families.

Every time you add a family to your market, you’re adding more diversity to the fabric of the neighborhoods you serve, while boosting your revenue streams. Families can be finicky about where they decide to plant roots. By focusing on promoting family-friendly amenities, you can make your service more irresistible to moms and dads who are ready to become homeowners.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

A federal judge made quick work of signing off on the 15 combined settlements of two commission-related antitrust cases Tuesday afternoon.

On June 24, Judge Stephen R. Bough of the U.S. District Court for the Western District of Missouri granted final approval to deals reached in two cases known as Keel and Gibson after their lead plaintiffs.

The first hearing, for the Gibson case, lasted 18 minutes, from 1:30 p.m. to 1:48 p.m. With the final approval, six defendants in that case have now resolved the claims against them: NextHome, Inc.; The Keyes Company and Illustrated Properties; John L. Scott Real Estate Affiliates, Inc., and John L. Scott, Inc.; The K Company Realty, which does business as LoKation; Real Estate One; and Baird & Warner Real Estate.

The second hearing, for the Keel case, was even shorter: 11 minutes, from 2:29 p.m. to 2:40 p.m. The judge’s order resolves claims against these nine defendants: Side Inc.; House of Seven Gables Real Estate; Washington Fine Properties; JPAR Real Estate Services and affiliated firms; Signature Premier Properties; First Team Real Estate-Orange County; Sibcy Cline; Brooklyn New York Multiple Listing Service (Brooklyn MLS); and Central New York Information Service (CNYIS).

A group of homesellers first filed the Keel case in January, at which time they also proposed a settlement that would see the defendants pay a combined total of $10,570,000. The case ended up on a fast-track, at least compared to other suits, and by February the proposed settlements had received preliminary approval.

Gibson is a somewhat higher-profile case because it was the first of the so-called copycat suits — or lawsuits filed immediately after a jury in 2023 agreed with homesellers that the National Association of Realtors and major franchisors engaged in anticompetitive practices.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

A company that smooths out the many rough patches in the road to investing in U.S. real estate from overseas is now better prepared to meet that growing need, according to a June 24 press release from Waltz, the tech-enabled property investing platform.

The company said it has secured a new $25 million line of credit from Setpoint Capital that will enable it to fund up to $1 billion in loan volume.

The capital will “support Waltz’s official launch across Latin America (LATAM), with a focus on Mexico, Brazil, Colombia, and Argentina—the first three being the region’s largest sources of U.S. real estate investment,” the company said.

Waltz provides a digital on-ramp for foreign real estate investors to buy property in the United States. It helps them establish a banking presence, an LLC, gain an EIN, transfer currencies and safely wire funds. The company conducts direct marketing efforts to investors and works with real estate agents to educate them on workflow efficiencies and the financial requirements needed to assist families and investors hoping to own in the States.

“The demand from Latin America was immediate and that is not surprising — U.S. real estate is a blue chip investment for foreign nationals,” Yuval Golan, founder and CEO of Waltz, said. “The stability, rooted in the historical strength of the U.S. economy, facilitates wealth creation from financing options, the potential for passive income streams, and property value appreciation. When paired with customer-centric digital solutions, it becomes clear why digital platforms like Waltz resonate with today’s global investors.”

The National Association of Realtors found in its 2024 Profile of International Transactions in U.S. Residential Real Estate that residents of Canada lead in outside U.S. investment at 13 percent of foreign buyers. Then comes citizens from China (11 percent) and Mexico (11 percent). In total, foreign buyers account for $42 billion in total home sales, or 2.0 percent of the total $2.1 trillion market.

Waltz’s software experience was reviewed by Inman in 2024. It was recognized for how it flattened a typically convoluted process for the buyer and the other stakeholders common to the transaction.

“Because Waltz is ultimately a fintech solution and the lender behind most of its customers’ deals, it’s the primary source of truth for the deal. This means agents and brokers don’t have to wade through layers of logins or voicemails to find out which conduit has held up the transaction,” the review stated.

Waltz states that it has processed more than $300 million in loan applications across four continents since its launch a year ago and to date has raised $50 million.

New offering lets existing homeowners tap their equity to buy before they sell and make non-contingent offers to better compete with cash buyers in competitive markets.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

After leading the nation in refinancing last year, Rocket Mortgage hopes to do more business with homebuyers with a new bridge loan product that lets existing homeowners buy before they sell and make non-contingent offers to compete with cash buyers.

Rocket Mortgage’s bridge loan, announced Monday, gives homebuyers up to six months to sell their home and make interest-only payments during that period.

Bill Banfield

The average homeowner has $181,000 in untapped equity, and providing immediate access to that money for a down payment or closing costs “removes one of the biggest barriers to moving,” Rocket Chief Business Officer Bill Banfield said in a statement.

In markets that remain highly competitive for buyers, Rocket said, the ability to make non-contingent offers can help win over sellers who are considering multiple offers.

Even in less competitive markets, bridge loans help buyers “avoid the hassle of double moves and temporary housing, while taking the time to secure the best offer on their existing property,” the company said.

Homebuyers can also turn to competitors including HomeLight and Calque, who partner with multiple lenders to offer “Buy Before you Sell” products, and power buyers like Knock and Zavvie.

Detroit-based Rocket Mortgage is licensed in all 50 states and Washington, D.C., sponsoring 3,602 mortgage loan originators working out of 57 branch locations nationwide, according to records maintained by the Nationwide Mortgage Licensing System (NMLS).

Rocket Mortgage was the nation’s second biggest mortgage lender in 2024, with $97.6 billion in funded loans accounting for 5.4 percent of originations by volume, according to Home Mortgage Disclosure Act (HMDA) data tracked by iEmergent.

Pontiac, Michigan-based United Wholesale Mortgage, which overtook Rocket as the leading U.S. mortgage lender in 2022, originated $139.7 billion in mortgages last year, accounting for 7.7 percent market share, according to iEmergent HMDA data.

Most of Rocket’s 2024 origination volume came from refinancing existing mortgages (56 percent) or providing home equity loans (6 percent). UWM did most of its business (63 percent) with homebuyers, iEmergent HMDA data shows.

With $44.5 billion in refinancings last year, Rocket Mortgage edged out UWM’s $43.4 billion in 2024 refi volume.

Rocket expects its pending acquisition of the nation’s biggest loan servicer, Mr. Cooper, will help grow its refinancing business, while a deal to acquire national real estate brokerage Redfin will put it in contact with more homebuyers.

Speaking at an investment conference in May, Rocket Companies CEO Varun Krishna said the lender has set a goal of handling 8 percent of purchase mortgages and 20 percent of refinancings.

After acquiring Mr. Cooper, Rocket will be collecting payments on about one in six U.S. mortgages with $2.1 trillion in outstanding balances. When those homeowners are ready to refinance, Rocket will have a leg up on “recapturing” their business, Krishna said.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.